Google is being sued by 11 states and the federal government, who claim the tech company “is a monopoly gatekeeper for the internet.” Google maintains this monopoly “through anticompetitive and exclusionary practices” in violation of the Sherman Antitrust Act, they allege.

To reach this conclusion, the complaint—filed Tuesday in the U.S. District Court for the District of Columbia—employs a loose conception of monopoly and barely bothers trying to offer a theory of consumer harm. The complaint’s big beef with Google is basically that it’s big, as well as useful, stubbornly popular, and extremely profitable.

Google is “one of the wealthiest companies on the planet, with a market value of $1 trillion and annual revenue exceeding $160 billion,” the government notes in the suit’s second paragraph.

For search users, Google algorithms “deliver more relevant results, particularly on ‘fresh’ queries (queries seeking recent information), location-based queries (queries asking about something in the searcher’s vicinity), and ‘long-tail’ queries (queries used infrequently),” it says. And “few general search text advertisers would find alternative sources [to Google] a suitable substitute.”

The lawsuit against Google does not accuse it of conspiring with its competitors or of acting unilaterally to block new entrants into the market. Nor does it cite common political gripes about Google, such as the idea that it’s working too many different hustles and needs to be “broken up,” or the claim that Google search and YouTube are ideologically biased.

Rather, it accuses Google of unfairly dominating the U.S. markets for general search services, search advertising, and general search text advertising, mainly through distribution deals that give Google apps or search preset default status on some browsers and mobile devices.

To win its suit, the Department of Justice (DOJ) “will need to show that Google is dominant in the market, abusing the power associated with that dominance, and harms consumers,” notes the American Action Forum’s Jennifer Huddleston.

Antitrust experts say the government’s case isn’t great. “U.S. v. Google has a long, long way to go,” said Anthony M. Sabino, a professor at St. John’s University, in a statement. “This case won’t be easy for the government,” said Willaim Rinehart, senior research fellow at the Center for Growth and Opportunity at Utah State University.

“They know they have an uphill battle,” said the Mercatus Center’s Brent Skorup. “Most of Google’s services are offered for free to consumers, so authorities will need compelling evidence of anticompetitive agreements or harm to consumers.”

These default deals are the primary mechanism by which the suit claims Google acted unlawfully and harmed consumers. Yes, all of this hoopla is over the fact that Google—mostly through a combination of leasing its Android operating system to third-party phone manufacturers and paying Apple and others to put Google as the default search option on browsers—comes as an easily changeable default option on many browsers and mobile phones.

For this very ephemeral status it “pays billions of dollars each year to distributors,” including Apple, LG, Motorola, and Samsung, says the lawsuit.

The government calls these arrangements “exclusionary,” saying Google “owns and controls” search access at these points, which make up “roughly 80 percent of the general search queries in the United States.” But no one is obligated to keep these default applications or search settings (in fact, Google’s own app store offers alternatives). Google only “owns and controls” these distribution points until consumers get their hands on the phone.

That’s one of many times the complaint bandies about muddled statistics to make it sound like Google is more powerful than it is. At another point, the lawsuit states that “for mobile browsers, Google is the default search provider for both Apple Safari (approximately 55 percent share) and Google Chrome (over 35 percent share), which together account for over 90 percent of the browser usage on mobile devices in the United States.” But—again—being set as the default doesn’t mean people continue to use it, and besides, there are many ways to search that don’t involve a mobile phone web browser.

The evidence “suggests that Google has become the default through a product most people prefer, not by anti-competitive behavior,” writes Huddleston. “Additionally, a growing number of product searches now start on Amazon, not Google. .. In many cases, consumers already have easily accessible alternatives and a growing number of innovative choices.”

Nonetheless, the government argues that it’s default status deals—not what it acknowledges is Google’s greater scale, greater name recognition, and more relevant results—that make it popular. And they say this popularity itself presents Google with an unfair advantage over competitors since it makes Google a more attractive option for advertisers and phone providers than competitors like Yahoo, Bing, or DuckDuckGo.

The government claims “countless advertisers must pay a toll ” because of Google’s alleged monopoly, and accuses Google of unfairly maintaining this edge through such nefarious tactics as being high quality. “Google discovered that it could increase the number of clicks—and its own profits—by ranking ads to promote those with greater relevance,” the government complains. “To help determine placement of ads, Google uses a ‘quality score.'”

It’s hard to see how either consumers or advertisers would benefit—or change their ways—just because Google apps didn’t come preloaded on some phones or as the default search in some browsers. Presumably, Google wouldn’t magically lose its huge name recognition and Bing or Yahoo wouldn’t suddenly have better results. The government can meddle around the market’s edges all it wants, but they can’t force consumers to choose inferior products just to equalize market share.

“The complaint makes a lot of hay out of Google’s deal with Apple to be the default search engine on Safari,” and “of course, being the default helps increase market share,” tweeted Alec Stapp, director of technology policy at the Progressive Policy Institute. “But Tim Cook has also said that Google is the best search engine. Should the default be an inferior product?”

“It will be a heavy lift for the DOJ to show real consumer harm,” said Jessica Melugin, associate director of Center for Technology and Innovation at the Competitive Enterprise Institute. “That this bar is unlikely to be met is precisely why so many antitrust enthusiasts are calling for a fundamental rewriting and expansion of U.S. antitrust laws. Those proposed changes sacrifice the primacy of consumer welfare and insert competitors and broader socio-economic goals in its place.”

This has been a progressive goal for a while. After a “liberalization trend” that saw consumer welfare emerge as the main goal of antitrust law enforcement, “it’s being tugged back to form a support system protecting ‘competitors’—guarding against low prices, escalating quality, and market rivalry,” explained Thomas W. Hazlett for Reason last year.

One of this movement’s biggest proponents has been Sen. Elizabeth Warren (D-Mass.). “America has a long tradition of breaking up companies when they have become too big and dominant—even if they are generally providing good service at a reasonable price,” Warren wrote in 2019, citing Gilded Age forebears as a guide for how to “restore competition to the tech sector” and promising to use antitrust law against Google and Amazon.

Oddly enough, Republicans are celebrating these moves.

“I applaud this suit as desperately needed and long overdue,” tweeted Sen. Josh Hawley (R–Mo.) this week. “Google is a monopoly and I think they have been abusing their monopoly power,” said Sen. Ted Cruz (R–Texas) on CNBC.

The 11 states joining in the Google lawsuit are all states with Republican attorneys general.

But the Google antitrust suit is a profoundly anti-free market document, wholly in line with modern progressive and leftist conceptions of heavier government intervention in today’s marketplace. Ultimately, the government is going after Google for being bigger and more capable than others, not to stop some consumer harm, but to try and level the playing field.

from Latest – Reason.com https://ift.tt/31zTuGP

via IFTTT

Hunter Biden, COVID Likely To Light Up Last Debate Tyler Durden

Thu, 10/22/2020 – 14:05

As President Trump and Joe Biden prepare to face off during tonight’s second and final debate before the November 3rd election, America, if not the world, is preparing for a ‘shitshow‘ of epic proportions thanks to “October Surprise” revelations of Biden family corruption contained on an abandoned laptop, and attested to by former Hunter Biden business partners.

But, assuming for a moment that things won’t immediately and irrecoverably go off the rails out of the gate (they will), the six topics for tonight’s debate are as follows:

“Fighting COVID-19,” “American Families,” “Race in America,” “Climate Change,” “National Security” and “Leadership.”

The Debate Commission notably changed the main theme from foreign policy to ‘national security,’ undoubtedly in light of recent Biden bombshells.

“All the issues voters care about are places where President Donald Trump has succeeded,” Hogan Gidley, national press secretary for the Trump campaign told “Just the News AM” television show. “People’s lives have been improved by Donald Trump’s policies — regardless of race, religion, color or creed. You don’t have to guess what Donald Trump would do with the economy. We’ve seen record high employment for African-American, Asian American, Hispanic Americans, women employed at record numbers. We saw more jobs than there were people to fill them.” –Just The News

“You also notice they took away the topic of foreign policy? Of course they would,” Gidley said. “President Trump has a record of success there too, already. He’s already been nominated for a Nobel Peace Prize multiple times because of his work in the Middle East, something that Joe Biden couldn’t have thought about ever accomplishing. And all the experts told Donald Trump he couldn’t get it done. He got two peace deals. He’s drawing down troops from our foreign wars.”

Donald Trump and Joe Biden will soon meet for a final debate tonight in Tennessee to discuss that pandemic and to argue over who is better suited to lead the country through that crisis and for the next four years. The moderator will have a mute button.

This is unusual, as the Commission on Presidential Debates is not in the business of silencing speech. But the chaos of the last Trump-Biden debate so closely mirrored the chaos of the last year that that the commission decided it needed a way to shut up either candidate, or at least lower their decibel levels. There is a lot to argue about, and it will get personal.

The Trump campaign complained in an open letter when the debate commission changed the topic from international affairs to domestic issues. The president and his team described the decision as unfair on the grounds it ignored major administration achievements in foreign policy during the last four years. Left unsaid was that the topic change makes it more difficult for Trump to bring up Hunter Biden and his foreign business deals. It seems likely he’ll do it anyway.

Trump tried repeatedly, with limited success, to label his opponent “Corrupt Joe.”More recently he has pointed to reporting by the New York Post to argue that the former vice president used the influence of that office to direct foreign policy and to benefit his son’s business dealings in both China and Ukraine.

“This is major corruption, and this has to be known about before the election,” Trump said during a Tuesday interview on “Fox and Friends.”

But while the president has publicly said the Department of Justice should look into the matter, the major media outlets have declined to take the allegations seriously. During an ABC News town hall last week with Biden, moderator George Stephanopoulos never mentioned it. The final debate may be Trump’s last time to force the question.

The former vice president has mainly ignored the allegations so far except to belittle journalists who bring it up. “I knew you’d ask it,” Biden fired back at a CBS reporter who asked last week. “I have no response, it’s another smear campaign, right up your alley, those are the questions you always ask.”

Trump isn’t likely to let him off the hook so easily, even as some of his own advisers urge him to focus on the pre-pandemic economy rather than allegations of international graft. Biden would rather discuss the coronavirus than the latest October surprise. His campaign has spent the better part of the pandemic hammering the president over his response to it, and recently Trump offered his challenger another gift.

Trump warned an Arizona crowd that his opponent would bring back the lockdowns if elected and “wants to listen to Dr. Fauci,” the most visible member of the COVID-19 task force who has advocated for the measures. The Biden campaign responded quickly with an ad copping to the charge – yes, he would most definitely listen to Dr. Anthony Fauci.

“Trump’s closing message in the final days of the 2020 race is to publicly mock Joe Biden for trusting science,” the Biden campaign later wrote in a statement. “Trump is mocking Biden for listening to science. Science. The best tool we have to keep Americans safe, while Trump’s reckless and negligent leadership threatens to put more lives at risk.”

Asked during a town hall in the Rose Garden on Tuesday if there were anything he would have done differently to combat the pandemic, Trump responded, “Not much.”

Like the polarized country they want to lead, the two candidates profess to have little in common, and no one seriously expects bipartisanship to break out on stage. But they share one trait. Even though the RealClearPolitics National Average has Biden leading Trump by 7.5 points, neither campaign says it believes the polls.

“We cannot become complacent because the very searing truth is that Donald Trump can still win this race,” Biden campaign manager Jen O’Malley Dillon wrote in a memo obtained by Fox News. “And every indication we have shows that this thing is going to come down to the wire.”

Republicans are banking on the same dynamic.

“We’re going to win,” Trump told reporters last week.

“I wouldn’t have told you that maybe two or three weeks ago.”

On the same call, his campaign manager Bill Stepien added, “I don’t often agree with the Biden campaign, but I do agree with the Biden campaign when they say that this is a close race, because it absolutely is. When we look at the numbers we very, very much like the trajectory of this race.”

Republicans are in the habit of summoning the ghost of 2016 to ward off concerns about their current polls. They note that Hillary Clinton led Trump by a similar margin, 6.1 points per the RCP average, at this time in that race. Aggregate polling of top battleground states from 2016 and 2020 is also nearly identical. The Trump campaign argument? Another upset is possible.

Tonight is Trump’s last chance to make that case against Biden, the final debate in supposedly the most important election ever.

via ZeroHedge News https://ift.tt/37yhKwS Tyler Durden

A new preprint study estimates that COVID-19 deaths in the United States cut lives short by a total of 2.5 million years as of early October. The author, Harvard Medical School geneticist Stephen Elledge, says he did the analysis to correct “the false impression that the impact on society of these deaths is minimal” because they are concentrated among the elderly.

According to the most recent data from the Centers for Disease Control and Prevention (CDC), people 65 or older, who represent 17 percent of the U.S. population, account for nearly 80 percent of COVID-19 deaths. But as Elledge emphasizes, people in that age group are not necessarily on the verge of death. The average life expectancy at 65 in the United States is about 83 for men and 86 for women.

“Because the great majority of COVID-19 deaths occur among the elderly,” Elledge writes, “the false impression that the impact on society from these deaths is minimal may be conveyed since these individuals were closer to a natural death. Aside from any troubling ethical implications associated with rationalization of COVID-19 mortality along these lines, such a conclusion is unwarranted for at least two reasons. First, as individuals age, their life expectancies increase too, well beyond the life expectancy at birth, which is the value most familiar to the general public. Second, a significant number of relatively young individuals have also died from COVID-19 and had decades of remaining life expectancy.”

Based on actuarial data on life expectancy and the age distribution of COVID-19 fatalities, Elledge roughly calculated that the 194,087 deaths reported by CDC as of October 3 amounted to 2,572,102 years of potential life lost (YPLL). The average loss based on that calculation was about 13 years and three months. Because the CDC breaks COVID-19 deaths into 10-year age ranges and the risk of dying from COVID-19 rises with age, Elledge performed an adjustment that reduced the YPLL number by 3.5 percent, to 2,486,160. That implies an average loss of nearly 12 years and 10 months.

Elledge notes that his analysis did not adequately account for “the effect of comorbidities on life expectancy.” Since people who are less healthy to begin with are more likely to die from COVID-19, a calculation based on average life expectancies by age group is apt to exaggerate the years of potential life lost due to the disease. Elledge takes a stab at adjusting for comorbidities by including a calculation that reduces COVID’s YPLL toll by 15 percent, from about 2.5 million to about 2 million. But this is really just a guess.

Other metrics of death-related costs, such as disability-adjusted life years (DALY) and quality-adjusted life years (QALY), try to take into account how healthy people would have been during their remaining years. That consideration is obviously relevant when comparing deaths at a young age to deaths at an advanced age, even leaving aside the difference in years of life expectancy.

“We did not undertake those analyses but note that there is a growing awareness of lasting effects on those infected with SARS-CoV-2 that lead to serious medical consequences,” Elledge says. The implication is that a QALY or DALY approach would cut both ways: discounting years lost by people who were already in poor health while taking into account the lasting effects of nonfatal infections.

Leaving those issues aside and taking Elledge’s numbers at face value, how do they compare to the losses associated with other causes of death?

In 2018, according to CDC data, unintentional injuries among Americans 85 or younger, including traffic accidents, were responsible for about 5.3 million years of potential life lost. Although those injuries caused fewer deaths (about 167,000) than COVID-19 has, the average loss was much bigger: more than 31 years, compared to about 13 years for COVID-19 per Elledge.

The average YPLL is only slightly higher for cancer than Elledge’s estimate for COVID-19: 14 vs. 13 years. But because cancer causes more deaths (nearly 600,000 in 2018, per the CDC), the total loss is much bigger: about 8.5 million years. And while heart disease, according to the CDC’s numbers, claimed an average of 10 years in 2018—less than the figure Elledge calculated for COVID-19—the total loss was still much higher: 6.6 million years of potential life.

In 2008, the CDC calculated that smoking was responsible for about 443,000 deaths per year (many of those from cancer and heart disease), amounting to 5.1 million YPLL, or more than 11 years on average. This year the CDC estimated that “excessive alcohol use” causes about 93,000 deaths a year (including about 7,000 motor vehicle deaths), resulting in a YPLL toll of 2.7 million annually, or an average of 29 years. By contrast, the 2.5 million YPLL toll calculated by Elledge for COVID-19 is higher than the annual loss that the CDC attributes to suicide (1.8 million), homicide (944,000), chronic lower respiratory disease (1.5 million), and diabetes (1.2 million)—all of which are considered serious problems worthy of national attention.

Contrary to Elledge’s implication, however, people who emphasize the age distribution of COVID-19 deaths are not saying those deaths are “minimal” or don’t matter. They are saying that years of potential life lost, and perhaps also the quality of those years, should be considered when weighing the costs and benefits of policies aimed at curtailing the epidemic. Elledge seems to agree.

from Latest – Reason.com https://ift.tt/31tJsac

via IFTTT

“A Long Way To Go” – Tudor Jones Says Bitcoin Rally In “First Inning” As Prices Top $13,000 Tyler Durden

Thu, 10/22/2020 – 13:50

The unprecedented monetary stimulus unleashed by the Federal Reserve to combat the virus-induced downturn, earlier this year, has worried legendary trader and famed macro hedge fund billionaire Paul Tudor Jones so much, that at the time (May), he told clients, in a note, that he purchased Bitcoin as a hedge against the inflation he sees emerging from the Fed’s money-printing.

On Thursday, PJT joined CNBC’s “Squawk Box,” discussing his increasingly bullish views on Bitcoin, naming it one of the best inflation hedges.

“I like bitcoin even more now than I did then. I think we are in the first inning of bitcoin and it’s got a long way to go,” PJT said.

“I also made the case for owning Bitcoin, the quintessence of scarcity premium. It is literally the only large tradeable asset in the world that has a known fixed maximum supply.”

He told CNBC, his current position in the cryptocurrency is only a “small single-digit investment.”

“The reason I recommended bitcoin is because it was one of the menu of inflation trades, like gold, like TIPS breakevens, like copper, like being long yield curve and I came to the conclusion that bitcoin was going to be the best inflation trade,” PJT said.

PJT compares investing in Bitcoin today to putting money behind the biggest tech companies like Apple and Google decades ago.

“Bitcoin has this enormous contingence of really, really smart and sophisticated people who believe in it,” PJT said.

He added, “It’s like investing with Steve Jobs and Apple or investing in Google early.”

PJT told CNBC in May that Bitcoin is an inflation hedge against the dangers of America’s “crazy” monetary-fiscal mix since at least January, which he warned the situation in current markets reminded him of 1999.

Bitcoin has surged 16% in the last three sessions to $13,000. The cryptocurrency has gone parabolic from the March low of around $3,850, up 244% to roughly $13,000, but at levels not seen since June 2019, and far from the $19,000 mark recorded in December 2017. The latest spark of bullish Bitcoin activity stems from PayPal news, saying that it has entered the cryptocurrency market.

PJT told clients earlier this year that bitcoin reminds him of “the role gold played in the 1970s”.

PJT appears to be worried about the long-term ramifications of the Fed’s actions as balance sheet expansion will have to continue as the recovery in late 2020 wanes.

* * *

Read the full report – entitled “the Great Monetary Inflation” – below:

COVID-19 is a one-of-a-kind virus that has triggered a one-of-a-kind policy response globally.

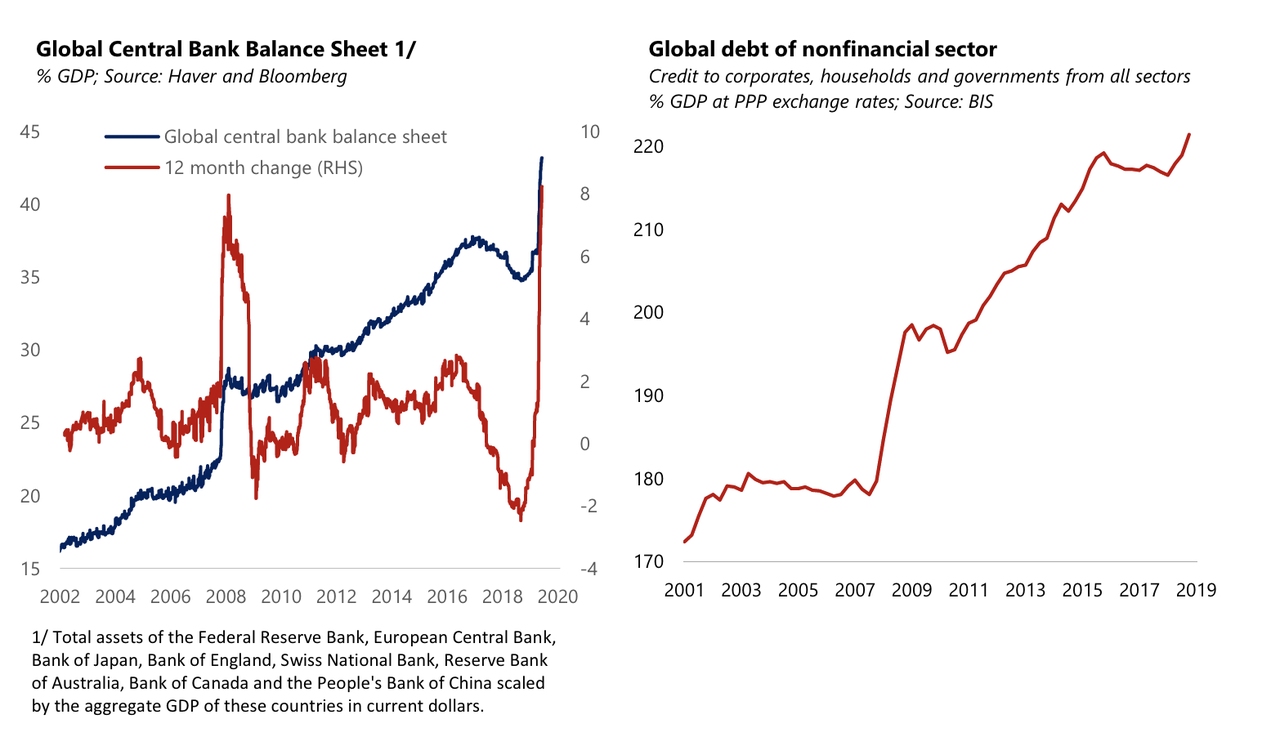

The depth and magnitude of the economic drop-off took modern monetary theory—or the direct monetization of massive fiscal spending—from the theoretical to practice without any debate. It has happened globally with such speed that even a market veteran like myself was left speechless. Just since February, a global total of $3.9 trillion (6.6% of global GDP) has been magically created through quantitative easing. We are witnessing the Great Monetary Inflation (GMI)—an unprecedented expansion of every form of money unlike anything the developed world has ever seen.

Global debt was very elevated entering the pandemic, and this monetary expansion is funding additional large debt creation, for now, without provoking the disciplining response of rising market yields. So far, the result has been asset price reflation. A large demand shortfall will prevent goods and services inflation from rising in the short term. The question is whether that will be the case in the long term with a central bank whose central focus will be repairing the worst employment crisis since the Great Depression.

One thing is for sure, there will be many assets that will move as a result of this money creation. So what is an investor to do? Traditional hedges like gold have done well, and we expect investors to continue to seek refuge in this safe asset. One thing I have learned over time is the best thing to do is let market price action guide your decision-making and then try to understand the fundamentals as they become more evident and comprehensible. Quite often, how the markets respond will be at odds with your priors. But remember, the P&L always wins in the long run. With that in mind, in a world that craves new safe assets, there may be a growing role for Bitcoin.

Debt Addiction

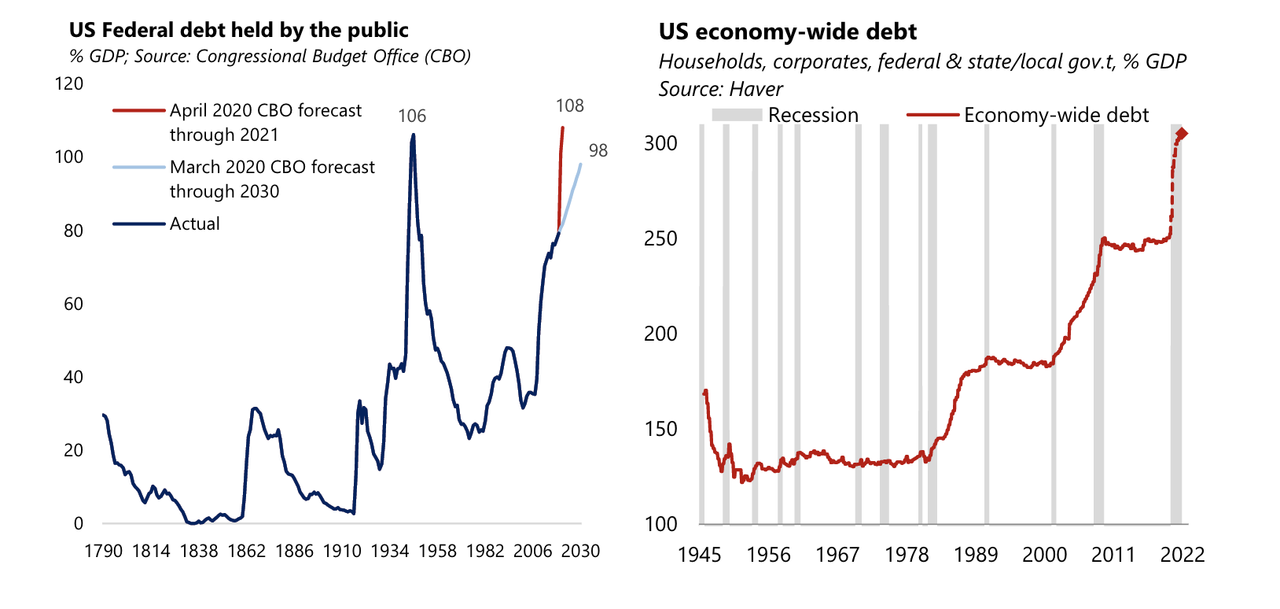

What is apparent to all is the global ramp-up in debt from every sector to deal with the economic downturn. In addition to debt ratios increasing by virtue of a larger numerator, such ratios will also be buoyed by a falling denominator: it may take more than two years to bring nominal GDP back to its pre-shock level. The Congressional Budget Office, for example, projects the US government debt ratio to reach a new historic high next year, above the World War II peak. Corporate debt is also rising briskly to record levels as firms draw down revolving credit lines to self-fund cash flow shortfalls. At this pace, it is not inconceivable that the economy-wide debt ratio may increase by 50% of GDP over the next year and a half.

Money Printing is a Hard Habit to Kick

Central banks are on the hook to help fund this debt increase. Since the end of February, the Fed’s balance sheet has already grown by 60% and is on track to more than double by the end of the year. Even two QE novice central banks have unleashed their printing presses. The Bank of Canada has already tripled its balance sheet, and the Reserve Bank of Australia has allowed its balance sheet to increase by 43%.

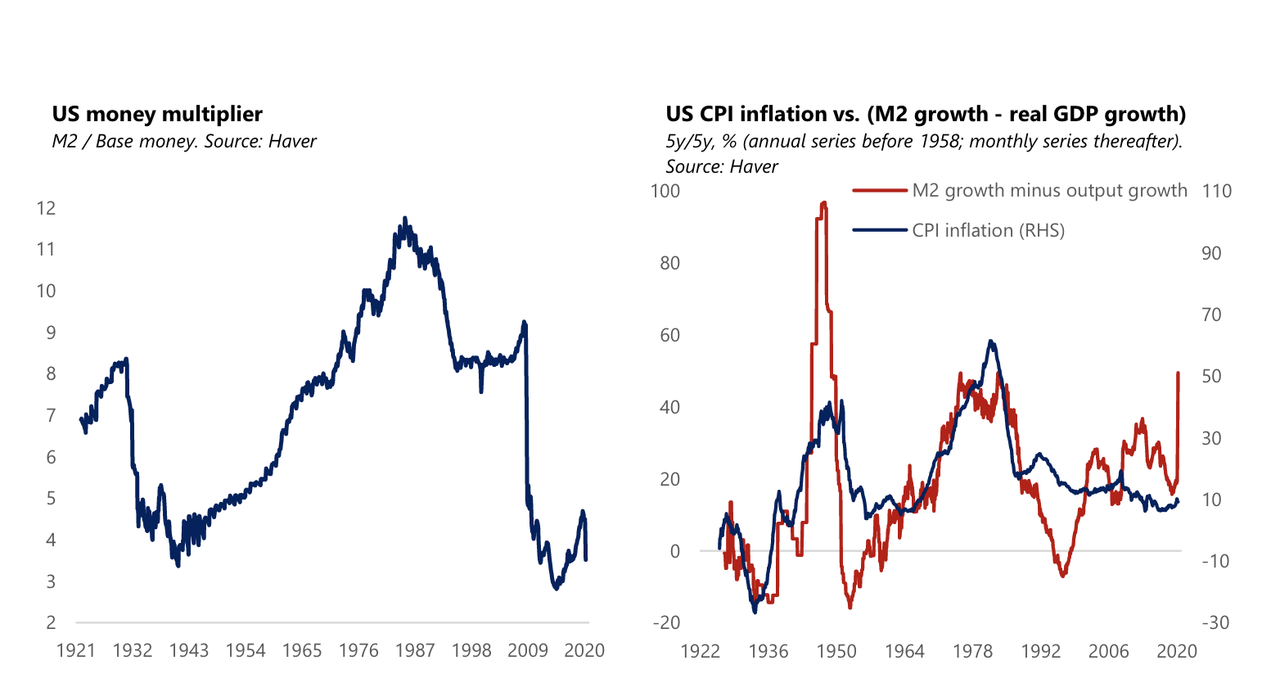

The counterpart of this rapid central bank balance sheet expansion has been a sharp increase in monetary aggregates. In the last weekly release of the Fed’s Money Stock data, M2 rose 18.5% over a year ago, an unprecedented pace of growth in the history of the weekly time series starting from 1981. It is likely that the annual growth in M2 will continue to increase to somewhere between 20% and 40% by year-end. We got these estimates on M2 from a few of the dinosaurs who still work on Wall Street. Rarely have we ever seen so many economists dismissive of an economic metric than when we asked about their notion on this record M2 growth and its meaning. The last time M2 grew at such a high pace was during World War II, when annual M2 growth peaked at almost 27%.

But, monetary expansion alone is not sufficient to generate inflation. The context is very important too. Take Japan, the poster child of debt-deflation. Arguably, this is a case where monetary financing of the deficit has been ineffective. But, Japan was already in a prolonged deflationary spiral that had unanchored inflation expectations when this policy was unleashed in full. In any event, since 1999, their M2 never grew by more than 5% a year. A hobbled banking system focused on healing from a prolonged banking crisis had probably a lot to do with this. In the US, it can also be argued that a large deficit combined with massive money printing were ineffectual at stoking inflation in the aftermath of the Global Financial Crisis (GFC).

Again, context matters, and the post-pandemic recovery may be different from the GFC aftermath. First, an austerity movement similar to the one that swept the Tea Party to prominence in the 2010 US mid-term elections is very unlikely to emerge. The opposite forces are at play today as growing income inequality breeds populism. Second, the bank-centric GFC induced a one-time paradigm shift in banks’ preference for liquidity, later enforced through regulatory changes. As a result, only a small share of the Fed’s massive injection of high-powered money was re-lent in the banking system: M2 never grew by more than 10% a year even after subsequent rounds of large-scale asset purchases by the Fed. Effectively, banks’ preference for liquidity and the need to rebuild their capital cushions quashed the money multiplier. While the multiplier has recently started to fall—in a crisis, banks are wary to lend to potentially insolvent borrowers and, in fact, start building provisions for loan losses—this time banks entered the crisis in a stronger footing and policy is more squarely aimed at putting liquidity directly in the hands of businesses and households shielding, to some extent, banks from losses. As such, the chance of a large fall in the multiplier as seen in the aftermath of the GFC is now smaller. Plus, the Fed’s elimination of the reserve requirement means that the theoretical money multiplier is now infinite (the multiplier is the inverse of the reserve requirement).

Milton Friedman famously stated that “inflation is always and everywhere a monetary phenomenon that arises from a more rapid expansion in the quantity of money than in total output.” And while the relationship between inflation and M2 growth in excess of real output growth has not been stable over short horizons, it seems to hold over longer horizons. There are only a few times in history when M2 growth exceeded real output growth over a 5-year span by the same or a faster pace than is currently the case: the inflationary periods of the 1970s–80s and the late 1940s.But remember, it is reasonable to expect inflation to first fall in the coming months, given the large contraction in demand relative to supply.

The issue is whether a large monetary overhang in the recovery phase will eventually stoke consumer price inflation.

To answer this question, we need to ask, how reasonable is it to expect that in the recovery phase the Fed will be able to deliver an increase in interest rates of a magnitude sufficient to suck back the money it so easily printed during the downswing? The current Fed leadership has made it a centerpiece of its new monetary policy framework to do whatever it takes to overshoot the inflation target in the recovery phase. This is a risky strategy. If the Phillips curve is truly flat, it requires a large increase in interest rates to bring inflation under control. But, a more levered economy is also one that does not digest interest rate increases well. So, when the time for lift-off finally occurs, any hiking cycle is likely to be delayed and unambitious. Furthermore, the risk of a complicit (politically-appointed) central bank chairman cannot be easily dismissed given that central bank independence is no longer a sacred cow.

High debt accommodated by money printing is difficult to banish. Inflation expectations could one day respond to this reality. It is the risk of fiscal dominance that makes the current GMI potentially inflationary during the next cyclical upswing. After all, fiscal dominance was a key reason for inflation to flare up in the late 1930s and the 1940s when the Fed was strong-armed to keep rates low and to monetize Treasury debt issuance well beyond the economic recovery phase.

There are other reinforcing considerations to fear a resurgence of inflation down the line. The pandemic has exposed the vulnerability inherent in global interdependence and stoked tensions between the US and China. There may come a tipping point when a breakdown in global supply chains spills overs to goods prices, undoing two decades of disinflation attributable to globalization.

Seeking Refuge from the Great Monetary Inflation

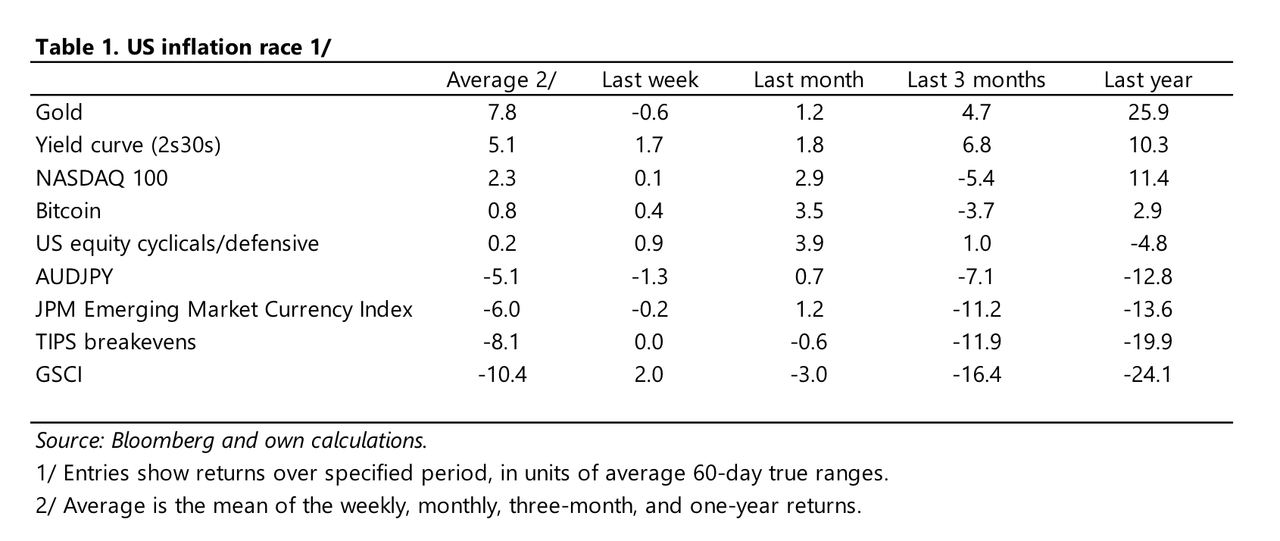

So with this type of monetary growth as a backdrop, here is one way to navigate these extraordinary times and policy actions. Below is a list of inflation hedges, rank-ordered in what we call the Inflation Race. While some of this list will track inflation in the classic sense, other instruments have been added to pick up the assets that will respond best to an acceleration in monetary growth, not just consumer goods and service price inflation.

So, it includes a host of assets that at one time or another have worked well in reflationary periods:

Gold–A 2,500 year store of value

The Yield Curve–Historically a great defense against stagflation ora central bank intent on inflating. Forour purposes we uselong 2-year notes and short 30-year bonds

NASDAQ100–The events of the last decade have shown that quantitative easing can rapidly leak into equity markets

Bitcoin–There is a lengthy discussion of this below

US cyclicals (long)/US defensive (short)–A pure goods’inflation play historically

AUDJPY–Long commodity exporter and short commodity importer

TIPS(Treasury Inflation-Protected Securities) –Indexed to CPI to protect against inflation

GSCI(Goldman Sachs Commodity Index) –A basket of 24 commodities that reflects underlying global economic growth

JPM Emerging Market Currency Index–Historically when global growth is high and inflationary pressures are building, emerging market currencies havedone quite well

Now it would be wonderful if we knew ex-ante which horse to bet on. The goal,of course,is to be invested in the fastest horsesover the duration of the ride. And to help monitor this,we review the horse race over the short, intermediate, and long term by averaging price performance over such periods. This provides a snapshot such as shown below, which was taken on May 6th (Table 1). We have rank-ordered the instruments below by averaging the 1-week, 1-month, 3-month, and 12-month returns. We show the performance in volatility-adjusted returns,not in nominal returns, so think of each unit as approximately a day’s average trading range. So,gold under the “Last year” column has gone up about 26 daily ranges, which also equates to about $406, from $1,280 to $1,686

From the table, gold is the clear winner of the Inflation Race at this time. In second place is long the US 2s30s yield curve. In third place is the NASDAQ100: remember this GMIis going to show up somewhere so why not stocks? And in fourth place it is Bitcoin – yes, Bitcoin. It did trade $18 billion of volume on the last day of April and is an “emerging” asset class by any metric. Of course, bringing up the bottom with a hugely damaging return of negative10 daily ranges (also equivalent to -46% in the trailing 12 months) is the Goldman Sachs Commodity Index. This index has been pummeled due to the crash in oil prices as producers are at war to preserve their market share and stay afloat.

One thing that piqued my interest from this list of assets,and that one day might be brought to prominence by the GMI, is Bitcoin. Truth in advertising, I am not a hard-money nor a crypto nut. I am not a millennial investing in cryptocurrency, which is very popular in that generation, but a baby boomer who wants to capture the opportunity set while protecting my capital in ever-changing environments.

One way to do that is to make sure I am invested in the instruments that respond first to the massive increases in global money. And giventhat Bitcoin has positive returns over the most recent time frames, a deeper dive into it was warranted. I did have some experience with it back in 2017, having a tiny amount in my personal account for fun. Amazingly, I doubled my money and got out near the top when it was apparent to any market technician we were blowing off. It is amazing how well one can trade when there is no leverage, no performance pressure and no greed to intrude upon rational reflection! When it doesn’t count, we are all geniuses.

But the GMI caused me to revisit Bitcoin as an investable asset for the first time in two and a half years.It falls into the category of a store of value and it has the added bonus of being semi-transactional in nature. The average Bitcoin transaction takes around 60 minutes to complete which makes it “near money.” It must compete with other stores of value such as financial assets, gold and fiat currency, and less liquid ones such as art, precious stones and land. The question facing every investor is, “What will be the winner in ten years’ time?”

At the end of the day, the best profit-maximizing strategy is to own the fastest horse. Just own the best performer and not get wed to an intellectual side that might leave you weeping in the performance dust because you thought you were smarter than the market. If I am forced to forecast, my bet is it will be Bitcoin.

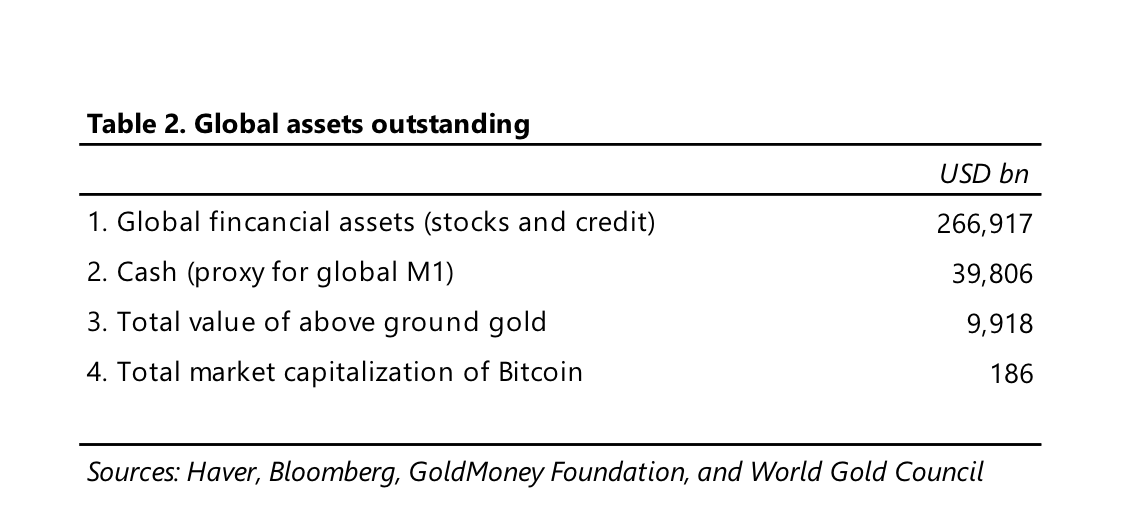

A store of value is anything that holds its purchasing power in the future. It is completely a function of people’s perception of its worth. Even tulips at one time were considered a store of value. Financial assets comprise the largest store of wealth in the world as they generally have the added advantage of providing yield,which helps offset the impact of inflation. Gold has survived the test of time although a rational person could ask “Why gold over any of the other 118 elements?” Fiat currency (cash) is backed by the full faith and credit of the people of that country,although that promise has high variability,as history has shown. And the newest entrant is Bitcoin, which seems to have emerged from the crypto war of 2017 as the clear winner with a market cap 10x that of its closest competitor.

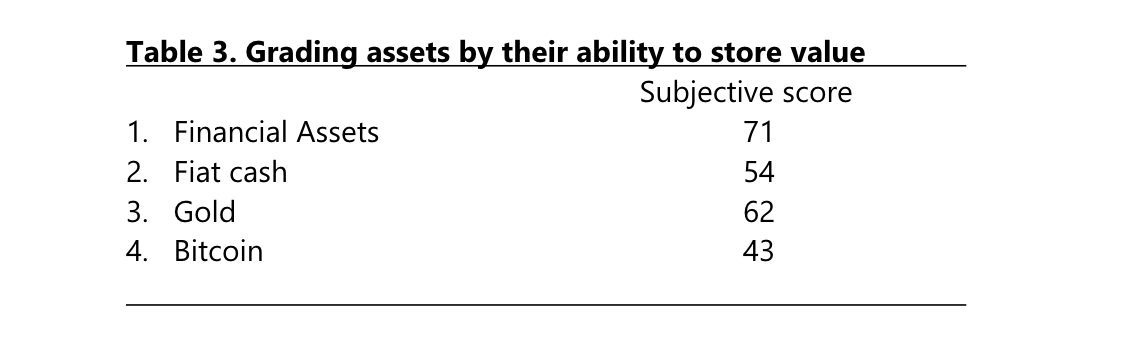

So how do these storesof value stack up against each other? We graded stores of value on four characteristics:

Purchasing Power–Howdoes this asset retain its value over time?

Trustworthiness–How is it perceived through time and universally as a store of value?

Liquidity–How quickly can the asset be monetized into a transactional currency?

Portability–Can you geographically move this asset if you had to for an unforeseen reason?

For the purpose of this exercise, real estate, art and precious stones have been excluded as they will fall to the bottom of the ranking automatically because of generally poor liquidity and portability characteristics. So let’s focus on financial assets, fiat currency, gold, and now Bitcoin. To offer perspective, Table 2 shows the value of these assets at the present time. It is an important table, which I will come back to.

Remember, the challenge here is to understand which store of value will be the winner in the next ten years. The first thing is to score the four assets against the four criteria laid out above. So I polled my research group to see what this team of informed persons thought. After discussion, we created a scoring system for a store of value with the maximum score being 100. We considered some categories more important than others, so we allocated 30% each to the categories of purchasing power and trustworthiness and 20% to each of liquidity and portability. Then, we scored the four sets of assets above and came up with a composite and highly-subjective value for each in Table 3 below.

Before drawing broad conclusions, here were some of the more salient points in each category. When it came to purchasing power, everyone was a carry merchant arguing the only way to defeat inflation was with some type of yield—i.e., financial assets. This was particularly popular with the 30-something crowd who gave financial assets the highest score across the board. I reminded them that in the 1970s, inflation was near double-digits at times and the road to hell was paved with carry. In fact, virtually all financial assets were shunned because the yield could not keep up with inflation—in many cases like now.

I also made the case for owning Bitcoin, the quintessence of scarcity premium. It is literally the only large tradeable asset in the world that has a known fixed maximum supply. By its design, the total quantity of Bitcoins (including those not yet mined) cannot exceed 21 million. Approximately 18.5 million Bitcoins have already been mined, leaving about 10% remaining. On May 12th Bitcoin’s mining reward – the pace at which the supply of Bitcoin is increased – will for the third time be “halved” (falling from 12.5 to 6.25 Bitcoins per block of transactions added to the blockchain). Future halvings will likewise occur approximately every four years consistent with Bitcoin’s design, thus continuing to slow the rate of supply increase and causing some to estimate that the last available Bitcoin will not be mined for another 100+ years. This brilliant feature of Bitcoin was designed by the anonymous creator of Bitcoin to protect its integrity by making it increasingly near and dear, a concept alien to the current thinking of central banks and governments.

The most surprising result of our research group poll was the score ascribed to fiat cash. It got a 0 almost across the board! The cry from the troops was “If something is by design going to depreciate 2% per year through inflation, why own it?”

The next category we discussed in determining whether or not something was a good store of value was trustworthiness. No surprise here Bitcoin got the lowest score because it is also the youngest entrant at 11 years of age. Someone mentioned that it has 60 million users in almost 200 countries, but that did nothing to sway people. Gold, as one would have guessed, scored first in this category, as it has stood the test of time for thousands of years.

Liquidity is one of those things that never matters until it does (every 10 years it seems), which is why we weighted it only 2/3 of the value of purchasing power and trustworthiness. But as we have all probably experienced in the last two months, liquidity is hugely important when things go pear shaped. It is reasonable to assume, given the number of bankruptcies we are about to witness and the number of people who will be jobless and near poverty, that both companies and individuals will have a much higher preference for liquidity in coming years. Cash scored the highest here and rightly so. Financial assets are a mixed bag because some, like private equity and bespoke credit instruments, take forever to liquidate and often at severe discounts. Interestingly, Bitcoin is the only store of value that actually trades 24/7 in the entire world.

Finally, there is portability. Like liquidity, it is not an issue until it is. Imagine a geographic upheaval whether it be caused by war, an epidemic, or change in government that becomes hostile to holders of wealth. A great store of value can be seamlessly moved from one jurisdiction to another with little or no transaction costs. Cash is obviously good for that; gold is ok but clunky; but, of course, nothing beats Bitcoin, which can be stored on a smartphone among other options.

So that was the flavor behind some of the discussions that were had when scoring the suitability of each asset as a store of value. What was surprising to me was not that Bitcoin came in last, but that it scored as high as it did. Bitcoin had an overall score nearly 60% of that of financial assets but has a market cap that is 1/1200th of that. It scores 66% of gold as a store of value,but has a market cap that is 1/60th of gold’s outstanding value. Something appears wrong here and my guess is it is the price of Bitcoin.

The most compelling argument for owning Bitcoin is the coming digitization of currency everywhere, accelerated by COVID-19. Bull markets are built on an ever-expanding universe of buyers. Central to the price of Bitcoin is how many more (or less) owners of Bitcoin will there be beyond the 60 million who currently own it? The probable introduction of Facebook’s Libra (whose value will be pegged to the US dollar and will not be a store of value in that sense) as well as China’s DCEP, also tied to the yuan, will make virtual digital wallets a commonplace tool for the world. It will make the understanding, utility, and ease of ownership of Bitcoin a much more commonplace option than it is today.

Owning Bitcoin is a great way to defend oneself against the GMI, given the current fact set. As Satoshi Nakamoto, the anonymous creator of Bitcoin, stated in an online forum around the time he launched Bitcoin, “the root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust.”I am not an advocate of Bitcoin ownership in isolation, but do recognize its potential in a period when we have the most unorthodox economic policies in modern history. So, we need to adapt our investment strategy. We have updated the Tudor BVI offering memoranda to disclose that we may trade Bitcoin futures for Tudor BVI. We have set the initial maximum exposure guideline for purchasing Bitcoin futures to a low single digit exposure percentage of Tudor BVI’s net assets, which seems prudent.We will review this exposure guideline regularly.

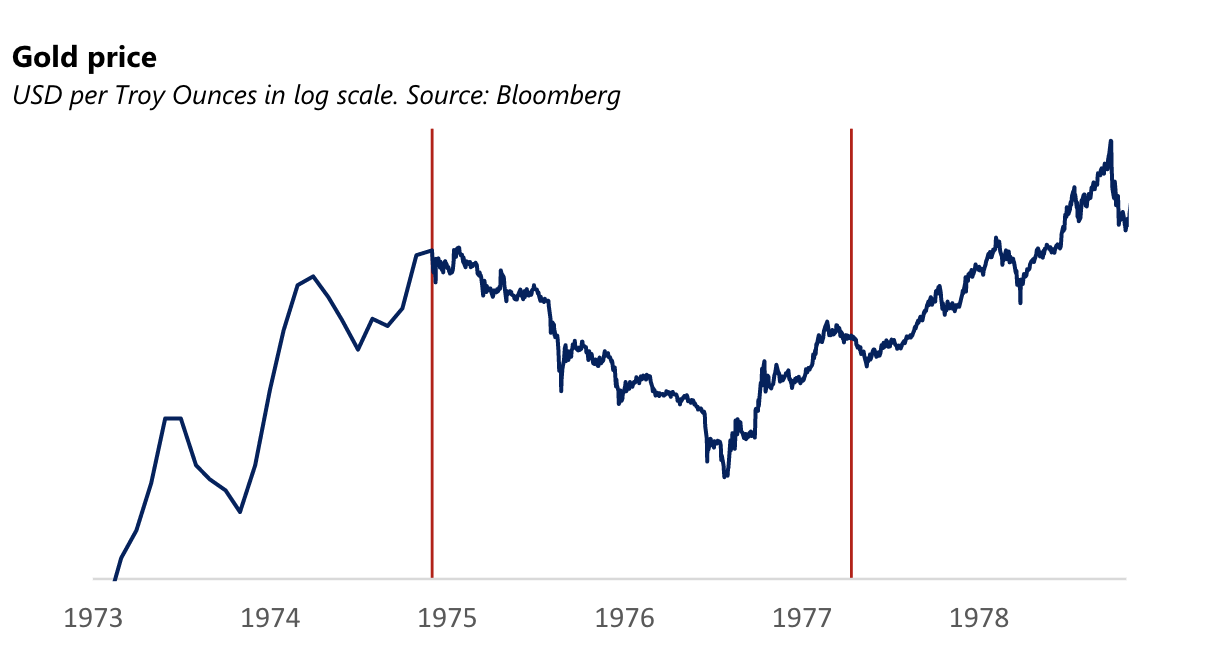

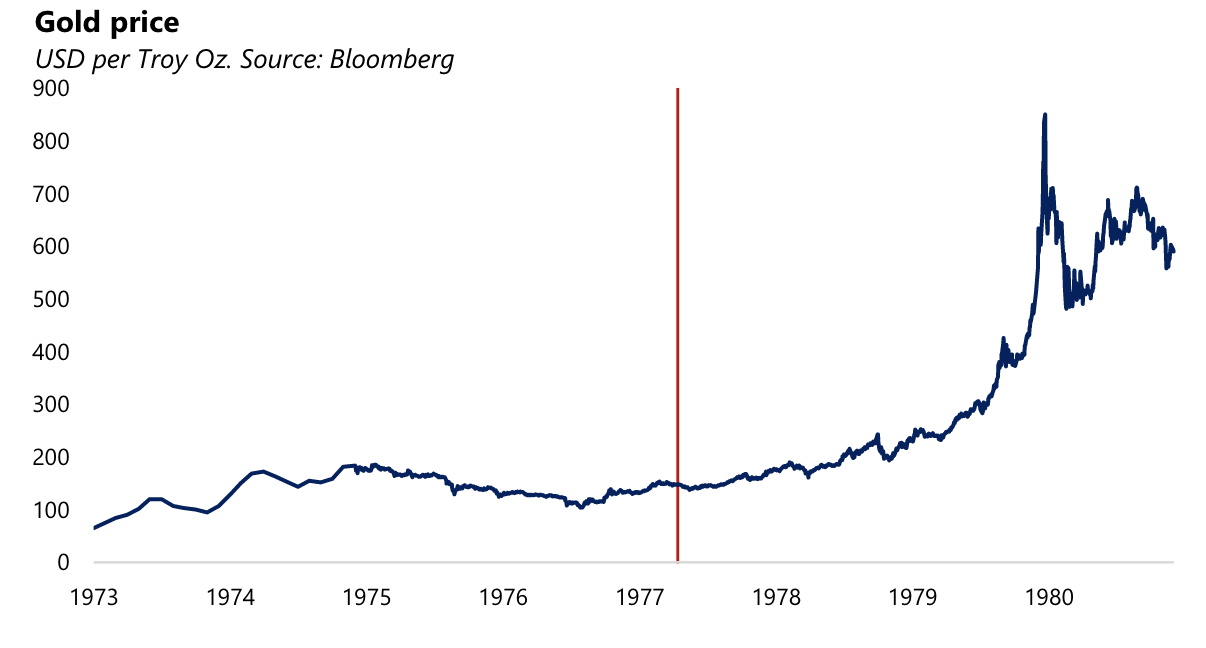

Many of you know my fondness for analogues. Bitcoin reminds me of gold when I first got in the business in 1976. Gold had just been productized as a futures instrument (like Bitcoin recently) and had enjoyed a heck of a bull market, almost tripling in price. It then corrected almost 50% in nearly two years similar to Bitcoin’s 28-month 80% correction! You can see the similarities in the two charts below.

But in the case of gold, it was a tremendous buying opportunity as gold went on to more than quadruple past the prior highs. The red line in the chart below is where we might be in Bitcoin today.

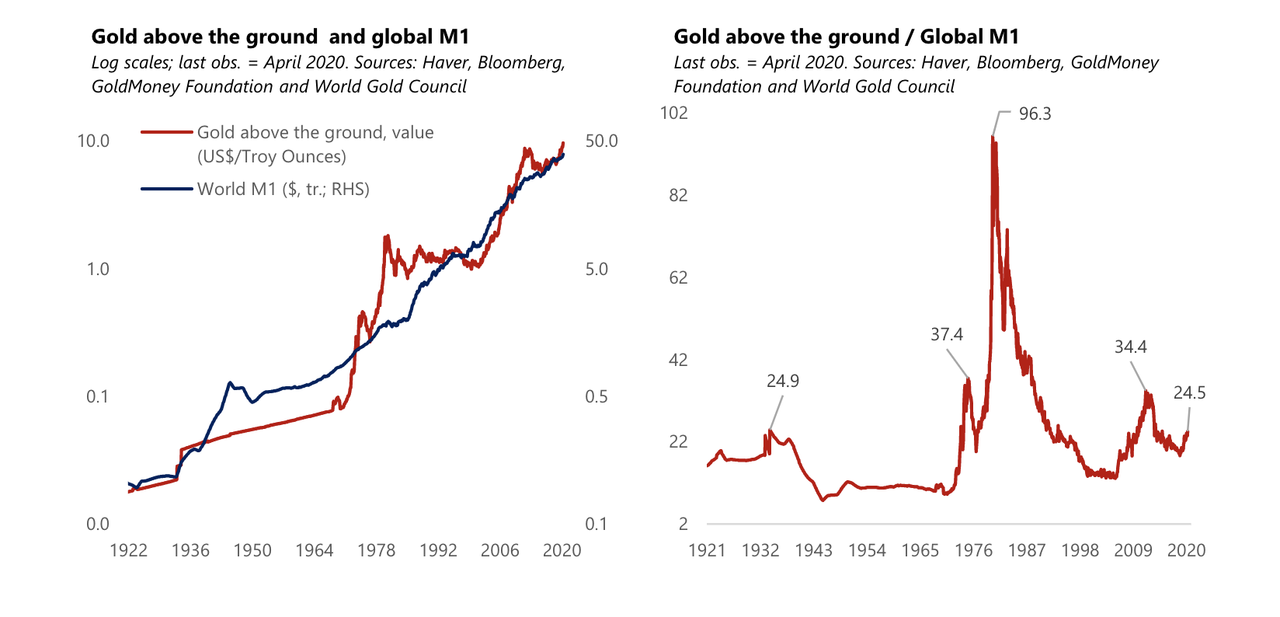

Speaking of gold, in a low-carry world, gold remains a very attractive hedge against the Great Monetary Inflation and hedges against other risks clouding the outlook, including a renewed flare up in the China-US relationship where financial sanctions could eventually be used in a brute-force decoupling. How far can gold rally from its current price? A simple metric based on the ratio of the value of gold above ground to global M1 suggests gold could rally to 2,400 before it reaches valuations consistent with the lowest of the last three peaks in this valuation metric and 6,700 if we went back to the 1980 extremes.

One thing is for sure, these are going to be incredibly interesting times.

via ZeroHedge News https://ift.tt/3jmoS1x Tyler Durden

A new preprint study estimates that COVID-19 deaths in the United States cut lives short by a total of 2.5 million years as of early October. The author, Harvard Medical School geneticist Stephen Elledge, says he did the analysis to correct “the false impression that the impact on society of these deaths is minimal” because they are concentrated among the elderly.

According to the most recent data from the Centers for Disease Control and Prevention (CDC), people 65 or older, who represent 17 percent of the U.S. population, account for nearly 80 percent of COVID-19 deaths. But as Elledge emphasizes, people in that age group are not necessarily on the verge of death. The average life expectancy at 65 in the United States is about 83 for men and 86 for women.

“Because the great majority of COVID-19 deaths occur among the elderly,” Elledge writes, “the false impression that the impact on society from these deaths is minimal may be conveyed since these individuals were closer to a natural death. Aside from any troubling ethical implications associated with rationalization of COVID-19 mortality along these lines, such a conclusion is unwarranted for at least two reasons. First, as individuals age, their life expectancies increase too, well beyond the life expectancy at birth, which is the value most familiar to the general public. Second, a significant number of relatively young individuals have also died from COVID-19 and had decades of remaining life expectancy.”

Based on actuarial data on life expectancy and the age distribution of COVID-19 fatalities, Elledge roughly calculated that the 194,087 deaths reported by CDC as of October 3 amounted to 2,572,102 years of potential life lost (YPLL). The average loss based on that calculation was about 13 years and three months. Because the CDC breaks COVID-19 deaths into 10-year age ranges and the risk of dying from COVID-19 rises with age, Elledge performed an adjustment that reduced the YPLL number by 3.5 percent, to 2,486,160. That implies an average loss of nearly 12 years and 10 months.

Elledge notes that his analysis did not adequately account for “the effect of comorbidities on life expectancy.” Since people who are less healthy to begin with are more likely to die from COVID-19, a calculation based on average life expectancies by age group is apt to exaggerate the years of potential life lost due to the disease. Elledge takes a stab at adjusting for comorbidities by including a calculation that reduces COVID’s YPLL toll by 15 percent, from about 2.5 million to about 2 million. But this is really just a guess.

Other metrics of death-related costs, such as disability-adjusted life years (DALY) and quality-adjusted life years (QALY), try to take into account how healthy people would have been during their remaining years. That consideration is obviously relevant when comparing deaths at a young age to deaths at an advanced age, even leaving aside the difference in years of life expectancy.

“We did not undertake those analyses but note that there is a growing awareness of lasting effects on those infected with SARS-CoV-2 that lead to serious medical consequences,” Elledge says. The implication is that a QALY or DALY approach would cut both ways: discounting years lost by people who were already in poor health while taking into account the lasting effects of nonfatal infections.

Leaving those issues aside and taking Elledge’s numbers at face value, how do they compare to the losses associated with other causes of death?

In 2018, according to CDC data, unintentional injuries among Americans 85 or younger, including traffic accidents, were responsible for about 5.3 million years of potential life lost. Although those injuries caused fewer deaths (about 167,000) than COVID-19 has, the average loss was much bigger: more than 31 years, compared to about 13 years for COVID-19 per Elledge.

The average YPLL is only slightly higher for cancer than Elledge’s estimate for COVID-19: 14 vs. 13 years. But because cancer causes more deaths (nearly 600,000 in 2018, per the CDC), the total loss is much bigger: about 8.5 million years. And while heart disease, according to the CDC’s numbers, claimed an average of 10 years in 2018—less than the figure Elledge calculated for COVID-19—the total loss was still much higher: 6.6 million years of potential life.

In 2008, the CDC calculated that smoking was responsible for about 443,000 deaths per year (many of those from cancer and heart disease), amounting to a loss of 5.1 million YPLL, or more than 11 years on average. This year the CDC estimated that “excessive alcohol use” causes about 93,000 deaths a year (including about 7,000 motor vehicle deaths), resulting in a YPLL toll of 2.7 million annually, or an average of 29 years. By contrast, the 2.5 million YPLL toll calculated by Elledge for COVID-19 is higher than the annual loss that the CDC attributes to suicide (1.8 million), homicide (944,000), chronic lower respiratory disease (1.5 million), and diabetes (1.2 million)—all of which are considered serious problems worthy of national attention.

Contrary to Elledge’s implication, however, people who emphasize the age distribution of COVID-19 deaths are not saying those deaths are “minimal” or don’t matter. They are saying that years of potential life lost, and perhaps also the quality of those years, should be considered when weighing the costs and benefits of policies aimed at curtailing the epidemic. Elledge seems to agree.

from Latest – Reason.com https://ift.tt/31tJsac

via IFTTT

Kamala Harris, Schumer, Cuomo And Feinstein Listed As ‘Key Contacts’ For Biden-China Joint Venture Tyler Durden

Thu, 10/22/2020 – 13:30

Democratic Vice Presidential Candidate Kamala Harris is listed along with other prominent Democrats as a “key domestic contact” for a Biden family joint venture involving Hunter and Jim Biden in the now-bankrupt CEFC China Energy Co., according toFox News.

An email exclusively obtained by Fox News, with the subject line “Phase one domestic contacts/ projects” and dated May 15, 2017, Biden’s brother, Jim Biden, shared a list of “key domestic contacts for phase one target projects.”

The email is unrelated to the laptop or hard drive purportedly belonging to Hunter Biden, the former vice president’s son. –Fox News

Also included are: “Senate Minority Leader Chuck Schumer, D-N.Y.; Sen. Amy Klobuchar, D-Minn.; Sen. Dianne Feinstein, D-Calif.; Sen. Kirsten Gillibrand, D-N.Y.; New York Gov. Andrew Cuomo; New York City Mayor Bill de Blasio; former Virginia Gov. Terry McCauliffe, among others.”

The email with the ‘key contacts’ was sent by Jim Biden to institutional investor Tony Bobulinski, Hunter Biden, Rob Walker and James Gilliar. It is unclear if any of the Democrats listed above were contacted about the “target projects.”

Bobulinski is a former Lieutenant in the U.S. Navy, and served as the CEO of SinoHawk Holdings, which he said was the partnership between the CEFC/ Chairman Ye and the Biden family.

As an aside, Bobulinski was notably admonished by Gilliar for mentioning Joe Biden’s involvement with their dealings:

In text messages obtained by @FDRLST, Hunter Biden’s biz partner James Gilliar admonished Tony Bobulinski on May 20, 2017: “Don’t mention Joe being involved, it’s only when you are face to face[.]”

And then he brings up Hunter’s role in a 2020 Joe Biden presidential campaign… pic.twitter.com/XGeyOfbera

“I was brought into the company to be the CEO by James Gilliar and Hunter Biden,” Bobulinski told Fox News. “The reference to “the Big Guy” in the much-publicized May 13, 2017 email is in fact a reference to Joe Biden. The other “JB” referenced in that email is Jim Biden, Joe’s brother.”

Bobulinski, in a statement to Fox News, said “Hunter Biden called his dad ‘the Big Guy’ or ‘my Chairman,’ and frequently referenced asking him for his sign-off or advice on various potential deals that we were discussing.”

“I’ve seen Vice President Biden saying he never talked to Hunter about his business,” Bobulinski said “I’ve seen firsthand that that’s not true, because it wasn’t just Hunter’s business, they said they were putting the Biden family name and its legacy on the line.”

He added: “ I realized the Chinese were not really focused on a healthy financial ROI. They were looking at this as a political or influence investment.”

“Once I realized that Hunter wanted to use the company as his personal piggy bank by just taking money out of it as soon as it came from the Chinese, I took steps to prevent that from happening,” he added.

via ZeroHedge News https://ift.tt/31tGMJG Tyler Durden

How Gov Cuomo’s Missteps Allowed COVID-19 To Overwhelm The US Tyler Durden

Thu, 10/22/2020 – 13:15

Earlier this week, NY Gov. Andrew Cuomo attacked the governors of New Jersey and Connecticut over outbreaks that recently sent case numbers in those states to their highest levels in months. He then turned his attention to President Trump, his perpetual antagonist, and in an unusually scathing denunciation, Cuomo slammed Trump as a “super spreader” and claimed Trump was personally responsible for every death caused by COVID-19 in the state.

Gov. Andrew Cuomo (D-NY): “I hold Donald Trump responsible for every death in New York state from COVID … He lied. And in combination with his lies, he was incompetent.” pic.twitter.com/6p6uRWUk0d

Cuomo has stepped up his public briefings again lately, as the number of COVID-19 cases is once again on the rise in his state, which reported more than 2,000 new cases yesterday for the first time in months. But the governor has also just published a new book detailing his experience as ‘America’s governor’, stepping up to lead during the early days of the crisis, when his briefings were carried live on national cable news.

No other governor received such fawning treatment by the press. But in a new report, the Financial Times, a British newspaper respected for its impartial coverage of American politics, digs into the “mythology” surrounding Cuomo’s reputation. The paper found that both Gov Cuomo and NYC Mayor Bill de Blasio repeatedly ignored warnings from experts, wasting six weeks (including the entire month of February) urging citizens to go about their lives, as the virus silently spread across the city.

When confronted with their initial response, both men have claimed that they were ‘flying blind’, forced to battle the virus without adequate testing resources thanks to the ineptitude of the Trump Administration. Other reports have detailed the bureaucratic incompetence at the CDC that seemed to almost deliberately delay the widespread availability of tests. But both men had been advised of the risks, and still they resisted closing schools and businesses – for fear it might hurt the city’s economy – or take other precautions to limit travel into and out of the state.

The inadequate government response led to divisions between public hospitals and wealthy private hospitals, between the rich and poor, the suburbs/Manhattan vs. the Bronx and the outerboroughs. Oxiris Barbot, who quit early on after being sidelined by Mayor de Blasio, warned in early February that New Yorkers should stay calm because “this is not something that you’re going to contract in the subway or on the bus.” Even back then, the scientific community knew enough to call this statement into question.

But the reality is that scares over previous epidemics hitting New York had proven to be just that – scares. And the mayor and governor were treating the disease like Ebola, preparing for isolated cases, not a full-scale outbreak.

Others claimed New York should have been heading into lockdown when the first National Guardsmen arrived in New Rochelle. But that’s not what happened. Instead, public health professionals who warned that hospitals needed to start stocking up on PPE in February were ignored. A few weeks later, nurses in the Bronx were treating patients while swathed in garbage bags, while hospitals on the Upper East Side still had empty ICU beds and more than enough masks to go around.

That’s not to say mistakes at the federal level didn’t play a role – they did. For more than a month, the CDC refused to allow world-class labs in the state to run tests independently of the CDC. This made impossible for NY to scale up testing, allowing the virus to infect tens of thousands of people before the city could confirm even a single case.

“We had our hands tied behind our back,” recalls Melissa DeRosa, Mr Cuomo’s closest aide, as federal authorities tested people arriving from Asia and Iran but kept flights open from Europe, where cases were rising. More than 1.7m people flew in from Europe in “the lost month” of February, she says, while “Covid-19 was silently ravaging the entire north-east”.

Every major decision, from closing schools, to shutting down NYC and, ultimately, the rest of the state, was preceded by petty squabbles between Albany and City Hall over who would announce the plan, and what language would be used, etc.

“The mayor and the governor were in a constant pissing contest. The people in the middle get urinated on,” said Gustavo Rivera, a state senator and leader of the state’s health committee, who was one of the key on-the-record voices in the FT story. “The notion that we should be celebrating when we still have more deaths than in most countries in the world is just insanity.”

Another New York pol, Jumaane Williams, said “days were wasted” thanks to Cuomo’s distaste for terms like “lockdown” and “shelter-in-place”.

“Days were wasted because [the governor] was afraid of the term shelter-in-place,” echoes Jumaane Williams, New York City’s public advocate. “It cost people’s lives: 10 to 15 lives an hour.”

“It is very hard to watch the governor selling books when tens of thousands of lives were lost.”

David Engelthaler, a genomic epidemiologist at Arizona’s Translational Genomics Research Institute, said that genetic research has shown that the strain that spread in NY was the European strain, which went on to infect most of the country, not the Chinese strain responsible for early outbreaks on the West Coast.

Instead of serving as a bulwark against a nationwide outbreak, New York became “Grand Central station” in the spread of the virus across the US, an outbreak that is now working its way across the Midwest.

Of course, when it comes to COVID-19, Gov Cuomo’s “all talk” approach is mirrored by his younger brother, Chris Cuomo, who was recently issued a letter by the management from his building warning him that he could face a $500 fine if he’s caught again violating rules surrounding wearing masks during public spaces in a building.

“You have been observed entering and exiting the building and riding the elevator without the required face coverings,” reads part of the Aug. 6 letter.

“Even though staff members have asked you to comply with this requirement, you have refused to do so. This is a violation of the Executive Order, building policy, and places other residents and our staff at risk. There are no exceptions to this rule, and you are required to comply.”

Tucker Carlson has more on that below:

Tucker Carlson reveals a letter to CNN anchor @chriscuomo from the management of his New York City apartment complaining about how he refuses to wear a mask. pic.twitter.com/2y5KCqpAix

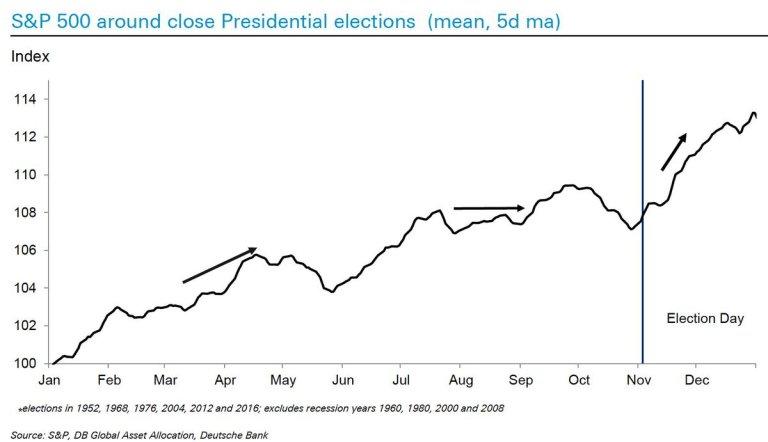

Time to put up or shut up for bulls and bears as we enter the final 2 months of the year and with the US election just a few days away.

As traders are watching the ongoing stimulus headline drama unfolding the bull case may be rather obvious but worth highlighting in the charts. At a time when valuations no longer seem to matter and most of traditional correlations lay in ruins due to unprecedented interventions by central banks the bull case is the obvious one: Get more stimulus and markets will rally higher once again.

After all, and it must be acknowledged, the intervention has so far once again worked in 2020, indeed interventions have created the largest break in correlation between the economy and market prices ever:

And indeed, all corrections since the March lows have found steady support on retests and have engaged in a series of higher lows.

So if nothing matters and more stimulus is to come the bull case then counts on historic distortions to continue unabated.

And there is a standard seasonal script in favor of bulls into year end, that of the presidential election year kind:

In context the current chop and weakness since the September peak is fitting perfectly with that seasonal script..

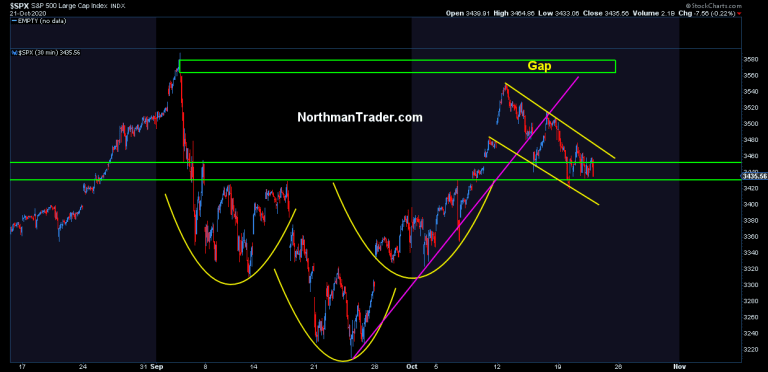

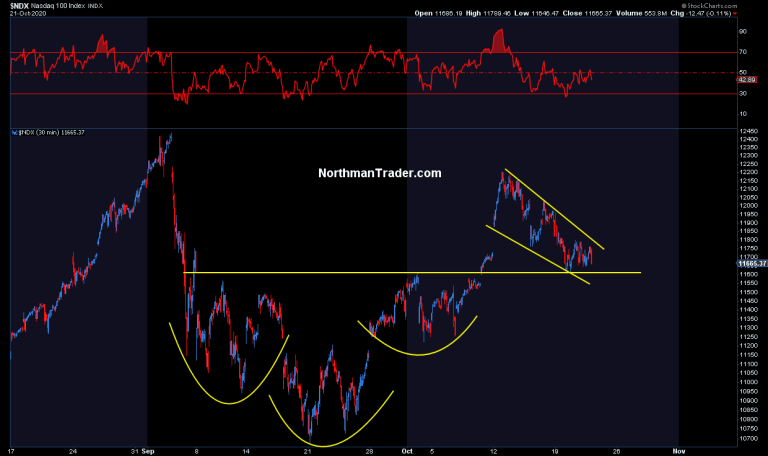

And speaking technically now, the bullish pattern I highlighted in my recent videos have not been invalidated despite several downdrafts this week.

For reference the pattern I mentioned again last Friday:

And now with several more days of price action under their belt this pattern continues to defend the backtest of the neckline and is sporting a potential bull flag to boot, see $NDX and $SPX charts below:

So yea, get more stimulus or the belief in more stimulus and these charts are primed for a rip.

Even last night’s further drop in futures found perfect support at the bottom of the flag on the futures chart:

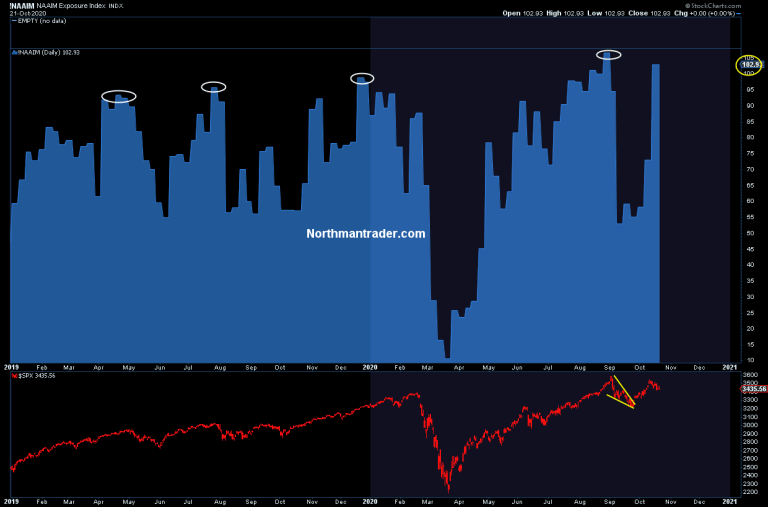

So yes, the bullish case is obvious and apparently very much embraced by participants as asset managers have again loaded fully long:

For bears the challenge is clear:Invalidate these patterns and fast for the potential dollar cup and handle pattern is teetering at the brink of extinction as markets continue to expect more stimulus:

Perhaps of note here is that bulls have not been able to take advantage of this renewed weakness in the dollar and that could prove to be an important divergence.

Why? Because, for one, these bullish patterns, while not invalidated, have yet to validate themselves.

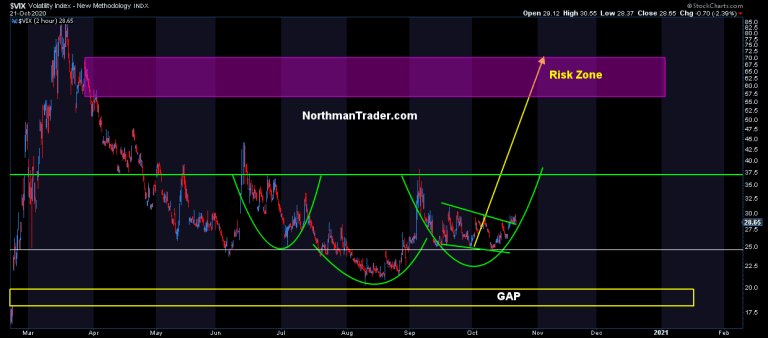

And the $VIX? Well, oddly enough it keeps staying in its potential very bullish structure having defended the breakout out of its consolidation pattern several times this week:

The battle line for control in all of this? Perhaps equal weight and the tightening price structure in $SPX:

Bulls need to break above equal weight resistance and bears need to prevent the breakout.

The battle zone for control is inside the $SPX pattern structure above. Upside risk per the inverse pattern outlined is into 3650 and the upper trend line.

So you see, the next few hours, days and weeks are be key for all this and the time is rapidly approaching for bulls and bears to put up or shut up.

The bear case? We can visit that one once/if the patterns outlined above are invalidated, but know the downside risks are vast and if $VIX maintains its structure the bear case may come in a hurry, but at the time of this writing bulls are maintaining control with a razor thin margin above $SPX 3400-3430.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/35rAWtk Tyler Durden

After weeks of failing to offer a straight answer to the question of whether he’d support adding additional justices to the U.S. Supreme Court, Democratic presidential nominee Joe Biden is testing out a new answer in advance of Thursday’s debate.

In a preview of an interview that will air Sunday on 60 Minutes, Biden outlines a plan for what he calls a “bipartisan commission” to examine potential reforms to the federal courts. In the clip, posted to the show’s Twitter feed on Thursday morning, Biden says he would fill the commission with constitutional scholars from across the ideological spectrum and that he would give the body 180 days to review not only court-packing but “a number of other things,” though he does not elaborate.

As dodgy political answers go, this one is actually pretty brilliant. Biden is giving the appearance of fleshing out a substantial plan to answer his critics, throwing a bone to liberal activists who favor increasing the number of justices on the Supreme Court, and still allowing himself plenty of ways to avoid actually doing that once he’s elected. It’s a Rorschach test of an answer, one that probably sounds good to most voters—who generally oppose court-packing but like the sound of bipartisanship—without committing a future President Biden to any particular course of action.

Recall that Biden has a long track record of opposing court-packing. In 1983, he referred to President Franklin Delano Roosevelt’s 1937 attempt to add justices to the Supreme Court as a “bone head idea” that “put in question for an entire decade the independence of…the Supreme Court.” He was still opposed as recently as last year’s presidential primary debates, saying in October 2019 that he “would not get into court-packing” due to fears that it would delegitimize the Supreme Court.

That’s the sort of decadeslong, consistent record that most politicians would be proud to highlight on the campaign trail. But Biden has gone soft on the question in recent months as some Democrats have suggested adding seats to the court to counter the expected confirmation of Amy Coney Barrett to replace the late Justice Ruth Bader Ginsburg. Biden has tried, sometimes awkwardly, to find a middle ground between his longstanding opposition to court-packing and his party’s fear of a 6-3 majority conservative Supreme Court.

In that context, this new promise to create a “national commission” seems mostly like a way to make the question go away. It’s a tried and true political strategy: punt a controversial issue to a panel of supposed experts to make it look like you’re doing something. As a longtime creature of the U.S. Senate—which isn’t called the “world’s most deliberative body” for nothing—Biden understands the value of doing nothing while looking like you might do something someday.

Still, there are two things we can definitively say about Biden’s newest take on court-packing. He has objectively backed away from his former position of opposing the idea, even if he’s opening the door only a crack. And he’s committed to waiting at least six months into his potential first term before doing it—in other words, it’s not important enough to rise to the very top of a Biden administration’s agenda. That’s good.

One more thing: You can almost certainly expect Biden to roll out this answer at tonight’s debate if the issue of court-packing comes up.

Indeed, this new approach to the question is a campaign strategy too: The image of a bipartisan commission mulling over high-minded constitutional questions about the right way for the country’s government to operate draws a pretty stark comparison with how the executive branch is currently running.

from Latest – Reason.com https://ift.tt/34iu7v4

via IFTTT

3rd-Degree Murder Charge Dropped Against Former Cop In George Floyd Case Tyler Durden

Thu, 10/22/2020 – 12:44

A third-degree murder charge against former Minneapolis police officer Derek Chauvin was dropped by a Minnesota judge on Thursday. Chauvin was shown on video kneeling on the neck of George Floyd, a black man who died in police custody after the incident.

Floyd’s autopsy revealed that he had fentanyl and methamphetamine in his system, and was positive for COVID-19 at the time of his death.

Hennepin County District Court Judge Peter Cahill also let stand all other charges against Chauvin’s co-defendants.

Cahill ruled that while third-degree murder is applicable in cases when a defendant’s actions could have harmed others, prosecutors are accusing Chauvin in the death of just one victim, Floyd. –NBC News

“The language of the third-degree murder statute explicitly requires the act causing the ‘death of another’ must be eminently dangerous ‘to others’,” wrote Judge Cahill.

According to Minnesota Attorney General and Antifa supporter Keith Ellison, the dismissal is no big deal.

“The court has sustained eight out of nine charges against the defendants in the murder of George Floyd, including the most serious charges against all four defendants,” Ellison said in a statement.

“This means that all four defendants will stand trial for murder and manslaughter, both in the second degree. This is an important, positive step forward in the path toward justice for George Floyd, his family, our community, and Minnesota. We look forward to presenting the prosecution’s case to a jury in Hennepin County.”

That said, according to law professor Mark Osler of the University of St. Thomas in Minnesota – a former federal prosecutor – losing the 3rd degree charge might mean jurors who are uncomfortable convicting Chauvin of second-degree murder won’t have the lesser charge to fall back on.

“They wouldn’t have charged it if they didn’t want it going in front of a jury,” Osler told NBC News. “You always want to give options to a a jury.”

via ZeroHedge News https://ift.tt/3jkTCQw Tyler Durden