The outbreak of the coronavirus epidemic in China has shaken the global asset markets—and with good reason. The coronavirus has the potential of being the ‘trigger’ which will push the world into a global depression.

Here, we briefly explain why.

The outbreak

It looks that the virus spreads very easily, through droplet infection and with a “latency” period that allows infected people to spread the virus before they themselves exhibit symptoms. This implies that the virus has already spread much more widely than original estimates indicate. The individual cases popping up across the globe are one confirmation of this.

Fortunately, the fatality rate is still relatively low: under 2 percent. However, this can change, especially if the virus mutates, and there’s already speculation, whether the figures provided by China can be trusted.

China in trouble

As we have been warning through 2019 (see, e.g., this and this), China’s economy is ripe for a serious downturn. Beijing used most of its remaining firepower last year, when it desperately tried to postpone the inevitable recession, probably to appear strong in the trade negotiations.

Despite record-breaking stimulus enacted in 2019, the Chinese economy has grown at a sub-par rate of around six percent. And this is according to the official statistics! In reality, the actual Chinese growth rate has probably been much lower.

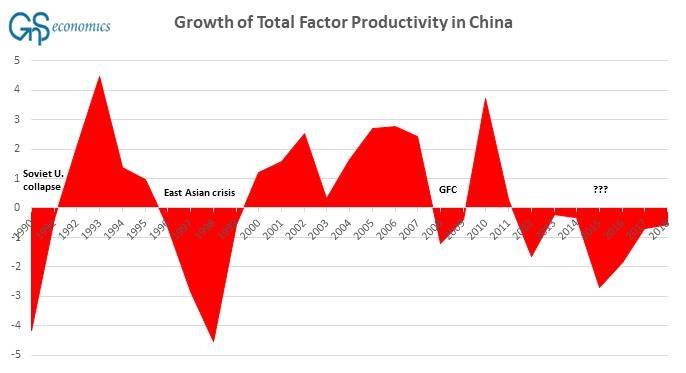

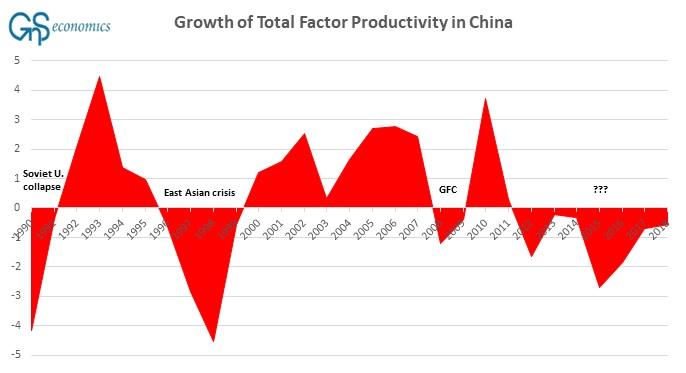

As China’s State-Owned Enterprises, or “SOEs”, have become riddled with debt, their ability to increase production has stagnated. This has also contributed to the broader stagnation of productivity growth in China (see Figure 1). After the growth of SOEs faltered in 2017, the Chinese consumer has become an important driver of the economy.

Figure 1. Growth (%) of total factor productivity in China. Source: GnS Economics, Conference Board

It’s clear that the current coronavirus scare is hitting the Chinese consumer and so affecting the economy as well. The massive plunge in the price of copper—the longest since 1986—implies that the Chinese economy has come to a near-standstill.

If the virus turns into a pandemic, which is definitely possible, the economic and human costs could become very dire not just for China, but for the whole world.

Virus and the world economy

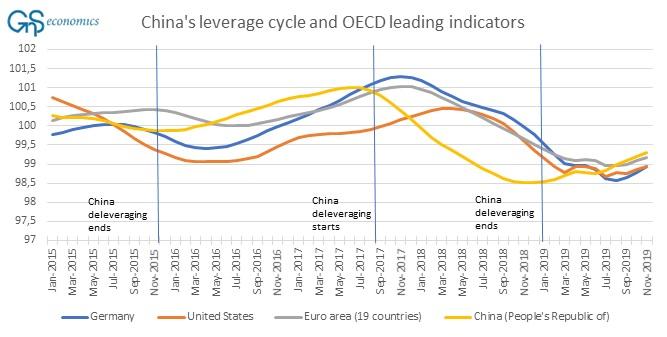

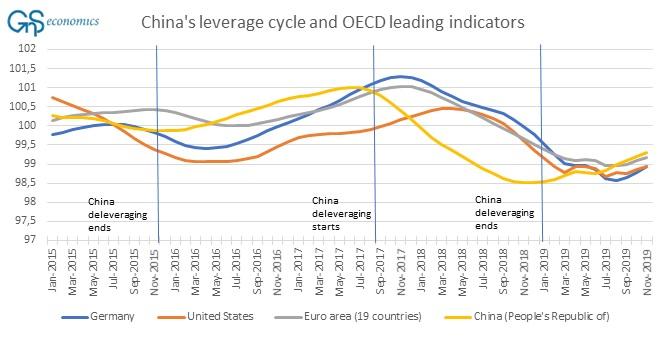

It is probable that the coronavirus will push Chinese economy into recession sometime this year. As China has led this global cycle (see Figure 2), the rest of the world will follow.

Figure 2. The leading economic indicators of the OECD and the deleveraging/leveraging policies enacted by China. Source: GnS Economics, OECD, PBoC

The first shoe to drop outside China is likely to be the export-and China-dependent Eurozone. And, as we have warned on several occasions, many European banks will be unable to withstand a recession (see also Q-Review 3/2019 and Q-Review 4/2019).

When the European banking crisis, driven by the ensuing recession, resumes it will “go-global” fast as Europe holds the biggest concentration of globally systemically important banks, or G-SIBs.

It is also unlikely that hyper-valued U.S. stock markets will be able to endure the impact of a global recession. This is even more the case if the Fed tapers its term repo-operations in February, as planned.

Global recession, a European banking crisis and a crash in the U.S. capital markets will produce a global economic collapse which will almost certainly overwhelm any attempts—massive and coordinated as they may be—to turn the tide by over-stretched central banks and over-indebted governments.

This is, why the coronavirus outbreak should be treated for what it is: a potential harbinger of human and economic calamity.

Last May, John Cox was worried he had accidentally hurt his newly adopted infant by rolling into her when they both dozed off. Erring on the side of caution, he brought her to Children’s Wisconsin hospital—where he worked, coincidentally, as a pediatric emergency doctor—just to make absolutely sure she was fine. It turned out she had suffered a minor fracture that is common in babies and heals on its own.

Two weeks later, child protective services declared him a child abuser and took the baby from him and his wife.

The child has been in foster care now for eight months. She is only nine months old.

What happened? According to a remarkable investigative story by ABC’s Mike Hixenbaugh, it’s possible for the authorities to interpret almost any bump or bruise as evidence of evil intent:

What followed, according to more than 15 medical experts who later reviewed Cox’s case, was a series of medical mistakes and misstatements by hospital staff members that has devastated Cox’s family and derailed his career. A nurse practitioner on the hospital’s child abuse team confused the baby’s birthmarks for bruises, according to seven dermatologists who have reviewed the case. A child abuse pediatrician misinterpreted a crucial blood test, four hematologists later said. Then, two weeks after the incident, armed with those disputed medical reports, Child Protective Services took the child.

Those misjudgments—and a deep suspicion of all parents with injured kids—led to the child being taken.

“In hindsight,” Cox said in a recent interview, “taking her to our own hospital was the single most harmful decision that we made for our baby.”

Children’s Wisconsin, like many hospitals, has bought into the theory of “sentinel injuries”—the idea that minor bruises can be warning signs of future abuse, so each bruise must be treated as suspicious. But as Hixenbaugh writes:

Several emergency room doctors described an “out of control” child abuse team that is too quick to report minor injuries to authorities and that is too closely aligned with state child welfare investigators. …

Five doctors told a reporter they’re even afraid to bring their own children to their hospital after accidental injuries, fearing that a misdiagnosis or miscommunication might lead Child Protective Services to break their family apart.

“This is a disease in our hospital,” one physician said. “The way John’s case has been mishandled has opened all of our eyes to how big the problem is.”

In part, the problem can be traced to the advent of the child abuse pediatrician, who claims to be able to tell adult-inflicted injuries from innocent ones.

“Child abuse pediatricians very often operate under secret contracts with police, child protection, and prosecution offices—never disclosed to the parents bringing their children in for emergency treatment,” Diane Redleaf, the legal consultant at Let Grow, tells Reason. “These individuals have been billed as having special superhuman powers to tell abuse from accidents and rare diseases, superior to the powers of other doctors because they ‘know child abuse when they see it.'”

Some of the doctors have at times overstated the certainty of their conclusions, the investigation found. Child welfare agencies and law enforcement officials often rely on their reports as the sole basis for removing children and filing criminal charges, sometimes in spite of contradictory opinions from other medical specialists.

In Cox’s case, the family could afford to get outside doctors to review the records, and many were shaken by what they saw. They pointed out not just several stone-cold mistakes, but how eager the authorities seemed to be to find abuse.

A police detective who grilled both Cox and his wife—Sadie Dobrozsi, also a pediatric doctor—said he didn’t understand how the hospital could have concluded they did something wrong. That didn’t stop child protective services, though: The authorities insisted on a safety plan for the baby, involving supervised visits monitored by grandparents.

Eventually, child services removed the baby from the home, anyway:

As the caseworker was leaving with the child, Dobrozsi asked what was making them so certain that she and her husband were abusive? The caseworker mentioned a new bruise on the baby’s foot.

Mom was completely baffled. She had no idea where that bruise came from, until she obtained her baby’s medical records. It turned out the hospital itself had pricked the child’s heel for a blood test. The mom didn’t know this because she had not been allowed in the room when it happened.

At this point, the baby is still in foster care. The couple’s other two kids are terrified that they may be taken, too. (One keeps his favorite toys in a backpack in case he’s suddenly taken away). Now the father faces a possible six years in jail on felony charges of child abuse.

The prosecutor is bolstering his case with a report prepared by a yet another child abuse pediatrician, this one in nearby Minnesota, whom he hired to look over the files. “In summary,” this child abuse pediatrician wrote, “there is no explanation for [the baby’s] injuries other than trauma.”

And yet the trauma of separating an infant baby from her loving parents for months does not seem to concern the authorities.

from Latest – Reason.com https://ift.tt/38WFZ59

via IFTTT

A coalition of 40 privacy rights groups has sent an open letter to the Privacy and Civil Liberties Oversight Board (PCLOB), requesting that the agency recommend a suspension of all federal use of facial recognition technology.

The PCLOB was set up as an independent federal agency in 2007 to review executive branch anti-terrorism efforts with the goal of making sure that citizens’ privacy and civil liberties are protected. The PCLOB can also review proposed anti-terrorism legislation, regulations, and policies and advise the president and executive branch agencies on their privacy and civil liberties implications. Advocates are asking the agency to exercise what power it has to recommend against the use of facial recognition technology.

In early December, the Department of Homeland Security initially announced that it was rolling out facial recognition system that would require that all travelers, including U.S. citizens, be photographed upon entry and departure at airports and seaports. Their photos would be matched against a database of passport and visa photos created and maintained by Customs and Border Protection. In response to pushback from civil liberties organizations, the CBP has withdrawn, for the time being, its proposal.

Now in an open letter to the PCLOB, a coalition of 40 privacy and civil liberties activist organizations asks the Board in light of the “rapid deployment of facial recognition systems directed toward Americans within the United States by federal agencies” to “recommend to the President and the Secretary of Homeland Security the suspension of facial recognition systems, pending further review.”

Citing the PCLOB’s enabling legislation, the letter’s signatories are entirely correct when they declare: “The rapid and unregulated deployment of facial recognition poses a direct threat to ‘the precious liberties that are vital to our way of life.'”

from Latest – Reason.com https://ift.tt/317hTlG

via IFTTT

A coalition of 40 privacy rights groups has sent an open letter to the Privacy and Civil Liberties Oversight Board (PCLOB), requesting that the agency recommend a suspension of all federal use of facial recognition technology.

The PCLOB was set up as an independent federal agency in 2007 to review executive branch anti-terrorism efforts with the goal of making sure that citizens’ privacy and civil liberties are protected. The PCLOB can also review proposed anti-terrorism legislation, regulations, and policies and advise the president and executive branch agencies on their privacy and civil liberties implications. Advocates are asking the agency to exercise what power it has to recommend against the use of facial recognition technology.

In early December, the Department of Homeland Security initially announced that it was rolling out facial recognition system that would require that all travelers, including U.S. citizens, be photographed upon entry and departure at airports and seaports. Their photos would be matched against a database of passport and visa photos created and maintained by Customs and Border Protection. In response to pushback from civil liberties organizations, the CBP has withdrawn, for the time being, its proposal.

Now in an open letter to the PCLOB, a coalition of 40 privacy and civil liberties activist organizations asks the Board in light of the “rapid deployment of facial recognition systems directed toward Americans within the United States by federal agencies” to “recommend to the President and the Secretary of Homeland Security the suspension of facial recognition systems, pending further review.”

Citing the PCLOB’s enabling legislation, the letter’s signatories are entirely correct when they declare: “The rapid and unregulated deployment of facial recognition poses a direct threat to ‘the precious liberties that are vital to our way of life.'”

from Latest – Reason.com https://ift.tt/317hTlG

via IFTTT

In The Past 30 Years, The “Top 1%” Has Bought $1.2 Trillion In Stocks; The “Bottom 99%” Has Sold $1 Trillion

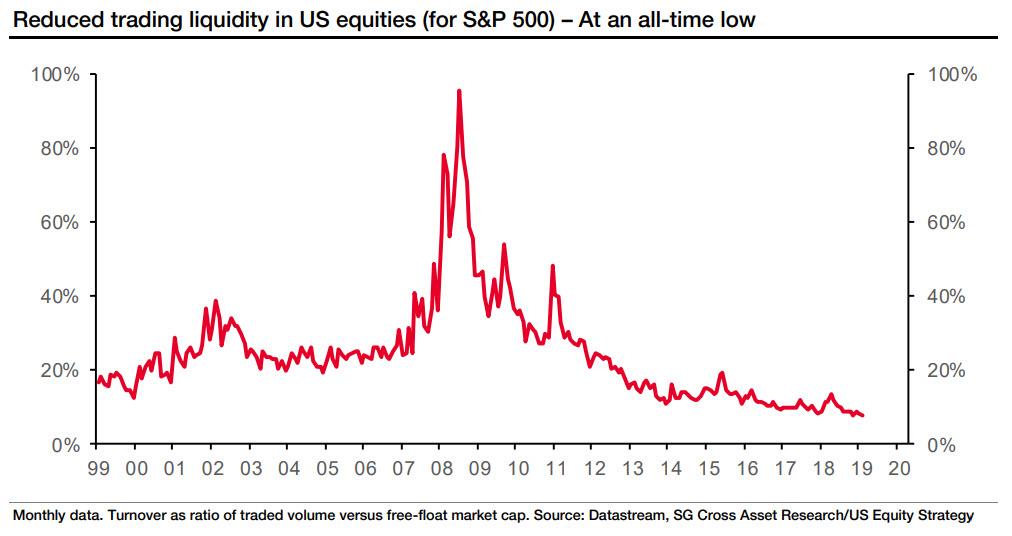

For years, the market had been stumped by what in 2019 we dubbed a “great conundrum” – namely, how was it possible that equity funds were liquidating stocks at a furious pace, with outflows hitting a post-crisis high last year, and yet stock prices not only kept hitting daily all time highs but unleashed a furious meltup in September which has lasted to this day?

Some suggested answers, most notably SocGen, which explained that the offset to fund selling was record (and price indiscriminate) stock buybacks which, due to prevailing market illiquidity, had a disproportionate bullish impact on price discovery, to wit: “the lack of market liquidity, as measured by S&P 500 turnover – the ratio of trading volume vs free float market capitalization – has exacerbated the impact of share repurchases on US equities.”

And while intuitively that explanation did make sense, it did not seem complete: was there some aspect of investor selling (or buying) that was being ignored by the market, which was simply focusing on aggregate fund flow numbers?

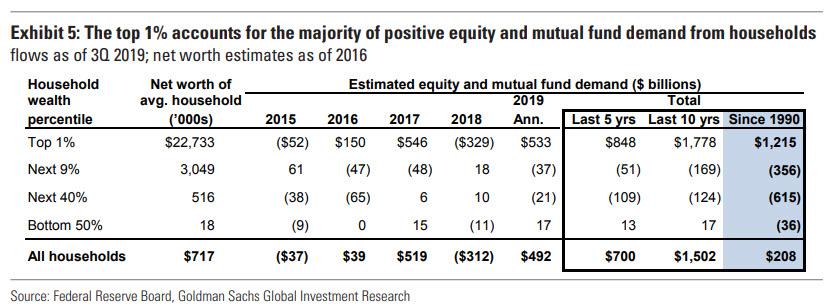

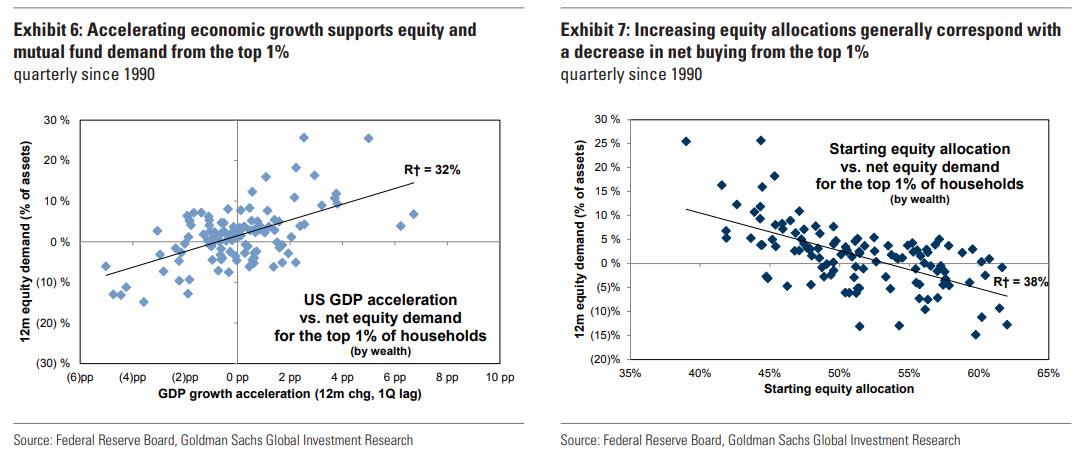

As it turns out, the answer is yes: according to a just released analysis from Goldman’s Arjun Menon, household equity purchases have been driven solely by the wealthiest 1% during the past 30 years. Specifically, since 1990, the top 1% has bought $1.2 trillion of equities and mutual funds compared with $1 trillion of net selling by the remaining 99%. And, confirming what we discussed in “The Rich Have Assets, The Poor Have Debt“, based on the Federal Reserve’s Distributional Financial Accounts (DFAs), the concentration of household equity ownership among the wealthiest households is at an all-time high.

Where does this buying vs selling differential come from?

While there are more details in the full report, Goldman simplifies the dynamic by noting that starting equity allocations and US economic growth have been the most significant drivers of equity demand from the top 1%. The wealthiest households typically increase their net buying of equities following periods of accelerating economic growth but reduce demand as their equity allocations rise. Meanwhile, the remaining 99% of households generally buys stocks after interest rates decline, although the current period appears to be an outlier.

Below we present some more details from Goldman, which analyzed the Fed’s newly published Distributional

Financial Accounts:

Using the DFAs, Goldman estimates equity demand from each household wealth subgroup, identifying the factors that drive this demand, and determine the potential implications for equity prices in 2020.

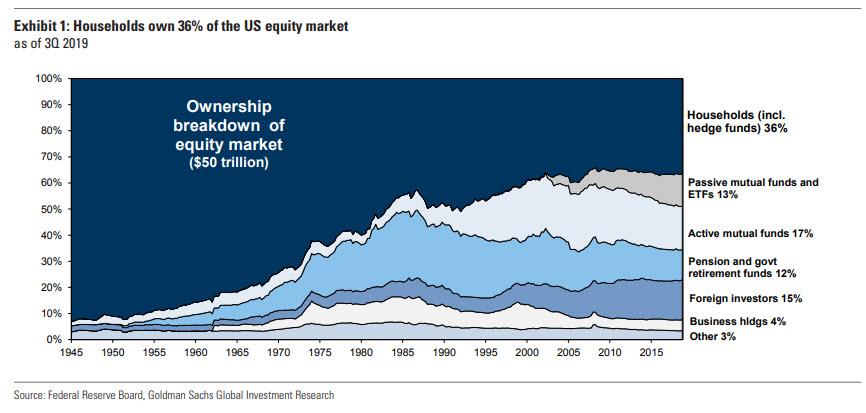

In aggregate, US households own 36% of US equities, which is at least two times larger than any other major investor category. As a result, the concentration of household wealth and asset allocation across US households can have significant implications for equity supply and demand. The “Household” sector described in the DFAs includes retail investors and private funds (such as hedge funds). The DFAs combine aggregate household balance sheet data from the Federal Reserve’s Financial Accounts of the US (Z.1 release) and distribution of wealth from the Survey of Consumer Finances (SCF). Aggregate household balance sheet data include both retail investor and private fund holdings. However, based on the most recent 13-F filings, Goldman estimates that hedge funds own only 10% of aggregate “Household” sector equities. Also, the SCF samples only retail investors (including wealthy individuals) and therefore, the distribution of wealth is also not affected by private funds.

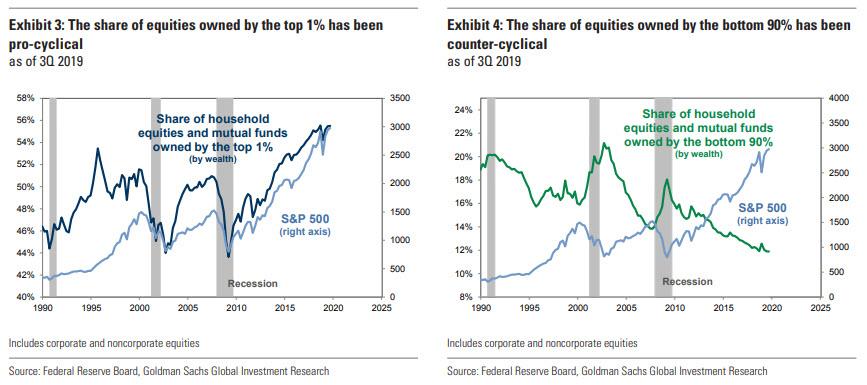

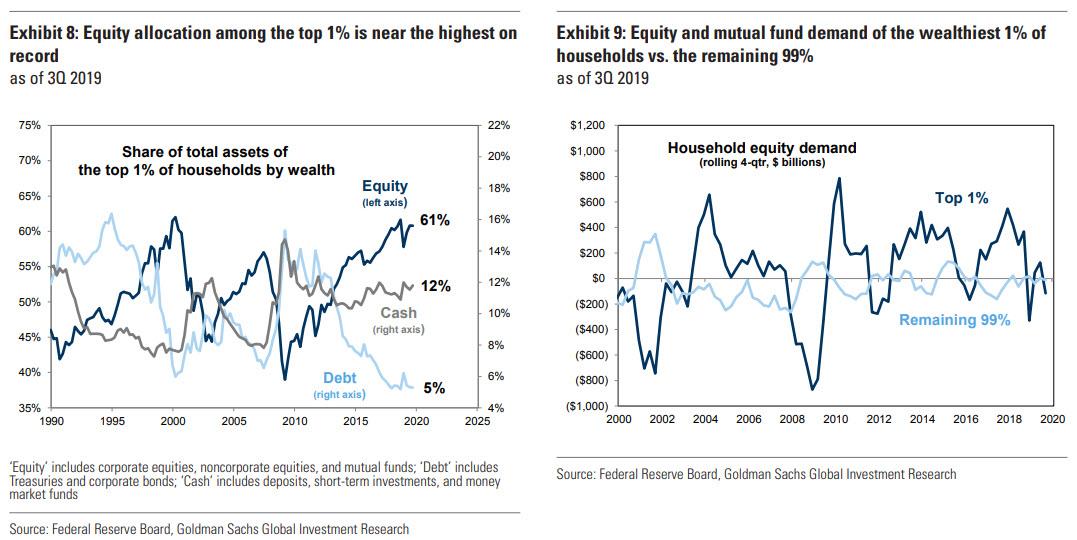

This brings us to the report’s first striking observation: the concentration of household equity ownership among the wealthiest households is at an all-time high. Specifically, the top 1% of US households by wealth owns $21.4 trillion of equities (corporate, noncorporate, and mutual funds), which represents 56% of aggregate household equity ownership. In contrast, the bottom 90% owns $4.6 trillion of equities (12% of total).

This gap between the share of equities owned by the top 1% and the bottom 90% is nearing its widest in 30 years alongside the record long economic expansion. And here an amazing admission by Goldman which crushes any argument the Fed may have to continue engaging in QE and monetary easing to “boost” the wealth of the middle class: “The equity share of the top 1% has generally been pro-cyclical during the past 30 years while the share for the bottom 90% has been counter-cyclical.”

Of course, a less politically correct way of describing the above is “distribution”: the rich buy all the way up, then dump to gullible retail investors who load up on stocks… just as the recession begins.

This, in turn, brings us to the troubling punchline, one which explains precisely how the Fed has made the rich richer, while crushing the middle class: The top 1% has also been by far the main source of equity demand from households during the past 30 years. Since 1990, the top 1% has bought $1.2 trillion of equities and mutual funds compared with $1 trillion of net selling by the remaining 99%.

Some more observations on why the superrich vs the non-super rich have such a different purchasing pattern:

Since 1990, starting equity allocations, US economic growth, and equity market returns have had a significant impact on equity demand from the wealthiest households. The top 1% has generally been a net buyer of equities when economic growth has been accelerating and stock prices have been rising. In contrast, equity demand from this cohort has been negatively correlated with equity allocations.

Interest rates have been the most significant determinant of equity demand from the remaining 99% of households. Outside of the top 1%, households have typically increased their equity demand after the 10-year US Treasury yield falls. For the least wealthy households, rising stock prices and wage increases have also been drivers of equity purchases.

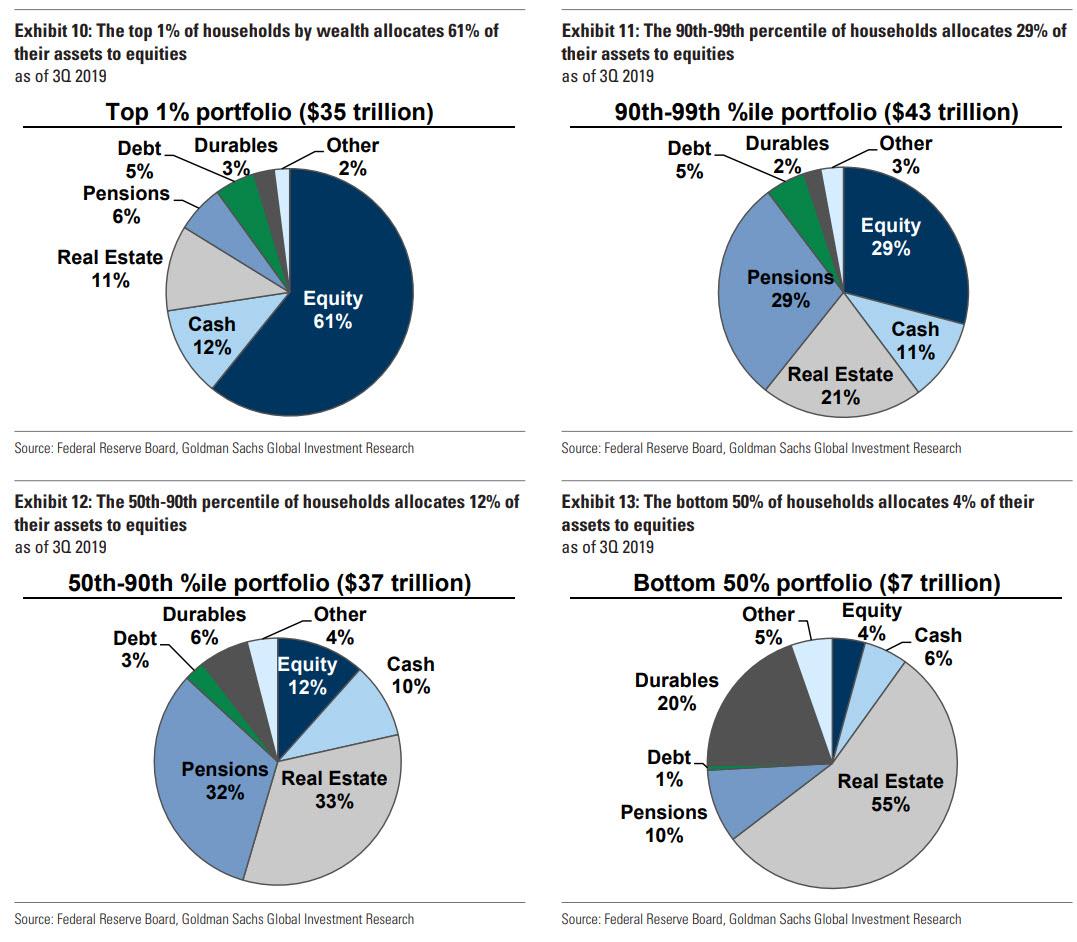

Portfolio allocations among the “bottom 99%” are less concentrated in equities than those among the top 1%, in absolute terms and relative to history. Equity allocation among the top 1% (61% of assets) is more than two times greater than the next 9% (29% of assets) and six times greater than the bottom 90% (10% of assets). The 90th-99th percentile of households allocates the majority of their assets to pension entitlements (29% of assets) while the next 40% and bottom 50% allocate most to real estate (Exhibits 10 to 13)

So what does this mean for market demand dynamics in 2020 and onward?

According to Goldman, while households will remain net buyers of equities this year, they will reduce their purchases relative to 2019. As we showed above, the wealthiest households have been by far the biggest driver of positive household equity demand. “Accelerating US economic growth and rising stock prices should continue to support equity purchases by the top 1%”, the Goldman strategists predict citing their economists who expect US GDP growth will accelerate from 2.1% to 2.5% (q/q ann.) between 4Q 2019 and 4Q 2020.

However, the equity allocation of the top 1% has risen near its all-time high, which will likely be a greater headwind to aggregate equity demand this year than in 2019. The top 1% allocates 61% of their total assets to equities ($21 trillion of $35 trillion), which ranks in the 97th percentile since 1990. Equity exposure at the start of 2019 stood at 58% (87th percentile). In contrast, this cohort’s allocation to debt, which has been generally been inversely correlated with its equity allocation, is close to its lowest in 30 years.

Meanwhile, rising interest rates will likely weigh on equity demand from the remaining 99% of households. Goldman’s rates strategists’ expect the 10-year US Treasury yield will rise from 1.64% to 2.25% by year-end 2020 alongside faster economic growth and rising inflation expectations. Then again, Goldman’s sellside researchers have been notoriously terrible at getting anything right in the past decade, and if only looks at where the 10Y is trading now (1.5%), this will be another catastrophic prediction by Goldman.

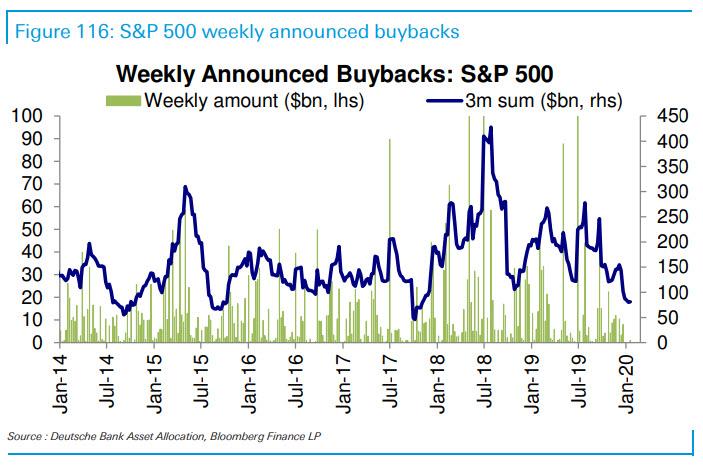

Assuming Goldman gets it right, however, the reduced aggregate household equity demand combined with the previously observed sharp decline in corporate repurchases…

… suggests only modest potential upside to equity prices this year, according to the Goldman team. In addition, rising equity prices relative to bonds and outflows from mutual funds will likely drive pension fund and mutual fund selling this year, respectively.

Goldman’s conclusion is troubling: the bank now expects the S&P 500 will rise by only 4% to 3400 by year-end, a far cry from the nearly 30% increase in 2019:

Aggregate allocation to equities among households, mutual funds, pension funds, and foreign investors has risen to 46%, ranking in the 95th percentile since 1990. The fact that these four investor categories, which own almost 90% of the equity market, have limited potential to increase their equity allocations is consistent with our forecast of single-digit equity market returns this year.

There is, of course, a simple solution: the Fed turns activist, and in taking a page from the BOJ and SNB playbook, bypasses households entirely and starts buying stocks and ETFs in the open market. In fact, considering the tremendous success central banks have had in the past decade, this “final solution” to fair and efficient markets is only matter of when not if.

The theme for today’s post is from Scott Galloway’s (@profgalloway on Twitter) “Casper Should Not Go Public” post on Medium, which he wrote in response to the news that Casper, a mattress company I had never heard of, had filed to go public, having lost $73.4 million on $250.9 million revenues in 2017 and another $92.1 million loss on $357.9 million in 2018.

This post isn’t about Casper, the Galloway article is superb in analyzing exactly why anybody dumb enough to buy this IPO deserves to lose the 30% decline in stock price he posits for the first year (which I think is being charitable).

However, Casper will not go public, as it has no business being public. Casper’s numbers are a sign of a frothy economy: firms that should be sold in the private market doing a kabuki dance (“technology” mentioned over 100 times in prospectus), asking people to suspend their disbelief until the founders, VCs, and bankers sell their shares and get their fees. That’s not going to happen. Here too, yogababble won’t cut it: “We believe we are the first company that understands and serves the Sleep Economy in a holistic way.”

The economics work better if Casper sent you a mattress for free, stuffed with $300.

He also compared Casper to other players in their space, and adjacent space, mentioning that Away, is better differentiated in a less competitive space (there are 175 online mattress retailers!), and Warby Parker, who actually looks to be headed toward a successful IPO (because they actually have a real business).

It was a phrase near the end of the post which grabbed me, having circumscribed almost perfectly the frustration and angst rational economic actors have been feeling these past several years. Said rational economic actors include

non-VC funded business owners

people who save money

people who pay down or pay off their debts

fiduciaries responsible for investing and allocating capital

and most anybody with a time horizon longer than the next quarterly earnings report

What he said was this:

Casper is being drowned and likely won’t survive. Away needs to be adopted by someone who will feed, clothe, and protect them. Warby looks to have the muscle and fat to survive an Amazon winter and emerge stronger.

It was that phrase “Amazon winter” that got me. Amazon poses such an existential threat to any sector it enters that even speculation that it may enter a space is enough to tank every public stock in it.

But it isn’t just Amazon that is scouring the economy looking for spaces to disrupt and so-called “value to unlock”, it’s every Amazon wannabe, trying to become the Amazon of their own space, or to lock up a “blue ocean” before somebody like Amazon can move in and eat it.

The end objective of all these players isn’t to have viable businesses, ones that do business the old fashioned way, at a profit.

Instead the end objective is to set in motion a cascading series of financial events at successively higher valuations. That’s the game now, and I’ve decided to call that game Unicorn Bingo. The macro effects of Unicorn Bingo are to usher in Unicorn Winter.

Unicorn Winter is the long, hard slog where credit induced asset bubbles on Wall Street suck up all the oxygen from Main Street.

It’s the Cantillon Effect, when geometrically increasing central bank balance sheets lift up the Unicorns’s valuations while pushing up the cost-of-living for everybody else.

The Unicorn Winter brings central bankers out of hibernation if the stock market pulls back 5%.

“Free markets”

Futures go up -> shorts get smoked

Futures crash -> CME steps in immediately -> Trump makes statement -> Powell capitulates -> Exchanges use circuit breakers -> Plunge protection team steps in -> Media starts doing 24/7 specials about buying the dip

The Unicorn Winter isn’t about making money, as in profits. It’s about monetizing what goes on in the mind of people who have no idea they’re being datamined.

Unicorns don’t create jobs. For the most part they create gigs. Temporizing everything from your home, your office, your server space, everything is delivered as-a-service, most likely at-a-loss and if there’s any humans involved in the chain at all it’s as part of somebody’s side hustle. Because that’s all there is now that everything else has been disrupted away in a sweeping tide of financialization.

In the Unicorn Winter even the also-rans get their hallowed exits.

And it all started when an entire class of banksters got bailed out for creating a financial crisis…

None of the bailed-out financiers here at #Davos2016 who live in Greenwich & collect Lamborghinis can understand why US voters are unhappy.

— Rudy Havenstein, Not a Communist. 99.8°F. (@RudyHavenstein) January 21, 2016

But in the Unicorn Winter the people who didn’t want to play Unicorn Bingo don’t get exits. They get shut down, liquidated, foreclosed or stripped out in asset sales.

Ground Hog Day is Coming

We’re now in that part of winter that usually gets to me the most, when it’s cold, wet, miserable. It’s dark in the morning when I walk the dog before I take the kid to school, it’s dark when I walk her again after dinner. It’s always dark, always cold. The dog doesn’t seem to mind. She’s a Siberian Husky who was named “Tenacity” by the rescue folks who found her, all those years ago, chained to a pole in a swamp and left for dead.

During these early dark mornings it feels like it will be like this forever and I can’t even imagine walking her around in shorts and my “Got Hedge?” t-shirt someday in the future. But even though it feels like winter will last forever, I know it won’t.

To rest of us, exiles from game of Unicorn Bingo during the longest and strongest Unicorn Winter on record, we could use a dose of this Tenacity. Owning gold (and silver) is one way to just wait it out. As Bill Fleckenstein opined on a QTR podcast in the fall of ’19 (I think this one), you can argue with the Unicorns, you can try to short them, because they should be shorted and they should come back to earth, someday.

But it’s usually a disaster because of the Fed put, which looks to keep working until finally, one day, it won’t. There was another podcast I recently listened to with Grant Williams (which I can’t seem to find now), when he talked about his witnessing the end of the Nikkei Bubble from his vantage point in Japan at the time. No crash, no notable day of reckoning, the way he described it, “one day the Nikkei just stopped going up every day. It just started going down”. And it’s been down ever since, for thirty years.

But if you buy gold then everything the central banks do to keep the Unicorn Winter going is actually wind at your back. It feels good not to be endlessly fighting the Fed and doing it without having to actually drink the kool-aid.

If you run a business, like I do, that has to survive the Unicorn Winter, then you need that muscle and fat Galloway ascribes above. You need actual customers for whom you can provide value, not data cows to mine and surveil. If you’ve made it this far without taking on VC, don’t start now.

Connect with other unfunded, real businesses doing actual stuff and start working together: joint ventures, co-branding, white labeling, sell your customers what they want instead of loading up on VC and taunting them with shiny new objects.

If you aren’t already, get involved in the crypto economy. After the everything bubble pops, I think it will be one of the segments that fills the vacuum.

If you can get your business to the point where you can continue operating in your niche no matter how long the Unicorn Winter lasts, just imagine how things will be when it’s over. I’ve said it before, the two periods where we experienced the most explosive growth at easyDNS were immediately after the bursting of the .com bubble and then again after the GFC.

* * *

My latest book: Unassailable: Protect Yourself From Deplatform Attacks, Cancel Culture and other Online Disasters is available now.

Citizen Journalist Exposes The Brutal Truth: China Is Losing The Battle In Wuhan

Over the past week, millions of Chinese have been worrying about the safety of friends and relatives trapped in Hubei and Wuhan. Most suspect that Chinese censors have been blocking some of the more dispiriting details of the crisis, and many believe the real number of deaths and confirmed cases is higher than the government has disclosed.

And as the US, UK, Japan and other governments work to evacuate their citizens from the city, fewer reporters are daring to venture out to the hospitals in Wuhan where teams of overwhelmed healthcare workers are fighting along the front lines of the virus.

Amid the media blackout, the government in Beijing has enlisted the WHO to help assuage the worries of a skeptical public that has already been exposed to videos depicting what appear to be bodies piled up in hospital corridors.

Recently, one self-styled ‘citizen journalist’ traveled to Wuhan to try and document the situation on the ground. What he discovered was even more alarming than he had feared: By quarantining the city, the government in Beijing had basically condemned the people of Wuhan to battle the virus on their own.

Hospitals are so overwhelmed, that people with obvious symptoms of the virus are still being turned away. Some severely ill people have been forced to visit five or six hospitals before being accepted for testing and treatment.

Residents who don’t live within walking distance of a hospital treating virus victims have few options. Each district reportedly only has four volunteer taxis picking up patients and bringing them to the hospital to be tested. Streets are closed, and public transportation has been shuttered. So if patients cant’ get a taxi, they might be stuck walking many miles to a hospital.

Even more alarming: Hospitals in Wuhan have struggled with dire shortages of testing kits. Some only have ~100 kits per day, dramatically slowing the process of confirming new cases of the virus. It’s just the latest sign that the true number of infections in China is much higher than the numbers that have been released by the government.

Twitter user @You_Shu_China took the video from the anonymous citizen journalist, who said he’s being targeted by local authorities who are trying to silence him.

“I’m afraid,” the anonymous journalist says. “Behind me is disease. In front of me is China’s legal and administrative power…I’m not afraid of dying. Why should I be afraid of you, Communist Party?”

The below video has English subtitles (users must remember to click the “cc” button):

Read the translated text below:

Btw, this is a very rough translation, I’ve reorganised the flow a bit, as he jumps around, & I’ve also missed things out etc. I’ve kept him speaking as “I” etc. I think it was recorded yday (29 jan). With those caveats.

“This video is a bit long. Usually I do short videos for WeChat etc. I’m in Wuhan, this is my 6th day. My name is already a ‘sensitive word’, so I can’t put anything on Wechat. Don’t put any of my videos on Wechat, or your account will be frozen. Mines already been frozen.

In the first few days, I’ve been to a few hospitals, been working with some volunteers, been to some markets. Yesterday, I went to the Sixth People’s Hospital. A lot of doctors there have been reported to have gotten ill. But doctors won’t accept my interview.

They’ve all been told not to do interviews. Even some have their phones taken away, we think. We know that eight doctors were arrested before (in Dec).

Some volunteer groups are helping deliver stuff (to patients in) hospital. I joined them for a bit. They’re really tired. People don’t believe in the China Red Cross. So people send donations, lots of small parcels, have been sent direct to the hospitals.

But they need sorting out, it’s really inefficient work, and hospital staff don’t have time. Volunteers are helping with that. I was also at Huashenshan Hospital. Lots of staff are working 24 hours. No rest. Sleeping 2-3 hours a day.

Most people are shut up at home; if you don’t have transport its really hard to get to the hospital. And if you go, some people are not getting checked. Each area (jiedao) is only allocated 4 taxis, that’s 4 taxis per 1000s+ people.

If you need a taxi, you have to call the district management; it’s impossible to get one. So if you don’t have a car, you have to walk to the hospital – but Wuhan is huge, so many people don’t go to the hospital. Call 120 for an ambulance – but there aren’t enough.

Taxi drivers in the middle of Dec, they already knew there was a serious disease. Why cant they say its SARS? It’s just as serious as SARS.

The Wuhan Police haven’t even apologized now (for arresting people talking about SARS).

I tried getting tested at a hospital to see what the process was like. They asked me questions and told me to queue for testing. I went with a patient to Tongji Hospital. Lots of patients had been to multiple hospitals. I was genuinely scared.

The corridors in the out-patients department were all full of beds, lots of people were breathing with masks and oxygen tanks. In the corridors. They had to be seriously ill.

Dr said we need to select which patients to do the test on. There are only I was told 100 or several hundred test-kits per hospital per day. There aren’t enough, so doctors need to select those to check. So some people have been to 5-6 hospitals trying to get tested.

All hospitals say they don’t have spare beds. I’m really scared now. People are scared. I’m envious of CCTV, they’re safe when they do interviews, they’ve got all the clothes/kit. I can’t go onto the wards, so I’m just in the outpatients dept. I just have a mask and a coat.

I thought of contacting Caixin journalists. No other media is here. But they don’t take my messages. I heard a HK journalist was still here,I was excited to talk to him. But when I contacted him, he said the last 5-6 days he’s been at the hotel, his HQ told him not to go out.

No one (ie journalists) is going to the front-line at the hospitals. I’ve mostly been in the hospitals the last 5-6 days. I’m really scared. I feel under a lot of pressure. I’ve got some breathing problems, maybe it’s the mask. Only one guy knows where I’m living.

The most important thing is they lack testing kits. They lack other things too, masks etc. Qingdao Public Security called me, asked me where I was. They asked me to chat. They asked my parents to talk.

I’m afraid. In front of me is disease; Behind me is China’s legal and administrative power. But as long as I’m alive I’ll speak what I’ve seen and what I’ve heard. I’m not afraid of dying, why should I be afraid of you, Communist Party.”

Notably, SCMP reported Thursday that the Supreme People’s Court in Beijing has ruled that authorities should have tolerated messages posted about the illness in a group chat, even if they were not completely accurate. Wuhan officers were found to have wrongly punished a group of people in a messaging group sharing information about the illness.

Of course, there’s still plenty of evidence that Beijing is still obscuring the true extent of the outbreak.

Rare decision by #China top court that gets at Beijing transparency over virus. Court ruled #Wuhan medical workers accused by police of spreading rumors due to online chat about SARS-like illness were mistreated. China signaling wants locals to share info. https://t.co/XRQu9w1TUA

We reported earlier that frustrated Chinese have been defying the government censors: “We gave up our rights in exchange for protection,” one Weibo user wrote in a post. “But what kind of protection is it? Where will our long-lasting political apathy lead us?”

Watch Live: WHO Reveals Decision On Coronavirus ‘Pandemic’ Status

After a brief delay, the WHO is finally ready to hold a press conference to discuss the outcome of its third straight emergency session.

A few hours ago, the CDC confirmed the first case of human-to-human transmission in the US, bringing the total number of countries that have recorded human-to-human cases to four (Germany, Japan, South Korea, Thailand and the US).

The WHO is now widely expected to label the nCoV breakout a global pandemic, potentially triggering another leg lower in stocks.

After flat-lining over the last several years, gold mine output fell by 1% in 2019. This is further evidence that we could be heading into a long-term and perhaps irreversible decline in gold mine production.

According to the World Gold Council, total gold mine output in 2019 came in at 3,463.7 tons.

A particularly weak fourth quarter drove the overall decline in gold production. Mine output fell 2% year-on-year in Q4 to 859.5 tons. According to the WGC, it was the lowest level of fourth-quarter mine output since Q4 2016.

Gold production declined year-on-year in every quarter of 2019.

Although last year marked the first absolute decline in gold production since 2008, it continues a general trend of falling mine output. Gold mine production was up a modest 77.72 tons between 2015 and 2016, 33.92 tons between 2016 and 2017, and 28 tons between 2017 and 2018.

Historically, mine production has generally increased every year since the 1970s. There was a drop in production in 2008, but that was something of an anomaly, as it occurred at the onset of the 2008 financial crisis. The recent slowdown in mine production is more concerning. In fact, many people speculate we may be at or near “peak gold.”

Peak gold is the point where the amount of gold mined out of the earth will begin to shrink every year. Some prominent players in the mining industry think we’re close to that point.

Over the last couple of years, several gold-mining executives have warned we have found most of the world’s minable gold.

For instance, last year, Goldcorp chairman Ian Telfer said, “We’re right at peak gold here.” And during the Denver Gold Forum in September 2017, World Gold Council chairman Randall Oliphant said he thought the world may have already reached that point. Franco-Nevada chairman Pierre Lassonde has also indicated he expects a significant dip in gold production in the coming years. And last spring, a report in Deutsche Welle made the case that we’re approaching peak gold.

Case in point – South Africa was once the world’s leading gold producer. It’s now dropped to number nine globally. In 2018, a study came out saying South Africa could run out of gold within four decades. Analysts say that at current production levels, the country has only 39 years of accessible gold reserves remaining.

China ranks as the world’s largest gold producer. Chinese mine output fell 6% y-o-y in 2019, marking the third consecutive year of decline.

Overall gold supply was actually up about 2% in 2019 due to a surge in recycling with gold prices on the rise. According to the WGC Recycled gold supply rose 16% y-o-y in Q4, totaling 335 tons. This brought the annual supply of recycled gold to 1,304.1 tons in 2019. That was the highest total since 2012.

But recycled metal cannot meet demand over the longterm.

The biggest problem facing miners is that the easy to mine gold has mostly been dug out of the earth. We’ve had a three-decade decline in the discovery of new gold deposits despite increases in exploration funding. CFRA Research analyst Matthew Miller told Deutsche Welle that gold miners are struggling to grow reserves in line with production.

“The largest and most prolific reserves have already been found.”

Even with gold prices rising, mining companies are having a difficult time coving the higher cost of mining the harder to reach, lower-quality deposits of gold left in the earth.

“We continue to try and manage costs in order to ensure the sustainability of the operations. Given the above-inflation increases in wages (approximately 50% of operating costs) and electricity prices (approximately 20% of operating costs), this has been a challenge,” Senior vice president at Sibanye-Stillwater James Wellsted told MoneyWeb.

When we look at the future of gold, it’s easy to get caught up in the latest geopolitical turmoil or the most recent policy pronouncement by the Federal Reserve. Of course, it’s important to keep abreast of the latest developments in the news cycle. But investors should never lose sight of the most basic fundamentals – supply and demand. The gold industry may well be entering a long-term — and possibly irreversible — period of less available gold. As mining companies find it more difficult to pull gold out of the earth, it will mean less gold for refiners to produce for the consumer market. Remember, gold gets its value from its scarcity.

Dershowitz: Media ‘Willfully Distorted’ Comments – Challenges Haters To Debate

Alan Dershowitz slammed the media on Thursday for ‘willfully distorting’ his arguments in defense of President Trump during Wednesday’s impeachment trial in the Senate.

In particular, Democrats and the MSM took issue with Dershowitz’s description of the legal boundaries governing a presidential quid pro quo.

“If a president does something which he believes will help him get elected in the public interest, that cannot be the kind of quid pro quo that results in impeachment,” Dershowitz argued on Wednesday – which many media outlets construed as suggesting that the President has virtually limitless power.

“They characterized my argument as if I had said that if a president believes that his reelection was in the national interest, he can do anything,” said Dershowitz, who accused CNN, MSNBC and other news outlets of mischaracterizing his comments.

“I said nothing like that, as anyone who actually heard what I said can attest.“

They characterized my argument as if I had said that if a president believes that his re-election was in the national interest, he can do anything. I said nothing like that, as anyone who actually heard what I said can attest.

He goes on to explain that he was arguing that a president who acts in both self-interest and the national interest cannot “by itself – necessarily be deemed corrupt.”

I said that the 3rd was often the reality of politics and that helping one’s own re-election efforts cannot — by itself— necessarily be deemed corrupt.

I did not say or imply that a candidate could do anything to reassure his reelection, only that seeking help in an election is not necessarily corrupt, citing the Lincoln and Obama examples. Critics have an obligation to respond to what I said, not to create straw men to attack.

Kellyanne Conway: “Our crack group of attorneys… are doing an amazing job of not preening for the cameras and not being partisans politicians, frankly, but lawyers.” pic.twitter.com/kcaKZOLnD9

The American public would be informed better by a debate than by childish epithets such as those that are being hurled at me by partisan pundits, academics and politicians. Please respond if you accept.

{kind=link}

{kind=link}