The First World War wasn’t just itself a great horror. In Wasteland, W. Scott Poole makes a compelling case that it launched a great age of horror fiction.

After the armistice of November 1918, a wave of vivid memoirs, plays, novels, and poems tried to grapple with the civilization-shaking event that everyone had just experienced. These gradually gave way to more sanitized recollections, as each nation tried to move on from the conflict. Yet that wartime experience didn’t disappear from the culture, Poole argues. It went underground, feeding a resurgent horror genre, especially in the new medium of film. Movies transmuted the effects of poison gas, flamethrowers, machine guns, and massive artillery barrages into creatures that reminded audiences of their all-too-real confrontations with death and dismemberment. While most of Europe and America tried to turn away from an industrial war’s killing fields, the horror genre stared deeply into those abysmal years and brought forth fascinating monstrosities.

Poole, a historian at the College of Charleston, begins with the 1922 German vampire film Nosferatu, the opening titles of which call it an “account of the great death.” The card is dated to the early 19th century and a nonmilitary story follows, but as Poole notes, the phrase surely conjures thoughts of the great death that the picture’s German audiences had just been through (nearly 2 million soldiers killed, plus approximately one quarter of that in civilian dead). The titular vampire, glimpsed in a soil-filled coffin underground, “evoked all the corpses of the age, scattered across battlefields.” The scale of the vampire’s ravages becomes “a flood of death…just as the Great War had brought to all of Europe.” Many of the movie’s creators fought in the war, including director F.W. Murnau and producer Albin Grau; Grau described the conflict as “a cosmic vampire, drinking the blood of millions.”

Another director, Paul Wegener, was a decorated veteran of the Eastern Front. In Poole’s telling, Wegener’s The Golem (1920) is saturated in the war’s terror, with its monster created of mud (think of trenches) and acting as a remorseless, inhuman killing machine (think of mechanized warfare). That kind of mechanical monster, a frightening reflection of dehumanized humanity, also appears in The Cabinet of Dr. Caligari (1920). Poole sees Caligari‘s hypnotized killer as a metaphor for the well-drilled soldier—a suggestion of the ease with which the authorities could turn ordinary Europeans into mass murderers.

Poole’s thesis is more overt in Abel Gance’s J’accuse. At the climax of this 1919 war drama, a legion of dead soldiers rise from their graves to march on a nearby village, anticipating many zombie stories to come. They return to their coffins, Poole notes, only after the villagers acknowledge that they didn’t pay enough attention to the soldiers’ suffering while they were alive.

An even better example may be Edgar G. Ulmer’s strange and underappreciated The Black Cat (1934), in which two veterans duel through means both physical and semi-supernatural in a modernist home built on the site of a Great War massacre, the basement of which is filled with preserved corpses. One of the leads, Bela Lugosi, was really a veteran, and his war stories unnerved the other actors and the crew.

Other films took the image of horrific corpses in different directions: dummies, puppets, mummies, waxworks—figures inhabiting the uncanny valley between human beings and fantastic shapes. At times these forms echoed not just the dead but the mutilated living.

The First World War saw breakthroughs in medical technology, allowing some soldiers who would have died in previous conflicts to live—but in altered form. Disfigured veterans, such as those with facial injuries (gueules cassées, or “broken faces”) mitigated by innovative prosthetics, were mirrored in such movies as The Phantom of the Opera (1925), The Man Who Laughs (1928), and Freaks (1932). For Poole, these modern monsters were creatures of the war, even when they had pre-1914 origins: “The double, the doll, the wax figure, the puppet all mimicked the Great War dead. They evoked the mechanical automata of the war of steel against flesh that had so completely reminded Europeans of their mortality.”

Poole also lets us see anew the horrific images of machines devouring people in Metropolis (1927), linking them to the war as well as one of the war’s spinoffs, the Soviet revolution. The film’s mobilization of people into inhuman masses reminds us not just of industrial labor but of industrial war. The director, Fritz Lang, was yet another World War I veteran.

Poole doesn’t limit his coverage to film. He discusses literary figures, from Franz Kafka to T.S. Eliot, whose The Waste Land (1922) finds a clear real-world source in the Western Front. Painters turned to horror too—notably veterans Otto Dix and Max Ernst. In Poole’s account, the shocking visions of dada and surrealism flow from the Great War’s deep terror and trauma: “Horror offered the surrealists the grammar for the new language they sought to create.”

The American role in this story is somewhat different, as the U.S. entered the war late and suffered only a fraction of the European nations’ death tolls. But the experience did occur, and its cultural reckoning was buttressed by the transatlantic flow of European artists. James Whale fought in the Somme campaign of 1916, then won fame by staging and filming the play Journey’s End, a tense drama set entirely in a British dugout. In Hollywood, Whale directed part of the World War I epic Hell’s Angels (1930)—and then, in 1931, made Frankenstein.

In Whale’s hands, the latter story’s monster represents the terrifying war dead—not just one body but the brutally recombined fragments of many. His existence on the boundary between life and death, between the human and the inhuman, recalls Caligari‘s Cesare as well as the shell-shocked soldier. To Poole, he also recalls “the maimed and mutilated returning veteran,” another object of mingled dread and sympathy.

Outside the medium of film, Poole’s analysis of the Americans sheds new light on the fiction of H.P. Lovecraft. Many of Lovecraft’s short stories openly featured the war, such as “Dagon” (1919) and “The Temple” (1925), whose plots are driven by U-boat raids, or “Herbert West—Reanimator” (1922), whose mad scientist brings an assistant to Europe to recover corpses from the war. Lovecraft’s visions of vast ruins and immense massacres can be seen as refractions of the Western Front. One source for his imagined apocalypses was the real apocalypse the world had just experienced.

After making the case for postwar horror’s ties to World War I, Poole takes the genre forward into World War II. In so doing, the author takes issue with Siegfried Kracauer’s influential 1947 book From Caligari to Hitler, which sees Germany’s turn to fascism anticipated in imaginative film. Poole argues that Kracauer underestimates the power of the popular horror genre at recollecting the Great War. Poole does think the Nazis made canny use of horror not just in what they wreaked upon the world but in the rhetoric and movies they supported. Jews, Slavs, communists, backstabbing politicians, and homosexuals appeared as monsters to be feared and destroyed, a trope drawing on two decades of interwar monster fiction.

Horror films made later in the 20th century still carry echoes of 1914–1918, even when they’re clearly connected to contemporary wars, as with Night of the Living Dead (1968) and Vietnam or World War Z (2006) and Iraq. “In every horror movie we see, every horror story we read, every horror-based video game we play, the phantoms of the Great War skittle and scratch just beyond the door of our consciousness,” Poole writes.

Wasteland overshoots at times. The book struggles to summon M (1931) to the bar, but it cannot quite make the connection between the war and the film’s tale of a child murderer, the police, and the underworld. Some of Poole’s connections are a touch too abstract, as when he compares Victor Frankenstein’s lonely lab to “an industrial process” and thus to the First World War. (The links he draws between 1932’s Island of Lost Souls and the terrifying science of that era is more persuasive.) Identifying King Kong‘s creators as veterans is useful, but it is less accurate to argue that New York City has become a necropolis by the film’s end. At times the book’s focus on later works of art blurs subsequent conflicts with World War I.

Such issues aside, Poole has made an important contribution to cultural history. Wasteland reveals how horror stories can have even darker roots.

from Latest – Reason.com https://ift.tt/2OnWVfK

via IFTTT

We have heard much this year about how much the country needs a Green New Deal to reverse the negative effects of climate change, ensure economic security, revamp the nation’s transportation system, restore damaged ecosystems, secure a sustainable environment, and achieve justice and equality. Overlooked in all of the analyses of the Green New Deal is that Americans didn’t need the original New Deal.

The Green New Deal

On February 7, newly elected Rep. Alexandria Ocasio-Cortez (D-N.Y.) introduced in the U.S. House a resolution (H.Res.109) “recognizing the duty of the Federal Government to create a Green New Deal.” On the same day, the veteran Sen. Edward Markey (D-Mass.) introduced a companion resolution (S.Res.59) in the U.S. Senate. According to the U.S. Senate, “A simple resolution addresses matters entirely within the prerogative of one house,” is “also used to express the sentiments of a single house,” or may simply give “advice.” Simple resolutions require neither the approval of the other House of Congress nor the signature of the president, as they do not have the force of law.

Prior to the introduction of her Green New Deal resolution, Representative Ocasio-Cortez issued a “Green New Deal FAQ.” A similar FAQ sheet was sent to the media on the day the resolution was introduced. The Green New Deal “is a 10-year plan to create a greenhouse gas neutral society that creates unprecedented levels of prosperity and wealth for all while ensuring economic and environmental justice and security.” The Green New Deal achieves this “through a World War 2 scale mobilization that focuses the robust and creative economic engine of the United States on reversing climate change by fully rebuilding our crumbling infrastructure, restoring our natural ecosystems, dramatically expanding renewable power generation, overhauling our entire transportation system, upgrading all our buildings, jumpstarting US clean manufacturing, transforming US agriculture, and putting our nation’s people to work doing what they do best: making the impossible possible.” The Green New Deal also “calls for an upgrade to the basic economic securities enjoyed by all people in the US to ensure everybody benefits from the newly created wealth.” This “upgrade” builds on “FDR’s second bill of rights” by guaranteeing to every American:

A job with family-sustaining wages, family and medical leave, vacations, and retirement security

High-quality education, including higher education and trade schools

High-quality health care

Clean air and water and access to nature

Healthy food

Safe, affordable, adequate housing

An economic environment free of monopolies

Economic security to all who are unable or unwilling to work

And that is just the beginning: “The economic securities and programs for justice and equity laid out in this Green New Deal resolution are a bare minimum of what we need to do to successfully execute the Green New Deal.”

And how will the Green New Deal be paid for? It will be paid for “the same way we paid for the original New Deal, World War II, the bank bailouts, tax cuts for the rich, and decades of war — with public money appropriated by Congress.” But also, “the Federal Reserve can extend credit to power these projects and investments,” “new public banks can be created to extend credit,” and the government can “take an equity stake in Green New Deal projects so the public gets a return on its investment.” In the end, the Green New Deal is not an expenditure; it is “an investment in our economy that should grow our wealth as a nation.”

It’s not just the Democratic Party that is pushing the Green New Deal. Not at all surprising, the Green Party also supports a Green New Deal. Although the centerpiece of the Green New Deal “is a transition to 100% clean energy by 2030,” it also “includes an Economic Bill of Rights, which ensures all citizens the right to employment through a Full-Employment Program that will create 20 million jobs by implementing a nationally funded, but locally controlled direct-employment initiative.” Unemployment offices will be replaced “with local employment offices offering public sector jobs that are ‘stored’ in job banks in order to take up any slack in private sector employment.” The Green New Deal “will provide assistance to workers and local communities that now have workers employed in the fossil fuel industry and to the developing world as it responds to climate-change damage caused by the industrial world.” It will “end unemployment in America once and for all by guaranteeing a job at a living wage for every American willing and able to work.” Once implemented, the Green New Deal “will revive the economy, turn the tide on climate change and make wars for oil obsolete.”

And how will the Green Party’s Green New Deal be paid for? “We will need revenues between $700 billion to $1 trillion annually for the Green New Deal,” says the Green Party. Cutting the military budget by 50 percent and subsequently saving “several hundred billion dollars per year would go a very long way toward creating green jobs at home.” The revenue from a carbon tax “will provide funding for the Green New Deal as well as safety nets for low-income households vulnerable to higher prices on certain items due to rising carbon taxes.” A tax “on the assets of oil and gas companies” will “help deal with the effects of climate change and smooth the transition to a low-carbon economy.” Wealthy Americans “should pay increased taxes to help with the cost of transitioning to a green economy.” The top income tax rate and the estate tax should both be raised. And on top of all that, “the Green New Deal largely pays for itself in healthcare savings from the prevention of fossil fuel-related diseases, including asthma, heart attacks, strokes and cancer.”

The Green Party’s Green New Deal invokes Franklin Roosevelt’s New Deal several times: “building on the concept of FDR’s New Deal,” “establish a Renewable Energy Administration on the scale of FDR’s hugely successful Rural Electrification Administration,” “this would include a WPA-style public jobs program.” “So it’s like the New Deal that got us out of the Great Depression, but it’s a Green New Deal so it also solves the crisis of the climate,” says Jill Stein, Green Party presidential candidate in 2012 and 2016.

The cost of the Green New Deal has been conservatively estimated in the tens of trillions of dollars — and that is the case even if only the costs of guaranteed jobs, universal health care, affordable housing, and food security are considered. Indeed, according to Robert Murphy, senior economist with the Institute for Energy Research (IER), “The Green New Deal is simply a wish list of standard progressive social goals, rather than an actual blueprint for fighting the technical problem of (alleged) human-caused harmful climate change.” The underlying philosophy of the Green New Deal is that government intervention in the economy and society is absolutely essential to effect the change that is needed to right every wrong and fix every problem.

The original New Deal

Much as conservative politicians invoke the name of Ronald Reagan when they want to hoodwink grassroots conservatives into believing how “conservative” they are, so liberal and progressive supporters of the Green New Deal invoke the original New Deal. Just as the unregulated free market and unbridled capitalism caused the Great Depression and Roosevelt’s New Deal cured the Great Depression, so only the “massive investment” of government akin to the original New Deal can save the planet and eliminate economic injustice and inequality. The New Deal is viewed as the model for what government should do for the poor, needy, and vulnerable members of society in times of economic instability, crisis, and uncertainty.

As explained by journalist and New Deal historian Michael Hiltzik, “The New Deal instilled in Americans an unshakable faith that their government stands ready to succor them in times of need. Put another way, the New Deal established the concept of economic security as a collective responsibility.” The only reason the radical goals of the Green New Deal can even get a hearing is that most Americans — of any political persuasion — look favorably on the original New Deal. After all, not only did it (eventually) end the Great Depression, it gave us Social Security — the most popular government program in history, and which is defended by conservative Republicans to this day. Yet it was government intervention by Presidents Herbert Hoover and Roosevelt that exacerbated and prolonged the Depression. The New Deal made the Depression the Great Depression.

After heading the federal Food Administration during World War I, Hoover concluded, in the words of Jim Powell, author of FDR’s Folly: How Roosevelt and His New Deal Prolonged the Great Depression,“that the vast power of the U.S. government could do wonders during an emergency.” He thought that government could spend its way out of a depression. Hoover supported dramatically increased subsidies to business and agriculture and massive public-works projects. To pay for this spending, he backed both higher tariffs and higher taxes. In 1930, he signed into law the Smoot-Hawley tariff — the most protectionist legislation in U.S. history — that crippled international trade. In 1932, he signed into law the Revenue Act — the largest peacetime tax increase in history — which revived wartime excise taxes, imposed new taxes, restored eliminated taxes, reduced exemptions and credits, raised the corporate income tax, and doubled the estate tax and personal income tax.

The 1932 Democratic Party platform, as summarized by Lawrence Reed, president of the Foundation for Economic Education, in Great Myths of the Great Depression “called for a 25 percent reduction in federal spending, a balanced federal budget, a sound gold currency, the removal of government from areas that belonged more appropriately to private enterprise and an end to the extravagance of Hoover’s farm programs.” Throughout the 1932 election campaign, “Roosevelt blasted Hoover for spending and taxing too much, boosting the national debt, choking off trade, and putting millions on the dole.” He accused Hoover of “reckless and extravagant” spending, of thinking “that we ought to center control of everything in Washington as rapidly as possible,” and of presiding over “the greatest spending administration in peacetime in all of history.” Roosevelt’s running mate charged that Hoover was “leading the country down the path of socialism.”

During a speech on July 2 from the floor of the 1932 Democratic Convention in Chicago, Roosevelt said, “I pledge to myself a new deal for the American people.” The phrase was not original to Roosevelt, but he made it his own. Once elected, he did everything he accused Hoover of and more. His remedies, which were inspired by European socialist or fascist models, were, in the words of Rexford Tugwell, one of the architects of the New Deal, “extrapolated from programs that Hoover started.”

The New Deal greatly increased the power of the presidency. In his first inaugural address, Roosevelt asked for “broad Executive power to wage a war against the emergency, as great as the power that would be given to me if we were in fact invaded by a foreign foe.” He got it. He issued 3,728 executive orders, including one that ordered Americans to surrender their gold to the government or face a fine of $10,000 and ten years in prison. The New Deal’s National Recovery Administration (NRA) forced most manufacturing industries into cartels with codes that regulated prices. The New Deal’s Agriculture Adjustment Act (AAA) paid farmers to destroy crops and livestock. The New Deal’s National Labor Relations Act (NLRA) empowered labor unions to organize strikes, seize plants, and commit violence with impunity. The New Deal’s Works Progress Administration (WPA) gave rise to the term “government boondoggle.” No one who valued any degree of individual liberty, private property, free markets, and limited government would ever invoke the New Deal to give credence to any social or economic proposal.

Laissez faire

The alternative to a socialist or fascist economy — elements of which can still be found in our interventionist economy in the twenty-first century — is a laissez-faire economy; that is, an economy where exchange, commerce, business, and trade between individuals, groups, companies, and corporations are free from government intervention, whether such intervention takes the form of regulation, mandates, oversight, management, control, licensing, certification, privilege, tariffs, or subsidies. I want to explore three key issues in the context of a laissez- faire economy.

Trade. In a laissez-faire economy, trade is absolutely free. It is neither managed by the government nor distorted by protectionism. There are no government trade agreements or trade treaties with other countries. There are no government memberships in trade organizations or associations. There is no 3,700-page Harmonized Tariff Schedule of the United States. There is no government trade representative or Export-Import Bank. The government doesn’t calculate a meaningless trade deficit and, even worse, seek to remedy it by intervening in the economy. Managed trade is not free trade. It is a misnomer to call thousand-page trade agreements “free-trade agreements.” The World Trade Organization (WTO) is a globalist bureaucracy.

It is not the proper role of government to protect domestic industry from foreign competition. Protectionism is not just tariffs; it can also take the form of quotas, barriers, sanctions, or dumping rules. Calls for protectionism are actually calls for Soviet-style central planning. All forms and levels of protectionism require central planning. Government economists and bureaucrats must determine which industries to protect, against which countries to impose protectionist measures, which items should be subject to tariffs, how much the tariffs should be, and what the duration of the tariffs should be. Trade is fair when it is not subject to government interference, regulations, or restrictions.

Free trade is fair trade. Trade cannot be made more fair by making it less free. Protective tariffs and retaliatory tariffs are counterproductive. Raising tariffs will not make the country great again. Trade is not a zero-sum game in which one party gains at the expense of the other. Trade does not result in winners and losers. In every exchange, both parties give up something they value less for something they value more. Each party to a transaction anticipates a gain from the exchange or it wouldn’t engage in commerce with the other party. Tariffs are no different from taxes. Any way you look at it, a tariff is a tax. American importers suffer when they have to pay a tariff to the U.S. government, just as American exporters suffer when they have to pay a tariff to a foreign government.

Commerce. In a laissez-faire economy, commerce is unrestricted and free enterprise and the free market are truly free. There is no National Economic Council or Council of Economic Advisers. There is no Small Business Administration, Securities and Exchange Commission, Federal Communications Commission, Federal Trade Commission, Consumer Financial Protection Bureau, or Commerce Department. All businesses handle their own security. Private industry delivers the mail, provides utilities, and collects garbage. No place of business is forced to provide handicapped parking spaces or is prohibited from selling alcohol after a certain time of day or on Sunday. No industry is singled out for special protection or provision by the government.

The banking, education, housing, transportation, and health-care sectors of the economy provide services just like any other business. There are no government grants, subsidies, vouchers, loans, or loan guarantees to any individual, group, organization, profession, occupation, business, or industry. There is no Federal Reserve to manipulate interest rates and distort the money supply.

There is no AMTRAK or public transit, no government deposit insurance, no rent-control laws, and no government accreditation of educational institutions. There are no departments of Health and Human Services, Agriculture, Transportation, Education, or Housing and Urban Development.

The free market allows buyers (who want to acquire goods at the lowest price possible) and sellers (who want to sell their goods at the highest price possible) to come together in harmony. Market forces of supply and demand allocate goods and resources and determine prices. Unhampered competition keeps prices in check. There are no government regulations to stifle businesses or anti-trust laws to “protect” consumers. Government intervention is not necessary to ensure competition or prevent

monopolies. There are no price-control, price-gouging, predatory-pricing, price-discrimination, or usury laws. The just price is the market price.

Not only is it not the business of government to regulate how people engage in commerce, attempts to regulate markets by governments always have unintended consequences that are often worse than the problems that regulations were meant to cure. Government interference in the market cannot make the market fairer or more competitive; it can only distort or disrupt the market.

Employment. In a laissez-faire economy, employment is strictly a contract between employer and employee. The government doesn’t interfere in the employer/employee relationship in any way. There is no Bureau of Labor Statistics, Department of Labor, National Labor Relations Board, Americans with Disabilities Act, Family and Medical Leave Act, or Equal Employment Opportunity Commission.

There are no government job- training programs. There is no government unemployment-compensation program. Unemployment insurance is private, voluntary, and purchased on the free market just like any other form of insurance. There are no government occupational-licensing or certification requirements to prevent people from working. There are no minimum-wage or overtime-pay laws. Regular wages and overtime pay are set entirely by agreement between employers and employees, as are employee fringe benefits, since there are no other government-mandated employee benefits. Employers can hire anyone regardless of his citizenship or immigration status. Affirmative Action policies are not only voluntary, they can be based on anything, not just race. Union membership and participation in collective bargaining is voluntary, and employers are free to mandate or disallow either. Subject to any restrictions in an employment contract, striking workers can be summarily fired and replaced for the simple reason that any employee can be fired and replaced at any time and for any reason.

Discrimination in hiring, pay, or promotions on any basis and for any reason is perfectly lawful. No one deserves to have a particular job, even if he is fully qualified for it. No one has the right to a “living wage” or a particular rate of pay. No employee is entitled to pay equal to that of any other employee. Workplace dress codes, hairstyles, headwear, appearance, and religious accommodations related to these things are solely the prerogative of employers.

Americans don’t need a Green New Deal any more than they needed the original New Deal. Each of them is a grab bag of progressive social and economic goodies with horrific consequences for liberty and property. Americans need laissez faire. They need it now, just as they needed it in the 1930s.

via ZeroHedge News https://ift.tt/2JZAlpq Tyler Durden

Philippine President Rodrigo Duterte has posted a bounty for the literal head of a communist insurgent leader behind the killings of four police officers in central Philippines, according to SCMP.

Members of the New People’s Army (NPA) ambushed and shot the motorcycle officers while they were riding in Negros Oriental province on July 18, according to police.

“Still not satisfied with the blood of their prey, the terrorists also looted the dead of their firearms, valuables and personal belongings, and drove off with the victims’ motorcycle,” reads a statement by the Philippine police.

In response, Duterte on Thursday offered three million pesos ($59,000 US) to whoever could bring him the “head” of NPA’s leader – up from one million pesos earlier, for what he said was an Islamic State group-style killing.

“They were burned like (by) ISIS that’s why I got mad,” said Duterte in a speech.

Duterte – who said he only wants the “head” and not the body of the leader – said he intended to increase the bouty to 20 million pesos ($392,000 US)

The president said he only wants the “head” and not the body of the leader of the killers because a complete body would only be used by activists in a ceremony to generate sympathy. –SCMP

The attack was claimed by communist guerillas in the insurgency-hit province, according to the report, however they denied torturning the police officers as claimed earlier.

The communist insurgency has raged in the Philippines for more than 50 years in one of Asia’s longest-running rebellions.

Battle losses, surrenders and infighting, however, have reduced the number of armed insurgents to about 3,500 from more than 20,000 at the height of their rural-based rebellion, the military says.

Earlier this week, Duterte urged lawmakers to bring back the death penalty as part of his internationally-condemned crackdown on narcotics in which police have already killed thousands. –SCMP

While giving his State of the Nation address on Monday, Duterte – whose approval ratings are sky-high, urged action on his zero-tolerance stance on crime.

“I respectfully request congress to reinstate the death penalty for heinous crimes related to drugs as well as plunder,” he said – drawing condemnation from the likes of Amnesty International.

Amnesty International immediately warned over the proposal’s impact on a nation where police claim to have killed more than 5,300 drug suspects, but activists say the true toll is at least four times higher.

“Talk of bringing back the death penalty for drug-related crimes is abhorrent, and risks aggravating the current climate of impunity,” Amnesty section director in the Philippines Butch Olano said.

Though Duterte’s campaign is the subject of a recently launched review by the United Nations’ rights body and a preliminary inquiry from International Criminal Court (ICC) prosecutors, he was defiant in his address. –SCMP

“Duterte – extrajudicial killing – report to the ICC,” said Duterte. “If you can provide me with a good comfortable cell, heated during winter time… unlimited conjugal visits, we can understand each other.”

via ZeroHedge News https://ift.tt/2JVqwJ3 Tyler Durden

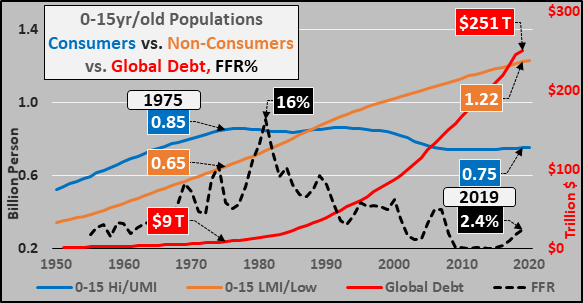

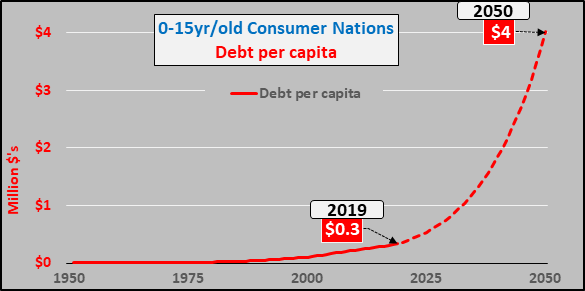

Global debt is currently at $246.5 trillion and primarily in the Wealthier, Consumer Nations of the world.

The population of young in Consumer Nations has fallen 12% or over 100 million Since Peaking in 1975.

Debt on a per capita basis gauged against the consumer nations young is going parabolic.

For nearly a half century wealthy nations young populations have been declining versus rising young among poor nations…offset by secularly declining interest rates and the addition of over $240 trillion in global debt to maintain unnaturally high rates of economic growth. The consumer nations population of relatively wealthy young has been declining for nearly 4 and a half decades, falling over 100 million or 12% during that span. The population of relatively poorer nations young has increased by nearly 190% or increased by 570 million. On average, each wealthier nations young person represents $26.5k in per capita consumption versus each poor nations young represents $1.5k in per capita consumption.

Said otherwise, it takes 15 more poor nations inhabitants to replace the loss of every one wealthier nations inhabitant to simply maintain flat consumption, thus the impetus for interest rate cuts and massive increases in debt among the wealthy. Obviously, consumption hasn’t been flat but has grown tremendously, primarily thanks to interest rate cuts, cheap debt, and only in a very small part from growth in consumption among the poorer nations population gains.

As I started in my last article, the world is characterized by stark inequalities among the global nations of “haves” and “have-nots”. The World Bank is kind enough to categorize the world’s nations into four buckets by the Atlas Gross National Income per capita (geographically detailed HERE and listed HERE). High income nations range from $84k to $12k per capita, Upper Middle income nations $12k-$4k per capita, Lower Middle income nations $4k to $1k, and Low income nations less than $1k per capita. To simplify what is taking place, I sweep the high and upper middle income nations 0-15yr/old populations together (blue line below), as these nations represent 90% of the global income, savings, and access to credit. They consume 90% of the global energy and purchase 90% of the global exports. They drive global economic activity. Likewise, I sweep the have-nots 0-15yr/old populations together (tan line, below). To view the full picture, I include global debt (red line) and the Federal Funds rate (black dashed line).

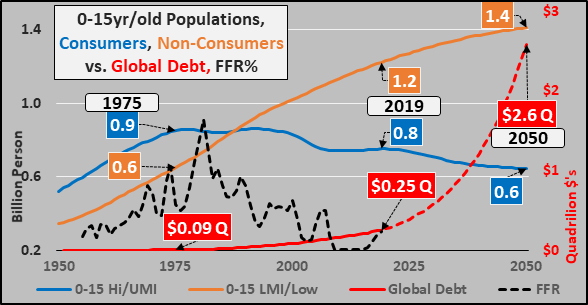

Looking at the same chart but running through 2050, with UN population projections and debt estimated to continue growing at the same pace it has since 1950 (these #’s are inclusive of the impact of immigration and emigration). Continued declines among the wealthy young consumers, growth among poor young non-consumers, and debt running from the current $250 trillion up to $2.6 quadrillion. NIRP (negative interest rate policy) will be necessary to enable this sort of wildly irresponsible debt load.

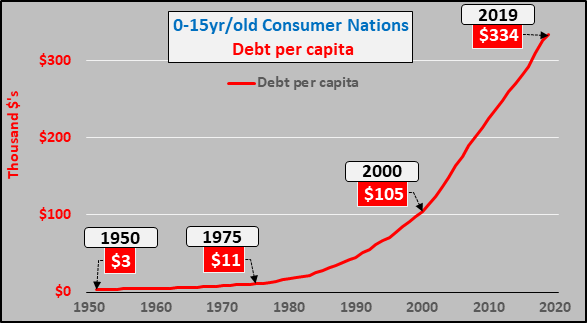

And looking at the debt on a per capita basis of young in the consumer nations, the chart below shows the impressive rise of debt against a long decline in consumer nations young. As of 2019, the per capita debt is over $334k per youngster. But that is nothing compared to what is coming…

The chart below takes the UN population projection and estimated global debt through 2050, and drum roll please, by 2050 every consumer nation under 15 year old will be responsible for over $4 million in per capita debt. That is the magic of surging debt and declining population…and that is entirely unworkable. There is no possible way to repay or even service this sort of debt load in any free-market based fashion.

And just to round things out, the chart below shows annual changes in the populations of wealthier versus poorer nations under 15 year olds. Also included is the rising debt, for some perspective on the role of debt in maintaining the growth of consumption.

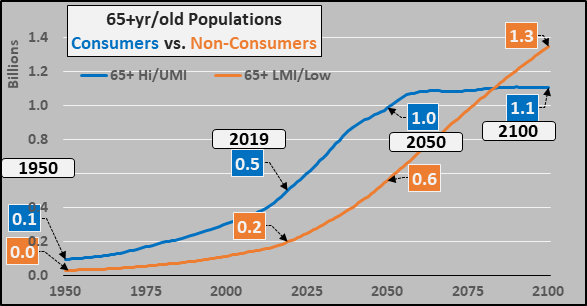

Ok, to really round out the picture, here is the flip side of the equation…the 65+ year old populations of the same groupings of nations.

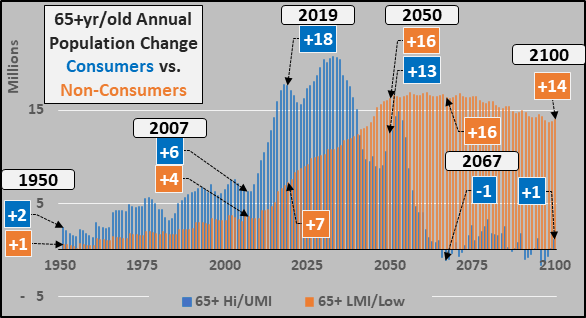

And annual changes in the populations…note the sharp acceleration in annual growth of consumer nations elderly since 2007 and the massive increases still to come. This isn’t even mentioning the unfunded pensions and liabilities due to these elderly.

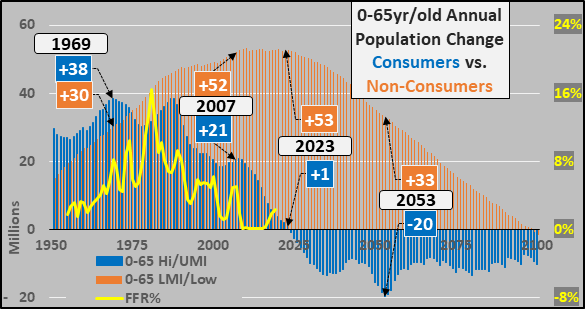

And putting the changing population growth in perspective, the same groupings below but showing only the 0-65 year old annual changes among the wealthier and poorer nations alongside the Federal Funds rate (yellow line). Note the deceleration of wealthier under 65 year old population growth from 2007 to now, and by 2023 turning to secular outright depopulation of consumer nations under 65 year olds throughout the remainder of the century.

Again, the growth in potential consumption among the far poorer populations in no way offsets the declining potential of consumption among the declining wealthier populations…without ZIRP (or more likely NIRP) and debt of gargantuan proportions.

via ZeroHedge News https://ift.tt/2SKZC9v Tyler Durden

Thanks to a ‘broken regulatory process,’ the Federal Aviation Administration has been passing off routine oversight tasks to manufacturers for years. In the case of the beleagured 737 Max, however, the plane was so advanced that the regulator “handed nearly complete control to Boeing,” which was able to sign off on its own safety certificates, according to the New York Times.

The lack of regulatory oversight meant that the FAA had no clue how Boeing’s automated anti-stall system, known as MCAS, worked. In fact, “regulators had never independently assessed the risks of the dangerous software” when they issued a 2017 approval for the plane.

The company performed its own assessments of the system, which were not stress-tested by the regulator. Turnover at the agency left two relatively inexperienced engineers overseeing Boeing’s early work on the system.

The F.A.A. eventually handed over responsibility for approval of MCAS to the manufacturer. After that, Boeing didn’t have to share the details of the system with the two agency engineers. They weren’t aware of its intricacies, according to two people with knowledge of the matter. –New York Times

During the late stages of the Max’s development, Boeing engineers decided to increase the plane’s reliance on MCAS to fly smoothly. Unfortunately, a new version of the system relied ona single sensor which could malfunction and push the plane into a nosedive.

Boeing never submitted a formal assessment of the MCAS system following its upgrade – which wasn’t required by FAA rules. An agency official claims that an engineering test pilot was familiar with the changes, however his job was to evaluate its effect on how the plane flew – not on its safety.

The jet was eventually certified as safe to fly, and the FAA required very little pilot traininguntil the second Max crashed less than five months after the first.

The plane remains grounded as regulators await a fix from Boeing. If the ban persists much longer, Boeing said this past week that it could be forced to halt production.

The F.A.A. and Boeing have defended the plane’s certification, saying they followed proper procedures and adhered to the highest standards. –New York Times

“The agency’s certification processes are well-established and have consistently produced safe aircraft designs,” said the FAA in a Friday statement undoubtedly written by lawyers. “The 737 Max certification program involved 110,000 hours of work on the part of F.A.A. personnel, including flying or supporting 297 test flights.”

Boeing, meanwhile, said that “the F.A.A.’s rigor and regulatory leadership has driven ever-increasing levels of safety over the decades,” adding that “the 737 Max met the F.A.A.’s stringent standards and requirements as it was certified through the F.A.A.’s processes.”

Chris Hart, former chairman of the National Transportation Safety Board is trying to get to the bottom of these regulatory shortcuts.

“Did MCAS get the attention it needed? That’s one of the things we’re looking at,” said Hart, who now leads a multiagency task force investigating the Max’s approval. “As it evolved from a less robust system to a more powerful system, were the certifiers aware of the changes?”

Rushed Orders

In an effort to compete with its rival Airbus, Boeing was “racing to finish” the 737, according to the report. And when it came to cutting through red tape to speed that process along, the FAA handing the regulatory reigns over to Boeing was crucial.

At crucial moments in the Max’s development, the agency operated in the background, mainly monitoring Boeing’s progress and checking paperwork. The nation’s largest aerospace manufacturer, Boeing was treated as a client, with F.A.A. officials making decisions based on the company’s deadlines and budget.

It has long been a cozy relationship. Top agency officials have shuffled between the government and the industry.

During the Max certification, senior leaders at the F.A.A. sometimes overruled their own staff members’ recommendations after Boeing pushed back. For safety reasons, many agency engineers wanted Boeing to redesign a pair of cables, part of a major system unrelated to MCAS. The company resisted, and F.A.A. managers took Boeing’s side, according to internal agency documents. –New York Times

The FAA, meanwhile, was ‘surprised’ to learn after last October’s Lion Air crash that they didn’t have a complete analysis of the MCAS system – including the fact that the system could “aggressively push down the nose of the plane and trigger repeatedly, making it difficult to regain control of the aircraft, as it did on the doomed Lion Air flight.”

And what did the agency do after the October incident? Instead of grounding the plane, they issued a notice reminding pilots of existing emergency procedures (which made no mention of how the MCAS system works – after an FAA manager told agency engineers to remove the only mention of the system).

French Finance Minister Bruno Le Maire has publicly admitted something normally reserved for backroom discussion in the circles of Europe’s governing elite at an event honoring the 75th anniversary of Bretton Woods (the conference which created the foundations for the post WWII world order).

At this event, Le Maire stated ever-so candidly that “the Bretton Woods order has reached its limits. Unless we are able to re-invent Bretton Woods, the New Silk Road might become the New World Order”.

He went onto state that “the pillars of that order have been the International Monetary Fund and its sister institution, the World Bank since their inception at the Bretton Woods conference in New Hampshire in 1944.”

Were a radical transformation not undertaken immediately, then Le Maire laments “Chinese standards on state and on access to public procurements, on intellectual property could become global standards”.

The finance minister’s statements reflect the growing awareness that two opposing systems operating on two conflicting sets of principles and standards are currently in conflict, where only one can succeed. Yet as much as he appears to be aware of the forces at play between two systems, Le Maire fails miserably to identify what the Bretton Woods System was meant to accomplish in the first place, or what type of “radical transformation” is needed to save Europe from the collapse of its own speculation-ridden system.

Le Maire dives so deeply out of reality that he actually believes that the radical transformation desperately needed in the west does not involve collaborating with the New Silk Road, but rather to strengthen the power of Brussels, while becoming more technocratic and more green (aka: de-industrialized, de-populated).

The Bretton Woods of 1944 and New Silk Road of Today

Seventy five years of revisionist historians largely funded by the British Roundtable/Chatham House and its American branch (The Council on Foreign Relations) have obstructed the true anti-imperial nature of the founding intention of Bretton Woods and the post war order centered on the United Nations.

Then, much as today, two opposing factions were vying to shape the essence of the world order as the Nazi machine (funded by Wall Street and London’s Bank of International Settlements) was drawing to a close. I am not talking about Capitalism vs. Communism.

This faction fight was between New Deal nationalists led by Franklin Roosevelt vs those racist imperialists represented by Sir Winston Churchill who wished to use the crisis of the war to establish a revived British Empire strengthened by American muscle. FDR’s New Dealers were characterized by their total adherence to the belief that the plague of colonialism had to be undone and a new age of long term development of great infrastructure projects had to characterize the community of sovereign nations for the coming century. These patriots believed in the internationalization of the New Deal, were committed to working with Russia and China as natural allies of America and profoundly distrusted the British.

In the case of Bretton Woods, where representatives from 44 nations convened for two weeks to create a new post war system in July 1944, this fight amounted to a battle between FDR’s trusted economic advisor Harry Dexter White (first director of the IMF and ally of FDR’s vice-president Henry Wallace) and Lord John Maynard Keynes (eugenicist, pedophile and defender of the British Empire).

Churchill and Keynes: Hard Racist/Soft Racist of the Empire

Where Churchill represented the unapologetic conservative proponent of the “White Man’s Burden” to exercise dominion over the “inferior” colored peoples of the earth, Keynes represented the soft cop of the Empire as a “Fabian Society Socialist” (aka: Social Engineer) from the London School of Economics. Where Churchill’s ilk preferred mowing down their enemies with Canons, body counts and torture as seen in the Boer War or opium wars or WWI, Keynes’ Fabian methods preferred attrition and slow subversion. Either way, the result of either pathway was the same.

While many know of the racist and pro-fascist views of Sir Churchill who spoke admiringly of Mussolini and even Hitler in the early days when it was still believed that these fascists and corporatists would act as marcher lords for the financial oligarchy, but most people are unaware that Keynes also supported Hitler and despised FDR.

Contradicting the mythos that FDR was a Keynesian, FDR’s assistant Francis Perkins recorded the 1934 interaction between the two men when Roosevelt told her:

“I saw your friend Keynes. He left a whole rigmarole of figures. He must be a mathematician rather than a political economist.”

In response Keynes, who was then trying to coopt the intellectual narrative of the New Deal stated he had “supposed the President was more literate, economically speaking.”

In his 1936 German edition of his General Theory of Employment, Interest and Money, Keynes wrote:

“For I confess that much of the following book is illustrated and expounded mainly with reference to the conditions existing in the Anglo Saxon countries. Nevertheless, the theory of output as a whole, which is what the following book purports to provide, is much more easily adapted to the conditions of a totalitarian state.”

Keynes Contaminates Bretton Woods

Lord Keynes was deployed to lead the British delegation to Bretton Woods and advance a Delphic plan that called for creating an International Clearing Union controlled by the City of London denominating all payments in a common accounting unit: the Bancor.

The Bancor would be used to measure all nations’ trade or surplus deficits- expropriating surpluses by the end of the year and taxing countries with deficits. The imposition of a “mathematical architecture” upon the physical (non-mathematical) systems of nations was the surest way to keep an invisible cage upon the earth under an ideal of “mathematical equilibrium.” The sadistic fiscal austerity demanded by mathematical economists and other technocrats in Brussels reflect the still active force of Keynes’ spirit haunting the world today.

The Bretton Woods as a Global New Deal

In opposition to Keynes, FDR’s America was represented by his close ally Harry Dexter White in Bretton Woods. White (today slandered as a Soviet agent by CFR historians) fought tooth and nail to ensure that Britain would not be in the driver’s seat of the new emerging economic system or the important mechanisms of the IMF that he would go onto lead, World Bank or monetary policy more generally. White ensured the colonial economic “preference” system Britain used to maintain free trade looting across its empire was destroyed, and the pound sterling did not play a primary role in global trade. Instead a fixed exchange rate system was set up to guarantee that speculation could not run rampant over national growth strategies and the dollar (then backed by a powerful PHYSICAL economic platform) was a backbone for world trade (1).

White, like Franklin Roosevelt, Henry Wallace, and Harry Hopkins believed that the US currency (rather than the pound sterling) had to become the foundation for the world economy as America exited WWII as the most powerful productive, growing nation of the world untouched by the ravages of Eurasian war.

Just as the Reconstruction Finance Corporation (RFC) was used like a national bank to fund thousands of great infrastructure, transport, energy, and water projects during the New Deal and just as Glass-Steagall broke the monopoly of private speculative finance over the productive economy, these New Dealers wished to use the World Bank and IMF to issue long term, low interest productive credit for long term mega infrastructure projects around the world. Not just in Europe’s reconstruction.

FDR’s battle with Churchill on this matter was well documented in his son/assistant Elliot Roosevelt’s book As He Saw It (1946):

“I’ve tried to make it clear … that while we’re [Britain’s] allies and in it to victory by their side, they must never get the idea that we’re in it just to help them hang on to their archaic, medieval empire ideas … I hope they realize they’re not senior partner; that we are not going to sit by and watch their system stultify the growth of every country in Asia and half the countries in Europe to boot.”

FDR continued:

“The colonial system means war. Exploit the resources of an India, a Burma, a Java; take all the wealth out of these countries, but never put anything back into them, things like education, decent standards of living, minimum health requirements–all you’re doing is storing up the kind of trouble that leads to war. All you’re doing is negating the value of any kind of organizational structure for peace before it begins.”

Writing from Washington in a hysteria to Churchill, Foreign Secretary Anthony Eden said that Roosevelt ”contemplates the dismantling of the British and Dutch empires.”

In 1942, FDR sent his close ally Wendell Wilkie on a world tour to meet with international leaders of colonial nations in order to spread the President’s vision for a global new deal. On his return Willkie gave a speech saying:

“In Africa, in the Middle East, throughout the Arab world, as well as in China, and the whole Far East, freedom means the orderly but scheduled abolition of the colonial system. I can assure you that this is true. I can assure you that the rule of people by other people is not freedom and not what we must fight to preserve… Men and women all over the world are on the march, physically, intellectually and spiritually. After centuries of ignorant and dull compliance, hundreds of millions of people in Eastern Europe and Asia have opened the books. Old fears no longer frighten them. They are no longer willing to be eastern slaves for western profits. They are beginning to know that men’s welfare throughout the world is interdependent. They are resolved, as we must be, that there is no more place for imperialism within their own society than in the society of nations.”

This vision was expressed continually by FDR in his hundreds of speeches, as well as by his Vice-President Henry Wallace, in the creation of the Atlantic Charter, and Four Freedoms. It was embedded in the defense of national sovereignty in the UN Constitution (conspicuously non-existent in the British-directed League of Nations earlier). It was meant to be the governing spirit animating the world as mankind entered a matured age of creative reason.

So What happened?

Describing the deep British penetration of the American state department, infested with Rhodes Scholars and Fabians, FDR described his understanding of the problem to his son:

“You know, any number of times the men in the State Department have tried to conceal messages to me, delay them, hold them up somehow, just because some of those career diplomats over there aren’t in accord with what they know I think. They should be working for Winston. As a matter of fact, a lot of the time, they are [working for Churchill]. Stop to think of ’em: any number of ’em are convinced that the way for America to conduct its foreign policy is to find out what the British are doing and then copy that!” I was told… six years ago, to clean out that State Department. It’s like the British Foreign Office….”

As long as FDR was in office, this British-run hive was kept at bay, but as soon as he died, the infestation took over America and immediately began undermining everything good FDR and his allies had created.

Harry Dexter White was ousted from his position as director of the IMF and labelled a communist agent. Henry Wallace was ousted for similar reasons and worked with White on a 1948 presidential bid as third party presidential candidate. William Wilkie (who had discussed creating a new party with FDR) died in October 1944, and FDR’s right hand man Harry Hopkins who did the most to initiate a close bond of friendship with Stalin, died in 1946. Elliot Roosevelt interviewed Stalin a few years later, and recorded that Stalin always believed that Elliot’s father was poisoned “by Churchill’s gang.” By 1946, Churchill ushered in the Cold War setting former allies at each other’s’ throats for the remaining 70 years while dropping nuclear bombs on a defeated Japan. Stalin bemoaned Roosevelt’s death saying “the great dream has died”.

It took the oligarchy another 25 years to dismantle the fixed exchange rate system of the Bretton Woods leading to Nixon’s 1971 floating of the US dollar onto the speculative markets, converting the world ever more into a militarized casino system. Rather than used as instruments for long term growth as they were intended, the IMF and World Bank were used as tools of debt slavery and re-colonialization as outlined in John Perkins’ Confessions of an Economic Hitman.

Today the world has captured a second chance to revive the “great dream”. In the 21st century, this great dream has taken the form of the New Silk Road, led by Russia and China (and joined by a growing chorus of nations yearning to exit the invisible cage of colonialism).

If western nations wish to survive the oncoming collapse, then they would do well to join this new framework rather than drink more of the poison promoted by the likes of Le Maire, Ursula von Leyen and their masters who want to transform the dying remains of Bretton Woods into a “Green New Deal”.

* * *

Appendix: Churchill, Keynes and FDR in their own words…

“Galton’s eccentric, sceptical, observing, flashing, cavalry-leader type of mind led him eventually to become the founder of the most important, significant and, I would add, genuine branch of sociology which exists, namely eugenics.”

-John Maynard Keynes on Galton’s Eugenics, Eugenics Review 1946

“I do not agree that the dog in a manger has the final right to the manger even though he may have lain there for a very long time. I do not admit that right. I do not admit for instance, that a great wrong has been done to the Red Indians of America or the black people of Australia. I do not admit that a wrong has been done to these people by the fact that a stronger race, a higher-grade race, a more worldly wise race to put it that way, has come in and taken their place.”

– Winston Churchill to the Peel Commission, 1937

“There never has been, there isn’t now, and there never will be, any race of people fit to serve as masters over their fellow men… We believe that any nationality, no matter how small, has the inherent right to its own nationhood.”

– Franklin Delano Roosevelt, March 1941

“They who seek to establish systems of government based on the regimentation of all human beings by a handful of individual rulers call this a new order. It is not new and it is not order.”

– Franklin Roosevelt

via ZeroHedge News https://ift.tt/2Y78IDv Tyler Durden

John Christensen was a government economist living on the beautiful island of Jersey, off England’s southern coast, in a “hillside villa with views of France.” But that lifestyle ended after he spoke out on a fraudulent currency trading scheme involving a UBS subsidiary in Jersey, according to Bloomberg.

Christensen had a head of dark hair when he helped to expose the Jersey currency scheme, which resulted in UBS’s Jersey unit and accounting firm Touche Ross & Co. — now Deloitte — paying almost $40 million to settle lawsuits. Regular bike rides keep Christensen as trim as two decades ago, but his hair has turned pearl white.

He said: “I was set. We had a pretty good lifestyle and plenty of friends.”

But he was forced to move to London as a result, where he now fights governments and campaigns against financial secrecy, including on his home island of Jersey.

He founded the Tax Justice Network in 2003 for the purposes of pushing greater regulation of tax havens. It’s estimated that $5 trillion to $32 trillion is currently stashed offshore for tax purposes – this is about a third of the entire global domestic product. Christensen thinks the number is at the “top end of that range”.

He said:

“We’ve won many of the intellectual and political arguments. And yet we’re not seeing it happen in practice. Look at where we are now. Rates of tax on capital have collapsed, inequality has gone through the roof and we’re now in a very dark place for democracy generally.”

But there’s some legitimate reasons to keep money offshore. Hedge funds and money managers often pool assets into Cayman Islands master funds to reduce costs. Offshore havens also sometimes offer protection against unstable political regimes. But their lack of transparency also makes them attractive to drug dealers, kleptocrats, and money launderers.

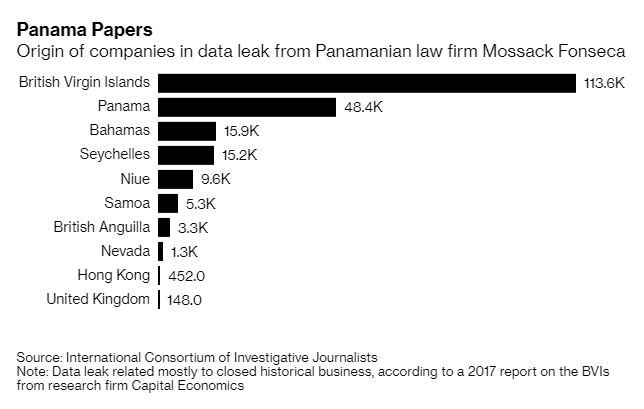

After the Panama Papers leaked, governments have been pressuring offshore tax havens to disclose more details. Regulators are starting to hone in on long-established locations, too. So now the tax adverse wealthy are seeking out mainland arrangements in places like Hong Kong, London and the U.S.

Christensen continued:

“Capital has moved literally lock, stock and barrel beyond the ability of nation-states to regulate tax. If you don’t have a good referee in a football game, neither team is any good and it becomes a free-for-all and everything deteriorates.”

Russia leads the way for offshore stashing, with 60% of the country’s GDP held offshore. This compares to 15% in Continental Europe and just a few percent in Scandinavian countries.

But Russians are leaving one of their favorite offshore spots: the British Virgin Islands.

Increased transparency in the BVIs, combined with tighter tax laws, means that Russians can no longer anonymously accumulate tax free funds there. Legislation adopted this year in the BVIs requires companies registered there to actually show economic activity like hiring employees and renting offices or they are faced with fines.

Christensen and the Tax Justice Network are campaigning for public registers of company owners, and they’ve had some success so far. The U.K.’s overseas territories and crown dependencies, like Jersey and the BVIs, are set to introduce legislation by the end of 2023. But this still isn’t quick enough for Christensen.

“It took the allied powers six months to plan and successfully carry out the D-Day landings. It took Thomas Edison two years to create the light bulb,” he said, arguing against the timeline.

His Tax Justice Network was started over tea and cake in Jersey in 2002. Christensen and two friends discussed their concerns over the grip of the financial industry on the economy of Jersey.

By writing reports, posing questions at conferences and working with nonprofit groups, the network eventually caught the attention of policymakers. Two ideas that Christensen and his colleagues championed from the start — country-by-country breakdowns of multinational firms’ finances and improved exchanges of tax data between nations — helped shape global tax reforms this decade by the Organization for Economic Cooperation and Development.

Labour Party lawmaker Margaret Hodge said of Christensen’s group: “Their campaigning work is grounded in good analysis and proper facts. Without them, I wouldn’t have achieved as much as I’ve been able to do in Parliament.”

Two years ago the Organization for Economic Cooperation and Development introduced its tax disclosure system with tropical locations like the Cayman Islands and BVIs adopting it early. Both places have avoided the EU’s blacklist of tax havens, which now includes 15 jurisdictions like Bermuda and the U.S. Virgin Islands, where Jeffrey Epstein has a private island.

Instead of signing on to OECD’s system, the U.S. is sticking with the Foreign Account Tax Compliance Act, or FATCA, which has created loopholes for people putting foreign money in the U.S.

Offshore specialists follow the cash. Geneva-based Cisa Trust Co. has applied for a license in South Dakota and Trident Trust, another offshore trust provider, has moved dozens of accounts from Switzerland and Grand Cayman to Sioux Falls, South Dakota.

Christensen said: “It’s kind of Wild West stuff in South Dakota and Wyoming. Anything goes. The law no longer really applies.”

But the influx into the U.S. doesn’t mean that traditional tax havens still don’t have plenty of foreign cash.

Last year, four Chinese tycoons transferred more than $17 billion into family trusts with the ownership structures all involving entities in the Caribbean. Chinese individuals will account for about one-third of the total inflows for offshore financial centers over the next five years, according to an analysis by Boston Consulting Group.

Even though it resulted in exile, Christensen doesn’t regret outing the UBS subsidiary.

“I knew that if I didn’t do that, I would regret it for the rest of my life. Everything I stood for would’ve been shunted to one side if I hadn’t,” he concluded.

via ZeroHedge News https://ift.tt/2Kax5pX Tyler Durden

Following up on our previous article discussing the unexpected collapse of US corporate operating profits in yesterday’s post-revision GDP data, JPMorgan makes an interesting observation.

First the good news. As we noted on Friday morning, US GDP grew more rapidly than expected last quarter as a strong 3.5% rise in domestic final sales offset a large drag from net trade and inventories. However, the slowing in stock building was less than expected and corporate efforts to lower its pace further likely will continue.

However, it was the annual revision to US national accounts that showed a significant change in two key items.

On one hand, there was a substantial upward revision in labor compensation. This, according to JPMorgan, is encouraging as it promotes a necessary normalization in labor’s income share and breathes life into the wage Phillips curve relationship.

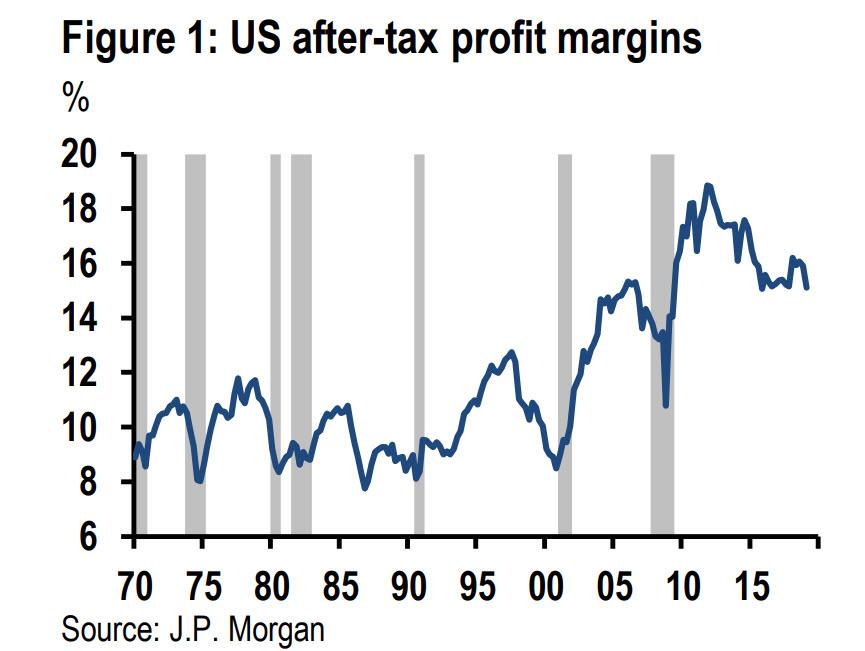

However, this was more than offset by negative revisions to US corporate profitability showing a sustained decline in US corporate profits, which have slumped to the lowest level in over 5 years even as the S&P has risen by 50% in the same period, indicating that all of the upside in the stock market was due to PE multiple expansion, something Goldman discussed earlier.

It gets worse: in light of solid revenue growth in recent years, and considering stagnant corporate profits, this implies that profit margins have been tumbling, and as shown in the chart below from JPMorgan, US after-tax profit margins have plunged to the lowest level since the financial crisis, despite – as JPM chief economist Bruce Kasman observes – the benefits from last year’s tax cuts.

This is notable for two reasons: non-GAAP profit margins are just off all time highs, yet profit margins as calculated by national accounts which is far more indicative of the underlying profit reality, are near the financial crisis lows, begging the question – just how fake is the non-GAAP world used by analysts and economists to justify the all time high in the S&P 500?

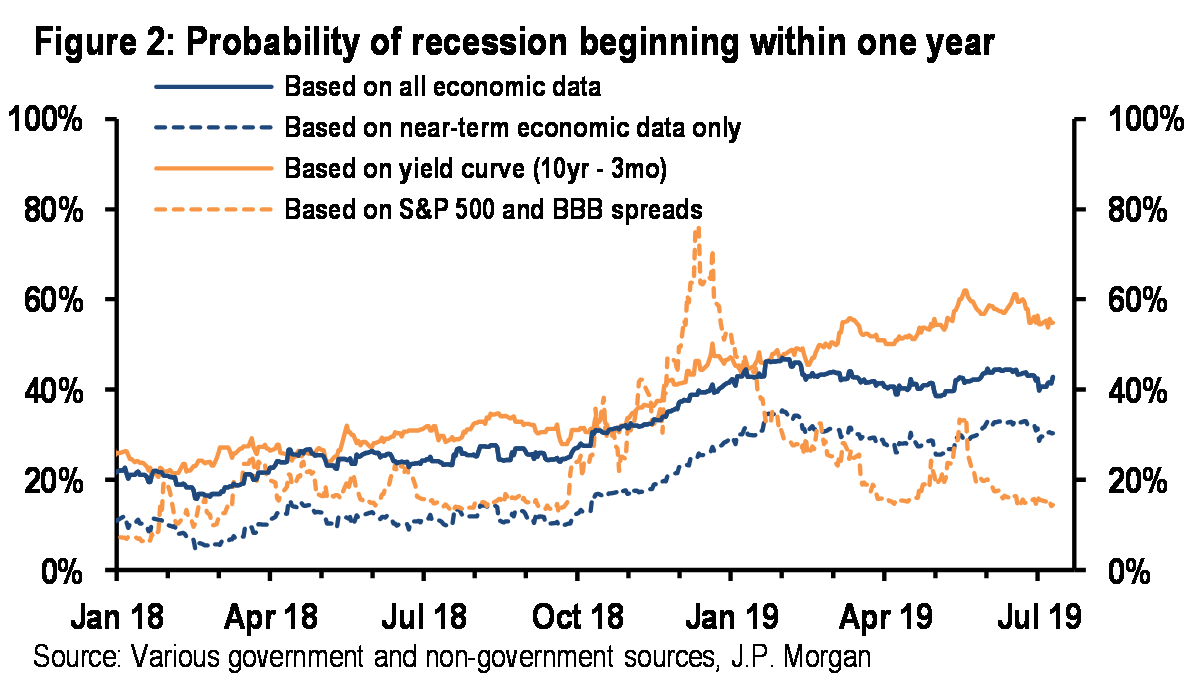

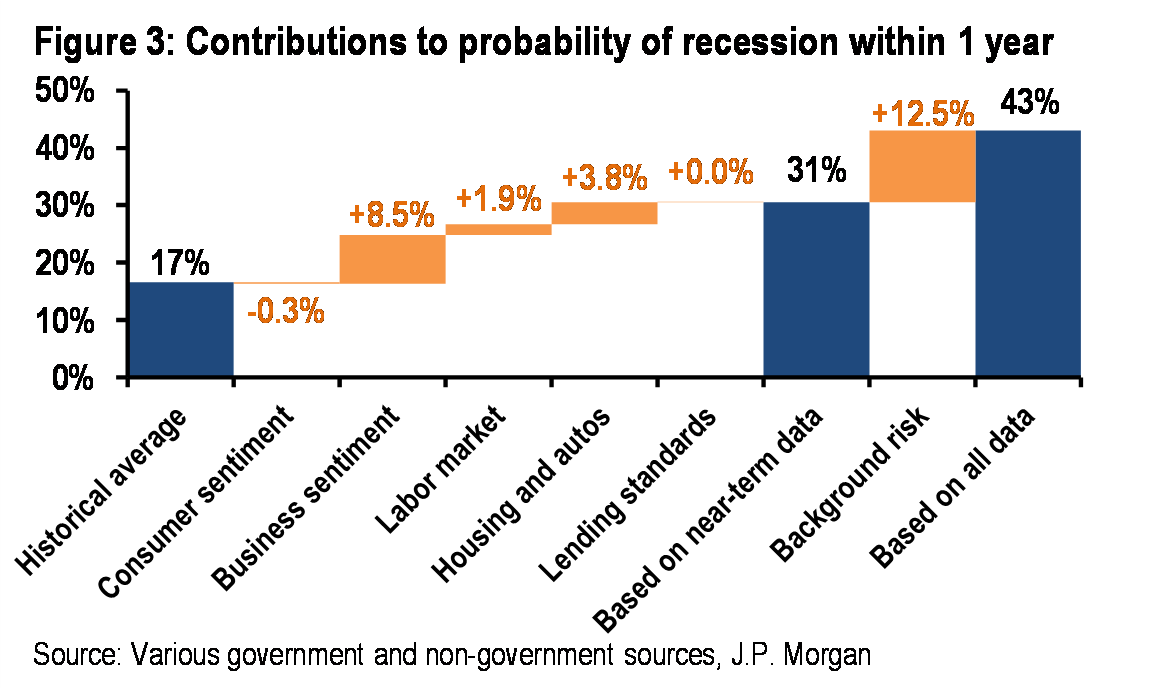

The second reason this is important is that while margins remain at high levels, such sustained compression has been a sign of vulnerability preceding recession, according to JPMMorgan, and as a result of this, JPM’s 12-month-ahead US recession probability model rose another 2pts this week, largely because of this news.

And speaking of a coming recession, considering the unexpected revised plunge in corporate profits which has clear adverse consequences for the entire economy, JPM’s model estimate of the risk of recession beginning within one year based on economic data has remained above 40% for much of 2019, as most survey measures of business confidence have stubbornly refused to rebound despite a string of positive policy news. This experience suggests that caution in the business sector could linger even after this week’s budget deal removes another source of tail risk.

The silver lining: this caution has thus far remained quite contained, suggesting additional shocks would be necessary to produce a broader downturn.

via ZeroHedge News https://ift.tt/2JZPmHP Tyler Durden

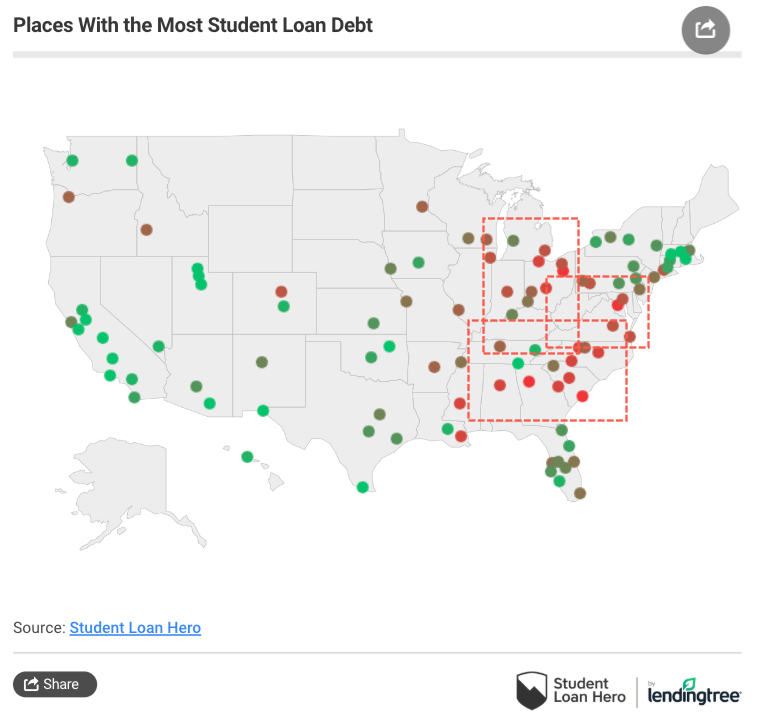

LendingTree has revealed a new study that identifies certain US metropolitan areas with the highest student loan balances.

The study’s release comes at a time when total student loan debt has reached $1.6 trillion, set to unravel in the next economic downturn. The study gives an eye-opener to the cities where millennials will suffer the most significant financial distress when the crisis unfolds.

About 70% of the cities and surrounding areas with the highest median loan balances are located in the South, including large balances in Georgia, Alabama, Louisiana, and the Carolinas. These areas are known for widespread deindustrialization, high opioid addiction, and weak economic activity.

LendingTree’s map shows high concentrations of student loan balances in the South, Rust Belt, and Mid-Alantic.

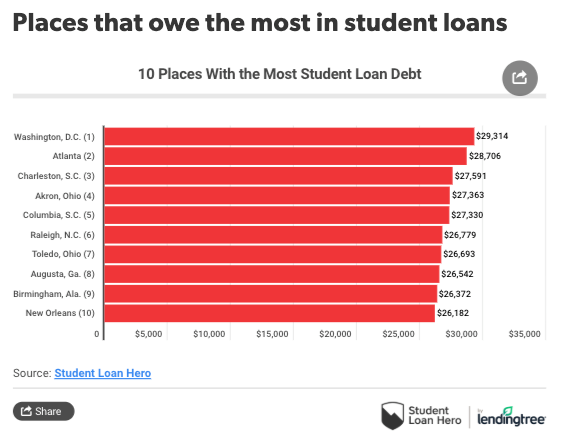

Borrowers in Washington, DC, carry the most student debt median balance of $29,314. And about 15% of those borrowers owe more than six figures, the highest percentage among the 100 metros surveyed.

Atlanta and Charleston, SC, have the second and third highest balances, averaging both around $28,000.

1. Washington, D.C. (Median balance: $29,314)

Roughly half of the people over the age of 25 in the Washington, D.C., metro have a postsecondary degree — that’s significantly higher than the 28% of all Americans who’ve earned a bachelor’s or higher.

Even more significant: Nearly 1 out of 4 have professional or graduate degrees, more than double the national rate of 10.5%. This helps explain why Washington also has the highest percentage of student debt holders who owe more than $100,000.

But that doesn’t necessarily mean these borrowers are in financial crisis, as most completed their degrees and are earning accordingly. While 22% of Americans left college before finishing, the same is true for only 16.5% of those residing in and around the nation’s capital.

2. Atlanta (Median balance: $28,706)

Atlanta is another highly educated city — 37% of Atlanta residents ages 25 and older have completed at least a four-year education, and nearly 14% have a graduate or professional degree, which is higher than the nation as a whole (10.5%).

However, that doesn’t completely explain why about 13% owe more than $100,000, well above the 8.7% average of the metros we reviewed. The area is home to a plethora of higher learning institutions, including the Georgia Institute of Technology, Georgia State University, Emory University, Morehouse College and Spelman College. Perhaps the need for so many professors helps to explain why Atlanta is more educated — and in more student debt — than the nation as a whole.

Unfortunately, 1 in 5 Atlanta residents left college before finishing a degree, which is in line with the rest of the country.

3. Charleston, S.C. (Median balance: $27,591)

The first of two South Carolina metros among our top five overall, Charleston placed third by a narrow margin. Still, the average borrower here has 4.6 loans, more than any of the 99 other metros we studied.

More students going to college also equals more student loans overall: About 34% of the metro area’s population has at least a bachelor’s degree, trumping the national average of 28%.

4. Akron, Ohio (Median balance: $27,363)

High balances brought Columbia into the top five of metros with the most education debt. About 45% of borrowers in the metro area had at least $50,000 in student debt — and more than 13% of were staring at a six-figure hole.

Interestingly, while the fellow Palmetto State cities of Columbia and Charleston ranked high on the list, Greenville, S.C., did much better, coming in at 39th overall for median education debt.

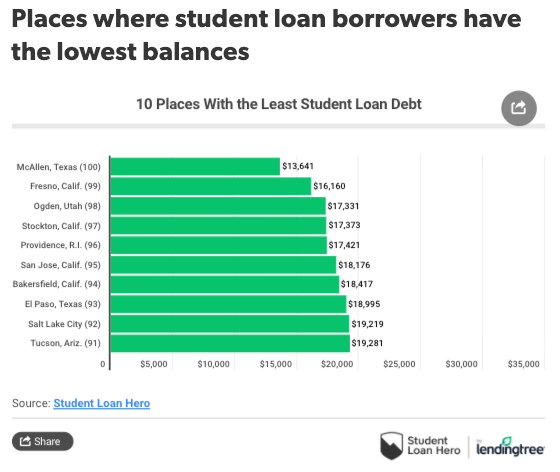

And metro areas with the lowest median balances were mostly west of the Mississippi River. College graduates in California, Texas, and Utah had some of the tiniest balances in the country.

Student debt is the fastest-growing consumer debt in the country, with $1.6 trillion outstanding, cracks are already starting to appear with 22% of borrowers defaulting.

The economic downturn which started in the summer of 2018, has already manifested into a broad industrial slowdown that is already starting to spread into other parts of the economy.

Millennials will be most impacted in the next recession, and thanks to LendingTree’s study, the exact metro areas of this financial stress are now known.

via ZeroHedge News https://ift.tt/2KalWFA Tyler Durden

A CIA-written Bill called the Intelligence Authorization Act (SB 3153) would criminalize whistleblowers and reporters.

Section 733 Sense of Congress on WikiLeaks:

“It is the sense of Congress that WikiLeaks and the senior leadership of WikiLeaks resemble a non-state hostile intelligence service often abetted by state actors and should be treated as such a service by the United States.”

The Bill is also known as the Damon Paul Nelson and Matthew Young Pollard Intelligence Authorization Act for Fiscal Years 2018, 2019, and 2020 (H.R. 3494).

“House Intelligence Committee Chairman Adam Schiff is once again putting the interests of the intelligence agencies in concealing their misdeeds ahead of protecting the rights of ordinary Americans by criminalizing routine reporting by the press on national security issues and undermining congressional oversight in his Intelligence Authorization bill,” Daniel Schuman, policy director, of Demand Progress said.

He added:

“Schiff’s expansion of the Intelligence Identities Protection Act beyond all reason will effectively muzzle reporting on torture, mass surveillance, and other crimes against the American people — all at the request of the CIA. Schiff is clearly the resistance to the resistance, and he should drop this provision from his bill.”

Ron Paul clarifies the real reason for this bill:

“The measure is designed – in the CIA’s own words – to prevent the kind of transparency that was provided by Wikileaks. It is a war on the free press!”

via ZeroHedge News https://ift.tt/2KbOiQ9 Tyler Durden