Taiwan’s President Warns Of “Daily Threats” From “Authoritarian Forces” Amid US Arms Sales Tyler Durden

Tue, 12/08/2020 – 17:05

Taiwan says it’s coming under increasingly direct threats from the mainland amid pending US weapons sales to the breakaway republic.

President Tsai Ing-wen warned in urgent statements made Tuesday that Taiwan now faces military threats on a “daily basis” from “authoritarian forces” – a clear reference to China as it presses its claims over the island.

She said to a security forum in Taipei that there are huge threats especially in the “increasingly militarized South China Sea” – an area which has seen soaring tensions based on US patrols flying near Chinese-claimed artificial islands.

“Authoritarian forces consistently attempt to violate the existing norms-based order,” Tsai said. “Taiwan has been at the receiving end of such military threats on a daily basis.”

Beijing has repeatedly a series of US arms sales transfers since the summer, with the latest being a newly announced $280 million arms sale package, which is the sixth this year.

Sales have included drones, anti-air defense systems, radar equipment, and a coastal invasion early warning system and missiles. China has said it will retaliate, but has never been specific in its threats, but in the last months has clearly ramped up PLA military exercises across from and near the island.

It’s connected with Trump’s pressure campaign on China which the administration has vowed to ramp up right till Biden’s inauguration on Jan.20. Reuters summarizes the arms sales as follows:

The outgoing Trump administration has ramped up support for the island democracy, with 11 arms sale packages in total, and on Monday the U.S. government notified Congress of the sale of a new Field Information Communications System.

Such sales – $5 billion worth this year – have riled China, adding to existing tension between Beijing and Washington, with China placing sanctions on U.S. companies involved and stepping up its military activities near Taiwan, including regular air force missions.

2020 is a record year for US arms sales to Taiwan. Previous high was $7.1 billion according to DSCA. Would be interesting to map these sales figures against the state of relations between the US and China. @securitysplatpic.twitter.com/b0x9p2g2h8

The question remains the degree China is willing to hit back at Washington sanctions and ‘illicit’ arms sales, which Beijing officials have long condemned as violating the ‘One China’ status quo, while Trump remains in office.

Waiting out the clock will be made difficult given there’s near daily escalation out of Washington, whether it be the latest sanctions on Chinese officials related to Hong Kong, or the recent ban on select Chinese cotton imports, as well as severe visa restrictions on Communist Party members and their families.

via ZeroHedge News https://ift.tt/3qHsCzu Tyler Durden

With the nomination of California Attorney General Xavier Becerra for Secretary of the Department of Health and Human Services, the list of presumed front-runners for Attorney General is narrowing. One name remains prominently at top: former Associate Attorney General Sally Yates.

Yates’ appointment would be one of the most controversial for Biden and would likely lead to an intense confirmation fight over her standoff with President Donald Trump at the start of his Administration as well as her role in the Russian investigation. However, in a strange way, Yates’ controversy could be exactly what both President Trump and President-Elect Joe Biden need if they are looking a basis for a self-pardon.

The short list for Attorney General contains some notable and less controversial figures like Judge Merrick Garland and former Homeland Security Secretary Jeh Johnson. However, Sally Yates is one of the most astute political operatives in Washington. She went from relative obscurity to legendary status in one of the most cynical and successful calculations in history. She engineered her own firing at the hands of Trump – a virtual canonizing act for the media and many liberals.

When Trump was inaugurated, Yates had only a few days left in government. She became acting attorney general in January 2017, following the departure of Attorney General Loretta Lynch. Yates had already been instrumental in signing off on secret surveillance of Trump associate Carter Page during the Obama Administration and had pushed for the investigation of incoming National Security Adviser Michael Flynn. Both investigations of possible Russian collusion were found to be without merit and Yates recently said that she would not have signed off on the surveillance if she knew then what she knows today.

Yates had just become acting Attorney General when she was given the opportunity of a lifetime. Trump was about to sign his travel ban and had sent the draft to the Justice Department’s Office of Legal Counsel, an office ordinarily given considerable deference on the legality of policies and orders. The career staff at the OLC had found that the order was legal and within Trump’s authority. Yates however quickly sent out an unprecedented order to the entire department not to assist the White House on the executive order. The move thrilled commentators and media figures who had long accused Trump of religious and racial bigotry. I was (and remain) critical of her action on the travel ban.

For the record, I was one of the earliest critics of the order both on policy and drafting grounds. The order failed to address such groups as green-card holders and others legally present in the United States (those errors would later be addressed in subsequent orders). However, Yates did not say that the order was illegal. Rather, she declared that she was not convinced the order was “wise or just” or “lawful.” It was a bizarre order since it is not the job of Justice Department attorneys to decide if a president is acting in a “wise or just.” Former Justice official and Harvard professor Jack Goldsmith pointed out that Yates neither determined the immigration order to be unconstitutional nor cited any basis for refusing to defend it. Accordingly, he said, Yates left the impression of “insubordination that invites the president to fire her.”

Of course, if Yates felt the order was morally or legally wrong, Yates could have resigned like Attorney General Elliot Richardson and Deputy Attorney General William Ruckelshaus in the infamous “Saturday Night Massacre” under President Nixon. Why didn’t she?

The reason seems obvious. An official resigning a few days before she was scheduled to resign is hardly news. Yates appeared to want to be fired. She knew that such an order would make her termination virtually inevitable. Since ancient times, the only path to instant glory other than slaying a great tyrant is to fall by his hand. Trump fired Yates and she immediately entered the Pantheon of fallen heroes for the left.

Notably, while the order would be expanded and altered in later superseding orders, the core of the travel ban remained the same. Indeed, the challengers went to the Supreme Court and said that it was essentially the same order with the same underlying discriminatory impact. Yates later explained that she considered the order discriminatory for the same reason. Yet, the Supreme Court ruled that she was wrong and the OLC was right. The order was constitutional. It was not struck down but expanded. That does not mean that reasonable people could not have disagreed on that point. As I mentioned, I was a critic of the order. However, as I also noted, the existing case law favored Trump and, at best, this was a close matter for the courts to decide (not Sally Yates).

It did not matter. The legend was made. She spoke at the Democratic National Convention and declared:

“I was fired for refusing to defend Trump’s shameful and unlawful Muslim travel ban.”

It did not matter that the order was not unlawful but upheld by the Supreme Court.

It seems odd that Biden would even consider the addition of another controversial nomination to his Cabinet while arguing that he wants to heal and unify the country. Yates is clearly an intelligent person and her nomination would be very popular with many on the left. Yet, there is also an interesting dynamic to the nomination as it relates to the controversy over the self-pardon. This may not be the impetus behind the push for Yates but it could be an unexpected benefit. This could be a case where two controversies (like two negatives in mathematics) make a positive.

There has been much discussion over the possibility that Trump could grant himself a self-pardon before leaving office. While this question has bedeviled law professors for years, I have long held the view (before the Trump Administration) that a president can grant a self-pardon but should not do so. Judge Richard Posner discussed the issue in commentary and also concluded that “it has generally been inferred from the breadth of the constitutional language that the president can indeed pardon himself.”

Others disagree (including an excellent piece by Michael Luttig today which is the subject of a response on this blog). Recently, Professor Larry Tribe insisted that Trump cannot constitutionally grant himself a pardon and noted that, if that were the case, Trump’s joke about shooting someone on Fifth Avenue, would “would make that literally true.” (In truth, it would not. Murder is first and foremost a state offense which is not in any way limited by federal pardon power). While I honestly doubt the courts would ultimately uphold Tribe’s view, we may be moving to resolve this interesting question.

On a political level, a Trump self-pardon would might be quietly welcomed by Biden. The President-elect is already getting increasing demands from the left to carry out proposals ranging from packing the Supreme Court to free college tuition to major tax increases to D.C. statehood. There are also rising calls for the prosecution of Trump and many in his inner circle. Biden needs those prosecutions like another election recount. It will continue divisions and discord into his Administration.

So why would Yates help? Because her nomination would be the ultimate argument for Trump to use for a self-pardon. Yates would rekindle far-right deep state conspiracies and confirm for many that the same biased, anti-Trump officials were being returned to the Justice Department. I would hope that Yates would not act in such a predatorial fashion but Biden could not pick anyone (short of James Comey) who would be more triggering for the right.

So everyone might win in a strange way with a Yates confirmation.

Yates would pull off the most dramatic staged demise since Romeo and Juliet.

Biden would have an excuse not to investigate and prosecute Trump.

Trump would reduce his exposure to only state prosecutions while claiming that he had no choice but to self-pardon.

Everyone was left no choice and politics again triumphs over principle. To paraphrase the move “The Bronx Tale,” “you can ask anybody from my neighborhood, and they’ll just tell you this is just another [Beltway] tale.”

via ZeroHedge News https://ift.tt/2JPRa8S Tyler Durden

WTI Dips After Biggest Gasoline Build In 8 Months Sparks Demand Fears Tyler Durden

Tue, 12/08/2020 – 16:35

Oil prices waffled around today with WTI unable to break away from $45.50 with any confidence as the market weighed near-term demand risks from rising virus cases against hopes for more stimulus and a vaccine rollout.

“The key for oil demand is to get the pandemic under control by the summer travel season,” said Jay Hatfield, CEO at InfraCap in New York. “You’re going to have some bad Covid headlines, but every bad Covid headline seems to be paired with a good vaccine headline.”

Analysts expect a third weekly draw of very small size in crude…

API

Crude +1.141mm (-700k exp)

Cushing -1.845mm

Gasoline +6.442mm – biggest build since April

Distillates +2.316mm

API report a 1.14mm barrel crude build, a big surprise relative to the 700k draw expected, but it was the stocks of products that increased significantly…

Source: Bloomberg

WTI hovered around $45.60 ahead of the API print, and slipped lower on the surprise build…

“For demand to continue to pick up, a big part of that is going to be travel and an open economy,” said Peter McNally, global head for industrials, materials and energy at Third Bridge. “That goes back to vaccines.”

via ZeroHedge News https://ift.tt/39QqmQE Tyler Durden

The past two years have been especially brutal to so-called equity ‘bears’. Against all odds, and despite all the shocks, global capital markets—if not the real economy they are supposed to represent—have continued to climb to new heights. After the onset of the coronavirus catastrophe, the relentless rise of the asset markets, particularly in the U.S., has completely baffled many.

But it should not. We are in the midst of an asset market mania—perhaps the biggest of all time.

All the while we have been warning about the possibility of collapse of the world economy, beginning in March 2017, when we issued our first-ever warning of global crash. Then we wrote:

The crisis of 2007 – 2008 reversed the trend of financial globalization, which has undermined global growth. The pull-back in financial globalization has been masked by central bank-induced liquidity and continuous stimulus from governments which have created an artificial recovery and pushed different asset valuations to unsustainable levels. This implies that we live in a “central bankers’ bubble”.

We have noted in several times this year how central banks and especially the Federal Reserve (or the “Fed”) has been acting as the ‘de facto’ market-loss back-stopper, successfully pushing asset markets to new heights. However, it is obvious that the central bankers are only following the script they had written before. This is no ‘New Normal’.

So, let’s take a tour of the bailouts over the past 11 years.

Starting with a bang

In the depths of the Global Financial Crisis at the end of 2008, standard monetary policy tools became ineffective. After slashing the Fed funds rate below one percent in October 2008, the Federal Open Market Committee (FOMC) decided that more drastic action was needed.

Fed officials came up with the idea (not a new one, actually) to start buying assets from the secondary market. Probably to make such a measure sound like a sophisticated component of an up-to-date arsenal of monetary policy, it was called quantitative easing, or “QE”.

The Fed, when beginning the current cycle of QE-programs (the Bank of Japan ran a similar program from March 2001 till March 2006; more on that later), linked QE tightly to the ability of a central bank to lower short-term interest rates to the ‘zero lower bound’, where short-term rates are zero (the Fed has less control over longer-term rates, though it can affect them, too.)

During the first round of QE, enacted on November 25, 2008, the Fed bought marketable securities issued by U.S. Government Sponsored Enterprises (GSE) and mortgage-backed securities (MBS). In March 2009, the program was extended to include purchases of U.S. Treasury debt.

China to the rescue

When the financial crash of 2008 resulted in a burgeoning global recession, Chinese leaders enacted USD multi-trillion infrastructure programs that powered the world economy out of a deep ditch into a renewed upward trajectory. These programs were financed by credit issued by state-controlled banks, which Beijing can essentially compel to lend. As Beijing ordered banks to ramp-up lending, the banks responded by doubling the volume of loans on a year-over-year basis—a truly fantastic level of stimulus.

Between 2007 and 2015, 63% of all new money created globally came from China, and most of this increase was created by Chinese commercial banks. Such colossal credit stimulus pushed the world economy, and especially Europe, into a fast recovery, and without it, the story after the GFC would almost certainly have been completely different.

And the bailouts kept on coming…

But the Chinese were not the only players on the field. To get a sense of the consistency and extent of these coordinated interventions, let us review the main bailout operations of the past ten years:

In October 2010, the Bank of Japan started to buy Exchange Traded Funds (ETFs) linked to the Japanese stock market. It became customary that the BoJ would begin to buy whenever the Topix stock market index fell more than a 0.2 percentage points by midday.

In August 2012, the European Central Bank enacted the Outright Monetary Transactions (OMT) program to halt the rise in sovereign yields in the Eurozone.

In 2015, the Chinese economy started to roll over again. Authorities directed funds for investment through the shadow banking sector which led to an unprecedented credit spree.

Also in 2015, in an effort to devalue the Swiss Franc, the Swiss National Bank started to “invest” in foreign assets, including U.S. equities including many of the top technology names. In many cases, such purchases by the SNB coincided with episodes of increased market turbulence, as during the first rate-hike cycle of the Fed in 2016-2017.

During 2017 central banks across the globe forced over $2 trillion worth of artificial central bank liquidity into the global markets, mostly through their aggressive asset purchase programs.

In December 2018, the People’s Bank of China started to support the domestic banking sector by injecting hundreds of U.S. billions worth of liquidity into the system to stop a run on the weaker banks in the system.

The ‘pivot’ of the Fed

On January 4, 2019, following a three-month long market rout which escalated in early January, the Fed pivoted from its firm assurances of several interest rate rises in 2019 and automated balance sheet run-off that would be like “watching paint dry.”

Between January and March 2019, the Federal Reserve made a complete U-turn. In early December 2018, Chairman Powell was still anticipating several interest rate rises for 2019, but by March they had reverted to possible cuts and ending the balance sheet normalization program altogether.

The Fed cut interest rates for the second time for the year in August 2019, and the ECB pushed rates further into negative territory and restarted its QE-program in September. The majority of central banks globally dutifully followed suit.

Despite these desperate efforts, the repurchase agreement (“repo”) markets blew up in September 2019, forcing the Fed to intervene in this market for the first time since 2009. This was also the likely starting point for a resumption of the ongoing global financial crisis.

And then the coronavirus pandemic struck.

In comes the Corona shock

On March 16th, 2020, rates on the U.S. short-term bonds, on which cities and states often rely for their short-term financing needs, exploded higher. Liquidity and buyers evaporated from several key parts of the U.S. capital markets, including corporate fixed-income and even Treasury markets.

There was an immediate sense of panic in the stock markets. On the March 16th, 2020, the “implied volatility index” or “VIX”, of the U.S. stock markets reached 82.69, the highest on record, ever. The DJIA plunged by 2,997 points, or 12.9 percent, the worst point drop on record. And then, the authorities stepped in.

On the 16th, the New York Fed announced that it would add $500 billion in overnight loans to the repo-market. On Tuesday, the 17th, the Fed announced that it would use $1 trillion to mop-up corporate paper from issuers. On Wednesday, the 18th, the ECB announced that it would buy 750 billion euros worth of bonds and securities. On the 19th, the Fed announced that it would create a lending facility to support money-market mutual funds. Other central banks across the global launched similar support operations.

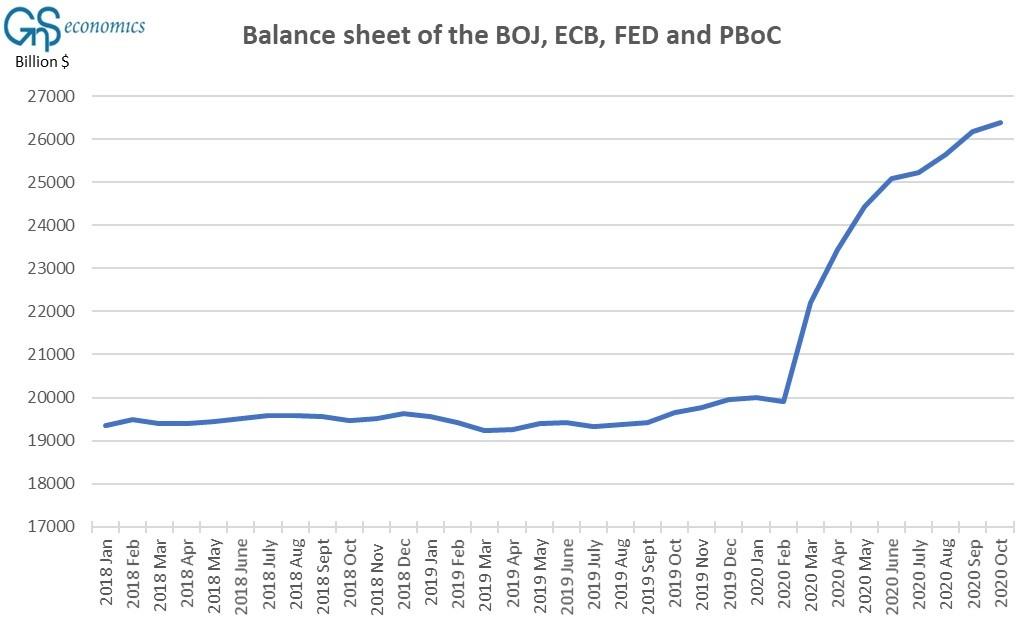

And now, we are here.

Figure. The combined balance sheet of the BoJ, ECB, Fed and PBoC. Source: GnS Economics, BoJ, ECB, Fed, PBoC

Is this the ‘New Normal’? (No)

Many seem to be under the impression that this sort of thing can go on forever. In all fairness, judging from the past, their case seems to be supported by facts. If central banks have been able to keep everything from falling apart up to this point, why couldn’t they simply keep on going indefinitely?

We outlined the ways central banks can fail—or become obsolete—in Q-Review 3/2019. Effectively, it always requires a political decision to either audit or dismantle a central bank, or to not recapitalize in the case of overwhelming capital loss. However, there is an additional ‘neutron bomb’ to consider, a factor the central banks cannot control: the banking system.

If confidence between large financial institutions in the all-important “interbank market” is broken, there is practically nothing a central bank can do to fix it. It can provide cheap loans to banks, but they are just loans.

If, for example, there is a risk of sudden re-emergence of foreign exchange risk, and a redenomination of outstanding loans in that currency, banks will reprice this risk in the interbank markets, which may then freeze-up. This is a real risk in the Eurozone with the possibility of various national “exits”, and the likely reason why the ECB is pushing so hard for the acceptance of the “recovery fund”. We have detailed the specifics of this kind of financial crisis in this blog.

So, there are, in fact, several ways central banks can lose control of the today’s highly-levered and highly-speculative financial systems. And, when that happens, look out below!

* * *

December issue of our Q-Review will deal with the Aftermath -scenarios of the coronavirus pandemic. Check out our year-end offer for Annual Q-Review Subscriptions from GnS Store. Stay informed how the world economy and the global economic crisis through our Q-Review reports and Deprcon Service.

via ZeroHedge News https://ift.tt/3lVaAGt Tyler Durden

“No End In Sight”: Watch Gundlach’s DoubleLine Webcast Tyler Durden

Tue, 12/08/2020 – 16:17

It’s been a few months since Gundlach last held one of his open webcasts for his DoubleLine bond fund. Among other things, it will be interesting to hear his comments on the market meltup, the ongoing dislocation between stocks and bonds, the K-shaped recovery, and of course his thoughts on the next president (Gundlach famously predicted that Trump would win again, with the caveat that a flare up in Covid-19 cases could change the outcome).

Today’s webcast is titled “No End in Sight,” probably a reference to the liquidity firehose unleashed by central banks to prop up stock markets and to make the wealth divide even greater.

Courtesy of Bloomberg, the last time Gundlach made the following observations:

The Dollar: He is a long-term dollar bear, but said that even in the short-run, the dollar got ahead of itself.

Treasuries: He expected the yield curve to steepen with 30-year yields rising. He also bet against the TIPS market

Stocks: Gundlach said the S&P 500 was in “nosebleed territory. This is not a cheap market.” He added the market was the most overvalued in history when looking at market cap relative to U.S. GDP.

Corporate Bonds: Gundlach warned of a wave of downgrades of BB-rated bonds into the high yield spaces, saying the spread between BBB-rated bonds and BB-rated bonds were historically narrow.

Most recently, Gundlach ominously tweeted that “lots of financial trends are quietly reversing”- we are confident he will dig into this topic as well.

Lots of financial market trends quietly reversing. Will be addressing that in the weeks ahead.

Stocks oscillated gently lower overnight then went wild as the cash markets opened, soaring all day but appeared to roll over a little when McConnell suggested slashing the liability protections and state/local aid from the COVID Relief bill (implicitly reducing the amount of free money to be handed out) and extended losses a little more when headlines on SCOTUS taking up Texas’ election case against MI, PA, and WI…

Small Caps continued their rebound against mega-tech again…

Source: Bloomberg

Another day, another massive short-squeeze…

Source: Bloomberg

The SMART money ain’t buying it…

Source: Bloomberg

“This is madness”…

Homebuilders got hit today…

Source: Bloomberg

Bank stocks have trod water for two weeks now…

Source: Bloomberg

TSLA managed to get green despite selling another $5 billion of stock…

Notably, Cyclicals relative to Defensives continue to have stalled at a key level. Is it time to catch down to yields?

Source: Bloomberg

The value rotation is starting to lag again…

Source: Bloomberg

Despite stocks gains, bonds were also bid today – erasing all of the payrolls spike in yields…

Source: Bloomberg

And so was bullion…

Source: Bloomberg

But Bitcoin was sold back below $19k…

Source: Bloomberg

As the dollar chopped around in a newly unusual tight range…

Source: Bloomberg

Copper’s exuberant run higher relative to gold appears to have stalled out at key resistance. We’ve seen this before (cough Q1 2019 cough)…

Source: Bloomberg

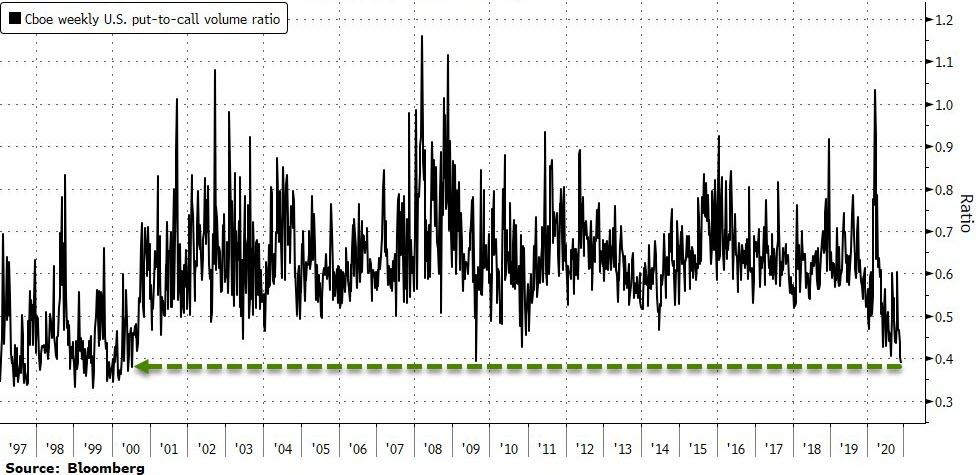

Finally, complacency has gone to ’11’ as the weekly Cboe ratio of volume traded in puts versus calls fell to the lowest since July 2000 just as the S&P 500 Index hit an all-time high.

Source: Bloomberg

This implies extreme positioning to the upside, as investors look beyond short-term uncertainty toward a continuing global recovery in 2021.

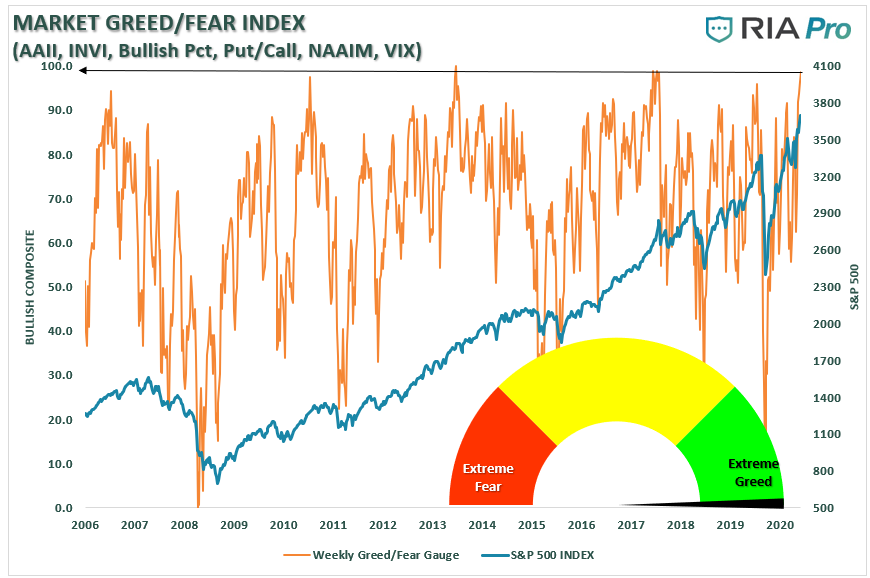

And Greed is good-est…

And Nomura Stock Sentiment is at its highest since 2004…

What could go wrong?

Especially with global stocks over $100 trillion and massively extended relative to world GDP…

Source: Bloomberg

via ZeroHedge News https://ift.tt/2VVJuo0 Tyler Durden

Surprise: Student Debt Relief Will Mostly Help Middle- And Upper-Income Households Tyler Durden

Tue, 12/08/2020 – 15:40

Now that the air is heavy with talk of debt forgiveness, initially starting with the government’s $1.6 trillion student loan portfolio before Democrats move to a broad debt jubilee much to the chagrin of all those Americans who responsibly have paid their obligations every month, investment banks have started analyzing the impact of the various student loan forgiveness proposals.

One such analysis comes from Goldman’s economics team which, in what will likely come as a disappointment for progressives, has calculated that even substantial debt reilef “would only have a small effect on GDP”, specifically, forgiving federal student loans up to $10k would add less than 0.1% to the level of GDP starting in 2021, and cumulatively add only $0.43 in real GDP for each $1 of forgiven debt over the next 10 years. A more generous debt relief program that forgives federal loan balances up to $50k would provide a slightly bigger boost to GDP, but would have a smaller per-dollar impact.

Meanwhile, forgiving federal student loans up to $10k would likely cost around $300bn (1.6% of GDP), while forgiving loans up to $50k would cost around $800bn (4.1% ofGDP). However, since these loans have already been funded through prior Treasury issuance, the impact on Treasury financing would be spread out over many years due to the lack of interest and principal payments. If loans were forgiven immediately, Treasury’s financing needs might actually decline, as tax payments on the forgiven amounts would likely more than offset the lack of scheduled loan payments.

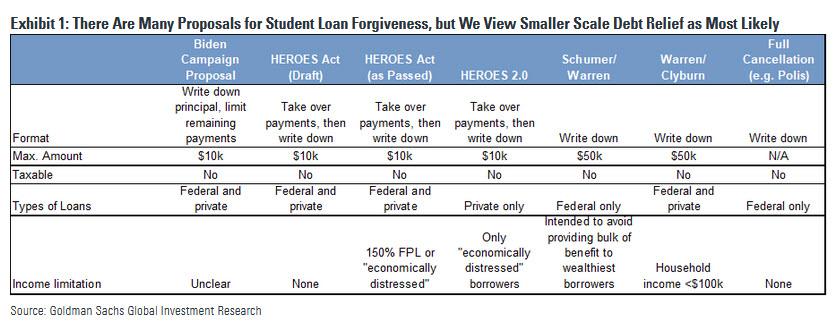

Taking a step back, loan forgiveness provisions have made it into the initial version of the HEROES Act—the House Democrats’ $3.4 trillion COVID-relief proposal that the Senate never passed—though none of the leading stimulus proposals in front of Congress at the moment deal with the issue. In light of the seemingly dim prospects for near-term legislative approval,several Democrats, including Senate Majority Leader Chuck Schumer (D-N.Y.) and Senator Elizabeth Warren (D-Mass.), have instead shifted their sights to executive action. The chart below summarizes several of the recent proposals.

While noble in theory – if only to those who have never paid down their debt while a slap in the face to all those who have – in practice this rush to appeal to populism carries numerous traps, besides just the modest boost to the economy.

One is that while loan forgiveness is fairly popular in concept — 55% to 60% of voters in several recentsurveys support forgiving up to $50k in student loans — it is likely to become more controversial once the cost and distribution of benefits of such a policy becomes clear, especially if it amounts to $800BN (as noted above).

Second, there are potentially significant tax implications that could do more harm than good to some borrowers in the near term. Debt forgiveness is usually treated as taxable income to the borrower. Some student debt is excepted from this, either because of specific exemptions in the HEA or the tax code, or through Treasury’s interpretation of the tax laws in specific circumstances. However, as it currently stands, debt forgiven through a broad federal forgiveness program would be taxable to the borrower. (Some tax lawyers argue that the Treasury would have the authority to exempt this debt without Congress, but whether this could or would happen is hard to predict.) For example, forgiving $50k in student debt for a borrower with $100k in income (and a marginal tax rate of around 25%) would leave them with a tax bill of around $12.5k in a single year, probably more than the entire tax bill on their other income. Beyond a legislative or administrative change to tax rules, one potential way to mitigate this might be to spread forgiveness over several years by relieving borrowers of their responsibility for scheduled payments or simply forgiving loan principal in several installments.

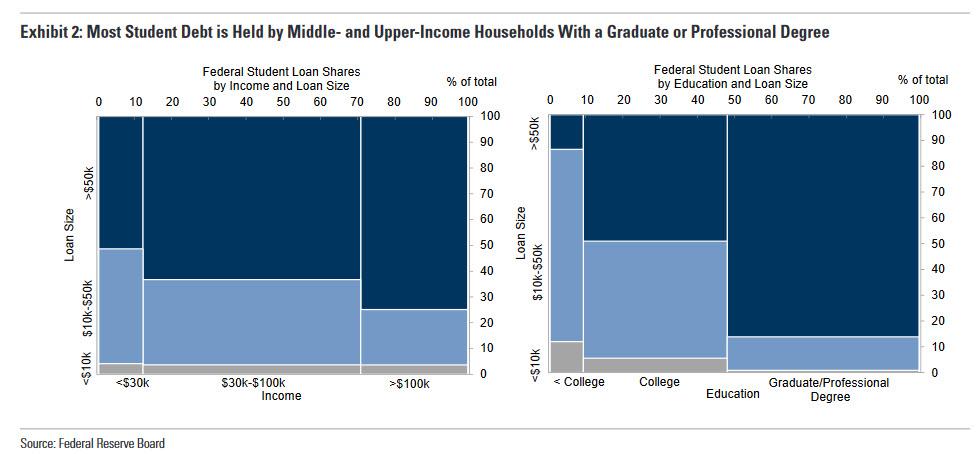

The third and biggest reason we Goldman expects the Biden Administration to take a much more incremental approach is not only that the boost to consumption from widespread student debt relief would likely be modest in comparison to the budgetary cost (as noted above), but that it would mostly benefit the middle and – drumroll – upper classes. As Goldman’s Jan Hatzius writes, “although over 43 million individuals have federal student loans totaling almost $1.6tn, most federal student debt is held by middle- and upper-income households, and over half—including the vast majority of large debt balances—is held by highly-educated households with a graduate or professional degree (Exhibit 2).” According to Goldman – and frankly anyone with half a brain – these households likely have significant earning potential (we do not adjust for pervasive laziness or a predisposition to sit on your ass and ruminate rather than actually doing something useful with your life) and are less likely to be resource constrained, so eliminating their loan payments i) might not generate a large spending response and ii) once the peasants realize that their progressive heroes are once again bailing out the rich, the outcry would be a sight to behold.

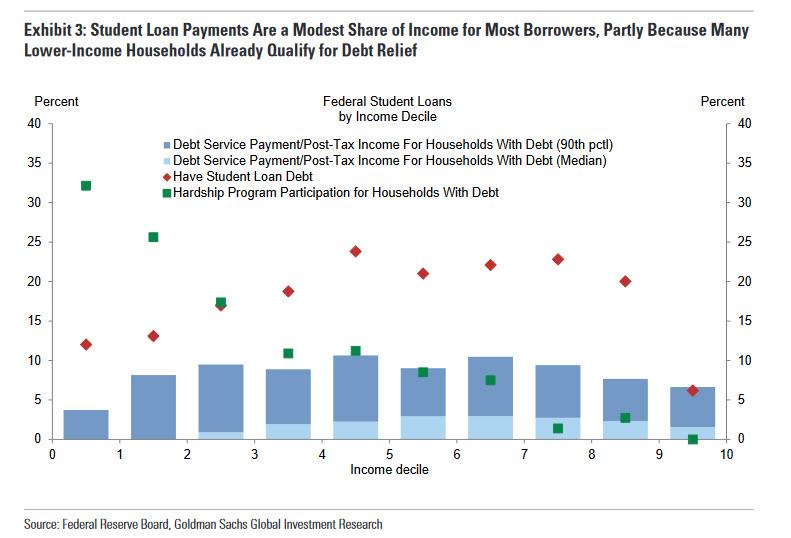

As an aside, despite what you may have read, federal student loan payments account for only a modest share of after-tax income for most borrowers. The next chart shows that the median payment-to-income ratio for households with outstanding federal student debt is below 3% for all income deciles, and the 90th percentile is less than 11%. These low payment-to-income ratios reflect low interest rates on federal student loans, and that many households that would otherwise struggle to meet payments already qualify for debt relief (that’s right: all those feminism and classical harpsichord majors who make about $15,000 a year already have debt forgiveness). Indeed, as Goldman confirms, over 32% of households with federal student debt in the bottom income decile are already enrolled in an income-based repayment or hardship deferral program.

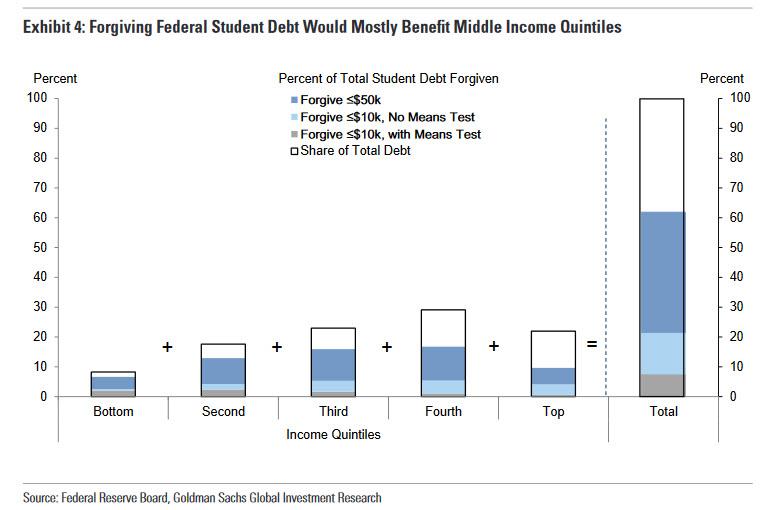

Finally, the chart below, looks at the share of total student debt that would be forgiven under a 10K and 50K forgiveness policy. Forgiving up to $10k in student loans per borrower would reduce total federal student debt balances by 22%, with the benefits most concentrated among middle-income households (Applying a means test by only forgiving debt for households that either have income less than 150% of the federal poverty line or are economically distressed would make the policy significantly more progressive). The more expansive policy that forgives all federal debt up to $50k per borrower reduces total debt balances by 62%, but middle- and upper-income households receive an even greater share of the benefits.

Yet despite this analysis showing the student debt forgiveness would i) do little to boosting consumer spending or the economy, ii) would mostly benefit middle and upper-income households, we are confident that Biden will sign an executive order forgiving at least $10,000 in student loans.

Why? Because as we showed recently, blue states have the highest average student debt.

And since this proposal has little to do with actually stimulating the economy (and certainly encouraging responsible financial behavior) and everything to do with further widening the red-blue divide, it is virtually assured that it will pass if only for that reason.

via ZeroHedge News https://ift.tt/37Jyy2o Tyler Durden

The conventional view of inflation is that it’s not only low, but dangerously low and in need of aggressive stimulus.

But that view is becoming increasingly hard to defend, given all the things that are soaring in price. Consider:

The above charts show the price action in industrial commodities that, while not something individual consumers tend to buy (and therefore not part of the official “cost of living”) do affect the price of consumer goods. In other words, when they go up, so eventually do the prices of cars, TVs and buildings.

Speaking of buildings, the next chart shows US home prices – which have been rising steadily since the bottom of the last recession – steepening this year. Note the upward inflection at the right of the chart. Home prices are now higher than they were during the previous decade’s housing bubble, and they’re accelerating.

And last but not least, the US dollar – whose rate of decline is the official definition of inflation – has begun to fall versus not just real things but even against the other crappy fiat currencies.

Add it all up and today’s world has emphatically stopped looking deflationary or even disinflationary. Price increases have morphed from isolated to wide-spread, and it’s just a matter of time before people start to notice and act accordingly.

via ZeroHedge News https://ift.tt/36ZkFhz Tyler Durden

With Democrats and Republicans still stuck at an impasse on stimulus negotiations, one Maryland Congressman and erstwhile presidential candidate named John Delaney has engineered a novel strategy for killing two birds with one stone: dispersing another round of stimulus funds, while ensuring that enough Americans consent to receiving the vaccine that the US can quickly top the roughly 70% immunity threshold at which point scientists believe the vaccine will stop propagating.

And that plan is: Offering Americans a $1,500 “incentive payment” to acquiesce to receiving both doses of the vaccine. Delaney argued that the plan would benefit all Americans, even those who still refuse, because it might help the country crush the virus more quickly.

“The faster we get 75% of this country vaccinated, the faster we end Covid and the sooner everything returns to normal,” Delaney said in an interview with CNBC.com.

To be sure, Delaney’s plan has virtually zero chance of becoming law. Republicans and Democrats can’t even seem to agree on basic things like the size of the package ($600BN or $900BN) and whether businesses deserve a liability shield to stop them from being sued by people claiming to have been infected in their establishment (GOP leader Mitch McConnell sees this as a must). President Trump recently promised Americans that the vaccine wouldn’t be mandatory.

Delaney initially conceived of the scheme as a workaround for the widespread public skepticism about the vaccine. While recent opinion polls show that the number of Americans planning to get the vaccine as soon as it’s available has been on the upswing, more than 40% of the population either has already been infected, doesn’t see any urgent need for a vaccine, or simply doesn’t trust the data.

It’s also the latest indication that public health officials are anxious that the vaccine won’t have enough credibility to convince enough Americans to accept it. With so much at stake, it makes sense that some other “incentives” might be considered.

Delaney told CNBC that Americans are going to need some kind of an incentive to encourage them to take the vaccine.

“We have to create, in my judgment, an incentive for people to really accelerate their thinking about taking the vaccine,” Delaney said. To be sure, those who are not comfortable receiving the vaccine would not be forced to do so.

Though he reckoned that even those who refuse to participate will still benefit from the program, which he said could cost roughly $380MM, because once COVID is eradicated, everybody will benefit.

“If you’re still afraid of the vaccine and don’t want to take it, that’s your right,” Delaney said. “You won’t participate in this program. “But guess what?” he added. “You’re going to benefit anyhow, because we’ll get the country to herd immunity faster, which benefits you. So I think everyone wins.”

To be sure, while Delaney’s plan might seem workable on the surface, experts pointed out that it would likely be difficult and costly to pull off.

Some experts are skeptical that such a plan could work. “It’s an interesting idea,” said Bill Hoagland, senior vice president at the Bipartisan Policy Center and a former Senate staffer, however, he felt it would be wrong to tie people’s stimulus checks to vaccine timetable, given the initial shortage of doses. Plus, the IRS’s dated IT systems might buckle from the effort of cross-checking whether individuals actually had received their vaccinations before doling out the stimulus money.

Other countries, including Mexico, have used “incentive” payments like this to get their vaccination rate up. But as Delaney willfully admits, in the US, we already have a pretty strong system of incentives to encourage vaccinations, and what’s more, it’s mostly targeted at children: states have vaccination rules that require students to get their shots before they’re allowed in a classroom.

So, why should the federal government spend all that money when there are other, cheaper, ways to pressure families into submitting?

via ZeroHedge News https://ift.tt/3gnRK9W Tyler Durden

Billionaire Ray Dalio Holds Reddit AMA To Discuss Rise Of China, Threats To Dollar’s Reserve Status Tyler Durden

Tue, 12/08/2020 – 14:50

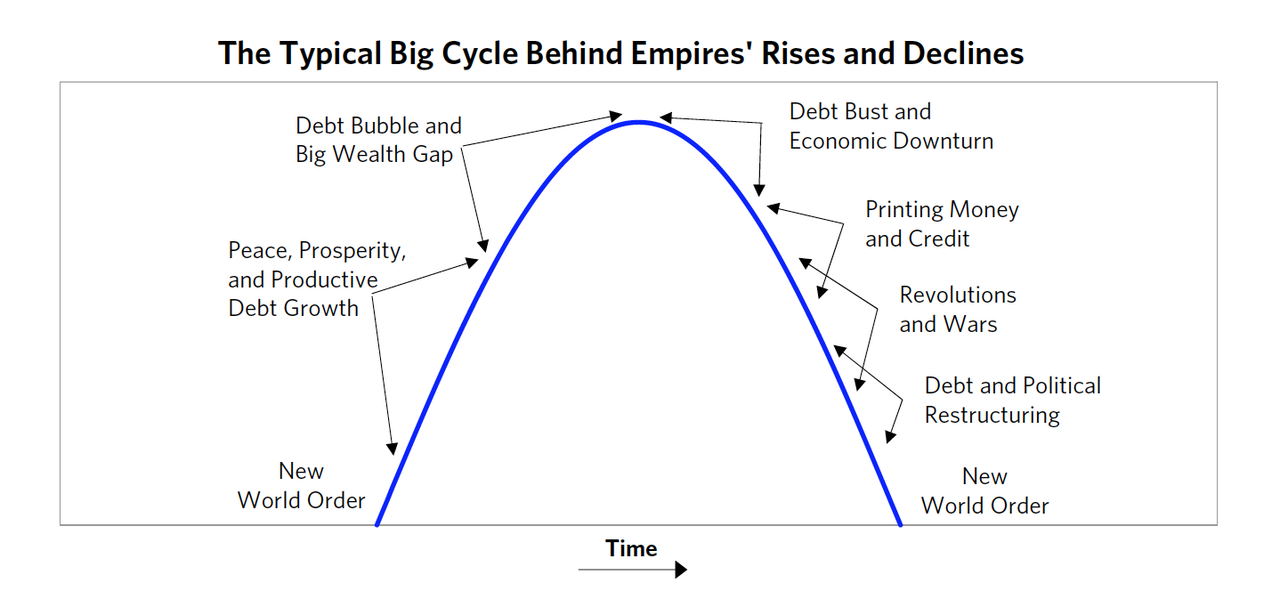

For the past few years, as Bridgewater, the titanic hedge fund, mostly continued on autopilot with the computers handling most of the investing, the firm’s founder and longtime leader, Ray Dalio, has been refining his thesis about the next major turning point in global history, which Dalio believes will be precipitated by the growing tensions between a rising China and falling America.

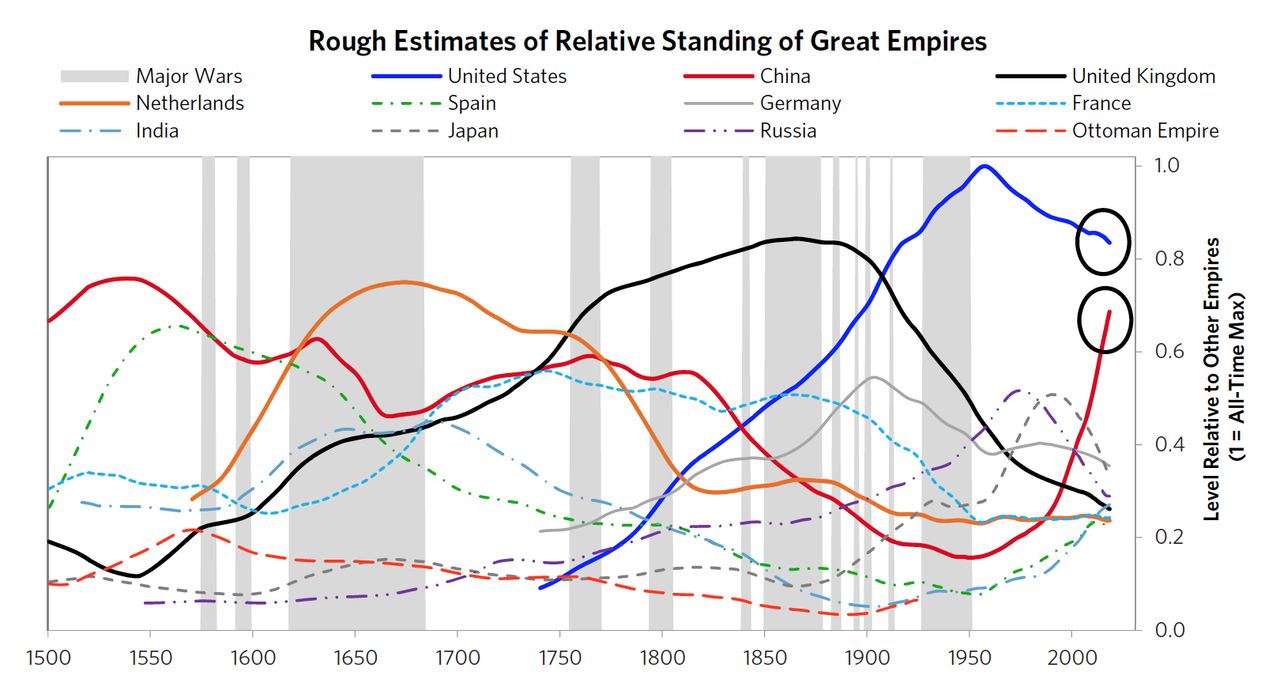

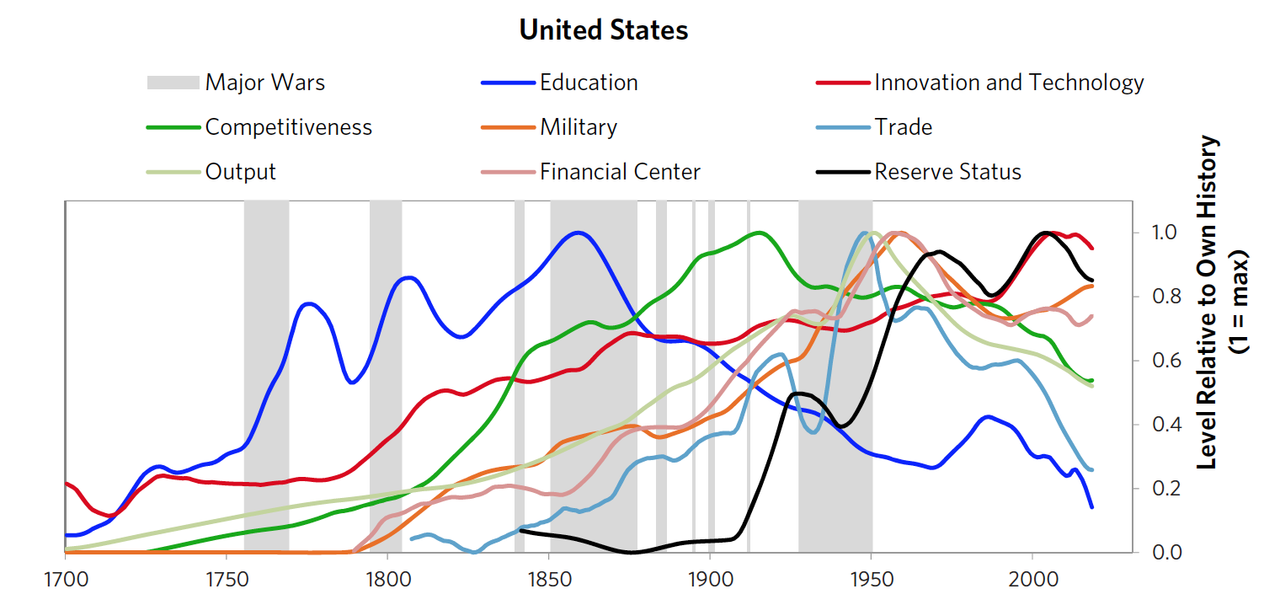

That empires rise and fall is nothing new to history, Dalio says. He even produced a helpful chart that illustrates the waxing and waning standing and influence of the world’s ‘Great Powers’ dating back to the 1500s.

Using a handful of metrics measuring national performance in areas including education and innovation, Dalio produced a chart breaking down this ‘decline’ in American Greatness – so to speak. Though declines in “education” and “trade” are at the lowest levels relative to history, other critical indicators – including “innovation and technology” and “reserve status” (which allows America to borrow so heavily without driving surging interest rates and inflation) – have – according to Dalio’s analysis – only just turned over.

Looking back across the vast sweep of history, Dalio claims that dissolution of empires is almost always driven by a handful of factors, including unsustainable debt & money printing and growing political animosity and unrest. Sound familiar?

Of course, with US stocks pressing back toward record highs on Tuesday, investors are signaling that all is well in the US. In fact, despite a brutal pandemic and one of the worst economic crises in a century, things have apparently never been better. Well, at least for the roughly half of Americans who are lucky enough to own stocks.

This is why Dalio re-upped his warnings a few days ago about the US being on the cusp of another civil war or revolution. Both people and politicians are “at each other’s throats” with an intensity that outweighs anything Dalio has seen before during his 71 years on this planet. Whether this dynamic gets worse, or better, will have profound implications for the future of the country, according to Dalio’s latest LinkedIn essay.

“People and politicians are now at each other’s throats to a degree greater than at any time in my 71 years,” Dalio wrote noting that disorder is rising in a number of countries. “How the U.S. handles its disorder will have profound implications for Americans, others around the world, and most economies and markets.”

As it happens, Bridgewater fanboys and/or frustrated bears eager for a heavy dose of FUD will have yet another opportunity to question Dalio directly about his views, when he signs on to Reddit later on Tuesday for a 90-minute AMA to discuss his China thesis. The live Q&A, which will take place here, is set to begin at 1500ET, and run through 1430ET.

As many of you know, I’ve been studying the forces behind the rise and fall of great empires and their reserve currencies throughout history, with a focus on what that means for the US and China today. Many of the things now happening the world… (1/3) pic.twitter.com/JECV5Q9Gwo

…like the creating a lot of debt and money, big wealth and political gaps, and the rise of new world power (China) challenging an existing one (the US)—haven’t happened in our lifetimes but have happened many times in history for the same reasons they’re happening today. (2/3)

Today, I’ll be doing a Reddit AMA from 3-4:30PM EST, where I can discuss this with you and we can explore the patterns of history and the perspective they can give us on what is happening today. You can join here: https://t.co/5MK9URu76L (3/3)

Interested parties will need a reddit account to ask questions. We imagine this Q&A might generate more interest than in the past as the dollar’s recent weakness has spurred plenty of speculation about whether the dollar’s reign as the unchallenged global reserve currency has finally come to an end.

via ZeroHedge News https://ift.tt/3mYURaR Tyler Durden