In what was undoubtedly the most closely watched earnings report of the session, Dow component Walgreens saw its shares drop more than 6% in pre-market trading after the company slashed its earnings guidance, becoming the latest corporate to undercut the economic growth narrative by slashing its earnings guidance.

After reporting results for its fiscal second quarter, the company said it’s now expecting roughly flat EPS growth, down from a prior forecast of 7%-12%.

Here are the highlights from the report:

-Net Sales: $34.5B (est $34.52B)

-Adj EPS: $1.64 (est $1.72)

-2Q adjusted gross margin 22.6%, estimate 23.5%

-2Q adjusted operating margin 5.3%

Cuts Forecast

via ZeroHedge News https://ift.tt/2Ibnq3n Tyler Durden

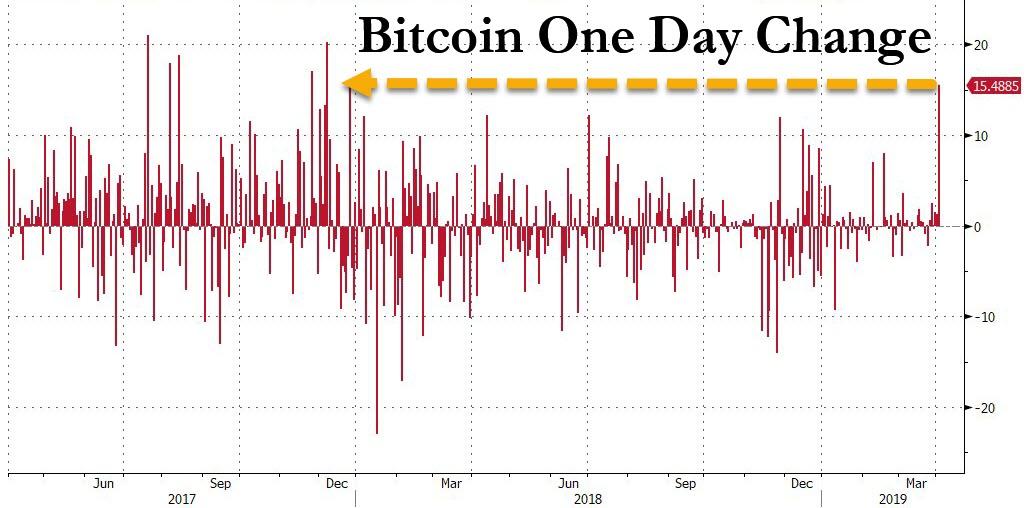

The CBOE may be regretting its decision to halt Bitcoin futures trading this morning, when shortly after midnight Eastern time, bitcoin suddenly broke the calm that had blanketed the crypto space for over three months, when it exploded as much as 23% higher in minutes, rising briefly above $5,000, its highest level since November, and pushing the entire $160 billion cryptocurrency space sharply higher, with rival coins Ether, Litecoin also soaring, as did cryptocurrency-linked stocks including Remixpoint and CMC Markets Plc, as well as that old market favorite Riot Blockchain.

At its peak, the intraday move, which added more than $17 billion to the value of digital assets tracked by CoinMarketCap.com, was the biggest since early 2014. Even after paring some gains, with bitcoin currently up just over 15% at $4,777.81, the daily swing was the biggest since the euphoric peak bubble days of late 2017.

Understandably, traders was keenly focused on identifying the catalyst behind the move although a clear reason for the sudden surge has yet to emerge. George Harrap, chief executive officer at Bitspark, told Bloomberg he’s putting “most things on pause” until the market settles down. His contacts in the Bitcoin community have yet to identify a catalyst for the sudden jump.

“The reason why? Anybody’s guess at the moment,” Harrap said.

Some of the potential triggers cited on trading desks and in social media included a sizable block of expiring puts, short covering by traders who had stop-loss orders around the $4,200 level and an April Fool’s Day story on a little-known online news site claiming that the U.S. Securities and Exchange Commission had approved Bitcoin exchange-traded funds, although that was quickly discounted as the gains persisted even after the story was discounted.

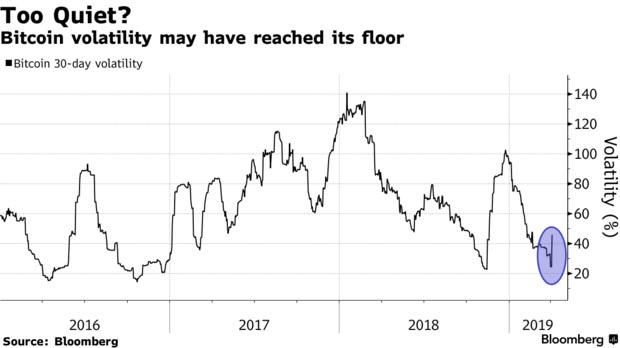

Another possible reason: crypto vol has troughed, prompting renewed interest in the asset class by investors seeking volatility at a time when cross-asset vol has likewise collapsed.

Another theory: renewed interest in money “offshoring” by Asian and/or Turkish investors.

To be sure, bitcoin susceptibility to unexplained, erratic price swings is nothing new and made it very popular among speculators, who are seeking a return to the glory days of 2017 when Bitcoin surged more than 1,400%. However, since its peak around $20,000 in late 2017, bitcoin suffered a 74% crash which eliminated much if not all of the froth in the former asset bubble.

Market participants say big buy orders in Bitcoin can often lead to outsized moves, in part because volume is spread across dozens of venues. Trend-following individual investors and short covering can also exacerbate volatility.

Of course, erratic moves such as this one have deterred institutional investors, whose concerns about cryptocurrencies range from uncertain regulation to exchange hacks and market manipulation.

“Bitcoin is still primarily retail-led,” said Craig Erlam, senior market analyst at Oanda Corp. in London. “It’s still a relatively unsophisticated area of trading.”

Predictably, the skeptics promptly emerged despite the sudden price gains which pushed the price of bitcoin back to levels last seen in November 2018 when the crypto broke down below a former support just above $6,000:

“Events such as today’s will probably be seen negatively, or viewed as this market doesn’t conform to the trading of traditional instruments,” said Dave Chapman, CEO of crypto exchange ANXONE. “We have to realize that this asset class is only a decade old, and it only started getting mainstream attention five years ago.”

* * *

Below we present the full market analysis from Bequant seeking to explain the sudden move:

Last week we asked, “When FOMO?”, pointing to the market where Bitcoin was trying to consolidate above the key $4,000 level while also having to deal with expiring futures and options contracts. In particular, as we pointed out, decent size was noted at 3500 strike (puts). For those that are yet to be convinced of the importance that derivatives market has on the underlying, it is worth pointing out that last Friday was another record day for Deribit with more than $40mln BTC options traded.

The market is very unpredictable, the price action overnight is a testament to that, when Bitcoin rallied over 15% and reached the highest level since November last year. It really remains to be seen whether the gains will be sustained but the market, which is very much retail driven and highly leveraged, but the impact of FOMO is not to be underestimated…

Source: TradeBlock (5min Bitcoin price movement 02.04.19)

Still, looking into the future (June options), there are early indications that the market is turning more bullish, with plenty of interest noted at 6,000 strike (calls) where there is already OI of 2342.9 (delta 0.23).

Looking elsewhere, as pointed out by The Block, Tether (USDT) has experienced its highest daily volume since first being issued in 2015. According to data from CoinMetrics.io, on March 31, 2019, there were 38,150 USDT transactions processed. As a reminder, Tether Limited updated its website to clarify how its reserves are made up. The company now claims that each coin is backed by “reserves, which include traditional currency and cash equivalents and, from time to time, other assets and receivables from loans made by Tether to third parties.”

Finally, something to ponder about…when Bitcoin futures were launched back in Dec’2017, the influx of hot money saw the prices rocket all the way to $20,000 but what is more interesting is that the futures curve was trading in contango. Since then, the curve has evolved and is generally trading in backwardation. However, Ethereum futures curve has been trading in contango for a long time and many argue that this is because of oversupply. Could it be that the natural state of the Bitcoin & Ethereum curves is a contango? As opposed to Keynes’ longstanding theory that the natural state of commodity markets is backwardation.

via ZeroHedge News https://ift.tt/2CNnEdg Tyler Durden

Though there’s no stopping a lawsuit brought by the administration and more than 20 state AGs seeking to finally declare ObamaCare unconstitutional, the Republican Party’s latest push to throw out ObamaCare and replace it with something better and affordable has officially been cancelled by President Trump.

After a pair of pundits lashed out at Trump acting Chief of Staff Mick Mulvaney and accused Republicans of jeopardizing the health coverage of more than 20 million people without a clear plan to replace ObamaCare, Trump tweeted late Monday night that Republicans will wait until after the 2020 election to try and pass a still-ill-defined Republican plan that will feature “far lower premiums (costs) and deductibles” and “always support Pre-Existing Conditions” – in the latest example of him setting policy via Twitter.

Though it’s possible that the Texas lawsuit seeking to invalidate parts of the law after US District Judge Reed O’Connor ruled that it should be scrapped in its entirety could result in the rest of ObamaCare (Republicans have already done away with the hated individual mandate) being thrown out long before 2020, for now at least, Republicans will put their legislative push to come up with an alternative health-care plan, which Mulvaney said over the weekend would likely fall to lawmakers to sort out, on hold.

Whatever the details of the 2020 plan might be, “it will be truly great HealthCare that will work for America,” Trump said, and “the party will be known as the Party of Great HealthCare”. The vote will take place “right after the Election when Republicans hold the Senate & win back the House.”

Everybody agrees that ObamaCare doesn’t work. Premiums & deductibles are far too high – Really bad HealthCare! Even the Dems want to replace it, but with Medicare for all, which would cause 180 million Americans to lose their beloved private health insurance. The Republicans…..

….are developing a really great HealthCare Plan with far lower premiums (cost) & deductibles than ObamaCare. In other words it will be far less expensive & much more usable than ObamaCare. Vote will be taken right after the Election when Republicans hold the Senate & win……

….back the House. It will be truly great HealthCare that will work for America. Also, Republicans will always support Pre-Existing Conditions. The Republican Party will be known as the Party of Great HealtCare. Meantime, the USA is doing better than ever & is respected again!

Last week, Trump told a group of reporters that “We are going to be the Republicans, the party of great health care”…and that “the Democrats, they let you down. They came up with Obamacare and it is terrible.” In his tweets, he once again denounced Democratic plans for “Medicare for All”, which he said would “cause 180 million Americans to lose their beloved Private health insurance.” Despite its high costs, polls show that ObamaCare has gradually become more popular with voters, and some pundits cited it as a key factor in the Democratic takeover of the House last fall.

But by punting on the ObamaCare debate, Trump has given Republicans to avoid upsetting the status quo, while running on their opposition to Medicare for All.

via ZeroHedge News https://ift.tt/2OE74RT Tyler Durden

Venezuela is home to the largest oil deposits in the world, which makes the political stakes involved much higher than they would be otherwise. Enter Juan Guaidó, Washington’s puppet leader in Caracas, who will be attempting to rally the country against legitimate (i.e., democratically elected by the people) President Nicolas Maduro next month.

Venezuelan opposition leader Juan Guaidó has announced that April 6 will kick off a nationwide “tactical actions” as part of the so-called Operation Freedom protests, which are designed to oust President Nicolas Maduro.

“On April 6 will be the first tactical actions of the # Operation Freedom across the country,” Guaidó declared over Twitter this week.

“That day we must be ready, prepared and organized, with the Aid and Freedom Committees already formed. The rescue of Venezuela is in our hands!”

Is this the start of Maidan 2.0?

But first, who is Juan Guaidó? That’s a questioning worth pondering momentarily because just a few months ago, the overwhelming majority of Venezuelans – 81 percent of the population – had never heard of the young man before. That all changed when Guaidó, 35, was awakened by a phone call from none other than US Vice President Mike Pence. Literally overnight he had become the poster boy of the political opposition in Venezuela and leader of the National Assembly. “Juan Guaidó is a character that has been created for this circumstance,” Marco Teruggi, a sociologist and leading observer of Venezuelan politics, told the Grayzone. “It’s the logic of a laboratory – Guaidó is like a mixture of several elements that create a character who, in all honesty, oscillates between laughable and worrying.”

In fact, Washington recognized Guaidó more than just an opposition leader; it recognized him, without a drop of legality, as the de-jure president of the Latin American country (Just this week, Guaidó’s wife Fabiana Rosales was the guest of honor at the White House, as the media referred to her as “first lady” and “first-lady-in-waiting”).

Meanwhile, the US media has wasted no time placing the laurels on Guaidó’s young, inexperienced head, declaring the quiet coup d’ etat the “restoration of democracy” in a land where the election process, which provides its voters with a digital receipt, is considered to be the most transparent and reliable in the world. In other words, if Maduro is in office, which he is, it is due to the will of the people, not the will of Mike Pence.

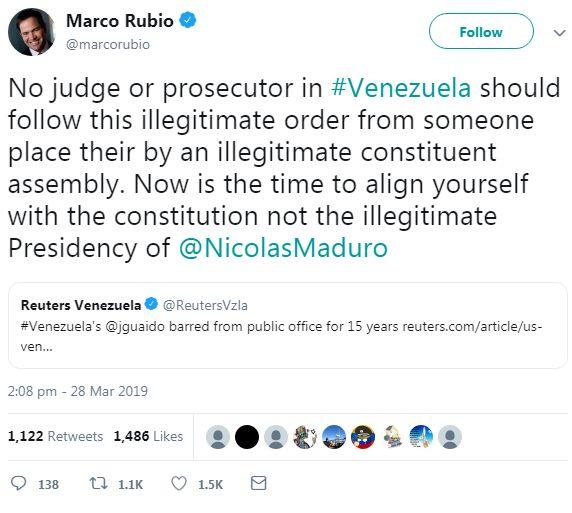

So what should Venezuela expect on April 6 with the commencement of Guaidó’s organized protest? Anything is possible, but the likelihood of some sort of event or incident that will heighten the tensions in the country cannot be discounted. It certainly does not help that Trump’s national security advisor John Bolton warned in the past of “serious consequences” if any harm comes to Guaidó.

“Let me reiterate – there will be serious consequences for those who attempt to subvert democracy and harm Guaidó,” Bolton tweeted back in January. Those sorts of threats must be treated with extreme caution and due consideration. Suffice it to recall what followed like clockwork in Syria after such red-line threats were delivered about what would happen in the event of a chemical attack. Unsurprisingly, a chemical attack would eventually occur, whereupon the United States would immediately blame the event on the government, as opposed to the ragtag terrorist rebels who had infinitely more reason for resorting to such methods, and more so following such declarations from the US. In other words, should anything untoward happen to Guaidó, the West would have its perfect pretext for whatever follows next, which are better left to the imagination.

Although it appears as though Juan Guaidó’s popularity is on the wane – his motorcade was attacked by a pro-Maduro crowd just this week, while turnout for his anti-government marches has been reportedly dwindling – Caracas took the step of barring him from holding public office for 15 years due to irregularities in his financial records. According to the State Comptroller, Juan Guaidó has taken 90 international trips without indicating who provided the estimated $94,000 in expenses.

“We’re going to continue in the streets,” Guaidó responded.

Meanwhile, back in the United States, a number of government officials are taking a very unhealthy interest, if not suspicious interest, in what is happening in Caracas. Senator Marco Rubio, for example, sounds worse than any opposition figure in Venezuela, and tweets about practically nothing else than what is happening south of the border. On one particularly lamentable occasion, Rubio was delusional enough to actually post before-and-after images of former Libyan leader Muammar Gaddafi. The first showed him in power, the second just moments before being brutally murdered by a street mob. It boggles the mind to think that this man, who has a strange penchant for quoting Bible verse while fomenting for violent upheaval, stood on a platform as a Republican presidential hopeful.

In any case, there have been several events that strongly suggest that the United States has some sort of plan to bring about the crisis that could lift Guaidó into power, as well as open up the Latin American oil industry to foreign private interests, as he has already promised to do.

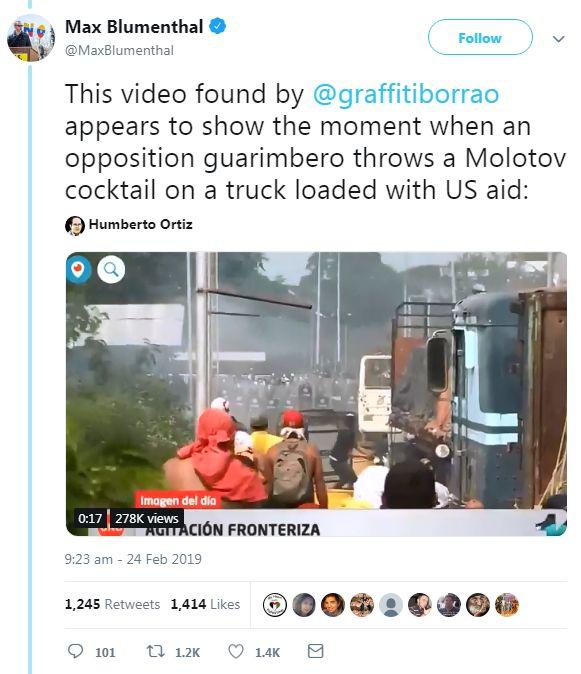

First, there is the well-documented incident from last month in which a ‘humanitarian supply’ truck, attempting to cross into Venezuela from Colombia, was torched. The US quickly blamed the incident on Maduro, however, video footage seems to indicate that it was actually anti-government protesters who carried out the attack with the use of Molotov cocktails.

Meanwhile, the beleaguered Latin American country has suffered a spate of electricity blackouts this month, which Maduro has been quick to blame on the United States. Guaidó, of course, blamed the outages on the “incompetence” of the Maduro government. However, Maduro may be forgiven for seeing the hand of the United States every time the lights go out. In fact, such things were discussed years ago, as revealed in a Wikileaks email dump that show even during the reign of Hugo Chavez, the problem of energy supplies was considered as a crowbar to break down the government. The following email was from Stratfor, which provides intelligence analysis.

“A key to Chavez’s current weakness is the decline in the electricity sector. There is the grave possibility that some 70 percent of the country’s electricity grid could go dark as soon as April 2010… This could be the watershed event, as there is little that Chavez can do to protect the poor from the failure of that system. This would likely have the impact of galvanizing public unrest in a way that no opposition group could ever hope to generate.”

Now, to what degree, if any, the United States may be tempted to hack/attack the Venezuelan power grid is anybody’s guess, but it certainly does not seem to be beyond the realm of possibility. And this could explain why the United States is so rattled by the presence of some 100 Russian cyber specialists in Venezuela, which arrived last week.

Russian Foreign Ministry spokeswoman Maria Zakharova said Russia’s relations with Venezuela are conducted“in strict accordance with the Constitution of this country and in full respect of its legislation.”

Understandably, the last thing that Moscow would like to see is yet another regime change fiasco, this time in Caracas, similar to the one that occurred on its border in Ukraine with the Maidan uprising, which continues to wreak havoc on global relations. In that sense, the global community can only hope that common sense and scruples wins out over opportunism and rogue politics, all in the name of oil profits.

via ZeroHedge News https://ift.tt/2V7sclX Tyler Durden

Two former traders from Barclays were sentenced to as much as five years in prison by a London judge for manipulating a benchmark interest-rate in favor of their bank’s trading positions. As Bloomberg reports, with today’s sentencing the judge meant to put those still working in the industry on notice that similar transgressions would lead to extended time spent being Bubba’s bunk mate.

Former swaps trader Carlo Palombo received a four year sentence and his colleague, Colin Bermingham, got a five year sentence. They’ll both be eligible for parole after serving half of their prison time. Another Barclays trader, Sisse Bohart, was acquitted last week.

The traders were charged with manipulating the Euro interbank offered rate, which is tied to trillions of dollars of loans and derivatives. The rate is calculated with submissions by major banks and is supposed to reflect the cost of borrowing between them. The convicts were accused of rigging the rate between 2005 and 2009.

The judge, Michael Gledhill, said in his remarks that he wanted to send a message to others in the industry. “Those convicted of manipulating interest rates will face substantial custodial sentences,” he said.

The verdicts were a victory for the UK Serious Fraud Office, which is frequently criticized for mishandling high profile cases. However, that hasn’t stopped the agency from accumulating other convictions against prominent bankers. For example, UBS LIBOR trader Tom Hayes was found guilty in 2015 and Deutsche Bank’s Christian Bittar was found guilty last year.

Palombo and Bermingham’s prosecutions hit road bumps early on when multiple defendants refused to come to the UK for trial.

Lisa Osofsky, director of the SFO said: “These men deliberately undermined the integrity of the financial system to line their pockets and to advantage the banks they worked for. We are committed to tracking down and bringing to justice those who defraud others and abuse the system.”

Palombo’s lawyer John Hartley said: “This is a very disappointing end to a very hard fought case. He and his family are of course devastated by the outcome and he will need some time to come to terms with this decision while we consider the issue of any appeal.”

Throughout the trial, both defendants maintained there was nothing wrong with taking a trader’s positions into account while setting the rate, as long as the bank still submitted a legitimate rate from within a range. And even in the Judge’s remarks, he noted that there was no code or definition that gave guidance or assistance as to how the panel banks should determine the rates they submit.

Despite this, the judge said the traders’ actions were contrary to the spirit of the code and that senior managers should have been aware of it.

Judge Gledhill said: “That failure might be thought by an interested observer to be at best foolhardy, if not utterly negligent. It was an open door for those involved in the conspiracy to manipulate, or attempt to manipulate, the Euribor rate for the advantage of their own bank’s trading positions.”

via ZeroHedge News https://ift.tt/2FQ5Q3c Tyler Durden

Former Paterson, New Jersey, police officer Ruben McAusland has been sentenced to five years in prison for drug dealing and assaulting a hospital patient. Video shot by the cop’s partner showed McAusland striking a man in a hospital bed hard enough that blood sprayed onto the bed. A second video shot by a security camera showed McAusland and his partner attacking the man as he sat in a wheelchair in a waiting area of the hospital earlier.

In recent years, the controversial subject of global warming and a potential “climate disaster” has received a lot of media attention.

There are progressive politicians who are now arguing that unless profound changes in public policy are made to reduce worldwide carbon emissions, we face an impending world-wide climate related catastrophe.

Former Presidential aspirant and Vice-President Al Gore was one of the first national personalities to raise the subject of global warming and the potentiality of an impending climate related catastrophe with the release of his Oscar-winning documentary, An Inconvenient Truth in 2006.

Needless to say, such dire prognostications have gained the attention of both the scientific and political communities. So important is the issue of global warming, in 2016, many different countries around the world agreed to sign the “Paris Agreement,” an accord within the United States Framework on Climate Change (UNFCCC), pertaining to greenhouse gas-emissions and other climate related issues.

The Paris Agreement’s long-range aspiration is to regulate the economy to keep the global average temperature to well below 2°C above pre-industrial levels; and to limit the increase to 1.5 °C, since this, it is claimed, would substantially reduce the risks and effects of climate change.

However, the Paris Agreement has had its detractors, as evidenced by U.S. President Donald Trump who announced in June 2017, that he would withdraw the United States from the agreement.

In the nation of France itself, the Paris Agreement has been controversial and gave impetus to the “Yellow Vests movement,” a populist grassroots protest movement that saw hundreds of thousands of citizens mobilize against French President Emmanuel Marcon and his government for significantly raising taxes at the pump in an effort to reduce fossil fuel consumption out of concerns related to global warming.

Conversely, many political progressives in the United States have decried and protested President Trump’s decision to pull out of the Paris Agreement and have argued that the citizens of earth are sitting on a virtual ticking time bomb and have issued dire warnings that we have just a decade to avert an unparalleled catastrophe of unfathomable proportions.

Some of these progressive politicians and purveyors of the “Green New Deal” have argued that unless the United States government spends trillions of dollars on combating the epic destruction almost certain to come in approximately a decade or a little more, it is almost certain that the world will come to an end due to climate related foods, droughts, epidemics and killer heat waves without parallel in human history.

While I will not contest that we all need to care about the environment and avoid polluting the earth, I find it interesting that those who say that there is an impending climate disaster, keep pushing the date further into the future when such a worldwide cataclysm is supposed to take place.

Case in point: Al Gore distributed his documentary An Inconvenient Truth to the American public in 2006. In that film, Gore argued that the world come to an end in ten years due to global warming from the release of that film.

However, that was thirteen years ago, and we now find ourselves in the year 2019 and the global warming apocalypse has not yet taken place.

Similarly, progressive superstar Rep. Alexandria Ocasio-Cortez (D-N.Y.) said recently that she thinks that there is an urgency needed in addressing man-made climate change, warning that it will “destroy the planet” in a dozen years if humans do not address the issue, no matter the cost.

The fever pitched alarmism over global warming seen in the contemporary progressive circles appears to be a form of “secular apocalypticism,” that foretells that the eminent destruction of the earth is just right around the corner.

The main function appears to be to convince voters and taxpayers to acquiesce to ever-higher taxes to combat climate change. But it has apparently become necessary to keep pushing the date for such an impending climate related catastrophe further and further into the future. As the Steve Miller Band song once said, “Time keeps on slippin’, slippin’, slippin’ into the future.”

via ZeroHedge News https://ift.tt/2FSfpP7 Tyler Durden

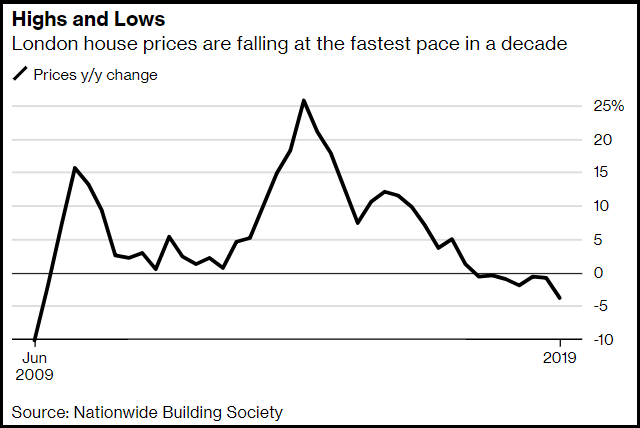

London continued to lead the pack amid the UK’s weakening property market at the start of 2019, according to Bloomberg, which reports that prices have fallen the most since the financial crisis a decade ago.

Values in the capital dropped 3.8% year-over-year according to the Nationwide Building Society, marking the seventh straight decline. The lackluster performance leaves London as the worst-performing region in Britain.

Brexit, of course, is to blame according to some:

Some of weakness relates to Brexit, which is having an impact on sentiment. Consumer confidence remains close to its lowest level since 2013, according to GfK.

The Bank of England said on Friday that mortgage approvals dropped last month. Business investment fell for a fourth quarter at the end of last year, the statistics office said in a separate report.

The uncertainty over when and how the U.K. will leave the European Union has gotten worse this month as the government extended the deadline, having so far failed to get lawmaker approval for its exit deal. Still, a shortage of homes, record employment and low interest rates are preventing an even sharper downturn in the property market. –Bloomberg

It’s not all terrible, however. Nationwide property values rose 0.2 percent in March from February, while the annual rate of change improved to 0.7% from 0.4% – or relatively flat.

As we noted last August, UK house price growth slowed last June to the lowest annual rate in five years according to official figures, likely driven by falling prices in London, Brexit and increasing economic and geo-political uncertainty.

The UK’s annual house price growth rate has been on a downward trajectory since mid-2016.

via ZeroHedge News https://ift.tt/2WCi70B Tyler Durden

Last week, the ECB announced the reintroduction of targeted long-term refinancing operations for the third time. TLTRO-III is scheduled to start from next September. The idea is to make yet more money available for the banks at attractive rates on condition they increase their lending to non-financial entities.

The policy is justified because the ECB sees growing signs the Eurozone economy is stalling, possibly badly. The weaker Eurozone economies are moving into outright recession, and Germany’s motor exports appear to have dramatically slowed, putting a constraint on her whole economy.

The ECB’s reintroduction of TLTRO is an offer of yet more monetary and credit inflation, despite the evidence that unprecedented waves of monetary inflation in the last ten years have failed in all the objectives for which they were designed, except two: governments have continued to get the funds to spend without meaningful restraint, and insolvent banks have been preserved.

Only two months after its asset purchase programme officially ended, the inflationists are at it again. But one wonders why the ECB bothers to delay TLTRO-III until September. If it is such a good thing, why not introduce it now?

There is another explanation, and that is the ECB is intellectually adrift with no economic compass. We do not know how many economists and monetary specialists are employed in the Eurosystem, which includes the ECB and the regional central banks, but they are certainly not economists, otherwise they would understand money. They may be technicians, which is not the same thing. If they were economists, or more precisely properly schooled in the human sub-science of catallactics (the theory of exchange ratios and prices) they would more fully appreciate the consequences of monetary inflation. They would understand Bastiat’s broken window fallacy: it’s not what you see, but what you don’t see. They see the supposed benefits of inflation but appear blind to the strangulating burden imposed on ordinary people who make up the productive economy.

The destruction and transfer of wealth from Eurozone savers to debtors and from the general public to the banks, government and large corporations are the principal and hidden consequences of monetary inflation. Monetary stimulation is progressively destroying Eurozone economies, which coupled with high taxes and excessive regulation has turned the Eurozone into one massive economic zombie. Any student of catallactics learns this early on. Yet, state-employed economists ignore the mathematics of dilution and are unaware of the changes in relative values people place on an unbacked currency, when they finally realise what the central bank is doing to it.

The ECB’s functionaries are similarly ignorant of catallactics as are their confrères in the other major central banks, but that must not excuse them from ignoring the contradictions inherent in their actions. They wield power, and that has responsibilities. Instead, they are trying for a third time a policy, that even if it appears to briefly succeed, emasculates the Eurozone’s economy even more.

Pumping yet more credit into the Eurozone is as effective as giving adrenalin to a dead horse. Lack of credit is not the problem. Put simply, there is a global momentum of economic contraction evolving, which any business and lending banker would be foolish to ignore. There is a developing crisis, the consequence of earlier monetary inflation in the credit cycle. Economic actors may not understand the origins of the crisis, but we can be certain they are becoming acutely aware of its looming presence. And as the crisis rapidly develops, those that require additional loans will already be insolvent.

The signal sent by the ECB to lending-bankers is likely to be misinterpreted when credit contraction is the looming threat: if TLRTO-III is the smoke, there must be a fire, possibly out of control. Better surely to call in existing loans to businesses rather than waiting to be repaid from profits unlikely to materialise. An encouragement to lend early in the credit cycle is more effective and less likely to be misunderstood than a similar encouragement later in the credit cycle. This is why a renewed TLTRO policy will almost certainly fail.

The inability of bureaucrats, with their heads buried in spreadsheets, to appreciate the role of human psychology is not the ECB’s only failing. Its executives do not even understand what interest rates represent, thinking it is simply the price of money. This is why it believes in keeping interest rates suppressed as a means of increasing credit. Earlier in the credit cycle, rate suppression does generate some credit expansion, mainly in financial rather than non-financial activities, because lower interest rates lead to higher prices for financial assets. That is basically a spreadsheet, almost non-human function. Large industrial corporations are opportunist, borrowing to fund buy-backs and to take over weaker rivals. Smaller and medium-sized business borrowers are usually offered credit only later in the cycle, when it is a mistake to accept it.

Consequently, in a zombie economy, such as that of the Eurozone, the only borrowers are wealth-destroying, socialising, debt-entrapped governments, taking full advantage of the Basel accords, which rates them for lending banks’ purposes as riskless borrowers.

The True Role of Interest Rates

Interest is not the price of money. It is a reflection of the difference between future values compared with present values. It has its origin in the human expression of time-preference. When a businessman agrees loan terms with a banker, they should reflect existing time-preference, so as to defer some consumption sufficient to fund investment. Anything else is a distortion with Bastiat-like consequences. Central banks have destroyed the basic function of capital intermediation based on time-preference by replacing savers with money and credit inflation as the principal source of investment capital.

This was wished for by Keynes in his General Theory, published in 1936. He wanted to see savers euthanised (his word) and for the state to provide the necessary capital to businessmen. He expected the entrepreneur to accept state direction of capital. Entrepreneurs “who are so fond of their craft that their labour could be obtained far cheaper that at present” should move from a risk-based approach to business to a socialising function.1

Keynes’s wish is granted posthumously, and ordinary people in the Eurozone and elsewhere are paying for it. Economic strangulation and wealth destruction are the consequence. Functionaries such as Mario Draghi and his fellow directors at the ECB are fully committed to pursuing these Keynesian objectives. Having promised their political masters economic salvation on Keynesian principals, they have delivered instead the Keynesian dream, but at the expense of the economy.

Yet, the deferral of TLTRO-III to September suggests that in the back of their collective minds, the panjandrums at the ECB suspect they may be on a path to perdition. Or perhaps it is the influence of the few sound-money men left at the Bundesbank, across the road in Frankfurt, whose families suffered two currency destructions in the twentieth century and vowed never again.

But even they have been silenced. The protests against the ECB in the German and European courts are in the past. If, as this writer expects, the global economy proves to be on the edge of an abysmal credit crisis, there will be no meaningful objection to a further acceleration of monetary inflation to the point where the euro becomes worthless. If so, Mario Draghi will be identified by future generations as a latter-day Rudolf Havenstein, who famously printed the Reichsmark out of existence.

Unlike the Reichsmark, the euro is a cut-and-shut of a number of fiat currencies with very different time preferences. A knowledge of catallactics would have advised against its creation, proof if it was needed of institutional ignorance in matters of money and exchange. If its origin had been one currency, we could expect its demise to follow the path of all fiat currencies in the past. A single state granting itself the sole right to issue the medium of exchange can never resist the temptation to use it as a source of finance until its destruction. But the euro is a compromise between states with track records of widely different rates of inflation. What suits Germany does not suit Italy. The euro could face a quicker destruction, simply by the Eurozone falling apart.

However, Germany and a few Northern states like her appear trapped, this time through TARGET2 imbalances whereby the Bundesbank is owed approaching a trillion euros by the system. Inflation of money and credit, ultimately the cause of these imbalances, has taken the ECB beyond a point of no return. Inevitably, at some future point, ordinary people will replace their wishful thinking, that the ECB and the national central banks have control over the purchasing power of the euro, with a growing realisation that they don’t. And when they awaken to that reality, they will dump all euros surplus to their essential requirements.

We know that attempts by the authorities to side-step successive credit crises ultimately fail, and it is in that light we should look at TLTRO-III. We must conclude that it is a diversion, window dressing for the shop-front of a failing ECB. It will achieve nothing, because the banks do not want to lend to non-financials, with the exception perhaps of the most credit-worthy large corporations, the corporations that have the political class in their pockets.

It is not just the ECB following economically destructive policies, but an unholy alliance between big business and politicians, which is what Brussels and the ECB is all about.

via ZeroHedge News https://ift.tt/2UaNDpN Tyler Durden

Ukrainian elections are in full farce mode, with a comedian – Volodymyr Zelenskiy – who plays the president on TV leading in the polls (according to exit polls cited by the BBC receiving 30.4% of the vote), and current president Petro Poroshenko is in a distant second with just 17.8%.

Ukrainian comedian and presidential candidate Volodymyr Zelensky, via Pacifica Press.

And that gap between Poroshenko and Zelenskiy does not look like narrowing anytime soon.

The average monthly salary in Ukraine in September 2018 was 9,042 hryvnia (about $320), according to the country’s State Statistics Service.

Poroshenko’s fortune totaled 1.56 billion hryvnia (US$57 million) over 12 months through March 31, which is 95 times as much as he reported in the same period a year ago. In 2017, Poroshenko’s gains reportedly reached 16.3 million hryvnia ($600,000).

Meanwhile, his official paycheck totals $12,400.

However, as RT reports,most of Poroshenko’s income – around $40.4 million – reportedly comes from return on investment in Zurich-based Rothschild Trust Schweiz, a trust subsidiary of Rothschild Bank AG.

As no candidate received an absolute majority in the first round of elections, the Ukrainian Central Election Commission is set to hold the second round on April 21.

Of course, none of this matters, as we await to discover who Washington wants installed.

via ZeroHedge News https://ift.tt/2WEX11z Tyler Durden

Former Paterson, New Jersey, police officer Ruben McAusland has been sentenced to five years in prison for drug dealing and

Former Paterson, New Jersey, police officer Ruben McAusland has been sentenced to five years in prison for drug dealing and

{kind=link}

{kind=link}