GE Freezes Pension Benefits For 20,000 Employees To Lower Debt Burden

In what looks like a dry run of the looming pension crisis facing corporate America, GE said on Monday that it would freeze pension plan benefits for 20,000 American employees with salaried benefits, WSJ reports. The company also plans to freeze supplementary benefits for roughly 700 employees who became executives before 2011 in an attempt to shave as much as $8 billion off its long-term pension deficit.

With GE shares down 20% since Larry Culp took over as CEO last year, the CEO who was supposed to rescue the company’s perennially-languishing share price is facing pressure to cut GE’s debt burden amid a downturn in the company’s power-equipment business, Bloomberg reports.

To offset the cuts, the company is planning to pre-fund $4 billion to $5 billion of the retirement obligations it’s anticipating for 2021 and 2022 (the obligations are owed according to the Employee Retirement Income Security Act, or Erisa).

The money will come from $38 billion GE expects to net from divestitures and savings from the pension freezes.

GE’s plans to offer 100,000 former employees who haven’t yet started collecting retirement benefits the option of a lump sum, in effect buying them out of the company’s retirement obligations. It expects roughly one-fifth of those offered to accept the buyout.

The company’s shares climbed 2% on the news in premarket trading.

The cuts are part of an already-announced net debt reduction plan intended to shave between $9 billion and $11 billion off GE’s debt burden, helping to lower the company’s leverage ratio to roughly 2.5x net debt to EBITDA by the end of next year.

“Returning GE to a position of strength has required us to make several difficult decisions, and today’s decision to freeze the pension is no exception,” said Kevin Cox, GE’s chief human resources officer, in a statement.

GE closed its pension plan to new entrants at the start of 2012.

While several states, including Illinois and New Jersey, have opted recently to start reducing their pension shortfalls, US corporations are often in even worse shape than the public sector. But these cuts should help forestall the pension nightmare facing the US, if only for a little while.

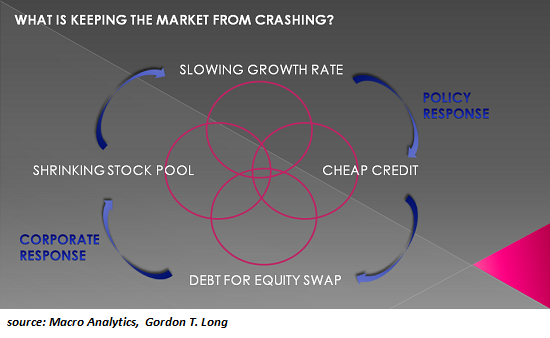

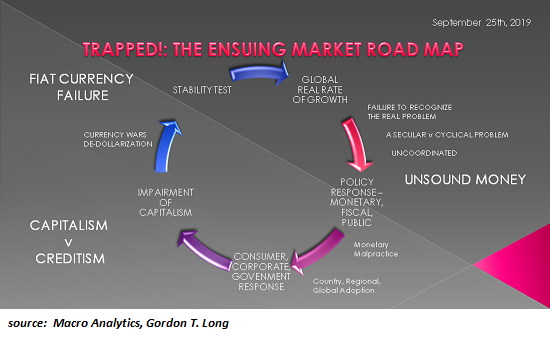

The Fed’s nearly free money for financiers policies in support of the Super-Rich do not exist in a vacuum – the disastrous consequences are already baked in.

What’s holding up the U.S. stock market? The facile answer is the Federal Reserve (“the Fed has our back,” “don’t fight the Fed,” etc.) but this doesn’t actually describe the mechanisms in play or the consequences of a market that levitates ever higher on the promise of more Fed money-for-nothing injected into the diseased veins of the financial system.

As Gordon T. Long and I discuss in our latest half-hour video program, What’s Holding the Market Up? (34 minutes), the primary prop under stock valuations are corporate buybacks, which total in the trillions of dollars since the 2008-09 Global Financial Meltdown and the Fed’s “rescue of the rich,” which continues to this day.

Rather than risk capital in productive investments, U.S. corporations have borrowed trillions of dollars and used the cash to buy back their own shares. The Fed’s suppression of interest rates has incentivized stock buybacks in several ways:

1. When it’s cheap to borrow billions, the biggest bang for the buck is to use the borrowed bucks to buy back shares, which creates an illusion of growth as per-share sales and earnings both rise as shares are withdrawn from the public market.

Let’s say a company has a million shares outstanding and earns a net profit of $1 million. The per-share net profit is thus $1 per share. If the company borrows money and buys back 500,000 shares of its own stock, the per-share net earnings double to $2 per share.

Presto-magico, the company appears to be more profitable, and so its valuation based on its price-to-earnings ratio (P-E) adjusts higher, even though revenues and earnings have remained stagnant.

2. If a corporation piles up cash, it becomes an attractive target for acquisition. The way to avoid being taken over is to pile up debt (borrow money or sell corporate bonds, swapping debt for equity) and use the funds to buy back shares. As the corporation’s remaining shares soar in value, the company can use its own shares to acquire rivals.

These perverse incentives are the heart of the Federal Reserve’s policies, as depicted here: as real economic growth has slowed, the Fed’s largesse of cheap money has flowed into corporate buybacks because that’s what’s incentivized.

The Fed’s nearly free money for financiers policies in support of the Super-Rich do not exist in a vacuum–the disastrous consequences are already baked in. As Gordon’s chart shows, Fed policies effectively replace capitalism (investing capital productively and accepting risk) with creditism, a debt-dependent speculative system that transfers risk to the Fed and the taxpayers (i.e. profits are private, losses are socialized).

Needless to say, this doesn’t end well, as expanding credit and borrowing to fund speculation and consumption inevitably ends in a currency crisis that devalues the currency for everyone, rich and poor alike.

We’ve all read the headlines. America incarcerates the most people, and does so at the highest rate, of any country in the world. In 2017 there were 1.5 million people in U.S. prisons and another 745,000 in jail. This means that the U.S. incarcerates at a rate that is 5-6 times higher than countries like Germany, the U.K., and France, and has a higher number of inmates than the reported figures for China and Russia. The U.S. numbers also are dramatically large when compared to our own history, as the prison population increased more than 700% since the early 1970s. Small wonder that “mass incarceration” is now the standard label to describe the state of U.S. corrections.

Despite the gloomy big picture, there are some reasons for optimism. States—which house almost all the inmates—are well aware of the situation, and some have been impressively active (and even more impressively, bipartisan) in addressing it. Many states have created criminal reform commissions whose goal is to reduce the incarceration rates, and over the last few years there has been a modest to significant drops in the number of people behind bars, although the numbers are still high. (Reports on state efforts can be found here, here, and here).

Targets of reform vary, but there are some usual suspects: efforts to reduce the prison population often focus on reducing mandatory minimums, reducing the sentences for certain drug crimes, and modifying 3-strikes laws. Efforts to reduce jail populations are increasingly targeting bail decisions and the effect of money bail on keeping poor arrestees behind bars.

But while the recent decline in prison populations is real, there are also reasons to wonder. Given the size of the U.S. inmate population and the extremely high rate at which we put people behind bars, will any reform efforts be enough to shed the “mass incarceration” label?

Over the next few posts I will be discussing this question, and (to cut to the chase) conclude that the answer is, sadly, no. There are both obvious and subtle barriers to reducing the inmate population to levels, ones that range from difficult to near-impossible to overcome. The size of the problem, the difficulties posed by violent crime, and the under-appreciated financial costs of reform all conspire to make it likely that any change will be marginal rather than dramatic. This series of posts will conclude with some suggestions on how we might approach these barriers, even if there are no guarantees that they will be overcome.

But before turning to the problems, two preliminary points:

1. Maybe this whole exercise is misguided. People are in prison (mostly) because they commit crimes, and so we might view incarceration simply as the inevitable byproduct of crime, prosecution, and conviction. Stated differently, maybe we don’t have a mass incarceration problem, maybe we have a “mass criminality” problem, one that is more deserving of our attention.

Interestingly, both advocates and skeptics of efforts to reduce incarceration rates cite the intersection of imprisonment and crime rates to support their views. Reformers argue that while the crime rate has been steadily dropping since the mid-1990s, incarceration rates continued to climb for another 15 years—surely proof that as a society, we have simply become more punitive. Skeptics respond that of course crime declined while incarceration rates increased: that’s the whole point. Whatever its other flaws, prison incapacitates those who are the most likely to engage in future crime, making mass incarceration a feature, not a bug.

The relationship between crime and incarceration rates is complex, and to wildly over-simplify the research, it appears that:

Increased incarceration rates have had a meaningful effect on reducing crime, particularly in the early years of rapid prison growth. It is hard, however, to fix precisely the size of this effect.

The continued high incarceration rates seem to provide a vanishingly small return in terms of crime reduction. As the National Research Council put it, “The incremental deterrent effect of increases in lengthy prison sentences is modest at best. Because recidivism rates decline markedly with age, lengthy prison sentences, unless they specifically target very high-rate or extremely dangerous offenders, are an inefficient approach to preventing crime by incapacitation.”

Still, regardless of the inefficiency, we know that prisons work to some degree as a tool of incapacitation, making it tempting to swing our focus away from incarceration (the symptom) and toward criminality (the disease). But we shouldn’t. Even if we can’t solve the prison problem without tackling the crime problem, there are still reasons to address the high levels of incarceration, because if we don’t, we miss the central point of the reform efforts.

Reformers argue that the status quo has two related problems. First, we now incarcerate a huge number of inmates unnecessarily—we keep too many people locked up and for too long who pose little statistical risk of reoffending, people who could be adequately sanctioned without incapacitative effect of prison. (Note that this argument does not come to grips with the retributive role that prison plays, a huge topic that requires a separate discussion.) Second, incarcerating people who do not pose a risk to society does affirmative harm: low-risk inmates who spend too much time around high-risk inmates become worse off, reducing their chances of successfully reentering society once they are released. It is worth our efforts to identify these people, regardless of the levels of crime in society.

2. It is shortsighted to discuss incarceration without acknowledging its intersection with race and poverty. The percentage of African Americans behind bars is substantially greater than their percentage of the population, a situation that has been true for decades. The high percentage of criminal defendants who poor has a similarly long history.

The merger of prison-reduction efforts with efforts to reduce the disproportionate effect on race and class raises wickedly complex questions. We might assume that reducing the prison population would inevitably benefit minorities and the poor, because currently they are so overrepresented among the incarcerated. But what if the reform efforts were to make the imbalance worse? Suppose, for example, that in looking for people who don’t really “need” to be behind bars, we decide that those who commit corporate offenses should qualify. If this reform would disproportionately help the wealthy and increase the ratio of poor inmates, is it still a good idea?

Not surprisingly, I don’t have solutions that will untangle the threads of incarceration, race, and poverty. But it is important when thinking about change to keep in mind the moral and political implications of these moves, and to remember that the “incarceration problem” is just as subject to the law of unintended consequences as every other reform effort.

In the next post, we’ll begin at the beginning and ask what we mean by mass incarceration, and then look at some numbers to decide if there is any realistic hope of shedding that label.

from Latest – Reason.com https://ift.tt/2LRkI4g

via IFTTT

S&P Futures Rebound From Session Lows As Traders Ignore Trade Talks On Verge Of Unraveling

Global stocks were little changed on Monday as U.S. equity indexes rebounded from session lows despite a Bloomberg report China was set to reject a broad trade deal with the Trump administration, which sent the yuan sliding. European stocks gained and Treasuries fluctuated after Friday’s generally favorable US jobs data quelled some fears about an economic slowdown.

Emini S&P index futures came off session lows but still pointed to a weak start on Wall Street after Bloomberg reported that senior Chinese officials have indicated the range of topics they’re willing to discuss at upcoming talks has narrowed considerably.

The Stoxx Europe 600 index climbed as energy and telecoms shares advanced while the Stoxx 600 Automobiles & Parts Index fell as much as 1.4%, making it the worst-performing group on the broader gauge, with declines led by car-parts makers including Valeo, Continental and Faurecia. European shares rebounded from early negative prints after the latest drop in German industrial orders data (-6.7% Y/Y) underscored concerns about a looming recession in Europe’s largest economy.

Separately, morale among Eurozone investors dropped in October to its lowest level in more than six years as stimulus measures taken by central banks failed to allay recession fears, a survey by the Sentix research group showed. Besides the steady trickle of weak economic data, investors also had their eyes on U.S.-China trade talks. Bloomberg reported that Chinese officials are signaling they are increasingly reluctant to agree to a broad trade deal pursued by U.S. President Donald Trump.

Earlier in the session, Asian stocks rallied following Friday’s torrid Wall Street short-squeeze , with MSCI’s broadest index of Asia-Pacific Shares outside Japan rising 0.1%. Japan’s Nikkei stock index opened higher but reversed course and fell 0.2%. A key Japanese economic index fell in August and the government downgraded its outlook for the economy to “worsening”, suggesting export-reliant Japan could slip into recession. Shanghai markets are yet to re-open after China’s holidays, while Hong Kong was also shuttered for a holiday, leaving traders with limited options to respond to escalating violence in the city, where protesters set fires and vandalized train stations and banks over the weekend. The yuan dropped in offshore trading by the most since late September.

Stocks globally took a battering last week, falling to their lowest level in over a month on fears of a U.S. economic slowdown. But positive U.S. jobs data on Friday helped spark a turnaround. “I think the fact that the U.S. jobs report was broadly positive really put the brakes on the fear factor that was circulating last week – that the U.S. has been hit hard by the trade war,” said David Madden, market analyst at CMC Markets in London.

So far concerns about a Trump impeachment have yet to appear in markets: an impeachment drive by U.S. Democrats over a whistleblower’s allegations that Trump leveraged $400 million in aid to secure a promise from Ukraine’s President to investigate political rival Joe Biden will continue this week. Several U.S. diplomats will head to Capitol Hill for closed-door testimonies. On Sunday, lawyers said a second whistleblower had come forward to substantiate the first complaint from an unnamed U.S. government official, which touched off the investigation.

“I think it’s fair to say the second whistleblower coming forward will be an issue for Trump. This strengthens China’s bargaining position in the trade war,” Madden said.

Investor focus will now shift back to foreign trade this week as Chinese Vice Premier Liu He and an entourage of officials head to Washington to resume talks with their U.S. counterparts. As economic indicators flash warnings, traders have been ramping up bets for further Federal Reserve rate cuts. They’ll search for new clues on the policy path when minutes from the latest Fed meeting are released in coming days.

In geopolitics, Turkish President Erdogan and US President Trump discussed in a telephone conversation the plan to establish a safe area east of the Euphrates in Syria. Erdogan expressed unease with the US military and added that security bureaucracies are not doing what is necessitated by the agreement between US and Turkey. President Trump agreed to meet with Erdogan in Washington next month, upon Trump’s invitation. US White House confirmed the call between the two Presidents and notes that US will not be involved or stand in the way of Turkey’s long planned operation into Northern Syria. Turkey will now be responsible for all ISIS fighters captured in Northern Syria.

In Brexit news, PM Boris Johnson is reportedly willing to go to the Supreme Court to avoid having to write a letter asking for a delay to Brexit, as set out in the Benn Act, according to sources. Senior UK Government figures are reportedly considering a series of proposals to “sabotage” EU’s structure if Brussels does not agree to a new deal or lets UK PM Johnson leave the bloc without one, according to sources. Plans under consideration include blocking the EU’s 2021-27 budget which is due to be agreed early 2020.

Concluding the overnight session, US Treasuries were largely steady Monday, with the curve steeper and the long-end having underperformed during Asian session and early European trading, which was muted. There were gains during the Asia session amid reports that China may be increasingly reluctant to agree to a broad trade deal, but these were broadly unwound as S&P 500 futures pared earlier decline. Yields rose by around 2bps at the long-end of the Treasury curve, up to 1.5375%, while the 2s10s remains within a basis point of Friday’s close.

Euro zone government bond yields were little changed with the German 10-year Bund yield falling 0.4 basis points to -0.59%. Portuguese bonds were also supported by news on Friday that DBRS has upgraded Portugal’s credit rating.

In currencies, the dollar was 0.1% higher against a basket of peers. The euro was 0.1% lower at $1.0967 while Sterling fell as investors fear Britain and the European Union are no closer to agreeing a Brexit withdrawal deal. The Swedish krona and the Australian dollar led G-10 currency losses as risk appetite weakened amid signs that Washington and Beijing may struggle to make headway in trade talks this week. The Norwegian krone slipped on a manufacturing slump. The Swiss franc rallied amid a risk-off tone in markets

Market Snapshot

S&P 500 futures down 0.3% to 2,946.00

STOXX Europe 600 up 0.05% to 380.40

MXAP up 0.04% to 155.59

MXAPJ up 0.07% to 497.65

Nikkei down 0.2% to 21,375.25

Topix down 0.01% to 1,572.75

Hang Seng Index down 1.1% to 25,821.03

Shanghai Composite closed for holiday

Sensex up 0.1% to 37,723.81

Australia S&P/ASX 200 up 0.7% to 6,563.56

Kospi up 0.05% to 2,021.73

German 10Y yield fell 1.4 bps to -0.6%

Euro down 0.1% to $1.0966

Brent Futures up 0.6% to $58.71/bbl

Italian 10Y yield rose 0.5 bps to 0.493%

Spanish 10Y yield fell 1.9 bps to 0.113%

Brent Futures up 0.6% to $58.71/bbl

Gold spot down 0.2% to $1,502.14

U.S. Dollar Index up 0.2% to 98.96

Top Overnight News

Chinese officials are signaling they’re increasingly reluctant to agree to a broad trade deal pursued by President Donald Trump, ahead of negotiations this week that have raised hopes of a potential truce

German factory orders declined further in August, aggravating an industrial slump that has pushed Europe’s largest economy to the brink of recession

The European Central Bank’s latest stimulus salvo is failing to spark animal spirits, with investor sentiment in the region falling to the lowest level in more than six years. The Sentix economic index for the euro area dropped to -16.8 in October, the weakest level since April 2013

Prospects of a Brexit deal faded after talks between the two sides stalled and European leaders cast doubt on reaching an agreement in time for the Oct. 31 deadline.

The Japanese government cut its formula-based assessment of the economy to indicate that economic conditions were worsening in August, an outcome signaling a higher risk that Japan could be entering a recession.

Asian equities traded mixed after initially opening higher following the US jobs report, which was robust enough to temper recession fears but lacklustre enough to keep the Fed on track to cut rates again in October, albeit upside in the region is capped amid reports that China is narrowing scope for a trade deal with the US ahead of talks in Washington this week. ASX 200 (+0.7%) was kept afloat by mining names after base metals posted gains late Friday, meanwhile Nikkei 225 (-0.2%) traded lower throughout the session as exporters were pressured by an unfavourable currency. Elsewhere KOSPI (U/C) shrugged off the breakdown of North Korea/US denuclearisation dialogue on Sunday as South Korea focused on the upcoming large-cap earnings, with heavyweight Samsung Electronics expected to announce its Q3 guidance tomorrow. As a reminder, Hong Kong and Mainland China were closed due to public holidays. In Hong Kong a second teenager has been shot in the leg by police and is in a serious condition, according to Sky News citing sources. It is not clear if the teenager was shot by a rubber bullet or a live round.

Top Asian News

Hong Kong Activists Urge New Rallies as Stricken City Cleans Up

HSBC to Cut Up to 10,000 Jobs in Cost-Cutting Drive: FT

Singapore Convicts 2 Traders of Fraud in Futures Contracts

India’s Shadow Banking Crisis Tests Stock Bulls’ Faith in Rally

Major European indices (Euro Stoxx 50 +0.2%) are little changed, after a weekend report alleged that China is narrowing scope for a trade deal with the US ahead of principle-level talks in Washington this week, with Chinese officials this week expected to offer a deal that doesn’t include anything on industrial policy or subsidies. Some desks tried to frame the reports as a positive, arguing that such concessions from China at this stage were very unlikely anyway, and adding that the article also talked about the possibility of the US and China making progress on a “mini deal” (where China could agree to making large-scale agricultural/energy purchases from the US and alter some IP practices in exchange for the US rolling back a partial amount of the existing tariffs). Such a mini deal, as hinted by the report, would likely exceed expectations for the talks, as most investors look for something more akin to a truce rather than any meaningful de-escalation. However, US President Trump has repeatedly shot down the prospect of any mini-deal, saying he would rather a full and comprehensive deal. As such, China’s refusal to engage with key US demands is likely to be seen as a negative for the long-term prospects of a comprehensive trade deal between the two sides. The sector layout is reflective of fragile risk sentiment; the defensive Utilities (0.3%), Consumer Staples (+0.4%) and Health Care (+0.6%) sectors are well supported while Consumer Discretionary (-0.1%), Tech (U/C) and Industrials (-0.1%) are underperforming. In terms of individual movers; Osram Licht (-4.3%) shares sunk after ASM (-3.3%) failed in its takeover bid for the Co., but said it would explore further strategic options to pursue the acquisition, with ASM shares pressured over investor concerns about the companies continued pursuit of the German lighting company. HSBC (-0.4%) shares were under pressure on the news that the Co. is to undertake a cost-cutting programme, which may affect 10k jobs. Bayer (2.5%) shares moved higher on the news that its October 15th trial date for the its US glyphosate case had been delayed until February 2020 (indicatively February 10th). Finally, LSE (U/C) opened higher after the Co. set a Wednesday deadline for the Hong Kong Exchange to place a revised takeover offer.

Top European News

Lira Weakens as Turkey Readies Military Incursion Into Syria

Euro-Area Investor Sentiment Drop Highlights ECB Stimulus Limits

EU Summit Could Be a Game Changer on Brexit, Pound Options Show

Greece Sees Growth in 2020, Putting It on Track for Fiscal Goals

in FX, the Aussie and Kiwi are bearing the brunt of renewed trade and geopolitical tensions having benefited from initial/brief Greenback weakness in the aftermath of last Friday’s ‘Goldilocks’ US jobs report. China is reportedly setting a limited agenda for talks in Washington this week, while discussions between the US and North Korea about denuclearisation were cut short over the weekend as an envoy from Pyongyang called for the Trump administration to withdraw hostile policy. Moreover, Turkey is back in the headlines with a resumption of drilling off Cyprus and operations in Northern Syria, while efforts to quell protests in Hong Kong have failed to prevent more violence and clashes. Aud/Usd is back below 0.6750 and Nzd/Usd has lost grip of the 0.6300 handle even though the Aud/Nzd cross is straddling 1.0700 amidst a bearish call from ANZ for the Kiwi to hit 0.5900 vs the Buck by Q1 next year.

SEK/GBP – The other major underperformers as the Swedish Krona continues to lament last week’s contractionary manufacturing and services PMIs alongside relatively downbeat Riksbank rhetoric via Jansson, while Sterling is suffering from fresh UK political and Brexit jitters following a lukewarm reception to PM Johnson’s proposals for the Irish border and ultimatum from the EU to alter the alternative plan by the end of the week. Eur/Sek just notched a new 2019 peak over 10.8700 and Cable has slipped back below 1.2300 with Eur/Gbp nestling above 0.8900.

CHF/JPY – In contrast to other G10 currencies, and despite the Dollar’s overall recovery from post-NFP lows (DXY nudging 99.000 again vs 98.720 at one stage on Friday), the Franc and Yen are both holding firm with Usd/Chf pivoting 0.9950, Eur/Chf hovering above 1.0900 and Usd/Jpy meandering between 107.02-106.58. Safe-haven positioning is impacting to an extent, while the Franc is also consolidating after recent quite hefty losses and the Yen is contained by decent option expiries in close proximity (1.5 bn at 106.70, 1.2 bn from 107.00-10 and 1.1 bn from 107.40-50).

EUR/CAD – The single currency is still hugging a tight line just under 1.1000 against the Greenback, and not too perturbed by yet more evidence of Eurozone economic woes in the form of German factory orders and Sentix sentiment, but the headline pair may constrained by expiry interest like Usd/Jpy given 1.4 bn sitting at 1.0950-60 and 1.1 bn at 1.0990-1.1000 into the NY cut. Elsewhere, the Loonie is trying to cap losses south of 1.3300 following Friday’s collapse in both measures of the Canadian Ivey PMI.

EM – Broad losses vs the Usd, with the Try undermined by the aforementioned Turkish factors and not deriving much in the way of support from President Erdogan lauding the CBRT for its policy actions, albeit anticipating more easing ahead. The Lira has been sub-5.7550, but now paring back.

ANZ forecasts NZD/USD to 0.5900 by end of March 2020 and 0.6100 by end of June next year, citing RBNZ lower cash rate and uncertainty surrounding capital decision, ANZ sees the OCR at 0.75% in May 2020 (currently 1.00%)

In commodities, crude markets advanced on Monday, erasing losses seen at the futures open on Sunday night, where prices had initially been pressured by seemingly negative US/China trade headlines over the weekend; WTI Nov’ 19 and Brent Nov’ 19 futures have reclaimed the USD 53.00/bbl and USD 58.50/bbl levels to the upside respectively. Supply side factors could be providing some support; Chinese State Oil Company pulled out of a USD 5bln deal to develop a portion of Iran’s offshore natural gas field amid the country’s escalating tensions with the US. Moreover, on Friday, reports emerged that the Buzzard oilfield in the North Sea has been shut temporarily for pipework repairs, with no timeline on how quickly operations will return to normal. The Buzzard field is the key contributor to the Forties blend, says Platts, and output at the field has been running at around 120k bpd. ING conclude that “an extended outage would likely provide some relative support to Brent”. Elsewhere, Russian Energy Minister Novack said Russia should lower oil industry taxes and put into production some 10bln tonnes of oil reserves, before adding that Russia’s oil output will decline in the coming years if it does not change taxation laws. Novak also said he considers a mid-term oil price in the USD 50s are fair. In terms of metals, Copper and Gold prices moved lower on Monday but are cautious within recent ranges ahead of this week’s key risk events, which include US/China trade talks, FOMC and ECB Minutes, US CPI and a slew of Fed speak including a triple appearance from Fed Chair Powell. ING observe that the PBOC added 0.19mln/oz of gold to its reserves in the month of September, taking total reserves to 62.64mln/oz, a tenth consecutive month of gold purchases by China, which the bank says reflects the diversification drive away from the US dollar at a time of trade friction with the US. “Gold demand from Central Banks and ETFs has been stronger this year on economic and geopolitical concerns” the bank adds, “however higher prices have started to weigh on retail demand”, which recently is most evident in the large fall in demand by its usual largest buyer, India.

US Event Calendar

Oct. 7-Oct. 11: Monthly Budget Statement, est. $82.5b, prior $119.1b

3pm: Consumer Credit, est. $15.0b, prior $23.3b

DB’s Jim Reid concludes the overnight wrap

If you bump into me today check yourself over afterwards as the school fun run I went to yesterday was a “colour run”. The whole family got repeatedly sprayed and covered with various colour dyes and we spent the rest of the day finding it everywhere even after a bath. My bed this morning looked like one of those murder scenes on telly where the outline of the dead body has been chalked out. Well a multi-coloured version.

Following a turbulent and colourful week for markets which saw further evidence of deteriorating growth but increased Fed cut expectations that led to a v-shaped recovery in US equities, the focus this week turns to the scheduled trade talks between the US and China. It’s not a big week for data with US CPI (Thursday), PPI (Tuesday) and UoM consumer confidence (Friday) the highlights even if they will be seen as backward looking and less relevant to the current Fed debate. Comments from Fed Chair Powell and numerous other Fed officials will also be in focus, along with the FOMC minutes (Wednesday). Finally Brexit talks reach a crucial juncture with time ticking down.

On trade, Chinese Vice Premier Liu He is due to visit Washington for talks with meetings expected to take place on Thursday and Friday with the mood music in recent days seemingly more positive. However Bloomberg published a story last night that suggested that the Chinese are “increasingly reluctant to agree to a broad trade deal” and that the “range of topics they’re willing to discuss has narrowed considerably”. The same report also added that Vice Premier Liu He is likely to bring an offer that won’t include commitments on reforming Chinese industrial policy or government subsidies that have been the target of longstanding US complaints. So if the article is true the stakes have been raised ahead of these talks.

This news is holding back the Asian session after a strong end to the week in NY on Friday. The Nikkei (-0.24%) is trading down while the Kospi (+0.15%) is up in thin trading. Markets in China and Hong Kong are still closed for their week long holiday. The offshore Chinese yuan is trading weak (-0.31%) this morning while yields on 10y USTs are down -1bps. Elsewhere, futures on the S&P 500 are down -0.45%.

Back to the week ahead and in terms of Fedspeak, most attention will be placed on Fed Chair Powell who speaks tomorrow at a NABE meeting in Denver and then on Wednesday at a Fed Listens Event in Kansas. Comments are also due from Kashkari today, Evans and Kashkari on Tuesday, Mester and Bostic on Thursday and Kashkari, Rosengren and Kaplan on Friday. Also of note from the Fed will be the FOMC minutes from the September meeting due on Wednesday. As a reminder, the dot plot projections revealed sharp divisions within the Committee however the signals from the meeting still indicated a continued dovish bias. That being said, data since has mostly deteriorated.

Brexit will continue to take center stage headlines wise but it’s still doubtful we’ll know much more about the end game by the end of the week. The EU need the U.K. to improve their proposals to intensify the talks but such improvements would likely lose Mr Johnson’s Parliamentary ability to get any deal passed. So stalemate is the most likely. The most intriguing question for the next 12 days is how Mr Johnson intends to try to bypass the extension letter he’ll be legally forced to write by October 19th if he fails to get a deal. Interestingly the one opinion poll released over the weekend gave Mr Johnson and the Tories 38% of the vote and a lead of 15%. So if this is to be believed the hard line stance is seemingly paying off electorally. However it’ll be interesting to see if he gets the blame if the U.K. doesn’t leave by October 31st and losses support or whether he can continue to win enough of the “Parliament vs the people” argument to sweep up the leave vote while the remain vote is split.

Looking back to last week, Friday’s much-anticipated jobs report, coming after jarringly poor ISM surveys earlier in the week, ended up being a bit of damp squib with something for both the bulls and the bears. The headline change in payrolls was slightly below consensus (136,000 versus 145,000), but the employment rate fell 0.2pp to a new 50-year low of 3.5%. The private payrolls figure was similar, coming in at 114,000 compared to expectations for 130,000. These misses were offset somewhat by a healthy +45,000 net revision to the previous two months. More interestingly, wage growth was flat on the month, taking the year-on-year figure to 2.9%, its weakest pace in a year. Our economists think this will make the Fed more confident that the natural rate of unemployment has fallen, which should still enable them to cut rates later this month.

Markets took the jobs report as something of a “goldilocks” outcome; job growth continues but inflationary pressures remain muted. The S&P 500, which was down -3.57% on the week at its Thursday lows, managed to retrace to end the week just -0.33% lower (+1.42% on Friday). The DOW and NASDAQ (down as much as -4.01% and -3.02%) trended similarly, ending the week -0.92% and +0.54% (+1.40% and +1.42% Friday). In Europe, the STOXX 600 had been down an even steeper -4.37%, and ended the week still -2.95%, having missed the last part of the Friday rally (+0.73% Friday). The rebound was helped by a further drop in yields, with 10-year treasury yields ending the week -15.1bps (-0.5bps Friday). Bund yields were less exciting, ending the week -1.3bps lower (+0.4bps Friday). Meanwhile at the front end, the market moved to price in more rate cuts, with two-year treasury yields down -22.8bps on the week (+1.4bps Friday). That means the 2y10y curve steepened +7.1bps on the week to 11.9bps (-2.3bps Friday).

Chair Powell’s comments on Friday were mostly uneventful, though at the margin they were not as dovish as the market was expecting, with yields rising around 1bp and the dollar weakening slightly after the headlines hit the wires. Powell cited the strong labour market, but didn’t comment on Friday’s jobs report, and said that overall the economy is in a good place. It’s likely that he wants to confer with his FOMC colleagues to gauge their views regarding an October rate cut before he gives a firm signal either way. The market is pricing around an 80% chance for a cut this month, down from around 90% at the peak on Thursday. Meanwhile, Kansas City Fed President Esther George, a hawk, said overnight that she dissented against rate cuts at the past two policy meetings because the US economy is currently doing well, but she would be prepared to support a further reduction should she see evidence of a sharper slowing of growth. She said, “the moderation of economic growth in 2019 has been in line with my own outlook that calls for a gradual decline to a trend level over the medium term. ” Fed’s Rosengren, also a hawk, spoke over the weekend and said “If the economy grows at 1.7%, consumption continues to be strong, inflation is gradually going up and the unemployment rate is at 3.5%, I would not see a need for additional accommodation” at the Fed’s October or December policy meetings. This even as he acknowledged that economic reports on manufacturing, services and payrolls came in weaker last week than he anticipated but cited that the labor market remains tight and said he’s confident the U.S. consumer will continue to drive growth. So the hawkish Fed officials are continuing to shy away from a pivot towards a rate cut at this month’s meeting.

We’ve all read the headlines. America incarcerates the most people, and does so at the highest rate, of any country in the world. In 2017 there were 1.5 million people in U.S. prisons and another 745,000 in jail. This means that the U.S. incarcerates at a rate that is 5-6 times higher than countries like Germany, the U.K., and France, and has a higher number of inmates than the reported figures for China and Russia. The U.S. numbers also are dramatically large when compared to our own history, as the prison population increased more than 700% since the early 1970s. Small wonder that “mass incarceration” is now the standard label to describe the state of U.S. corrections.

Despite the gloomy big picture, there are some reasons for optimism. States—which house almost all the inmates—are well aware of the situation, and some have been impressively active (and even more impressively, bipartisan) in addressing it. Many states have created criminal reform commissions whose goal is to reduce the incarceration rates, and over the last few years there has been a modest to significant drops in the number of people behind bars, although the numbers are still high. (Reports on state efforts can be found here, here, and here).

Targets of reform vary, but there are some usual suspects: efforts to reduce the prison population often focus on reducing mandatory minimums, reducing the sentences for certain drug crimes, and modifying 3-strikes laws. Efforts to reduce jail populations are increasingly targeting bail decisions and the effect of money bail on keeping poor arrestees behind bars.

But while the recent decline in prison populations is real, there are also reasons to wonder. Given the size of the U.S. inmate population and the extremely high rate at which we put people behind bars, will any reform efforts be enough to shed the “mass incarceration” label?

Over the next few posts I will be discussing this question, and (to cut to the chase) conclude that the answer is, sadly, no. There are both obvious and subtle barriers to reducing the inmate population to levels, ones that range from difficult to near-impossible to overcome. The size of the problem, the difficulties posed by violent crime, and the under-appreciated financial costs of reform all conspire to make it likely that any change will be marginal rather than dramatic. This series of posts will conclude with some suggestions on how we might approach these barriers, even if there are no guarantees that they will be overcome.

But before turning to the problems, two preliminary points:

1. Maybe this whole exercise is misguided. People are in prison (mostly) because they commit crimes, and so we might view incarceration simply as the inevitable byproduct of crime, prosecution, and conviction. Stated differently, maybe we don’t have a mass incarceration problem, maybe we have a “mass criminality” problem, one that is more deserving of our attention.

Interestingly, both advocates and skeptics of efforts to reduce incarceration rates cite the intersection of imprisonment and crime rates to support their views. Reformers argue that while the crime rate has been steadily dropping since the mid-1990s, incarceration rates continued to climb for another 15 years—surely proof that as a society, we have simply become more punitive. Skeptics respond that of course crime declined while incarceration rates increased: that’s the whole point. Whatever its other flaws, prison incapacitates those who are the most likely to engage in future crime, making mass incarceration a feature, not a bug.

The relationship between crime and incarceration rates is complex, and to wildly over-simplify the research, it appears that:

Increased incarceration rates have had a meaningful effect on reducing crime, particularly in the early years of rapid prison growth. It is hard, however, to fix precisely the size of this effect.

The continued high incarceration rates seem to provide a vanishingly small return in terms of crime reduction. As the National Research Council put it, “The incremental deterrent effect of increases in lengthy prison sentences is modest at best. Because recidivism rates decline markedly with age, lengthy prison sentences, unless they specifically target very high-rate or extremely dangerous offenders, are an inefficient approach to preventing crime by incapacitation.”

Still, regardless of the inefficiency, we know that prisons work to some degree as a tool of incapacitation, making it tempting to swing our focus away from incarceration (the symptom) and toward criminality (the disease). But we shouldn’t. Even if we can’t solve the prison problem without tackling the crime problem, there are still reasons to address the high levels of incarceration, because if we don’t, we miss the central point of the reform efforts.

Reformers argue that the status quo has two related problems. First, we now incarcerate a huge number of inmates unnecessarily—we keep too many people locked up and for too long who pose little statistical risk of reoffending, people who could be adequately sanctioned without incapacitative effect of prison. (Note that this argument does not come to grips with the retributive role that prison plays, a huge topic that requires a separate discussion.) Second, incarcerating people who do not pose a risk to society does affirmative harm: low-risk inmates who spend too much time around high-risk inmates become worse off, reducing their chances of successfully reentering society once they are released. It is worth our efforts to identify these people, regardless of the levels of crime in society.

2. It is shortsighted to discuss incarceration without acknowledging its intersection with race and poverty. The percentage of African Americans behind bars is substantially greater than their percentage of the population, a situation that has been true for decades. The high percentage of criminal defendants who poor has a similarly long history.

The merger of prison-reduction efforts with efforts to reduce the disproportionate effect on race and class raises wickedly complex questions. We might assume that reducing the prison population would inevitably benefit minorities and the poor, because currently they are so overrepresented among the incarcerated. But what if the reform efforts were to make the imbalance worse? Suppose, for example, that in looking for people who don’t really “need” to be behind bars, we decide that those who commit corporate offenses should qualify. If this reform would disproportionately help the wealthy and increase the ratio of poor inmates, is it still a good idea?

Not surprisingly, I don’t have solutions that will untangle the threads of incarceration, race, and poverty. But it is important when thinking about change to keep in mind the moral and political implications of these moves, and to remember that the “incarceration problem” is just as subject to the law of unintended consequences as every other reform effort.

In the next post, we’ll begin at the beginning and ask what we mean by mass incarceration, and then look at some numbers to decide if there is any realistic hope of shedding that label.

from Latest – Reason.com https://ift.tt/2LRkI4g

via IFTTT

Since January 2017, litigants have alleged that President Trump is violating the Foreign and Domestic Emoluments Clauses. We have filed several amicus briefs in these cases. We contend that the phrase “emolument” used in the Constitution does not extend to business transactions for value. Rather, “emoluments” are thelawful compensation or profits that are derived from the discharge of the duties of an office.

Our briefs have discussed an important historical incident in the early years of our Republic. In 1793, President George Washington purchased four lots of land at a public auction in the new federal capital. (We wrote about the transactions here.) If an “emolument” includes anything of value, then President Washington received something of value from the Federal Government, beyond his regular salary—that is, he received the land. Therefore, he would have violated the Domestic Emoluments Clause. The better reading, we contend, is that “emolument” is limited to the lawful compensation or profits that arise from the discharge of the duties of an office. Under this position, Washington was not a lawbreaker.

However, a January 2019 report from the Office of Inspector General, General Services Administration, reached a different conclusion. The report asserted that Washington purchased private, rather than public property at the auctions. (See pp. 15-16.) Specifically, the report stated that the sales “did not provide [President Washington with] a benefit from the United States.” Therefore, Carol F. Ochoa, the Inspector General reasoned, these transactions did not implicate the Domestic Emoluments Clause. This conclusion is not correct.

Bob Arnebeck, a historian with particular expertise concerning President Washington and land transactions in the early federal capital, responded to the Inspector General’s Report. He explained that our first President purchased public, not private land. And, if there were any doubts about this record, the President’s owncorrespondences repeatedly referred to the land and the sale as “public.” We discussed the Inspector General’s error at some length on pages 5-10 of our amicus brief submitted to the U.S. Court of Appeals for the Fourth Circuit.

The Inspector General’s error was understandable. She was reviewing intricate financial and historical records from two centuries ago in an area where her office and staff may lack the requisite expertise. However, she remains unwilling to acknowledge this serious error. Tillman contacted the Inspector General’s Office multiple times, flagging the plain error in the report. Ultimately, Edward Martin, Counsel to the Inspector General wrote back:

I have reviewed the documents you sent me on April 30, 2019. The GSA OIG’s Evaluation of GSA’s Management and Administration of the Old Post Office Lease, dated January 16, 2019, is a final report and speaks for itself.

The report does not speak for itself. It is in error. And the Inspector General has taken no steps to correct a plain historical error.

On September 25, the House Committee on Transportation and Infrastructure, Subcommittee on Economic Development, Public Buildings, and Emergency Management, held a hearing on the IG’s report. We were asked to testify, but could not attend in person. Instead, we submitted a joint written statement that flagged the IG’s plain error. Our testimony was flagged at several points during the hearing.

In this exchange, Rep. Mark Meadows asked Inspector General Ochoa about the error :

MEADOWS: I thank the gentleman from California. Ms. Ochoa, let me come to you. After your report was released, I think Seth Tillman, a lecturer for the Maynooth University Department of Law wrote you detailing a factual error in your constitutional analysis of the Emoluments Clause. Are you–are you aware that?

OCHOA: (OFF-MIC)

MEADOWS: –Can you hit your–

OCHOA: –asking that we adopt his particular argument.

MEADOWS: But–but pointing out that he felt like you had a factual error.

OCHOA: He expressed a different view.

MEADOWS: Well, did he say you were correct?

OCHOA: He–he expressed a different view–

MEADOWS: –It’s an easy–well, you got counsel behind you if you want to turn around and ask them. I mean, did he agree with your analysis?

OCHOA: No, he did not.

MEADOWS: Okay. So I would ask unanimous consent that we enter into the record the statement from Professor Josh Blackman and lecturer Seth Tillman detailing the exchange with Miss Ochoa’s office.

TITUS: Without objection.

MEADOWS: Thank you. I yield back.

We did not express a “different view.” The Inspector General is simply mistaken. And she is not the first public official who made an error about the Washington transaction. She follows in the footsteps of Judge Peter J. Messitte of the U.S. District Court for the District of Maryland. Relying on the Plaintiffs’ erroneous briefs, Judge Messitte conflated Washington’s 1793 transactions with a proposed transaction in 1794. We hope that both the Inspector General, and Judge Messitte, eventually acknowledge their errors.

from Latest – Reason.com https://ift.tt/2LWbjIZ

via IFTTT

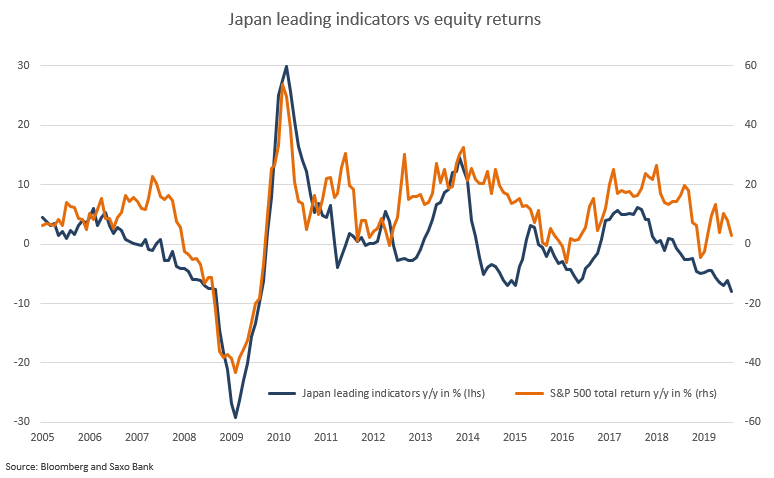

Summary: Japan’s leading indicators in August fell to the worst momentum levels since the 2008 financial crisis highlighting that the global economy is likely headed into a recession. However, global equities remain at high levels with low realised volatility levels reflecting a strong belief of recent weakness only being temporary. It’s a dangerous game for equity investors to be playing but maybe the negative yielding bonds are creating perverse behaviour nobody could think of just 10 years ago. Today’s equity update also discuss HSBC’s decision to cut 10,000 jobs and the prospects for the banking industry.

* * *

Overnight Japan released its leading indicators for August, and they are down 8% compared to last year showing the worst momentum since the 2008 financial crisis. Japan’s leading indicators are telling investors that the third largest economy in the world is most likely entering a recession soon following Sweden and Germany. Global equities have remained bid all indicators suggesting the slowdown is worsening and that global profits will fall. As we have said before we believe there is a massive disconnect between macro reality and equities likely made worse by policy action forcing rates deep into negative territory.

Tomorrow, OECD releases their global leading indicators for August, and we expect another decline extending it to a 19-month straight decline and further evidence that the global economy is likely headed into a recession. There are some indications about a stabilization measured on the real-time GDP tracker on the Eurozone economy called the Eurocoin Growth Indicator, but the stabilization is fragile. Worse than expected earnings from the upcoming Q3 earnings season is all it takes for sentiment to crumble.

On Thursday the US-China trade talks resume in Washington and according to the media China has firmly narrowed the scope of a trade deal refusing to cave into Trump’s demand of a grand deal. Specifically, the Chinese government will not allow changes to China’s industrial policy or government subsidies be part of the trade negotiations. This could be interpreted as China perceiving to have a stronger hand going with Donald Trump facing an impeachment with a second whistleblower emerging and apparently a person much closer to the actual content of the phone call between the US and Ukraine presidents.

While both the US and Chinese macro numbers have deteriorated, they also both face political issues ranging from impeachment to demonstrations, but the scoreboard in financial markets is still declaring the US as the winner judging by our trade war basket (see chart). US equity markets are not bad enough for Trump to waver in the US-China trade talks. We still see a low probability of even a narrower trade deal.

HSBC is out today announcing that it’s cutting 10,000 jobs to reduce costs and improve profitability. The endless exercise for banks failing to deliver the same returns for shareholders as before the financial crisis. In the first half of 2019 the 12-month trailing return on equity (ROE) stood at 8.4% down from the average of 16% pre-financial crisis of 2008. While HSBC has recently increased its ROE the bank still faces issues structural issues in North America and Europe. In the first half of this year HSBC generated 80% of its pre-tax profit from the Asia region. As we discuss in today’s Market Call podcast negative rates and general banking regulation are weighing on banks making it a difficult industry to invest in. Our view is still underweight banks but if we observe a policy change in the coming year with more focus on fiscal policy and a path away from negative yields then banks are clearly an overweight sector driven by low valuations.

Since January 2017, litigants have alleged that President Trump is violating the Foreign and Domestic Emoluments Clauses. We have filed several amicus briefs in these cases. We contend that the phrase “emolument” used in the Constitution does not extend to business transactions for value. Rather, “emoluments” are thelawful compensation or profits that are derived from the discharge of the duties of an office.

Our briefs have discussed an important historical incident in the early years of our Republic. In 1793, President George Washington purchased four lots of land at a public auction in the new federal capital. (We wrote about the transactions here.) If an “emolument” includes anything of value, then President Washington received something of value from the Federal Government, beyond his regular salary—that is, he received the land. Therefore, he would have violated the Domestic Emoluments Clause. The better reading, we contend, is that “emolument” is limited to the lawful compensation or profits that arise from the discharge of the duties of an office. Under this position, Washington was not a lawbreaker.

However, a January 2019 report from the Office of Inspector General, General Services Administration, reached a different conclusion. The report asserted that Washington purchased private, rather than public property at the auctions. (See pp. 15-16.) Specifically, the report stated that the sales “did not provide [President Washington with] a benefit from the United States.” Therefore, Carol F. Ochoa, the Inspector General reasoned, these transactions did not implicate the Domestic Emoluments Clause. This conclusion is not correct.

Bob Arnebeck, a historian with particular expertise concerning President Washington and land transactions in the early federal capital, responded to the Inspector General’s Report. He explained that our first President purchased public, not private land. And, if there were any doubts about this record, the President’s owncorrespondences repeatedly referred to the land and the sale as “public.” We discussed the Inspector General’s error at some length on pages 5-10 of our amicus brief submitted to the U.S. Court of Appeals for the Fourth Circuit.

The Inspector General’s error was understandable. She was reviewing intricate financial and historical records from two centuries ago in an area where her office and staff may lack the requisite expertise. However, she remains unwilling to acknowledge this serious error. Tillman contacted the Inspector General’s Office multiple times, flagging the plain error in the report. Ultimately, Edward Martin, Counsel to the Inspector General wrote back:

I have reviewed the documents you sent me on April 30, 2019. The GSA OIG’s Evaluation of GSA’s Management and Administration of the Old Post Office Lease, dated January 16, 2019, is a final report and speaks for itself.

The report does not speak for itself. It is in error. And the Inspector General has taken no steps to correct a plain historical error.

On September 25, the House Committee on Transportation and Infrastructure, Subcommittee on Economic Development, Public Buildings, and Emergency Management, held a hearing on the IG’s report. We were asked to testify, but could not attend in person. Instead, we submitted a joint written statement that flagged the IG’s plain error. Our testimony was flagged at several points during the hearing.

In this exchange, Rep. Mark Meadows asked Inspector General Ochoa about the error :

MEADOWS: I thank the gentleman from California. Ms. Ochoa, let me come to you. After your report was released, I think Seth Tillman, a lecturer for the Maynooth University Department of Law wrote you detailing a factual error in your constitutional analysis of the Emoluments Clause. Are you–are you aware that?

OCHOA: (OFF-MIC)

MEADOWS: –Can you hit your–

OCHOA: –asking that we adopt his particular argument.

MEADOWS: But–but pointing out that he felt like you had a factual error.

OCHOA: He expressed a different view.

MEADOWS: Well, did he say you were correct?

OCHOA: He–he expressed a different view–

MEADOWS: –It’s an easy–well, you got counsel behind you if you want to turn around and ask them. I mean, did he agree with your analysis?

OCHOA: No, he did not.

MEADOWS: Okay. So I would ask unanimous consent that we enter into the record the statement from Professor Josh Blackman and lecturer Seth Tillman detailing the exchange with Miss Ochoa’s office.

TITUS: Without objection.

MEADOWS: Thank you. I yield back.

We did not express a “different view.” The Inspector General is simply mistaken. And she is not the first public official who made an error about the Washington transaction. She follows in the footsteps of Judge Peter J. Messitte of the U.S. District Court for the District of Maryland. Relying on the Plaintiffs’ erroneous briefs, Judge Messitte conflated Washington’s 1793 transactions with a proposed transaction in 1794. We hope that both the Inspector General, and Judge Messitte, eventually acknowledge their errors.

from Latest – Reason.com https://ift.tt/2LWbjIZ

via IFTTT

The Harlan Institute and The Constitutional Sources Project (ConSource) announce their Seventh Annual Virtual Supreme Court Competition. This competition offers teams of two high school students the opportunity to research cutting-edge constitutional law, write persuasive appellate briefs, argue against other students through video chats, and try to persuade a panel of esteemed attorneys during oral argument that their side is correct. This year the competition focuses on Espinoza v. Montana Department of Revenue.

This competition has two stages, which mirror the process by which attorneys litigate cases.

Stage One: The Briefing and Oral Arguments

A team of two students will be responsible for writing an appellate brief arguing for either the petitioner or the respondent, as well as completing an oral argument video. The brief and video will be due by February 21, 2020.You can see the winning briefs from 2013, 2014, 2015, 2016, 2017, 2018, and 2020.

Stage Two: The Tournament

The Harlan Institute and ConSource will select the top teams supporting the Petitioner and Respondent, and seed them for the oral argument semifinals on April 4, 2020. All teams will compete in a virtual oral argument session over Google+ Hangout judged by the Harlan Institute and ConSource. Only teams that submit briefs that fully comply with all of the rules will be considered for oral argument. You can see the video from the 2013, 2014, 2015, 2016, 20172018, and 2019 competitions.

The final round of the Virtual Supreme Court Competition will be held in Washington, D.C. The Harlan Institute and ConSource will sponsor the top two teams, and their teachers, for a trip to Washington, D.C. in April 2019 to debate in front of a panel of expert judges, including lawyers, university level debate champions, and legal scholars.

The OT 2017 CompetitionThe OT 2018 CompetitionThe OT 2019 Competition

The Prizes

Grand Prize—The Solicitors General of FantasySCOTUS

The members of grand-prize winning team, the Solicitors General of FantasySCOTUS, and their teacher, will receive a free trip, including airfare and one night of hotel accommodations, to New York to attend the ConSource Constitution Day celebration in September 2020. This offer is open to U.S. residents only.

Second Prize

Members of the runner-up team will each receive an iPad Mini.

Third Prize

Members of the third and fourth place teams will each receive a $100 Amazon.com Giftcard.

{kind=link}