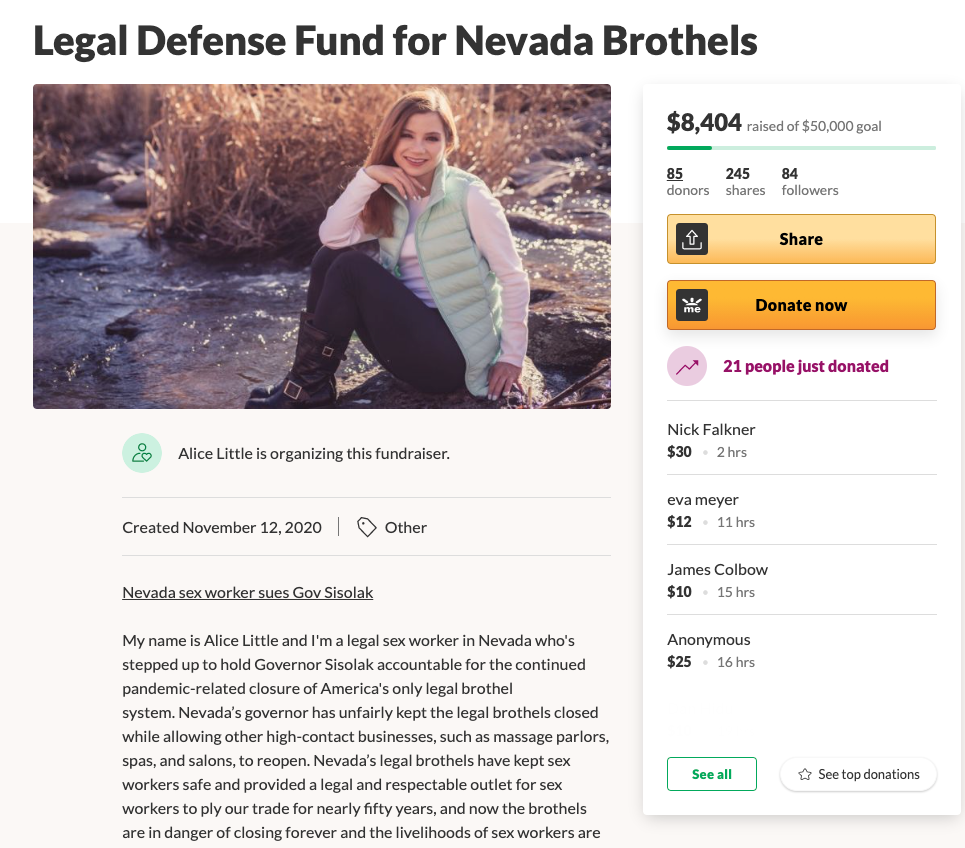

Alice Little, a legal sex worker in Nevada and quite possibly the highest-paid one in the US, is suing the state of Nevada to reopen its brothels, according to Yahoo Life.

Little is an employee at the BunnyRanch Legal Nevada Brothel in Mound House, Nevada. The brothel has been closed since Mar. 17, despite other “close contact” businesses reopening.

Little recently filed a complaint and motion for a preliminary injunction against Nevada’s Gov. Steve Sisolak in the Third Judicial District Court in Lyon County to reopen brothels. She cites unstated damages for her lost wages and seeks the right for her and other licensed sex workers to “ply their legal trade” at private locations.

The lawsuit said Sisolak has “without any rational basis, decided to single out brothels.”

Last month, a Nevada court ordered the state’s attorney general to respond to Little’s legal action within 30 days.

“It would be understandable if the governor kept all close-contact businesses closed. But the fact that massage parlors, estheticians, salons, escort services and other non-essential businesses have been allowed to reopen lead me to believe that the governor’s decision to keep brothels closed is just blatant discrimination against Nevada’s legal sex workers,” Little said in a press release.

“I just can’t let the governor arbitrarily decimate the livelihoods of an entire class of hard-working women. That’s why I decided to take legal action.”

Little is drumming up her legal battle with the state. She launched a GoFundMe campaign last month that has so far raised $8,404 for her legal defense.

The high-rolling hooker said her lawsuit has been “self-funded up to this point, and now I’m asking for your help to allow me to pursue this case all the way through to a successful victory.”

The Nevada Independent spoke with other sex workers who say the brothel shutdown is “discriminatory.”

Kiki Lover, an employee of the Sagebrush, told the local paper that Sisolak is “discriminating against sex workers,” adding that the industry’s collapse has forced many women out, and some are now homeless.

Little told Yahoo that the risk level of contracting COVID-19 is not that different from other services, such as a massage parlor.

In April, brothels were preparing to reopen, but eight or so months of closure, at the hands of the state government, has forced the industry into collapse.

via ZeroHedge News https://ift.tt/3lSxzC8 Tyler Durden

All right, that’s it. I’ve run out of patience. No more excuses. Where’s the Hitler?

Yes, you heard me. I’m talking to you. You respectable journalists and political pundits. You Intelligence officials and politicians. You fanatical liberals. You pseudo anti-fascists. All you members of the GloboCap “Resistance” who have been hysterically shrieking that “Trump is Hitler!” since he won the nomination back in 2016.

Well, OK, it’s November 2020. The show is almost over. When do we get Hitler?

No, do not tell me “any day now.” You’ve been telling us that for four straight years. Do we look like a bunch of gullible idiots that you can whip up into a four-year frenzy of mindless hatred and paranoia by screaming “Hitler!” over and over, and then not produce an actual Hitler?

Well, we’re not. We remember what you said. You promised us Hitler, and we want Hitler, or at least a decent facsimile of Hitler.

And don’t even think of trying to pretend that you didn’t actually promise us Hitler.

You did. You want me to prove it? OK.

Remember back in 2016, when The Wall Street Journal, The New York Times, The Guardian, the Washington Post, The Inquirer, and other such “leading respectable broadsheets,” and online magazines like Mother Jones, Forward, Slate, Salon, Vox, Alternet, and countless others, warned that Trump was sending secret anti-Semitic “dog whistle” signals to his underground army of Nazi terrorists by talking about “international banks,” “global elites,” the “political establishment,” and even “corporations” and “lobbyists” … all of which was supposedly code for “the Jews,” who he was going to exterminate if won the election?

Remember Aaron Sorkin’s letter to his daughter warning her that millions of “Muslim-Americans, Mexican-Americans and African-Americans [were] shaking in their shoes” as they waited for Trump to round them all up and send them to the camps, along with the “Jewish Coastal Elites”?

What about when the corporate media reported that Trump had called those tiki torch Nazis in Charlottesville “very fine people” (despite the fact that he demonstrably did not)? Or when they caught Trump calling somebody a “globalist”? (That episode was particularly disturbing to me, personally, as I had no idea that I was literally a Nazi until the corporate media and the ADL explained that talking about “global capitalism,” or “neoliberalism,” or, God help me, “banks,” was just Nazi codespeak for “Kill the Jews!”)

And who could forget when The New York Times published a full-blown dystopian fantasy in which Trump, Putin, Marine Le Pen, the AfD, and other notorious “globalist”-hating Hitler-alikes secretly formed an Evil Axis (the “Alliance of Authoritarian and Reactionary States”), dissolved the European Union and NATO, declared international martial law, and ethnically cleansed the world of immigrants? Or when they ran this propaganda film, “If You’re Not Scared About Fascism in the U.S., You Should Be!”

And the “emboldening”! I almost left out the “emboldening.” Surely, you remember when the corporate media reported that Trump was emboldening white-supremacist terrorism with his Hitlerian Tweets … as if homicidal racist psychopaths had been sitting around in their mother’s basements, semi-automatic rifles in one hand, smartphones tuned to Twitter in the other, just waiting to be “emboldened” by the president.

Look, the point is, you “Resistance” people promised us Hitler for four years straight, and now you’re acting like you just defeated Hitler, and, I’m sorry, but that is not going to cut it. We’re going to need some actual Hitler before we transition to the Brave New Normal, or we might start to … you know, doubt your credibility.

I mean, come on. Lawsuits? Recounts? Audits? Angry tweets? Golf, for Christsakes? This is not remotely Hitlerian behavior. You people promised us an attempted coup, a Reichstag fire, Nazi militias occupying the halls of Congress, stadiums full of Sieg-heiling rednecks, white-supremacist terrorists terrorizing everyone … and now all we get is Rudy Giuliani sweating rivulets of hair dye, or something, on TV? All right, granted, that was pretty scary, but it’s not exactly Joseph Goebbels fanatically barking about “total war,” or legions of Hawaiian-shirt-wearing fascists goose-stepping up Pennsylvania Avenue.

The way I see it, you people have got another four or five weeks to goad Donald Trump into going full-Hitler and staging a coup, or gratuitously mass-murdering the Jews, or somebody, or the public is going to feel … well, bamboozled, and insulted, and even a little angry. They are going to feel like you “Resistance” people regard them as a bunch of total morons that you can manipulate, over and over again, with blatantly ridiculous propaganda that anyone with half a brain could see through … some of which, frankly, has been downright offensive.

Seriously, fascism, Hitler, the Holocaust … these are solemn, sensitive subjects. They’re not just convenient emotional buttons that you can press to whip folks into a frenzy of mindless paranoia and murderous hatred whenever you feel like demonizing some foreign leader or unauthorized president.

The same goes for racism and anti-Semitism. These are real issues, which people care about. They’re not just glorified marketing buzz words that you can pull out of your bag of cheap tricks and slap onto your enemies like they don’t mean anything. If you spend four years accusing someone of literally being Adolf Hitler, or the resurrection of Adolf Hitler, and brainwash millions of credulous liberals into believing that America is on the brink of fascism, you can’t just suddenly say, “We were only kidding. We didn’t mean that he was actually Hitler, or that fascism was really on the rise.” People won’t stand for it. They’ll go ballistic. You’ll have some sort of revolt on your hands.

Or, all right, on second thought, maybe not. Maybe you can get away with pointing at some billionaire ass clown and howling “Hitler!” over and over, on a daily basis, for years and years, without ever providing any actual evidence that the ass clown in question resembles Hitler, or has done anything comparable to Hitler, or is in any way remotely similar to Hitler. Why not? You successfully Hitlerized Corbyn, not to mention Saddam, Gaddafi, and Milošević, and a long list of other “threats to democracy.” You’ll probably get away with Hitlerizing Trump.

After all, it appears you’ve convinced the public (or at least the vast majority of the public) that they are being attacked by an apocalyptic plague that causes mild to moderate flu-like symptoms (or, more commonly, no symptoms at all) in 95% of those infected and that over 99.7% survive, and thus we have to cancel constitutional rights, let government officials rule by decree, devastate the economy (or at least small businesses), have global corporations censor all dissent, force everyone to wear medical-looking masks, put whole societies under house arrest, psychologically terrorize children, and otherwise transform the planet into one big paranoid, totalitarian theme park.

If you can get people to go along with that … well, they’ll probably go along with anything.

via ZeroHedge News https://ift.tt/37JsIhG Tyler Durden

Tenants, Landlords Face Imminent Crisis As Pandemic Lifelines Expire Tyler Durden

Tue, 12/08/2020 – 23:05

January is going to be a mess. America’s small-time landlords, along with their tenants, are in trouble as safety nets are set to expire. Tenants haven’t paid rent in months, with a looming eviction moratorium expiring at the end of December. According to Reuters, the lack of rental income for landlords has also been troublesome, with many skipping mortgage payments, potentially resulting in a firesale of properties in the year ahead.

For 12 million Americans and their families – this Christmas will be their worst – as the extended unemployment benefits that have kept many of them afloat are set to expire later this month. Then on New Year’s Day, the Centers for Disease Control and Prevention’s eviction moratorium expires, which could result in a massive wave of evictions in the first half of 2021.

At the moment, $70 billion in unpaid back rent and utilities are set to come due, according to a new report via Moody’s Analytics Chief Economist Mark Zandi.

Last month, Maryland utility companies began to terminate customers with overdue bills, many of which were unable to pay because of job loss due to the coronavirus downturn.

New research from the Aspen Institute warns 40 million people could be threatened with eviction over the coming months as the real economic crisis is only beginning.

According to Stacey Johnson-Cosby, president of the Kansas City Regional Housing Alliance, landlords are also in deep turmoil. She said more than 40% of the landlords surveyed in her coalition said they will have to sell their units because of the lack of rental income.

“They are sheltering our citizens free of charge, and there’s nothing we can do about it,” said Johnson-Cosby. “This is their retirement income.”

She said small landlords are frightened to speak out about non-paying tenants because social justice warriors and their “Cancel Rent” groups have attacked landlords.

“What they don’t realize is that if they run us out and we fail, it will be private equity and Wall Street firms that buy up all our properties, just like they did with houses after the last foreclosure crash.”

Reuters interviewed Clarence Hamer, who may have to sell his house in the coming months because his “downstairs tenant owes him nearly $50,000.” He owns a duplex in Brownsville, Brooklyn – and without those rental payments, Hamer has been unable to pay his mortgage.

“I don’t have any corporate backing or any other type of insurance,” said Hamer, a 46-year-old landlord who works for the city of New York. “All I have is my home, and it seems apparent that I’m going to lose it.”

Hamer is not alone – millions of Americans are headed for a “dark winter” as they could be evicted or lose their homes in the coming months as government safety nets are set to expire.

Meanwhile, on Tuesday, stimulus talks quickly faded after it was reported that Senate Majority Leader Mitch McConnell touted his own plan rather than a bipartisan compromise for a deal.

John Pollock, a Public Justice Center attorney and coordinator of the National Coalition for a Civil Right to Counsel, recently said January could bring a surge of eviction and homelessness,” unlike anything we have ever seen” before.

via ZeroHedge News https://ift.tt/3oExp2P Tyler Durden

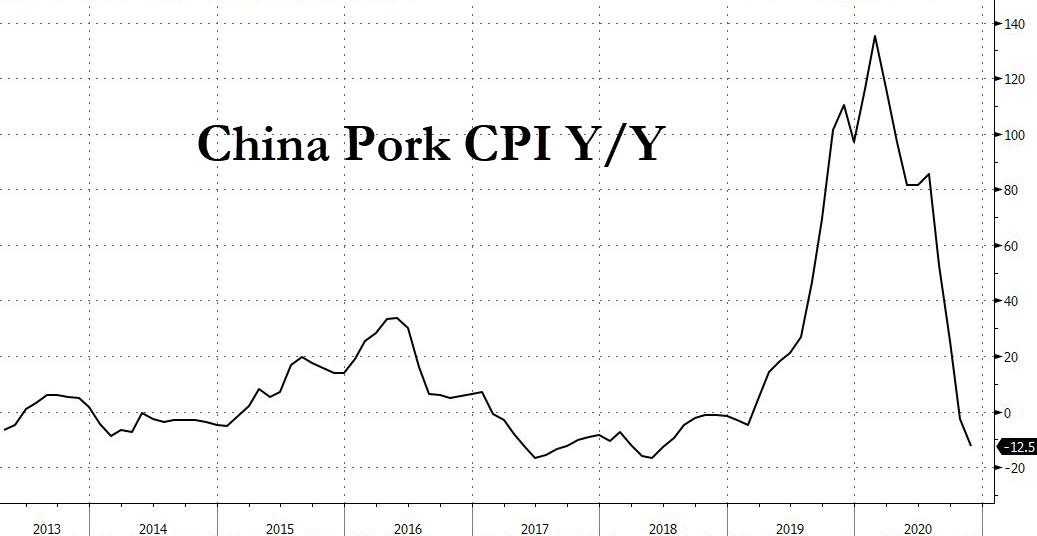

Deflation Is Back In China As CPI Turns Negative For First Time Since The Financial Crisis Tyler Durden

Tue, 12/08/2020 – 22:50

Yesterday, when discussing the biggest jump in Chinese FX reserves in 7 years we wondered if this was an indication that the PBOC was starting to lean against the surging yuan. Today, after the latest Chinese inflation data released moments ago, we are confident that it is only a matter of time before Beijing will once again aggressively intervene and/or devalue its currency.

According to the National Bureau Of Statistics, in November China’s CPI unexpectedly tumbled to -0.5% Y/Y in November, below market expectations and the first year-over-year decline in consumer prices since the financial crisis. While rapid decline of food prices continued to be the main driver for lower headline CPI inflation, non-food inflation also edged down to -0.1% yoy from 0% yoy in October, which begs the question: how much of China’s now deflation is the result of the surging yuan, and how much longer will Beijing tolerate the soaring currency (or, said otherwise, the plunging dollar). On the flip side, PPI inflation was at -1.5% yoy in November, which while still negative (the last positive PPI print was in January), was less negative than October as inflationary pressures increased along with the strong expansion of industrial activity.

Here are the key numbers:

CPI: -0.5% yoy in November, exp. +0.0%; down from October’s +0.5% yoy.

Food CPI: -2% yoy in November; October: +2.2% yoy.

Non-food CPI: -0.1% yoy in November; October: +0.0% yoy.

PPI: -1.5% yoy in November. exp. -1.8% yoy; up from October’s -2.1% yoy.

Some more details: in year-on-year terms, food inflation went down to -2.0% yoy in November from +2.2% yoy in October, largely because pork prices tumbled 12.5% on a year-over-year basis, lowering year-over-year CPI inflation by 0.6pp.

Egg prices also plunged, dropping 17.1% yoy, and lowering the headline CPI by another 0.1pp. Fresh vegetable prices rose albeit at a slower pace: Inflation in fresh vegetables was +8.6% yoy in November (vs 16.7% yoy in October), adding 0.2pp to headline CPI inflation.

Non-food CPI inflation edged down to -0.1% yoy in November, from 0.0% in October. Fuel costs fell further by 17.6% yoy, vs -17.2% yoy in October. Core inflation (headline CPI excluding food and energy) was unchanged at +0.5% yoy in November.

On the other side, PPI inflation rose modestly and was at -1.5% Y/Y in November, less negative than October. In month-over-month annualized terms, PPI rose by 5.6%, vs -1% in October. Price declines narrowed for producer goods (-1.8% yoy vs -2.7% yoy in October) but price decline for consumer goods widened (-0.8% yoy in November, vs -0.5% yoy in October) mainly on lower food and clothing price inflation. By major industry, PPI inflation increased on a year-over-year basis in most sub-industries except food processing and telecom industries.

According to Goldman, headline CPI inflation may remain at low levels in the coming months on falling food prices and a high base while PPI inflation could rise further as inflationary pressures continue to build in the industrial sector.

A bigger problem for China is that while PPI may be rising, it’s only a function of higher commodity prices and industrial strength on the back of massive credit injections; meanwhile consumer deflation is starting to emerge as a major concern for a country that has not had a negative CPI print since 2009.

One wonders how long Beijing will allow this, and how long will Chinese rates remain as high as they are, before the Politburo capitulates and realize it needs to aggressively devalued its soaring currency (and offset the tumbling dollar) if it hopes to keep deflation in check.

It may even have to decide between keeping interest rates highs, and thus yields on Chinese bonds attractive for foreign investors (as a reminder, everyone knows by now that one of Beijing’s top priorities is to have a steady source of offshore capital entering the negative current account nation), or finally conceding it needs to cut rates in order to let some of the air in the yuan out.

via ZeroHedge News https://ift.tt/33Sbq0n Tyler Durden

Fireworks, batteries and liquid ethanol were inside the 64 dangerous goods containers that went overboard with more than 1,750 others from the ONE Apus last week, whose plight we discussed over the weekend. None of the containers has been sighted.

In one of the single worst cases of container losses on record, 1,816 twenty-foot equivalent units (TEUs) were lost overboard after the year-old Apus reportedly encountered severe weather at about 11:15 p.m. Nov. 30 en route from Yantian, China, to the Port of Long Beach in California, the vessel’s owner, Chidori Ship Holding, and manager, NYK Shipmanagement, said.

Of the 64 containers identified as carrying dangerous goods, 54 held fireworks, eight had batteries and two contained liquid ethanol, according to a ONE Apus information center update Monday.

The update said Chidori and NYK Shipmanagement are working with the U.S. Coast Guard’s Joint Rescue Coordination Center in Honolulu, which “has advised that there have not been sightings of any containers” as of yet.

After the accident, the Apus turned back for Asia. The information center update said the container ship is “cautiously proceeding to the Port of Kobe, Japan,” and has an estimated berthing time of noon Tuesday (10 p.m. EST Monday).

“Once berthed, it’s expected to take some time to offload the dislodged containers that remain on board,” the announcement said. “Then a thorough assessment will be made on the exact number and type of containers that have been lost or damaged.”

Ownership of the goods lost has not been revealed and thus it’s not known whether some New Year’s Eve celebrations will be dimmer with 54 U.S.-bound containers of fireworks lost at sea. Henry Byers, FreightWaves’ maritime market expert, said the top importers using ONE as their ocean carrier into Long Beach the past 30 days were Flexport International, MOL Consolidation, Topocean Consolidation, UPS Ocean Freight Services, DHL Global Forwarding, Kuehne + Nagel and C.H. Robinson.

Rounding out the top 20 are Hecny Transportation, Rimports, Daniel M. Friedman & Associates, Apex Maritime, Hankook Tire America, Yusen Logistics, Ameziel, BDP Transport, Kintetsu World Express, Penguin Random House, Expeditors International, Harman International Industries and R.T. Express International.

Still other ONE customers through Long Beach are Living Spaces Furniture, APL Logistics, Signal Products, Wilson Sporting Goods, Sumitomo Rubber North America, Lexmark Juarez Distribution Center, Guardian Technologies, Konica Minolta Business Solutions and Hasbro.

Built in only 2019, the ONE Apus is 364 meters long and 51 meters wide and has a carrying capacity of 14,052 TEUs.

For many in the maritime industry, the Apus incident has brought to mind the June 2013 sinking of the MOL Comfort. The 7,041-TEU container ship cracked in half during an Arabian Sea storm. While efforts were made to tow the two halves of the ship to port, both eventually sank.

via ZeroHedge News https://ift.tt/3gvHXyK Tyler Durden

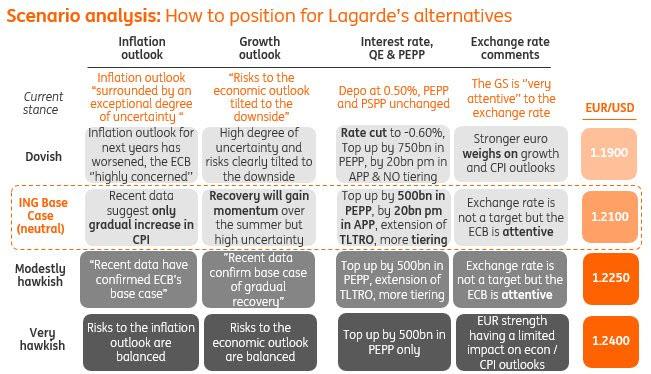

ECB Preview: Here Comes Another €500 Billion In QE Tyler Durden

Tue, 12/08/2020 – 22:25

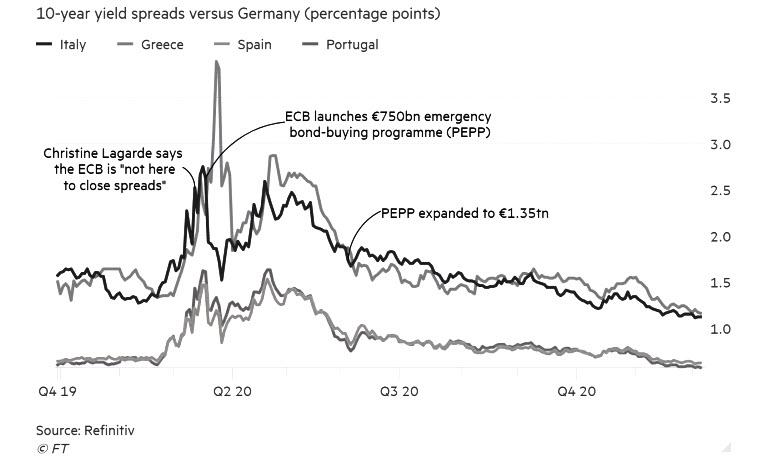

Last March, the ECB’s then-brand new boss Christine Lagarde sparked a mini crisis when quipped that it was not the job of the European Central Bank to narrow the gap in borrowing costs between the eurozone’s stronger and weaker members. The resulting bond selloff and market mess prompted the ECB’s chief economist Philip Lane to secretly call some of the largest asset managers to calm them that Lagarde had no idea what she was talking about and to stop selling.

Nine months on, investors have gone all-in on bets that the ECB boss has changed her mind, and is here “to close spreads” after all.

Ahead of the central bank’s next policy meeting tomorrow, the FT notes that spreads in the eurozone’s periphery have been squeezed by relentless demand for riskier bonds. The buying helped push Portugal’s 10-year yield below zero for the first time. Spain is not far behind, and Italy — the last big eurozone market to offer a significant positive yield over a decade — has seen its spread closing in on its lowest since the region’s debt crisis a decade ago.

With the ECB expected to expand its €1.35tn emergency asset purchase program by (at least) another €500bn tomorrow, investors are increasingly relaxed about holding peripheral bonds despite the explosion in debt levels driven by the pandemic.

Are they right? Courtesy of NewSquawk, here is a breakdown of what to expect tomorrow:

ECB policy announcement due Thursday 10th December; rate decision at 12:45GMT/07:45EST, press conference 13:30GMT/08:30EST

PEPP and TLTRO set to be tweaked, rates, PSPP and tiering expected to be left untouched

The upcoming release will also be accompanied by the latest round of staff economic projections

OVERVIEW: After telegraphing in October that further stimulus would be unveiled at the upcoming meeting, the consensus looks for a €500bln addition to the PEPP programme and 6-month extension until December 2021 (a longer extension has been speculated by some), while a majority of economists expect no change to its PSPP. Elsewhere, market participants expect policymakers to tweak the parameters of the Bank’s TLTROs. Rates are set to be left unchanged, whilst an adjustment to the tiering multiplier is not expected this time around. Accompanying economic projections are set to see a downgrade to the near-term inflation outlook, but greater focus could be placed on the initial 2023 forecast. For growth, any near-term optimism on vaccines could be tempered by how the ECB addresses the yet to-be passed recovery fund and disappointing Q4 2020 outturn.

PRIOR MEETING: As expected, policymakers opted to stand pat on policy settings, with rates and bond-buying operations held at current levels. The main takeaway from the initial announcement was the introduction of a new paragraph in the statement noting that risks to the economic outlook were “clearly tilted to the downside” and the new round of Eurosystem staff macroeconomic projections in December “will allow a thorough reassessment of the economic outlook and the balance of risks.” Additionally, “on the basis of this updated assessment, the Governing Council will recalibrate its instruments, as appropriate, to respond to the unfolding situation.” In terms of the policy measures set to be unveiled in the final meeting of 2020, President Lagarde did not delve into specifics. Despite policymakers acknowledging the bleak outlook for the region, the ECB chief stated that no discussion was held on unveiling measures at the October meeting with policymakers wanting to gather further evidence on the economic impact of the second wave of COVID across the Eurozone.

RECENT DATA: Q3 Eurozone GDP was confirmed as showing a 12.5% Q/Q expansion from Q2 with the Y/Y figure printing a 4.3% contraction. On the inflation front, the Y/Y flash CPI print for November remained at -0.3%, with core CPI holding steady at 0.4%. Survey data has highlighted the differing fortunes of the services and manufacturing sectors with the EZ-wide Markit PMI report showing the former in contractionary territory and the latter in expansionary, the broader composite reading fell to 45.1 in November from 50.0 in October. Markit noted, that while the EZ economy has slipped back into a downturn, the decline is of a far smaller magnitude than seen in the spring. The unemployment rate in the Eurozone for October came in at 8.3%, with the figure obscured by regional employment support schemes.

RECENT COMMUNICATIONS: Beyond the clear signposting at the October meeting by Christine Lagarde that stimulus is set to be unveiled in December, the ECB President has reaffirmed that all options are on the table. That said, Lagarde (Nov 11th) talked up the efficacy of PEPP and TLTROs throughout the pandemic, suggesting that they will “likely remain the main tools for adjustment”. Additionally, the central banker emphasised that “what matters is not only the level of financing conditions but the duration of policy support, too”, suggesting that any expansion to the PEPP could also be met with an extension from the current endpoint of end-June 2021. Chief Economist Lane – who many view as the thought-leader at the ECB –has echoed Lagarde’s views on the efficacy of PEPP and TLTROs, whilst also noting that it is essential that the macroeconomic recovery is not derailed by a premature steepening of the yield curve. Germany’s Schnabel, one of the more vocal members of the Governing Council, recently remarked that the ECB is not obliged to do what the market expects it to, before going on to state that a 12-month extension to PEPP is one option being considered, and that the ECB could also look at a longer duration or more favorable rate for TLTROs. Elsewhere, on vaccines, Ireland’s Makhlouf says the ECB will have to evaluate the emergence of the COVID-19 vaccine, suggesting that no firm view on the matter is currently held by the Governing Council at this stage; however, Vice President de Guindos noted that vaccine developments will be taken into account at the meeting. On the prospects for a further dive into negative territory for the deposit rate, Spain’s de Cos refused to rule out a rate reduction, but acknowledged that rates were close to the lower bound, Austria’s Holzmann has stated that such a move would not have an effect. In terms of lesser talked about measures the Bank could take, outgoing Hawk Mersch recently pushed-back on the prospect of the ECB expanding its purchase remit to include “fallen angels”

RATES: From a rates perspective, consensus looks for the Bank to stand pat on the deposit, main refi and marginal lending rates of -0.5%, 0.0% and 0.25% respectively. A recent research piece from the Bank noted that the reversal rate for the deposit rate stands around -1%, suggesting there is around 50bps of space until further rate reductions could become counterproductive. That said, whilst all options are said to be on the table (and it might help stem some of the recent EUR appreciation), commentary from central bank officials has done little to suggest that rate tweaks are on the cards. Additionally, when faced with the option of lowering the deposit rate in March as the crisis was unfolding, policymakers refrained from doing so. As a guide: markets currently assign a 13.5% chance of a 10bps cut to the deposit rate at the upcoming meeting and around a 55% probability by the end of next year.

BALANCE SHEET: With the balance sheet seen as the preferred easing tool for the Governing Council, focus remains on any adjustments to its bond-buying operations. Its PEPP currently has an envelope of EUR 1.35trl and is set to run at least until the end of June 2021, whilst its regular Asset Purchase Programme (of which the Public Sector Purchase Programme is a component) runs at a monthly pace of EUR 20bln together with the purchases under the additional EUR 120bln temporary envelope until the end of 2020. A Reuters survey of economists stated that expectations are for a EUR 500bln addition to the PEPP programme and 6-month extension until December 2021. UBS also expects the ECB to extend its commitment to reinvesting the principal of maturing securities purchased under PEPP by another year, from currently end-2022 to end-2023. Note, 33 of 44 surveyed do not think that the ECB will expand the PSPP, according to the survey. Going back to PEPP, expectations have continued to gather steam since the October meeting, and it remains to be seen if policymakers could trigger a “dovish surprise” on this front. Policymakers could opt to increase the PEPP by more than EUR 500bln, however, in recent weeks policymakers have placed greater emphasis on reassuring markets about the duration of its support. Accordingly, ECB’s Schnabel has touted the possibility of a 12-month (consensus looks for 6-month) extension to PEPP. Additionally, the prospect of including “fallen angels” into its Corporate Sector Purchase Programme (CSPP) lingers around the bank, however, this idea recently received pushback from outgoing hawk Mersch.

TLTROs: Given recent rhetoric from policymakers on the efficacy of Targeted longer-term refinancing operations (TLTROs), a tweaking of its current operations has also formed part of the consensus ahead of the meeting. As it stands, the facility has just two auctions left (10th December, and 18th March 2021) with current borrowing conditions running with a rate of -0.5% for three years or as low as -1% for banks that reach certain lending requirements. The Reuters survey found that 37 of the 48 economists surveyed expect the ECB to change the terms of its TLTROs, however, there are differing views on how this will be carried out. SocGen highlights four potential ways in which the ECB could act on this front, 1) it could go for a longer maturity, or signal continuous TLTROs, 2) it could lower the threshold for the best available rate, 3) lower the best interest rate below -1%, and 4) include new loan types such as mortgage lending. SocGen themselves predict “largely unchanged conditions” with “around five quarterly operations until March 2022, for corporate lending only, 3-year loans at -1% at best, lending threshold for best rate at 0%”.

TIERING: Another option for the ECB could be an adjustment to the existing tiering multiplier of six (exempt from negative interest rates) amid rising levels of excess liquidity. However, a complicating factor is that a large part of the recent increase in excess liquidity is attributed to the ECB’s TLTRO-III facility. Therefore, an increase in the tiering multiplier could undermine policymaker’s efforts to get banks to lend to the corporate sector. One option, UBS says, would be for the ECB to exempt funds from TLTRO-III, in which case it could raise the tiering multiplier to nine from six in order to keep banks’ deposit costs constant. However, UBS suggests that even this could prove to be too generous given the lending incentives in the TLTRO scheme that already reduce net deposit costs. As such, the Swiss bank looks for no adjustment on this front in December. Additionally, SGH Macro notes that an increase in the multiplier would be unlikely to occur unless met with an accompanying deposit rate cut.

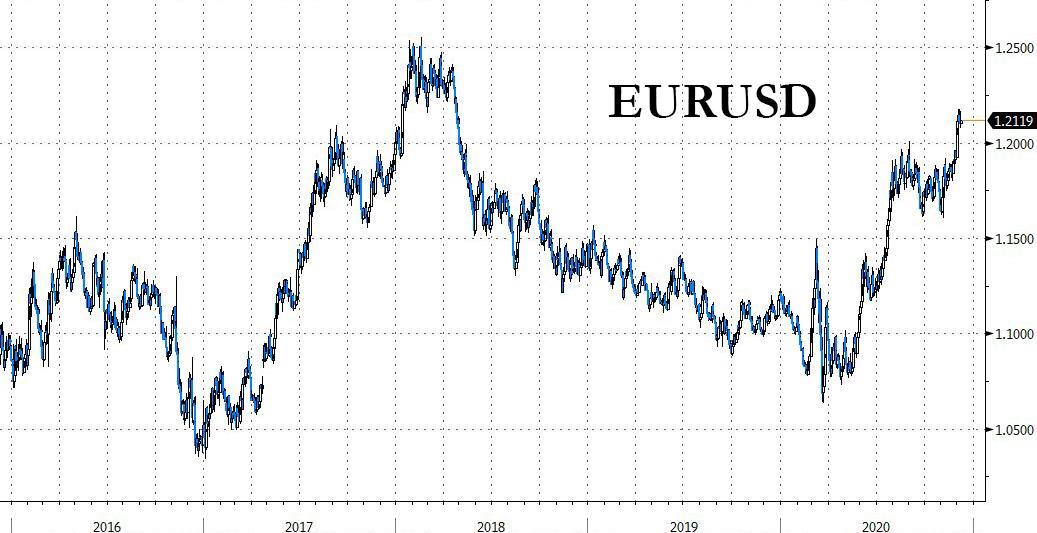

EUR: The recent appreciation of the EUR which has seen EUR/USD breach 1.20 and trade at levels not seen since 2018, has raised questions as to whether or not the ECB will attempt to talk down the currency. Note, at the September meeting after EUR/USD breached 1.20, President Lagarde noted that “the ECB does not target an FX level but will continue to monitor developments, including the EUR”. Morgan Stanley, however, suggests that we are not at levels that will concern policymakers given that the move in EUR/USD is more of a by-product of USD weakness, rather than EUR strength. In fact, the trade-weighted Euro is “a little weaker than in the summer,” the bank notes. As such, the EUR may prove to not be a major feature of the upcoming meeting.

ECONOMIC PROJECTIONS: Please see below for the September Staff Economic Projections: Inflation: 2020 +0.3% (unch), 2021 +1.0% (prev. 0.8%), 2022 +1.3% (unch) GDP: 2020 -8.0% (prev. -8.7%), 2021 +5.0% (prev. +5.0%), 2022 +3.2% (prev. +3.3%) This time around, from a growth perspective, despite a potentially disappointing Q4 outturn, better than expected growth in Q3 should see the ECB revise its 2020 estimate upwards to -7.2% from -8.0%, according to UBS. For 2021, despite the positive COVID vaccine updates, the fallout from Q4 2020 should prompt just a modest upgrade of its forecast to 5.0% from 5.5%, albeit this is largely dependent on how the ECB factors in the (yet-to-be passed) recovery fund. For 2022 and 2023, the Swiss bank pencils in growth of 3.9% and 1.9% respectively. On the inflation front, UBS expects the 2020 reading to be revised lower to 0.2% given softer prints in recent months relative to ECB expectations, whilst the better growth environment should offset any drag from softer oil prices in 2021 and 2022, leaving them unchanged at 1.0% and 1.3%. Of potentially greater interest will be the initial 2023 estimate, which UBS expects to remain below the pre-COVID inflation trend of 1.6% and therefore warrant additional stimulus.

STRATEGIC REVIEW: One issue lingering at the Bank is its ongoing strategic review. The review has been delayed by the pandemic with its findings now not due to be released until September 2021. However, on the 30th September, President Lagarde delivered a speech in which she highlighted some preliminary considerations for the review. Lagarde noted that the ECB would be considering whether to depart from its current inflation target of “below, but close to 2%” and move towards a more “symmetric” target that would tolerate overshooting the 2% threshold. Ahead of the October meeting, Morgan Stanley suggested that accelerating the release of the outcome of the review could amount to another policy option for the Bank. However, MS noted that given the current H2 2021 timeframe, it seems implausible that the findings could be released in the near-term, particularly given reports of differing views on the Governing Council, which will make fostering consensus a more difficult task.

* * *

Finally, here is the traditional scenario matrix analysis from ING Economics, which as usual should be rather useful for FX traders hoping to gauge how to trade the Euro based on what Lagarde unveils tomorrow.

via ZeroHedge News https://ift.tt/3lZqLmn Tyler Durden

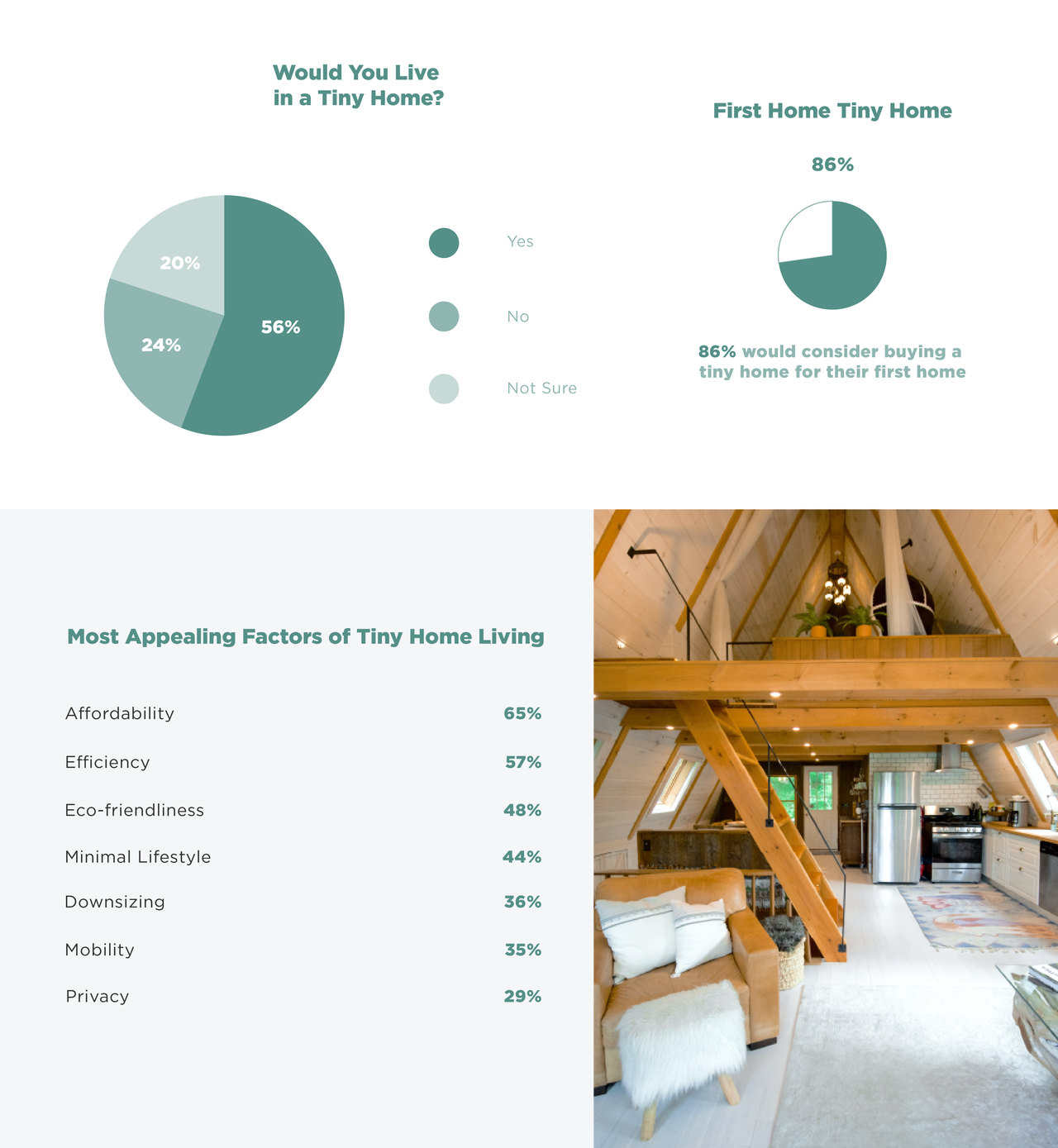

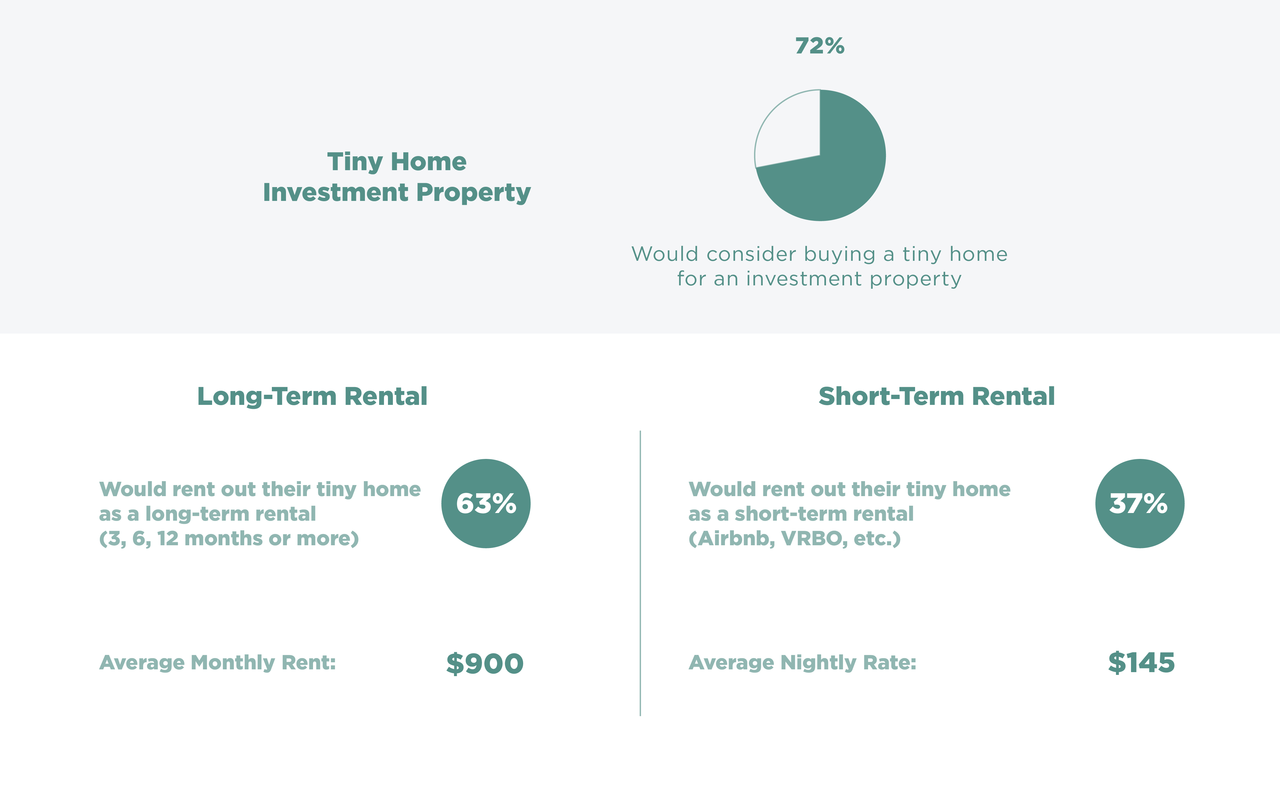

56% Of Americans Say They Would Live In A Tiny Home Tyler Durden

Tue, 12/08/2020 – 22:05

Although the micro home movement isn’t necessarily new, many have put tiny homes on their radar since COVID-19. Whether it’s a weekend escape from city living, or even a tiny backyard office, these dwellings have seen a recent boom in popularity. IPX 1031 recently did an extended analysis of the sector which is presented below, but here is a summary of what they found:

56% of Americans say they would live in a tiny home. 86% of first-time home buyers would consider a tiny home for their first home.

72% of home buyers would consider buying a tiny home as an investment property.

Most appealing factors of tiny home living: 1. Affordability 2. Efficiency 3. Eco-friendliness 4. Minimalist lifestyle 5. The ability to downsize.

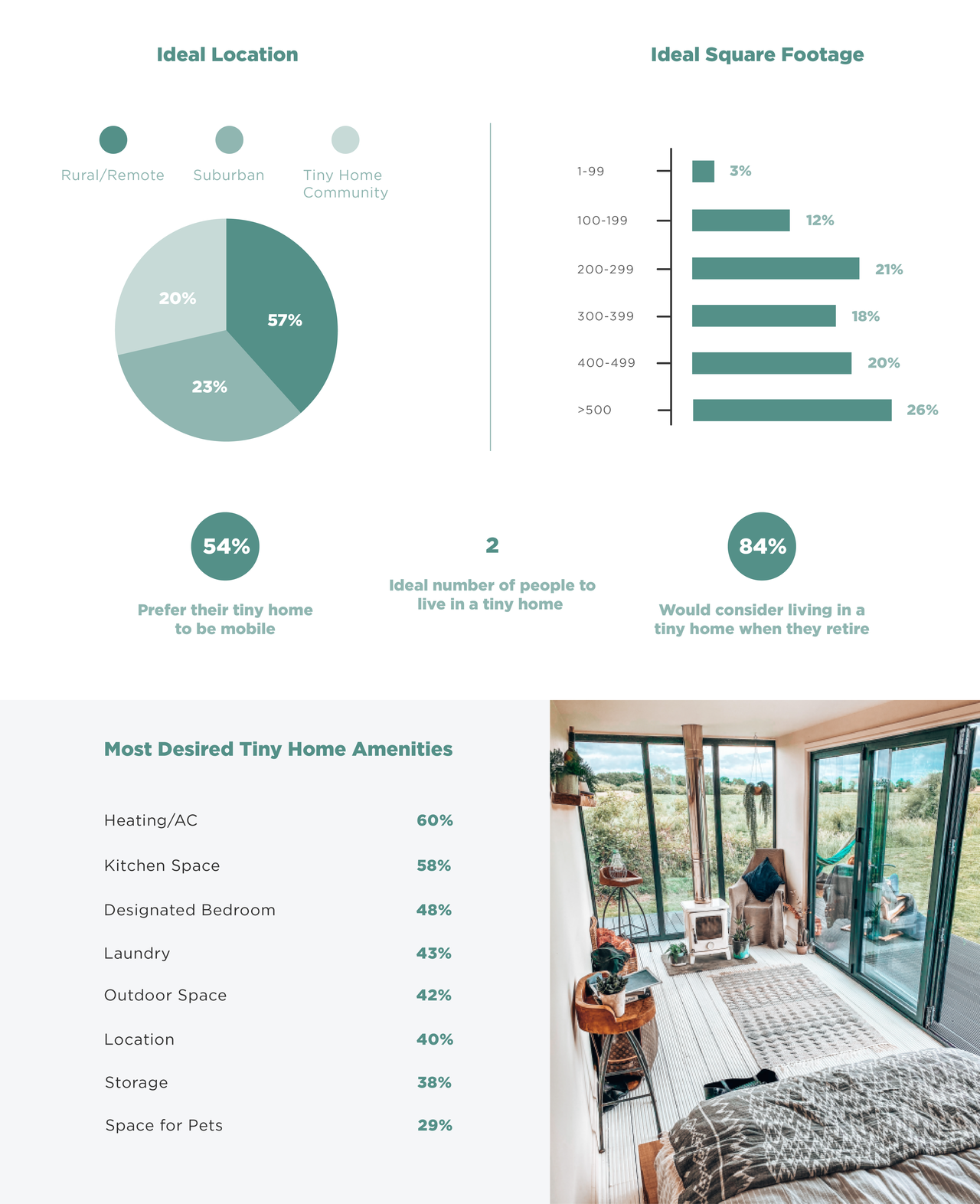

Most desired tiny home amenities: 1. Heating/AC 2. Kitchen space 3. Designated bedroom 4. Laundry 5. Outdoor space.

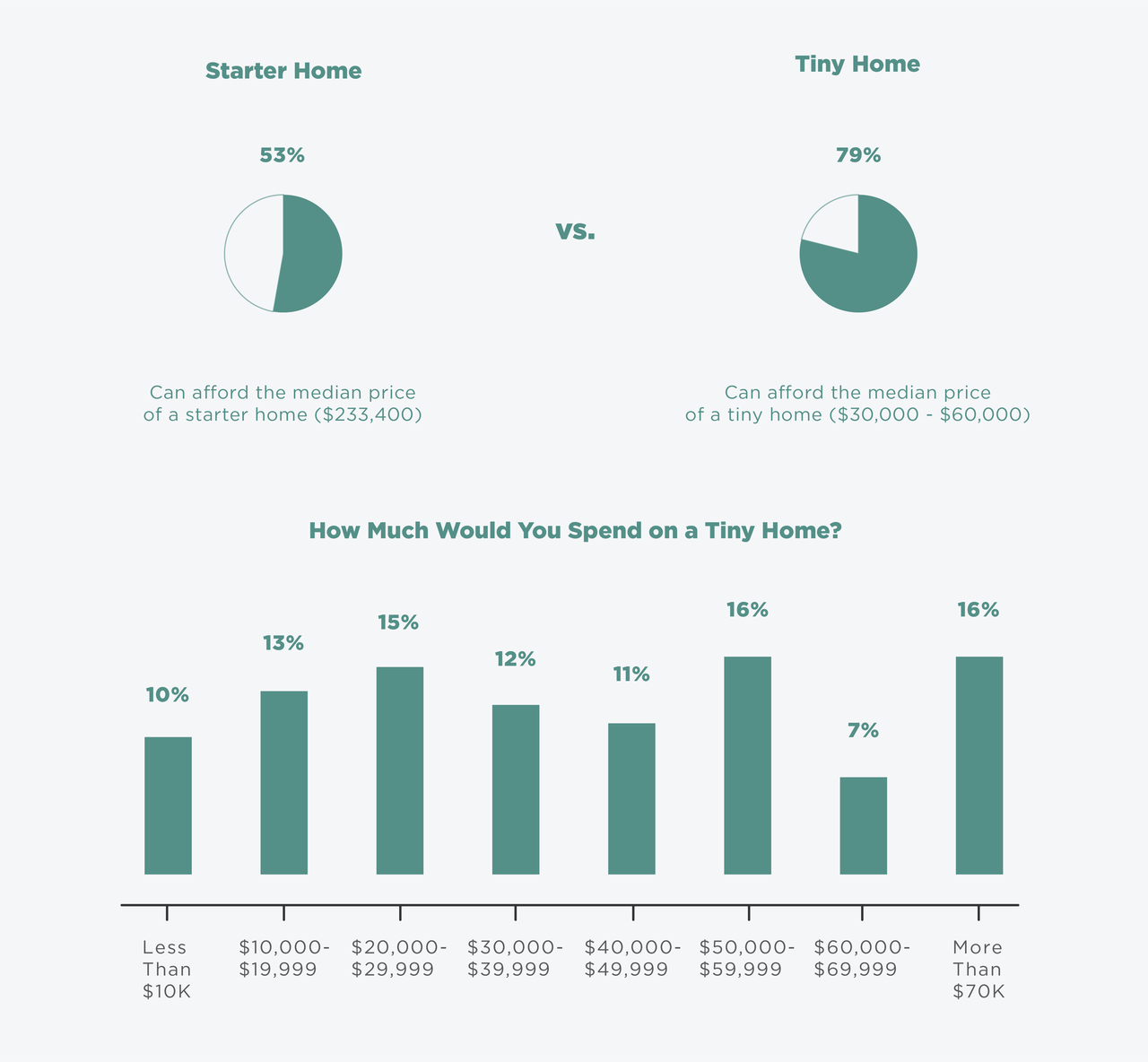

53% of Americans can afford the median price for a starter home ($233,400) vs. 79% of Americans can afford the median price of a tiny home ($30,000-$60,000).

Top states for tiny homes: 1. Vermont 2. New Hampshire 3. Maine 4. Wyoming 5. Washington 6. Idaho 7. Montana 8. Oregon 9. Rhode Island 10. Alaska.

In order to get more insight on tiny living, we surveyed 2,000 Americans across the country to find out how likely they would be to live in a tiny home and what amenities they would like to have in a tiny home. We also analyzed Google search volume to determine where tiny homes are most popular around the country.

Tiny Home Lifestyle

Living in a tiny home is certainly an adjustment that isn’t right for every lifestyle, but more than half of respondents say they would consider living in one. Unique factors such as affordability (65%), efficiency (57%), eco-friendliness (48%) and the ability to live a minimal lifestyle (44%) are among the top reasons why respondents say they would like to live in a tiny home.

It’s also interesting to note that among those who have never owned a home, 86% say they would consider buying a tiny home for their first home.

The Ideal Tiny Home

Considering that most tiny homes are 400 square feet or less, many can be built on wheels, which allow homeowners to live a mobile lifestyle. According to respondents, 54% would prefer their tiny home to be mobile and a majority (54%) would prefer that their home is under 400 square feet.

With such a small amount of living space, it’s no surprise that the ideal number of people to live in a tiny home is two. In terms of amenities, heating/AC (60%), kitchen space (58%), designated bedroom (48%), laundry (43%) and outdoor space with a view (42%) are the most desired and “must haves,” according to respondents.

Tiny Home Budget

The price to purchase or build a tiny home can vary and depends on a number of factors. Most tiny homes cost between $30,000 to $60,000 while the median price for a starter home is $233,400, according to the National Association of Realtors. Exactly half of respondents say they would spend less than $40,000 on a tiny home and 79% say they would be able to buy or finance a tiny home rather than a traditional starter home.

Where Are Tiny Homes Most Popular?

When most people think of tiny homes, images of a secluded lot in the woods or a home nestled near a lake come to mind. We were curious to see where tiny homes are the most popular, so we analyzed Google search volume for more than 1,300 terms and keywords related to tiny homes.

The results show that tiny homes have seen the most interest in rural states such as Vermont, New Hampshire, Maine, Wyoming and Washington. Illinois, Pennsylvania, Ohio and New York showed the least interest in searches for tiny homes.

Tiny Home Investment Property

With a low cost to build and maintain, tiny homes could bring big profits for property investors. According to respondents, 72% would consider buying a tiny home to serve as an investment property. Among those, 63% say they would rent out their tiny home as a long-term rental while 37% say they would rent their tiny home as a short-term rental. On average, respondents say their ideal monthly rent would be set at $900 per month for a long-term rental and $145 per night for a short-term rental.

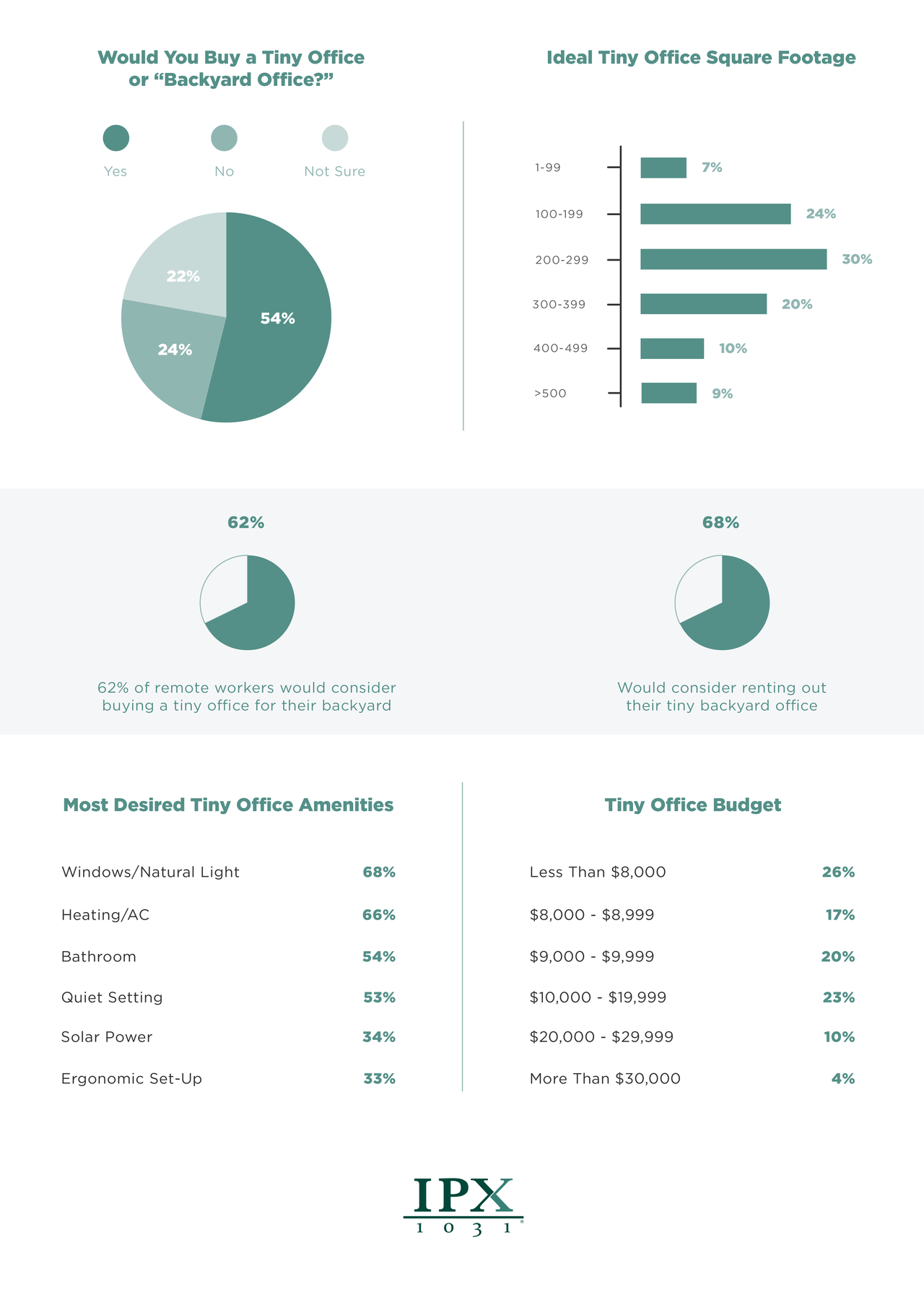

Tiny Office

With many Americans adapting to remote work or working from home, the concept of a tiny office (or a “backyard office”) is an appealing alternative to working inside a home office, kitchen or living room. In fact, more than half (54%) say they would buy a tiny office and 62% of remote workers would consider buying one. Ideally, more than a quarter of respondents say they would spend less than $8,000 on a tiny backyard office.

With many Americans adapting to remote work or working from home, the concept of a tiny office (or a “backyard office”) is an appealing alternative to working inside a home office, kitchen or living room. In fact, more than half (54%) say they would buy a tiny office and 62% of remote workers would consider buying one. Ideally, more than a quarter of respondents say they would spend less than $8,000 on a tiny backyard office.

via ZeroHedge News https://ift.tt/2K63SjA Tyler Durden

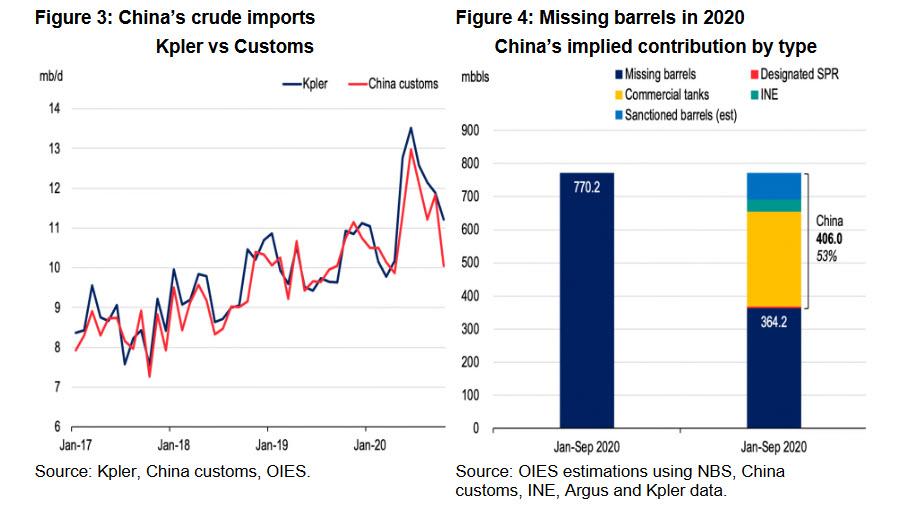

“This Is Astounding”: China Is Snapping Up Most Of The World’s “Missing” Barrels Of Oil Tyler Durden

Tue, 12/08/2020 – 21:45

In almost every oil cycle, the market is confronted with the problem of “missing barrels”, or the gap between the change in inventory implied by global supply-demand balances on the one hand and the observed change in inventory levels by commercial and government entities (adjusted for floating storage and oil in transit) on the other hand.

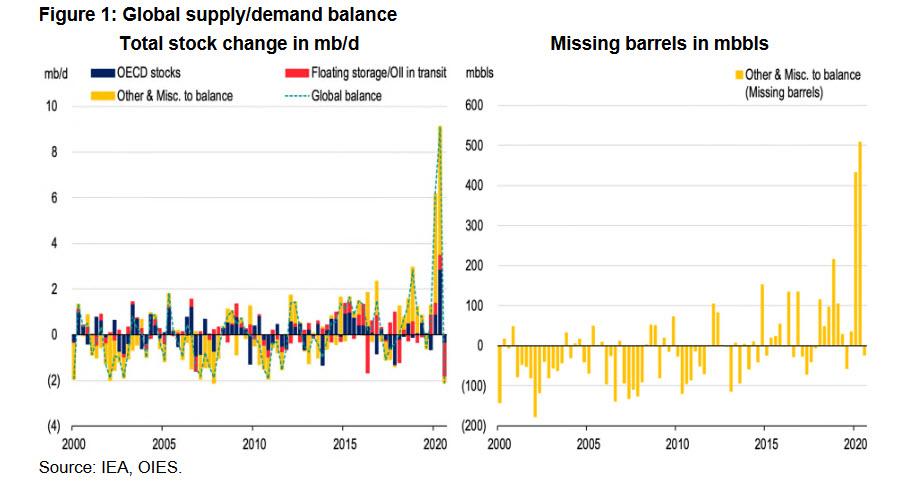

As the Oxford Institute for Energy Studies writes in a report published today, based on IEA global oil balances, the surplus during the first three quarters of 2020 averaged around 4.4 mb/d, with the surplus in the first half of 2020 reaching a record level of 7.6 mb/d due to the severity of the demand shock and the break-up of the OPEC+ agreement in March. This implies an inventory increase in H1 2020 of 1,390 million barrels (mbbls), before declining by 194.2 mbbls in Q3.

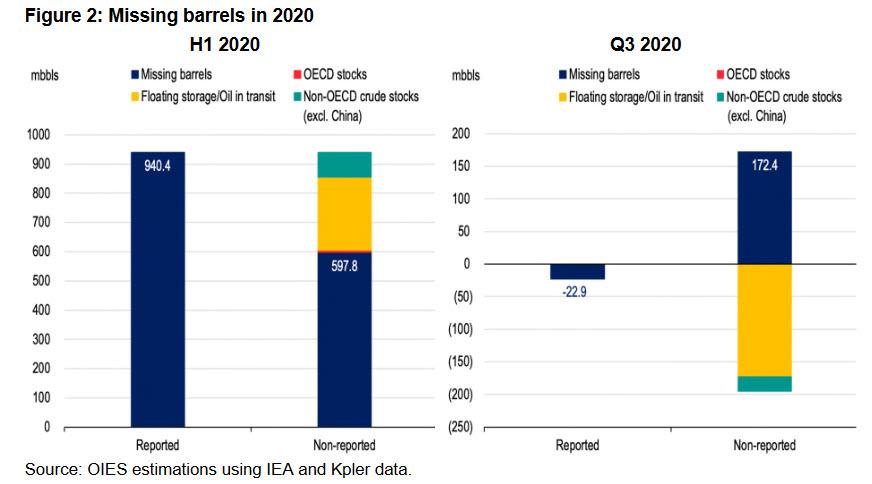

According to the IEA, out of the total stockbuild in the first half of the year, total OECD stocks accounted for 344.3 mbbls or 25% of the total increase, floating storage and oil in transit accounted for 105.3 mbbls or 8% of the total increase and the remaining 940.4 mbbls or 68% of the total increase to balance is essentially unaccounted for including changes in non-reported stocks in OECD and non-OECD areas that the IEA labels as “Other & Miscellaneous to balance” (as shown in Figure 1).

The volume of missing barrels in H1 2020, the OIES writes, “is the largest ever recorded gap between observed and implied stocks since at least 1990, being three times larger than previous historical downcycles such as in H1 1998 and more recently the H2 2018 downturn and nearly 10 times larger than the imbalance of H2 2008 in the aftermath of the global financial crisis.”

The “missing barrels” problem can arise due to a number of factors. The most obvious reason is that models could be generating “artificial barrels” by underestimating demand and overestimating supply. The severity of the oil crisis in 2020 due to the global coronavirus pandemic led to the break of some key relationships (for instance between economic growth and oil demand) and models had to be calibrated to account for the severity of the shock (for instance, including indicators of the severity of restrictions across countries).

Another factor is the coverage and quality of data on stocks. The reason for this is that very little publicly reported, accurate information exists for oil stocks outside of the United States. And yet the US oil stocks many not be an accurate reflection of the world situation. This observation increasingly holds as demand growth has shifted from OECD to non-OECD, especially given the key role that China is playing in global crude demand. In this latest cycle, China’s position as a key equilibrating mechanism was further highlighted as it absorbed surplus barrels from all over the world as it took advantage of relatively cheap crude to fill its large and growing storage capacity.

To put this in perspective, OIES utilized crude inventory and fleet metrics data from Kpler and attempted to identify some of the missing barrels implied from IEA balances. As Figure 2 shows, even accounting for additional floating storage and oil in transit (+250.4 mbbls), as well as OECD and non-OECD crude stock changes excluding China (+85.2 mbbls), all of which are not previously reported by IEA, we are still missing 597.8 mbbls or 64% of the total missing barrels in H1 2020. This issue becomes more complex in Q3 2020 for which the IEA balances imply a 194.2 mbbls deficit of which 171.3 mbbls are accounted for and 22.9 mbbls are missing. Kpler data, however, show a much larger draw of floating storage, suggesting one (or a combination) of three possibilities: the actual deficit is much larger than estimated by the IEA (by about 150 mbbls); there was a large build in non-OECD stocks, or the implied market surplus in H1 2020 was overestimated and carried over. Indeed, a large build in unaccountable stocks in Q2 2020 followed by a draw in Q3 2020 suggests that barrels were stored and drawn in places where they currently cannot be tracked.

The China Conundrum

The issue of “missing barrels” has long plagued Chinese data, but much like in the rest of the world, has become more pressing and perplexing in 2020. Net crude imports in the year-to-October averaged 11.09 mb/d, rising from 2019 levels by over 1 mb/d and maintaining their 2019 growth rates. According to the OIES report, “this is astounding given that economic activity has been considerably weaker and runs have averaged 13.3 mb/d in the first ten months of 2020, growing by an impressive 0.47 mb/d, but still lower than the 0.82 mb/d increment seen over the same period last year.”

Put simply: the data suggest China has overbought crude to put in storage.

But the key question is, how much has gone into storage and perhaps more critically, how much is likely to come back out?

In response to this rhetorical question, the Oxford Institute authors notes that assessing how much crude has gone into storage has become both an art and a science, given the limited official data. When looking at implied stockbuilds (i.e deducting crude used for refinery runs from the sum of domestic production and net imports), in the year-to-October, China has stored on average 1.6 mb/d, or a staggering 488 mbbls of crude.

While it has been clear that large volumes of crude oil have headed to China, judging by port congestion at Chinese shores, differentials and benchmarks, such volumes seem overstated as they would have likely led to tank tops earlier this year. According to OIES estimates, China had close to 1,100 mbbls of crude storage capacity at the end of 2019 (that’s over 1.1 billion and far, far more than Cushing and the US Strategic Petroleum Reserve). Assuming a roughly 60% utilization rate, crude stocks would have reached 650-680 mbbls. A build of an additional 500 mbbls, even when taking into account 250 mb of new tank space added over the year, would have overwhelmed China’s storage capacity leading to a slowdown in crude arrivals already earlier this year.

And even though imports into China are slowing somewhat and storage utilization rates are likely at over 75% currently, there are signs of a recovery in crude buying for early 2021. It is therefore useful to look more closely at implied stockbuilds.

First, many crude balances for China do not account for crude losses during the refining process or burnt at the field, which between 2000 and 2017, according to the National Bureau of Statistics, have averaged 0.30 mb/d8. In the five years prior to 2017, losses in refining increased to average 0.35 mb/d, so when deducting these losses, the implied stockbuild for the year-to-date falls to an average 1.3 mb/d, or just over 375 mbbls. While this is still a monumental build, it is more plausible.

At the same time, Chinese demand could also be underestimated. China’s independent refiners have been infamous for tax evasion and especially between 2016 and 2018 were estimated to have underreported refining throughputs by 0.3-0.8 mb/d10. So historically, Chinese crude demand has been understated. The shift to new tax reporting practices in early 2018 have limited the independents’ ability to under report runs, although a number of them subsequently turned to misrepresenting their product output. In late 2020, following an announcement by Shandong officials that they will be levying a windfall tax this year, which is based on product output, the independents may be resorting to some under reporting again, although any such volumes are likely small, given that China’s demand is recovering slowly and product tanks are also estimated to be two-thirds full. Some combination, therefore, of underestimated demand and crude in storage suggests that China could well be responsible for as much as half of the missing barrels and that these are indeed “real.”

The next question is then, how likely are these barrels to be drawn down, and will they weigh on Chinese imports?

Roughly a third of these volumes could have gone into bonded tanks. When looking at China’s crude imports, there is a discrepancy between waterborne flows as assessed by Kpler and arrivals reported by customs data, with assessed arrivals higher than customs data by 0.47 mb/d for the year-to-October (Figure 3). In previous years, the difference in assessed volumes and customs data were smaller, mostly due to discrepancies between the timings of arrival and discharge, alongside some crude going into bonded tanks.

This year, the discrepancy is more substantial and points to a large accumulation of crude in bonded tanks, which are not consistently counted as imports. Not only has the INE increased its storage capacity this year, with its tanks holding 34 mb of crude at the end of October according to the exchange but sanctioned barrels may have also gone into bonded tanks. For example, in the year-to-October, Kpler estimates point to 0.15 mb/d of Iranian crude going to China (compared to 75,000 b/d recorded by customs) as well as 0.21 mb/d of Venezuelan crude flowing to the country (although customs have reported no Venezuelan crude going into China). Theoretically, then, at the end of October, China had accumulated as much as 85 mb of Iranian and Venezuelan crude in bonded storage tanks over the course of the year, although some of these will have likely been drawn down by refiners, and if they have not been yet, they will be.

But that still leaves over 200 mbbls of crude in storage, of which only a fraction is likely to return to the market. This is because these volumes have gone into both commercial and strategic petroleum reserve (SPR) tanks that are used as buffer, both for refiners’ forward cover and strategic reserves. China has a small number of designated SPR tanks of close to 400 mbbls, that are likely 300 mbbls full, with Argus estimating 32 mbbls of fills this year alone (see Figure 4). At the same time, the government has been leasing out commercial tank space for its SPR programme, as the construction of dedicated SPR sites has been slow. But even with close to 150 mbbls of commercial tanks that are widely assumed to be leased out to the SPR, the SPR program only meets around 40 days of import cover (as 90 days at current import volumes would imply over 1,000 mbbls).

In addition, China’s refiners are mandated to hold 15 days of forward cover, which, for a system of close to 19 mb/d of nameplate capacity, means almost 300 mbbls of forward cover. Indeed, part of the increase in import licences awarded to non-state refiners this year was intended for them to build up their crude stocks while prices remain at relatively low levels.

In sum, when taking into account the crude requirements of storage tanks at the various ports and other commercial sites as well as pipeline fills, the crude requirement for China’s oil system is massive. As a result, most of the crude flowing into China this year has helped meet these needs. All in all, we estimate China now holds close to 1,000 mbbls in storage, which is roughly 90 days of its import needs, with capacity by year end reaching 1,300-1,400 mbbls. The good news for markets is that only a small part of these barrels will be drawn down, but the bad news is that China’s future stockpiling needs are now shrinking.

This is not to say that China’s crude imports will fall: with over 1 mb/d of new refining capacity starting up over the next two years, refiners will continue sourcing crude as refining throughputs continue to rise and as new plants require operating stocks. Moreover, additional infrastcuture including tanks and pipelines will need filling. But over the next two years, incremental demand for strategic stocks will slow, and crude imports will become more closely aligned with refiners’ needs.

Conclusion

The large accumulation of barrels in China suggests that “artificial” or “imaginary” barrels, as a result of imprecise measurement of global oil supply-demand balances, are not the only explanation to the missing barrels question. Indeed, even though China’s crude balances are riddled with inconsistencies, it is clear that the country has amassed large volumes of crude this year — potentially close to 400 mbbls — which have contributed both to the country’s strategic reserves and commercial forward cover. At the same time, Chinese demand may well be underestimated given refiners’ tax avoidance practices. So, as global supply and demand numbers get adjusted with the arrival of new information — which likely includes other Asian countries for which both demand and storage estimates are imperfect — the volume of missing barrels will shrink further, if indeed half have ended up in Chinese storage tanks and are unlikely to be released back into the market. In addition, some of the missing barrels are a result of unobservable barrels in important consuming centers and perhaps also stocks held at the distribution level and by final end consumers.

As the Oxford researchers conclude, “the complexities of global crude balances, despite the important contribution made by new technologies, highlight the ongoing challenges facing OPEC+ in estimating how long it will take to rebalance the market. In addition to the uncertainties surrounding the demand outlook in these unprecedented times, assessing the extent and nature of buffers in the system has become more complicated.”

The question is whether going forward, OPEC+ can afford to ignore non-OECD stocks? And if these stocks are being stored for strategic purposes and the bulk of these stocks will not be released back into the market, does targeting non-OECD stocks really matter for oil policy purposes? Should we exclude years of elevated stocks from the averages or have these become main features of the new cycles and the adjustment process? As we enter 2021 in an environment of extremely depressed oil demand, these questions will become more pressing.

via ZeroHedge News https://ift.tt/37LkjKt Tyler Durden

The United States Secretary of the Treasury bears a shameful job duty. They must place their autograph on the face of the Federal Reserve’s legal tender notes. Here, for the whole world to witness, the Treasury Secretary provides signature endorsement; their personal ratification of unconstitutional money.

Janet Yellen – first she got to print a lot of funny money, now she gets to autograph it. The Titanic meanwhile finds itself in uncharted waters and rumor has it that there may be icebergs lurking not too far from here. [PT]

If you recall, Article I, Section 8, of the U.S. Constitution empowers Congress to coin money and regulate its value. What’s more, Article I, Section 10, specifies that money be coined of gold and silver and cannot be bills of credit.

Indeed, paper dollars are illegal money per the U.S. Constitution on two counts. First, they’re issued by the Federal Reserve. Second, they are bills of credit with no ties to gold or silver.

This critical defect does not register even a passing concern for most Americans. But it should. Because illegal money – like paper dollars – has its deficiencies. Mainly, it’s prone to gross over issuance for political means. Thus, as it funds the unlimited growth of government, its payment quality grows evermore suspect.

Without question, illegal money has a whole host of problems. And the woman who will soon be autographing the illegal money – Biden’s nominee for Treasury Secretary, Janet Yellen – will further stimulate these problems.

Deceptive and Cruel

Janet Yellen, if you don’t remember, was Chair of the Federal Reserve from 2014 to 2018. She will be only the second bureaucrat to be both Fed Chair and then Secretary of Treasury. The first was G. William Miller, way back when Jimmy Carter was President. Miller was a poor steward of the dollar. Inflation went off the Richter scale on his watch.

The Miller years were quite a harrowing time with respect to galloping price inflation. The extent to which Miller can be blamed is debatable – the event was a co-production cooked up by an entire gaggle of loopy bien-pensants over the years. They were just as arrogantly confident in their prescriptions as their successors deciding today’s policies are. [PT]

Yellen, like Miller, will have the unique opportunity to authorize the money she previously issued. The consequences could be equally destructive for the dollar. They may even be worse.

Prior to her time as Fed Chair, Yellen held various positions with the Federal Reserve over a 20 year run. We don’t really know much about what she actually did. But, at a minimum, she participated in an era of unprecedented Fed activism.

Certainly, Yellen has spent hours squinting at aggregate demand graphs while contemplating how monetary policy can be twisted to boost spending. She also believes monetary policy is a moral issue.

In fact, back in 1995, at a Federal Open Market Committee meeting, Yellen argued in favor of allowing inflation to exceed inflation targets for moral reasons. The Economic Policy Journal offers the following account:

“Ms. Yellen told the committee that ‘the moral’ of all this is ‘that the Fed should pursue multiple goals.’ She said that ‘when the goals conflict and it comes to calling for tough trade-offs, to me, a wise and humane policy is occasionally to let inflation rise even when inflation is running above target.’”

Remember, inflation acts as a hidden tax on savers. It devalues the purchasing power of their savings. Ask any retiree living on a fixed income or a hardworking prudent individual skimping to squirrel away some nuts for retirement. Policies of inflation are not wise and humane; they are deceptive and cruel.

Janet Yellen: Too Dumb To Stop

After all these years Yellen still thinks she knows best. That she is the true arbiter of morality. Guided by silly academic models she thinks she is helping people when she is really hurting them.

Fiscal and monetary policies over the last 40 years have been characterized by increasingly extreme intervention. Over this period Yellen and other central planners have pursued inflationism as a means to perpetually stimulate demand.

The Fed creates the illegal money. The Treasury authorizes it. And the economy adjusts accordingly. Business transactions are made with the illegal money. Private and public buying and selling is conducted with it. All commerce is settled with it.

The over-issuance of illegal money has warped and distorted the economy… delivering extreme riches to asset holders while leaving the vast majority of wage earners with empty pockets. Alas, Yellen is too dumb to stop. In a Tweet following the announcement of her nomination, she wrote:

“We face great challenges as a country right now. To recover, we must restore the American dream—a society where each person can rise to their potential and dream even bigger for their children. As Treasury Secretary, I will work every day towards rebuilding that dream for all.”

But what will Yellen, as Treasury Secretary, really do to restore the American dream? Will she start new companies that employ people? Will she create more high paying jobs?

No, she won’t – because she can’t. Starting companies that create high paying jobs, and produce goods people demand, is out of the realm of what a Treasury Secretary can do. But what Yellen can do is work in concert with the Fed and Congress to authorize vast amounts of illegal printing press money.

It may be an overused cliché and who knows if it was really Einstein who said it, but in this case it certainly fits. [PT]

Should Yellen follow the path of 1980 through 2019 and inject new credit into the financial system, we will see further inflation of financial assets. Should Yellen follow the CARES Act model and send checks directly to the people, consumer prices will inflate. Perhaps she will be compelled by her high morality to do both.

Regardless, Yellen will not be up to the task of returning reverence and trust to the dollar. And without that, there is little hope of restoring the American Dream.

via ZeroHedge News https://ift.tt/2LjyOh8 Tyler Durden

MBA Applications Surge Despite Fed Defiling All Economic Laws As We Know Them Tyler Durden

Tue, 12/08/2020 – 21:05

Who in their right mind would want to be an MBA in this environment?

That’s the first question that came to our minds when we found out that MBA application volume was surging. Thanks to vast distortions in both capital markets and the economy brought on by the Fed rigging interest rates and introducing limitless money into the supply, we’re not sure any of the economic “basics” one would learn in an MBA program would even apply in the lunatic asylum our economic system has become in 2020.

Despite this, the upcoming MBA admissions cycle is “shaping up to be the most competitive in recent memory,” according to the Wall Street Journal. Full time residential MBA applications have seen higher volumes for next fall and expect to have fewer spots for enrollment than in years past.

Schools have also let some international students defer enrollment due to the pandemic’s travel restrictions, locking up supply for spots. The deferral rate for all students was up from 2% in 2019 to 6% in 2020 as a result of the pandemic.

Jeremy Shinewald, founder of admissions consulting firm mbaMission, said: “Everything points to this being the most competitive year ever for M.B.A. applicants. I wouldn’t be the least bit surprised if schools crush their records for application volume.” Consultations at his firm were up 30% from July to September, he said.

Applications to MBA programs in American “rose for the first time in five years” in 2020 as a result of lowered testing requirements and more applicants looking to bypass the economic slowdown caused by Covid.

“I feel the importance of the whole [application] package has increased. The bar is higher for applications,” applicant Jimmy Lin told the Journal. He is applying to Northwestern University’s Kellogg School of Management.

Georgetown has accepted a majority of its candidates during its sound round of applications this year, whereas it normally takes three to four rounds to fill out a class. The university doesn’t expect to increase its class size despite the surge in interest for its program.

Shelly Heinrich, the associate dean of M.B.A. admissions at Georgetown University’s McDonough School of Business, said: “It can be nerve-racking for applicants. They are now thinking, ‘Oh goodness, not only do you have deferrals who have secured spots in your class for next year but your applications are now up significantly, and so what does that mean for me?”

Applicants that schools are inviting for interviews have fallen about 8% at the Top 16 schools, the Journal notes, and the rejection rate is up 7% from a year prior.

Some schools, like Harvard Business School, are expanding their 2021 class sizes to try and meet some of the demand. Harvard said it would enroll 1,000 students over the next two years, up from the 730 it enrolled last fall.

Perhaps next they will alter their programs to specialize in how to get a multi-billion dollar market cap without ever turning a profit, the wonders of SPACs and why buying the dip will be a sound strategy for decades to come.

via ZeroHedge News https://ift.tt/3gpfVVw Tyler Durden