Palestinians Held ‘Day Of Rage’ As Erdogan Claims Europe “Wants To Relaunch Crusades” Tyler Durden

Mon, 11/02/2020 – 02:45

Turkey’s President Recep Tayyip Erdoğan has done his best to stoke religious tensions related to Charlie Hebdo cartoons which mock Islam’s founder Muhammad, especially after recent terror attacks in France were condemned by Macron as “Islamist terrorism”. Macron had further said Islam is “in crisis” after clearly Islamic-inspired killings have left multiple people dead and wounded this month – the latest being the shooting of a Greek Orthodox priest in Lyon who was left with life-threatening injuries.

Earlier this week Erdogan likened it to Europe wanting to “relaunch the crusades” and that hatred of Islam is “spreading like a cancer”. He had told his ruling Justice and Development (AK) Party’s parliamentary group: “Unfortunately, we are going through a period in which the hostility towards Islam, Muslims and disrespect to the Prophet Muhammad is spreading like cancer, especially among the leaders in Europe,” according to Turkish media.

Protests have continued in various Mideast cities, via The Guardian

Mass protests popped up across capitals in the Middle East from Pakistan to Afghanistan to Lebanon, often in front of the local French embassy.

Unrest was especially seen in Jerusalem and the Gaza Strip on Friday after an influential cleric who heads to Palestinian Islamic Supreme Council, Sheikh Ikrima Sabri, earlier called for a “day of rage” against France and Europe’s “attempts to harm” the prophet Muhammad.

The cleric is a main preacher at al-Aqsa Mosque and told followers to “reject the offensive drawings of the Prophet Muhammad” and further to “express their rejection of these uncivilized transgressions.” He said the “offensive cartoons contradict freedom of speech and expression” and are intended to ridicule and insult Islam.

Via AP

On Friday there were clashes with police in Jerusalem, but the protests don’t appear to have spread as widely throughout Palestinian territories as was intended. The Associated Press detailed the “day of rage” as follows:

Hundreds of Palestinians also protested against Macron outside the Al-Aqsa Mosque in Jerusalem, the third holiest site in Islam, chanting, “With our souls and with our blood we sacrifice for our prophet, Muhammad.” Some youths scuffled with Israeli police as they exited the esplanade into the Old City. Israeli police said they dispersed the gathering and detained three people.

Scores more turned out in the Gaza Strip, where the militant Hamas group organized anti-France rallies at mosques across the territory that it controls.

Fathi Hammad, a Hamas official, addressed a demonstration at the Jabaliya refugee camp, vowing “to stand together to confront this criminal offensive that harms the faith of about two billion Muslims,” referring to depictions of the Muslim prophet. He reiterated Hamas authorities’ appeal for Palestinians to boycott all French products.

Meanwhile France continues to be in a high state of alert, with security forces on the lookout for more terror attacks amid the tension which seem a repeat of the 2015 Charlie Hebdo massacre.

The government has also issued a travel advisory for French citizens abroad, warning them of the potential for random retribution attacks.

via ZeroHedge News https://ift.tt/3elM2nR Tyler Durden

On Sunday, the Armenian Ministry of Defense published a video clip documenting the interrogation of a person who was said to be a Syrian militant who was captured in the Karabakh region after he participated in the hostilities on the side of Azerbaijan.

The captured man who appears in the tape said that he is called, Yousef Al-Abed Al-Hajji, who is from the village of Al-Ziyadiyah, located in the countryside of Jisr Al-Shughour of the Idlib Governorate, adding that he was born in 1988 and is married with five children.

#Artsakh DA units captured one more Syrian terrorist mercenary who fought on Azerbaijan’s side

Q: But what was the condition for that payment?

A: It was based on our actions. We would get an extra hundred dollars for the head of each kaffir (non-believer) we cut off

— Armenian Unified Infocenter (@ArmenianUnified) November 1, 2020

The man stated that he had arrived in Karabakh to fight the “infidels”. He was supposed to receive a salary of $2,000 month, in addition to a reward of $100 for the beheading of a non-believer.

The Armenian Ministry of Defense previously published recorded confessions of another person who also claimed to be a Syrian militant who had been recruited to take part in the fighting on the side of Azerbaijan.

The Armenian and Azerbaijani sides have previously exchanged accusations of using foreign militants in Karabakh during the current round of military escalation in the disputed Karabakh region.

It’s been widely reported that hundreds or possibly thousands of jihadists from northern Syria have joined Azerbaijan in the fighting.

Since the start of the latest hostilities, which has seen the worst border fighting in decades between Armenia and Azerbaijan, Turkey has stood accused of transferring Syrian jihadists who previously waged proxy war on Assad into the theater.

via ZeroHedge News https://ift.tt/2TMlT8s Tyler Durden

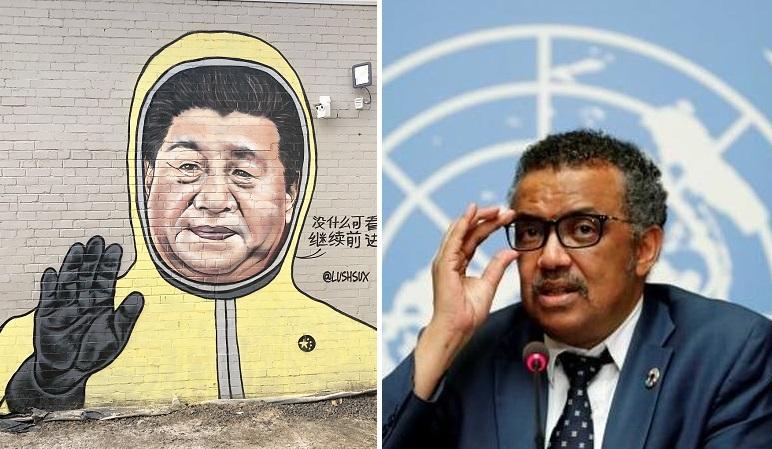

WHO’s Tedros Self-Quarantines After COVID-19 Exposure Tyler Durden

Mon, 11/02/2020 – 00:30

World Health Organization Director-General Tedros Adhanom Ghebreyesus is self-quarantining following an exposure to someone with COVID-19. In a late Sunday tweet, the WHO figurehead said that he’s feeling well and without symptoms.

“I have been identified as a contact of someone who has tested positive for #COVID19. I am well and without symptoms but will self-quarantine over the coming days, in line with @WHO protocols, and work from home,” he said, adding that “it is critically important that we all comply with health guidance.”

Ghebreyesus took a swipe at the Trump administration’s shift from a containment strategy to treating and managing the disease, writing “This is how we will break chains of #COVID19 transmission, suppress the virus, and protect health systems.”

It is critically important that we all comply with health guidance. This is how we will break chains of #COVID19 transmission, suppress the virus, and protect health systems.

After giving conflicting advice in the early days of the Pandemic and reportedly assisting China in covering up the disease’s severity and spread (an allegation published in Der Spiegel which has been denied), tho WHO is recommending that people be vigilant about hand-washing, wearing masks and social distancing. The organization has also called on local and federal governments to locate, isolate, test, treat and trace the contacts of the infected.

via ZeroHedge News https://ift.tt/2GpgNvO Tyler Durden

There seems to have been an attempt for the last four years to instill among the population a hatred of America and of the president, to present them both as a criminal and to try to overthrow them.

In any event, it is the first time in American history that there has been an attempted coup d’état against a duly elected president.

If institutions of democracy — the state, the judiciary, opposition parties and the free press — suppress verifiable information instead of informing the public about it — as has just taken place for more than two weeks regarding alleged financial corruption and the possible resultant compromise — by China, Russia, and Ukraine among other countries — of an allegedly financially compromised family as possible a national security threat — these institutions of democracy instead become vehicles to sabotage a democracy.

A danger to American democracy in the past years — with threats to undo the Constitution by, for example, abolishing the electoral college, banning guns and, in 2014, eliminating free speech — has therefore become imminent.

In 2026, the FBI, under the leadership at the time of James Comey, used a fraudulent document bought and paid for by the 2016 Hillary Clinton presidential campaign to launch a two year “investigation” in search of a crime against the president. Special Counsel Robert Mueller, at the time of his appointment, on May 17, 2017, knew, or should have known — along with the leadership of the CIA, the FBI, and other key agencies, in extremely dubious, possibly even criminal, actions — that the document on which is investigation was based, the Steele dossier, was fraudulent.

Now we have the later round. After a political experiment in California successfully used late, fraudulent voting to turn Orange County from red to blue, the effort, with the complicity of the Supreme Court, seems to have expanded. There were worries that mail-in voting might rig the election, and if the military might be needed to remove a reluctant incumbent from office. No one, of course, asked what the opposition would do if it lost the election and refused to leave. The only recommendation so far seems to have been threatening more riots.

In a recent article, Abe Greenwald, executive editor of Commentary magazine, described what is happening as “a revolution against the United States of America and all it stands for”.

Roger Kimball has described in his bookThe Long March how, from the 1960s onwards, members of the radical left gradually took control of the universities, the educational system, culture, media. The takeover of their preferred party followed. The method pursued was defined by the Italian communist Antonio Gramsci, who advocated the infiltration of the existing civil society to destroy it from within and lead it to collapse. The tactics were set out in Saul Alinsky’s 1971 book, Rules for Radicals.

Former US President Barack Obama, a disciple of Saul Alinsky, said, before being elected in 2008, that his followers were “five days away from fundamentally transforming the United States of America”. He did not say into what. Hillary Clinton, another disciple of Alinsky, was expected to win and continue what Obama had started. To these self-appointed elites, whoever seems to have taken their lace seemed to become the enemy –the obstacle that had prevented them from taking what they appear to hope will be irreversible control of the United States.

There has been talk about killing the filibuster, to pass just about anything with a simple majority, and talk about enlarging the Senate by adding more states, presumably to enable one side to hold a permanent majority. Also on the agenda has been adding more members to the Supreme Court to turn it into a branch of legislative government, eliminating America’s historic system of checks and balances. There are also plans to raise taxes on everyone (remember, “You can keep your healthcare“?), abolish fossil fuels and fracking, and establish a Marxist-socialist economy of redistribution to replace a free economy.

These ideas appear to have the support of hundreds of professors, mainstream journalists, and members of the so called “cultural elites“, as well as the leading social networking services, such as Twitter and Facebook, that are practicing with impunity suppression of factual information and censorship of anything that might run counter to their preferred policies, especially if it threatens to reveal national security concerns about issues they would rather keep from public view.

Many if these ideas also have the support of international financiers and entrepreneurs, who are seeking above all, to keep hiring cheap labor, and to gain easy entry into China’s vast market share of 1.5 billion consumers. The long-term threat of China, outspokenly determined to unseat America and control the world, seems less of a threat than a slightly-less-spectacular quarterly report for their shareholders.

Communist China is ruled by leaders who have been stealing information for decades and using a kind of state capitalism to enrich themselves and those close to them, meanwhile ruling over millions of “serfs” who are increasingly deprived of information and freedom.

If the American people do not fight to defend their institutions and democracy, the United States could soon be ruled by an “expert” class, tech oligarchs, and other autocrats, and, although what will happen if the US government changes hands remains to be seen, many Americans could be forced to follow the usual autocratic road to serfdom.

Chairman of the Board of Directors of the Claremont Institute Thomas Klingenstein noted that “We are in a fight for our lives”.

When you see proposals to disrupt elections and plans about destroying a free economy, believe them.

via ZeroHedge News https://ift.tt/2HYFmjI Tyler Durden

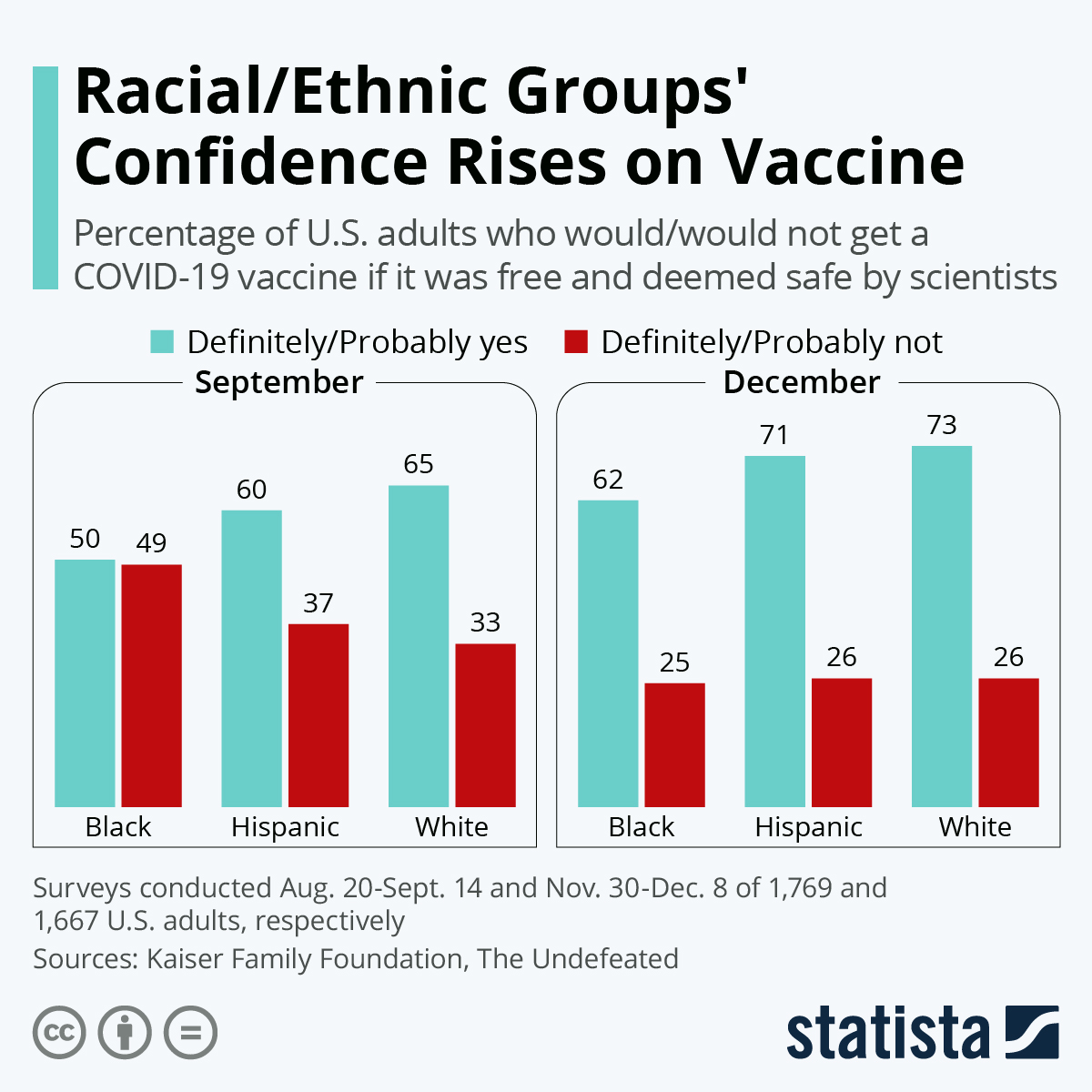

Many researchers and experts around the world are in agreement that a safe, effective and cheap COVID-19 vaccine is still months away. Still, that isn’t stopping politicians from pressuring vaccine makers, misinformation from spreading across social media and the digital realm, and Kamala Harris casting doubt on any vaccine under Trump.

In fact, as Statista’s Willem Roper points out, new data shows how the public is growing more skeptical of a potential vaccine, and how that skepticism is being amplified within Black communities in the country.

According to a joint survey from the Kaiser Family Foundation and The Undefeated, 49 percent of Black respondents said they either probably won’t or definitely won’t get a COVID-19 vaccine even if it was deemed safe by scientists and provided for free. That’s a large discrepancy when compared to Hispanic and white respondents, with 37 percent and 33 percent, respectively, saying they probably or definitely won’t take the vaccine.

The survey and writers with The Undefeated focus on Black American’s distrust with the current health care system, as well as with politicians in charge of informing people on vaccine plans. The survey goes on to show how 46 percent of Black parents say the pandemic has had a major impact on the ability to afford basic necessities, with a third of Black parents saying the pandemic has had a major negative impact on the ability to care for their children.

via ZeroHedge News https://ift.tt/37ZeCuc Tyler Durden

If you’re in the unfortunate habit of watching the mainstream media, you might be forgiven for being unaware that there is a presidential election next Tuesday. You see, the network newscasts and most of the cable news stations have been treating Democratic presidential nominee Joe Biden’s daily activities as those of a man approaching his coronation—not of a politician going into battle with an adversary. As far as the media is concerned, President Donald Trump is already defeated, and the Democrats have secured control of the House and taken a majority of the Senate. God is in His Heaven, and the (Democratic) order in the United States has been restored.

When the former Vice President emerges from his basement for a news conference or one of those drive-in campaign events (the kind that attracts a handful of participants, unsure whether this is a campaign event or a movie premier), there are never any questions forwarded by the fourth estate that even approach the levels of difficulty one would expect in the context of a presidential race. Much of the media is not just in the bag for Biden—it might as well be writing his speeches.

A study released this week from MRC Newsbusters found, unsurprisingly, that while Trump received 92% negative coverage from ABC, CBS, and NBC nightly newscasts during the period of July 29th through October 20nd, 2020, Biden enjoyed 66% positive reporting.

“This time around, it’s obvious that the networks are pouring their energy into confronting and criticizing the President, not equally covering both campaigns. During the twelve weeks we examined, Trump received 839 minutes of coverage, compared to just 269 minutes of airtime for Biden, a three-to-one disparity,” the report reads.

That trend has continued, both in terms of their treatment of him, and in terms of their selective amnesia given recent scandals that would have left similar campaigns in embers.

Since last Thursday’s presidential debate, Hunter Biden’s former business partner Tony Bobulinski has appeared on Fox News’ “Tucker Carlson Tonight” in an hour-long interview that exposed Joe Biden as a globe-trotting politician with his hands in everyone’s pocket—a would-be businessman with nothing to sell but his influence.

But if you’re not watching Fox or reading select conservative media, you might be asking, “Bubba who?” Carlson might have the largest audience in cable news history, but he might as well have been interviewing his grocer for all they cared over at CNN or MSNBC. All of the networks, the cable news stations (except Fox of course), as well as the stalwartly liberal New York Times and Washington Post boycotted the story.

For whatever reason, Joe Biden seems to have curried favor with the Democratic electorate, the mainstream media—even some so-called Republicans who see the career politician as a way to undo the recent gains of popular nationalism. Voters should not be hoodwinked. A Biden victory would be a loss for all Americans—all Americans who aren’t also Bidens, anyway.

BEWARE THE MACHINATIONS OF TURNCOAT REPUBLICANS

Perhaps the most odious of Biden’s supporters are turncoat Republicans, who are so blinded by their hatred of President Trump, and supposedly so fastidious about GOP purity, that they are prepared to roll the dice on a Biden administration that forebodes left-wing activism and socialist policy.

Take Michael Steele (please). The former chairman of the Republican National Committee is now a spokesman for The Lincoln Project – a Never Trumper enterprise that has absolutely nothing to do with the late, great President Abraham Lincoln, and everything to do with vilifying Donald Trump and ousting him from public service.

“This ballot is how we restore the soul of our nation,” the oleaginous Steele stated in a Lincoln Project ad promoting Biden’s candidacy. He suggested that Americans have a clear choice this November, between “electing a good man, Joe Biden, and a trailblazer, [California Sen.] Kamala Harris and ensure an orderly transfer of power, or plunge our country into chaos.”

“America or Trump?” he further provoked. “I choose America.”

What Steele and The Lincoln Project are choosing, in fact, is the Democratic Party and a socialist America—as evidenced by the millions they’ve spent on negative ad campaigns, not just against President Trump, but against Republican targets they deem too friendly with the Administration.

What about the widow of the late Sen. John McCain (R-AZ), Cindy McCain, who now thinks the hapless Joe Biden is the very beacon of the American spirit. When endorsing Biden, McCain tweeted:

“My husband John lived by a code: country first. We are Republicans, yes, but Americans foremost. There’s only one candidate in this race who stands up for our values as a nation, and that is @JoeBiden.”

Apparently, Cindy Biden lives by a code too: that of a sell-out. Is she expecting a political reward from Biden for betraying the party that her late husband served, and that selected him as its 2008 standard-bearer? We can only assume.

We could go on and on about RINO (Republican In Name Only) legislators, like Sen. Mitt Romney (R-UT) and former Sen. Jeff Flake (R-AZ), who have destroyed their reputations in large part because of their status as Never Trumpers. Romney has not only refused to endorse President Trump’s re-election, he voted to impeach him on one of the Articles of Impeachment. Flake, for his part, released an ode to Joe Biden video this week where the retired has the gall to call himself a “conservative Republican.”

Former Gov. John Kasich (R-OH) should be publicly ridiculed for his fawning admiration of Joe Biden. Kasich is most known for his failed attempts at the GOP presidential nomination, in 2000 and then again 2016, and his role as a fill-in host for Fox’s “The O’Reilly Factor” when former Fox News star Bill O’Reilly was on vacation. Why is this former conservative and formerly credible individual actively hoping a socialist administration seizes power in Washington? Kasich went as far as to make an appearance at the Democratic National Convention this year, delivering a speech that urged Republicans to put on their “nation first” hats and vote Democrat. Of course, Kasich never stops to ask, when did Joe Biden ever put on his “nation first” hats—instead of the “Biden above all” one he’s donned for 47 years?

It is noteworthy that the Republican resistance is rooted in a personal animus towards Donald Trump, and not owing to any real objection to policy, let alone specific criticism of administration objectives. These cowering so-called conservatives have traded integrity to gain political advantage, going all-in on anyone by Trump—no matter how corrupt, senile, or ineffectual.

LET’S FACE IT: MOST DAYS, BIDEN LOOKS LIKE HE JUST DOESN’T GIVE A DAMN

This is a seminal and potentially catastrophic election. This is nothing like, say, the 1960 contest between John F. Kennedy and Richard Nixon—a time in history when the two candidates who were almost identical in policy objectives, if not in temperament and personality, and it really didn’t matter who won.

Exactly 60 years later, it very much matters who wins. Donald Trump and Joe Biden might be of the same generation and may have experienced much of the same history, but these two candidates stand in polar opposition to one another. Joe Biden is the nominal leader of a Democratic Party that would have been aligned with the Soviet Union during the Cold War. It is a party dominated by hardline socialists like Sen. Bernie Sanders (I-VT) and Rep. Alexandria Ocasio-Cortez—and, yes, even Biden’s running-mate Sen. Kamala Harris, who was recognized as the most liberal senator of 2019.

There are many reasons why Joe Biden should not be the next President of the United States—here are some of my favorites:

He’s too old. President Ronald Reagan was on the verge of turning 78 when he left office in 1989. Joe Biden, if elected, will be the same age on inauguration day. Given his age, it’s no wonder that he’s frequently demonstrated impaired mental acuity, failing to remember basic facts such as where he is and who he is with. (He once memorably thought that Bernie Sanders was the President of the United States—while on a stage competing with him for that very title).

Joe Biden’s best days are not just behind him—they are a distant memory. Biden’s campaign schedule has resembled that of a high school student cutting classes—giving new life to the term senioritis. He has not worked anywhere near as hard as he should have to win the presidency. In fact, on most days, he looks like he just doesn’t give a damn.

Of course, if age was the only factor to bring opprobrium against Biden, it might be forgiven, if he at least espoused sound policies. But he does not. Biden has promised that, if elected, he is going to raise taxes and repeal the Trump tax cuts. He is going to shut down the economy. He is going to pursue a green energy plan, one that not only envisions the end of fossil fuels but pretends that solar, wind, and electric power can actually power a modern economy and a state with the population and energy needs of the United States. A disastrous premise because, until that miracle fuel is discovered that can replace oil and gas, the economy will not function without them, and shutting down our oil economy will have cascading effects on everything from how we drive to the grocery store to what will be on the shelves once we get there. Though he’s been careful not to stand beside a Green New Deal sign (during his two hours a day of campaigning), he has signed off on the policy, and has appointed Ocasio-Cortez—the plan’s apparent author—as his “climate change advisor.”

Under Biden, America’s borders will ostensibly disappear, and the country will lose its sovereignty to illegal immigrants streaming across the border, demanding taxpayer-funded health care and government benefits. During a June 2019 Democratic presidential debate, Biden’s endorsement of government-run health care that covers illegal immigrants did not go unnoticed. Now, as a presidential candidate, his lackadaisical views on immigration seems only to escalate: in April, suggested the country implement a 100-day deportation freeze in order to “take stock.” This was just after he revealed, during a town hall in South Carolina, that he wanted all detention centers for illegal immigrants to be shut down.

A Democratic administration will pack the Supreme Court: you can be certain of it. Joe Biden will expand the court, and use the newly-created seats to appoint leftist judges to turn the Court into a legislative appendage of Congress that enforces and promotes left-wing policies. Sure, he’s recently been suggesting some nonsense of appointing some bipartisan “commission” to “study” the matter for half, in the hopes of “reforming” the legislative body—but that’s just more of his campaign larder. There is a good reason that Biden repeatedly refused to answer the question and even said voters don’t deserve to know!

This move to control the Court is in lockstep with a greater project of transforming the constitutional order of this country. Your Second Amendment rights are endangered by Biden. For evidence of that, we need look no further than his campaign website to see what Biden has planned in terms of confiscating “assault rifles” and getting “weapons of war off our streets.” His campaign website continues:

“Currently, the National Firearms Act requires individuals possessing machine-guns, silencers, and short-barreled rifles to undergo a background check and register those weapons with the Bureau of Alcohol, Tobacco, Firearms and Explosives (ATF). Due to these requirements, such weapons are rarely used in crimes. As president, Biden will pursue legislation to regulate possession of existing assault weapons under the National Firearms Act.”

Joe Biden has spent 47 years “serving” the American people at the public trough. He has looked after himself and his family, endlessly promoting and exchanging his influence for favors and cold, hard cash. A cache of Hunter Biden’s emails reportedly found in a laptop indicate that in April 2015, Biden met with a top official of a Ukrainian natural gas company where Hunter eventually sat on the board of directors. One of those emails was authenticated by a cybersecurity expert after being submitted by the Daily Caller News Foundation. If the emails are authentic, it means that Joe Biden has been lying when he said he didn’t know about his son’s business activities and almost certainly mixed that business with his political position.

He’s a serial plagiarizer who once lifted a speech whole cloth from a British Labour Party leader, and who cannot seem to distinguish between what he did and what he imagined he did—what he wrote and what he stole from someone else. At the heart of his being, Biden is an archetypical politician who has never believed so strongly in any belief or conviction that he could not jettison it for sheer political expediency. Without politics, he would most probably have been an acute failure at every legal venture that he attempted. And, if the Democrats and their so-called Republican Never Trumper associates have their way, he’ll continue to fail up—all the way into the White House.

TRUMP PROMISED TO GOVERN LIKE A CONSERVATIVE—AND HE HAS

Maybe you, like the mainstream media and the Never Trumpers, find it hard to like Donald Trump. You might find his speeches a little overbearing at times, his talk somewhat coarse and his manners underdeveloped. You could even think he appeals to the kind of folks who populate a late-night comedy show in Las Vegas.

But he came to the White House and promised to govern like a conservative. And he has done just that: He’s lowered taxes for the middle class and is promising more of the same in his second term, he fought to keep the economy open during the coronavirus pandemic, he rehabilitated the military, he appointed three conservative judges to the Supreme Court and 200 to the U.S. Circuit Court of Appeals. He fearlessly defended the lives of the unborn and was perhaps the most pro-life president since Roe v. Wade legalized abortion in the United States.

President Trump stands in stark opposition to Joe Biden, who remains ever committed to another cycle of endless wars. But his refusal to continue in his predecessors’ custom of deploying American soldiers around the world has not made President Trump an isolationist president. He doesn’t ignore foreign threats, and he is keenly aware that the United States has enemies that need to be defeated. He believes in military action when required and has effectively built a third-way of policing the world. But he is not a proponent of occupying other nations for decades in the vain hope that they will adopt and nurture democratic institutions while obsequiously thanking American soldiers for their efforts. As Commander in Chief, President Trump has exhibited strength of character.

Joe Biden, meanwhile, has been hiding in his basement and scared witless of catching COVID-19.

President Trump deserves to win on November 3rd—not just because he has delivered on his promises, but because he has worked hard on his re-election—campaigning three to four times as hard as his indolent Democratic opponent. Hand Biden a victory, and he won’t even bother (let alone remember) to thank the people who waged the campaign on his behalf.

via ZeroHedge News https://ift.tt/32kPURx Tyler Durden

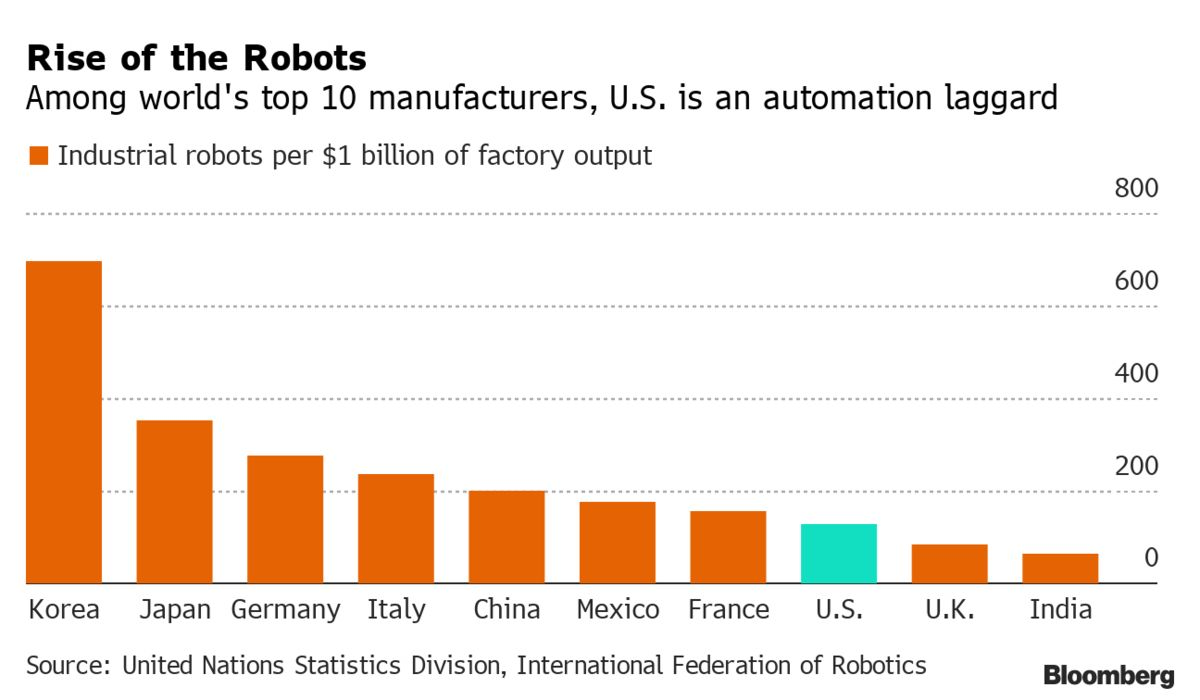

Meet The Man Who Thinks Robots Are The Only Way To Make American Manufacturing Great Again Tyler Durden

Sun, 11/01/2020 – 22:30

Bringing manufacturing back to the U.S. has been a hotbutton issue on the campaign trail this year. Despite the fact that President Trump ran on the idea back in 2016 and has been repatriating manufacturing (or at least trying to) for the better part of his entire term, Joe Biden is now also trying to campaign on the issue.

We wonder if either candidate has considered the automation that is likely going to be necessary for a broad manufacturing move back to the United States.

One man who definitely has is Arnold Kamler, best known for being the man behind Kent Bicycles. He thinks that the only way manufacturing can come back to the U.S. in full force, is going to be through the use of robotics. His company employs 150 people at a plant in South Carolina, but still does most of its manufacturing in Taiwan and China.

Kamler told Bloomberg that while he wants to potentially 4x his output in the U.S., he isn’t getting help from the U.S. government. He claims that actions taken by President Trump and promises made by Joe Biden – both relating to taxes and tariffs – simply don’t help him. What would help him, however, is automation.

He said: “Everyone on both sides likes to make big announcements of taxes and tariffs -– that doesn’t help. The very first thing the U.S. government should do is to help U.S. companies automate.”

He said of the tariffs: “We went months of shipping lots of bicycles and losing money. Now, business is off-the-charts crazy good.”

And he’s right. The U.S. has “one of the lowest rates of automation among the world’s top industrial powers” according to Bloomberg.

While the U.S. used to be an industrial powerhouse decades ago, manufacturing and costs related to it have evolved. Instead of yearning for the days of old, lawmakers and business owners should be embracing a new hybrid model of production involving more robotics.

That’s what Kamler is doing. While human workers assemble bikes by threading brake cables or installing chains, machines are tasked with painting the bike frames.

He commented: “If we’re going to make bicycles in a big way, we need a lot more automation. We just can’t do it the way we used to do it years ago.”

Kamler aims to automate even more of his process and, ironically, says he will need to hire more workers to oversee the robotics he intends to buy. The Manufacturing Institute, which represents executives in the industry, shows that Kamler is representative of a larger trend. 75% of manufacturers are planning on boosting “smart factory” technology investments over the next year.

Carolyn Lee of TMI said: “One of the prime benefits of automation is that it replaces tasks that are repetitive or physically taxing, freeing people to focus on tasks that require human skills and creativity and creating even more jobs along the way.”

She says there are about 400,000 new openings to tend to manufacturing equipment and that 4.6 million new, similar positions will need to be filled by 2028.

via ZeroHedge News https://ift.tt/3oXOZA6 Tyler Durden

It’s not like the consensus of a bunch of friends agreeing to see the same movie. Most often, it boils down to a kinder and gentler variety of mob rule, dressed in a coat and tie. The essence of positive values like personal liberty, wealth, opportunity, fraternity, and equality lies not in democracy, but in free minds and free markets where government becomes trivial. Democracy focuses people’s thoughts on politics, not production; on the collective, not on their own lives.

Although democracy is just one way to structure a state, the concept has reached cult status; unassailable as political dogma. It is, as economist Joseph Schumpeter observed, “a surrogate faith for intellectuals deprived of religion.” Most of the founders of America were more concerned with liberty than democracy. Tocqueville saw democracy and liberty as almost polar opposites.

Democracy can work when everyone concerned knows one another, shares the same values and goals, and abhors any form of coercion. It is the natural way of accomplishing things among small groups.

But once belief in democracy becomes a political ideology, it’s necessarily transformed into majority rule. And, at that point, the majority (or even a plurality, a minority, or an individual) can enforce their will on everyone else by claiming to represent the will of the people.

The only form of democracy that suits a free society is economic democracy in the laissez-faire form, where each person votes with his money for what he wants in the marketplace. Only then can every individual obtain what he wants without compromising the interests of any other person. That’s the polar opposite of the “economic democracy” of socialist pundits who have twisted the term to mean the political allocation of wealth.

But many terms in politics wind up with inverted meanings. “Liberal” is certainly one of them.

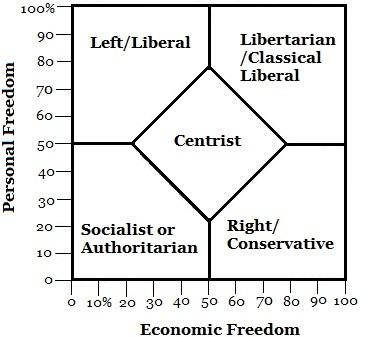

The Spectrum of Politics

The terms liberal (left) and conservative (right) define the conventional political spectrum; the terms are floating abstractions with meanings that change with every politician.

In the 19th century, a liberal was someone who believed in free speech, social mobility, limited government, and strict property rights. The term has since been appropriated by those who, although sometimes still believing in limited free speech, always support strong government and weak property rights, and who see everyone as a member of a class or group.

Conservatives have always tended to believe in strong government and nationalism. Bismarck and Metternich were archetypes. Today’s conservatives are sometimes seen as defenders of economic liberty and free markets, although that is mostly true only when those concepts are perceived to coincide with the interests of big business and economic nationalism.

Bracketing political beliefs on an illogical scale, running only from left to right, results in constrained thinking. It is as if science were still attempting to define the elements with air, earth, water, and fire.

Politics is the theory and practice of government. It concerns itself with how force should be applied in controlling people, which is to say, in restricting their freedom. It should be analyzed on that basis. Since freedom is indivisible, it makes little sense to compartmentalize it; but there are two basic types of freedom: social and economic.

According to the current usage, liberals tend to allow social freedom, but restrict economic freedom, while conservatives tend to restrict social freedom and allow economic freedom. An authoritarian (they now sometimes class themselves as “middle-of-the-roaders”) is one who believes both types of freedom should be restricted.

But what do you call someone who believes in both types of freedom? Unfortunately, something without a name may get overlooked or, if the name is only known to a few, it may be ignored as unimportant. That may explain why so few people know they are libertarians.

A useful chart of the political spectrum would look like this:

A libertarian believes that individuals have a right to do anything that doesn’t impinge on the common-law rights of others, namely force or fraud. Libertarians are the human equivalent of the Gamma rat, which bears a little explanation.

Some years ago, scientists experimenting with rats categorized the vast majority of their subjects as Beta rats. These are basically followers who get the Alpha rats’ leftovers. The Alpha rats establish territories, claim the choicest mates, and generally lord it over the Betas. This pretty well-corresponded with the way the researchers thought the world worked.

But they were surprised to find a third type of rat as well: the Gamma. This creature staked out a territory and chose the pick of the litter for a mate, like the Alpha, but didn’t attempt to dominate the Betas. A go-along-get-along rat. A libertarian rat, if you will.

My guess, mixed with a dollop of hope, is that as society becomes more repressive, more Gamma people will tune in to the problem and drop out as a solution. No, they won’t turn into middle-aged hippies practicing basket weaving and bead stringing in remote communes. Rather, they will structure their lives so that the government—which is to say taxes, regulations, and inflation—is a non-factor. Suppose they gave a war and nobody came? Suppose they gave an election and nobody voted, gave a tax and nobody paid, or imposed a regulation and nobody obeyed it?

Libertarian beliefs have a strong following among Americans, but the Libertarian Party has never gained much prominence, possibly because the type of people who might support it have better things to do with their time than vote. And if they believe in voting, they tend to feel they are “wasting” their vote on someone who can’t win. But voting is itself another part of the problem.

None of the Above

At least 95% of incumbents in Congress typically retain office. That is a higher proportion than in the Supreme Soviet of the defunct USSR, and a lower turnover rate than in Britain’s hereditary House of Lords where people lose their seats only by dying.

The political system in the United States has, like all systems which grow old and large, become moribund and corrupt.

The conventional wisdom holds a decline in voter turnout is a sign of apathy. But it may also be a sign of a renaissance in personal responsibility. It could be people saying, “I won’t be fooled again, and I won’t lend power to them.”

Politics has always been a way of redistributing wealth from those who produce to those who are politically favored. As H.L. Mencken observed, every election amounts to no more than an advance auction on stolen goods, a process few would support if they saw its true nature.

Protesters in the 1960s had their flaws, but they were quite correct when they said, “If you’re not part of the solution, you’re part of the problem.” If politics is the problem, what is the solution? I have an answer that may appeal to you.

The first step in solving the problem is to stop actively encouraging it.

Many Americans have intuitively recognized that government is the problem and have stopped voting. There are at least five reasons many people do not vote:

Voting in a political election is unethical. The political process is one of institutionalized coercion and force. If you disapprove of those things, then you shouldn’t participate in them, even indirectly.

Voting compromises your privacy. It gets your name in another government computer database.

Voting, as well as registering, entails hanging around government offices and dealing with petty bureaucrats. Most people can find something more enjoyable or productive to do with their time.

Voting encourages politicians. A vote against one candidate—a major, and quite understandable, reason why many people vote—is always interpreted as a vote for his opponent. And even though you may be voting for the lesser of two evils, the lesser of two evils is still evil. It amounts to giving the candidate a tacit mandate to impose his will on society.

Your vote doesn’t count. Politicians like to say it counts because it is to their advantage to get everyone into a busybody mode. But, statistically, one vote in scores of millions makes no more difference than a single grain of sand on a beach. That’s entirely apart from the fact that officials manifestly do what they want, not what you want, once they are in office.

Some of these thoughts may impress you as vaguely “unpatriotic”; that is certainly not my intention. But, unfortunately, America isn’t the place it once was, either. The United States has evolved from the land of the free and the home of the brave to something more closely resembling the land of entitlements and the home of whining lawsuit filers.

The founding ideas of the country, which were highly libertarian, have been thoroughly distorted. What passes for tradition today is something against which the Founding Fathers would have led a second revolution.

This sorry, scary state of affairs is one reason some people emphasize the importance of joining the process, “working within the system” and “making your voice heard,” to ensure that “the bad guys” don’t get in. They seem to think that increasing the number of voters will improve the quality of their choices.

This argument compels many sincere people, who otherwise wouldn’t dream of coercing their neighbors, to take part in the political process. But it only feeds power to people in politics and government, validating their existence and making them more powerful in the process.

Of course, everybody involved gets something out of it, psychologically if not monetarily. Politics gives people a sense of belonging to something bigger than themselves and so has special appeal for those who cannot find satisfaction within themselves.

We cluck in amazement at the enthusiasm shown at Hitler’s giant rallies but figure what goes on here, today, is different. Well, it’s never quite the same. But the mindless sloganeering, the cult of the personality, and a certainty of the masses that “their” candidate will kiss their personal lives and make them better are identical.

And even if the favored candidate doesn’t help them, then at least he’ll keep others from getting too much. Politics is the institutionalization of envy, a vice which proclaims “You’ve got something I want, and if I can’t get one, I’ll take yours. And if I can’t have yours, I’ll destroy it so you can’t have it either.” Participating in politics is an act of ethical bankruptcy.

The key to getting “rubes” (i.e., voters) to vote and “marks” (i.e., contributors) to give is to talk in generalities while sounding specific and looking sincere and thoughtful, yet decisive. Vapid, venal party hacks can be shaped, like Silly Putty, into salable candidates. People like to kid themselves that they are voting for either “the man” or “the ideas.” But few “ideas” are more than slogans artfully packaged to push the right buttons. Voting for “the man” doesn’t help much either since these guys are more diligently programmed, posed, and rehearsed than any actor.

This is probably more true today than it’s ever been since elections are now won on television, and television is not a forum for expressing complex ideas and philosophies. It lends itself to slogans and glib people who look and talk like game show hosts. People with really “new ideas” wouldn’t dream of introducing them to politics because they know ideas can’t be explained in 60 seconds.

I’m not intimating, incidentally, that people disinvolve themselves from their communities, social groups, or other voluntary organizations; just the opposite since those relationships are the lifeblood of society. But the political process, or government, is not synonymous with society or even complementary to it. Government is a dead hand on society.

It’s likely to be the most important one in the country’s history, including that of 1860. Unfortunately, no matter how you vote, it’s unlikely to head off what history likely has in store for us. Something wicked this way comes.

* * *

The political trajectory is troubling. Unfortunately, there’s little any individual can practically do to change the course of these trends in motion. Do you want to know exactly what you should be doing differently with your portfolio and in your personal life? It reveals what you can do to prepare so that you can avoid getting caught in the crosshairs. Click here to watch it now.

via ZeroHedge News https://ift.tt/35UapFt Tyler Durden

Associated Press Blames France’s “Secular Policies” For Terror Beheadings, Then Deletes Tweet Tyler Durden

Sun, 11/01/2020 – 21:30

Here’s how the Associated Press responded to the latest terrorist beheadings to rock France which has placed the country in a state of ‘maximum security alert’: the major US-based international news organization essentially blamed France itself.

This despite that in the two decapitation attacks and stabbings which came within two weeks of each other (leaving multiple innocent French citizens dead), the perpetrators made it very clear they were committing the brutal murders in the name of Islam as revenge against President Macron and France’s supposed ‘anti-Islamic’ stance and statements, specifically free speech related remarks made in defense of Charlie Hebdo cartoons which depicted Muhammad in a mocking fashion.

Astoundingly, AP’s verified Twitter account appeared to offer some level of ‘justification’ for the killings that included blame of the country’s “staunch secular policies” and the “tough-talking president” who appears “insensitive” to Muslims.

While linking to an article the prominent news outlet wrote: “AP Explains: Why does France incite anger in the Muslim world? Its brutal colonial past, staunch secular policies and tough-talking president who is seen as insensitive toward the Muslim faith all play a role.”

The backlash was so immediate and fierce that the AP soon deleted its outrageous tweet, replacing it with this:

This replaces a tweet about France and the Muslim world that asked why France “incites” anger. The word was not intended to convey that France instigates anger against it.

Though short of an apology, the fact that it was deleted constitutes a rare, embarrassing moment for the press agency. However, the follow-up message did little to alleviate suspicions that this is yet another case of media elites trying to downplay or ignore Islamic terrorism.

More worrisome, the outlet is in reality “inciting hatred against France and its people” – as one journalist observed.

Protesters in Islamabad, Pakistan via EPA

The article itself that the original tweet link to also seemed to lay blame for the slayings on France’s secular traditions and on the government and people themselves.

Many angry commenters underscored that it was a blatant and unbelievable case of victim blaming, while simultaneously failing to condemn the murderers and essentially ignoring their own statements and motives. One emphasized that it was no less than a “justification for decapitation”.

This paragraph from the @AP is astonishing for where it selects to place its emphasis. It glances at the beheading, but only as a means of teeing up the real rebuke of Macron for not renouncing cartoons. There’s not even a hint of awareness that decapitations must stop first. pic.twitter.com/Pan4DcL1Kd

— Thomas Chatterton Williams 🌍 🎧 (@thomaschattwill) November 1, 2020

Especially in the case of French school teacher Samuel Patty’s murder, his killer made it abundantly clear what his motives were.

The 18-year old murderer was shot and killed by police just after the Oct. 16 attack. But just prior to the shoot-out he posted a gruesome image of the aftermath of the beheading to social media as a “message” to others who promote the Charlie Hebdo cartoons or “insults” to Muhammad.

via ZeroHedge News https://ift.tt/3ej56U0 Tyler Durden

Hedge Fund CIO: To Markets It No Longer Matters Who Wins The Election Tyler Durden

Sun, 11/01/2020 – 21:00

By Eric Peters, CIO Of One River Asset Management

When 2020 started, Trump seemed destined to win. The economy was strong, unemployment low, markets were priced accordingly. The odds of a Democrat victory were low, though market consequences of such an outcome seemed clear – higher taxes and re-regulation would knock equities lower. A 25% S&P 500 decline, give or take 10%, seemed reasonable.

Then came Covid. When stocks bottomed on March 23rd, Trump narrowly led Biden in betting markets. But pandemics have consequences and this catastrophe hit a nation that had spent decades optimizing its economy to spur asset price appreciation. America’s financial system was as overleveraged as it was unstable. A depression was inevitable in the absence of something utterly unprecedented.

On March 27th Trump signed the $2.2trln CARES Act, and this, combined with a breathtaking array of asset purchase programs marked the effective start of MMT (Modern Monetary Theory) – with the Fed and Treasury coordinating policy.

And ever since, it has mattered less who wins this election. Because you see, once the link is broken between what the government must collect and what it can spend, who leads the nation is less consequential – at least to stock markets in the near-term.

Tuesday’s election will be a critical one for the nation. No matter who wins, investors can rest easy knowing there will still be long-term opportunities in the market—and Jerome Powell will still be running the Fed. In this week’s issue: pic.twitter.com/gsFIQI5teO

But to a nation descending into tribalism, who wins elections matters greatly.And by early September, with betting markets showing Trump and Biden tied, a new risk emerged: a contested election that would tear the nation to shreds. Provoking civil conflict. War. Stocks declined. But since the first presidential debate on Sept 29th, Biden gained on Trump in the polls.

This is how a decisive Biden victory that had once been seen to be bearish has now become bullish, thanks to MMT which ensures that whoever runs the nation will spend money with reckless abandon.

And we are thus left to trade the impact of a virus that is not finished with us, even if we are desperate to be done with it. As we all pray for a decisive electoral outcome.

Anecdote:

Ten years from today, what will market historians write about the present time? This is among the most important questions.

In 2012, they wrote that Gordon Brown sold half of the UK government’s gold between 1999-2002 at 20yr lows, around $300/ounce. The world had lost its mind, wildly overvaluing intangibles, shunning hard assets. No sooner had Brown hit sell then gold began a 10yr rally to $1,915/ounce.

What will market historians write in 2029 about the 2019 Saudi Aramco IPO with oil at $75/barrel? That was the world’s largest exporter puking reserves. They’re nowhere near finished. The pain for exporters has only just begun.

But far more importantly, what will historians write about the panic adoption of today’s new policy paradigm? Without even a brief public debate, the US government chose to borrow somewhere between 15-20% of GDP from the central bank, which itself engaged in all sorts of financial asset purchases to inflate their prices.

And this shielded those people least touched by the pandemic from pain, as those who hold no stocks and bonds were simultaneously devastated. And this dramatically amplified the inequality that was already tearing the nation’s fabric to shreds.

Traders who spent a decade watching quantitative easing and low interest rates fuel stock price gains, applied yesterday’s lessons to tomorrow. Equity prices surged. While this felt somehow wrong, they could no longer bear the pain of underperformance and convinced themselves that there is no alternative.

But never in the history of humanity has a state of no alternatives sustained for long. For decades, an ever-growing share of the economy’s profits had been awarded to capital owners at the expense of laborers. And as financial asset prices were lifted to record highs, forming a secular top, the system that had driven itself to a state of severe imbalance, instability, was facing tumultuous change. And lurking below, suspended in those watery vaults, a white whale.

via ZeroHedge News https://ift.tt/2GjsaoZ Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}