Major Military Search Underway After US F-15 Jet Crashes In North Sea Tyler Durden

Mon, 06/15/2020 – 11:03

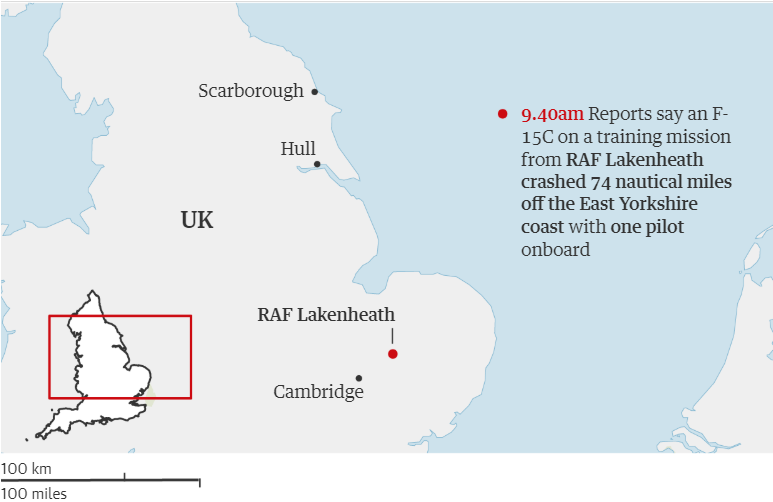

A US Air Force F-15 fighter jet has crashed in the North Sea off England’s coast on Monday, triggering a major UK search and rescue mission as the fate the pilot is as yet unknown.

“A U.S. Air Force F-15C Eagle crashed at approximately 0940 [local time] today in the North Sea. The aircraft was from the 48th Fighter Wing, RAF Lakenheath, United Kingdom,” a UK 48th Fighter Wing statement said. “At the time of the accident, the aircraft was on a routine training mission with one pilot on board.”

The F-15 Eagle is an all-weather, extremely maneuverable, tactical fighter. Image source: US Air Force

“The cause of the crash as well as the status of the pilot are unknown at this time, and U.K. Search and Rescue have been called to support,” it added.

The UK coast guard is leading the search effort alongside the US military after the coast guard received alerts of “an aeroplane going down into the sea 74 nautical miles off Flamborough Head.”

The US Air Force also confirmed the F-15C Eagle was reported going down over the sea in an area off the coast frequently used for military flight training exercises.

Via The Guardian

The US routinely conducts joint training and military readiness exercises with the RAF’s 48th Fighter Wing.

Hours after the crash, the pilot still has not been recovered. “Search and Rescue effort are currently under way, but the pilot and of the aircraft is still missing. We will provide updates as they become available, while prioritizing respect and consideration for the pilot’s family,” US AF Col. Will Marshall said in an update.

via ZeroHedge News https://ift.tt/30GkncF Tyler Durden

While not perfect, we can add an increase in “trash stock” speculation as another potential signal for the peak of the market cycle.

That signal may have arrived, according to ZeroHedge:

In nearly every market cycle, speculation in low-quality, virtually valueless and literally bankrupt stocks, marks a market top.

This brings into question the Dow’s recovery that began in late March, which has humbled Stanley Druckenmiller:

That Fed stimulus, combined with investor excitement about the gradual reopening of U.S. business, is leading to broad outperformance among those stocks hit the hardest in March… He added that the technical momentum the market has right now, what he called “breadth thrust,” could carry equities even higher.

The Fed stimulus pumped trillions into the markets. Investor excitement can inflate stock prices. Reopening businesses can spark more optimism.

However, if Doug Kass at Seabreeze Partners is correct, he may be seeing through the hubris. In a recent piece, he directed attention toward another fact:

If you look carefully at the Nasdaq… you would be surprised to see how many stocks have underperformed – as a handful of large stocks coupled with a group of speculative (but valueless) equities have been carrying the weight of the Average.

It’s those “trash stocks” that have the potential to take the wind out of the market recovery and the overall cycle. And this wouldn’t be the first time this has happened.

The 1999-2002 “dot-com boom” is the most recent such instance, filled with examples of overvalued “trash stocks” that eventually left investors hanging.

Which leads us to today…

Those Who Fail to Learn From History Are Doomed to Repeat It

Kass continued his article by providing this year’s glaring current examples of “trash”:

Already bankrupt JCPenney (CNPQ), Chesapeake (CHK)… (WLL), (NKLA), and leveraged energy small caps – (XTEG), Noble (NBL), and so many others.

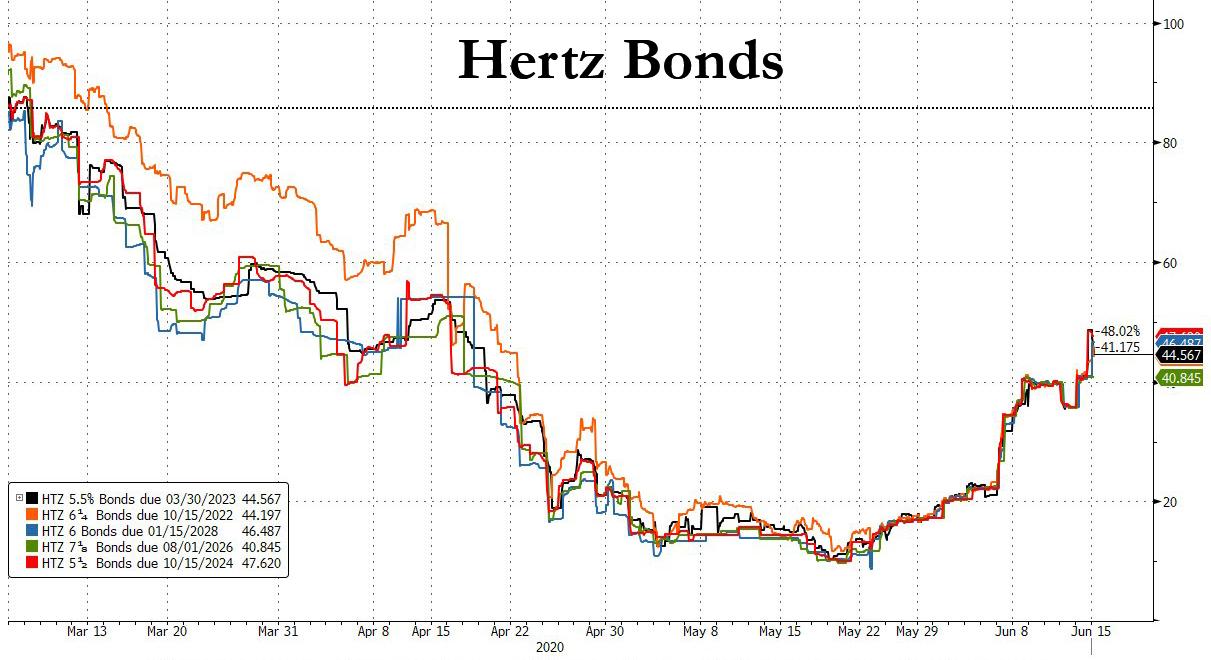

The Hertz Corporation, which recently filed bankruptcy on May 22, has speculators salivating for a little quick cash.

On May 22 the stock was trading at 80 cents a share. By June 8, it had shot up to $5.50, to give Hertz a market capitalization of $787 million. For a bankrupt car rental company.

With 400,000 cars on credit from every major car manufacturer, if Hertz goes bust, that could put a big dent in the bottom line of GM, Ford, Fiat, Chrysler, and others.

This Thursday, the Dow may have offered a dose of reality for the optimist’s “dash for trash,” plummeting 6.9%.

Of course we don’t know what will happen next, but if this “marks a market top” like Kass suggested, the only way for the Dow to go is down.

Make Sure Your Portfolio Doesn’t Contain “Trash”

As more investors dive into risky investments, the markets could get extremely volatile – just as they did in 1999-2002. So now is a great time to examine your own risk levels in your savings.

If you want to hedge against the potential economic “dumpster fire” as risky companies go under, consider diversifying your portfolio with assets that are historically known as a hedge.

Precious metals like gold and silver can provide your retirement a “safe haven” if markets again crash anything like they did in February and March this year.

* * *

With global tensions spiking, thousands of Americans are moving their IRA or 401(k) into an IRA backed by physical gold. Now, thanks to a little-known IRS Tax Law, you can too. Learn how with a free info kit on gold from Birch Gold Group. It reveals how physical precious metals can protect your savings, and how to open a Gold IRA. Click here to get your free Info Kit on Gold.

via ZeroHedge News https://ift.tt/2AGerFI Tyler Durden

Supreme Court Rules American Workers Can’t Be Fired For Being Gay Or Trans, Defying White House Tyler Durden

Mon, 06/15/2020 – 10:41

Update (1100ET): In a series of tweets, Glenn Greenwald parses the logic undergirding the majority opinion, and what it portends for future rulings from the conservative-dominated court.

The Gorsuch opinion was joined by John Roberts, as well as the 4 court liberals.

This @voxdotcom article from last year by @imillhiser proved prescient in explaining why Gorsuch made very well side with the court’s liberals in holding that Title VII bars the firing of gay and trans employees for being LGBT: https://t.co/zTmYTPPetK

Gorsuch didn’t conclude that he personally believes it’s wrong to fire employees for being LGBT. He didn’t conclude it *should* be illegal to do so.

He only concluded that the plain language of the 1964 Civil Rights Act, whether it intended this or not, requires that outcome: pic.twitter.com/CCHYDhGppG

In other words, Gorsuch set aside his own personal beliefs about what the law should be – and ignored what he believed the framers intended – to interpret the law as it was written: its text (that’s why Roberts joined).

In a landmark ruling by the US Supreme Court (which now features two new justices appointed by President Trump) gay, lesbian, bisexual and trans individuals cannot legally be discriminated against by employers – meaning they can’t be fired, or not hired, simply for being LGBTQ.

In decisions in two separate cases, the court finally added LGBTQ people as a “protected class” under Title VII of the Civil Rights Act of 1964.

HUGE: Supreme Court rules that federal civil rights law protects gay and transgender workers.

The justices conceded that sexual orientation may not have been on the minds of anyone in Congress when the civil rights law was passed back in the wake of President John F Kennedy’s assassination. But the judges ruled that firing a male employee for dating men, but not a female employee for dating men, would represent illegal discrimination.

The ruling in the first case was a victory for Gerald Bostock, who was fired from a county job in Georgia after he joined a gay softball team, and the relatives of Donald Zarda, a skydiving instructor who was fired after he told a female client not to worry about being strapped tightly to him during a jump because he was “100% gay”. Zarda died before SCOTUS decided to accept the case.

In a separate case, SCOTUS also ruled that Title VII outlaws discrimination against transgender employees, upholding a lower court ruling that found Aimee Stephens was impermissibly fired from her job at a Michigan funeral home two weeks after coming out as trans to her boss.

Her former employer claimed she was fired for failing to follow the dress code. Like Zarda, Stephens did not live to see the case decided, having died on May 12 while in hospice care for kidney disease.

The cases mark the first notable rulings on gay rights since the retirement of former justice Anthony Kennedy. Notably, the Trump administration opposed the court’s ruling, reversing the stance from the Obama Administration. Chief Justice John Roberts also sided with the liberal justices, though this isn’t the first time he’s ruled on a gay rights issue.

BREAKING: US Supreme Court outlaws discrimination against LBGTQ workers, 6-3.

Incompetence and Errors in Reasoning Around Face Covering

SIX ERRORS:

1) missing the compounding effects of masks,

2) missing the nonlinearity of the probability of infection to viral exposures,

3) missing absence of evidence (of benefits of mask wearing) for evidence of absence (of benefits of mask wearing),

4) missing the point that people do not need governments to produce facial covering: they can make their own,

5) missing the compounding effects of statistical signals,

6) ignoring the Non-Aggression Principle by pseudolibertarians (masks are also to protect others from you; it’s a multiplicative process: every person you infect will infect others).

In fact masks (and faceshields) supplemented with constraints of superspreader events can save us trillions of dollars in future lockdowns (and lawsuits) and be potentially sufficient (under adequate compliance) to stem the pandemic. Bureaucrats do not like simple solutions.

I want to travel this summer

First error: missing the compounding effect

People who are good at exams (and become bureaucrats, economists, or hacks), my experience has been, are not good at understanding nonlinearities and dynamics.

The WHO, CDC and other bureaucracies initially failed to quickly realize that the benefits of masks compound, simply because two people are wearing them and you have to look at the interaction.

Let us say (to simplify) that masks reduce both transmission and reception to p. What effect on the R0(that is, the rate of spreading of the infection)?

Simply the naive approach (used by the CDC/WHO bureaucrats and other imbeciles) is to say if masks reduce the transmission probability to ¼, one would think it would then drop from, say R0= 5, to R0=1 ¼. Yuuge, but there is better.

For one should count both sides. Under our simplification, with p=1/4 we get R0′= p² R0 . The drop in R becomes 93.75%! You divide R by 16! Even with masks working at 50% we get a 75% drop in R0.

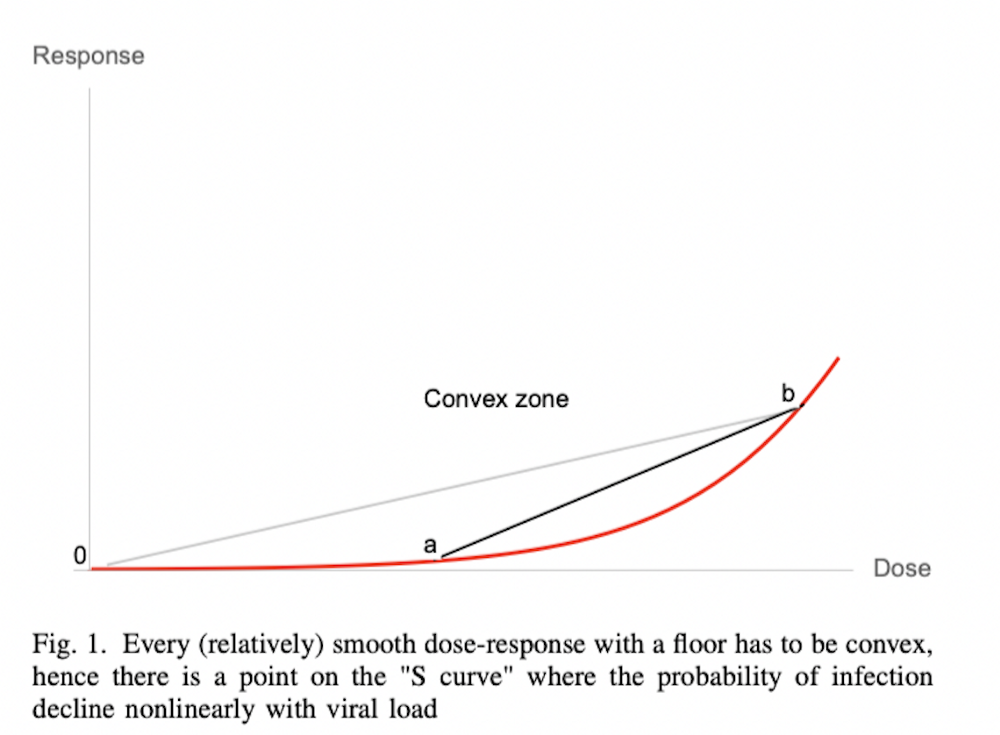

Second error: Missing the Nonlinearity of the Risk of Infection

The error is to think that if I reduce the exposure to the virus by, say, ½, I would then reduce the risk, expressed as probability of infection, by ½ as well. Not quite.

Now consider (Fig 1) that probability must follow a nonlinear dose-response, an “S curve”. In the convex part of the curve, gains are disproportionately large: a reduction of x% of viral exposure leads to a drop of much more than x in risk of infection. And, patently we are in the convex part of the curve. For example, to use the case above, a reduction of viral load by 75% for a short exposure could reduce the probability of infection by 95% or more!

Third Error: Mistaking Absence of Evidence for Evidence of Absence

“There is no evidence that masks work”, I kept hearing repeated to me by the usual idiots calling themselves “evidence based” scientists. The point is that there is no evidence that locking the door tonight will prevent me from being burglarized. But everything that may block transmission could help. Unlike school, real life is not about certainties. When in doubt, use what protection you can. Some invoked the flawed rationalization that masks induce false confidence: in fact there is a strong argument that masks makes one more alert to the risks and more conservative in behavior.

Fourth Error: Misunderstanding the Market and People

Paternalistic bureaucrats resisted inviting the general public to use masks on grounds that the supply was limited and would be needed by health professionals — hence they lied to us saying “masks are not effective”. They did not get the inventiveness and industriousness of people who do not need a government to produce masks for them: they can rapidly convert about anything into well-functioning protective face covering appendages, say rags into which one can stitch coffee filters… about anything. Nor did bureaucrats heed the notion of markets and the existence of opportunists who can supply people with what they want.

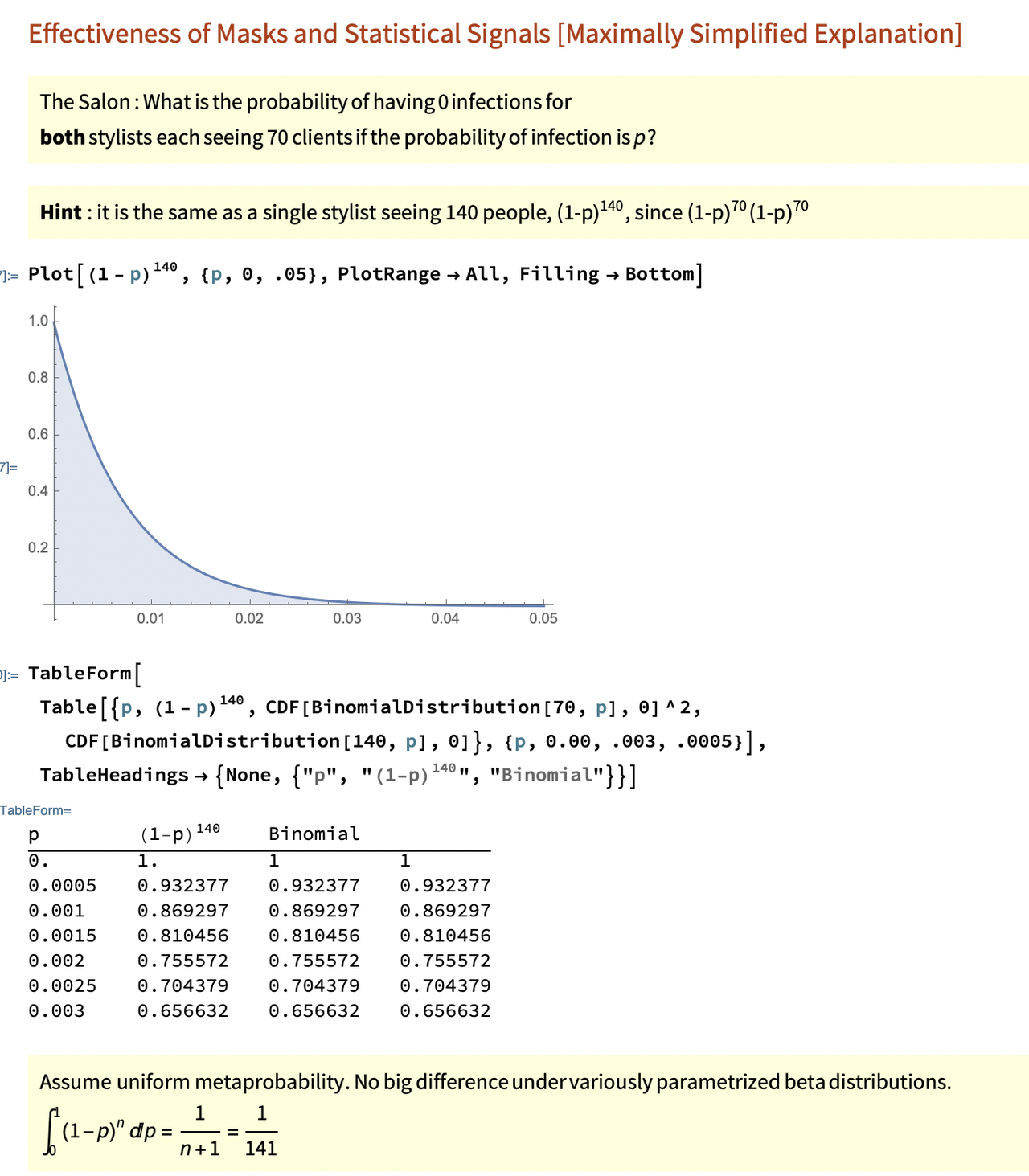

Many people who deal with statistics think in terms of either mechanistic concepts (say correlation) they don’t quite understand, or local results; they fear to be presenting “anecdotes”, and fail to grasp the broader notion of statistical signals where you look at the whole story, not the body parts. For here, again, evidence compounds. We have a) the salon story where two infected stylists failed to infect all their 140 clients (making the probability of infection for bilateral mask wearing safely below 1% for a salon-style exposure) — we know the probability of infection for non mask wearers from tens of thousands of data points and the various R0 estimations) plus b) the rate of infection of countries where masks were mandatory, plus c) tons of papers with more or less flawed methodologies, etc.

Sixth Error: The Non-Aggression Principle

“Libertarians” (in brackets) are resisting mask wearing on grounds that it constrains their freedom. Yet the entire concept of liberty lies in the Non-Aggression Principle, the equivalent of the Silver Rule: do not harm others; they in turn should not harm you. Even more insulting is the demand by pseudolibertarians that Costco should banned from forcing customers to wear mask — but libertarianism allows you to set the rules on your own property. Costco should be able to force visitors to wear pink shirts and purple glasses if they wished.

Note that by infecting another person you are not infecting just another person. You are infecting many many more and causing systemic risk.

Wear a mask. For the Sake of Others.

* * *

Notes

1- I commend the very very very few writers such as Zeynep Tufekci who have been fighting the fight in the media.

2- I truly believe that the pseudolibertarians are sociopaths and misanthropes looking for a political party that they think fits their misanthropy.

1918

1918

via ZeroHedge News https://ift.tt/2CaN0Ez Tyler Durden

Bankrupt Hertz Warns Buyers They’ll Need A Miracle To Avoid Total Loss As Bonds Value Equity At Negative $2 Billion Tyler Durden

Mon, 06/15/2020 – 10:05

Two days after Hertz’ own lawyer, White & Case’s Tom Lauria warned that the trading price of Hertz shares was “disconnected from fundamentals” just as bankruptcy court approved the company’s plan to sell up to $1 billion in stock, the company has issued an 8-K in which it cut the offering price in half – now seeking to raise up to $500 million perhaps as a result of the drop in HTZ stock this morning – with a bevy of risk factors laying out the terms of the deal that Jefferies will pursue in its quest to sell hundreds of millions of HTZ shares to retail investors, including using the word “worthless” to describe its stock no less than five times.

On June 15, 2020, Hertz Global Holdings, Inc. (the “Company” or “we”) entered into an open market sale agreementSM (the “Agreement”) with Jefferies LLC (the “Agent”) under which the Company may offer and sell, from time to time at its sole discretion, shares of its common stock, par value $0.01 per share (the “Common Stock”), having an aggregate offering price of up to $500.0 million through the Agent as its sales agent and/or principal (the “ATM Program”).

The Agent may sell the Common Stock by any method permitted by law deemed to be an “at the market offering” as defined in Rule 415(a)(4) of the Securities Act of 1933, as amended, including without limitation block transactions, sales made by means of ordinary brokers’ transactions on the New York Stock Exchange or sales made into any other existing trading market of the Common Stock, or in negotiated transactions with the consent of the Company. The Agent will use commercially reasonable efforts to sell the Common Stock from time to time, based upon instructions from the Company (including any price, time or size limits or other customary parameters or conditions the Company may impose). The Company will pay the Agent a commission of up to 3.0% of the gross sales proceeds of any Common Stock sold through the Agent under the Agreement, and also has provided the Agent with customary indemnification rights.

We already knew that; we also knew that in order to minimize the risk of lawsuits from buyers of stock who end up with a big, fat nothing – who will sue nonetheless – the company would have to make it clear that nothing short of a miracle will be needed for buyers to avoid a total loss, let alone make a profit. And sure enough in a risk factor geared exclusively to Robin Hood traders, “We are in the process of Chapter 11 reorganization cases under the Bankruptcy Code, which may cause our common stock to decrease in value, or may render our common stock worthless” the company warns that “any trading in our common stock during the pendency of our Chapter 11 Cases is highly speculative and poses substantial risks to purchasers of our common stock.”

In case that wasn’t enough, Hertz also said that “although we cannot predict how our common stock will be treated under a plan, we expect that common stock holders would not receive a recovery through any plan unless the holders of more senior claims and interests, such as secured and unsecured indebtedness (which is currently trading at a significant discount), are paid in full, which would require a significant and rapid and currently unanticipated improvement in business conditions to pre-COVID-19 or close to pre-COVID-19 levels” something which the company’s bondholders clearly do not expect as of this moment. In fact, after surging in the past weeks, HTZ bonds dipped modestly this morning, with prices on the company’s roughly $4 billion in unsecured bonds – which are all trading below 50 cents on the dollar – suggesting the equity “value” is worth negative $2 billion.

Finally, Hertz also made it clear that it expects “our stockholders’ equity to decrease as we use cash on hand to support our operations in bankruptcy. Consequently, there is a significant risk that the holders of our common stock will receive no recovery under the Chapter 11 Cases and that our common stock will be worthless.”

While retail buyers of HTZ stock are facing a virtually certain total loss, the big winners from the Jefferies led offering are, well, Jefferies which will collect a 3% commission, the lawyer who will make $200K on the deal, and of course the company’s creditors whose recoveries will be boosted by whatever amount Jefferies manages to sell.

Despite the repeat warnings, HTZ stock was last seen trading at $2.50, largely unchanged from Friday’s close after sliding as much as 25% in pre-market trading, even as Jefferies is likely already dumping millions of share At The Money as of this morning.

via ZeroHedge News https://ift.tt/2B6xCIX Tyler Durden

So what do we know with any sort of certainty about the claim that “the pandemic is over”? Very little.

Is the pandemic over in China, Europe, Japan and the U.S./Canada? Is the much-anticipated V-Shaped economic recovery already baked in, i.e. already gathering momentum? The consensus, as reflected by the stock market (soaring), the corporate media and governmental easings of restrictions seems to be “yes” to both questions.

But science is not a consensus-based activity, and so skeptics of consensus are looking to the sciences of epidemiology, virology, etc., and economics for evidence-based answers.

But as scientist and author Michael Crichton explains in this seminal paper he gave at Caltech in 2003, much of what is presented (“sold”) as “hard science” is nothing but guesswork / conjecture and consensus, i.e. reaching a politically appealing conclusion and then conjuring up some junk science to support the conclusion. Aliens Cause Global Warming (by Michael Crichton) (via Michael M.)

The scientific method is pretty straightforward: propose a testable hypothesis and then design an experiment that acts on only one variable: one group in which no action is taken and another in which one action is taken. If the action taken has a recordable effect, then that data must be replicated by other labs performing the same experiment to confirm that there weren’t errors in the protocol, equipment or data collection.

A variation of this protocol is a double-blind study, so-called double blind because neither the subjects/volunteers nor the researchers administering the experiment know which subjects received the active compound and which received a placebo.

In the case of natural systems such as the movements of planets, the method is to propose a model of Nature that can be reduced to mathematical predictions that can be confirmed by observations.

Unfortunately, it’s virtually impossible to run these sorts of experiments on a pandemic or economy. It would be unethical to let the virus run rampant in one city and then control the pandemic with lockdowns in another, or treat one group of patients with a worthless placebo while giving others a potentially life-saving treatment.

Even if such an experiment of two cities could be run, the great number of variables would reduce the certainty of any conclusions.

For example, the exact same variation of the virus would have to be unleashed in both cities, both cities would have to have very similar weather, air quality, ethnic groups, demographic profiles and so on. If any of these weren’t controlled, then they could skew the results, meaning any conclusion based on a single variable could be completely erroneous.

The same can be said of economics, which strictly speaking doesn’t qualify as science because despite its heavy use of arcane equations, it is essentially impossible to reduce an economic setting down to only one variable and then stage a controlled double-blind study.

Much of the “science” being presented about the Covid-19 pandemic and the economy are models, and Crichton subjects the claims and protocols of models to a scathing analysis. It turns out that measuring or even estimating the variables in complex models is impossible, meaning the models are nothing more than guesswork, which is highly susceptible to biases such as confirmation bias: this are the results we want, and by golly, these “estimates” yield the results we wanted.

We’ve already seen models rejected as hopelessly defective, studies of treatments (pro and con) hopelessly compromised, and in multiple ways: sloppy math, sloppy data collection, data that can’t be confirmed, and on and on.

As longtime readers will recall, I began covering the pandemic on January 24, 2020, the day after the Chinese government and WHO confirmed the Wuhan outbreak. I concluded the pandemic was consequential (based on the large-scale Chinese response and satellite imagery suggesting the number of deaths was an order of magnitude higher than what the Chinese officials claimed) and that it had already spread globally due to unrestricted air travel in and out of Wuhan and other cities in China.

If we step back and review the data pertaining to the question, is the pandemic over in the developed-world nations?, we find a mass of data of questionable value, for the basic reason that there are too many uncontrolled variables in every data set, too much guesswork in the models, and essentially zero experiments controlled for the number of variables and bias that meet rigorous standards for protocols and data collection.

Another Achilles Heel of the pandemic data is the small sample size of many of the studies. Since everyone is in a rush to reach actionable conclusions, many groups are working with small sample sizes–often just a few dozen people. Careful observations of small sample sizes–for example, the study I posted on the occupants of a single bus in China carrying one asymptomatic passenger, and carefully identifying who else on the bus caught the virus–can be useful, because the bus was in effect a controlled experiment with relatively few variables.

But as those of you who study Phase I and Phase II drug trial data know, small sample sizes, even in double-blind studies, are notoriously unreliable. A new drug may seem to have a measurable effect on a significant percentage of a control group of 35 subjects, but subsequent larger trials reveal that the effect was actually statistical noise.

So what do we know with any sort of certainty about the claim that “the pandemic is over”? Very little. And there are still important open questions about the effects of the Covid-19 virus on younger, healthy people: though the virus kills relatively few people under the age of 50, some significant percentage of younger, healthy people suffer long-term organ damage, possibly as a result of the blood clotting the virus appears to trigger in roughly 3% of younger, healthy people who come down with severe cases.

These people didn’t die, and so they drop off the statistical count everyone is following as the key statistic. But the after-effects of the disease are long-term and serious, and deserve careful study.

Let’s say the death rate is 0.25%, but the number of cases that lead to long-term organ damage and disability is 2.5% — ten times higher than the death rate. Are we focusing on the wrong data set? Do we know why the virus affects some younger, healthy people and not others? Are there treatments that minimize or reverse organ damage? These are still questions without science-based answers.

As for the study of economics and the V-shaped recovery: the Employment Report that triggered a 1,000 point rally in the Dow Jones Industrial Average is notoriously inaccurate, as it has all the core flaws described above:

1. An imprecise sample size

2. A defective model (the birth-death model of business formation)

3. No control for variables

4. Extreme vulnerability to bias: these reports often trumpet huge job increases which are subsequently “revised away” months later, completely ignored by the very stock markets that skyrocketed on the bogus headline number.

Do we have any real data on how much money at-risk groups (people over 60) will spend compared to their pre-pandemic consumption? No.

Do we have any reliable data that can be confirmed by independent researchers on the number of small businesses that are only opening to liquidate inventory before they close for good? No.

Every consequential question we have about the economy after restrictions ease cannot be answered with even the barest shred of scientifically reliable data. Everything the consensus and economists are claiming or projecting is nothing but guesswork.

In summary, we know very little about the pandemic’s future course or the economic consequences. If our leadership and media were actually concerned with scientific accuracy, the paucity of confirmed science would be the first fact everyone stipulated. Instead, we’re inundated with guesswork gussied up to mask the preferred narratives and biases of self-interested parties.

The cautious approach would be to maintain a skeptical circumspection about models, projections, conclusions, studies and narratives being promoted/”sold.” We can start a skeptical inquiry by asking: cui bono, to whose benefit?

Second, we can study the two key variables identified by Nassim Taleb: mobility and the interconnections of networks. The greater the mobility of the human populace and the greater the number of connections between groups, the greater the number of pathways for the virus to spread.

“Herd immunity” is being presented as the solution, but do we know with any certainty that the presence of antibodies confers strong immunity for years to all variations of Covid-19? It seems way too early to claim immunity is certain and long-lasting.

Once the general public understands there are still significant uncertainties, the lack of certainty may have economic consequences that will be difficult to measure or predict.

The other point is that now that the time for authoritarian lockdowns has passed, everyone needs reliable information to make their own assessment of risk as part of deciding what activities they will do or not do to further their own interests.

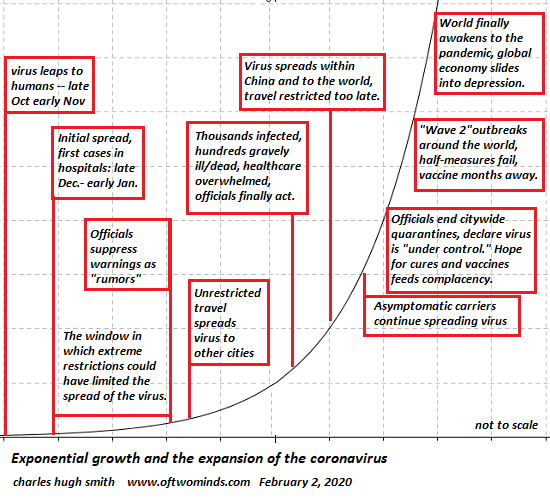

Here is my global projection from February 2, 10 days after the WHO officially confirmed the Wuhan outbreak. Four-and-a-half-months later, this projection is still playing out.

White Woman Filmed Setting Fire To Atlanta Wendy’s After Latest Police Killing Tyler Durden

Mon, 06/15/2020 – 09:40

Atlanta police are offering a $10,000 reward to anyone who offers information that could lead to the arrest of whoever set fire to the Wendy’s on University Avenue where Rayshard Brooks was shot and killed by a police officer Friday night after a brief struggle.

The department also released photos of a suspect believed to have started the fire…

Additionally, please see attached video/photos of the individual attempting to hide her identity. A video of the woman was posted on social media and can be viewed here: https://t.co/XCH14ydbO8

— Atlanta Police Department (@Atlanta_Police) June 14, 2020

…and although their face can’t be seen, rendering their identity a mystery, it was clear that the suspect identified by the APD is white.

Well, on Monday morning, the Daily Mail published some new cellphone footage of the suspect starting the fire. And although the suspect’s identity still isn’t clear in the video, another fact was made apparent: Not only was the suspect white, but it appears the person starting the fire is another angry white woman.

The fast-food outpost was torched late on Saturday during demonstrations that erupted over the death of Rayshard Brooks. In the video, peaceful protesters in the crowd can be heard criticizing the woman as she broke a window, sprayed a flammable substance on the ground, then set the building on fire.

The protesters insisted on the video, which was shared by the Daily Mail, that ‘Black Lives Matter’ demonstrators weren’t responsible for the looting and damage, and that the suspect seen in the footage was acting on her own.

“Look at the white girl trying to set s*** on fire…look at that white girl trying to burn down a Wendy’s,” the anonymous camera man can be heard saying.

“This wasn’t us,” he added, referring to BLM. “This wasn’t us!”.

As the fire grew, fears mounted that it could ignite a neighboring gas station, but by midnight the fire had burned out without spreading further.

via ZeroHedge News https://ift.tt/3huQ5zp Tyler Durden

Key Events This Week: Central Banks Try To Talk Up Stocks Tyler Durden

Mon, 06/15/2020 – 09:29

While markets will be paying very close attention to the resurgence in virus cases in China as well as the rising infections in the US to determine if the V-shaped recovery is over, there are quite a few other things to keep track of this week. As DB’s Jim Reid writes, central banks will feature highly on the agenda, with decisions from the Bank of Japan (tomorrow), the Bank of England (Thursday) and a number of others, while Fed Chair Powell will also be testifying before Congress (tomorrow and Wednesday).

European politics will also be in focus, with a European Council meeting taking place on Friday where the recovery fund will be discussed, as well as talks between Prime Minister Johnson and EU leaders on today about their future relationship. Meanwhile we’ll get an increasing number of hard data releases for May, offering further insight into how different economies have fared as various lockdown measures have been eased.

Starting with central banks while the BoJ (tomorrow) is likely to see no policy change, the Bank of England (Thursday) are expected by DB to ramp up QE by a further £125bn with more QE likely over the course of the year. Their decision comes against the backdrop of Friday’s data showing UK GDP contracting by -20.4% in April, following its -5.8% decline in March, and with the country still only slowly easing lockdown restrictions.

Another central bank highlight will be Fed Chair Powell’s appearances before the Senate Banking Committee tomorrow and the House Financial Services Committee on Wednesday. He’ll be delivering a testimony as part of the semiannual Monetary Policy Report that’s submitted to Congress. It’ll be interesting to hear what he has to say on the outlook and how he sees the recovery progressing given his remarks in the most recent press conference that “we’re not thinking about thinking about raising rates”. So close to last week’s FOMC there is unlikely to be much new news but his tone will be closely watched as many in the market have criticised his downbeat nature at last week’s press conference. Rightly or wrongly, markets like a bit of sparkle from their central bank leaders and didn’t feel they got enough last week. Finally, central banks elsewhere will also be making a number of decisions next week, including in Switzerland, Norway, Indonesia, Russia and Brazil.

At the end of the week, the European Council summit on Friday will be of particular importance, with EU leaders due to discuss the recovery fund to deal with covid-19, along with the EU’s new long-term budget. Last month, Commission President von der Leyen presented a proposal for a €750bn recovery fund, which would include a mixture of grants and loans to member states. As part of this, the Commission would borrow from markets on behalf of the EU. However, the plans would require unanimity among the member states, and there are differences of views between them, not least on the extent to which the fund should be balanced between grants and loans. However, talks on the issue are expected to keep going into July, when Germany will take over the rotating EU Presidency.

Staying on European politics, and Brexit will return to the headlines as a high-level meeting between UK Prime Minister Johnson and the Presidents of the European Commission, Council and Parliament takes place by video conference this afternoon. The two sides have now agreed to an intensified timetable for negotiations on a free-trade agreement, with talks in each of the 5 weeks from the week commencing 29 June to the week commencing 27 July. The question will be whether today’s high-level talks can provide fresh impetus for the negotiations.

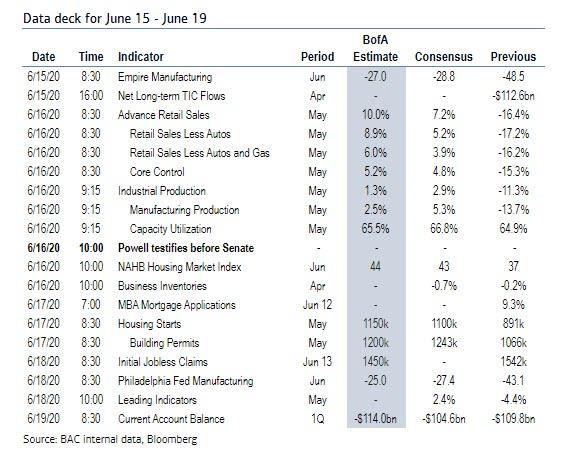

On the data front, it isn’t a particularly eventful week. The US will be releasing more hard data for May, with retail sales, industrial production and capacity utilisation figures coming out tomorrow, before housing starts and building permits for May are released on Wednesday. Our economists believe the trough of activity was in early May where their tracker showed YoY growth of -11%. It’s now around -9%. Moving across the Atlantic, here in the UK, this week sees inflation, retail sales and unemployment data released. For more on the rest of the week’s calendar see the day by day week ahead at the end.

Day-by-day calendar of events courtesy of Deutsche Bank

Monday

Data: China May industrial production, retail sales, Japan April tertiary industry index, Italy final May CPI, Euro Area April trade balance, Canada April manufacturing sales, May existing home sales, US June Empire State manufacturing survey, April foreign net transactions

Central Banks: Fed’s Kaplan and Daly speak

Politics: Meeting between UK Prime Minister Johnson and the Presidents of the European Commission, Council and Parliament.

Tuesday

Data: UK April unemployment rate, Germany final May CPI, June ZEW survey, Canada April international securities transactions, US May retail sales, industrial production, capacity utilisation, June NAHB housing market index

Central Banks: Bank of Japan monetary policy decision, Fed Chair Powell appears before Senate Banking Committee, Fed’s Clarida speaks, RBA release minutes of June policy meeting

Wednesday

Data: Japan May trade balance, UK May CPI, EU27 May new car registrations, Italy April industrial sales, industrial orders, Euro Area final May CPI, US weekly MBA mortgage applications, May housing starts, building permits, Canada May CPI

Central Banks: Brazil monetary policy decision, Fed Chair Powell appears before House Financial Services Committee, Fed’s Mester speaks

Thursday

Data: Italy April trade balance, Canada April wholesale trade sales, US June Philadelphia Fed business outlook, weekly initial jobless claims, May leading index

Central Banks: Monetary policy decisions from the Bank of England, Swiss National Bank, Norges Bank and Bank Indonesia, ECB publishes Economic Bulletin, Fed’s Mester speaks

Friday

Data: Japan May nationwide CPI, UK May retail sales, public sector net borrowing, Germany May PPI, Euro Area April current account balance, US Q1 current account balance, Canada April retail sales

Central Banks: Central Bank of Russia monetary policy decision, BoJ release minutes of April meeting, Fed’s Powell, Quarles, Mester and Rosengren speak

Politics: European Council meet via videoconference

Finally, here is Goldman focusing on the US, where the most important economic data releases next week are the retail sales and industrial production reports on Tuesday and the jobless claims report on Thursday. There are several scheduled speaking engagements by Fed officials this week, including Chair Powell’s congressional testimony on Tuesday and Wednesday.

Monday, June 15

10:00 AM Dallas Fed President Kaplan (FOMC voter) speaks: Dallas Fed President Robert Kaplan will take part in an online discussion hosted by the Money Marketeers at New York University.

12:30 PM San Francisco Fed President Daly (FOMC non-voter) speaks: San Francisco Fed President Mary Daly will take part in an online discussion on monetary policy hosted by the National Press Club. Prepared text is expected. Media and audience Q&A are expected.

Tuesday, June 16

08:30 AM Retail sales, May (GS 9.5%, consensus +8.0%, last -16.4%); Retail sales ex-auto, May (GS +7.5%, consensus +5.3%, last -17.2%); Retail sales ex-auto & gas, May (GS +7.5%, consensus +5.0%, last -16.2%); Core retail sales, May (GS +7.0%, consensus +5.8%, last -15.3%): We estimate that core retail sales (ex-autos, gasoline, and building materials) rebounded by 7.0% in May (mom sa), reflecting a partial reopening of the economy indicated by sharp gains in credit card spending and other high-frequency data. We believe the April and May reports received a boost from non-response among the hardest hit retailers, and we note scope for downward revisions as additional responses are received. In May, we expect even strong sequential gains in the higher level aggregates in this week’s report reflecting rebounding spending at restaurant and car dealerships. We expect a 9.5% increase in the headline measure and an 7.5% rise in ex-auto.

09:15 AM Industrial production, May (GS +4.5%, consensus +3.0%, last -11.2%); Manufacturing production, May (GS +6.5%, consensus +5.0%, last -13.7%); Capacity utilization, May (GS 67.5%, consensus 66.9%, last 64.9%): We estimate industrial production rose by 6.5% in May, reflecting a rebound in manufacturing output after last month’s plunge. We estimate capacity utilization rose by 2.6pp to 67.5%.

10:00 AM Fed Chair Powell appears before the Senate Banking Committee: Fed Chair Jerome Powell will deliver the semi-annual policy report before the Senate Banking Committee. Prepared text is expected.

04:00 PM Fed Vice Chair Clarida (FOMC voter) speaks: Fed Vice Chair Richard Clarida will give a speech on the outlook for the US economy and monetary policy at a Foreign Policy Association dinner. Prepared text is expected.

Wednesday, June 17

08:30 AM Housing starts, May (GS +25.0%, consensus +23.5%, last -30.2%); Building permits, May (consensus +17.3%, last -20.8%): We estimate housing starts rebounded by 25.0% in May following coronavirus-related declines in April and March.

12:00 PM Fed Chair Powell appears before the House Financial Services Committee: Fed Chair Jerome Powell will deliver the semi-annual policy report before the House Financial Services Committee. Prepared text is expected.

04:00 PM Cleveland Fed President Mester (FOMC voter) speaks: Cleveland Fed President Loretta Mester will take part in an online discussion hosted by the Council for Economic Education. Prepared text is expected. Audience Q&A is expected.

Thursday, June 18

08:30 AM Philadelphia Fed manufacturing index, June (GS -23.0, consensus -25.0, last -43.1): We estimate that the Philadelphia Fed manufacturing index increased by 20.1pt to -23.0 in June.

08:30 AM Initial jobless claims, week ended June 13 (GS 1,300k, consensus 1,290k, last 1,542k): Continuing jobless claims, week ended June 6 (consensus 19,650k, last 20,929k): We estimate initial jobless claims declined but remain elevated at 1,300k in the week ended June 13.

12:15 PM Cleveland Fed President Mester (FOMC voter) speaks: Cleveland Fed President Loretta Mester will take part in a virtual discussion hosted by the Global Interdependence Center. Audience Q&A is expected.

07:00 PM San Francisco Fed President Daly (FOMC non-voter) speaks: San Francisco Fed President Mary Daly will deliver a commencement address to the Preuss School at UC San Diego. Prepared text is expected.

Friday, June 19

10:15 AM Boston Fed President Eric Rosengren (FOMC non-voter) speaks: Boston Fed President Eric Rosengren will take part in a webinar on the US economy and current financial conditions hosted by the Greater Providence Chamber of Commerce. Prepared text is expected. Audience Q&A is expected.

12:00 PM Vice Chair for Supervision Quarles (FOMC voter) speaks: Federal Reserve Board Vice Chair for Supervision Randal Quarles will discuss stress testing at a Women in Housing and Finance Policy Event. Text is expected. Moderated Q&A is expected.

01:00 PM Fed Chair Powell (FOMC voter) and Cleveland Fed President Mester (FOMC voter) speak: Fed Chairman Jerome Powell and Cleveland Fed President Loretta Mester will speak via video on building a resilient workforce in the era of Covid at a Youngstown Community Event. Text is expected.

Source: DB, Goldman, BofA

via ZeroHedge News https://ift.tt/3e6KSM7 Tyler Durden

Rabobank: A “V For Vendetta” Recovery? Tyler Durden

Mon, 06/15/2020 – 09:11

Submitted by Michael Every of Rabobank

Recent market pricing has been based on expectations of V-shape patterns in key indicators; as such we can expect volatility as we get the wrong kind of Vs. Not a boarded-up Winston Churchill in London, but rather an upsurge in virus cases.

New infections are up in many parts of the US – mostly in states where reopening continues anyway. They are up in ‘ahead-of-the-virus-curve’ Israel – where a senior health official says a second wave is already underway…and yet weddings of up to 250 are now allowed. They are up in Iran and in Tokyo. Moreover, in China parts of Beijing are once again locked down after an outbreak at a major food market – blamed on foreign fish so far. In short, Covid-19 appears stubbornly persistent despite political claims of total or partial victory over it: and this is summer: imagine what winter might look like.

Regardless, efforts keep being made to get the economy moving again. In the UK, for example, the government appears ready to make the “2-metre distance” rule the 1-metre rule – just as the WHO report arguing the reduction in distance is safe is rubbished by other experts. As we keep repeating, voluntary lockdowns are not something one can control for, and the British public are shown to NOT be keen for 2 to become 1.

As an example of that China’s latest data releases have mostly disappointed. New home prices were up 0.5% m/m, as that epic bubble shows yet another mini-leg higher. However, in the actual economy we saw industrial production up only 4.4% y/y (vs. 5.0% expected, and despite steel and cement output climbing to a new record high); retail sales -2.8% y/y (vs. -2.3%); property investment -0.3% y/y (vs. -0.8%, the only ‘good news’ aside from unemployment dropping from 6% to 5.9%, which is not a series the market takes seriously); and fixed asset investment -6.3% y/y (vs. -6.0%). In short, even with a ‘build it and they will come’ attitude, and even with the virus “having been beaten”, it still looks like China’s Q2 GDP will be negative y/y.

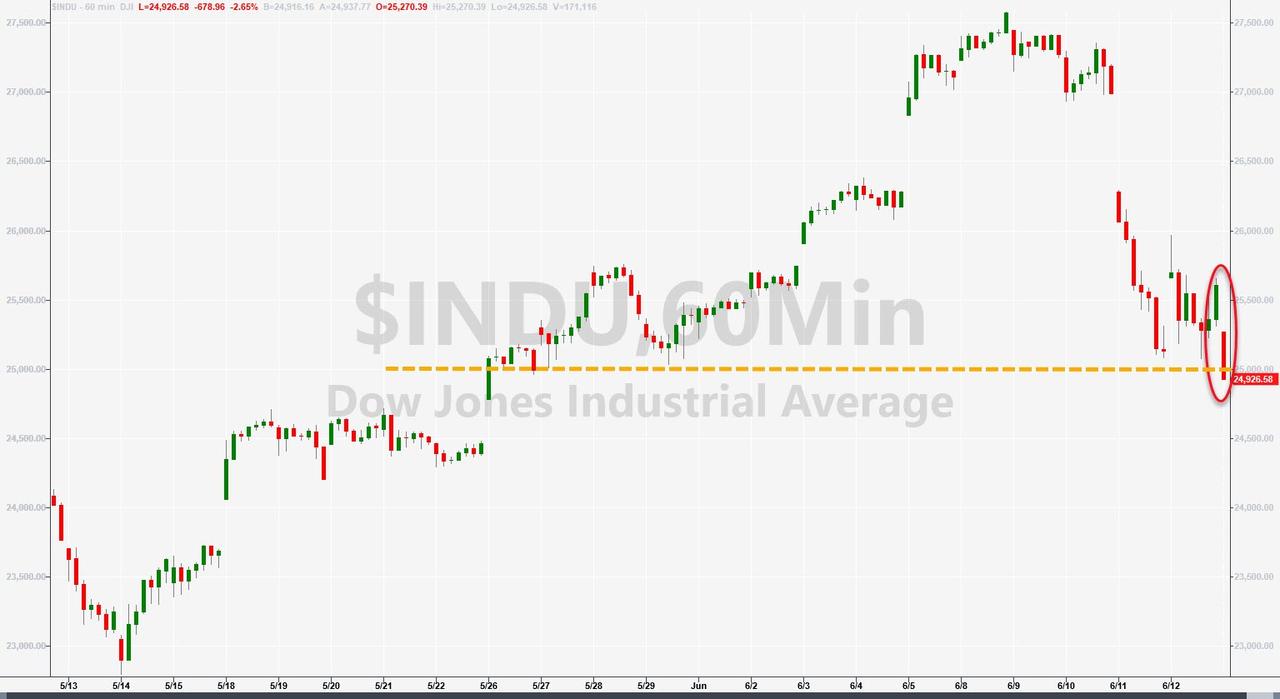

Don’t expect an economic V to follow either. Bloomberg is running a story titled “One-Third of US Job Losses Are at Risk of Becoming Permanent”. The Fed’s Powell already alluded to this, which helped prompt a market sell-off on Thursday that was immediately reversed by misplaced optimism on Friday. Yet imagine what high structural unemployment on top of our current unfair asset-rich, income-poor global paradigm is going to look like. Think we face a shrinking centre, declining middle-class, political polarisation, and populism now? Add millions of people whose jobs just disappeared with no cash cushion to see them through to retraining for work in a new, worse-paid sector about to be flooded with applicants. Do that and you have to imagine another ‘wrong kind of V’: the movie “V for Vendetta”. Unless you really think everyone is going to be sat at home day-trading; or that governments are going to keep up a WW2 level of spending for at least another 18 months. Either way it’s lower for longer forever on rates until we eventually reach the tipping point where inflation is V-shaped. Yet that’s a political story, and David vs Goliath for the moment.

That’s not to say slingshots are not being prepared. One needs to see the link between these kind of domestic problems and the international arena: as Klein and Pettis argue in their new book “Trade Wars are Class Wars”. In short, inequality at home and trade surpluses/deficits run internationally, and subsequent trade tensions, are always two sides of the same coin.

Is it pure coincidence then that the South China Morning Post reports “Beijing can expect more concerted efforts against it from the US, Australia, Britain, Canada and New Zealand”, as the Five Eyes group coalesces into a new coalition, which other recent actions show also involves India, Japan, Vietnam, and perhaps Indonesia. (A potential ‘Mahan’ grouping I have been flagging for some time.) Perhaps. But it’s ‘useful’ coincidence.

So is proposed US legislation targeting China on everything from trade to technology to capital. Moreover, Friday saw US Treasury Secretary Mnuchin reportedly float the possibility that looming US sanctions on Hong Kong could include USD usage too.Watch that space very closely. Meanwhile Graham Allison, the author of the recent retelling of the ‘Thucydides Trap’ where the US and China are Athens and Sparta, is now arguing in The National Interest that Huawei could potentially also prove a US-China casus belli.

EU foreign policy chief Josep Borrell this weekend reiterated that Europe will not pick a side and will work with both on areas of mutual interest. Really? Let’s see who replaces Germany’s Angela Merkel, who is pro-China in her (in)actions. Further, let Borrell digest the speech US President Trump gave at West Point over the weekend, where he stated: “It is not the duty of US troops to solve ancient conflicts in faraway lands that many people have never even heard of.” US politicians make increasingly-Churchillian statements about China, but that’s a line lifted from Chamberlain: the EU had better hope “many people” in the US still know where Europe is on a map! (On which note, Poland just invaded the Czech Republic in a “misunderstanding”.) Yes, the EU super-tanker turns slowly, but it may need to do so rapidly. As with the UK’s banning then unbanning of “The Germans” episode of ‘Fawlty Towers’, will it be a case of ‘Don’t mention the don’t mention the “Don’t mention the war”’?

None of this virus, economic data, or geopolitical backdrop is bullish EM, except perhaps for Mexico (which is bolted on to the US via the USCMA). Neither is it bullish risk. Instead, it still says long USD strategically, if not tactically, and long bonds, and long duration. Yet we cannot forget that central banks are determined to see ‘the right kind of V’ and will do whatever it takes to get one…even when it isn’t actually possible.

via ZeroHedge News https://ift.tt/2C3VTzz Tyler Durden

{kind=link}

{kind=link}