Whichever aggrieved Phoenixus board member leaked a story about Martin Shkreli running the pharma company from prison using a contraband cellphone has probably achieved their goal: After a year in New Jersey’s Fort Dix prison, Shkreli has been thrown into solitary confinement, rendering him incommunicado.

Though the Bureau of Prisons wouldn’t comment on Shkreli’s accommodations, a member of the Hacker crew Crackas with Attitude, who told Forbes he had befriended the one-time “most hated man in America” and “pharma bro”, Shkreli is currently in the “Special Housing Unit”, or “SHU”. The BOP did say, however, that “when there are allegations of misconduct, they are thoroughly investigated.” Of course, anybody who read the WSJ’s story about Shkreli’s big comeback plans – he’s hoping to build Phoenixus, essentially his old Turing Pharmaceuticals run under a different name – probably sensed that it would bring unwanted heat down on Shkreli, who was sentenced to seven years for allegedly defrauding investors (though, as his defense repeatedly pointed out during his trial, none of them actually lost any money).

It appears Shkreli has been in the SHU since the article was published on March 7. His lawyer, Ben Brafman, declined to comment to Forbes.

One source close to Shkreli’s legal team said the fraudster was in the special housing unit (SHU) a week and a half after the article was published on March 7, but the source had not received an update on his status. But according to Justin Liverman, a fellow inmate and ex-member of notorious hacker crew Crackas With Attitude, Shkreli was indeed put in solitary and was still there as of Sunday. “Martin is in the SHU,” Liverman told Forbes.

According to Justin Liverman, the hacker mentioned above, Fort Dix is “cellphone heaven” – that is, theere are hundreds of contraband phones floating around the prison, and inmates can rent time from holders or even buy one for $1,000. One inmate was sentenced to another 30 years after masterminding the murder of his ex-girlfriend’s new boyfriend from behind bars. Another group was busted using the phones to share child pornography.

Using a cellphone behind the vast redbrick walls of Fort Dix is against the rules, but Liverman claims it isn’t difficult to obtain one. Fort Dix is like a “cellphone heaven…. There are hundreds of phones on this compound. You can either rent phone time or buy one for $1,000,” says Liverman, who was given a five-year sentence for his involvement in the hacker crew Crackas With Attitude. In the outfit’s most notorious attack, they broke into the AOL account of then-CIA director John Brennan and shared emails and files with Wikileaks.

Fort Dix has had problems with contraband phones before. In the past year, guards caught inmates sharing child pornography using smuggled devices. In another incident in 2018, prisoner Omar Adonis Guzman-Martine was sentenced to an additional 30 years for using a cellphone to organize an attack on his girlfriend and murder her boyfriend.

By the sound of it, at least when Shkreli has been returned to genpop, he won’t have much trouble getting his business back up and running…if the company’s board hasn’t wrested control of Phoenixus in the mean time.

via ZeroHedge News https://ift.tt/2UlPAiz Tyler Durden

LYFT shares are now down over 26% from their opening highs, having crashed well below their $72 IPO price as investors scramble to take profits (or reduce losses) on the cash-burning ride-share venture.

There is one little problem though – the shorts haven’t even started yet…

As Bloomberg reports, Ihor Dusaniwsky, managing director of predictive analytics at S3 Partners, blamed the drop on shareholders exiting the stock, rather than short sellers, because IPO shares aren’t finalized yet and therefore not in lending programs.

“It’s going to be interesting because you’ll have long holders that are already on the fence,” he said in an interview.

“If the shorts come in, they are going to push the longs out.”

“There’s going to be a ton of demand and not a lot of supply,” said Dusaniwsky, who expects the imbalance to result in borrow fees exceeding 10 percent, a level he called “very expensive.”

Short interest should steadily increase as more and more shares become available, and early indicators are pointing to strong demand from short sellers.

via ZeroHedge News https://ift.tt/2HUgDeO Tyler Durden

In the news this morning we’ve got a raft of stories to wake up and think about. Yesterday’s hotly anticipated US and China data was benign and won’t roil markets. Rolls Royce engines on B-787 Dreamliners are still not functioning properly – 2 have been grounded suffering from “premature blade deterioration”. Its bad news for operators as further checks are mandated. Lyft’s successful IPO soared from $72 to $88.60, but this morning its tumbled to $65 – what does that tell us about valuations? (And, let’s not mention the lack of earnings or its massive borrowings because these don’t matter: companies not making any money don’t pay taxes… and that’s a good thing?)

I was a bit disappointed by my failure to catch many readers with yesterday’s April Fool’s story. My imaginary tale of an IDIET Withholding Tax on German Securities to drive European growth only netted a solitary chap working for a German fund who asked if this meant assets would be transferred back to London. Nope.. I made it all up.

Most readers spotted the obvious clues like the imposition date of June 31st. A couple got it on Shane Longman – the fictional brokerage from the 1980s series Capital City. No one seemed to get Autoclytus Strada; a reference to the first ever Eurobond launched by Autostrada in 1963 following the imposition of the US interest equalisation tax which triggered the offshore dollar market – the Euromarket, which is why we are all here today. I remember it well… (And incidentally; Autoclytus, the grandfather of the wily Odysseus and the King of Thieves, sums up the way the Euromarkets used to behave when it was all still fun!)

However, many readers did comment the idea of directing savings and consumption from Germany into the rest of Europe is the key to restoring normal growth across the EU… and reckoned my imaginary IDIET tax was a way to kick start it. It’s a ridiculous notion that Germany would ever support anything that reeked of German savers and taxpayers paying for the rest of Europe. And that’s the problem.

This years April 1 joke was based on the core problem at the centre of the Euro zone: how to make 19 imbalanced economies function under the same currency. Thus far, the Euro has produced one winner (Germany) and 18 losers. The result is imbalance and one-way target 2 distortions because one economy is so strong. For the single currency to work, the Euro requires not only closer fiscal homogeneity from economies closely aligned with each other – spawning the need for closer union across taxation, banking and business, but ultimately closer political union. It’s just not happening. In fact, its reversing and we’re likely to see that proved in the May EU elections.

The likely failure of Europe diverse states to achieve a stable sustainable currency through union is a risk. It appears political union in Europe isn’t working – witness populism, the breakdown of banking union initiativess, ets. While the Euro shows extraordinary resilience, maybe its best the UK stays out the way and lets Europe try to solve its problems without our tedious interference and lack of commitment to the Brussels project?

Time to buy Sterling?

I’m a bit surprised by a Bloomberg report that Goldman’s head of FX and EM says: “We’re coming to a big finish here” on Brexit. The chap, Zach Pandl, says “we think we’re making progress despite these failed votes”. He might be right. Much as I hate to agree with the Vampyre Squid (Goldman for younger readers), Pandl’s comments do make a curious kind of sense. The sense of profound despair across Parliament – with MPs resigning and the country generally losing the will to continue makes it increasingly likely there will be a final scrabble to secure a deal, any deal!, before the final deadline.

It’s likely that any last minute compromise will be a soft-Brexit. It’s likely to lesser deal than what May was proposing. Personally, I see little point in exiting if its only a half exit. We may as well stay in and continue to fight from within for reform, the scaling back of the Euro-proto-state, the undoing of further banking and political union, and focus on trade with our partners. It would not be an ideal outcome.. but we could live with it.

If Europe doesn’t reform, we can still walk out down the line – this time with a plan and firm leadership. Stepping back from Brexit now will be embarrassing, will trigger unrest and cause a wave of ennui to envelop and hold back the economy as our spirits are dampened. I would have been happy with the May deal – taking the view we’d quietly undo the backstop and get on with “stuff”.

Although I do support exit, what we’re seeing in the UK is extraordinary and deeply disconcerting. 10 days to go till the second deadline and there is still nothing even approaching an agreement. Cabinet will meet, pontificate, argue, posture and preen later today. All the while, the Right-Wing ERG group will try to play down the clock to a no-deal Brexit.

We are all aware it’s been a thoroughly botched process which boils down to leadership failure, careerists willing to exploit weakness as opportunity, and ignorance. There has been failure from the top down; the absence of any plan, leadership, political skills, or understanding of the political processes required from the top down has been extraordinary. Parliamentary disciple has broken down across the board.

Perhaps the only functional team are the Hard Brexit ERG – because they had a plan. Even though their represent a tiny minority in Parliament and in their own party, they have successfully exploited May’s parliamentary minority to break her. Had May retained a majority of 30 votes going into Brexit, we’d still be regarding Jacob Rees Mogg as a rather quaint and irrelevant pedant with a fondness for the detail in legal documents, Latin and the 18th Century. Today? He might be on the cusp of leading a successful parliamentary coup.

via ZeroHedge News https://ift.tt/2FMsVCt Tyler Durden

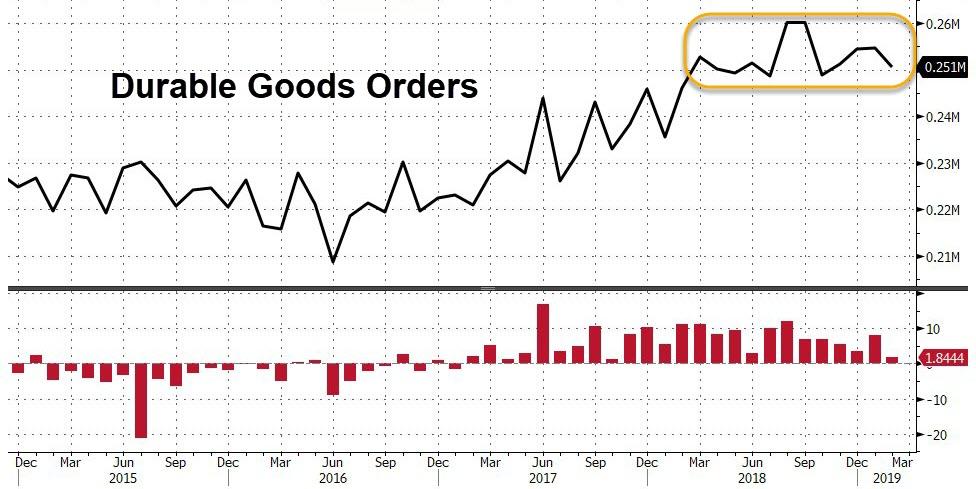

After a modest rebound from October’s collapse, Durable Goods Orders were expected to slide lower once again in February but the drop (down 1.6% MoM) was slightly better than expected (down 1.8% MoM).

Additionally, January’s data was revised lower (from +0.3% to +0.1%).

On a year-over-year basis, durable goods headline data rose at only 1.844% – the weakest since Oct 2017.

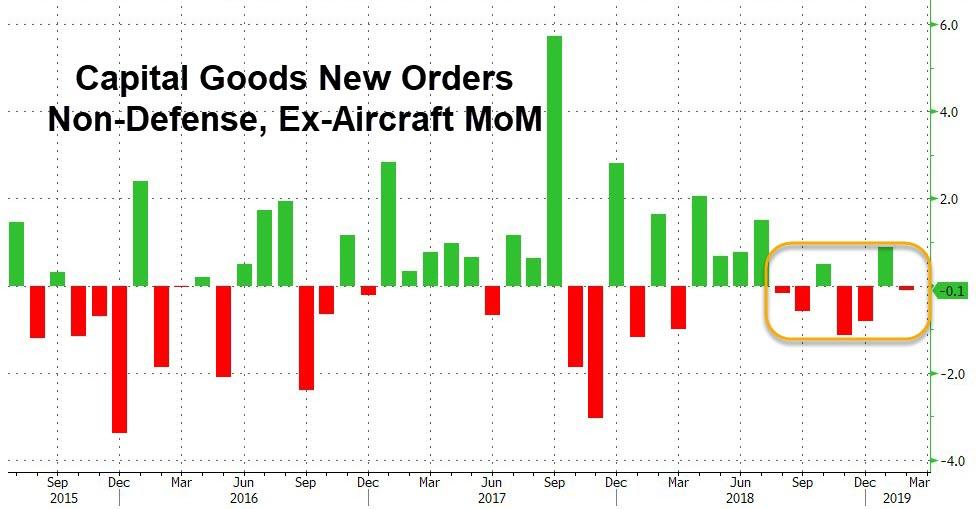

Capital Spending proxy (Cap Goods Non-Defense, Ex-Air) slipped 0.1% (worse than expected) for the third time in four months, suggesting corporate investment remains subdued amid a slowing global economy and uncertainty over the trade war with China.

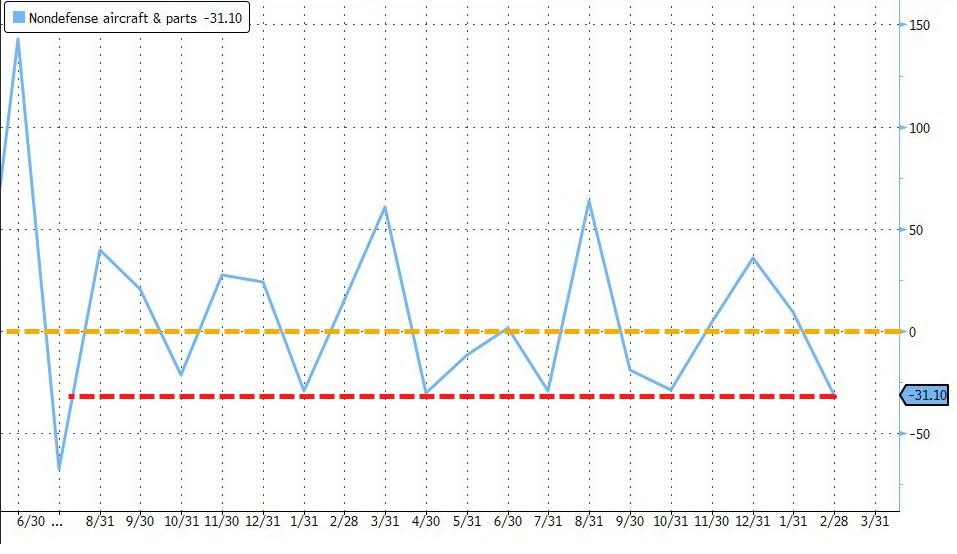

Critically, non-defense aircraft and new parts orders plunged 31.1% MoM – and this is before Boeing’s impact.

Categories posting gains in orders included electrical equipment, primary metals and fabricated metal products.

Sectors with declines included motor vehicles and parts, computers and electronic products and machinery.

via ZeroHedge News https://ift.tt/2FR3MrD Tyler Durden

As investors await the findings from Ethiopian Airlines’ preliminary report, another concerning headline about a different class of Boeing jets has hit the tape.

Singapore Airlines has grounded two Boeing 787-10s – better known as the “Dreamliner” – after discovering “premature blade deterioration” on their engines, which were manufactured by Rolls-Royce Co. The airline discovered the deterioration during routine inspections, and has been working with the manufacturer to get a handle on what appears to be a widening problem for the Rolls-Royce Turbines.

After the discovery, Singapore Airlines inspected all of the jets equipped with the Rolls Trent 1000 TEN engines, and is currently inspecting planes employed in its Scoot Airline. But this is just the latest hiccup for the Rolls engines, which is one of two models used in that class of Boeing jets.

The airline said it is “working closely” with Rolls-Royce to rectify the issue.

“During recent routine inspections of Rolls-Royce Trent 1000 TEN engines on Singapore Airlines’ Boeing 787-10 fleet, premature blade deterioration was found on some engines,” Singapore Airlines says in a statement.

“SIA is working closely with Rolls-Royce and the relevant authorities for any additional follow-up actions and precautionary measures that may be required going forward.”

Rolls has reportedly determined that 8% of its global Dreamliner fleet has been impacted by the premature blade deterioration. The problem will likely eat into Rolls’ share of the Dreamliner engine business, for which it competes with rival GE, which produces its own turbine.

A discovery of faster-than-expected blade deterioration affected about 120 Trent 1000 turbines, or about 8 percent of the global fleet, a person familiar with the matter said in September. That was a further setback to Rolls-Royce’s efforts to reduce the number of idled planes after flaws in the engine design led the company to record more than $1 billion in charges.

Design glitches have plagued the Trent program for two years and eaten into Rolls-Royce’s share of engines for 787 jets, known as Dreamliners, against rival General Electric Co. The intermediate pressure turbine blades – which had already been flagged for replacement – aren’t lasting long enough to meet the previously set maintenance schedule.

In other news, more than 300 Boeing 737s remain grounded as the company has delayed submitted a revised version of an anti-stall software to the FAA. But while Boeing shares were down only marginally on Tuesday, Rolls-Royce shares dropped nearly 3%.

via ZeroHedge News https://ift.tt/2JXCow5 Tyler Durden

After months of trying, a cross-party group of backbenchers finally succeeded late last month in wresting control of the Commons agenda from the government in an unprecedented move. But in an indication of just how dysfunctional the Brexit process has become, the group’s hopes for formulating a consensus around an alternative to Theresa May’s now thrice-rejected withdrawal agreement have been dashed, as the Commons has rejected every alternative proposal raised during two separate indicative votes over the past week.

Now, with Speaker Bercow reportedly contemplating stopping May from bringing her deal back for a fourth vote, and different factions in the Commons demanding the prime minister push for a “managed” no deal exit (a possibility that the EU has already rejected) while another pushes May to ask for a lengthy Article 50 extension, and EU chief negotiator Michel Barnier warning that a no-deal exit for Britain is looking “more likely by the day” and that extending Article 50 would pose “significant risks.”

Another group of Brexiteer cabinet ministers is reportedly urging May to issue a “final ultimatum” for the EU to change the Irish Backstop, while Chancellor of the Exchequer Philip Hammond is reportedly planning to admonish the Commons for failing to deliver Brexit, and urge them to now consider calling another referendum.

Sir Oliver Letwin

Amid the chaos, Sir Oliver Letwin, the leader of the backbenchers group, told Sky News on Tuesday that he has no plans to call for another indicative vote on Wednesday, though his group will once again control the agenda thanks to a business motion passed yesterday. Furthermore, in perhaps the clearest sign that Letwin, the would-be Brexit savior, has thrown in the towel, he reportedly said he’s now “90% sure we’ll drop out with No Deal.” His ally Nick Boles, who sponsored a proposal in Monday’s indicative vote that would have called for a softer Brexit, resigned the Tory whip and left the conservative party last night after blaming the party for failing to get its shit together.

NEW: Told Letwin et al have no plans for Indicative Votes on Weds. Instead trying to pave way for Cooper bill to be laid on Thurs to legislate against No Deal & mandate govt to put forward proposal. But mood grim. MP tells me Letwin is now “90% sure we’ll drop out with No Deal”

Meanwhile, No. 10 officials reportedly told the cabinet during a five-hour marathon meeting on Tuesday that if the Commons doesn’t pass May’s withdrawal agreement on the fourth attempt, that the most likely alternative would be a lengthy extension of Brexit. Though it’s unclear how they arrived at this conclusion, considering the EU has said it probably won’t approve another extension.

Brexit latest:

In a meeting before political cabinet, No.10 officials briefed senior ministers that a long extension to Brexit would be the most likely outcome if the withdrawal agreement doesn’t pass Commons on a fourth attempt.

There was no date mentioned in this pre-political cabinet meeting, although ministers think the end of the year is most likely. During the briefing there was no explicit suggestion May would remain prime minister during this period.

I understand that May will tell political cabinet if it is a choice between revocation of Article 50 and pursuing a no-deal Brexit, she would opt for no-deal.

Political cabinet is discussing how to try and get the Brexit deal through the Commons. One option to be discussed is whether it could get through with Labour votes if a confirmatory referendum was tacked on. Surprisingly little hope of getting of the DUP back on board.

A general election is on the agenda but the Tory party’s precarious state has made it difficult to contemplate. Hearing party chief executive Sir Mick Davis might address ministers about this, as per my FT story last week.https://t.co/U1RGXDBMBI

The original plan for today was to hold political cabinet this morning, then regular Cabinet in the afternoon. But sources think No.10 was concerned ministers might meet to plot and brief in the lunch break. Hence why they were shortened and brought together.

As the Commons splinters into competing factions, another group of cross-party MPs is preparing to put forward a bill that would try to definitively rule out ‘No Deal’…though it’s not exactly clear how this would work (remember, MPs have already ruled it out in a non-binding vote). For now at least, the pound has erased its gains from overnight on the latest batch of disheartening Brexit news…though if ‘No Deal’ is confirmed during an emergency EU summit later this month, analysts see more downside ahead.

via ZeroHedge News https://ift.tt/2Uc3Jj1 Tyler Durden

The global stock rally fizzled overnight following a blockbuster start to the week and quarter, with U.S. equity futures unchanged near the highest level of 2019, even as European shares edged up following a muted Asian session while bond yields resumed their ominous slide; the dollar rose to a fresh 3 week high and the pound weakened after Britain’s parliament once again failed to reach a consensus on Brexit.

Following some brightening of the global industrial mood – at least in China and the United States – was competing for attention with another dismal U.S. retail sales report, Britain’s broken Brexit plans and more central bank caution, this time from Australia. Even as positive sentiment in Q1 spilled over into the second, a myriad of risks remain, including Europe’s slowing growth, Britain’s difficult split with the European Union and the lingering trade war. U.S.-China talks are set to resume when Vice Premier Liu He leads a delegation to Washington later this week.

US equity futures were all little changed ahead of the New York open even as European stocks hit 2-week highs with the Stoxx Europe 600 rising 0.3%, led by autos which extended Monday’s sharp rally. The banking sector index rose +0.6% as Swedbank rose the most in more than 5 years after last-week’s slump. Defensive sectors including telecoms and health care underperform. Britain’s exporter-heavy FTSE 100, which climbed as much as 0.5 percent as exporters cheered the fourth fall in sterling in the last five days.

And speaking of sterling, the Brexit tragedy continues as Britain is no nearer to resolving the chaos surrounding its exit from the EU bloc after parliament failed on Monday to find a majority of its own for any alternative to Prime Minister Theresa May’s divorce deal. May is due to hold hours of cabinet meetings with senior ministers on Tuesday to plan the government’s next moves. It meant investors stuck with UK Gilts and safe-haven German bonds, negative yields notwithstanding, in the bond markets despite a pop back higher in key U.S. yields in recent days.

“It does seem that British MPs want to avoid a no-deal Brexit by all means, but they are not voting for any of the alternatives and time is running out,” DZ Bank strategist Daniel Lenz said. “So I think investors have to prepare for the possibility that no-deal Brexit is on its way in 10 days’ time; it’s a little bit affecting yields this morning.”

Earlier, Asian stocks finished unchanged after Japanese shares reversed modest gains to finish lower, while stocks in Shanghai and Seoul rose fractionally. The MSCI Asia Pacific index ex Japan closed 0.2% higher and at a seven-month high after also rallying more than one percent in the previous session and a jump from Wall Street overnight. Chinese stocks hit a 10-month high leapfrogging Colombia to the top of the leaderboard of world share markets, while Australian shares gained 0.4 after the Aussie dollar had dropped following a meeting of the country’s central bank.

On Tuesday, the RBA held interest rates steady and again highlighted the strength of employment, showing no immediate inclination to echo the outright dovish tone of some of its global peers. Nevertheless as Reuters notes, it highlighted “downside risks for the global growth environment” and with national elections coming markets were betting the RBA will ultimately be forced to ease its rates, if only to stop the Aussie dollar from rising.

The market was “front-running” the Federal Reserve’s patience, Vishnu Varathan, head of economics and strategy at Mizuho Bank, said on Bloomberg TV. “At the margin it does provide relief,” he said. “But a lot of this is baked in and we are really running on fumes beyond this.”

And with markets “running on fumes”, attention drifted back to the bond complex, where the yield on 10-year Treasuries declined three basis points to 2.47 percent after surging on Monday and disinverting the 3 Month/10 Year curve, if only for the time being.

Germany’s 10-year yield decreased one basis point to -0.03 percent. Britain’s 10-year yield declined three basis points to 1.017 percent, the biggest fall in more than a week. The spread of Italy’s 10-year bonds over Germany’s increased two basis points to 2.5547 percentage points.

In the latest Brexit news, UK Parliament rejected all 4 Brexit options in indicative votes as MPs voted 273 For vs. 276 Against Motion (C) on Customs Union and voted 261 For vs. 282 Against Motion (D) for a Common Market 2.0, while MPs voted 280 For vs. 292 Against Motion (E) which called for a Confirmatory Public Vote and 191 For vs. 292 Against Motion (G) on Parliamentary supremacy. Following the rejection of all four options, Conservative Remainer MP Boles (one of the architects of the indicative vote plan) left the party stating “I accept I have failed. I have failed chiefly because my party refuses to compromise”.

As a result, as we reported overnight, Chancellor Hammond will tell the Cabinet on Tuesday that Tories may have to consider a referendum as neither party nor country can afford an election, according to Times political editor. Prior to the Cabinet Meeting reports indicated that it has been delayed and shortened, ministers are now going in at 09:30BST-11:30BST and there may be no afternoon session; source adds ‘maybe last night was not what was expected’., Daily Mail’s Doyle. Today’s cabinet meeting was initially supposed to be 5 hours long, with a ‘political cabinet’ initially to discuss party matters, followed by a traditional cabinet meeting.

The other big shift taking place in recent days was in oil markets where prices hit fresh 2019 highs after a U.S. official had said Washington was considering more sanctions on Iran and a key Venezuelan export terminal halted operations. U.S. crude futures traded at $61.82 per barrel, up 0.4 percent on the day while Brent futures were eyeing $70 a barrel for the first time since November at $69.19.

“China’s PMI number was the most significant monthly increase since 2012, which should ease concerns around a potential threat to oil demand,” said Stephen Innes, head of trading and market strategy at SPI Asset Management.

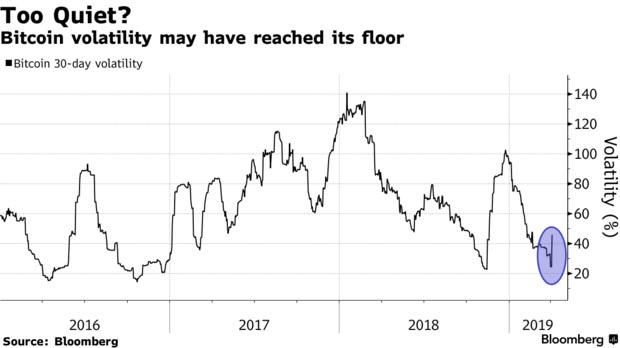

Copper and gold both ticked down in the industrial and precious metals markets but it was Bitcoin that stole the attention overnight when it suddenly exploded back to life, when it jumped as much as 23% to touch $5,000, its highest since November. Crypto-analysts pointed to a large order in a thin market, though there wasn’t any obvious trigger for than order immediately apparent.

The surge helped Bitcoin break through its 200-day moving average for the first time in more than a year. The crypto crashed 74% last year as authorities globally tightened their regulation on the market.

In currencies, the euro fell for a sixth day on growth concerns and the pound slid amid the Brexit impasse, boosting the Bloomberg Dollar Spot Index to a three-week high. Antipodean currencies led Group-of-10 losses as the Australian central bank’s statement was seen as dovish. In emerging markets, gains in MSCI’s EM share index were capped at 0.16 percent, after losses in countries such as Turkey and South Africa that were under pressure from political tension and weak local manufacturing.

The Turkish lira gave up 1.6 percent after the United States halted delivery of equipment related to the F-35 fighter aircraft to Turkey. The disagreement is the latest of a series of diplomatic disputes between the United States and Turkey, which were partly responsible for pushing the currency into a crisis last year. Playing into the lira’s recent volatility have been heavy-handed clampdown on the international lira market. Local elections at the weekend saw President Tayyip Erdogan’s AK Party lose Istanbul and Ankara.

Economic data include durable goods and capital goods orders. Walgreens Boots and Lamb Weston are due to report earnings

Market Snapshot

S&P 500 futures down 0.1% to 2,867.50

STOXX Europe 600 down 0.02% to 383.58

MXAP unchanged at 161.42

MXAPJ up 0.2% to 535.70

Nikkei down 0.02% to 21,505.31

Topix down 0.3% to 1,611.69

Hang Seng Index up 0.2% to 29,624.67

Shanghai Composite up 0.2% to 3,176.82

Sensex up 0.4% to 39,040.37

Australia S&P/ASX 200 up 0.4% to 6,242.36

Kospi up 0.4% to 2,177.18

German 10Y yield fell 1.1 bps to -0.037%

Euro down 0.1% to $1.1199

Brent Futures up 0.2% to $69.13/bbl

Italian 10Y yield rose 1.9 bps to 2.153%

Spanish 10Y yield fell 0.3 bps to 1.138%

Brent Futures up 0.2% to $69.13/bbl

Gold spot down 0.06% to $1,286.92

U.S. Dollar Index up 0.2% to 97.39

Top Headline News from Bloomberg

Theresa May is expected to confront her most senior ministers with the potentially explosive option to delay Brexit by months, as the U.K. struggles to find a plan for leaving the EU

European Commission President Jean-Claude Juncker stepped up his criticism of Chinese trade practices just days after President Xi Jinping sought to soothe European concerns in Paris

Investment intentions among U.K. firms slumped to an eight-year low, just one of the measures of economic health that weakened “considerably” amid recent Brexit turmoil, according to the British Chambers of Commerce

Australia’s central bank remained on the sidelines as it waits to analyze the economic impact of a fiscal injection designed to catapult Prime Minister Scott Morrison to a come-from-behind election victory.

European Union governments are struggling to reach consensus on a mandate to begin trade talks with the U.S., risking a delay that would further provoke Donald Trump’s ire after the bloc’s refusal to include agriculture in the negotiations

Mario Draghi is spending a chunk of his final year in office multitasking as a stopgap solution for the swelling empty-chair problem at the European Central Bank’s supervisory arm

Oil added to its biggest advance in more than two weeks after fresh evidence of the OPEC+ coalition’s resolve to cut output and a deepening crisis in Venezuela supported a bullish outlook for prices

European Union governments are struggling to reach consensus on a mandate to begin trade talks with the U.S., risking a delay that would further provoke Donald Trump’s ire after the bloc’s refusal to include agriculture in the negotiations

The Russian ruble has gained more than any currency in the world this year, and unrivaled carry returns fueled further inflows into ruble assets, making hedge funds the most bullish ever. But the best may be over if implied yields are any indication

Signs that China’s economy is stabilizing have kicked off a debate about whether the central bank should keep injecting liquidity into financial markets, with a former senior official warning of the risk of asset bubbles

Asian equity markets were mostly higher as the regional bourses picked up the bullish baton from Wall St where sentiment was underpinned and growth fears were eased by strong PMI data from US and China. ASX 200 (+0.4%) and Nikkei 225 (U/C) traded positive with tech, energy and financials leading the upside in Australia and with price action in the Japanese benchmark mainly currency-driven. Furthermore, participants had been awaiting any dovish clues from the RBA, as well as the Federal Budget which is seen as a platform for upcoming elections and is expected to include income tax cuts, billions for infrastructure spending and its first surplus in 12 years of AUD 4.1bln. Hang Seng (+0.2%) and Shanghai Comp. (+0.2%) remained upbeat after the recent recovery in factory data and amid optimism ahead of this week’s US-China trade talks in Washington, while outperformance was seen in gambling names following the better than expected Macau gaming revenue figures. Finally, 10yr JGBs were lower on spill-over selling from USTs and as the positive risk tone continued to dampen safe-haven demand, although some of the losses were pared following stronger demand and lower supply in today’s 10yr JGB auction.

Top Asian News

Australia Budget 2019: Winners and Losers

India Opposition Leader Gandhi Pledges to End Poverty by 2030

Bonds Advance as India’s Cash Boost Adds to Wagers of Rate Cuts

India Top Court Quashes RBI Attempt to Tighten Default Rules

A subdued session for European equities thus far [Eurostoxx 50 +0.2%] after the bullish momentum seen on Wall Street and Asia faded wherein major bourses were buoyed by the risk appetite. UK’s FTSE 100 [+0.5%] remains the outperformer as the export-heavy index benefits from the Brexit-beaten Pound. Sectors are relatively mixed with defensive sectors gaining as jittery investors hedge downside. In terms of individual movers, Pandora (-5.3%) fell to the foot of the of the Stoxx 600 (Unch) after Carnegie noted concern over the company’s Q1 results, adding that they would sell the stock at current levels. Elsewhere, Roll-Royce (-1.7%) nursed some losses after opening at the foot of its index Singapore Airlines grounded some planes due to their Rolls-Royce engines. On the more optimistic note, Pernod Ricard (+1.3%), Remy Cointreu (+1.1%) and Carlsberg (+0.4%) are all benefiting from an overweight initiation at Barclays. In recent US newsflow sources indicate that Exxon (XOM) hopes to raise USD 3bln for the potential sale of both onshore & offshore oil and gas assets in Nigeria.

Top European News

Korea Seeks Extradition of Ex-Deutsche Trader Over Manipulation

FTSE 100 Outperforms as Brexit Impasse Sends Pound Lower

Billionaire Mordashov Seeks $1.8 Billion Deal for Russia’s Lenta

Pandora Falls Amid Concerns Over China Sales in First Quarter

In currencies, AUD/NZD/GBP – The clear G10 underperformers, with Aud/Usd extending post-RBA declines to 0.7065 from a knee-jerk peak around 0.7130 on the back of much stronger than expected Australian building approvals overnight. The RBA maintained rates as widely expected, but alongside an ongoing neutral policy stance there was a tweak to the accompanying statement suggesting that keeping the status quo may not be enough to support growth as it has for the past 2 ½ years. Instead, data and developments will be monitored to see if the Cash Rate requires an adjustment. Note, little reaction to the pre-election Budget despite a significant rise in the projected 2019/2020 surplus vs December’s forecast and a proposed Aud158 bn tax cut package as the Government also acknowledged the emergence of genuine and clear downside risks that might impact an otherwise sound domestic economy. Elsewhere, Nzd/Usd has fallen in sympathy from circa 0.6804 to 0.6768, but also independently in response to a marked deterioration in Q1 NZIER sentiment, while Cable has retreated further from 1.3100+ highs due to UK-specific factors as yet another round of IVs in the HoC found no common ground on any of the 4 alternative Brexit strategies put forward, albeit with the CU motion moving a lot closer gaining a majority. Cable has pared some losses from a 1.3025 low and Eur/Gbp has eased back from a whisker under 0.8600 on a firmer than forecast UK construction PMI, though still sub-50. Technically, 1.3030 is daily chart support for Cable and the 200 DMA is 1.2977, while flow-wise a hefty 1.2 bn option expiry between 1.3045-55 may cap a firmer rebound, as could 1 bn rolling off in Aud/Usd at the 0.7100 strike.

CAD/EUR/CHF/JPY – All weaker vs the Greenback, as the DXY edges closer towards 97.500 and ytd peaks in wake of yesterday’s upbeat US manufacturing PMI and profiting from the demise of major rivals. Usd/Cad remains above 1.3300 after Monday’s disappointing Canadian PMI, while the single currency is struggling to keep hold of the 1.1200 handle where a hefty option expiry sits (1 bn) and has dipped just a few pips short of key Fib support (1.1187/6) protecting the 2019 low at 1.1177. Elsewhere, slightly above consensus Swiss CPI has not held the Franc recover vs the Buck within a par-0.9984 range, but it is holding just above 1.1200 against the Euro. Usd/Jpy has nudged up towards 111.50 and the 200 DMA (111.48) after its recent range break and clearance of chart resistance, but may yet be drawn back to the 111.00-20 region given 2.4 bn expiries.

EM – The Lira continues to underperform regional counterparts on political grounds and renewed Turkish-US tensions following the latter’s decision to suspend deliveries of F-35 jets, with Usd/Try back up near the upper end of a 5.6125-5.4775 range.

Australian Building Approvals (Feb) M/M 19.1% vs. Exp. -1.0% (Prev. 2.5%). (Newswires) Australian Building Approvals (Feb) Y/Y -12.5% vs. Exp. -27.0% (Prev. -28.6%)

In commodities, WTI (+0.9%) and Brent (+0.5%) futures extended earlier gains as supply-side developments keep the benchmarks afloat. Supply in Venezuela has been disrupted after its main oil port had to shut due to a lack of electricity, and with the US eyeing secondary sanctions on Iran, traders are speculating about further supply upsets. “Oil prices should move higher over the next two quarters as supply fundamentals remain constructive, with OPEC+ making good progress on pledged output cuts” says BNP Paribas Global Head of Commodities. Elsewhere, gold (Unch) trades lacklustre and remains near its lowest levels in over 3 weeks amid a firmer greenback and as safe-havens were shunned, while copper was steady and took a breather from recent advances amid the tentative tone around the market. Finally, Dalian iron ore futures hit a record intraday high with further supply concerns as BHP warned that iron ore output will fall by 6-8mln tonnes after damage caused by cyclones in Western Australia last week.

US Event Calendar

8:30am: Durable Goods Orders, est. -1.8%, prior 0.3%; Durables Ex Transportation, est. 0.1%, prior -0.2%

8:30am: Cap Goods Orders Nondef Ex Air, est. 0.05%, prior 0.8%; Cap Goods Ship Nondef Ex Air, est. -0.1%, prior 0.8%

Wards Total Vehicle Sales, est. 16.8m, prior 16.6m

DB’s Jim Reid concludes the overnight wrap

It might not quite be 21 years yet but it feels that way for all of us following Brexit as the House of Commons once again gathered last night to vote on the slimmed down list of options for the indicative votes or as one scribe wrote “vindictive votes”. Every motion failed to achieve a parliamentary majority though. The proposal for a customs union with the EU came the closest yet, losing by a vote of 276-273, while the option for a second referendum came second-best with a 292-280 loss. Some MPs argued for linking the two options into a single proposal later this week, but other members contended that watering down either motion would lose more votes than it would gain. Meanwhile parliament will have another chance to take over Brexit on Wednesday when further set of votes on alternatives are planned.

So with things looking deadlocked in the House of Commons, attention will shift to today’s marathon cabinet meeting, scheduled for 9am to 12pm and then again from 1pm to 3pm. The morning session will be political officials only, no civil servants, meaning that PM May and her team are likely to consider the options including calling for a general election. That’s the base case from DB’s Oliver Harvey, though there is space in the parliamentary timetable for May to bring her WA for a fourth vote tomorrow if she wanted to. Sterling had traded firmer through much of yesterday and was up around +0.52% when New York went home. After the votes, the currency dropped over half a percent and is trading slightly above those levels this morning.

In contrast to UK politics, markets have been a lot simpler to dissect over the last 24 hours. “China hints at a cycle turn, the world parties” would be a way of describing it as a Chinese proverb. Indeed the positive China PMI provided the excuse to rally all day and the excuse to not worry about the softer parts of the global data releases from yesterday. To be fair a similarly stronger-than-consensus US manufacturing ISM helped too. In the middle of that we had a slightly disappointing round of final manufacturing PMIs in Europe but if China is turning this will be seen as backward looking. If you wanted a confusing summary though of life in Europe then the strongest link Germany now has the lowest manufacturing PMI in the region (44.1) and the angst ridden, economic precipice leaning, Brexit suffering UK the highest (55.1) outside of the Scandi countries even if stockpiling was the reason. Also Greece (54.7) is now around 10pts higher than Germany and even Turkey (47.2) – for all the political and economic turmoil – is ahead of Europe’s powerhouse.

We’ll touch on these in more micro detail shortly but just quickly onto markets first. We saw the S&P 500 climb +1.15% last night to take it to a fresh 25-week high. Industrials and financials led the charge while the NASDAQ also climbed +1.29% for its third daily gain in a row and 12th in the last 16 sessions. In Europe, even downbeat comments from the EC’s Juncker about China’s trade practices failed to stop the STOXX 600 climbing +1.21% while European Banks rallied +2.80% for their biggest one-day gain since February 15th. The VIX fell to 13.40 (-0.31pts) as a result of all that and the V2X to 14.79 (-0.49pts) – both well below their YTD averages of 16.4 and 15.5, respectively. It was similarly strong for credit where HY spreads were -8bps tighter in Europe and -11bps tighter in the US. EM FX rose +0.85% with notable gains for the likes of the South African Rand (+2.30%) and Turkish Lira (+1.37%).

The big contrast was in rates where we saw a big slide. The most notable move was 10y Treasuries selling off +9.6bps, the most since January 4th, to take them back to 2.501%. That is also 16.3bps off the intraday lows from last week however yields are still -26.5bps off their March highs. The yield curve steepened, with the 2y10y and 3m10y spreads rising +3.0bps and +10.4bps, respectively, for a +5.4bps and +22.6bps improvement from last week’s lows. The spread between the 18m forward 3m yield and spot 3m yield rose +12.2bps to -12.2bps, which is +33.7bps off of last week’s low. So a big turnaround. Bunds (+4.4bps) even hit the dizzying heights of -0.026% and had their weakest day since January 9th.

Asian markets are eking out modest gains this morning with the Nikkei (+0.12%), Hang Seng (+0.09%), Shanghai Comp (+0.41%) and Kospi (+0.24%) all up. Elsewhere, futures on the S&P 500 are down -0.14% while, 2y and 10y treasury yields are both back down c. -3bps this morning.

Coming back to the data, in the US the big highlight was that the March ISM manufacturing survey printed at 55.3 versus expectations for 54.5. It also represented a jump of +0.9pts from February while the details affirmed the solid print. Indeed the employment component jumped to 57.5 from 52.3 and new orders to 57.4 from 55.5. Interestingly the prices paid component also jumped to 54.3 from 49.4, its biggest rise since 2017 and its highest level since last year. However it does remain well off the >70 levels from Jan-Oct last year.

That data helped to offset what was at face value a broadly weaker February retail sales report, however upward revisions to January did at least help to take the sting out of the tail. Retail control in February printed at -0.2% mom (vs. +0.3% expected) however the January reading was revised up a significant +0.6ppts to +1.7% mom. That is actually the largest monthly print since October 2001 and further explains away the oddly weak December number of -2.2% mom that caused so much head scratching when it came out. Retail sales momentum is certainly weaker than last year, but the first quarter data is developing less poorly than expected. Elsewhere, construction spending rose a better-than-expected +1.0% mom in February (vs. -0.2% expected) and business inventories also climbed more than expected in January (+0.8% mom vs. +0.5% expected). We should note that the Atlanta Fed GDP tracker for Q1 is now up to 2.1%, up from 1.7% at the end of last week.

Core euro area equity markets (the DAX and CAC) did come off their highs in Europe early in the morning following the final March manufacturing PMI revisions, though the FTSEMIB and IBEX rallied further. For the euro area the broad reading was revised down -0.1pt to 47.5 which confirms it as being the lowest in nearly 6 years. France was revised down -0.1pts to 49.7 (a 3-month low) however the big headline grabber was Germany being revised down -0.6pts to 44.1. That puts it at the lowest level in 80 months. In the periphery Italy also disappointed slightly at 47.4 (vs. 47.5 expected) and the lowest in 70 months. The two bright spots were Spain hitting a two-month high at 50.9 (vs. 49.7 expected) and Greece a 12-month high at 54.7. Staying with Europe we also got the March CPI report for the Euro Area yesterday where the core metric dipped two-tenths to +0.8% yoy, one-tenth lower than expected.

The biggest stand out from the EU country PMIs however was the UK – a claim we can still hold for now – after it jumped +3pts to 55.1 and far exceeding the consensus for 51.2. However stockpiling was cited as a big reason for the jump so the quality of the details didn’t match the headline level and the likelihood is that we’ll see a sharp reversal soon.

Looking at the day ahead now, this morning it’s quiet for data releases with only the March construction PMI in the UK and February PPI report for the Euro Area due. In the US this afternoon expect there to be plenty of eyes on the preliminary durable and capital goods orders data in the US (+0.1% mom core capex orders data expected) especially for firming up Q1 GDP forecasts, while at some point we should also get March vehicle sales data. Away from that the ECB’s Praet is due to speak this morning in Frankfurt while the WTO will at some point release its trade forecast report for 2019-20.

via ZeroHedge News https://ift.tt/2Vf7IrE Tyler Durden

When Bernie Sanders and Tucker Carlson agree on something, be afraid. The democratic socialist senator and the populist conservative pundit are not natural allies. But recently, they have converged on a single point of consensus with potentially terrifying consequences: Americans have too much stuff.

The far left of the American political spectrum is the longtime home of Starbucks-smashing protesters, militant recyclers, Naomi Klein acolytes, and Walmart boycotters—people who believe we are destroying the planet with our overconsumption of cheap stuff at the expense of workers’ well-being. On his 1987 folk album (yes, such a thing exists), Sanders pinpointed “consumerism, the futile striving for happiness by earning more and more money to buy more and more things,” as one of the world’s great problems, a theme the Vermont independent has returned to while lamenting everything from the wide variety of deodorant choices on drug store shelves to Chinese imports, writes Katherine Mangu-Ward.

In what was undoubtedly the most closely watched earnings report of the session, Dow component Walgreens saw its shares drop more than 6% in pre-market trading after the company slashed its earnings guidance, becoming the latest corporate to undercut the economic growth narrative by slashing its earnings guidance.

After reporting results for its fiscal second quarter, the company said it’s now expecting roughly flat EPS growth, down from a prior forecast of 7%-12%.

Here are the highlights from the report:

-Net Sales: $34.5B (est $34.52B)

-Adj EPS: $1.64 (est $1.72)

-2Q adjusted gross margin 22.6%, estimate 23.5%

-2Q adjusted operating margin 5.3%

Cuts Forecast

via ZeroHedge News https://ift.tt/2Ibnq3n Tyler Durden

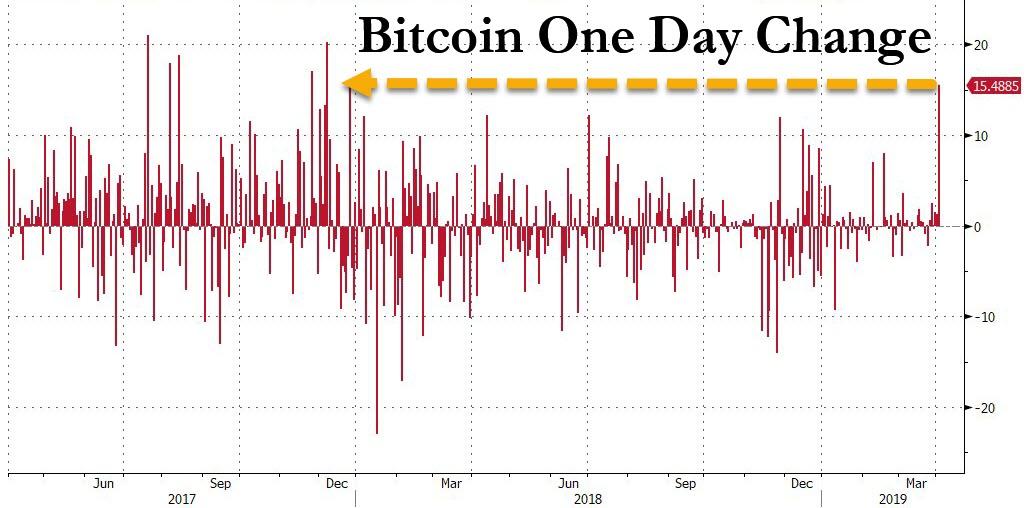

The CBOE may be regretting its decision to halt Bitcoin futures trading this morning, when shortly after midnight Eastern time, bitcoin suddenly broke the calm that had blanketed the crypto space for over three months, when it exploded as much as 23% higher in minutes, rising briefly above $5,000, its highest level since November, and pushing the entire $160 billion cryptocurrency space sharply higher, with rival coins Ether, Litecoin also soaring, as did cryptocurrency-linked stocks including Remixpoint and CMC Markets Plc, as well as that old market favorite Riot Blockchain.

At its peak, the intraday move, which added more than $17 billion to the value of digital assets tracked by CoinMarketCap.com, was the biggest since early 2014. Even after paring some gains, with bitcoin currently up just over 15% at $4,777.81, the daily swing was the biggest since the euphoric peak bubble days of late 2017.

Understandably, traders was keenly focused on identifying the catalyst behind the move although a clear reason for the sudden surge has yet to emerge. George Harrap, chief executive officer at Bitspark, told Bloomberg he’s putting “most things on pause” until the market settles down. His contacts in the Bitcoin community have yet to identify a catalyst for the sudden jump.

“The reason why? Anybody’s guess at the moment,” Harrap said.

Some of the potential triggers cited on trading desks and in social media included a sizable block of expiring puts, short covering by traders who had stop-loss orders around the $4,200 level and an April Fool’s Day story on a little-known online news site claiming that the U.S. Securities and Exchange Commission had approved Bitcoin exchange-traded funds, although that was quickly discounted as the gains persisted even after the story was discounted.

Another possible reason: crypto vol has troughed, prompting renewed interest in the asset class by investors seeking volatility at a time when cross-asset vol has likewise collapsed.

Another theory: renewed interest in money “offshoring” by Asian and/or Turkish investors.

To be sure, bitcoin susceptibility to unexplained, erratic price swings is nothing new and made it very popular among speculators, who are seeking a return to the glory days of 2017 when Bitcoin surged more than 1,400%. However, since its peak around $20,000 in late 2017, bitcoin suffered a 74% crash which eliminated much if not all of the froth in the former asset bubble.

Market participants say big buy orders in Bitcoin can often lead to outsized moves, in part because volume is spread across dozens of venues. Trend-following individual investors and short covering can also exacerbate volatility.

Of course, erratic moves such as this one have deterred institutional investors, whose concerns about cryptocurrencies range from uncertain regulation to exchange hacks and market manipulation.

“Bitcoin is still primarily retail-led,” said Craig Erlam, senior market analyst at Oanda Corp. in London. “It’s still a relatively unsophisticated area of trading.”

Predictably, the skeptics promptly emerged despite the sudden price gains which pushed the price of bitcoin back to levels last seen in November 2018 when the crypto broke down below a former support just above $6,000:

“Events such as today’s will probably be seen negatively, or viewed as this market doesn’t conform to the trading of traditional instruments,” said Dave Chapman, CEO of crypto exchange ANXONE. “We have to realize that this asset class is only a decade old, and it only started getting mainstream attention five years ago.”

* * *

Below we present the full market analysis from Bequant seeking to explain the sudden move:

Last week we asked, “When FOMO?”, pointing to the market where Bitcoin was trying to consolidate above the key $4,000 level while also having to deal with expiring futures and options contracts. In particular, as we pointed out, decent size was noted at 3500 strike (puts). For those that are yet to be convinced of the importance that derivatives market has on the underlying, it is worth pointing out that last Friday was another record day for Deribit with more than $40mln BTC options traded.

The market is very unpredictable, the price action overnight is a testament to that, when Bitcoin rallied over 15% and reached the highest level since November last year. It really remains to be seen whether the gains will be sustained but the market, which is very much retail driven and highly leveraged, but the impact of FOMO is not to be underestimated…

Source: TradeBlock (5min Bitcoin price movement 02.04.19)

Still, looking into the future (June options), there are early indications that the market is turning more bullish, with plenty of interest noted at 6,000 strike (calls) where there is already OI of 2342.9 (delta 0.23).

Looking elsewhere, as pointed out by The Block, Tether (USDT) has experienced its highest daily volume since first being issued in 2015. According to data from CoinMetrics.io, on March 31, 2019, there were 38,150 USDT transactions processed. As a reminder, Tether Limited updated its website to clarify how its reserves are made up. The company now claims that each coin is backed by “reserves, which include traditional currency and cash equivalents and, from time to time, other assets and receivables from loans made by Tether to third parties.”

Finally, something to ponder about…when Bitcoin futures were launched back in Dec’2017, the influx of hot money saw the prices rocket all the way to $20,000 but what is more interesting is that the futures curve was trading in contango. Since then, the curve has evolved and is generally trading in backwardation. However, Ethereum futures curve has been trading in contango for a long time and many argue that this is because of oversupply. Could it be that the natural state of the Bitcoin & Ethereum curves is a contango? As opposed to Keynes’ longstanding theory that the natural state of commodity markets is backwardation.

via ZeroHedge News https://ift.tt/2CNnEdg Tyler Durden

When Bernie Sanders and Tucker Carlson agree on something, be afraid. The democratic socialist senator and the populist conservative pundit are not natural allies. But recently, they have converged on a single point of consensus with potentially terrifying consequences: Americans have too much stuff.

When Bernie Sanders and Tucker Carlson agree on something, be afraid. The democratic socialist senator and the populist conservative pundit are not natural allies. But recently, they have converged on a single point of consensus with potentially terrifying consequences: Americans have too much stuff.

{kind=link}