San Francisco lived up to its reputation as the nation’s NIMBY capital this week by voting to reject a proposed apartment project over concerns that the new building would cast too much shadow on a nearby park.

On Tuesday, the city’s Board of Supervisors unanimously voted to delay the approval of a 65-unit apartment building slated to be built on Folsom and Russ Street in the city’s SoMa neighborhood. The project is being sponsored by developer Golden Properties LLC, and has been working its way through the approval process since August 2017.

Despite the fact that Golden Properties’ development would add new units of housing to a city in desperate need of it, supervisors thought the building’s costs would outweigh any benefits.

“We absolutely need more housing and affordable housing,” said Supervisor Matt Haney to the San Francisco Chronicle, but “this isn’t a meaningless shadow on someone’s backyard. This is a shadow that falls on the only multi-use public park in SoMa.”

Indeed, the proposed six-story building would, on the longest day of the year, cover an additional 18 percent of nearby Victoria Manalo Draves Park—which boasts a community garden, basketball court, and softball field—in shade, according to a study performed by the city’s Planning Department.

That might not sound like much, but it has been a sticking point for the South of Market Community Action Network (SOMCAN), a neighborhood group that has fiercely opposed the project and the additional shadow it would cast. Thanks to the byzantine nature of San Francisco’s development regulations, the group has had ample opportunity to delay the Folsom project.

San Francisco’s planning code prohibits new buildings from casting shadows on public parks managed by the city’s Parks Department if those shadows are found to have an “adverse impact.” However, what exactly counts as an “adverse impact” is ultimately left up to the city’s Planning Commission to decide. In a heated commission hearing on the project in December 2018, community activists spoke about the perceived damage the project would do to the neighborhood.

“The scale and size of the project seems to be monstrous,” said one member of SOMCAN, who also stressed the severe impact of the building’s shade, saying “any wet surfaces in the park that are shaded will continue to be wet, damp, and cold for a longer period after the shadow passes.”

Other neighborhood opponents expressed concern about the displacement of existing commercial tenants at the lots that were to be redeveloped into housing, or otherwise bemoaned the impacts on precious open space in an area of the city sorely lacking in it.

These arguments proved persuasive for some commissioners, with one saying that she’d “never supported any shadow on any park unless a project was 100 percent affordable or served a community purpose larger than private development.”

Nevertheless, commission voted to approve the project in a tight 4-3 decision.

That did not end the controversy, however. SOMCAN then appealed to the San Francisco Board of Supervisors, arguing that there had been insufficient study of the shadow question.

This time, the group was luckier, convincing a unanimous board to send the project back to the Planning Commission for further review. Given how fast costs for materials and labor are rising in the Bay Area, a delay of even a few months can cost developers hundreds of thousands of dollars.

This gives SMCAN incredible leverage to get more concessions from Golden Properties; possibly getting the developer to agree to a reduction in the size of their Folsom project, or an increase in the number of below-market-rate units it will include.

This series of events is hardly unique to the Folsom project. Indeed, it bears a striking similarity to another proposed San Francisco apartment project profiled byReason.

In that case, property owner Robert Tillman has struggled for years to get permission to redevelop a laundromat he owns into 75-unit apartment building in the neighboring Mission District over the objections of community activists who’ve argued that his laundromat is a historic resource, and that the shadow it would cast on a nearby school park would be detrimental to the health and safety of neighborhood children.

A big difference between the two cases is that the Board of Supervisors’ decision to delay the Folsom project has earned it some sharp criticism from San Francisco Mayor London Breed.

“You cannot claim to be pro-housing and then reject projects like this one,” tweeted Breed, a self-identified YIMBY (Yes in my Back Yard) who won election in June 2018 on a pro-housing platform. “Low- and middle-income folks continue to be pushed out of our city. Average rent for a one-bedroom apartment is ~$3,600. We. Need. More. Housing.”

The irony is that Breed, in one of her last acts in her previous job as city supervisor, bowed to the demands of neighborhood activists, and voted to delay Tillman’s project for lacking sufficient shadow study.

from Latest – Reason.com http://bit.ly/2Xawqde

via IFTTT

Nate Carter is bringing a $3 million lawsuit against the city of Chattanooga, Tennessee, its police department, and the officer responsible for his tasing and wrongful arrest.

According to the complaint, the April 2018 incident began when police responded to a 911 call about a man threatening the caller with a gun. The caller described the suspect as a black man with short hair, who was heavy-set and wearing green and black pants.

The suspect had fled by the time police arrived. Instead, they saw Carter, who was wearing a purple t-shirt and black shorts. Officer Cody Thomas asked Carter to identify himself. Carter, who said he was checking his mail outside, responded that Thomas was not welcome to come to his house. The situation escalated with Thomas telling Carter, “How about you watch your mouth before your ass gets thrown in the back of my car.”

Thomas pulled out a Taser and threatened to shoot Carter’s “fucking dog,” which was barking in the front yard. Carter attempted to go into his house, at which point Thomas shot Carter in the back with his taser, causing him to fall on his front porch. Carter managed to make his way inside, and Thomas called for backup. Carter then re-emerged from his home with his family while several officers, including Thomas, pointed guns and tasers toward Carter, his family, and his dog. After the family was out of the way, the officers moved to arrest Carter.

Body camera footage shows Carter’s arrest.

(The arrest begins after 3:27)

Thomas later claimed that Carter was standing in the street and “bolted” prior to the incident. He charged Carter with disorderly conduct and resisting arrest. Those charges were thrown out by a judge in November and Carter is now suing.

This is not the first incident involving Officer Thomas. In February 2018, Thomas and other officers entered the home of Dale Edmonds after a neighbor told emergency services that someone was sitting in a black vehicle in Edmonds’ driveway. The person in the vehicle was a Department of Child Services agent who was waiting while a second agent was meeting with Edmonds inside of the house. Though the agent explained to officers the purpose of their trip, Thomas and others entered the house through the backdoor without a warrant. The officers led Edmonds, his housemate, and the agent outside of the house at gunpoint, but not before Thomas “manhandled” Edmonds, who was recovering from a gunshot wound.

Robin Flores, an attorney and former police officer who works on police brutality cases, is representing Carter. Their suit argues that the city “has long-established patterns of overlooking or providing excuses and reasons to justify the misconduct of its officers.” Flores told Reason that the complaint highlights how the city fails to “discipline and supervise” officers. The complaint lists other reports of bad policing by Chattanooga police dating back to 2003, including excessive force, lingering investigations, domestic abuse, and sexual harassment.

Flores told Reason that the Supreme Court has ruled that the language Carter used during his arrest is a form of protected speech. In 1974, the court ruled against a Louisiana statute that criminalized the use of obscene language while an officer is performing their duties. Justices argued that the law was too broad to fit within the legal definition of “fighting words” and had the potential to be abused in instances lacking a valid reason for an arrest.

Though Thomas’ body camera was rolling during the incident, he turned his cruiser’s dash camera off in violation of the department’s policy. At one point, Thomas’ hand covers his body camera. The complaint argues that this was done either in an attempt to turn it off or conceal his interaction with Carter.

Flores says that the footage available in both Carter’s case and in the Edmonds case is “critical enough to bring a claim” against Thomas, the department, and the city. In other instances, footage has been enough to drop charges and reopen the cases of offending officers. He also mentions another case where he dismissed a suit after his client’s version of events did not match the camera footage. This, he says, also protects police officers.

from Latest – Reason.com http://bit.ly/2IgbpKD

via IFTTT

There are no extreme “fixes” to secular declines in sales, profits, employment, tax revenues and asset prices.

The saying “never let a crisis go to waste” embodies several truths worth pondering as the stock market nears new highs. One truth is that extreme policies that would raise objections in typical times can be swept into law in the “we have to do something” panic of a crisis.

Thus wily insiders await (or trigger) a crisis which creates an opportunity for them to rush their self-serving “fix” into law before anyone grasps the long-term consequences.

A second truth is that crises and solutions are generally symmetric: a moderate era enables moderate solutions, crisis eras demand extreme solutions. Nobody calls for interest rates to fall to zero in eras of moderate economic growth, for example; such extreme policies may well derail the moderate growth by incentivizing risk-taking and excessive leverage.

Speculative credit bubbles inevitably deflate, and this is universally viewed as a crisis, even though the bubble was inflated by easy money, fraud, embezzlement and socializing risk and thus was entirely predictable.

The Federal Reserve and other central banks are ready for bubble-related financial crises: they have the extreme tools of zero-interest rate policy (ZIRP), negative-interest rate policy (NIRP), unlimited credit lines, unlimited liquidity, the purchase of trillions of dollars of assets, etc.

But what if the current speculative credit bubbles in junk bonds, stocks and other assets don’t crash into crisis? What if they deflate slowly, losing value steadily but with the occasional blip up to signal “the Fed has our back” and all is well?

A slow, steady decline is precisely what we can expect in an era of credit exhaustion, which I’ve covered recently: ( The Coming Global Financial Crisis: Debt Exhaustion). The central bank “solution” to runaway credit expansion that flowed into malinvestment was to lower interest rates to zero and enable tens of trillions in new debt. As a result, global debt has skyrocketed from $84 trillion to $250 trillion. Debt in China has blasted from $7 trillion 2008 to $40 trillion in 2018.

A funny thing happens when you depend on borrowing from the future (i.e. debt) to fund growth today: the new debt no longer boosts growth, as the returns on additional debt diminish. This leads to what I term credit/debt exhaustion: lenders can no longer find creditworthy borrowers, borrowers either don’t want more debt or can’t afford more debt. Whatever credit is issued is gambled in speculations that the current bubble du jour will continue indefinitely– a bet guaranteed to fail spectacularly, as every speculative credit bubble eventually implodes.

As expanding credit no longer generates real-world growth, growth slows.Over time, marginal borrowers default as revenues and profits erode, and this triggers a corresponding erosion in employment and wages.

This erosion is so gradual, it doesn’t qualify as a crisis, and therefore central banks can’t unleash crisis-era fixes. Not only do they lack the political will to launch extreme policies in a moderate decline, it would be unwise to empty the tool bag of extreme fixes at the first hint of trouble; what’s left for the crisis to come?

Even worse, if the extreme policies fail to restore rapid growth and more importantly,confidence in future rapid growth, then ramping up extreme policies will be correctly interpreted as the desperate acts of clueless authorities. This will crush confidence and trigger the very crisis the authorities sought to forestall.

There are no extreme “fixes” to secular declines in sales, profits, employment, tax revenues and asset prices. Moderate stagnation will not be reversed with moderate fixes (lowering interest rates a quarter of one percent, etc.), and any attempt to institute extreme policies will expose authorities’ desperation right when confidence is vulnerable to collapse.

The Fed and other central banks are trapped in more ways than one.

* * *

If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

via ZeroHedge News http://bit.ly/2Xf1R6c Tyler Durden

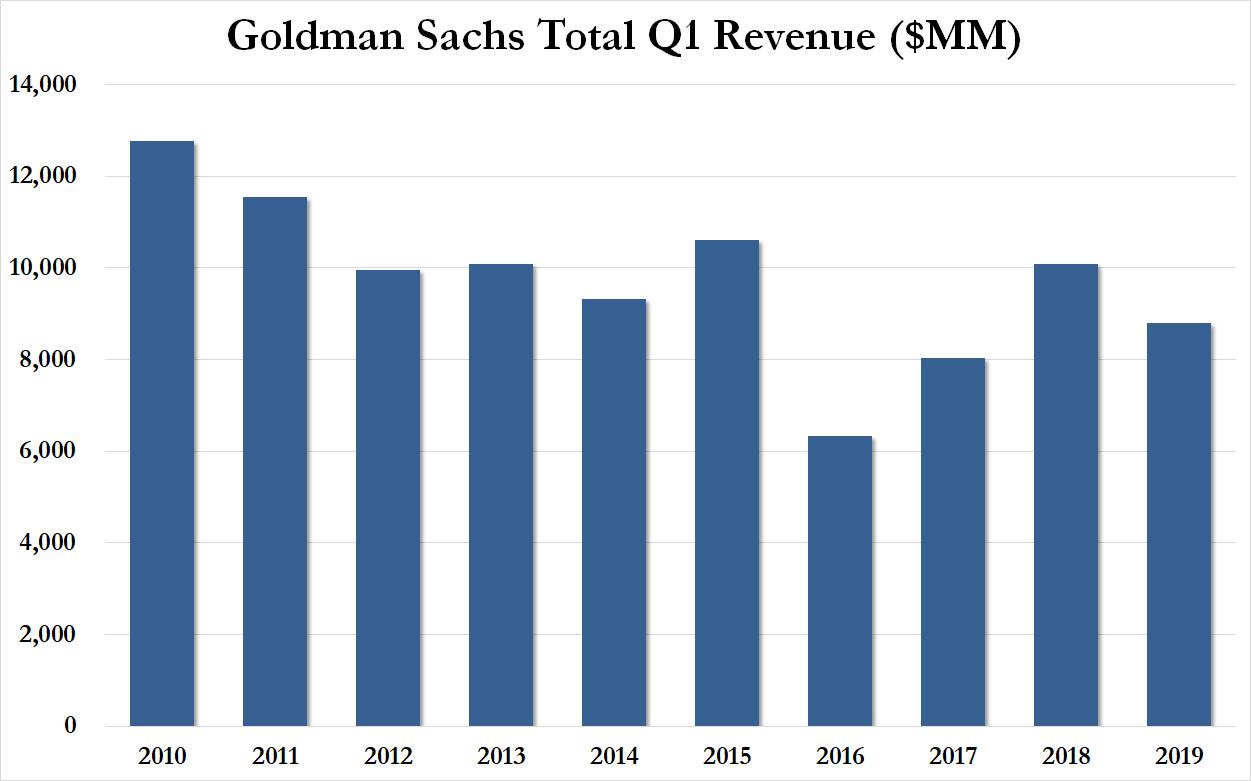

Following JPMorgan’s across the board beat, and Wells Fargo’s latest disappointing results, moments ago Goldman reported a mixed set of numbers, with the company solidly beating on earnings, as EPS came in at $5.71, above the $4.89 expected, while revenues disappointed, printing at $8.81BN, below the $8.99BN consensus exp., and down 13% from a year ago. Of note, Goldman reported an effective income tax rate for Q1 of 17.2%, up from the full year rate of 16.2% for 2018, as the tax cut tailwind is now officially over.

Looking at the big picture, in the positive column, was GOldman’s announcement that the company was boosting its dividend from $0.80 to $0.85, allaying fears that the 1MBD scandal is now well in the rearview mirror. The flipside, however, was that revenue has continued to shrink at the bank as the news management appears unable to find the sweet spot for the bank’s potential…

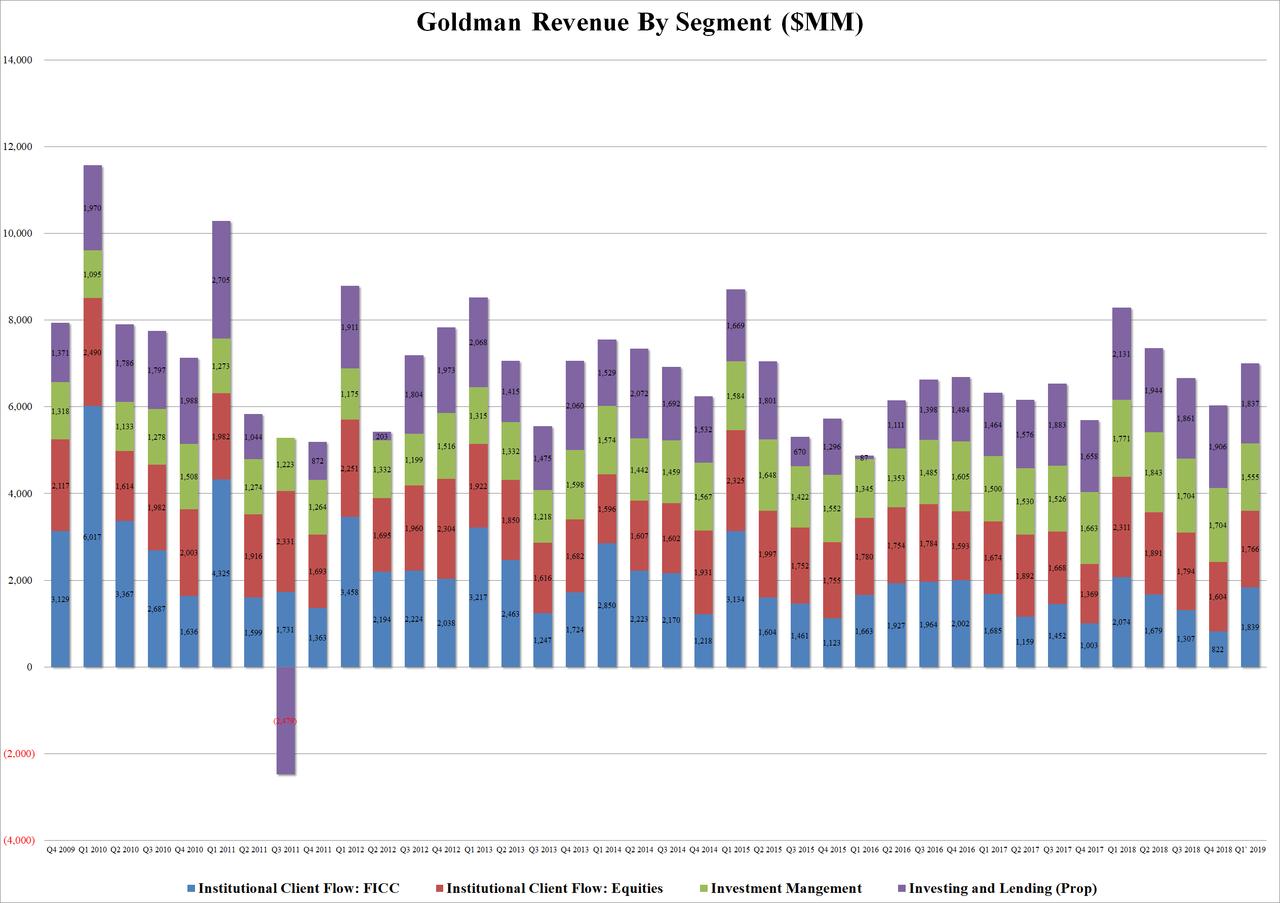

… while the company core verticals, FICC and equities, both underwhelmed, with the latter missing expectations, as Goldman’s equity traders brought in $1.77 billion, 24% lower than last year, and below the $1.83 billion expected. As Bloomberg notes, that’s basically inline with the $1.74 billion JPMorgan brought in. Discussing the disappointing results, Goldman said that Q1 net revenues significantly decreased YoY as the “market backdrop was more favorable in 1Q18”, to wit:

Equities client execution net revenues decreased significantly, particularly in derivatives, versus a strong 1Q18

Commissions and fees decreased, reflecting lower market volumes

Securities services net revenues decreased, primarily reflecting lower average customer balances

The equity weakness was offset by stronger than expected FICC numbers, as revenue in the highest margin segment printed at $1.84BN, above the $1.78BN expected, but well below the $2.084BN from a year ago. Commenting on the 11% drop Y/Y in FICC, Goldman said that this reflected “lower net revenues in interest rate products, currencies and credit products, partially offset by higher net revenues in mortgages and commodities.”

While trading disappointed on net, the biggest upside surprise came fromt he bank’s investment banking segment, which were $1.81 billion for the first quarter of 2019, unchanged compared with the first quarter of 2018 and 11% lower than the fourth quarter of 2018. And even as net revenues in Underwriting was $923 million, notably, or 24%, lower than the first quarter of 2018, due to significantly lower net revenues in equity underwriting, “primarily reflecting a significant decline in industry-wide initial public offerings, and lower net revenues in debt underwriting, primarily due to significantly lower net revenues from leveraged finance transactions,” the most impressive aspect of Goldman’s business was Financial Advisory revenues, which jumped to $887 million, well above the $819 million expected, and 51% higher than the first quarter of 2018, “reflecting an increase in completed mergers and acquisitions volumes.”

In other words as trading has continued to shrink, it was all up to the bank’s M&A bankers to salvage the quarter.

Visually, here is a breakdown of Goldman’s quarter:

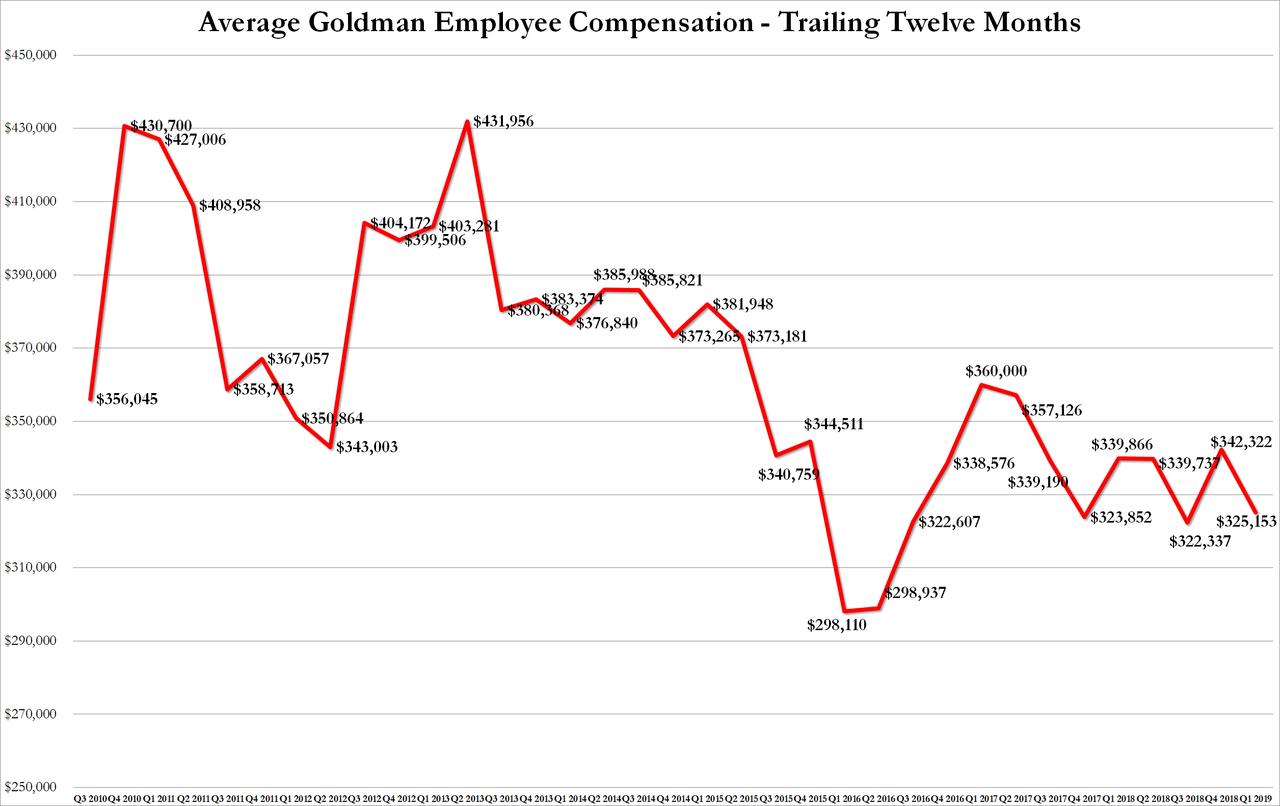

Reflecting the disappointing Q1 revenue, Goldman’s Q1 compensation expenses shrank to $3.26 billion from $4.1 billion a year ago, below the estimated $3.61 billion, and with Goldman’s headcount declining once more and shrinking to 35,900 from 36,600, this meant that average compensation per Goldman employee was fractionally lower, to $325,153 down from $342,322 a quarter ago, and has been stuck in a narrow range in the low $300,000s for the past two years.

Commenting on the results, CEO and DJ David Solomon was upbeat as expected, saying that “we are pleased with our performance in the first quarter, especially in the context of a muted start to the year. Our core businesses generated solid results driven by our strong franchise positions. We are focused on new opportunities to grow and diversify our business mix and serve a broader range of clients globally. With improving momentum across our businesses, we are confident that Goldman Sachs will generate attractive returns for our shareholders.”

The market reaction to Goldman’s earnings however was rather more muted, and reflected disappointment, as the stock initially spiked on the EPS beat and dividend boost, however it has since shrunk and was modestly in the red as traders digested the continuing weakness in the company’s trading group.

via ZeroHedge News http://bit.ly/2DeLmj4 Tyler Durden

Last week, the Federal Reserve released their March FOMC meeting minutes. Following the release, the markets surged higher as the initial reading by the markets was “the Fed is done hiking rates.” As the Wall Street Journal reported in Fed Minutes: Officials See Little Need to Change Rates This Year.

‘Minutes of the March meeting released Wednesday showed officials see little reason to continue raising rates due to greater risks to the U.S. economy from the global growth slowdown and muted inflation readings that took more officials by surprise.

‘A majority of participants expected that the evolution of the economic outlook and risks to the outlook would likely warrant leaving the target range unchanged for the remainder of the year,’ the minutes said.

At the same time, the minutes show officials didn’t perceive any need to cut their benchmark rate absent a broader deterioration in the economy. Officials said their view of the appropriate setting for interest rates ‘could shift in either direction based on incoming data and other developments.’

Since officials last met, President Trump has said he would like to see the Fed undo its last two rate increases. Fed officials have said they will base their decisions on the economic outlook and not political pressure.’

See, nothing to worry about as there are no recessions predicted by the Fed…ever.

As Peter Bookvar noted Wednesday afternoon, don’t believe for a moment the Fed isn’t specifically targeting the market:

“I’ve said many times to insert ‘S&P 500’ for ‘financial developments’ because that is essentially what we’re talking about here when its cited. So the Fed is referring to ‘significant uncertainties’ with regards to the S&P 500. What uncertainties exactly now since the S&P 500 is just off all time record highs?

They also acknowledged that their jawboning which shifted policy to one that is more ‘flexible’ is what boosted the stock market. ‘In their discussion of financial developments (S&P 500), participants observed that a good deal of the tightening over the latter part of last year in financial conditions (S&P 500) had since been reversed; Federal Reserve communications since the beginning of this year were seen as an important contributor to the recent improvements in financial conditions (S&P 500). Participants noted that asset valuations had recovered strongly.’

Thanks Fed, high five and the parenthesis and underline are obviously mine.”

But here is the problem with the market’s assumption:

“The Fed Did Not Say They Were Done Hiking Rates”

While the Fed said they would be “patient” for now, there are already indications that economic growth and inflation will pick up over the next couple of quarters, (No, this isn’t the revival of the economy, but simply a normal seasonal bounce from pent up demand following a cold winter.)

Complicating matters for the Fed is the strength of the dollar, the continued rise oil prices which is already leading to stronger inflationary prints, and increases in wages which will lead to concerns about an overheating economy. Such will put the Fed in a “box” with respect to both being “data dependent” as well as maintaining some semblance of “independence.”

In other words, while they may be “patient” for the moment, that doesn’t mean their position won’t change. As noted in their minutes:

“Most participants indicated that they did not expect the recent weakness in spending to persist beyond the first quarter.”

“Several participants noted that their views of the appropriate target range for the federal funds rate could shift in either direction based on incoming data and other developments. Some participants indicated that if the economy evolved as they currently expected, with economic growth above its longer-run trend rate, they would likely judge it appropriate to raise the target range for the federal funds rate modestly later this year”

Furthermore, as I noted in this past weekend’s missive, the Fed has already been dropping hints (since the March meeting) about further rates hikes in 2019 and 2020.

“Cleveland Fed President Loretta Mester:

‘Could we be done with policy rate increases this cycle? It is possible, but if the economy performs along the lines I think is the most likely case…the fed-funds rate may need to move a bit higher than current levels.’

Philadelphia Fed President Patrick Harker:

‘I continue to be in ‘wait-and-see mode‘ with expectations of at most, one hike for 2019 and one for 2020.”

Those comments don’t align with a Fed eager to sit on the sidelines, reduce rates, or begin to inject further stimulus.

However, while markets rallied on the idea the Fed will stay pat, for now, this still doesn’t alleviate the problems we noted previously:

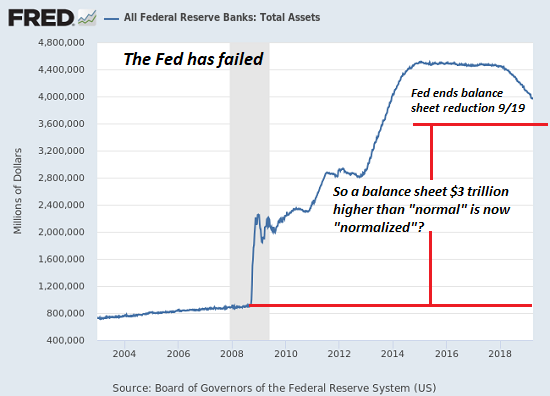

Yes, the Fed isn’t hiking rates, but they aren’t reducing them either.

Yes, the Fed isn’t reducing their balance sheet any more after September, but they aren’t increasing it either.

While economic growth outside of China remains weak, the year-over-year credit expansion in China IS slowing.

There is no massive disaster currently to spur a surge in government spending and reconstruction.

There isn’t another stimulus package like tax cuts to fuel a boost in corporate earnings

With the deficit already pushing $1 Trillion, there will only be an incremental boost from additional deficit spending this year.

Unfortunately, it is also just a function of time until a recession occurs.

Most importantly, even if the Federal Reserve does begin to reverse course and inject liquidity, the effectiveness of those actions will likely not have the same effect.

Why?

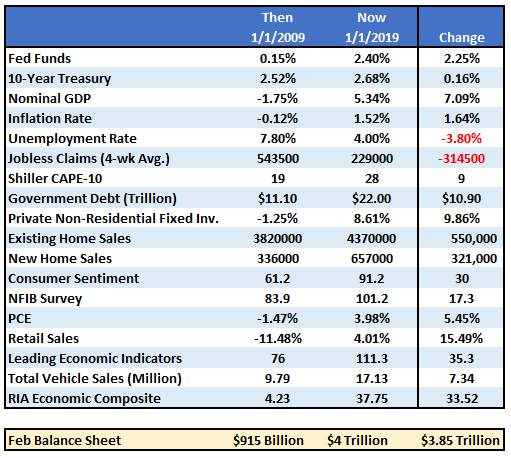

Because the economic backdrop is not what it was a decade ago. The table below compares a variety of financial and economic factors from January of 2009 to January 2019.

“The critical point here is that QE and rate reductions have the MOST effect when the economy, markets, and investors have been ‘blown out,’ deviations from the ‘norm’ are negatively extended, confidence is hugely negative.

In other words, there is nowhere to go but up.”

Unfortunately, the Fed is trapped between the data and their “need to do something” to keep the asset prices inflated to support economic growth.

But that may not be enough as the bond market is already sniffing out the problems. Back to Peter Bookvar:

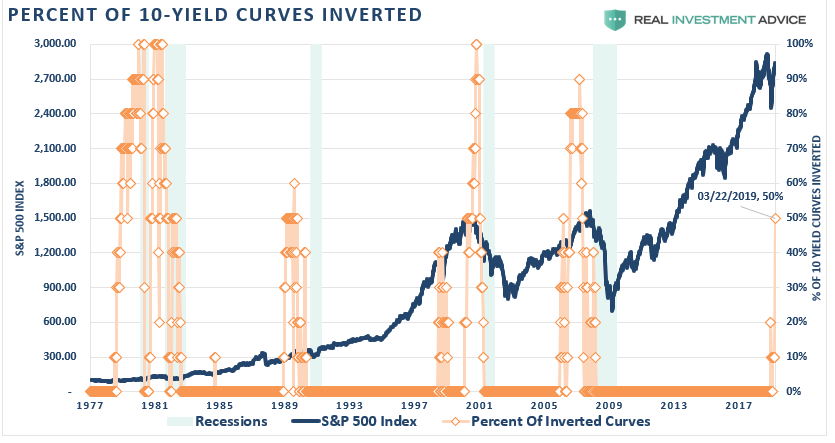

“The stock market is assuming…things will improve in Q2 and throughout the second half. The bond market has a less-optimistic take on that, saying that the data is weak, and we’re going to reflect that right now in lower yields and inversions within the yield curve.”

Currently, 5 out of 10 yield curves we track (50%) are now inverted. Such is the highest risk of a recessionary onset as we have seen since 2007.

For Boockvar’s part, the fixed-income market is the indicator to watch.

“The bond market is going to be right. We’re in a slowdown that’s not just temporary, and I think that’s something that’s going to last throughout the year.”

He is right.

While we are maintaining our equity exposure currently, we have also hedged those long-positions with gold and gold mining stocks, a heavier weighting than normal in cash, and have recalibrated the duration and credit risk in our bond holdings to account for the inversion.

This is simply because the “risks” continue to outweigh the reward for the markets currently. As Doug Kass recently noted:

“Negative or near zero interest rates represent conditions that understandably exist immediately following a deep recession, not 10-years after.

Fewer Tools Left in the Policy Shed as the Fed ends the tightening cycle with the absolute and real Federal Funds rate several hundred basis points lower than any economic cycle in history.

Debt Is a Governor to Growth and debt that is not self-funding is future consumption brought forward.

Deficit and Demographic Threats combined with a Fed balance sheet, which is four times normal, and slowing population growth, diminish intermediate to longer-term economic and profit growth prospects. Such is not supportive of higher valuations or asset prices.

No Country Is an Economic Island and the lack of coordination between the super economic powers in the world will likely exacerbate worldwide economic risks.

The Misallocation of Resources Causes Bubbles and low interest rates which we have experienced for years have always – in every cycle – been a source of ‘mischief’ and a misallocation of resources. The only question is ‘when’ something breaks it will ripple through the financial markets like a tidal wave. (Think about the proliferation of ‘covenant-lite’ loans.)”

Summary

While the Fed has successfully “jawboned” the markets recently to keep asset prices stable and positive, there will come a point where “verbal liquidity” simply isn’t enough. The fact that economic cycles will eventually complete seems to be lost on the Fed. As Mike Shedlock noted:

The weakness of inflation pressures given a strong job market and accelerating output last year has puzzled Fed officials. At last month’s meeting, they discussed reasons that inflation might have been more muted, including the prospect that the estimated level of unemployment rate consistent with stable prices is lower than previously thought.

Instead of wondering why inflation is weak, they ought to consider the absurdity of their models.

Stocks are priced beyond perfection, housing prices are so high no one can afford them, and the entire inflation expectations model they use is ridiculous.”

He is right about the Fed’s models and their reliance on low interest rates. Charlie McElligott discussed the three most important points about low interest rates (h/t Zerohedge)

Low interest rates are (ultimately) deflationary, sustaining zombie-firms in a “liquidity-trap,” which weigh on overall economic performance while also weakening investment.

Low interest rates and QE are deflationary as you incentivize mal-investment and blow perpetual speculative-asset bubbles, which (ultimately) correct and drive deleveraging—thus the ‘balance sheet recession.’

As there is still a lot of debt-related “scar tissue,” you can’t push credit on a string. This then leads to quick “muscle memory” returns to a defensive posture: “If there is no return on capital, capital should not be deployed.”

Here are the most important takeaways from all of this:

Despite an expected uptick in economic growth in Q2, look for weaker economic growth through the end of this year and into 2020.

Employment is set to weaken markedly over the next 12-24 months.

Wage growth gains will also reverse as tightness in the labor force eases.

Inflationary pressures will remain non-existent as debt, disruption, and demographic forces continue to suppress economic growth.

Go back to #1.

This is the cycle we are likely locked into currently and will continue to play out over the next several quarters. The markets are misreading what the Fed is really saying and investors will ultimately pay the price.

via ZeroHedge News http://bit.ly/2v6dyQA Tyler Durden

This is the part in Groundhog Day where Phil Connors kills himself again, and again, and again.

With stocks itching for a new excuse to levitate higher, they got that overnight when a Reuters report on fresh “progress” in the U.S.-China trade talks and renewed “optimism” in a trade deal helped propel world stock markets to a 6-month high on steered investors away from save havens such as the Japanese yen, even as 10Y treasury yields dipped modestly, as the same catalyst that has driven stocks higher on virtually every single day in the past quarter has continued to do so again and again, right out of the cult groundhog movie.

“It seems like bullish sentiment has decent grip for now and everyone is focused on the year to date performance of the equity markets,” said Naeem Aslam, chief market analyst at TF Global Markets (UK) Ltd in London.

Overnight Reuters reported that US negotiators tempered demands that China curb industrial subsidies as a condition for a trade deal after strong resistance from Beijing, marking a retreat on a core U.S. objective for the trade talks. According to the report, in the push to secure a deal in the next month or so, U.S. negotiators have become resigned to securing less than they would like on curbing those subsidies and are focused instead on other areas where they consider demands are more achievable, Reuters sources said. Those include ending forced technology transfers, improving intellectual property protection and widening access to China’s markets, the sources said. China has already given ground on those issues.

“It’s not that there won’t be some language on it, but it is not going to be very detailed or specific,” one source familiar with the talks said in reference to the subsidies issue.

Separately, on Saturday during the latest IMF conclave, Treasury Secretary Steven Mnuchin said the US is “hopefully very close” to final round of China talks; adding that the U.S. is open to facing enforcement penalties which work “in both directions.” all of which helped spawn a fresh sense of optimism that a deal announcement was imminent.

In addition to the new trade optimism, thanks to the pleasant aftertaste from China’s credit flood in March, which exceeded all estimates, concern over global growth has also eased, fueling demand for riskier assets. MSCI’s gauge for equities saw its 100-day moving average rise above the 200-day equivalent as the index rose 12 out of the past 13 days, signaling potential for further gains.

Following a muted Asian session, the European Stoxx 600 Index erased an earlier loss and extended gains to session highs with bank stocks contributing most to the increase. A gauge tracking lenders climbs for a third session as it holds above a barrier it breached last week. The European index advances 0.3% as of 11:30 a.m. in London, reversing a decline of as much as 0.1% earlier. BNP Paribas rose 2.5%, adding the most to the increase by index points. Other banks also stronger: Credit Suisse +2.2%; ING Groep +1.3%, Unicredit +2.2%

S&P500 futures nudged up after spending most of the session in the red, as results from Goldman Sachs and Citigroup loomed. In Asia, equities headed for a fresh six-month high, propelled by markets in Japan and Korea, after the Bank of China released upbeat credit data, although earlier, Chinese stocks closed in the red, fading initial trade-related gains as expectations for rate cuts fizzled following the latest credit deluge.

With Chinese trade and lending data showing signs of improvement for the world’s second-biggest economy, investors are turning to the US earnings season to confirm the resilience of corporate America in the face of numerous challenges to growth. JPMorgan Chase posted strong first-quarter results last week, Goldman and Citi report today and Bank of America is up on Tuesday.

“The environment of easier financial conditions is beginning to have an impact on the broader economy,” Principal Global’s Binay Chandgothia told Bloomberg TV. “If that is the case and growth does pick up, you’ll see an uptick in analyst expectations and earnings as well, which should help continue the rally.”

Bunds, US Treausrys and Gilts were confined to very tight ranges, as BTPs trade in a choppier range with peripheral yield spreads widening to core at the margin. G-10 currencies drift sideways in quiet trade, SEK marginally outperforms peers, CAD and NOK lag on commodities weakness.

In FX, South Korea’s won led an advance among emerging-market currencies, while Turkey’s lira underperformed as the unemployment rate climbed to the highest level in a decade. G-10 currencies drifted sideways in quiet trade, with the SEK marginally outperforming peers, CAD and NOK lag on commodities weakness. The yen dropped toward its 2019 low on Monday and the Swiss franc hit its weakest in nearly a month. The dollar also weakened slightly, allowing the euro to cement gains above $1.13.

In commodities, oil slipped after the longest run of weekly gains in three years as a report showed increased U.S. oil-rig activity. Oil provided big milestones last week, with Brent breaking through the $70 threshold and the U.S. benchmark posting six straight weeks of gains for the first time since early 2016. Brent crude oil futures was last off 23 cents at $71.32 while crude futures, the U.S. benchmark, eased 33 cents to $63.56.

Expected data include Empire State Manufacturing Survey. Schwab, Citigroup and Goldman Sachs are reporting earnings.

Market Snapshot

S&P 500 futures little changed at 2,912.00

STOXX Europe 600 up 0.01% to 387.56

MXAP up 0.6% to 163.25

MXAPJ up 0.1% to 543.51

Nikkei up 1.4% to 22,169.11

Topix up 1.4% to 1,627.93

Hang Seng Index down 0.3% to 29,810.72

Shanghai Composite down 0.3% to 3,177.79

Sensex up 0.3% to 38,897.72

Australia S&P/ASX 200 unchanged at 6,251.44

Kospi up 0.4% to 2,242.88

German 10Y yield rose 0.5 bps to 0.06%

Euro up 0.2% to $1.1319

Italian 10Y yield rose 15.4 bps to 2.171%

Spanish 10Y yield rose 1.5 bps to 1.064%

Brent futures down 0.7% to $71.04/bbl

Gold spot down 0.3% to $1,286.95

U.S. Dollar Index down 0.2% to 96.80

Top Overnight News from Bloomberg

The release of the almost 400-page Special Counsel Robert Mueller report this week could help President Trump put two years of suspicion and risk from the investigation behind him — or ensure that controversy over the Russia probe hangs over his re-election bid.

Trump, renewing his attack on the Federal Reserve, claimed the stock market would be “5000 to 10,000” points higher had it not been for the actions of the U.S. central bank. “Quantitative tightening was a killer, should have done the exact opposite!” he tweeted.

Job vacancies in London’s finance industry have halved in two years as uncertainty over Brexit knocks down business confidence, a survey by recruiter Morgan McKinley has found.

The mass production of iPhones will shift to India this year from China, Foxconn Technology Group Chairman Terry Gou said. The company is the largest assembler of Apple Inc.’s handsets and has long concentrated on China.

Finland looks set to get a more left-leaning government as voters rejected years of austerity in the tightest election in over half a century. Former trade unionist Antti Rinne is poised to become Finland’s first Social Democrat prime minister in 16 years, winning by fewer than 7,000 votes.

Asian equity markets began the week mostly positive as the region took impetus from last Friday’s gains on Wall St. where sentiment was underpinned by a strong start to earnings season and encouraging Chinese data. Nonetheless, ASX 200 (U/C) was dampened amid tentativeness ahead of key earnings and underperformance in gold miners, as well as trade-related news including a further decline of Chinese imports and dispute at the WTO on Australia’s restriction on Chinese 5G technology. The rest of the major Asia-Pac indices are mixed as recent advances in USD/JPY fuelled the upside in Nikkei 225 (+1.4%), while Hang Seng (-0.3%) and Shanghai Comp. (-0.3%) finished lower but were initially boosted as most of the recent Chinese data surpassed estimates including New Yuan Loans, Aggregate Financing, Trade Balance and Exports with the latter at a 5-month high. Furthermore, reports the US softened its demands on China for reducing state industrial subsidies and that both sides have agreed to measures to avoid China currency manipulation, added to the hopes for a looming trade deal. Finally, 10yr JGBs were softer as they tracked the recent losses in T-notes and with demand also dampened by gains in riskier assets as well as a lack of BoJ presence in the market today.

Top Asian News

The $18 Billion Electric-Car Bubble at Risk of Bursting in China

Turkey Bleeds Jobs as Unemployment Climbs to Highest in a Decade

Economist Snatched at Night, Questioned for ‘Insulting’ Erdogan

Jack Ma Again Endorses Extreme Overtime as Furor Rages On

A tepid start to the week for European equities thus far (Eurostoxx 50 Unch) after the optimism seen in Asia somewhat waned, although Japan’s Nikkei 225 closed higher by almost 1.5% amid currency tailwind. In Europe, Italy’s FTSE MIB (+0.5%) bodes well as the bourse hit eight-month highs, bolstered by banking names amidst the optimism surrounding US banks’ earnings (ahead of Goldman Sachs and Citigroup earnings today). As such the banking sector in Europe outperforms (Stoxx 600 Banks +0.9%) whilst its peers remain mixed. In terms of individual movers, France’s Publicis Groupe (+3.2%) leads the gains in the CAC 40 (+0.1%) on the back of an optimistic revenue update, whilst also supporting its UK peer WPP (+1.3%) in tandem. Elsewhere, Covestro (-4.2%) is the marked laggard in the DAX (Unch) amid ex-dividend trade. Finally, IWG (+22.4%) rests at the top of the Stoxx 600 [Unch] after reports that Japan’s TKP are to acquire the Co.’s workspace leading unit for JPY 50bln coupled with a broker upgrade.

Top European News

Trafigura to Take Control of Europe’s Biggest Zinc Smelter

Finns Eject Austerity Government as Leftists Win Election

Draghi Sticks to Cautious Optimism About Euro-Area Bounceback

SNB to Raise Rate at Start of 2020, Same Time as ECB, UBS Says

In FX, the Sterling remains underpinned and relatively optimistic after another Article 50 extension to avoid a no deal Brexit and amidst reports that talks between the Conservative and Labour Parties have been more detailed and constructive than some expected, per UK Foreign Secretary Hunt. Cable is eyeing 1.3100 again, albeit with a hefty helping hand from a broadly soft Dollar, as Eur/Gbp trades largely sideways within a 0.8633-50 range. Technically, 1.3132 (last Friday’s high) forms nearest resistance, but data could become pivotal as the week unfolds given jobs and earnings on tap tomorrow, then CPI on Wednesday and retail sales ahead of the long Easter break.

EUR – As noted above, the single currency is also firm and outperforming the Greenback as the DXY slips a bit further below 97.000 to just under 96.800. Eur/Usd is inching towards 1.1300+ upside chart levels, like a 50% Fib circa 1.1324 and the 200 WMA around 1.1341. Note also, 2 banks are long of the headline pair and looking for sizeable rallies to 1.1650 and even 1.1800.

NZD/AUD/JPY/CHF/CAD – All narrowly mixed vs the Usd with the Kiwi and Aussie both deriving some support from reports overnight suggesting the US has relaxed some demands over Chinese industrial subsidies in ongoing trade negotiations, as Nzd/Usd hovers between 0.6763-82 and Aud/Usd in a 0.7164-80 range. However, Usd/Jpy has not advanced as much as risk-on sentiment might have suggested overnight with the pair fading just shy of the 2019 peak (112.14) amidst supply from Japanese exporters according to market contacts and now revisiting the 200 WMA (111.98). Meanwhile, the Franc is sitting tight within 1.0010-28 parameters and Loonie between 1.3320-47 ahead of the BoC’s Business Outlook Survey and against the backdrop of softer oil prices that are also undermining the NOK (sub-9.6100 vs the Eur as SEK holds above 10.4700).

EM – The Try has been hit hard again and got closer to recent lows vs the Usd in wake of latest Turkish jobs data revealing a spike in the rolling 3 month average unemployment rate to 14.7% vs 13.5% previously. The Lira has nursed some losses since on the aforementioned Buck weakness, but remains on the backfoot in a 5.7600-8115 band in stark contrast to the Rand that has extended gains through 14.0000 even though one institution is anticipating a reversal in the Zar’s fortunes and rebound to 14.2700.

In commodities, there has been subdued trade in the energy complex as WTI (-0.8%) and Brent (-0.8%) futures gave up some of Friday’s gains, with the latter now straddling around the psychological USD 71.00/bbl level. Friday’s CFTC data showed that hedge funds raise bullish ICE WTI crude bets by 30.7k to 281.7k lots, whilst speculators increased net long positions in Brent crude (for a fifth consecutive week) by almost 9.5k to just over 358k in the week to April 9th. Over the weekend, Russia’s Finance Minister stated that OPEC+ could decide to raise production (at the June 25/26 meeting) to fight for market share with the US. Currently OPEC+ have agreed to curb output by 1.2mln BPD until June 2019, with IFX noting that Russia’s April production fell by 150k BPD vs the benchmark October level. Back in December, Russia committed to reducing output by 228k BPD from October levels of 11.4mln BPD in a gradual manner which would take place over several months. Elsewhere, the precious metals sector is mostly in the red with gold (-0.4%) edging lower and breaching its 100 DMA (USD 1288/oz) to the downside as last week’s Chinese data somewhat eases fears of a global growth slowdown. Meanwhile, copper (-0.3%) gave up its overnight gains as the risk sentiment became more cautious during early EU trade. Finally, Shanghai steel futures hit a seven-and-a-half year high as the alloy is supported by firm demand, whilst its base metal, Dalian iron ore futures remained near record highs on dwindling Chinese stockpiles which declined the most since 2015, according to SteelHome data.

US Event Calendar

8:30am: Empire Manufacturing, est. 8, prior 3.7

4pm: Net Long- term TIC Flows, prior $7.2b deficit

4pm: Total Net TIC Flows, prior $143.7b deficit

DB’s Jim Reid concludes the overnight wrap

Right. I’m writing this only an hour or so after the first episode of the final Game Of Thrones season had its global premier and am selectively looking through my normal newsfeeds very nervous that I’m going to see spoilers. So if I’ve missed anything today that’s my excuse. I’m not going to watch it until we move into our new house immediately after Easter so I will unleash my dragons to anyone that tells me what happens. Someone important is bound to have died already so that’s going to be tough to avoid if true!! Rather aptly the most difficult spoiler I’ve ever had to avoid was 30 years ago this week around the Masters. In my Easter school holidays I had a paper round and had to be up at 4.30am. As such I had to go to bed early and video tape my hero Nick Faldo’s attempt at the Masters with the view of watching it when I’d finished. Obviously all the papers had the result on the back page (he won). So I had to deliver them all with my eyes closed. I remember it well and the great difficulty involved. The locals must have thought me very odd. The modern equivalent will be me closing my eyes every time I open the internet for the next 10 days. Staying with the Masters, I did find it emotional to see a remarkable comeback victory for Tiger Woods yesterday. Our careers have moved in parallel. He’s a year younger than me, has had 4 knee surgeries to my 3 and 4 back operations while I’ve had several injections in the spine. The only real difference is 15 major championships. But has he ever won an II analyst award? Anyway, nice to see that 40-somethings still have a place in the world.

It might be Easter holiday from Friday but we should know a bit more about the global economy before we go away. The continuation of our tactically bullish view relies a lot on China data bouncing back and dragging Europe along with it. Well on Wednesday we see the important monthly data dump with the release of March’s industrial production and retail sales data and also Q1 Chinese GDP. March’s data will be especially important in assessing whether the recent tick up in PMIs were a genuine positive signal or not. Last Friday’s bumper credit numbers (more later) reinforces our view that China is going through another mini credit cycle. Indeed our Chinese economists put out a note yesterday ( link here ) suggesting that there is upside to their 2019 forecasts. They’ll update these after Wednesday’s numbers.

The other main highlight will be the flash April PMIs on Thursday, with releases for the Eurozone, Germany, France and the United States. It’ll be particularly interesting to see the manufacturing PMI for the Eurozone, which fell for an eighth consecutive month in March, moving deeper into contractionary territory with a 47.5 reading. The German manufacturing PMI was even more contractionary last month, with a 44.1 reading. If we’re right on China these should be turning up soon.

In a similar vein, Germany’s ZEW survey for April comes out on Tuesday, which is an important number in light of the above. In March, the ZEW survey of current activity fell to 11.1, its lowest level since December 2014, although the expectation reading rose to -3.6, which was its highest since March 2018, so it’ll be worth looking to see if there are any signs of improvements here.

The main other highlights are US Retail Sales (Thursday) and Q1 US earnings season picking up through the week. Retail Sales will be looked at for signs the consumption soft patch either side of the turn of the year is behind us. In terms of earnings today we’ll see Goldman Sachs and Citigroup reporting. Tomorrow there’ll be earning releases from Bank of America, Netflix, IBM and Johnson & Johnson. On Wednesday, there’ll be Morgan Stanley and PepsiCo, and on Thursday, there’ll be Philip Morris International and American Express. The day by day week ahead is at the end.

Over the weekend, the US President Trump renewed his criticism of the Fed by tweeting, “If the Fed had done its job properly, which it has not, the Stock Market would have been up 5000 to 10,000 additional points.” I can only assume he means the Dow rather than the S&P 500! He further added, “Quantitative tightening was a killer, should have done the exact opposite!” President Trump’s comments came after the IMF conference in Washington where ECB President Draghi said that he was “certainly worried about central bank independence” and especially “in the most important jurisdiction in the world.” Elsewhere, at the same IMF conference Germany came under pressure from global policy makers to ease fiscal policy.

Meanwhile, on US/China trade talks, Treasury Secretary Steven Mnuchin said that the US and China are discussing whether to hold more in-person meetings after talks in recent weeks while adding that “we’re hopefully getting very close to the final round of these issues.” He also said on the enforcement mechanism that, “I would expect that the enforcement mechanism works in both directions, that we expect to honor our commitments, and if we don’t, there should be certain repercussions, and the same way in the other direction.”

Asian markets have started the week on a positive note with the Nikkei (+1.47%), Hang Seng (+0.58%), Shanghai Comp (+1.12%) and Kospi (+0.49%) all up. Elsewhere, futures on the S&P 500 are trading flattish (-0.04%).

In other news, Finland will likely get a more left-leaning government after voters, in the tightest election in memory, rejected years of austerity and seemingly demanded more spending on welfare. Former trade unionist Antti Rinne is poised to become Finland’s first Social Democrat prime minister in 16 years after winning by fewer than 7,000 votes but his party faces tough coalition talks ahead as the ultra nationalist Finns Party emerged as the second-biggest party, beating the establishment conservative National Coalition for the first time.

On Brexit, David Lidington, PM May’s de facto deputy, said on Sunday that the government believed it would be possible to get “the benefits of a customs union” – which Labour wants – “but still have a flexibility for the U.K. to pursue an independent trade policy on top of that.” He added that even though parliament is in recess until April 23, negotiations will continue. Sterling is up +0.18% this morning.

Recapping last Friday and the week overall now. Equity markets advanced on Friday with the S&P 500 +0.66% (+0.51% for the week), the NASDAQ +0.46% (+0.57%) and the STOXX 600 +0.16% (-0.18%). This was the third consecutive weekly gain for the S&P 500, which closed at its highest level for six months. Financials led the advance following strong earnings from JPMorgan, which reported net income of $9.2bn in the first quarter, sending its shares up +4.69% on Friday. They also reported net interest income of $14.6bn in the first quarter, up 8% on the same quarter a year ago, while return on common equity reached 16%. Impressive numbers. The STOXX Banks index ended the day +2.78% (+3.05% – week) to reach its highest level since October (also helped by the China data and rising bund yields). The S&P 500 Banks index was also up +2.40% (+2.39%).

The market was also supported by stronger-than-expected data releases. Firstly, we had the credit numbers out of China where new total social financing came in at RMB2.86tr, much stronger than the market consensus forecast of RMB1.85tr. New bank loans also surprised on the upside at RMB1.69tr compared with consensus of RMB1.25tr. M2 (broad money) growth rebounded to 8.6% in March from 8.0% in Feb but the most significant part, according to our economists, was the rebound in M1, whose growth rate jumped to 4.6% in March, up more than 4ppts from its trough at 0.4% in Jan. Again see their report mentioned earlier for more.

The Chinese trade data was also positive, with the March trade balance coming in at $32.65bn (vs. $5.70bn expected) indicating that exports had recovered. In Europe, the Eurozone industrial production figures fell by -0.2% mom in February but above the -0.5% decline expected, while January’s figure was revised up to 1.9% mom (from 1.4% previously). However, in the US the University of Michigan consumer sentiment index fell more than expected, coming in at 96.9 (vs. 98.2 expected).

Government bond yields rose as the global data was generally pretty positive, with ten-year bund yields +6.4bps on Friday (+4.9bps on the week) to return to positive territory (0.054%). 10yr Treasury yields rose +6.8bps on Friday (+7.0bps – week), and the US 2s10s curve steepened to end the day +2.9bps (+1.8bps). Bond yields in the European periphery came off their recent lows with the rise in yields but spreads edged tighter. In Greece though, ten-year yields fell to their lowest level since September 2005.

via ZeroHedge News http://bit.ly/2KAOZph Tyler Durden

Ironically, while Europe has led the US in holding Silicon Valley tech firms accountable for anti-trust and data privacy violations, the shoe has been on the other foot when it comes to Diesel-gate – revelations that German automaker Volkswagen installed defeat devices in its diesel cars to help them cheat American emissions inspections.

After the US charged former Volkswagen CEO Martin Winterkorn with fraud, conspiracy and violations of the Clean Air Act last spring, Braunschweig public prosecutors revealed Monday that they were charging Winterkorn and four other executives with serious fraud and violations of competition law, BBG reported.

VW has had to recall hundreds of thousands of cars around the world since the company admitted in 2015 that it installed the illegal software in its diesel engines to cheat anti-emissions tests.

via ZeroHedge News http://bit.ly/2UfDEe9 Tyler Durden

In the latest indication of how the financial burden of the 737 MAX’s troubles will ultimately be borne by Boeing’s airline customers, American Airlines announced on Sunday that it would cancel all flights with Boeing 737 MAX 8 planes through Aug. 19, the longest stretch of cancellations announced by a US airline since regulators around the world grounded the planes following the March 10 crash of ET302. The cancellations will amount to 115 flights per day – about 1.5% of American’s total during each day of the summer travel season.

The airline had previously cancelled flights through early June. AA’s decision to extend cancellations follows United’s decision to cancel all MAX flights through June 5, and Southwest canceled them through Aug. 5. The cancellations are expected to severely hamper travel during the busy summer season, when families typically take vacations.

Read the full statement from American’s Chairman and CEO Doug Parker and President Robert Isom:

Dear fellow team members,

As we prepare for summer, our focus is around planning for the busiest travel period of the year. Families everywhere are counting on American Airlines for their summer vacations, family reunions, trips to visit friends and adventures overseas. Our commitment to each other and to our customers is to operate the safest and most reliable operation in our history.

To further that mission, we have made the decision to extend our cancellations for the Boeing 737 MAX aircraft through Aug. 19. Based upon our ongoing work with the Federal Aviation Administration (FAA) and Boeing, we are highly confident that the MAX will be recertified prior to this time.But by extending our cancellations through the summer, we can plan more reliably for the peak travel season and provide confidence to our customers and team members when it comes to their travel plans. Once the MAX is recertified, we anticipate bringing our MAX aircraft back on line as spares to supplement our operation as needed during the summer.

The planning team is working on this action now and in total, approximately 115 flights per day will be canceled through Aug. 19. These 115 flights represent approximately 1.5 percent of American’s total flying each day this summer.

We remain confident that the impending software updates, along with the new training elements Boeing is developing for the MAX, will lead to recertification of the aircraft soon. We have been in continuous contact with the FAA, Department of Transportation (DOT), National Transportation Safety Board (NTSB), other regulatory authorities and are pleased with the progress so far.

Our Reservations and Sales teams will continue to work closely with customers to manage their travel plans, and we appreciate their outstanding efforts to care for our customers. Your professionalism and care for customers is second to none, and we thank you for all you do every day for our customers and for each other.

AA said customers would have the option of rebooking their flights or receiving a refund. The airline said it might try to find other planes to fill in for 737 MAXs on certain scheduled flghts.

The FAA is still investigating the two deadly crashes, and it recently met with representatives from American, Southwest, United and their pilot unions to discuss the plane’s safety questions. Boeing said last week that it had completed 96 test flights of the 737 MAX with its software update.

Stiil, even after Boeing has managed to convince regulators that its planes are safe, there’s still the open question of whether the public will feel comfortable flying on the planes. It’s unclear how the company plans to deal with this problem, but President Trump on Monday morning tweeted one idea.

Conceding “what the hell do I know” about branding (despite previously running an airline and, of course, going from presidential long shot to clinch a historic, come-from-behind victory in the 2016 election), Trump said if it were up to him he would “rebrand” the Boeing 737 MAX 8 and “add some great features” to win back the public trust.

“No product has suffered like this one.”

What do I know about branding, maybe nothing (but I did become President!), but if I were Boeing, I would FIX the Boeing 737 MAX, add some additional great features, & REBRAND the plane with a new name.

No product has suffered like this one. But again, what the hell do I know?

Even those who have never played as stroke of golf probably understand that Tiger Woods’ historic Masters’ win on Sunday was a big moment – not just for a professional athlete who triumphed over a decade of scandal and adversity, but for America, a country that was built on the kind of grit and dedication displayed by Woods while capturing his fifth Masters’ title, his first in more than a decade. At 43, he became the second-oldest person to win the tournament after Jack Nicklaus, who won the tournament in 1986 at age 46.

Unfortunately, some couldn’t share in the excitement.

While Tiger’s victory was a huge moment for fans, for sportsbooks in New Jersey and Nevada, the losses generated by Woods’ come-from-behind win amounted to seven figures. Sports super-book FanDuel Group said it lost $2 million on the victory.

Another book, the Westgate Las Vegas SuperBook, lost nearly $100,000, its worst-ever showing for the Masters. A trader at William Hill US said the company’s book lost “seven figures,” according to Bloomberg.

“It’s great to see Tiger back,” said Nick Bogdanovich, director of trading at William Hill U.S. “It’s a painful day for William Hill – our biggest golf loss ever – but a great day for golf.”

However, Sunday’s losses won’t even begin to counterbalance the profits amassed during Woods’s decade in the doghouse, where he remained a favorite of the betting public despite repeatedly disappointing on the course. It wasn’t uncommon for Woods to be the betting favorite, despite the long odds.

“We are still doing well overall with wagers involving Tiger,” Jeff Sherman, vice president of risk at Westgate SuperBook, said in an email.

That dynamic played out again on Sunday, when 21% of bets on FanDuel’s platform were for Woods to win it all, a total that led to a net loss of $1 million. On top of that, the company ran a promotion where it promised to refund all bets if Woods won the tournament. That cost it another $1 million.

At William Hill, a Nevada resident placed a $85,000 bet on Woods to win it all paid out $1.2 million on 14-to-1 odds, the largest single-ticket payout in the casino’s history, according to CBS News.

The bet was so large that William Hill’s staff had to reach out to the bettor to verify the ticket, and that the bettor wasn’t off by a digit or two.

The wager was so large that it single-handedly pushed Woods to 10-to-1 odds at William Hill.

Not all sports books reported losses on Tiger’s win, with at least one telling BBG that it broke even.

Not all sports books took a loss. MGM Resorts Internationalbroke even on the event, according to Jay Rood, its vice president of race and sports. MGM had its biggest handle ever for a golf tournament.

“We were a small loser to Tiger before the start but were able to fade it over the course of the tournament,” Rood said.

Tiger’s win forced sports betting organizations to reevaluate odds related to his career. FanDuel is now giving him 5-to-1 odds of tying Jack Nicklaus’s record of 18 major tournament wins.

via ZeroHedge News http://bit.ly/2DdLX4v Tyler Durden

That will be a tall wall to climb, with Chinese, Korean, and Japanese firms dominating the space so far.

In November, the German government announced a €1 billion ($1.12 billion) fund for German companies to develop and build battery cells. It’s part of the country’s “National Industrial Strategy 2030,” unveiled in February, which voices concern that Asian battery makers will dominate electric vehicles and autonomous driving of the future.

Companies were assigned to express interest in tapping into the battery research and development fund by mid-March. They have until April 21 to submit their applications, and so far, about 30 projects have been submitted. Applicants include automakers, parts suppliers, and chemical companies

Chinese firms dominate the market for now, led by Contemporary Amperex Technology Co. Limited (CATL) and Build Your Dreams (BYD), whose rise was fostered by state subsidies for Chinese electric carmakers. China is expected to control 70% of the market in the next two years.

Japanese conglomerate Panasonic has held its own share of the market, with Tesla and Toyota as clients. Korean firms LG Chem and Samsung SDI also play a leading role in the EV battery market.

One German critic thinks that the government R&D fund is in the wrong place with its focus on battery cells and its manufacturing process. He thinks the money should be going to the main battery components: cathodes and anodes.

“The production value of the cell is about 15%. Sixty percent is just in the materials of cathode, and another 20% is the materials of anodes,” said Ferdinand Dudenhöffer, professor of automotive economics at the University of Duisberg-Essen and a veteran of automakers such as Opel and Porsche.

“The value does not exist in the manufacturing process in which they want to spend €1 billion ($1.13 billion). The value is in the materials.”

“It’s stupid,” he said. “It’s crazy, what our ministry of economics is doing.”

Germany’s BASF, one of the world’s largest chemical companies, might agree with that statement. The company is building a cathode materials factory in Finland, in cooperation with Russian miner Nornickel.

The German supplier does agree with the purpose of the government’s program. A BASF company spokesperson said that it has much to do with supporting large-scale production back home in Europe, rather than having to be dependent on imported cell supplies.

German automakers have been exploring the question of whether or not to manufacture their own EV batteries for years. Along with being Tesla-competitive, Volkswagen, Daimler, and BMW have made major commitments to bringing EVs to market and have explored the possibility of building their own battery packs.

German auto parts giant Bosch had explored entering the market. After determining building a battery plant would cost about €20 billion ($22.6 billion), the German conglomerate dropped the plan last year, saying that the risk was too high for the size of the needed investment.

China’s BYD would like to solve one of the chief problems around keeping its dominant role in electric car sales and battery packs — tapping into enough nickel metal. Securing enough nickel is a major worry for EV makers, a BYD executive said earlier this month. The company would welcome joint ventures that help guarantee supply.

China has benefitted greatly from controlling about half of the world’s lithium production. But nickel has been just as important as lithium, maybe even more so. Nickel sulfate powder is a critical ingredient in the cathode formulation for lithium-ion batteries. Analysts expect to see a boom in demand as EV sales continue to increase.

“The supply of nickel going forward is a big concern in everybody’s mind,” said Coco Liu, procurement director at BYD.

Analysts have warned that the market would be short of nickel if Chinese-led projects in Indonesia fail to deliver.

BYD says the JV would present a rich opportunity for a partner companies in supplying the whole EV value chain — from upstream mining to battery materials and finished products.

Joint ventures are “a good way to go forward” and can save costs, Liu said.

Some companies would disagree with the JV proposal, and see it as a way for China to maintain control over its manufacturing sector.

The Chinese government is starting to loosen up on those rigid constraints with electric carmaker Tesla recently winning the first rights to establish its own plant. That “gigafactory” is coming together in Shanghai, one of China’s available free-trade zones announced last year.

via ZeroHedge News http://bit.ly/2UlB3iV Tyler Durden