Anthony Scaramucci – White House Communications Director

Reince Priebus – White House Chief of Staff

Sean Spicer – White House Press Secretary

James Comey – FBI Director

“Every week is shark week in the Trump White House,” wrote The Hill contributing author Brad Bannon in August of 2018. A recent Brookings Institution study shows that the turnover in the Trump administration is significantly higher than during any of the previous five presidential administrations. The concern is that for a president without government experience, a rotating cast of top administration officials and advisors presents a unique challenge for the effective advancement of U.S. policies and global leadership. Bannon(no relation to former White House Chief Strategist Steve) adds, “Inexperience breeds incompetence.”

Although the sitting president has broken just about every rule of traditional politics, it is irresponsible and speculative to assume either ineffectiveness or failure by this one argument. One area of politics that falls within our realm of expertise is a “rule” that Donald Trump has not yet broken; firing the Chairman of the Federal Reserve.

Following the December Federal Open Market Committee (FOMC) meeting in which the Fed raised rates and the stock market fell appreciably, Bloomberg News reported that President Trump was again considering relieving the Fed Chairman of his responsibilities. This has been a continuing theme for Trump as his dissatisfaction with the Fed intensifies.

Not that Trump appears concerned about it, but firing a Fed Chairman is unprecedented in the 106-year history of the central bank. Having tethered all perception of success to the movements of the stock market, it is quite apparent why the president is unhappy with Jerome Powell’s leadership. Trump’s posture raises questions about whether he is more worried about his barometer of success (stock prices) or the long-term well-being of the economy. Acquiescing to either Trump or a genuine concern for the economic outlook, Chairman Powell relented in his stance on rate hikes and continuing balance sheet reduction.

Clamoring for Favor

Notwithstanding the abrupt reversal of policy stance at the Fed, President Trump continues to snipe at Powell and express dissatisfaction with what he considers to have been policy mistakes. Before backing out of consideration, Steven Moore’s nomination to the Fed board fits neatly with the points made above reflecting the President’s irritation with the Powell Fed. Moore was harshly critical of Powell and the Fed’s rate hikes despite a multitude of inconsistent remarks. Shortly after his nomination, Moore and the President’s Director at the National Economic Council, Larry Kudlow, stated that the Fed should immediately cut interest rates by 50 basis point (1/2 of 1%). Those comments came despite rhetoric from various fronts in the administration that the economy “has never been stronger.”

Now the Kudlow and Moore tactics are coming from within the Fed. St. Louis Fed President James Bullard dissented at the June 19th Federal Open Market Committee meeting in favor a rate cut. Then non-voting member and Minneapolis Fed President Neel Kashkari publicly stated that he was an advocate for a 50-basis point rate cut at the same meeting.

All this with unemployment at 3.6% and GDP tracking better than the 10-year average of 2.1%. Given Trump’s stated grievance with Powell, Bullard and Kashkari could easily be viewed as trying to curry favor with the administration. Even if that is not the case, to appear to be so politically inclined is very troubling for an institution and board members that must optically maintain an independent posture. It is unlikely that anyone has influence over Trump in his decision to replace or demote Powell. He will arrive at his conclusion and take action or not. If the first two years of his administration tells us anything, it is that public complaints about his appointed cabinet members precede their ultimate departure. Setting aside his legal authority to remove Powell, which would likely not stand in his way, the implications are what matter and they are serious.

For more on our thoughts on the ability of Trump to fire the Fed Chairman, please read our article Chairman Powell You’re Fired.

Prepare For This Tweet

Given Trump’s track record and his displeasure with Powell, we should prepare in advance for what could come as a surprise Tweet with little warning.

Ignoring legalities, if Trump were to demote or fire Powell, it is safe to assume he has someone in mind as a replacement. That person would certainly be more dovish and less prudent than Powell.

Under circumstances of a voluntary departure, a replacement with a more dovish disposition might be bullish for the stock market. However, the global economy is a complex system and there are many other factors to consider.

The first and largest problem is such a move would immediately erode the perception of Fed independence. Direct action taken to alter that independence would cast doubts on Fed credibility. Other sitting members of the Federal Reserve, appointed board members, and regional bank presidents, would likely take steps to defend the Fed’s independence and credibility which could create a functional disruption in the decision-making apparatus within the FOMC. Further, there might also be an active move by Congress to challenge the President’s decision to remove Powell. Although the language granting Trump the latitude to fire Powell is obtuse (he can be removed for “cause”), it is unclear that Presidential unhappiness affords him supportable justification. That would be an argument for the courts. Financial markets are not going to patiently await that decision.

With that in mind, what follows is an enumeration of possible implications for various key asset classes.

FX Markets

The most serious of market implications begin with the U.S. dollar (USD), the world’s reserve currency through which over 60% of all global trade transactions are invoiced. The firing of Powell and the likely appointment of a Trump-friendly Chairman would drop the value of the USD on the expectations of a dovish reversal of monetary policy. The question of Fed independence, along with the revival of an easy money policy, would likely cause the dollar to fall dramatically relative to other key currencies. An abrupt move in the dollar would be highly disruptive on a global scale, as other countries would take action to stem the relative strength of their currencies versus the dollar and prevent weaker economic growth effects. The term “currency war” has been overused in the media, but in this case, it is the proper term for what would likely transpire.

Additionally, the weaker dollar and new policy outlook would heighten concerns about inflation. With the economy at or near full employment and most regions of the country already exhibiting signs of wage pressures, inflation expectations could spike higher.

Fixed Income

The bond market would be directly impacted by Fed turbulence. A new policy outlook and inflation concerns would probably cause the U.S. Treasury yield curve to steepen with 2-year Treasuries rallying on FOMC policy change expectations and 10-year and 30-year Treasury bond yields rising in response to inflation concerns. It is impossible to guess the magnitude of such a move, but it would probably be sudden and dramatic.

Indecision and volatility in the Treasury markets are likely to be accompanied by widening spreads in other fixed income asset classes.

Commodities

In the commodities complex, gold and silver should be expected to rally sharply. While not as definitive, other commodities would probably also do well in response to easier Fed policy. A lack of confidence in the Fed and the President’s actions could easily result in economic weakness, which would lessen demand for many industrial commodities and offset the benefits of Fed policy changes.

Stock Market

The stock market response is best broken down into two phases. The initial reaction might be an extreme move higher, possibly a move of 8-10% or more in just a few days or possibly hours. However, the ensuing turmoil from around the globe and the potential for dysfunction within the Fed and Congress could cause doubt to quickly seep into the equity markets. Two things we know about equity markets is that they do not like changes in inflation expectations and they do not like uncertainty.

Economy

Another aspect regarding such an unprecedented action would be the economic effects of the firing of Jerome Powell. Economic conditions are a reflection of millions of households and businesses that make saving, investing, and consumption decisions on a day-to-day basis. Those decisions are dependent on having some certitude about the future.

If the disruptions were to play out as described, consumers and businesses would have reduced visibility into the future path for the economy. Questions about the global response, inflation, interest rates, stock, and commodity prices would dominate the landscape and hamstring decision-making. As a result, the volatility of everything would rise and probably in ways not observed since the financial crisis. Ultimately, we would expect economic growth to falter in that environment and for a recession to ensue.

Summary

Although economic growth has been sound and stocks are once again making record highs, the market and economic disruptions we have recently seen have been a long time coming. Market valuations across most asset classes have been engineered by excessive and imprudent monetary policy. The recent growth impulse is artificially high due to unprecedented expansion of government debt in a time of sound economic growth and low unemployment. In concert, excessive fiscal and monetary policy leave the markets and the economy vulnerable.

The evidence this year has been clear. Notwithstanding the Federal Reserve’s role in constructing this false reality, President Trump has not served the national interest well by his public criticism of the Fed. If Trump were to remove Powell as Fed chair, the prior sentence would be an understatement of epic proportions.

via ZeroHedge News https://ift.tt/2X5E90B Tyler Durden

In a wide-ranging interview on Fox Business this morning, President Trump told Maria Bartiromo, reflecting in the bias against conservative speakers, that “we should be suing Google and Facebook and perhaps we will,” sending social media stocks lower…

Additionally, Trump warned that substantial additional U.S. tariffs would be placed on goods from China if there’s no progress on a trade deal after his planned meeting with Chinese counterpart Xi Jinping at the G-20 Summit in Japan.

“My Plan B with China is to take in billions and billions of dollars a month and we’ll do less and less business with them,”

Additionally President Trump blasted Vietnam as “worst [economic] abuser of everyone” and called for ECB chief Mario Draghi as “our Fed person,” reiterating that he has the right to demote or fire Federal Reserve Chairman Jerome Powell.

via ZeroHedge News https://ift.tt/2xgaGSg Tyler Durden

The farce that is this “market” just took a whole new turn for the surreal.

As we reported earlier, the reason why stocks surged just after 5am EDT is because of a CNBC headline, according to which the US Treasury Secretary said that a US-China trade deal “is” – present tense – 90% complete.

This was quickly propagated by Bloomberg…

U.S. TREASURY SECRETARY STEVE MNUCHIN SAYS U.S.-CHINA TRADE DEAL IS 90% COMPLETE

… which triggered a flurry of algo buying.

Doubling down, CNBC also tweeted as much saying in a tweet that:

“Treasury Secretary Steven Mnuchin says a U.S.-China trade deal is “about 90% of the way there.” https://t.co/3Q0wvJKKxD pic.twitter.com/of6yH5y3rs”

The problem: CNBC made a huge grammatical mistake, because instead of saying “is”, Mnuchin was actually using the past tense, and what he really said – for those who listened to the video – is that “we were about 90% of the way’ on China trade deal.

CNBC also promptly deleted its tweet which said the deal “is” 90% completed, and the current on CNBC headline now says “Mnuchin: ‘We were about 90% of the way’ on China trade deal and there’s a ‘path to complete this.”

So basically Mnuchin said absolutely nothing new, and not only that, he did not provide any optimism that a deal was coming, but as we said earlier, was merely recapping what was already known.

But what is most absurd about this entire incident is that nobody who was buying futures – and global stocks – actually listened to the Mnuchin clip in which he clearly used the past tense, and a second just as absurd outcome is that after stocks surged at 5am on the patently wrong headline meant to boost optimism in a deal…

… they have yet to drop back to where they were before the Mnuchin fake CNBC news hit.

via ZeroHedge News https://ift.tt/2X7h2CJ Tyler Durden

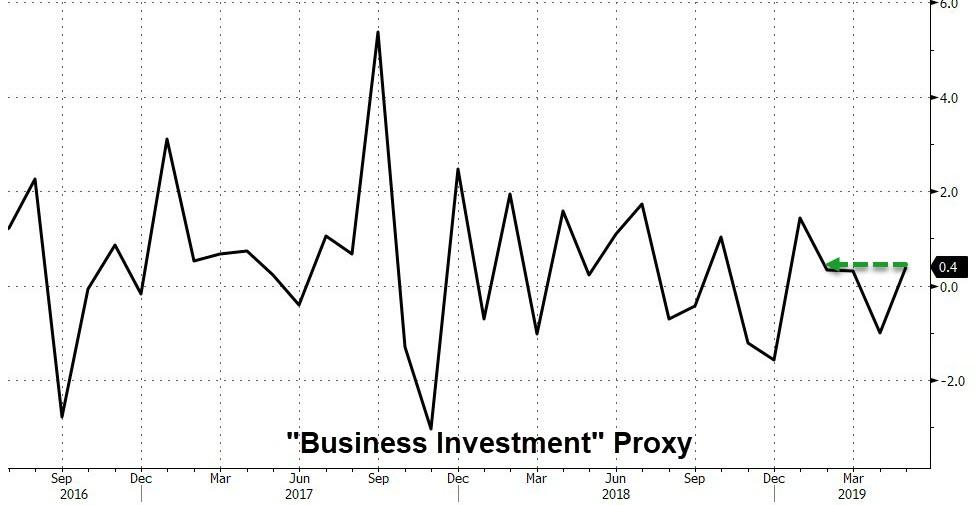

With manufacturing signals across the globe collapsing, expectations were for a modest drop in US Durable Goods Orders in May, however, the 1.3% MoM drop was far larger than expected and not helped by a notable downward revision in April.

Worst still, on a YoY basis, durable goods orders plunged 3.3% – the most since July 2016’s post-Brexit panic.

Under the hood there was some silver linings to cling to with Capital Goods Shipments (ex-Air) rising 0.7% MoM (well above the 0.1% expected rise).

And a proxy for business investment – non-military capital goods orders excluding aircraft – rose 0.4% after a 1% decline in the prior month.

As Bloomberg notes, the pickup in equipment orders may ease concerns that unpredictable trade policy is weighing on manufacturers and complicating business investment. Stronger demand would offer more of a tailwind to second-quarter economic growth after a downbeat April figure.

But in this brave new world, bad news is better than good to keep that 50bps bogey on the table.

via ZeroHedge News https://ift.tt/2XDzZwa Tyler Durden

Don’t talk to me about snowflakes. I have one daughter in college and one about to enter and we have had some very interesting and, let’s just say loud, discussions about free speech, triggers, snowflakes, and safe spaces. On one occasion, they became very upset that I took the position that the political shock-jock, Ann Coulter, who, by the way, is antithetical to my own political views and I find repulsive, should be able to speak on the UC Berkeley campus. In fact, I was ready to drive down to the campus and protest for her right to speak.

I tried to explain to my daughters if only popular ideas were protected, there would be no need for the First Amendment. If you do not defend the free speech rights of the unpopular, even if their views are repulsive to you, our liberty will never be secure. My experience is that many university students have trouble grasping this concept. It is not to say they don’t have the right to not invite someone to speak but to block a speaker, which one group has invited? Come on, man!

Ironically, when I mentioned to the youngest how much we paid in taxes during the bountiful years, she was outraged. Maybe today’s high schoolers are sensible fiscal conservatives?

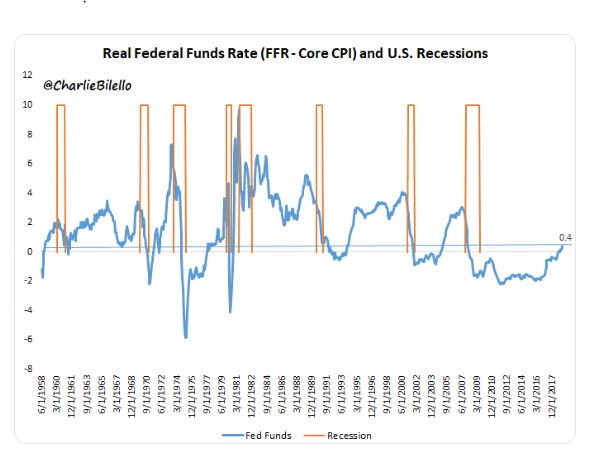

Lowest Terminal Real Fed Funds Rate Ever!

Moving on, Charlie B. throws together a nice chart and also notes,

The REAL Fed Funds Rate (Fed Funds minus inflation) stands at 0.4%, which, if the Fed is done hiking (market saying 100% probability of a cut next month), would be the lowest terminal rate of any expansion ever. Monetary policy remains extraordinarily easy. – Charlie Bilello

Now, do you still wonder why gold is having a Ralph Kamden moment? “One of these days. You’re going to the moon, Alice!”

Q: How robust is an economy or stock market that freaks out over a barely positive real Fed Funds rate, is triggered if the word “patient” is not removed from an FOMC statement, and considers a less than super-dovish Fed as a microaggression?

The market thought it had found its safe space with the dovish Fed and three rate cuts baked in. We seriously doubt it and are prepared for a macroagression.

Coming Up Next: The Trump Economy Scorecard

We have been very busy working on data to provide you with a full and comprehensive scorecard of the Trump economy as the presidential campaign gets underway and the B.S. starts to fly in earnest, on both sides. It should be out in the next few days so watch for it.

Here is a little appetizer.

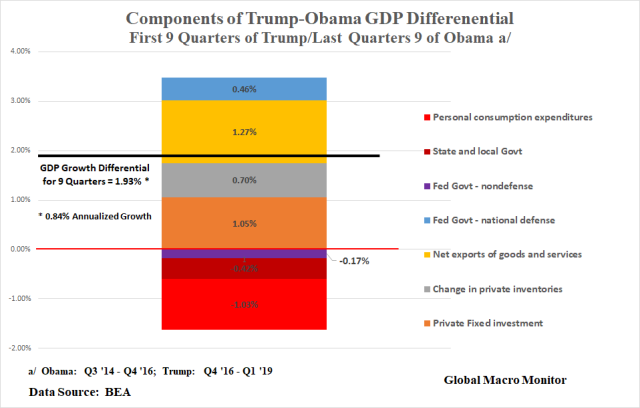

Because the current POTUS is always comparing his economy with that of his predecessors, we juxtapose several economic indicators during his first 2 1/2 years in office to the same timeframe as President Obama’s last few years in office. President Trump essentially inherited an economy on autopilot and goosed it with tax cuts and some deregulation.

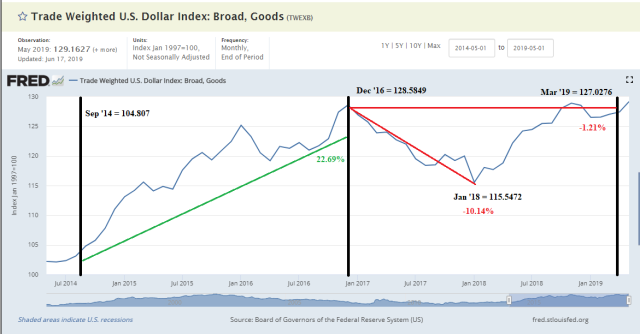

The chart below illustrates that economic growth in the first 9 quarters of President Trump economy was 1.9 percent (0.8 percent annualized) higher than the last 9 quarters under President Obama. Net exports were the main contribution to the differential, which makes sense as the trade-weighted value of the dollar increased by over 20 percent during the Obama timeframe and declined 1.2 percent under President Trump, which includes a 10 percent decline in his first year in office. By the way, not one peep from the Obama administration about the Fed as the strong dollar created a more than massive economic headwind during their last few years in office.

Private fixed investment, mainly in nonresidential structures and equipment, was the second largest contributor to the growth differential, though residential investment has significnatly lagged under Trump.

Personal consumption, federal nondefense and state and local govenrment consumption and investment were big drags (negative) on the Trump-Obama growth differential.

Though nominal wages have grown faster during the Trump economy, inflation has almost doubled, resulting in lower real wage growth than in Obama’s last several months in office, which is also consistent with lagging real growth of personal consumption expenditures. The Phillips Curve does liveth.

Much more to come. Stay tuned, folks.

via ZeroHedge News https://ift.tt/2NbEfz9 Tyler Durden

An advanced U.S. Navy combat ship that is slated to be commissioned as the U.S.S. Billings collided with a berthed freighter in Montreal on Monday, FreightWaves reported. Both ships were damaged as a result, but their crews were safe. The U.S. Freedom-class littoral combat ship hit the M/V Rosaire A. Desgagnes at about 2PM on Monday, according to Lt. Cmdr. Courtney Hillson, a Navy spokesperson.

The Billings is 378 feet long and sustained damage below the waterline as a result. The damage to the 452 foot dry bulk vessel it collided with has not been fully assessed yet. The bulk vessel is owned by Quebec-based Transport Desgagnés.

The U.S. Navy is reportedly still investigating the incident and despite the fact that the Billings was “capable” of making it to its Florida homebase, it is being kept in Montreal for additional damage assessments.

Hillson said: “The Navy is conducting an investigation to understand what happened and why. We will incorporate lessons learned to ensure we conduct safe and effective operations.”

The Billings launched in 2017 and is one of the newest ships in the Navy’s fleet. It cost $362 million and is billed as a “high-tech, cost-effective surface warfare vessel suited for modern defense needs”. Freedom class combat boats like the Billings have “been plagued by a host of issues, which have kept them from going operational.”

The Rosarie was delivered in 2007 and built by Volharding Shipyards in the Netherlands, in collaboration with Jiangzhou Shipyard in China. It has a capacity of about 16,000 cubic meters.

via ZeroHedge News https://ift.tt/2XtiT4j Tyler Durden

On the morning of April 6, 2018, the FBI arrested Michael Lacey and James Larkin and seized Backpage.com, the website they created in 2004, on allegations that it was a platform for underage sex trafficking. Lacey and Larkin were later charged with money laundering, conspiracy, and facilitating prostitution. The two men have maintained their innocence and are now confined to Maricopa County, Arizona, via ankle monitors. Their trial is scheduled for 2020.

Veteran newspaper publishers, Lacey and Larkin see their arrest and prosecution as an assault on the First Amendment. In the early 1970s, they built an alt-weekly empire specializing in muckraking journalism. In the process, they made enemies of powerful figures in Arizona politics, includingJohn McCain, his wife, Cindy, and former Sheriff Joe Arpaio.

After the internet and Craigslist gutted their business model, Lacey and Larkin launched Backpage.com, an online version of the classified sections of their print newspapers. Illegal activity was never allowed on Backpage, but sex workers advertised their services via innuendo. Connecting with clients online turned out to be considerably safer than walking the streets or working for a pimp. The internet empowered sex workers.

Lacey and Larkin were able to fend off legal challenges thanks to Section 230 of the Communications Decency Act (CDA), which said that website platforms aren’t responsible for third party content. As sex work became conflated with sex trafficking, that defense was eroded.

Lost in the panic was Lacey and Larkin’s behind-the-scenes collaboration with law enforcement in responding to subpoenas and even training vice officers on how to use the site to catch traffickers. Backpage’s Carl Ferrer even received a certificate from then-FBI Chief Robert Mueller for his outstanding cooperation helping with sex trafficking investigations.

This is the story of the rise and fall of a newspaper empire, and how a new moral crusade is endangering sex workers, shielding traffickers, empowering pimps, and undermining free speech online.

Written, shot, produced, edited, graphics, and narrated by Paul Detrick. Additional camera by Todd Krainin, Zach Weissmuller, Meredith Bragg, Alexis Garcia, Mark McDaniel, and Justin Monticello.

Video of Anti-Vietnam War Protesters and Richard Nixon at Sky Harbor Airport; Credit: Arizona State University Library

Video of Fiesta Bowl, 1971; Credit: Arizona State University Library

Photo of Cindy McCain; Credit: Jack Kurtz UPI Photo Service/Newscom

Photo of John McCain; Credit: BRIAN SNYDER/REUTERS/Newscom

Photo of John and Cindy McCain; Credit: BRIAN SNYDER/REUTERS/Newscom

Photo of Joe Arpaio; Credit: JOSHUA LOTT/REUTERS/Newscom

Photo of Village Voice; Credit: Glasshouse Images Glasshouse Images/Newscom

Photo of Craigslist; Credit: Scott Carson/ZUMAPRESS/Newscom

Photo of Craig Newmark; Credit: HYUNGWON KANG/REUTERS/Newscom

Photo of U.S. Capitol; Credit: CHUCK KENNEDY/KRT/Newscom

Photo of Classroom; Credit: J. Emilio Flores/LA Opinion/Newscom

Photo of Robert Mueller; Credit: Bill Clark/CQ Roll Call/Newscom

Photo of Robert Mueller; Credit: SIPA USA-KT/SIPA/Newscom

Photo of Ann Wagner; Credit: Bill Clark/CQ Roll Call/Newscom

Photo of Sheriff Thomas Dart; Credit: Michael Tercha/MCT/Newscom

Photo of Kamala Harris campaigning; Credit: Howard Lipin/ZUMA Press/Newscom

Photo of Kamala Harris walking; Credit: Bill Clark/CQ Roll Call/Newscom

Photo of Lacey and Larkin in courtroom; Credit: Hector Amezcua/TNS/Newscom

Photos of Kamala Harris on election night; Credit: ARMANDO ARORIZO/EFE/Newscom

Photo of Claire McCaskill; Credit: Joshua Roberts/REUTERS/Newscom

Photos of Ashton Kutcher before Congress; Credit: Bill Clark/CQ Roll Call/Newscom

Photo of computer with Backpage.com screen; Credit: Mirrorpix / MEGA / Newscom

Photo of Cindy McCain in 2018; Credit: Andreas Gebert/dpa/picture-alliance/Newscom

Photo of Sen. John McCain in 2018; Credit: Rok Rakun/ZUMA Press/Newscom

Photo of Sheriff Joe Arpaio in 2018; Credit: Tom Williams/CQ Roll Call/Newscom

Photo of Ann Wagner talking about sex trafficking; Credit: Alex Edelman—CNP/Newscom

Photo of U.S. Capitol; Credit: Aurora Samperio/ZUMA Press/Newscom

Photos of President Trump signing FOSTA; Credit: Chris Kleponis/UPI/Newscom

Photo of Craig Newmark; Credit: ROBERT GALBRAITH/REUTERS/Newscom

Photo of Backpage screen; Credit: ZUMA Press/Newscom

Photo of Department of Justice; Credit: Amr Alfiky/REUTERS/Newscom

Photo of Departmet of Justice; Credit: MARY F. CALVERT/REUTERS/Newscom

Photo of Department of Justice; Credit: LEAH MILLIS/REUTERS/Newscom

Photo of U.S. Capitol; Credit: Jim Bourg/REUTERS/Newscom

Photo inside U.S. Capitol; Credit: Cheriss May/ZUMA Press/Newscom

Photo of statue outside U.S. Capitol; Credit: Richard Maschmeyer/robertharding/robertharding/Newscom

Photos of Sacramento courtroom; Credit: Hector Amezcua/ZUMA Press/Newscom

Photo of Kamala Harris; Credit: Hector Amezcua/ZUMA Press/Newscom

Photo of President Bill Clinton; Credit: PETE SOUZA/KRT/Newscom

Photos of President George W. Bush; Credit: MARTIN H. SIMON/UPI/Newscom

Photo of Lusty Lady Theatre; Credit: ERIN SIEGAL/REUTERS/Newscom

Photos of Sheriff Joe Arpaio; Credit: JEFF GRACE/LA OPINION/Newscom

Photos of Craig Newmar;: Credit: MANTEL/SIPA/Newscom

Photo of Sheriff Joe Arpaio; Credit: JEFF TOPPING/REUTERS/Newscom

Photo of Demi Moore, Ashton Kutcher; Credit: SIPA USA/SIPA/Newscom

Photo of Sheriff Thomas J. Dart; Credit: Michael Tercha/MCT/Newscom

Photos of Ashton Kutcher and Demi Moore at Clinton Global Initiative; Credit: Sharkpixs/ZUMApress/Newscom

Photos of Village Voice; Credit: Richard B. Levine/Newscom

Photo of Kamala Harris in elevator; Credit: Jonathan Ernst/REUTERS/Newscom

Photos of Kamala Harris at podium; Credit: MARIO ANZUONI/REUTERS/Newscom

Photos of Kamala Harris at DNC; Credit: JASON REED/REUTERS/Newscom

Photo of John Cornyn; Credit: RON T. ENNIS/MCT/Newscom

Photo of Michael Rubio; Credit: Visions of America/Newscom

Photo of Attorney General Bill Schuette; Credit: Jessica Griffin/TNS/Newscom

Photo of Ann Wagner; Credit: Tom Williams/CQ Roll Call/Newscom

Photo of Lacey and Larkin; Credit: Giulio Sciorio

Photo of Lacey and Larkin; Credit: Stephen Lemons

Photo of Sen. John McCain; Credit: Nancy Kaszerman/ZUMA Press/Newscom

Photo of Sen. Kamala Harris; Credit: Jeff Malet Photography/Newscom

Photo of Sheriff Joe Arpaio; Credit: Jack Kurtz/ZUMA Press/Newscom

Photo of Rep Ann Wagner; Credit: Alex Endelman/SIPA/Newscom

Dramatic Swarm by Doug Maxwell is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=deb350454ec54ccb

Artist: Doug Maxwell

Falling Rain by Myuu is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=96243901d02a6971

Artist: Myuu

Loneliest Road in America (US 50) by Jesse Gallagher is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=d02070f8ae95fc0c

Artist: Jesse Gallagher

Armadillo by Silent Partner is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=cfa8d2f35697f58e

Artist: Silent Partner

Pitch by Lish Grooves is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=f94d362258166a8c

Artist: Lish Grooves

Pitch by Lish Grooves is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=f94d362258166a8c

Artist: Lish Grooves

Un Requited Love by Sir Cubworth is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=f94d362258166a8c

Artist: Sir Cubworth

Shibuya by Bad Snacks is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=bf4634fcab6e0d97

Artist: Bad Snacks

Fortress Europe by Dan Bodan is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=f8c8964f5a825b75

Artist: Dan Bodan

Bike Sharing to Paradise by Dan Bodan is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=99eeabfd699c7d07

Artist: Dan Bodan

Lunge Act by Freedom Trail Studio is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=43fbe7404b7b06ea

Artist: Freedom Trail Studio

A Revelation by Jeremy Blake is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=43730dcfc518a729

Artist: Jeremy Blake

Dreams Become Real by Kevin MacLeod is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://ift.tt/1rGWOLI

Artist: http://incompetech.com/

Timelapsed Tides by Asher Fulero is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=cf55568b30a3d007

Artist: Asher Fulero

A Stranger Thing by Bruno E. is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=42a0fc093d427400

Artist: Bruno E.

Under Cover by Wayne Jones is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=a32eccf37d37d5aa

Artist: Wayne Jones

Fresno Alley by Josh Lippi & The Overtimers is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=8cf72700de3ceb92

Artist: Josh Lippi & The Overtimers

Bellissimo by Doug Maxwell is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=01a754e39ba99c79

Artist: Doug Maxwell

Darkest Child A by Kevin MacLeod is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://ift.tt/WZCQww

Artist: http://incompetech.com/

Darkest Child by Kevin MacLeod is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://ift.tt/WZCQww

Artist: http://incompetech.com/

Dark Matter by Chasms is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=98ee262fd8f56a22

Artist: Chasms

Feather Waltz by Kevin MacLeod is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://ift.tt/2ggL6pu

Artist: http://incompetech.com/

Dreaming Blue by Sextile is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=fa83a7253598afe5

Artist: Sextile

Their Story, Them Seeing by Puddle of Infinity is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=3411c8740ed8b868

Artist: Puddle of Infinity

from Latest – Reason.com https://ift.tt/2X3YjD2

via IFTTT

On the morning of April 6, 2018, the FBI arrested Michael Lacey and James Larkin and seized Backpage.com, the website they created in 2004, on allegations that it was a platform for underage sex trafficking. Lacey and Larkin were later charged with money laundering, conspiracy, and facilitating prostitution. The two men have maintained their innocence and are now confined to Maricopa County, Arizona, via ankle monitors. Their trial is scheduled for 2020.

Veteran newspaper publishers, Lacey and Larkin see their arrest and prosecution as an assault on the First Amendment. In the early 1970s, they built an alt-weekly empire specializing in muckraking journalism. In the process, they made enemies of powerful figures in Arizona politics, includingJohn McCain, his wife, Cindy, and former Sheriff Joe Arpaio.

After the internet and Craigslist gutted their business model, Lacey and Larkin launched Backpage.com, an online version of the classified sections of their print newspapers. Illegal activity was never allowed on Backpage, but sex workers advertised their services via innuendo. Connecting with clients online turned out to be considerably safer than walking the streets or working for a pimp. The internet empowered sex workers.

Lacey and Larkin were able to fend off legal challenges thanks to Section 230 of the Communications Decency Act (CDA), which said that website platforms aren’t responsible for third party content. As sex work became conflated with sex trafficking, that defense was eroded.

Lost in the panic was Lacey and Larkin’s behind-the-scenes collaboration with law enforcement in responding to subpoenas and even training vice officers on how to use the site to catch traffickers. Backpage’s Carl Ferrer even received a certificate from then-FBI Chief Robert Mueller for his outstanding cooperation helping with sex trafficking investigations.

This is the story of the rise and fall of a newspaper empire, and how a new moral crusade is endangering sex workers, shielding traffickers, empowering pimps, and undermining free speech online.

Written, shot, produced, edited, graphics, and narrated by Paul Detrick. Additional camera by Todd Krainin, Zach Weissmuller, Meredith Bragg, Alexis Garcia, Mark McDaniel, and Justin Monticello.

Video of Anti-Vietnam War Protesters and Richard Nixon at Sky Harbor Airport; Credit: Arizona State University Library

Video of Fiesta Bowl, 1971; Credit: Arizona State University Library

Photo of Cindy McCain; Credit: Jack Kurtz UPI Photo Service/Newscom

Photo of John McCain; Credit: BRIAN SNYDER/REUTERS/Newscom

Photo of John and Cindy McCain; Credit: BRIAN SNYDER/REUTERS/Newscom

Photo of Joe Arpaio; Credit: JOSHUA LOTT/REUTERS/Newscom

Photo of Village Voice; Credit: Glasshouse Images Glasshouse Images/Newscom

Photo of Craigslist; Credit: Scott Carson/ZUMAPRESS/Newscom

Photo of Craig Newmark; Credit: HYUNGWON KANG/REUTERS/Newscom

Photo of U.S. Capitol; Credit: CHUCK KENNEDY/KRT/Newscom

Photo of Classroom; Credit: J. Emilio Flores/LA Opinion/Newscom

Photo of Robert Mueller; Credit: Bill Clark/CQ Roll Call/Newscom

Photo of Robert Mueller; Credit: SIPA USA-KT/SIPA/Newscom

Photo of Ann Wagner; Credit: Bill Clark/CQ Roll Call/Newscom

Photo of Sheriff Thomas Dart; Credit: Michael Tercha/MCT/Newscom

Photo of Kamala Harris campaigning; Credit: Howard Lipin/ZUMA Press/Newscom

Photo of Kamala Harris walking; Credit: Bill Clark/CQ Roll Call/Newscom

Photo of Lacey and Larkin in courtroom; Credit: Hector Amezcua/TNS/Newscom

Photos of Kamala Harris on election night; Credit: ARMANDO ARORIZO/EFE/Newscom

Photo of Claire McCaskill; Credit: Joshua Roberts/REUTERS/Newscom

Photos of Ashton Kutcher before Congress; Credit: Bill Clark/CQ Roll Call/Newscom

Photo of computer with Backpage.com screen; Credit: Mirrorpix / MEGA / Newscom

Photo of Cindy McCain in 2018; Credit: Andreas Gebert/dpa/picture-alliance/Newscom

Photo of Sen. John McCain in 2018; Credit: Rok Rakun/ZUMA Press/Newscom

Photo of Sheriff Joe Arpaio in 2018; Credit: Tom Williams/CQ Roll Call/Newscom

Photo of Ann Wagner talking about sex trafficking; Credit: Alex Edelman—CNP/Newscom

Photo of U.S. Capitol; Credit: Aurora Samperio/ZUMA Press/Newscom

Photos of President Trump signing FOSTA; Credit: Chris Kleponis/UPI/Newscom

Photo of Craig Newmark; Credit: ROBERT GALBRAITH/REUTERS/Newscom

Photo of Backpage screen; Credit: ZUMA Press/Newscom

Photo of Department of Justice; Credit: Amr Alfiky/REUTERS/Newscom

Photo of Departmet of Justice; Credit: MARY F. CALVERT/REUTERS/Newscom

Photo of Department of Justice; Credit: LEAH MILLIS/REUTERS/Newscom

Photo of U.S. Capitol; Credit: Jim Bourg/REUTERS/Newscom

Photo inside U.S. Capitol; Credit: Cheriss May/ZUMA Press/Newscom

Photo of statue outside U.S. Capitol; Credit: Richard Maschmeyer/robertharding/robertharding/Newscom

Photos of Sacramento courtroom; Credit: Hector Amezcua/ZUMA Press/Newscom

Photo of Kamala Harris; Credit: Hector Amezcua/ZUMA Press/Newscom

Photo of President Bill Clinton; Credit: PETE SOUZA/KRT/Newscom

Photos of President George W. Bush; Credit: MARTIN H. SIMON/UPI/Newscom

Photo of Lusty Lady Theatre; Credit: ERIN SIEGAL/REUTERS/Newscom

Photos of Sheriff Joe Arpaio; Credit: JEFF GRACE/LA OPINION/Newscom

Photos of Craig Newmar;: Credit: MANTEL/SIPA/Newscom

Photo of Sheriff Joe Arpaio; Credit: JEFF TOPPING/REUTERS/Newscom

Photo of Demi Moore, Ashton Kutcher; Credit: SIPA USA/SIPA/Newscom

Photo of Sheriff Thomas J. Dart; Credit: Michael Tercha/MCT/Newscom

Photos of Ashton Kutcher and Demi Moore at Clinton Global Initiative; Credit: Sharkpixs/ZUMApress/Newscom

Photos of Village Voice; Credit: Richard B. Levine/Newscom

Photo of Kamala Harris in elevator; Credit: Jonathan Ernst/REUTERS/Newscom

Photos of Kamala Harris at podium; Credit: MARIO ANZUONI/REUTERS/Newscom

Photos of Kamala Harris at DNC; Credit: JASON REED/REUTERS/Newscom

Photo of John Cornyn; Credit: RON T. ENNIS/MCT/Newscom

Photo of Michael Rubio; Credit: Visions of America/Newscom

Photo of Attorney General Bill Schuette; Credit: Jessica Griffin/TNS/Newscom

Photo of Ann Wagner; Credit: Tom Williams/CQ Roll Call/Newscom

Photo of Lacey and Larkin; Credit: Giulio Sciorio

Photo of Lacey and Larkin; Credit: Stephen Lemons

Photo of Sen. John McCain; Credit: Nancy Kaszerman/ZUMA Press/Newscom

Photo of Sen. Kamala Harris; Credit: Jeff Malet Photography/Newscom

Photo of Sheriff Joe Arpaio; Credit: Jack Kurtz/ZUMA Press/Newscom

Photo of Rep Ann Wagner; Credit: Alex Endelman/SIPA/Newscom

Dramatic Swarm by Doug Maxwell is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=deb350454ec54ccb

Artist: Doug Maxwell

Falling Rain by Myuu is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=96243901d02a6971

Artist: Myuu

Loneliest Road in America (US 50) by Jesse Gallagher is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=d02070f8ae95fc0c

Artist: Jesse Gallagher

Armadillo by Silent Partner is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=cfa8d2f35697f58e

Artist: Silent Partner

Pitch by Lish Grooves is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=f94d362258166a8c

Artist: Lish Grooves

Pitch by Lish Grooves is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=f94d362258166a8c

Artist: Lish Grooves

Un Requited Love by Sir Cubworth is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=f94d362258166a8c

Artist: Sir Cubworth

Shibuya by Bad Snacks is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=bf4634fcab6e0d97

Artist: Bad Snacks

Fortress Europe by Dan Bodan is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=f8c8964f5a825b75

Artist: Dan Bodan

Bike Sharing to Paradise by Dan Bodan is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=99eeabfd699c7d07

Artist: Dan Bodan

Lunge Act by Freedom Trail Studio is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=43fbe7404b7b06ea

Artist: Freedom Trail Studio

A Revelation by Jeremy Blake is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=43730dcfc518a729

Artist: Jeremy Blake

Dreams Become Real by Kevin MacLeod is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://ift.tt/1rGWOLI

Artist: http://incompetech.com/

Timelapsed Tides by Asher Fulero is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=cf55568b30a3d007

Artist: Asher Fulero

A Stranger Thing by Bruno E. is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=42a0fc093d427400

Artist: Bruno E.

Under Cover by Wayne Jones is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=a32eccf37d37d5aa

Artist: Wayne Jones

Fresno Alley by Josh Lippi & The Overtimers is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=8cf72700de3ceb92

Artist: Josh Lippi & The Overtimers

Bellissimo by Doug Maxwell is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=01a754e39ba99c79

Artist: Doug Maxwell

Darkest Child A by Kevin MacLeod is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://ift.tt/WZCQww

Artist: http://incompetech.com/

Darkest Child by Kevin MacLeod is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://ift.tt/WZCQww

Artist: http://incompetech.com/

Dark Matter by Chasms is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=98ee262fd8f56a22

Artist: Chasms

Feather Waltz by Kevin MacLeod is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://ift.tt/2ggL6pu

Artist: http://incompetech.com/

Dreaming Blue by Sextile is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=fa83a7253598afe5

Artist: Sextile

Their Story, Them Seeing by Puddle of Infinity is licensed under a Creative Commons Attribution license (http://bit.ly/1bFo3O7)

Source: https://www.youtube.com/audiolibrary_download?vid=3411c8740ed8b868

Artist: Puddle of Infinity

from Latest – Reason.com https://ift.tt/2X3YjD2

via IFTTT

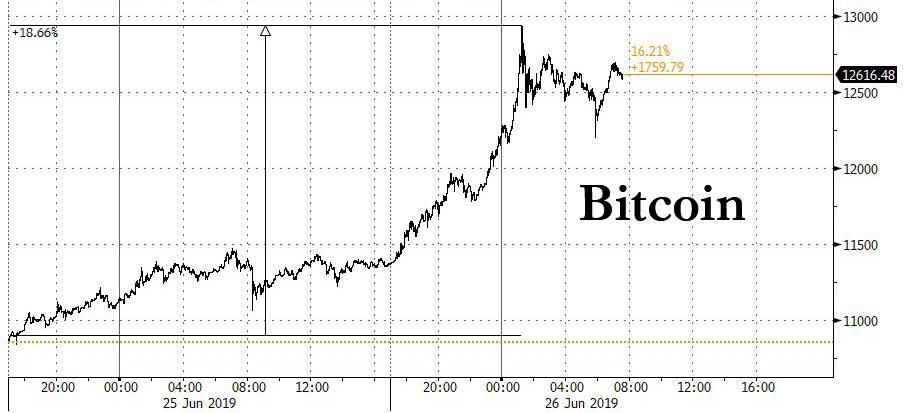

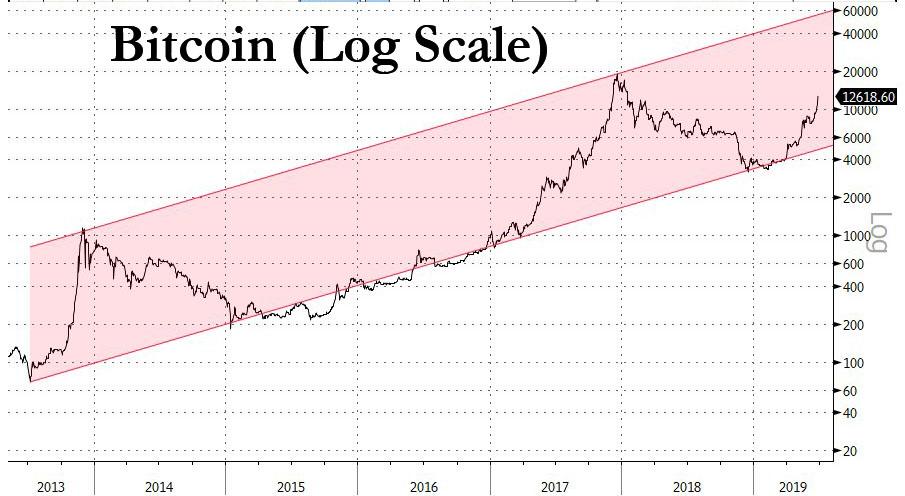

After breaching $10K over the weekend for the first time since March 2018, bitcoin has accelerated its sharp move higher and, trading close to $13,000 on Wednesday, up almost 20% in the past 24 hours. It is now up 240% since the start of the year, and even though it remains below its all-time high of nearly $20,000, at the current pace, it will surpass its all time high in just a few days.

The last time Bitcoin rose above $12,000 was in December 2017, when it continued to rally, on some days moving several thousand dollars inhours, eventually reaching its all time high as $19,511 just before Christmas 2017. That surge, however, was followed by a calamitous drop as retail investors fled, with the crypto dropping below $6,000 by February, and hitting $3000 just months later. All in all, in December 2017 and January 2018, Bitcoin spent about six weeks above $12,000.

Will this time be different, is the main question asked by traders. And as usual, the second biggest question posed by traders, investors, speculators and plain old haters is what is the reason behind the move.

According to some, Facebook’s announcement this month has revived interest in coins, while investors seeking safety have also pushed up Bitcoin’s price.

“It obviously does appear to be benefiting from some sort of flows that gold is benefiting, too,” CMC Markets chief strategist Michael Hewson said. “You’ve got all this stuff about Libra going on, which is renewing interest in bitcoin. Crypto is back in vogue.”

That part was right; what he said next, however, was not – he added that the investors buying bitcoin were speculative. That is precisely the opposite of what JPM found last weekend when the bank concluded that the current bout of buying is not retail – as was the case for much of 2017 – but institutional.

Meanwhile, as bulls cheer signs that the next bubble in cryptos is well and truly here, sparked by interest in virtual currencies from major companies like Facebook and JPMorgan, skeptics say it’s unclear how those initiatives will ultimately benefit Bitcoin and its peers.

It is also unclear if Facebook’s Libra “crypto” experiment has anything to do with the recent move. To be sure, it’s not news as it was well known months in advance that Facebook was launching its “crypto” product, which as explained here before, is not even crypto. Instead what appears to be causing the rush into bitcoin, ethereum and other cryptos is global monetary policy (and Chinese capital flight).

For an extended attempt to explain the recent surge in bitcoin, here is a tweet storm from CoinShares Chairman Danny Masters who lays out his, in our opinion, far more accurate take of what is behind the latest bubble in bitcoin.

1/ No, it’s not @facebook‘s “crypto” experiment. My trading instincts say it’s dollar weakness.

3/ Because of this, it’s inheriting the legal & regulatory hurdles associated with both crypto (difficult) & the legacy banking system (also difficult).

Our firm (@CoinSharesCo) is very familiar with this regulatory quagmire.

Facebook certainly has their work cut out for them.

5/ Though this news did not drive the recent price movement in my opinion, bitcoin will still benefit when (if) Libra manages to launch as it will provide a new crypto on-ramp for 2.9 billion users while familiarizing them with digital wallets and public-private key cryptography.

8/ Yet coincidentally #bitcoin is up over 200% through the first six-months of 2019, and continues to gain dominance as the crypto winter thawshttps://t.co/pwgL5c4rYS

9/ Another encouraging sign is that now we have more professional custodians:

– Fidelity @DigitalAssets is live

– @CoinbaseCustody too

– @ledgerx just secured @CFTC licenses

– @Bakkt futures supposedly launching in July

(Physical delivery is necessary for any true hedging.)

11/ Napkin math for CME $BTC futures volume compared to others supports this read…

– 1/5th of crude volume

– 1/16th of @Bitmex volume

– 1/100th of gold volume

In my view, we’ve got a long way to go before we can reasonably conclude that institutional money is here for good.

Finally, for those wondering where bitcoin may end up before the current bubble pops, here is the infamous bitcoin “log”chart which see the current hitting $60,000 some time soon.

via ZeroHedge News https://ift.tt/31XsjEn Tyler Durden

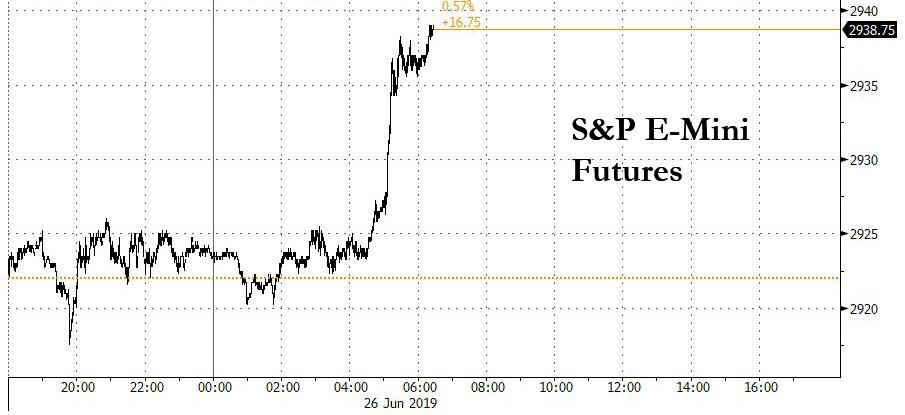

Global markets and US equity futures are so desperate for any trade war optimism that they positively soared just after 5am EDT when Treasury Secretary Steven Mnuchin regurgitated a long-running soundbite, saying that a trade deal between China and the United States was “90% completed”, days before a high-stakes meeting between the two countries’ leaders.

In an interview with CNBC on Wednesday morning, Mnuchin said this week’s G-20 summit in Osaka where Chinese President Xi Jinping and his US counterpart Donald Trump are expected to meet, would be “a very important G20” and adding that “we were about 90 per cent of the way there [to a trade deal] and I think there’s a path to complete this,” he said, without specifying the remaining 10 per cent.

On the other hand, it appears that nothing Mnuchin said was actually new as he footnoted his statement by saying that “the message we want to hear is that they want to come back to the table and continue because I think there is a good outcome for their economy and the U.S. economy to get balanced trade and to continue to build on this relationship.”

And while to many traders that was just a rehash of the default US position, one which has been voiced on many times before and did not offer any new facts or hint at the concessions demanded by China, it was enough to push US equity futures which until then had traded unchanged sharply higher, with European stocks following the move tick for tick.

Up until the Mnuchin comment, global stocks fell while the dollar rose on Wednesday as comments from Powell and Bullard dampened excitement about an aggressive rate cut as early as July from the world’s most important central bank. Fed Chairman Powell and St. Louis Fed President James Bullard on Tuesday pushed back on market expectations and presidential pressure for a significant U.S. interest rate cut of half a percentage point as soon as its next meeting.

Powell said the central bank is “insulated from short-term political pressures”. But he said he and his colleagues are currently grappling with whether uncertainties around U.S. tariffs, Washington’s conflict with trading partners and tame inflation require a rate cut.

As a result, the The European STOXX 600 index had fallen 0.3% to its lowest level in a week, while Germany’s Dax was down 0.15%, as the MSCI world equity index was down 0.16%, while U.S. futures indicated a flat to lower open.

All that reversed however on Mnuchin’s comments and the result was a sea of green across European markets and US futures, a move which however will be promptly reversed as traders realize that a trade deal with China only makes a rate cut by the Fed that much more unlikely, especially if the US does – as Bloomberg reported yesterday – delay the implementation on an additional $300 billion in Chinese imports as talks between the two superpowers restart.

Following Mnuchin’s comments, look for July rate cut odds to slide even more – according to latest market data, federal funds futures implied that traders saw a 27% chance of the Fed lowering rates by half a percentage point in July, compared to 42% on Monday.

While Mnuchin’s comments revived risk appetite, a major breakthrough may not come this weekend and Trump’s advisers are pushing him to avoid a hard deadline on implementing a new tranche of tariffs. Many traders hope the Federal Reserve will mitigate any headwinds to global growth with deep cuts, though Fed member James Bullard made clear Tuesday that’s not a given, as Bloomberg noted.

“My biggest concern here is that people think higher tariffs, or the threat of higher tariffs, can be offset by the promise of lower rates,” said David Kelly, chief global strategist at JPM Asset Management. “That’s not going to work.”

After sliding earlier, Europe’s Stoxx 600 Index erased an earlier drop of as much as 0.4% led by banks and autos shares, with health-care and utilities declining the most. Thyssenkrupp AG jumped on a report that Finnish manufacturer Kone Oyj is preparing a bid for the company’s elevator business.

Earlier in the session, and before Mnuchin’s comments hit, Asian stocks dropped for a second day driven by Powell’s hawkish comments combined with his warning of rising downside risks to the U.S. economy. Consumer staples and consumer discretionary were among the worst-performing sectors. Most markets in the region declined, with Japan and Taiwan leading losses. The Topix gauge fell 0.6%, driven by SoftBank Group and Kao. The Shanghai Composite Index edged down 0.2%, as Washington is said to delay imposing additional tariffs on China while both sides prepare to resume trade negotiations. CSC Financial and China Merchants Bank were among the biggest drags. The S&P BSE Sensex Index climbed 0.3%, led by HDFC Bank and ICICI Bank, as a deficient monsoon and signs of slowing growth raised hopes for stimulus in the federal budget next month.

Meanwhile, the Fed remains in a bind and will be unable to reverse its stance should any good news emerge: Richard Dias, multi asset strategist at Pictet Asset Management, said the Fed had effectively backed itself into a corner, making a cut in July or September highly likely.

“They are in a weird dichotomy, so many cuts are priced in and the market has rallied on this news and the bond market has rallied so if they don’t deliver what they have telegraphed, their credibility will be impinged,” he said, adding that he expected a cut of 25 basis points. “They would never do 50 bps, we are not in a recession,”

Elsewhere, in rates, what was initially a modest sell-off in U.S. Treasuries accelerates, and pushed 10Y Treasury yields climbed above 2% after closing around 1.98% yesterday. Euro-area bonds slipped as Austria looked to offer its second 100-year bond. Germany’s 10-year benchmark bond yield held around -0.32%.

In FX, the dollar steadied and the New Zealand dollar edged higher after the Reserve Bank of New Zealand (RBNZ) stood pat on monetary policy, keeping rates at a record low 1.50%. But the kiwi’s gains were limited as the central bank expressed concern towards economic risks at home and abroad. “Overall, today’s announcement provides a strengthened signal that another cut is coming, most likely soon, unless there is a marked improvement in the global outlook,” wrote economists at HSBC. The kiwi last traded 0.2% higher at $0.6651. Month- and quarter-end flows provided choppy price action in the euro and the pound, which traded with a defensive tone overall.

The yuan fell to its lowest since December against a basket of trading partners’ currencies but pared an earlier drop against the dollar, with investors remaining cautious ahead of this week’s G-20 summit. Investors are reluctant to be too bullish on the meeting between Presidents Donald Trump and Xi Jinping at this week’s G-20 summit, said Irene Cheung, a senior strategist at ANZ Bank. A third consecutive decline saw the Bloomberg CFETS RMB Index tracker fall to its lowest level since December. Hao Zhou, senior emerging markets economist at Commerzbank AG, said the yuan was pressured by an unwinding of EUR-CNY trades. He added that the yuan could edge lower on continued G-20 caution and on a report that three Chinese banks could face fallout from an investigation into North Korean sanctions violations.

A US admin official said USD would be less strong and the EUR would be less weak if the Fed took back rate hike from last fall, while the official added that there are many opinions in the White House about the President’s authority to demote Powell but also stated that the White House has no plans to demote Fed Chair Powell.

In the latest geopolitical news, North Korea said US extension of sanctions against North Korea is a direct challenge to Singapore summit agreement and an extreme act of hostility. Elsewhere, Iran’s atomic energy organisation spokesman says Iran will speed up the enrichment of uranium as the deadline given to European countries ends tomorrow, while Russia said it could ramp up safety measures for its workers in Iran, according to Russian press. Oh, and Iran’s Supreme Leader Khameni says Iran will not retreat in the face of US pressure.

U.S. crude oil futures advanced roughly 2% to touch a four-week high of $59.10 per barrel after data showed a decline in U.S. crude stocks. Gold retreated from a multi-year high.

Elsewhere, Bitcoin surged above $12,000 for the first time in more than a year, and briefly came within striking distance of the $13,000 mark.

Economic data include durable goods orders, inventory figures. Scheduled earnings include General Mills, Paychex, IHS Markit

Market Snapshot

S&P 500 futures up 0.5% to 2,936

STOXX Europe 600 up 0.1% to 383.91

MXAP down 0.4% to 158.68

MXAPJ down 0.06% to 522.99

Nikkei down 0.5% to 21,086.59

Topix down 0.6% to 1,534.34

Hang Seng Index up 0.1% to 28,221.98

Shanghai Composite down 0.2% to 2,976.28

Sensex up 0.1% to 39,490.07

Australia S&P/ASX 200 down 0.3% to 6,640.49

Kospi up 0.01% to 2,121.85

German 10Y yield rose 0.8 bps to -0.323%

Euro down 0.08% to $1.1358

Italian 10Y yield rose 0.6 bps to 1.797%

Spanish 10Y yield rose 0.8 bps to 0.388%

Brent Futures up 1% to $65.72/bbl

Gold spot down 0.8% to $1,412.41

U.S. Dollar Index up 0.1% to 96.26

Top Overnight News

In an interview with CNBC on Wednesday, Mnuchin expressed optimism that a U.S.-China trade deal could be reached by year end, saying the two sides “were about 90% of the way there and I think there’s a path to complete this,” with a need still for “the right efforts”

U.S. prosecutors are investigating an international network of traders suspected of infiltrating banks and companies to glean confidential information on megadeals, according to people familiar with the matter

Special Counsel Robert Mueller agreed to testify publicly before two House panels, setting up a dramatic hearing that promises to reinvigorate the national debate over his findings on Russian election interference and possible obstruction of justice by President Donald Trump

Algorithmic trading programs can be fast, but they also have to be right. While the RBNZ kept rates on hold Wednesday as widely expected, one tweet from a financial data company said rates had been cut, causing New Zealand’s currency fell as much as 0.6% before rebounding

The U.S. is willing to suspend the next round of tariffs on an additional $300 billion of Chinese imports while Beijing and Washington prepare to resume trade negotiations, people familiar with the plans said

Federal Reserve Chairman Jerome Powell said the downside risks to the U.S. economy have increased recently, reinforcing the case among policy makers for somewhat lower interest rates

Boris Johnson toughened his Brexit rhetoric with a “do or die” pledge to leave the European Union on Oct. 31 as Jeremy Hunt, his underdog rival to become U.K. prime minister, battled to persuade Tory party members the strategy is flawed

President Donald Trump threatened Iran with forceful retaliation for any attack on the U.S. after the Islamic Republic ruled out talks to resolve escalating tensions between the two nations

Oil ramped higher after an industry report suggested U.S. crude stockpiles continue to shrink, another bullish signal for a market that’s been boosted by the uncertain standoff in the Middle East.

Australia is urging Indo-Pacific nations to step up their commitment to free trade as the worsening fallout from the U.S.-China impasse threatens global growth

Special Counsel Robert Mueller has agreed to testify before two House committees on July 17, the chairmen of the panels said Tuesday night, promising to reinvigorate the national debate over his findings on Russia election interference and possible obstruction of justice by Donald Trump

Asian equity markets were mostly subdued following the headwinds from Wall St where stocks posted their worst performance in nearly a month as Fed speakers tempered rate cut bets. This was after Fed Chair Powell said many on the Fed see a case for more accommodation but also stressed the importance of not overreacting, and Fed’s Bullard who was the lone dovish dissenter at the last meeting, stated that he does not prefer a 50bps rate cut in July. ASX 200 (-0.3%) and Nikkei 225 (-0.5%) weakened with Australia led lower by gold miners after a pullback in the precious metal although resilience in healthcare, materials and industrials limited the downside, while sentiment in Tokyo was also downbeat with Japan Display among the laggards in the spotlight after several other groups withdrew from the Co. bailout. Elsewhere, Hang Seng (+0.1%) and Shanghai Comp. (-0.2%) were indecisive amid further PBoC liquidity inaction and ongoing uncertainty heading into the Trump-Xi meeting at this week’s G20, with the US said to be unwilling to give concessions on trade at the meeting and that no broad deal is expected, although it was also reported that the US is considering suspending the next round of tariffs on an additional USD 300bln of Chinese imports as the sides prepare to resume trade discussions. Finally, 10yr JGBs tracked the late losses seen in T-notes as market pricing of a 50bps Fed cut in July declined to 25% from around 43% the prior day, although the downside for Japanese bonds was cushioned by the negative risk tone and BoJ Rinban operation for JPY 775bln of JGBs concentrated in 1yr-5yr maturities.

Top Asian News

Bank of Thailand Holds Key Rate as Growth Weakens, Baht Surges

Asia’s Monster Trade Pact Could Be Done This Year, Minus a Few

China Urges U.K. to Not Interfere in Hong Kong Affairs

SGX Upholds Trades That Briefly Wiped $2 Billion From UOB Value

European equities rebounded off lows [Eurostoxx 50 +0.4%] after US Treasury Secretary Mnuchin sounded upbeat on US-China trade negotiations heading into this week’s G20. Mnuchin reiterated that the deal is “90% done”, albeit US officials have previously noted that the last 10% remains the hurdle. Although some suggested that Mnuchin was speaking in the past tense. Nonetheless, this boosted bourses out of the neutral/flat territory they had been in. Sectors are mixed, with energy and material names supported by price action in oil and base metals respectively, while financials outperform as yields nursed some recent losses post-Bullard and Powell, meanwhile the latest bout of Mnuchin-sparked “risk on” also weighed on bonds. Furthermore, chip names are supported amid optimistic earnings from Micron after-market yesterday (STMicroelectronics +2.5%, AMS +4.1%, Infineon +1.2%). In terms of other individual movers, Thyssenkrupp (+7.0%) shares spiked higher at the open amid speculation that Kone (-0.1%) is readying a bid for the Co’s elevator unit. Meanwhile, Brenntag (-4.1%) rest at the foot of the Stoxx 600 amid reports that the Co. sold dual-use chemicals to Syria.

Top European News

U.K. Breakeven Yields Fall as Lords Seeks Response on Inflation

Italian Bonds Briefly Extend Decline as 1Q Deficit Touches 4.1%

Italy First Quarter Budget Deficit at 4.1% of GDP

As Johnson Eyes No-Deal, MPs Vow to Fight Him: Brexit Update

In FX, FOMC easing prospects prompted by Powell and Bullard that have both cautioned against reacting too aggressively to downside growth and inflation risks. Hence, market pricing has shifted further towards 25 bp from 50 bp and the Greenback is clawing back some losses, especially against safer-havens amidst pre-G20 comments from US Treasury Security Mnuchin reiterating that 90% of the trade accord with China has been completed. The index is holding within 96.145-322 parameters, and for now at least not succumbing to bearish spot month end rebalancing requirements according to 3 if not more bank models.

NZD/AUD/CAD – The Kiwi is extending its winning run in wake of the RBNZ’s latest policy meeting and accompanying statement that reinforced guidance for lower rates, but was tempered somewhat by a balanced assessment of the economic outlook due to softer property prices vs more expansive fiscal policy. Moreover, the aforementioned latest US-China reports have sparked a broad rise in risk appetite with Nzd/Usd just topping out around 0.6680 and Aud/Usd retesting offers/resistance ahead of 0.7000. Meanwhile, the Loonie is consolidating gains made on the back of yesterday’s upbeat Canadian wholesale trade data with the aid of rebounding oil prices, with Usd/Cad hovering close to the bottom of a 1.3193-42 range and not visibly reacting to China extending its import ban to include all meat from Canada.

NOK – Another marked G10 outperformer and also fuelled by the post-API crude comeback, but deriving additional momentum from much better than forecast Norwegian jobs data, as Eur/Nok nestles around 9.6600 vs 9.7125 at one stage.

JPY/CHF – As noted above, the Yen and Franc have been undermined by less dovish Fed perceptions and revived US-China trade aspirations even though the Mnuchin ‘revelation’ is likely a statement about how things stood before talks ended in accusations of blame for reneging on pledges by both sides. Nevertheless, Usd/Jpy has nudged up over 107.50 from sub-107.00 on Tuesday and into the upper echelons of option expiries extending to 108.00-10 in decent size – see our 7.11BST post on the headline feed for full details. Similarly, Usd/Chf has rebounded to 0.9780 or thereabouts and Eur/Chf is back above 1.1100.

GBP/EUR – Sterling and the single currency are both relatively rangebound as Cable flits between 1.2705-2664 amidst BoE testimony to the TSC ostensibly on the now dated May QIR that merely underlined ongoing Brexit dependent policy guidance and Eur/Gbp pivots 0.8950. Eur/Usd has pulled back further from its modest 1.1400+ advance, but finding support ahead of 1.1350 and decent technical levels a fraction below, such as the 200 DMA and WMA. Note also, large expiry interest from 1.1370-80 (3.2 bn) and 1.1385-90 (1.8 bn) are likely to cap the headline pair.

WTI and Brent futures have held onto most of their API-inspired gains (crude stocks -7.7mln vs. Exp. -2.5mln) with the former hovering close to the USD 59/bbl mark (having briefly breached the level to the upside) whilst the latter eyes USD 66/bbl. News-flow for the complex has been light thus far, albeit prices are also underpinned by supply-side disruptions after Exxon’s Beaumont Texas refinery (366K bpd) suffered multiple upsets due to a power loss, while Philadelphia Energy Solutions, the largest refinery in the US East coast (335K BPD), is expected to be closed down after a recent fire. Elsewhere, gold remains just above the USD 1400/oz after retreating form 6yr highs as the USD recoiled after Fed’s Bullard and Powell tempered expectations of a 50bps cut. Meanwhile, copper prices extend gains above USD 2.7/lb, now eyeing 2.75/lb as strikes in the world’s largest open-pit mine (Codelco’s Chuquicamata mine) continue, with the workers reportedly blocking roads leading to other mines. In other news, Philadelphia Energy Solutions is expected to close its oil refinery following the recent fire, while the refinery is the largest in the east coast of the US with a capacity of 335k bpd.

US Event Calendar

7am: MBA Mortgage Applications 1.3%, prior -3.4%

8:30am: Durable Goods Orders, est. -0.2%, prior -2.1%; Durables Ex Transportation, est. 0.1%, prior 0.0%

8:30am: Cap Goods Orders Nondef Ex Air, est. 0.1%, prior -1.0%; Cap Goods Ship Nondef Ex Air, est. 0.1%, prior 0.0%

8:30am: Retail Inventories MoM, est. 0.3%, prior 0.5%, revised 0.5%; Wholesale Inventories MoM, est. 0.45%, prior 0.8%

DB’s Jim Reid concludes the overnight wrap

For those stuck on a trading floor or maybe in a hotel room this morning, I’ll be on CNBC at 9.30am London time. I was on Bloomberg TV a couple of weeks back and my wife said that one of the twins ran up to the TV and said “Dada” when he saw me. Meanwhile my daughter told my wife it was boring and insisted she put “Paw Patrol” back on. So clearly the bid-offer as to when children turn from adoration to boredom towards their parents is 1.75-3.75 years in my family.

Markets were a little less boring yesterday than on Monday as rates gyrated again and risk sold off even with Fed Chair Powell not revealing too much new information in his speech last night. He seems intent on maintaining optionality ahead of the pivotal July Fed meeting. Yields nevertheless rose and equities fell, as St. Louis Fed President Bullard was not as dovish as expected in comments at a separate event. This seemed to be a spark for sentiment deteriorating, alongside some weaker data.

In Powell’s remarks, on the dovish side, he said that “investment by businesses has slowed,” that “crosscurrents have re-emerged,” and that inflation expectations have declined. On the other hand, he said that “solid fundamentals are supporting continued growth” and that he does not want to “overreact to any individual data point or short-term swing in sentiment.” So something for everyone there, and on the policy front he repeated his previous comments in favour of acting “as appropriate to maintain the expansion.” Asset prices initially reacted in a way consistent with a hawkish interpretation of his comments, with yields trading higher, equities falling, and the dollar strengthening, but the moves were minor and subsequently retraced.

What’s ended up being more impactful for markets were earlier comments from regional president Bullard. He is a voter this year and is considered the most dovish member of the committee, having dissented in favour of a rate cut at the June meeting. He spoke ahead of Powell and said that while the current environment seems like a good time for an “insurance rate cut,” the situation does not call for an immediate 50bps cut, saying such a move would be “overdone.” He went on to confirm that he is one of the FOMC members who favours 50bps of easing overall this year. Accordingly, this signals that he prefers to begin with a 25bps cut in July, which is less than currently discounted by the market. Two-year yields initially shot up +5.8bps after his remarks and the dollar strengthened +0.37%.

Equities had already been trading lower before the Fedspeak, after several economic releases fell short of expectations earlier in the morning (more below). The S&P 500 ultimately ended -0.95%, with over half of the losses coming after Bullard and Powell spoke. The NASDAQ and DOW ended -1.51% and -0.67%, respectively. The moves in rates proved less persistent, with 2-year treasuries ending flat (albeit before a +3.2bps move this morning) and 10-year yields down -2.9bps, but with 10 years closing below 2% for the first time since the US election day in 2016 – although they are back above that in Asia this morning. However, the shift in fed funds futures pricing proved durable, with the yield on the August contract closing +3.5bps higher, reflecting the reduced odds of a 50bps cut next month. The market reaction was indicative of slightly higher odds of a policy mistake, with 10-year inflation breakevens falling -3.8bps and the yield curve (2s10s) flattening -3.1bps.

In Asia overnight, the Nikkei (-0.59%) and Shanghai Comp (-0.23%) have followed Wall Street’s lead however the Hang Seng (+0.05%) and Kospi (-0.01%) are flattish. The recent rally for the Japanese yen which saw it hit the strongest level since April 2018 has abated a bit this morning, weakening -0.25%. The big mover overnight is oil though where WTI is up +2.09% following a report from the American Petroleum Institute indicating that US crude stockpiles fell by 7.55 million barrels last week.

Away from the Fedspeak, Bloomberg has run a story overnight suggesting that the US is willing to suspend the next round of tariffs on an additional $300bn of Chinese imports. The report notes that the decision is still under consideration and may be announced after a meeting between Trump and Xi this Saturday. Supposedly a call between Lighthizer and China Vice Premier Liu He was described as “productive” on Monday. Meanwhile, the US senate passed a resolution yesterday that “will consider all necessary measures” to limit risks of the US government or military using networks “compromised” by Huawei or ZTE equipment. The measure, which will move on for further votes, called for more pressure for allies to shun the companies’ network equipment. In other news, Special Counsel Robert Mueller has agreed to testify before two House committees on July 17 over his findings on Russia election interference and possible obstruction by President Trump.

Back to yesterday, where Powell’s remarks came as data from the Conference Board earlier in the day showed consumer confidence falling to 121.5 in June (vs 131.0 expected), down from May’s revised 131.3 reading and the lowest since September 2017. There weren’t many positives to find elsewhere in the data either, with the present situation falling to 162.6, the lowest since June last year, while the expectations reading fell to 94.1, the lowest since January. My colleague Torsten Slok sent round an interesting chart over the weekend (which we’ve recreated in the pdf today if you want to click) which shows the gap between the two being as wide as it is now is a good historical predictor of an upcoming recession.

Also of note from the Conference Board, the proportion saying that jobs were “hard to get” rose to 16.4%, the highest since November 2017, while the proportion saying that jobs were “plentiful” fell to 44.0%. The differential between the two, a closely-watched gauge of labour market sentiment, had its sharpest shift in over a decade. In previous cycles, this differential being stretched ended up being a good signal for the bottom in unemployment, so if maintained, it would certainly refocus the Fed’s attention on incoming labour data, especially the next jobs report due next Friday. Other US data proved no more promising, with new home sales for May falling to 626k (vs 684k expected), the Richmond Fed manufacturing index falling -2pts to 3, and retail sales figures getting revised lower.

Before Powell’s speech, equity markets in Europe closed lower, with the STOXX 600 -0.10% as the index lost ground for a third consecutive session. It was a similar picture elsewhere on the continent, with the DAX (-0.38%), the CAC 40 (-0.13%) and the FTSE MIB (-0.73%) all posting losses. Banks led the declines, with the STOXX Banks index -0.51% to close at its lowest level since December last year.

Rates had earlier rallied in Europe too, with bund yields falling to another record low yesterday of -0.333bps, down -2.4bps. French ten-year debt also closed in negative territory for their first time ever at -0.009% having shed -2.8bps, while Spanish and Portuguese yields fell -2.9bps and -4.7bps respectively to fresh lows. Meanwhile, the UK sold 30-year debt at an average yield of 1.421%, also a record low. However, in a sign that the ECB’s dovish pivot may already be wearing off on markets, and in a similar vein to the price action in the US fixed income market, five-year forward five-year inflation swaps fell -5.4 basis points to 1.214%, 12 basis points lower from Friday’s intraday high. A big and worrying shift.

As the war of words continued between the US and Iran, President Trump tweeted yesterday that “Iran leadership doesn’t understand the words “nice” or “compassion,” they never have. Sadly the thing they do understand is Strength and Power”. He also described their statement as “very ignorant and insulting”, and said that “Any attack by Iran on anything American will be me with great and overwhelming force.”

With rising geopolitical tensions, and ultra dovish central banks, it’s worth noting that gold reached a fresh six-year high yesterday of $1423/oz, though it did pare its gains after Bullard’s hawkish comments. It nevertheless has just had its biggest one-week increase in over three years. Another striking fact is that the ratio of gold and silver prices has risen to its highest level since 1993 at 92.6.

It’s not just gold that’s rising, with Bitcoin also at its highest level in over a year at $12,154 this morning, with a 203% rise since the start of April. We’re still some way from the peak above $19,000 reached in trading at the end of 2017, but the scale of the recent appreciation is striking. Obviously recent dovishness from central banks has seen investors look towards alternative currencies, but perhaps Facebook’s unveiling of its Libra currency has seen investors look again at cryptocurrencies with fresh eyes.

In terms of yesterday’s other data, sterling pared back gains against the dollar and the euro to close -0.42% weaker after the CBI’s survey of retail sales showed a reported balance of -42 in the year to June, the lowest since March 2009, with just 16% of retailers reporting higher sales volumes compared with last year. However it’s worth noting this has been a volatile series, and the figures will have been affected by last summer’s unseasonably hot weather. In France, the Insee’s business confidence remained at 106 for a third consecutive month in June, in line with expectations.

In other political news, the frontrunner to be the UK’s next Prime Minister, Boris Johnson, appeared to harden his rhetoric on Brexit yesterday, saying in an interview with talkRADIO that his commitment to leave the EU on the 31 October deadline was “Do or die. Come what may.” Later on, in a letter to his leadership rival, Foreign Secretary Jeremy Hunt, Johnson said that “I have been clear that, if I am elected leader, we will leave on 31 October with or without a deal.” Yesterday the Conservative Party also confirmed that the new leader would be announced on July 23rd in just under four weeks’ time.