One day later, after a week where leading vaccine developers like Pfizer and Moderna warned about supply constraints, hinting that they’re widely touted projections might be unrealistic, and forcing President Trump to sign an executive order to try and ensure American patients are treated as a priority, the Britain’s pharma regulator has dropped a bombshell warning.

The MHRA (Britain’s regulator) warned Wednesday that any patients with histories of having “powerful allergic overreactions” should avoid the vaccine. For a report published by a professional news agency like Reuters, the details were surprisingly vague. Since a huge number of Americans are allergic to something, a little more clarity would be appreciated.

As someone who has many allergies, I wish we had more info on which allergens were an issue. “any person with a history of significant allergic reactions to vaccines, medicine or food should not receive the Pfizer/BioNTech vaccine.” https://t.co/ja6SNtiEbA

According to public opinion polls, state and federal health officials have apparently been succeeding in establishing “credibility” to these vaccines. But there’s no question that setbacks like this could have a profound affect on individuals’ willingness to accept the vaccine, which also reportedly comes with punishing sideeffects.

Britain began mass vaccinating its population on Tuesday in a global drive that poses one of the biggest logistical challenges in peacetime history, starting with the elderly and frontline workers National Health Service medical director Stephen Powis said the advice had been changed after two NHS workers reported anaphylactoid reactions associated with receiving the vaccine. “As is common with new vaccines the MHRA (regulator) have advised on a precautionary basis that people with a significant history of allergic reactions do not receive this vaccination, after two people with a history of significant allergic reactions responded adversely yesterday,” Powis said. “Both are recovering well.”

A relatively scant report released yesterday by the FDA argued the Pfizer vaccine’s efficacy and safety data met its expectations for authorization. It also warned that 0.63% of people in the vaccine group and 0.51% in the placebo group reported possible allergic reactions in trials, which Peter Openshaw, Professor of Experimental Medicine at Imperial College London, brushed off as a “very small number.”

What’s more: In the US, at least 2, possibly 3, participants from the Pfizer and Moderna trials have died in the following weeks.

As more serious questions arise, fueling “conspiratorial” skepticism directly challenging the narrative that the vaccines have been thoroughly and appropriately studied before being unleashed upon the population, more bold faced names are speaking up to denounce the skeptics after Joe Biden yesterday labeled wearing masks – to be fair, a totally different subject from vaccines – one’s “Patriotic Duty”. On CNBC earlier, author Walter Isaacson warned that choosing not to get a COVID vaccine was tantamount to endangering lives everywhere you go.

via ZeroHedge News https://ift.tt/3m1vML8 Tyler Durden

“Eureka! The formula for success is letting others do the work, and then take all the credit!”

The excellent Saxo “Outrageous Predictions”, and Tesla Does It Again!

Investment managers dread the approach of the Christmas holidays. They get deluged in a ton of turgid year-end outlooks which are unified in only one thing – their utter unreadability. I suspect many Bank year-end outlooks are written primarily to get past the desk of the compliance gauleiter overseeing them, to impress their bosses, and only then, maybe, to interest customers.

There is one exception, and much as hurts to congratulate a competitor in the “scribbler” market, the brilliant Steen Jakobsen of Saxo Bank’s “outrageous” predictions for 2021 are about the best thing when it comes to Christmas outlooks. They are so good, because they are so plausible… and therefore possible. They make you think – which is always a good thing.

1. I absolutely agree the Covid-19 vaccines could well prove a company killer – as I wrote yesterday, the start of the vaccination programme may mark the high-point of the rally as the recovery reality becomes clearer. Economies will V-Shape, leading to the unwind of stimulus and QE support as the economy “overheats”, triggering rising rates and the end of many zombie struggling companies – led by the retail high street. Recovery will precipitate crisis.

2. Amazon buying Cyprus is a bit out there – but why not? Amazon redomiciles its EU HQ to a beautiful island and resets its own tax rules? It could trigger an enormous backlash and harmonisation of taxation across Europe – spelling danger for Ireland.

3. Germany bailing out France is a schweet thought, but unlikely. (Or is it….?)

4. The innovation of blockchain source-checking on fake-news by the major social media platforms to block is a very timely suggestion – allowing news to be checked and the source veracity validated. If it’s really possible this really could be someone at last finding something distributed ledgers are good for! (Rather than just driving idle crypto-frauds).

5. China’s new digital Yuan takes over capital markets! It could make China far more open to foreign investment at the expense of the US.

6. A new AI run Fusion energy source creates massive energy abundance and solves absolutely everything ushering in a new age of plenty? Lovey idea, but everyone knows fusion power is always, always 10-years down the road.

7. Universal Basic Income, mass unemployment, working from home decimates cities and moves life back to the country – it’s happening. Society is changing!

8. Silver price rises on soaring solar power demand. Why Not?

9. The idea of a Disruption Dividend Citizens Tech fund in response to rising inequality is an interesting idea – moving/transferring assets from the wealthy to the general population in order to rebalance work/life. I like the idea…

10. A new tech revolution, including satellite based systems, drone tech and new batteries, new ways of making things and an acceleration in productivity from AI and robotics, and automation across whole sectors will create a new industrial revolution! I reckon its already underway, and will have ramifications across the global economy and society.

The thing about all these predictions from Saxo is they are all investible – but for some of them only to a limited number of investors able to take illiquid, not-regulated positions – for instance in Frontier and Venture Capital.

Doing anything in Financial Assets at present is fraught with risk because of just how hyper-inflated stock and bond prices have become. You can’t make meaningful real returns in liquid assets and it’s difficult to buy the higher return Private Debt and Private Equity deals that do promise substantial returns. Therefore, you need to take risk to make returns.

Yesterday I highlighted a Venture Capital deal we’re financing through our Alternative Assets desk here at Shard Capital. I neglected to mention the deal is very much targeted at institutional investors only, but it turns out the “Morning Porridge” is very widely read on sites like Zerohedge that I got deluged in emails from retail investors wanting to know more. Unfortunately, the rocket deal – in its current format – is not for them.

One of the things I intend to do next year is work with my investment colleagues at Shard to identify some of the more interesting alternative issue strategies that we can put in place for knowledgeable, well informed, smaller investors to access. For a start, if you are looking for an entrée to new tech, check out or Sure Valley Fund.

Meanwhile… Tesla does it again!

Two years ago the bet driving the shorts was Tesla would go bust before it could possibly succeed. It was racing to build 500k cars per annum while trying to avoid going down. The numbers all suggested it was skinny on cash and likely to face a solvency crisis. It dodged, dived and pulled the wool as many times as possible.

Not any more. Tesla has raised $7 bln from equity markers already this year, and yesterday its coming back to market for a further $5 bln of effectively free money, building a cash pile big enough to do all kind of interesting things with. Here was me thinking Tesla might get acquired by a big auto player. Silly me… its Tesla that may be the predator in the room.

Its extraordinary… Tesla is heading towards becoming one of the most valuable, cash rich firms on the planet, powered solely by investor belief! Tesla now has over $14 bln cash at hand. GM produces a multiple number of cars profitably, but trades on 8x earnings. Tesla makes no money selling cars and trades on 1400x. Yet…

If anyone else thinks that’s hatstand.. let me know..

Meanwhile, for all the hype about what a great guy Musk is, and what a wonderful company it is… check out this story about how shabbily Tesla treated a female engineer. All that glitters is not gold.

* * *

This is the last week of this year’s charity appeal – raising money for Walking With The Wounded, helping ex-military with mental health issues. My wife and I areTeam Morning Porridge. Please read about the charity and make a donation.

via ZeroHedge News https://ift.tt/33TvoYD Tyler Durden

Futures Hit New All Time High As Manic Melt Up Won’t Stop Tyler Durden

Wed, 12/09/2020 – 08:04

The market meltup just won’t let up, with futures and global stocks reaching new record highs on Wednesday as sentiment was stoked after Treasury Secretary Steven Mnuchin unveiled a surprise $916 billion pandemic-relief package proposal (which was quickly slammed by Pelosi and Schumer) coupled with now daily positive news on COVID-19 vaccines, overshadowing fears about resurgent coronavirus cases while sterling made gains as British and European leaders meet for talks on a Brexit trade deal. Treasuries dropped as did the dollar, while the Chinese yuan surged above 6.50 for the first time in 2 years.

MSCI’s index of world stocks rose to a record 635.65, up 0.23%. The index has been on a roll for weeks, gaining 15% since the beginning of last month. Global equities were “energized” after the White House’s surprise re-entry into pandemic-relief talks with a $916 billion proposal late on Tuesday that opened a potential new path to a year-end deal.

As of 7:30am Dow e-minis were up 76 points, or 0.28%, S&P 500 e-minis were up 5 points, or 0.14% to a new all time high, and Nasdaq 100 e-minis were down 15 points, or 0.08%. U.S. banks JPMorgan Chase and Citigroup as well as industrial bellwethers Boeing and 3M rose about half a percent. Car-battery producer QuantumScape surges 27% in premarket trading, adding to a 31% jump on Tuesday.

Travel stocks including United Airlines and American Airlines Group Inc gained 1.3% and 2.7% amid new covid hopes: the race for a vaccine narrowed on Tuesday after the FDA raised no new issues about the safety or efficacy of Pfizer’s candidate, while Johnson & Johnson reported it could obtain late-stage trial results for a single-dose vaccine earlier than expected. Both drugmakers’ shares gained about 1% in early trading, as did Moderna. Joe Biden also vowed that his administration would vaccinate 100 million Americans during his first 100 days in office, push to reopen schools and strengthen mask mandates.

“Momentum will be a little bit less than it has been. There are certain questions to be answered about the logistics of the vaccines, and vaccines don’t change the winter picture for the virus, but we are expecting positive returns for next year … there’s a lot going for the global economy,” said Seema Shah, chief global strategist at Principal Global Investors.

Separately, Congress continued to negotiate on a long-awaited coronavirus relief package, but provisions on liability protections for businesses and aid to state and local governments are causing divisions between Republicans and Democrats. Late on Tuesday, the Trump administration proposed a new $916 billion aid package on Tuesday, after congressional Democrats shot down a suggestion for a pared-down plan.

As Bloomberg notes, with little time left before the year-end holiday break and no let-up in Covid-19 cases in some of the biggest economies, investors are clinging to prospects for an 11th-hour stimulus deal and more progress on vaccine roll-outs. Emergency-use authorization for Pizer’s shot in the biggest economy may come as early as Thursday.

The opportunities are “in equities and credit, so we are overweight, we are risk on,” Richard Lacaille, global chief investment officer at State Street Global Advisors, said on Bloomberg TV. “We know that we will be tested again next year in terms of Covid and elsewhere.”

In Europe, equities reached their highest level since February but traded slightly off best levels, fading an early DAX-led rally, with the Stoxx 600 trading 0.5% higher as pro-cyclical mining and chemical firms led gains, and travel, autos and insurance companies also outperformed. The German DAX index gained 0.9% and Britain’s FTSE 100, which has been hardest hit of the main global indexes this year, added 0.36%. However, Britain injected a note of caution into the vaccine euphoria, saying people with a history of significant allergic reactions responded adversely to the Pfizer vaccine.

Earlier in the session, MSCI’s index of Asia-Pacific shares ex-Japan rose 0.6%, touching a record high. Japan’s Nikkei rose 1.3% to approach a 29 1/2-year high. South Korean stocks also jumped by 1.6% to trade near a record high after falling on Tuesday. Shares in China bucked the trend and fell 0.7% on profit taking. SoftBank shares rose almost 6% in Tokyo after Bloomberg reported it’s debating a new strategy to go private (now that the Nasdaq Whale is a distant memory). And machinery orders in Japan jumped at the fastest pace in more than a decade, adding to signs that the global economy is continuing to recover from the pandemic.

In rates, Treasuries retreated and curves steepened as hopes for a U.S. stimulus deal dented demand for havens. Treasury 10-year yields at ~0.94% were 2.2bps higher on day, vs 2.6bp increase for U.K. 10-year, 1.2bp for German bunds. Portugal’s 10-year bond yield, which fell this week to a record low of -0.01%, was trading at zero. “That caps off a remarkable journey from the height of the sovereign debt crisis, when in early 2012 (the yield) was trading above 18% intraday,” Deutsche Bank analysts said in a note. Spain’s 10-year yields could be next to go sub-zero.

Crude futures give back early gains. WTI reverses a move up to $46.24 to trade little changed; Brent fades a similar move to trade near $48.90. Spot gold holds a narrow range near $1,860/oz. Base metals trade in the green with LME aluminum and zinc outperforming.

In FX, the Bloomberg Dollar Spot Index fell, erasing a two-day advance, and the greenback weakened against all Group-of-10 peers amid an advance led by risk-sensitive currencies in the wake of the U.S. relief proposal. The euro advanced, ending a three-day decline, but stayed within recent trading ranges; bunds edged lower, yet outperformed Treasuries. The pound rallied above $1.34, boosted by a broadly weaker dollar, as traders positioned for a meeting between U.K. Prime Minister Boris Johnson and European Commission President Ursula von der Leyen in Brussels. British Prime Minister Boris Johnson heads to Brussels on Wednesday for a meeting over dinner with European Commission President Ursula von der Leyen in a push to avoid a turbulent breakup in three weeks. There was a glimmer of hope on Tuesday after Britain said it would drop clauses in draft domestic legislation that breach the already agreed Brexit divorce settlement, after reaching an “agreement in principle” with the EU over how to manage the Ireland-Northern Ireland border.

Elsewhere, the Aussie dollar pushed toward its strongest close in more than two years, catching the updraft from the highest consumer confidence reading in a decade and hawkish views on the central bank’s likely stance. China’s offshore yuan pared an advance after earlier breaching the key 6.5 per dollar level for the first time since 2018. HUF and PLN were the best EM FX performers, bolstered by positive news on EU stimulus.

In commodities, oil prices rallied as the positive vaccine news lifted investor hopes for a recovery in fuel demand. Brent crude futures rose 15 cents to $48.99 a barrel. WTI futures gained 13 cents to $45.73. Spot gold fell 0.9% as the start of vaccine treatment reduced safe-haven demand for the precious metal.

On today’s calendar, we get data on mortgage applications, wholesale inventories and the JOLTS job openings from the US for October. There are also monetary policy decisions from the Bank of Canada and the Central Bank of Brazil.

Market Snapshot

S&P 500 futures up 0.2% to 3,711.00

STOXX Europe 600 up 0.4% to 395.35

MXAP up 0.8% to 195.03

MXAPJ up 0.6% to 646.21

Nikkei up 1.3% to 26,817.94

Topix up 1.2% to 1,779.42

Hang Seng Index up 0.8% to 26,502.84

Shanghai Composite down 1.1% to 3,371.96

Sensex up 1.1% to 46,107.01

Australia S&P/ASX 200 up 0.6% to 6,728.47

Kospi up 2% to 2,755.47

Brent futures up 1.1% to $49.39/bbl

Gold spot down 0.6% to $1,860.17

U.S. Dollar Index down 0.2% to 90.77

German 10Y yield rose 0.7 bps to -0.6%

Euro up 0.2% to $1.2125

Italian 10Y yield fell 2.0 bps to 0.479%

Spanish 10Y yield rose 0.5 bps to 0.034%

Top Overnight News from Bloomberg

Global central banks are embarking on fresh waves of bond-buying to fight the fallout from the pandemic, despite mounting claims that the once-mighty policy is losing its power to boost the economy

Poland and Hungary have agreed on a compromise with Germany to unblock the European Union’s $2.2 trillion budget and pandemic stimulus plan, a senior government official in Warsaw said

China’s state-backed coronavirus vaccine protected 86% of people against Covid-19 in trials conducted in the United Arab Emirates, state media there reported, giving credence to the quickly developed shot that China intends to distribute around the developing world

Chancellor Angela Merkel urged Germans to make an additional sacrifice over the Christmas holidays to contain the coronavirus as daily coronavirus-related deaths rose the most since the outbreak began

About seven weeks before the inauguration, Biden’s picks for top administration slots are making clear that economic restrictions on countries will remain an essential tool, even if they don’t like everything about the way Trump used them

Norway’s mainland gross domestic product, which adjusts for Norway’s offshore industry, expanded 1.2% in October from the previous month, the Oslo-based statistics office said on Wednesday. That’s three times the bounce expected by analysts surveyed by Bloomberg, strengthening the case for the central bank to be among the first to raise interest rates

While trial results published Tuesday in The Lancet found that a vaccine developed by the University of Oxford and AstraZeneca Plc is safe and effective, more analysis will be needed to see how well it works in people over 55, among those at higher risk from the pandemic

A quick look at global markets courtesy of NewSquawk

Asia-Pac bourses traded positively as the region took impetus from the record highs on Wall St with sentiment underpinned by ongoing vaccine optimism and amid stimulus hopes which were also spurred after US Treasury Secretary Mnuchin presented a USD 916bln coronavirus relief proposal, although key Democrats have since labelled it as unacceptable as it cuts unemployment insurance from the bipartisan proposal. ASX 200 (+0.6%) was led higher by outperformance in the healthcare sector amid firm gains in Healius following its performance update and share buyback announcement, with an improvement in Westpac Consumer Sentiment contributing to the tailwinds. Nikkei 225 (+1.3%) was lifted after stronger than expected Machinery Orders which jumped 17.1% for the month of October and as exporters found reprieve from a pause in the recent currency appreciation, while SoftBank shares surged on reports that the Co. was said to be in discussions on going private through a slow burn buyout in which it could gradually repurchases shares until its founder can squeeze out other investors. Hang Seng (+0.8%) and Shanghai Comp. (-1.1%) were mixed with Hong Kong conforming to the overall upbeat mood, although the mainland lagged amid currency strength and ongoing tensions after China’s Vice Foreign Minister summoned the US embassy representative over US sanctions on Chinese officials and reiterated to take reciprocal countermeasures. The release of Chinese inflation data was also discouraging as CPI printed in negative territory at -0.5% and its lowest since 2009 which although was mostly due to a 2% drop in food inflation and in particular a 12.5% slump in pork prices, it still highlighted a weak consumer profile given that non-food CPI also contracted by 0.1%. Finally, 10yr JGBs were flat with the prior day’s upside losing steam amid gains in stocks and an overnight pullback in T-notes, with demand also sapped by the lack of BoJ presence in the market today.

Top Asian News

UAE Says Sinopharm Vaccine Has 86% Efficacy Against Covid-19

First Electric Air Taxis Set to Fly in Singapore by 2023

Indonesia Virus Deaths at Record High on Local Election Day

Stocks Push Higher Amid U.S. Stimulus Wrangling: Markets Wrap

Central Banks Step Up $5.6 Trillion Bond Binge Despite Doubts

European equities (Eurostoxx 50 +0.5%) are on the front-foot following on from an upbeat Asia-Pac handover and further record highs on Wall St. Sentiment has been underpinned by ongoing vaccine optimism and stimulus hopes with the latter spurred after US Treasury Secretary Mnuchin presented a USD 916bln coronavirus relief proposal which included money for state and local governments, as well as liability protections for businesses. The proposal was later deemed as unacceptable by House Speaker Pelosi and Senate Minority Leader Schumer as it cut unemployment insurance, however, they noted that Senate Majority Leader McConnell agreeing to the White House proposal was progress. Closer to home in Europe, beyond the ongoing Brexit stalemate, attention is firmly fixated on tomorrow’s crunch ECB meeting in which policymakers have set the bar for a “dovish surprise” particularly high (a full preview of the event can be found in the Newsquawk research suite). From a sectoral standpoint all sectors, with the exception of IT names trade firmer with the tech sector hampered by losses in STMicroelectronics (-9%) after the Co. abandoned its EUR 1bln sales target by a year to 2023; Infineon (-0.5%) are seen lower in sympathy. In terms of broader follow-through to equities in the US, the tech-heavy e-mini Nasdaq is flat on the session, lagging the e-mini S&P and Russell 2000 which trade higher by 0.2% and 0.7% respectively. To the upside, energy names are the clear outperformers, supported by modestly firmer crude prices with other cyclically exposed sectors such as autos and banks also near the top of the leaderboard. Corporate updates are once again on the light side with two standouts being German-listed Covestro (+4.6%) after upgrading its FY 20 EBITDA and FCF guidance, whilst Signify (-5.4%) are a noteworthy loser after announcing it expects the COVID-19 pandemic to impair sales by 13-13.5%.

Top European News

Deutsche Bank’s Loetscher Steps Aside Pending Wirecard Probe

U.K. Urged to Levy $350 Billion Wealth Tax to Pay for Pandemic

French Retailer Casino Unveils Debt Plan to Bolster Finances

UniCredit May Consider Deal With BPER Under a New CEO, Sole Says

Norway GDP Surprise Shows Pandemic Grip Weaker Than Feared

In FX, all eyes on Sterling as PM Johnson gears up for a make-or-break evening meeting with EU’s von der Leyen (19:00GMT/14:00EST) in the run up to the European Council meeting tomorrow. In terms of the lie of the land, optimistic omens came out of the UK’s Cabinet Minister Gove in early hours intimating scope for compromise on fisheries, whilst Irish Deputy PM Varadkar expressed a similar tone but noted the LPF remains the most difficult outstanding issue. Nonetheless, Cable garnered impetus from the comments whereby the pair rose to a fresh session high at 1.3460 (vs. low 1.3350) surpassing Monday’s peak and the psychological 1.3450 mark. Subsequently, flows into Sterling translated into pressure on the EUR/GBP cross which dipped below 0.9050 from 0.9081 at best to a current base at 0.9035. As such, EUR/USD fails to fully benefit from the softer Buck but retains its 1.2100+ status having had risen to a whisker away from 1.2150 before it side-lined the wider-than-expected German trade data for October.

DXY, Yuan – The broad Dollar and Index kicked off the mid-week session on the back foot, with some downside pressure seen in light of the Sterling bounce, but with attention remaining on State-side negotiations over government funding and the COVID relief bill. DXY remains sub-91.000 after printing an overnight base around 90.700 with the next immediate downside level comprising of Monday’s 90.612 low followed by the psychological 90.500 mark. Elsewhere, the strengthening Yuan garnered focus overnight whereby the offshore hit the firmest level against the Buck since June 2018 despite a relatively stable PBoC fix and discouraging Chinese CPI figures. USD/CNH printed a base at 6.4975 with bears now eyeing the 76.4% retracement of the 2018 low to the 2019 high at 6.4626.

AUD, NZD, CAD – The high-beta non-US Dollars see gains across the board amid tailwinds from the positive risk sentiment coupled with follow-through from the firmer Yuan. Sources overnight suggested Chinese trade officials are unlikely to reassess their bilateral free-trade agreement with Australia this month as outlined in the ChAfta deal. The news has seen varying interpretations, with one suggestion being the deal signed with goodwill remains intact despite the ever-deteriorating ties between the countries, whilst others suggests this takes away a platform for negotiations to improve ties. Nonetheless, the Aussie outpaces its peers vs. the USD following a breach of 0.7450 to the upside from its overnight low of ~0.7400 to a current peak at 0.7471 with the next level to the upside around 0.7486 marking the highs set on the 9th and 10th July 2018. NZD/USD meanwhile continues to gain ground above 0.7050 (vs. low 0.7036). The Loonie is also supported as USD/CAD remains sub-1.2800 (vs. high 1.2822) but remains cautious in the run up to the BoC policy announcement (full preview available in the Newsquawk Research Suite).

JPY – Contrary to its G10 peers, the Yen fails to glean support from the softer Dollar as haven outflows hamper gains. USD/JPY remains contained within a tight 104.07-25 band in early European trade with OpEx seeing USD 704mln rolling off between 104.40-50 and USD 750mln at strike 104.65.

In commodities, WTI and Brent front-month futures have erased overnight losses as the complex piggy-backed on the positive risk tone in broader trade with gains of some USD 0.40/bbl apiece. Losses overnight stemmed from the private sector inventory report which showed a surprise build in headline crude and larger than expected build to gasoline stockpiles at 6.4mln (exp. 2.3mln), whilst the EIA STEO also cut its world oil demand growth forecasts for 2020 and 2021, with the OPEC and IEA’s respective monthly reports due next week. Notwithstanding yesterday’s bearish supply/demand side updates, WTI Jan hovered around USD 46/bbl (vs. low 45.33/bbl) before losing ground below the figure whilst Brent Feb sees itself just south of USD 49/bbl (vs. low 48.54/bbl). Looking ahead, the weekly DoE inventory figures will be released at the usual time, with headline crude stocks expected to see a draw of 1.424mln bbls. Elsewhere, precious metals are relatively uneventful and lacklustre with the former still north of USD 1850/oz, but off its overnight high of 1871/oz, whilst spot silver sees itself under USD 24.50/oz (vs high 24.58/oz). In terms of forecast, Commerzbank anticipates gold will approach USD 2100/oz by end-2021 whilst the German bank sees silver at USD 28/oz in the same timeframe. In terms of base metals, iron ore prices hit the highest level since March 2013 amid firm demand from steel plants coupled with woes surrounding the deteriorating Aussie-Sino relationship, prompting China’s Dalian Commodity Exchange to limit non-future members’ single day open position for iron ore futures for May 21 delivery to 5k lots from Dec 14th. Finally, LME copper is firmer on the day as the red metal sees tailwinds from the softer Buck and constructive risk tone.

Yesterday was a landmark day as the first non-trial Covid vaccine was administered to the Developed World population. This happened here in the U.K. to a 91 year old lady called Margaret Keenan. However the first man to be vaccinated was William Shakespeare which is taking prioritising the elderly to new heights as according to Wikipedia he is now 456 years old. On a serious note his name sake was 81 years old and his family suggests they may have been related to the famous playwright. Good publicity for the vaccine.

Anyway to be vaccinated or not to be vaccinated, that is the question. This brings us nicely onto our monthly survey which we launch today and will keep open until this Friday December 11th at 11AM BST. You can fill it in here. The bulk of this month’s survey is covering your views on vaccines, Covid-19 and the impact it’s having on your life and the world around you – including several new questions along with selected ones from prior months to enable us to see trends. We also have a few market-related questions and have added a few 2021-specific questions as well as a fun Christmas one at the end. All help greatly appreciated as ever.

Moving onto markets and risk assets recovered steadily all day yesterday and hit a fresh record high in the US at the close after a tougher early session. The grind higher in equities can be partially attributed to legislative headway on fiscal stimulus in the US as well as news that the UK government dropped controversial parts of the Internal Market Bill. The S&P 500 rose +0.28% even if there was continued rotation under the surface, though not necessarily led by cyclicals. The odd pairing of Energy (+1.57%) and Biotech (+1.26%) helping lead the broad index higher, while Autos (-0.44%) and Consumer Durables (-0.65%) were among the worst performers. Europe rose a similar +0.20%, though the threat of renewed or elongated lockdowns saw a return of cyclical caution. Travel & Leisure (-1.00%), Retail (-0.69%) and Banks (-0.63%) were the worst three sectors, while Personal Care Drug Stores (+1.19%) and Media (+0.96%) were the best.

As noted above, US stimulus talks took a more positive turn with Senate Majority Leader McConnell suggesting that the two parties set aside their top priority demands – State and Local aid for Democrats and business liability protections for Republicans – in order to reach deal to “pass those things that we can agree on knowing full well we’ll be back at this after the first of the year.” He went on to acknowledge that “the new administration is going to be asking for another package.” This may not be suitable for Democrats, as Senate Minority Leader Schumer said that the state and local aid funds were necessary for “thousands of workers, including police and firefighters.” However the conciliatory tone was welcomed by markets, which reached intraday highs shortly after McConnell’s comments. After the market closed, Treasury Secretary Mnuchin presented a new $916 billion bill to Speaker Pelosi, which was the first salvo from the Trump Administration since just before the election. “This proposal includes money for state and local governments and robust liability protections for businesses, schools and universities,” Mnuchin said. It was a joint proposal from the White House, the House minority leader McCarthy and McConnell, and though Pelosi and Schumer put out a statement saying the deal was “progress” they wanted to keep working on the bipartisan framework already making its way through Congress. They also said that “The President’s proposal starts by cutting the unemployment insurance proposal being discussed by bipartisan Members of the House and Senate from $180 billion to $40 billion. That is unacceptable”

US 10yr Treasuries yields fluctuated with the stimulus news and were down 3bps shortly after the New York open before ending nearly unchanged (-0.5bps) at 0.918%. They are a further 2bps higher overnight. European sovereign bond markets earlier rallied strongly as the focus turns to tomorrow’s ECB meeting, where it’s anticipated there’ll be a further easing of the monetary policy stance. 10yr bunds fell -2.5bps to -0.607% while gilts fell -2.6bps to 0.26%. A whole array of new records were set, with perhaps the most notable being that Portugal’s 10-year yield closed in negative territory for the first time, at -0.006%. That caps off a remarkable journey from the height of the sovereign debt crisis, when in early 2012 it was trading above 18% intraday. Given the moves yesterday, Spain might be next to join the negative rates club, with its own 10-year yield falling to an all-time low of 0.029%, as Italy’s similarly fell to an all-time low of 0.590%.

On the vaccine, we now have the publication of detailed trial results for the AstraZeneca/Oxford vaccine, which confirm the original findings that giving patients an initial half dose and then a full dose was the more effective method, with an efficacy rate of 90%. Though it’ll require further analysis to see how it affects the elderly, that was because older adults were brought into the studies later so there’s been less time to study those age groups. In the US, the FDA published a report indicating that the Pfizer vaccine is highly effective in preventing Covid-19 and that there are no safety concerns that would prevent it from being granted an emergency-use authorization. This comes ahead of the meeting on Thursday of outside advisers to the agency, after which the FDA can clear the vaccine for immediate use.

Overnight in Asia, markets have largely taken Wall Street’s lead with the Nikkei (+1.00%), Hang Seng (+1.06%), Kospi (+1.54%) and Asx (+0.61%) all advancing. Chinese bourses are trading a bit more mixed with the Shanghai Comp (+0.06%) up while the CSI (-0.12%) and Shenzhen Comp (-0.53%) are down. Meanwhile, S&P 500 futures are up +0.23% while the US dollar index is down -0.16% and yields on 10y USTs are up +2bps to 0.940%. In commodities, spot gold prices are down -0.55% to $1860.31/oz. In terms of data this morning, China’s November CPI fell -0.5% yoy (vs. 0% yoy expected) , making this the first contraction since October 2009 while PPI came in at -1.5% yoy (vs. -1.8% yoy expected). Elsewhere, Japan’s October core machine orders printed at +17.1% mom (vs. +2.5% mom expected), marking a record gain with comparable data going back to 2005. Its worth nothing that the data series is quite volatile though.

Turning to the latest on the virus, it is continuing to spread at an accelerated pace in the US as the country reported 218,310 cases in the past 24 hours. Meanwhile in Europe, Switzerland has said overnight that it will reduce opening hours for shops and restaurants from December 12 to January 20 and has indicated that measures could be tightened further on December 18, when restaurants and shops might be asked to shut altogether, if caseloads don’t come down. France’s Health Minister Veran has also said that the country could introduce a new curfew or stick to the current lockdown for some additional days as the number of virus cases continues to remain high. This comes ahead of further scheduled easing of restrictions on December 15 and the French government is supposed to discuss the situation today with an announcement due before end of the week. For more on the virus spread see the table below.

In terms of the latest on Brexit, UK Prime Minister Johnson and European Commission President von der Leyen will be meeting in Brussels tonight. Not much new has happened in public over the last 24 hours. We did see a report from Sky News’ Europe correspondent that the EU’s chief negotiator Michel Barnier had told ministers yesterday morning that the chances of a deal were “very slim”. This continued nervousness has seen market jitters continue, with sterling weakening by a further -0.19% against the US dollar in its 3rd consecutive move lower, while 1-week sterling/dollar implied volatility rose to its highest level since March.

We did get a positive development yesterday as it was announced that an agreement in principle had been reached on a number of issues relating to the application of the already-reached Withdrawal Agreement, including on arrangements for Northern Ireland. As a result of this, the UK government announced that they’d be withdrawing the contentious provisions from their Internal Market Bill that would have enabled them to break international law. Though this doesn’t resolve the main issues in the trade talks, this does remove a stumbling block from the talks that led to major unease on the EU side.

Staying on EU politics, we got reports yesterday saying that hope for a deal with Hungary and Poland was increasing over their budget standoff, which could see the EU clarify how its rule-of-law mechanism would work. As a reminder, the two countries have vetoed the EU’s long-term budget and recovery fund over the fact that other member states wanted there to be conditions requiring EU countries to adhere to certain rule-of-law requirements in order for funds to be disbursed. However, these have been seen by both Poland and Hungary as unacceptable infringements on their national sovereignty, and in turn there have been threats to remove both countries from the recovery fund altogether if they didn’t lift their vetoes.

In Germany, the ZEW survey showed the expectations reading rising to a stronger-than-expected 55.0 (vs. 46.0 expected), up from the previous 39.0 reading in November. The current situation reading actually fell slightly however, down to -66.5 (vs -66.0 expected). Separately, the Euro Area’s GDP reading for Q3 was revised down slightly to show growth of +12.5% quarter-on-quarter (vs. flash +12.6%). And over in the US, the NFIB’s small business optimism index fell to 101.4 (vs. 102.5 expected).

To the day ahead now, and the data highlights include the JOLTS job openings from the US for October, as well as the German trade balance for that month. There are also monetary policy decisions from the Bank of Canada and the Central Bank of Brazil.

via ZeroHedge News https://ift.tt/39T8mF9 Tyler Durden

F-16 Fighter Jet Crashes In Michigan, Rescue Crews Search For Pilot Tyler Durden

Wed, 12/09/2020 – 07:57

A General Dynamics F-16 Fighting Falcon crashed in Michigan’s Upper Peninsula Tuesday night, according to WLUC.

The F-16 was assigned to the Wisconsin Air National Guard’s 115th Fighter Wing at Truax Field Air National Guard Base in Madison.

The Wisconsin National Guard’s Facebook account said that the aircraft was on a “routine training mission at the time of the incident.” The crash occurred around 8 p.m. Tuesday.

An F-16 Fighting Falcon assigned to the Wisconsin Air National Guard’s 115th Fighter Wing at Truax Field Air National Guard Base in Madison crashed in Michigan’s Upper Peninsula at approximately 8 p.m. Tuesday, December 8, 2020.

At the time of the incident, the aircraft was on a routine training mission with one pilot on board.

Emergency responders are on scene. The cause of the crash, as well as the status of the pilot, are unknown at this time, and the incident is under investigation.

The 115th Fighter Wing will provide an update via the 115th Fighter Wing website and social media pages as soon as additional details are available.

An F-16 Fighting Falcon assigned to the Wisconsin Air National Guard’s 115th Fighter Wing at Truax Field Air National…

The cause of the crash is still under investigation – as well as there is no word on the status of the pilot. WLUC said emergency responders had been dispatched to the incident scene.

“Emergency responders are on scene, searching for the pilot, with more crews expected to arrive by daylight. Poor cell phone connectivity in the very rural area is hindering communication efforts,” said WLUC.

via ZeroHedge News https://ift.tt/36X7zkP Tyler Durden

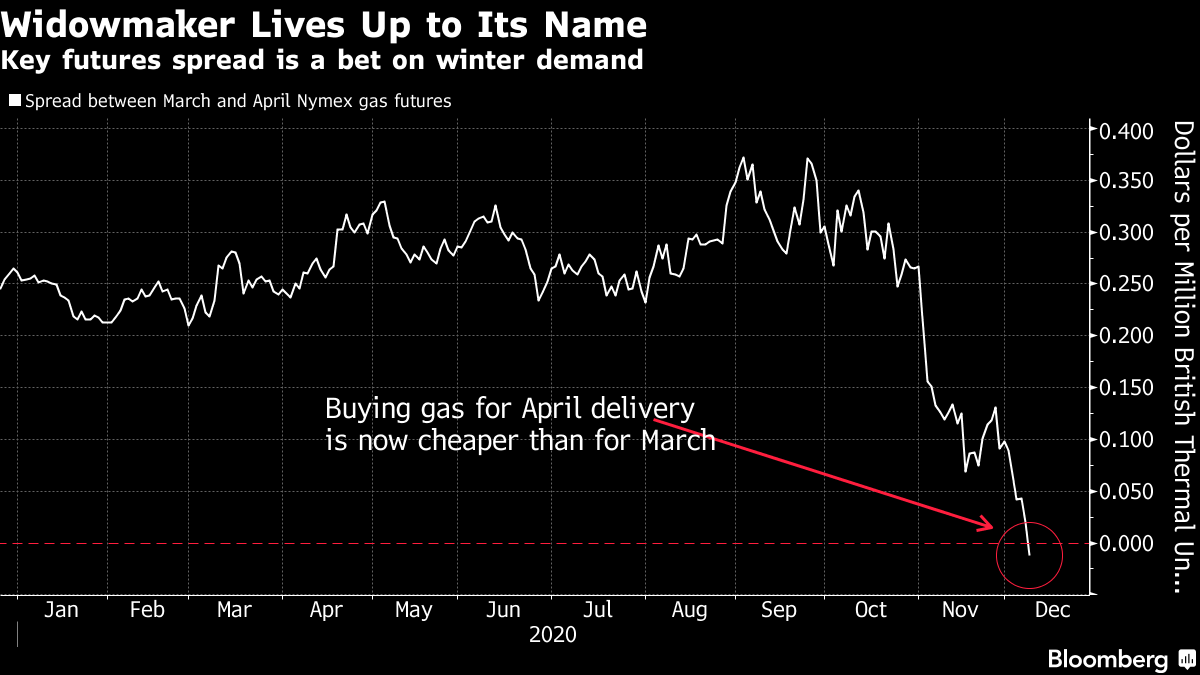

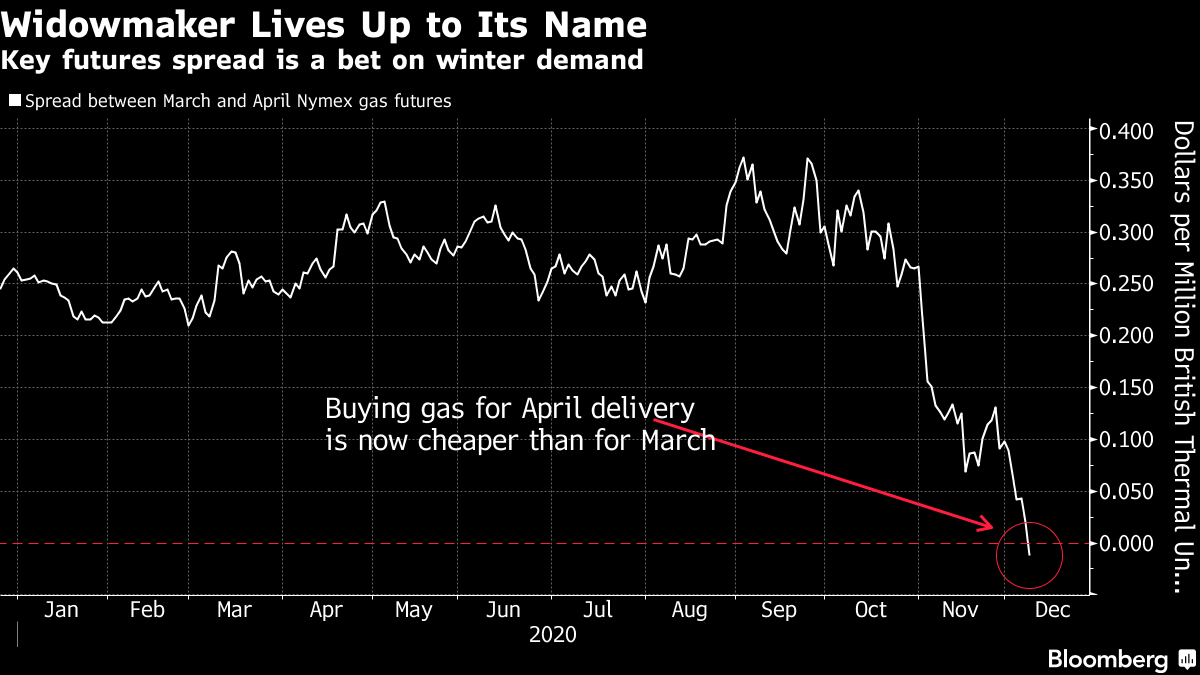

“Widowmaker” Nat Gas Trade Plunges On Mild Start To Winter Tyler Durden

Wed, 12/09/2020 – 07:40

The spread between March and April natural gas futures collapsed to zero on Tuesday. The spread is critical in gauging how tight supplies will be for the North American winter. In one of the earliest collapses to less than zero, for the first time since 2015, this suggests traders are forecasting a mild winter that will dent energy demand.

Bloomberg calls the collapse in the spread the “widowmaker.” It’s a signal that traders are giving up on hopes of a frigid U.S. winter.

“It’s a significant event,” said Gary Cunningham, a director at Stamford, Connecticut-based Tradition Energy. “We may end winter with very strong gas inventories.”

Nat gas prices have tumbled since the start of November as persistent mild weather has caused inventories to rise rather than draw down with seasonal trends.

On Monday, we attributed the plunge in nat gas future prices on new weather models suggesting “December could end top 3 warmest all time.”

Earlier in the heating season, there was the anticipation of a colder winter, pushing prices up – but with the Lower 48 states now 25% through the winter heating season with mild temperatures expected – demand will be lackluster.

Newsmax Ratings Surge, Surpass Fox For First Time Tyler Durden

Wed, 12/09/2020 – 07:27

Before Nov. 3, neither OAN nor Newsmax could come anywhere close to matching, or surpassing, the ratings from America’s reigning king of cable: Fox News, the conservative-leaning news and opinion network that helped cultivate the base of GOP voters which Trump rallied to victory in 2016, has finally lost its crown.

According to media reports, Newsmax beat Fox News among the coveted 25- to 54-year-old demographic for the first time ever on Monday evening. The ratings win comes amid a breakthrough in the Trump Administration’s push to challenge the election results in the court of public opinion to try and “delegitimize” Biden’s presidency (just like how many on the left refused to accept Donald Trump as their president 4 yeas ago).

The battle has at times impacted Fox’s shares.

CNN’s Brian Stelter, who clearly likes to think of himself on the de facto “reporter of record” when it comes to covering the American media industry (the eptiome of naval gazing, as far as we can tell), broke the news late Tuesday.

“Before the election, Newsmax was not regarded as a formidable competitor to Fox; it was mostly dismissed as one of a handful of wannabe challengers,” CNN’s Brian Stelter reports. “But President Trump’s loss on Nov. 3 changed the cable TV calculus. Viewers who were frustrated when Fox admitted the truth of Trump’s loss sought other options,” and “Newsmax — and Kelly in particular — offered a safe space in which Biden was not called president-elect and Trump was not yet defeated.”

Of course, many on the left are blaming Fox’s “Fall From Grace” on the fact that it “stood up to Trump” by calling the vote for Biden, even as supreme court challenges and other questions remian unresolved. Trump’s most loyal followers are likewise repudiating Fox, and embracing Sinclair-owned Newsmax and OAN.

While this is only the first time any Newsmax programming blocks has topped Fox, we imagine it won’t be the last, particularly as Newsmax copies more and more of what worked at Fox, while filtering out everything that didn’t.

via ZeroHedge News https://ift.tt/3oFFft1 Tyler Durden

Meet The Little Known Investment Holding Up David Einhorn’s Greenlight Capital This Year Tyler Durden

Wed, 12/09/2020 – 05:45

Greenlight is finally having some respite after years of tough performance. Since the beginning of 2015, the fund has lost 34% while the broader market has done nothing but go up. Now, it’s about flat for the year.

But in 2020, his losing bets, which include shorting Netflix and Tesla, have been offset by a “years-long investment” in homebuilder Green Brick, according to Bloomberg. In 2020, the homebuilder has added 15 percentage points of performance, the article notes. The fund is down 1.1% through November and would be far better off without Green Brick’s contributions.

Greenlight owns almost 50% of Green Brick, which is outside the norm of Einhorn’s investing style: taking smaller stakes in companies while looking for deep value in longs and for bubbles to short.

And while Greenlight has sputtered, so has its AUM. The fund is down to $2.6 billion from $12 billion in 2015. Einhorn has averaged a 7% annual loss from 2015 to this January. The firm is “open to new investments” but there’s been “no sign of any takers,” Bloomberg writes.

Einhorn’s streak of great performance since starting the fund ended in 2015 – right about the same time that the markets became solely driven by Fed policy and company fundamentals (and macro data) stopped mattering. Thus, we had the birth of such public company gems as Tesla.

Green Brick, born of out Einhorn’s personal relationship with Texas developer Jim Brickman, went public in 2014 after Einhorn invested in 2009. With mortgage rates the lowest they have ever been and the Fed providing unlimited liquidity to hyperinflate real estate assets, the company’s stock has gone from $10 earlier this year, to $22. It’s up 22% last month.

And while Einhorn’s continued prognostications of a popping tech bubble still seem to be far off, Green Brick has helped his fund remain flat for the year where it would otherwise be down. The S&P, in the interim, is up 13.5%.

Einhorn said in August: “Our investing style is not a closet index of long value and short growth. We look for security-specific differences of opinion and hope to capitalize on being right and the market eventually seeing it our way.”

via ZeroHedge News https://ift.tt/3gsIHo8 Tyler Durden

Global debt is expected to soar to a record $277 trillion by the end of the year, according to the Institute of International Finance. Developed markets’ total debt—government, corporate, and households—jumped to 432 percent of GDP in the third quarter. Emerging market debt-to-GDP hit nearly 250 percent in the third quarter, with China reaching 335 percent, and for the year the ratio is expected to reach about 365 percent of global GDP. Most of this massive increase of $15 trillion in one year comes from government and corporates’ response to the pandemic. However, we must remember that the total debt figure had already reached record highs in 2019, before any pandemic and in a period of growth.

The main problem is that most of this debt is unproductive debt. Governments are using the unprecedented fiscal space to perpetuate bloated current spending, which generates no real economic return, so the likely outcome is that debt will continue to rise after the pandemic crisis is ended and that the level of growth and productivity achieved will not be enough to reduce the financial burden on public accounts.

In this context, the World Economic Forum has presented a roadmap for what has been called “the Great Reset.” It is a plan that aims to take the current opportunity to “to shape an economic recovery and the future direction of global relations, economies, and priorities.” According to the World Economic Forum, the world must also adapt to the current reality by “directing the market to fairer results, ensur[ing] investments are aimed at mutual progress including accelerating ecologically friendly investments, and [starting] a fourth industrial revolution, creating digital economic and public infrastructure.” These objectives are obviously shared by all of us, and the reality shows that the private sector is already implementing these ideas, as we see technology, renewable investments, and sustainability plans thriving all over the world.

We are witnessing in real time the proof that businesses adapt rapidly and provide better goods and services at affordable prices for everyone achieving a level of progress in environmental targets and welfare that would be unthinkable if governments were in charge.

This crisis shows that the world has escaped the risk of scarcity and hyperinflation thanks to a private sector that has surpassed all expectations in a seemingly unsurmountable crisis.

The overall message of the World Economic Forum sounds promising. Only three words spoil the entire positive message: “directing the market.”

The risk of governments taking these ideas to promote massive interventionism is not small.

The idea of the Great Reset has been quickly embraced by the most bureaucratic and government-intervened economies as a validation of rising government implication in the economy. However, this is incorrect.

The idea that governments will promote an economic system that reduces inflation, improves competition, and empowers citizens is more than farfetched. As such, the World Economic Forum cannot ignore the risk of government intervention within this idea of a Great Reset that does not need to be enforced, as it has already been in place for years.

Technology, competition, and open markets will do more for sustainability, social welfare, and the environment than government action, because even the best-intentioned governments will try to defend at any cost three things that go against the well-intentioned messages of the World Economic Forum: governments will continue to try to defend their national champions, rising inflation, and more control of the economy. Those three things work against the idea of a new world with better and more affordable goods and services for all, with better welfare, lower unemployment, and a thriving high-productivity private sector.

We should always be worried about well-intentioned ideas when the first ones to embrace them are those who are against freedom and competition.

There is an even darker part. Many interventionists have welcomed this proposal as an opportunity to wipe out the debt. It all sounds nice until we understand what it really entails. There is an enormous risk that governments will use the excuse of canceling part of their debt with a decision to cancel a large part of our savings. We must remember that this is not even a conspiracy theory. Most proponents of the modern monetary theory start their premise by stating that government deficits are matched by households and private sector savings, so there is no problem…Well, the only minor problem (note the irony) is matching one’s debt with another’s savings. If we understand the global monetary system, we will then understand that erasing trillions of government debt would also mean erasing trillions of citizens’ savings.

The idea of a more sustainable, cleaner, and social economic system is not new, and it does not need governments to impose it. It is happening as we speak thanks to competition and technology. Governments should not be allowed to reduce and limit citizens’ freedom, savings, and real wages even for a well-intentioned promise. The best way to ensure that governments or large corporations are not going to use this excuse to eliminate freedom and individual rights is by promoting free markets and more competition. Forward-thinking investments and welfare-enhancing ideas do not need to be nudged or imposed; consumers are already making companies all over the world implement increasingly higher sustainability and environmentally friendly policies. This market-oriented approach is more successful than letting the risk of interventionism and government meddling take hold, because once it happens it is almost impossible to undo.

If we want a more sustainable world, we need to defend sound money policies and less government intervention. Free markets, not governments, will make this world better for all.

The same massive government intervention that brought us here is not going to get us out of here.

via ZeroHedge News https://ift.tt/37M31wN Tyler Durden

UK Gangs Launch ‘Fast & Furious-Style’ Highway Thefts On Trucks To Steal PlayStation 5s Tyler Durden

Wed, 12/09/2020 – 04:15

The Times reports criminal gangs in the UK are launching daring raids on highways to steal PlayStations, TVs, mobile phones, cigarettes, and cosmetics from tractor-trailers, all while moving more than 50 mph.

Since the beginning of the year, police say at least 27 examples of these highway heists have been reported to authorities, including crooks climbing on the hood of a vehicle with cutting gear to break into the back of tractor-trailers to steal merchandise.

These highways thefts are something out of the Fast and Furious movies or Grand Theft Auto video games. Detectives are worried that criminals will be stepping up highway robberies ahead of Christmas.

The National Vehicle Crime Intelligence Service (Navcis) urged trucking companies to increase security measures on their routes to thwart such thefts. In the first nine months of the year, Navcis said it received 3,055 notifications of cargo crime.

The Times, citing one career criminal, said the weakest point of the supply chain, exposing valuable merchandise, are on highways, has increasingly become the focus for criminal gangs.

Here’s an example of a highway theft in Romania, while others are taking place across the globe.

In Baltimore, Maryland, criminal gangs have been robbing USPS, FedEx, UPS, and Amazon vehicles, and in some cases, actually stealing the vehicles.

We noted earlier that cargo theft across the US surged during the second quarter of the virus-induced downturn.

via ZeroHedge News https://ift.tt/2K6MQ4S Tyler Durden

Russia’s experimental Kalashnikov attack drones were tested during the ongoing conflict inside Syria, a new report revealed this week. The head of Rostec, Sergey Chemezov (state defense firm Rostec has at least a 25% stake in Kalashnikov), told reporters that the plane has proven itself well, and is very effective, despite its low power. In addition to reconnaissance aircraft, the Russian Ministry of Defense will also acquire military drones.

A report by RT Arabic revealed that these drones, which are new to the Russian military, were tested against enemy targets during the ongoing conflict inside the Syrian Arab Republic. Previously Fox News and others detailed the Kalashnikov suicide drones’ development.

Via Zala Aero Group

It is noteworthy to mention that the Kalashnikov complex last year displayed the Kub-BLA and Lancet kamikaze drones developed by its subsidiary. In fact, these devices are projectiles that fly in remote control mode over the battlefield and detonate upon reaching an enemy position.

The Kub-BLA carries a payload of about three kilograms, can fly for up to 30 minutes at a speed of 80-130 kilometers per hour and is able to hit the target regardless of its concealment and terrain.

The Lancet has two versions: Lancet 1 weighs five kilograms and carries one kilogram of payload and hits targets in a radius of 40 kilometers, and Lancet 3 carries a payload of three kilograms with a total weight of 12 kilograms.

The developer calls the vehicles “a smart multi-role weapon capable of independently searching for and destroying a specific target, unlike the Kub-BLA, it has a TV directive channel, thanks to which it does not lose video contact with the operator until it touches the target.”

It also described as dispensing with navigation via satellites, because they determine the coordinates from different sources and locations, and thus, the drone can strike in the air, on the ground, and in the water without needing additional infrastructure.

Other unmanned vehicles are also being tested in Russia, Chemezov added: “If we talk about the creation of medium-sized drones, we can also mention the Corsar drones, which can carry weapons.”

via ZeroHedge News https://ift.tt/3gpyGYU Tyler Durden

{kind=link}

{kind=link}