Mortgage Market Meltdown: Even The Wealthiest Loan Applicants Are Now Being Turned Down By Lenders

The global pandemic has mortgage lenders steering away from even their wealthiest clients, as fears are abound that lost income could turn the industry’s best clients into its biggest risks.

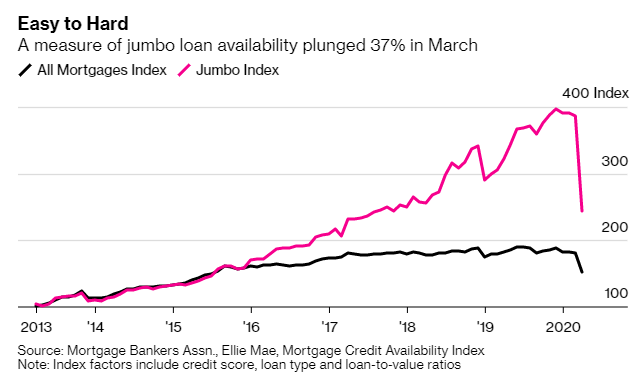

Jumbo loans, which got their name because they are bigger than most conventional mortgages, have completely fallen out of favor with lenders – a far cry from how they were looked upon just months ago, according to Bloomberg. Availability of jumbo mortgages is down 37% in March, more than double the overall home-loan market. They exceed the limit for government backed mortgages of $510,400.

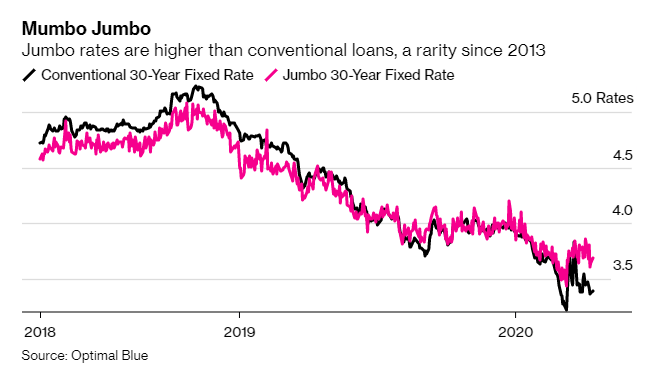

Rates for jumbo loans were 3.68% last week, which is almost 30 bps higher than the average conventional rate. The spread is the highest since 2013. Jumbo borrowers were previously seen as welcome clients, generally with great credit, money in the bank and collateral to put up.

Tendayi Kapfidze, chief economist at LendingTree Inc. said: “Before this crisis hit us, jumbo loans were pretty attractive. But because they don’t have the government guarantee, a lot of those loans end up on the bank balance sheet.”

Lenders are charging more for these types of loans than they have in almost seven years. At the same time, they’ve tightened lending standards, requiring almost pristine credit to get a mortgage.

People like David Adler are finding out that refinancing isn’t at easy at it seems, either. David, with excellent credit, went to lower his 3.7% rate on his home but his bank’s rates were too high to help. Adler said: “I told the guy at the bank, ‘I’m trying to use logic here,’ And he said, ‘That’s your problem.’”

Wells Fargo ranks among the highest jumbo loan holders, producing about $70 billion of the mortgages last year.

Over the last couple of weeks, the bank has stopped purchases from other mortgage banks and limited refinancings to customers who have $250,000 or more with the bank. Banks like Truist Financial Corp. and Flagstar Bancorp Inc. have taken similar steps.

Stanley Middleman, chief executive officer of Freedom Mortgage Corp. said: “Much of this pullback is because investors who’d normally buy these loans no longer want them. Whether the assets are good or not good is irrelevant because there’s no liquidity to buy them.”

And the banks may be on to something. It turns out that wealthier buyers look just as likely to stop paying their mortgages as and regular buyers. 5.5% of jumbo loans, about 131,000 borrowers, have asked to postpone payments due to a loss of income.

But the jumbo market hasn’t totally dried up – it’s just getting more difficult to close loans.

Damon Germanides, a broker in Beverly Hills, says you can fall short of qualifying “despite good credit and owning a business that’s doing well during the pandemic because it’s deemed ‘essential’.”

Borrowers that were ready to put up 20% may now need to put up 30%. “A month ago, he was a no-brainer. Now he’s 50-50,” Germanides concluded.

Passive investing has eaten active management’s lunch for decades. Its market share has grown steadily, capturing disproportionate amounts of inflows and allocation changes. Backed by scores of academic research, passive investing is pitched as a way to earn market returns with drastically lower fees. Why pay up for active managers if they can’t consistently beat the S&P 500? However, this secular phenomenon might have created an “easy game” from which the astute active manager can (finally) profit. Fallout from the coronavirus (COVID-19) response could give us a preview.

Easy Games

In many ways, professional investing is a unique industry. Manager performance is not only judged against peers with whom they directly compete, but with whom they directly transact. In fact, these interactions are the source of profit and loss. You just don’t see this in many other industries. True, Coke and Pepsi are fierce competitors, but their profits come from third parties (i.e. customers), not each other. Coke doesn’t buy or sell anything from or to Pepsi, and vice versa.

This dynamic—whereby profits come from other participants—likens it to poker. The analogy is quite useful sometimes. Other times, however, if can be harmful. Michael Mauboussin’s “easy game” analogy is a case of the former.

The value proposition of investment funds is providing superior returns. Superior returns to what? Well, other investment options. Said simply, gains are made by buying low and selling high. Thus, there must be another investor on each leg of the trade. Here’s where investing resembles a game of poker since generating relative (excess) returns are zero-sum. According to Mauboussin:

“Active managers must believe in differential skill to justify their existence. Recall the poker metaphor. You want to join the game only if you are more skilled than some of the other players and hence can expect to take their money. In markets as in poker, excess gains and losses net to zero. For you to win, someone has to lose on the other side of the trade.”

To win the most money in poker, it helps to be the best player at the table. Don’t be the pasty. According to Mauboussin, studies show that individual investors tend to lose to institutions. The latter are the card sharks feasting upon the retail patsies succumbing to a laundry list of behavioral biases. It’s an easy game for the professional to win.

One Door Shuts, Another One Opens

The proliferation of passive investing turned the investment management industry on its head. Investors (both retail and institutional) fired their expensive active managers (or themselves) in favor of cheaper passive investment vehicles. Thus, there are simply fewer traders now. As the number of participants shrink, so too does the pool of patsies. As a result, there’s less “alpha” available.

This creates an interesting dynamic. The investing skill level is significantly up. It’s no longer an “easy game”, at least compared to its prior form. But like all industries undergoing disruption, when one door shuts, another one opens.

What’s So Easy About Passive

While the competitive landscape of investing drastically shifted, the fundamentals have not. It’s still about buying low and selling high. However, the motives of buyers and sellers have changed. Ace still trumps jack irrespective of the players’ strategies. Perhaps a few adaptations can make active management an easy game again.

Passive investing vehicles are rigidly algorithmic, transparent, and simple. These attributes make them an easy game candidate. No matter how complex the strategy, each investment action reduces to: Did money come in? If so, then buy according to the published rule. Did money go out? If so, then sell according to the published rule.

Thus, you know exactly how each passive investment vehicle will transact in the presence of a capital flow—what it will buy and what it will sell given a set of conditions. There is zero mystery, which is actually part of their allure. This lack of discretion creates an opportunity to front-run passive investments if you can properly forecast their flows. Thus, this once touted advantage could become their greatest weakness.

The Demographic Shift

From what I can tell, no one has analyzed the market structures of passive investing more than Mike Green, a partner and the Chief Strategist at Logica Capital Advisers. Fortunately for us, Green has shared his findings in a number of public interviews (most notably here, here, and here).

Green believes that the regulatory framework incentivizes passive investing in retirement accounts. Thus, these vehicles benefited from decades of inflows, which in turn helped buoy prices. Remember: Cash in, then buy. Thus, the mere act of saving for retirement helped inflate investment values.

“The idea that passive players are passive players is just completely absurd. What they are is active players that have super, super simple rules and a massive regulatory advantage. … Passive is assuming that they’re not having any influence on that next price but they have to be because they are transacting.”

Mike Green, The Acquirers Podcast (Ep. 55)

However, this trend may now be reversing. Baby Boomers are the first generation to have defined contribution retirement accounts (401(k)s, IRAs, etc.). They are now at the age that legally mandates distributions—i.e. they have to sell. Thus, we are at the beginning of a demographic shift from buying passive investments to selling them! Remember the algorithm: Money out, then sell.

“The rule is constructed … that once you turn 70.5, you have to start taking distributions. The baby boomers are the first generation that had 401(k)s and IRAs as their primary mode of retirement vehicles. The generations that came before them had defined benefit plans. … The year they just turned 70.5 is 2017, the year after that is actually when they had to first start selling. That, in my estimation, is what happened in 2018, is that we saw large supply that occurred in the fourth quarter of 2018.”

Mike Green, The Acquirers Podcast (Ep. 55)

Faulty Foundations

However, it’s not just demographics that may plague passive investments. They are built upon several questionable assumptions. The most glaring one is that passive investments don’t impact market prices. By definition, every market participant does. Perhaps when passive investing was a negligible part of the markets this assumption held. However, the more AUM they garner, the more problematic this assumption.

Another theoretical fault is that investing is a closed system, like poker. This is plainly false. Capital routinely enters and leaves investment markets as individual cash needs wax and wane. Nor do passive investments approximate the entire universe of investment options, as required by theory. For example, an S&P 500 ETF only invests in the 500 stocks comprising the index—hardly a complete set of market assets.

Ergodicity is another dubious assumption presumed by the foundational theories of passive investing. An ergodic system is one where the future distribution of outcomes is known in advance since it’s the same as the historical one. Investing is anything but; past performance does not guaranty future results. We simply can’t know what the future will bring. This is another important way in which investing differs from poker and other games of chance.

A COVID-19 Catalyst

Green specifically identified demographics as a secular market structure trend supporting passive investing’s success. However, the recently imposed economic lockdowns related to the COVID-19 outbreak could give us a preview of his thesis.

As noted, passive investment strategies play central roles in defined contribution retirement plans. Thus, they are inextricably linked to employment. Workers can only participate if they have jobs. Retirements, layoffs, and furloughs may not only halt contributions, but could even catalyze withdrawals.

The recent spike in initial jobless claims are unlike anything experienced before.

Recently, new unemployment claims spiked to staggering levels due to COVID-19, the likes of which have never been seen. Over the past 3 weeks, initial jobless claims totaled nearly 19 million! More could come if the quarantines continue. Thus, capital inflows to retirement accounts may soon dry up and could even reverse. The recently passed CARES Act could exacerbate the latter since it relaxed penalties for early retirement account withdrawals. That said, layoffs have yet to hit those most with retirement accounts.

Playing Easy Games

Capital steadily flowed into passive investment vehicles for decades. This created a self-reflexive loop, whereby their inflows helped bid up their very own prices, boosting their relative performance (vis-à-vis active managers), which in turn attracted more assets, etc., etc., etc. Strong academic backing, fierce lobbying efforts, and low fee structures have universally embedded them in investment portfolios of institutions and individuals alike.

Green’s passive investment thesis is as unique as it is interesting. He’s one of the few outspoken critics of the passive investment industry and the faulty assumptions at its foundation (markets are complete, ergodic, and that passive investments do not influence market prices, to name a few). If he’s right, the secular capital flow-tailwinds into passive investment vehicles may soon reverse. The recent spike in unemployment may even provide a preview.

We already know how passive investment vehicles will transact in the presence of capital flows. If these become realistically forecastable, say due to legally mandated retirement distributions, or a cyclical surge in unemployment, then so too may the transactional behaviors of passive investments become. For the astute active manager, this kind of setup may have the makings of an easy game.

Ali Lumsden’s East Lodge Capital Plunges 26% In March As Mortgage Market Implodes

Ali Lumsden’s East Lodge Capital isn’t quite having the same success it did the last time the mortgage bond market melted down.

Lumsden, famous for gaining 73% when the mortgage bond market went belly up last time, saw 26% declines in March in its main hedge fund and a 16% in another of its funds, according to Bloomberg.

The fund specializes in securitized credit, which has suffered as the global economy has ground to a halt over the last 2 months. The good news for Lumsden is that East Lodge may have a tailwind in Central Bank policy, which is now apparently to bail out and backstop all bond markets, of all sizes, secured or unsecured.

Lumsden, who has worked in structured credit for 30 years, formerly averaged 28% annually while working at Michael Hintze’s CQS, an asset back securities fund, from 2006 to 2012.

In 2008, he made his score betting big against subprime mortgages and the banks that held them on their respective balance sheets. CQS, where Lumsden no longer works, was also down in March – to the tune of 40%.

East Lodge manages $1.9 billion and invests primarily in residential and commercial mortgage backed securities and collateralized loan obligations.

The mortgage market appears to be in complete shambles. We wrote just days ago that JP Morgan will be raising borrowing standards for most new home loans as the bank “moves to mitigate lending risk stemming from the novel coronavirus disruption.”

Days prior to that, we reported that JPMorgan had quietly halted all non-Paycheck Protection Program based loan issuances for the foreseeable future. We predicted the reason why JPMorgan would “temporarily suspend” all non-government backstopped loans such as PPP, is because the bank expects a default tsunami to hit, coupled with a full-blown depression that wipes out the value of assets pledged to collateralize the loans.

The First Amendment lawyer famous for Citizens United has taken up arms against a new foe: all-mail voting.

Jim Bopp, Jr. filed two lawsuits in federal court this week — one in Nevada and one in Virginia — to stop officials in those states from mailing out ballots to everyone on the voter rolls, not just those who request them.

“I don’t use the word ‘voters,’” he says, “I use the word ‘people on the registration rolls’ because many of them are ineligible to vote. They’re not voters. They’re people that are on the registration rolls that are ineligible to vote.”

As the COVID-19 pandemic gripped the nation, Democratic officials and activists began pushing states to switch to voting by mail, eliminating in-person voting altogether – and probably permanently.

But organizations that have spent years reviewing the voter rolls in many states estimate that more than 20 million of the names nationwide are duplicates, people who have moved away, are deceased, non-citizens or felons who have not had their voting rights restored.

“Democrats have been trying to register everybody in the country and then fight purging the rolls of ineligible people, and now they want to mail ballots to every single one of them,” says Bopp.

“It’s just like, talk about the most massive fraud scheme in the history of America. Makes Tammany Hall looks like a bunch of pikers, or the Pendergast Machine in Kansas City look like they didn’t even know how to steal elections.”

Earlier this month, Bopp filed a brief in New Mexico on behalf of the organization True the Vote and individual voters, whose votes could have been canceled out by the votes of ineligible voters if the court sided with plaintiffs — county clerks who wanted ballots mailed to everyone, not just those who’d requested them.

“What the parties request this court to do here is little else than pure anarchy that robs both the legislature and the eligible, registered voters of New Mexico of the authority and protections afforded each under the New Mexico [Constitution] and the United States Constitution,” the brief reads.

Bopp argued that the rights of voters were “imperiled” by the plaintiffs’ request and that the plaintiffs have attempted to “entice” the court to “utilize the national emergency created by the COVID-19 virus as a guise to usurp the constitutionally delegated authority of the legislature and overrule and replace current election laws with robust protections against voter fraud with a court-created scheme of mail-in balloting.”

The Supreme Court of New Mexico sided with Bopp and denied the request for ballots to be sent to all names on the rolls.

But now the push is on for all-mail voting in the November presidential election, as well. About a half dozen state have already legalized it.

“They are bringing suits all over the country to impose it through court orders,” says Bopp.

“All-mail. Their ideal is all-mail.”

All-mail voting is not the same as absentee voting as voting absentee involves the voter requesting an absentee ballot, usually by mail, with a signature.

Some states have more stringent requirements than others. In Kansas, for example, people requesting an absentee ballot are required to send a copy of a driver’s license or State ID with the application for an absentee ballot.

“Part of the problem with this discussion is, we are familiar with absentee ballots, and that does involve quote mailing a ballot, end of quote,” says Bopp, “but there are numerous safeguards, the most important of which is the prior application. You have to apply.

“You have an audit trail, and all sorts of things. And that’s why a lot of these Democrats and liberal activists don’t like absentee ballot,” he says.

“They want wholesale mailing out without application because it eliminates half the fraud protection.”

Science Teachers Adapt To Lockdown With ‘Burping Bags’ And Other At-Home Experiments

With most schools out across the country due to the coronavirus lockdown, science teachers have been getting creative when it comes to finding experiments to keeep their students entertained.

“My thing has been to get science into their homes and get them doing science… it’s about discovery,” said Lockhart, Texas science teacher Avri DiPietro, who’s assigned a “burping bag” experiment to her 160 or so students between the ages of 11 and 14.

The assignment calls for her sixth graders to combine vinegar and baking soda in a plastic bag, either in their kitchens or backyards. If all goes as planned, burps and belches will ring out across the small southeastern Texas town where DiPietro teaches, as the acidic vinegar meets the sodium bicarbonate, releasing gas from the bag. –Reuters

“This is pushing a lot of us educators in how to reach our kids,” said DiPietro.

As Reuters notes, teachers across the country have been scrambling to develop lesson plans with just a few days notice following a national lockdown to keep COVID-19 from spreading (a strategy which has come under increasing scrutiny). The challenge, of course, is keeping children from becoming distracted and tuning out.

DiPietro says that assigning hands-on experiments is a great way for students to stay engaged without access to the school laboratory.

Teachers will typically post lists of the ingredients needed for the experiment, detailed instructions, and possible observations and outcomes in their virtual classrooms. Then students spring into action, raiding their home’s pantries and cabinets for materials before turning their back porches and kitchens into makeshift science labs. –Reuters

“It really makes parents understand what teachers go through on a day-to-day basis… they have to find innovative ways to keep our kids busy,” said parent Heather Simpson, whose son Houstin is one of DiPetro’s students. Houstin made a “homemade lava lamp” using water, food coloring, salt, oil and a jar.

Meanwhile, second graders at Park Elementary School in Fairmount – a rural town in northeast Indiana, conducted a “walking water” experiment using strips of paper towels, food coloring, water and cups. Which we’re sure their parents had fun cleaning up.

“I understand now!” said one student in a video posted to Twitter, after successfully demonstrating “capillary action” – which allows liquid to flow upward in narrow spaces.

His teacher, Rebecca Freel, is happy watching her students make progress.

“It entertains me to watch their videos and seeing their pictures,” she said, adding “They are learning more from doing this than if I just gave them a paper to do or a website to go on. They really have to dive in and think.”

That said, it’s not always easy thinking of experiments for students when they don’t have access to online learning, or don’t have the necessary ingredients and materials for experiments. Because of this, most of the assignments are simple, and many are optional or for extra credit.

Glendora, California science teacher Libby Birmingham has been holding a virtual classroom from her front porch since her school closed on March 13 – conducting experiments such as the “cloud in a jar” – which uses shaving cream, water and food coloring to show precipitation.

“I’m trying to get them to be inquisitive and asking questions,” said Birmingham.

In another experiment known as “dancing raisins,” Birmingham showed how carbon dioxide affects the volume of fruit when it’s submerged in a carbonated liquid.

“They are fizzing… whoa… they have fizz bubbles on them. Cool,” exclaimed one of her students.

Stocks Tumble, Gilead Crashes After FT Reports Gilead’s Remdesivir “Flops” In First Clinical Trial

Just as we suspected, the sketchy Statnews report claiming that Gilead’s remdesivir had achieved miraculous results on patients in a small preliminary University of Chicago study has been exposed as complete BS.

The FT just reported that Gilead’s “miracle drug” remdesivir has flopped in during its first clinical trial

FT SCOOP: Gilead’s potential coronavirus candidate remdesivir has flopped in its first randomised clinical trial, according to draft documents published accidentally by the World Health Organisation and seen by the Financial Times. With @hannahkuchlerhttps://t.co/oGVnfZJox6

Stocks are sliding on news that the “miracle drug” is anything but…

….and Gilead shares – which soared nearly 20% on the original Statnews report – are taking it especially hard.

As @RANsquawk pointed out, the fact that the market puked so hard on this report after a few days of relatively boring action is extremely telling…

Reaction to the $GILD news is also quite telling in terms of market focus. Boring trade for days, then it is suggested that a treatment has flopped and the market pukes.

Three key catalysts for equities:

1) Vaccine/treatment/testing

2) When economies reopen

3) Shape of recovery

Of course, none of this should be a surprise to all the traders who actually read Gilead’s rebuttal of the Statnews report. Because when a drug company pours cold water on a report that one of the company’s own drugs might be a “miracle cure” for the worst pandemic in a century, you should know it’s serious.

Some even speculated that the original Statnews report could have been a setup by a handful of hedge fund managers hoping to profit off their Gilead positions.

The FT managed to get the “scoop” when the WHO accidentally published draft documents pertaining to the study.

Now will the mainstream media reporters who slammed Trump following reports that a VA study of hydroxychloroquine suggested it was ineffective?

Someday when the story of this scam is written, I hope it is clear who should be ashamed of themselves for slagging anyone calling for caution: Anti-malarial drug Trump touted is linked to higher rates of death in VA coronavirus patients, study says https://t.co/EKJoGtaRXm

Last week we learned about a badly timed decision that cost the California Public Employees’ Retirement System (CalPERS) more than $1 billion. CalPERS exited one of its two hedges just before the stock market began its unprecedented selloff. As bad as that sounds, it appears CalPERS has been outdone by the Alberta Investment Management Corporation (AIMCo). AIMCo, which manages nearly $125 billion for pension funds, sovereign wealth funds and other public accounts, lost $3 billion trading volatility.

AIMCo has since pulled the plug on its volatility-trading program after being on the wrong side of the volatility trade when markets crashed earlier this year. Sources say another complex strategy— the derivative-based “portable alpha” overlays, may have exacerbated AIMCo’s losses.

Public data on the now-defunct volatility-trading program at AIMCo is sparse. According to the LinkedIn profile of David Triska, he developed and oversaw “three equity volatility strategies across global developed and emerging markets” at AIMCo.

“The level of volatility that markets experienced in March 2020, the result of the Covid-19 pandemic, during which volatility rose faster, and on a more sustained basis that at any other time in history, is exceptional,” AIMCo communications director Dénes Németh told Institutional Investor. “AIMCo acknowledges that it is not immune to the challenges, unique as they may be, that institutional investors around the world have experienced.”

The losses on the volatility-trading program come at a particularly bad time for AIMCo. AIMCo is slated to fold-in about $13 billion in assets from the Alberta Teachers’ Retirement Fund. The Alberta Finance Minister’s office did not answer whether the fold-in will still occur as scheduled or be delayed as a result of AIMCo’s recent losses.

“The transition of ATRF’s assets has not yet occurred and AIMCo operates with full operational and investment independence from the Government of Alberta,” a spokesperson for the provincial Treasury Board and Finance told Institutional Investor. “AIMCo has a long track record of outperforming market benchmarks and providing great value to Albertans. We are facing unprecedented times and these are challenging market conditions for all investors. We are confident AIMCo will continue to meet the long-term investment objectives of their clients.”

One source who frequently trades with large institutional investors best summed up AIMCo’s trade gone awry, telling Institutional Investor “It’s not very hard to lose $3 billion selling volatility, you’re doing stuff that has a minus-infinity potential outcome.”

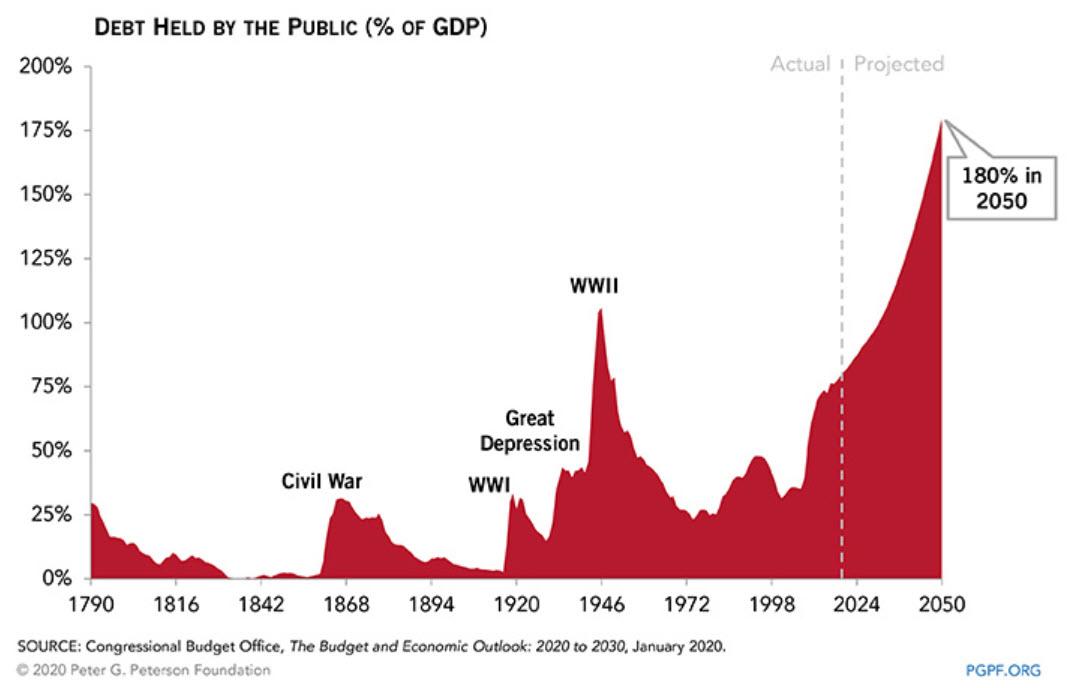

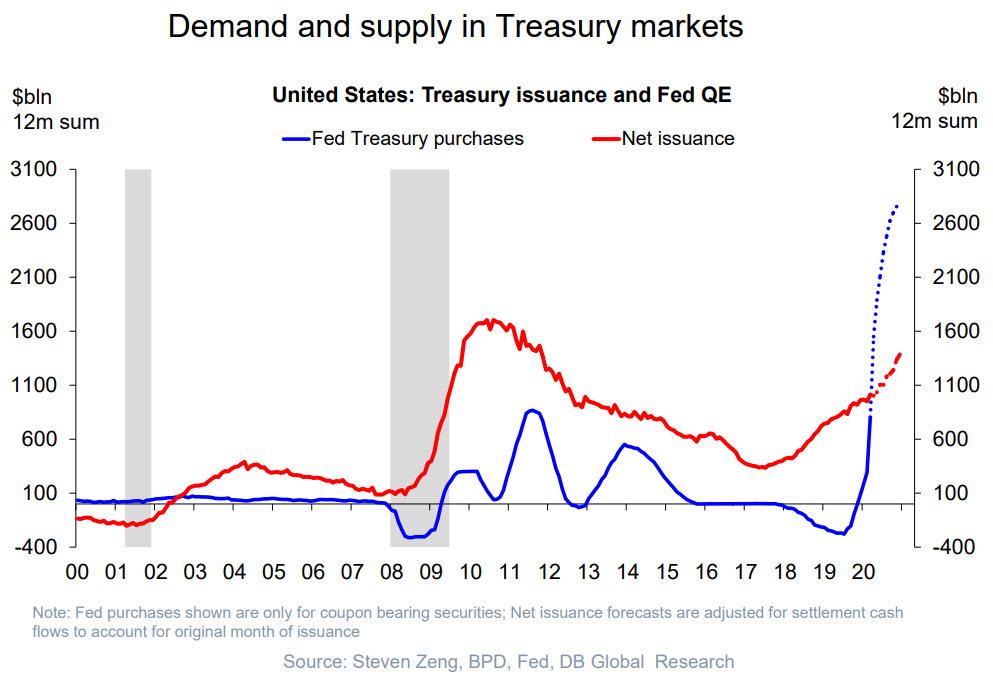

Lloyd Blankfein Can’t Understand Why Investors Are Still Buying US Treasurys; Here Is The Answer

Former Goldman Sachs CEO Lloyd Blankfein kicked the hornets’ nest at the nexus of modern finance and socio-economics – where topics such as MMT, Helicopter Money and debt monetization all intersect and keep the US empire funded – by tweeting a question that has stumped many others, to wit:

In finance, most surprising to me is that despite the trillions the US is adding to our budget deficit and national debt, investors (many foreign) will lend the US a virtually limitless supply of dlrs for .6 pct for 10 years.

In finance, most surprising to me is that despite the trillions the US is adding to our budget deficit and national debt, investors (many foreign) will lend the US a virtually limitless supply of dlrs for .6 pct for 10 years.

The answer is that what investors– plural – do, is irrelevant. All that matters is what one specific investor – the Fed – is doing and will continue to do.

As we have explained every single year since 2009, the reason why it is not at all surprising that Treasury yields are at 0.6% even as the US Treasury is expected to sell well over $3 trillion in debt this year, next year and likely every other year until the Treasury still exists…

… is because the yield on the US debt does not reflect market supply and demand – and hasn’t reflected the market for a decade – but merely the Fed’s constant intervention, and recently, take over of the bond market.

And here is the answer: as shown in the chart below, while the Treasury has issued a near record $1.5 trillion in net Treasurys in the past 12 months, over the same period, and really just in the past month, the Fed will monetize $3 trillion in debt, or – for the first time ever – the Fed will monetize double the total treasury issuance, an unprecedented development designed to achieve just one thing: avoid a selling cascade in Treasurys the kind we observed in mid-March.

And here is DB’s Torsten Slok verbalizing the threat presented by the chart above:

At the peak in late March, the Fed was buying $75bn in Treasuries every day, and we are now down to “only” $30bn per day, see also here. These enormous Fed purchases combined with rates moving sideways in recent weeks make you wonder where 10-year rates would have been if the Fed had not intervened. As the Fed gradually steps away over the coming weeks, and Treasury issuance continues to increase to finance the fiscal stimulus, the market will be focusing more and more on demand and supply in the US Treasury market.

Incidentally, Blankfein’s question is disingenuous to the point of farce for one simple reason: he knows the answer very well, after all it was under the watch of former Goldmanites Hank Paulson and Bill Dudley that the Fed unleashed QE, allowing the terminal disconnect between Treasury supply/demand dynamics and what the yield on the 10Y Treasury is.

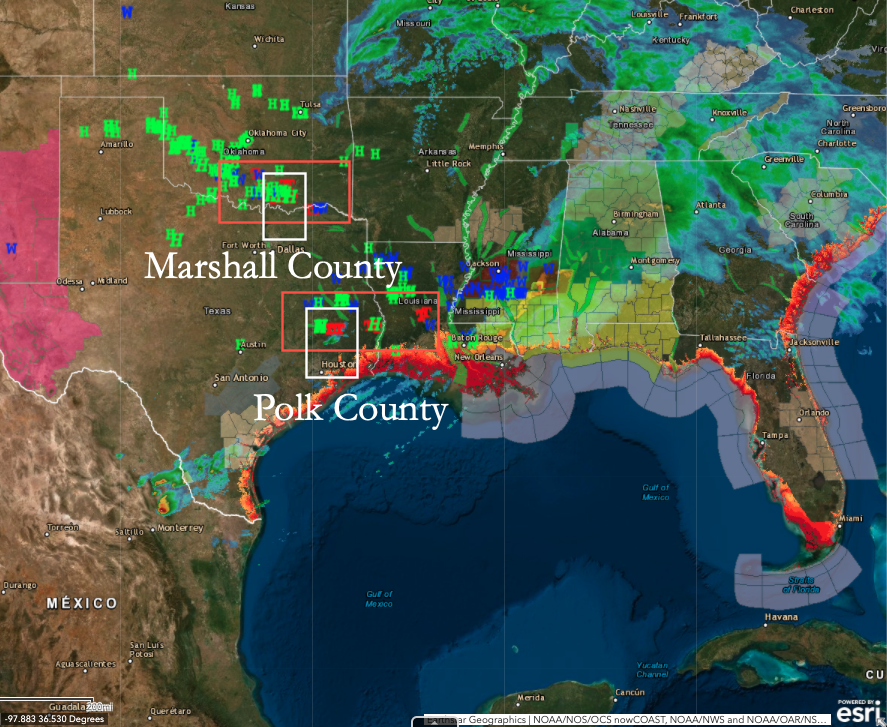

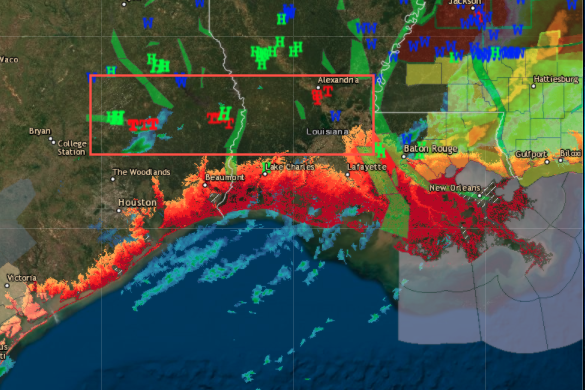

In Polk County, Texas, three people died and dozens were injured. A Polk County judge issued a national disaster declaration on Wednesday night due to “significant threats to life, health, and property.”

A late afternoon long-track large #Tornado caused massive damage in Onalaska, Polk County, TX. This damage is along the Trinity River just off Highway 356. There were some injuries here. #severeweather@NWSHoustonpic.twitter.com/6y2rIhsspN

Charles Stephens, a resident who witnessed the tornado, told the Houston Chronicle that he found his neighborhood dead in the water and several other neighbors severely injured.

“It’s a lot of devastation,” Stephens said. “I don’t think anybody is going to be able to get (into the neighborhood).”

Stephens said once the tornado cleared, it took him and his wife nearly 45 mins to climb out of the house.

“It took me 45 minutes to climb through the roof to get out,” he said, adding he was forced to use a hatchet to get his wife out of the debris.

Texas Governor Greg Abbott issued a statement that read:

“My office, the Texas Division of Emergency Management, and other state agencies are working with local officials to provide immediate support to the areas devastated by this tornado,” Abbott said. “The state has already deployed response teams and medical resources to help Texans in need and to provide assistance to these communities. Our hearts are with our fellow Texans tonight and the state will continue to do everything it can to support those affected by this severe weather.”

There were reports of tornados in Jasper, Texas, near the Louisiana border.

By 2230 ET Wednesday reports indicated that at least 21 tornados tore through Texas and Oklahoma.

In the early 1530s, a Spanish conquistador named Diego de Ordaz was exploring modern-day Venezuela when he first heard rumors of a nearby City of Gold.

Ordaz thought he was about to hit the jackpot. And he wasted no time ordering expeditions of the area to find this city– what eventually became known as El Dorado.

The mission failed, and most of Ordaz’s men died. But one survivor, a crewman named Juan Martinez, claimed that he had been captured and held prisoner for 10 years in El Dorado.

Martinez told sensational tales about the city’s golden structures adorned with precious stones, and even said that the local king bathed in gold dust every morning.

Martinez also said that the people of El Dorado were all so rich with gold that no one really had to work. They had constant festivals and would often feast for seven days straight.

Europeans were instantly hooked. And more expeditions were immediately launched.

The conquistador Gonzalo Pizarro (half brother to Francisco Pizarro) was so fanatical about El Dorado’s existence that he marched thousands of people through the jungles of South America for eighteen months looking for the city.

Pizarro came up empty-handed, and most of his men died.

And yet there were still countless expeditions launched over the next several decades in search of the lost City of Gold.

Everyone desperately wanted to believe in this fairy tale– that there was a place overflowing with money where everyone could live for free and spend their lives feasting and drinking.

Maybe this desire is hard coded in our DNA because there still seem to be people who believe in it.

Today’s version of El Dorado is the printing press. Politicians seem to have a fanatical belief that they can conjure paper money out of thin air and pay for everything.

For instance, #RentStrike2020 is a nationwide movement in the Land of the Free to simply cancel rent.

People want months of rent and mortgage payments to be forgiven. Poof, disappeared.

And the Bolsheviks have answered their call.

Congress is now considering the Rent and Mortgage Cancellation Act which would cancel all rent and mortgage payments for the duration of the pandemic, and possibly beyond for up to a year.

And the law would be retroactive, so they’d go back in time to March 13 to cancel rent.

The government would then set up a fund for landlords and mortgage holders “allowing them to recoup their losses, so long as they agree to abide by a set of fair renting and lending practices for a period of five years.”

Some of those conditions include not raising the rent for five years, and not denying renters based on credit history, or criminal record.

This is insane. First the government will tell landlords that the contracts they signed are void. And then, if someone wants to rent your property who has a history of not paying rent, you’re not allowed to reject them.

But as long as you bend the knee to DC, they’ll print the money to pay you.

Another bill proposes to pay $2,000 per month, for the next year, to every American over the age of 16 who makes less than $130,000 per year.

This includes high school students, and people who were previously not working.

Naturally the bill doesn’t mention costs. Why bother with such a trivial detail?

But based on the number of people who qualify, the cost could easily top $4 trillion.

That’s more than the entire federal tax revenue last year! They would literally spend every penny they collected in taxes last year just for that one program.

But no one really cares anymore. There are no rules, and both the government and central bank have decided they’ll do whatever it takes during this pandemic.

What’s really remarkable is that they seem to believe all this deficit spending and money printing will produce favorable results.

If you could simply print money to become a prosperous nation, then Zimbabwe would be the wealthiest country in the world.

But that’s not how it works. Creating more money is not the same as creating value.

Value creation is difficult. It requires talented people to work hard work and produce; it cannot be conjured out of thin air by a bureaucrat.

Right now the economy is shrinking. Millions of people have lost their jobs, which means there’s a whole lot less value being created.

Yet simultaneously they’re printing more money than ever.

You don’t have to have a PhD in economics to understand the mismatch here.

But then again, politicians aren’t exactly known for their grasp of finance.

For example– Queen Bolshevik, Alexandria Ocasio-Cortez, gleefully celebrated oil’s MINUS $40 price earlier this week, and predicted that the crash would prompt people to switch over to renewable energy sources.

What is this person thinking?? Ultra-cheap oil will compel people to use MORE oil, not less. Duh.

If anything she should hope for a $150 oil price and record high profits for oil companies. Renewable energy would be MUCH cheaper at that point, and people would have a big incentive to switch.

AOC clearly has no understanding of finance or economics… which is ironic because she’s one of the biggest fanatics of the printing press myth.

No one has to work. No one has to pay their rent. They government is just going to print money and send everyone a check every month.

It took nearly 500 years, but America has finally found the lost city of El Dorado. It’s called the Federal Reserve.

And just like El Dorado, its wealth is entirely mythical.