S&P Downgrades Ford To Junk – Biggest Fallen Angel Yet

Given where Ford’s CDS was trading – more in line with B1/BB- rated American Axle – it should hardly come as a surprise that S&P has finally bitten the bullet and downgraded Ford debt to junk.

Via S&P,

The decision to downgrade Ford Motor Co. from investment grade to speculative grade reflects that the company’s credit metrics and competitive position became borderline for the investment-grade rating prior to the coronavirus outbreak, and the expected downturn in light-vehicle demand made it unlikely that Ford would maintain the required metrics.

Ford Motor Co. announced it is suspending production at its manufacturing sites in Europe for four weeks and halting production in North America to clean these facilities and boost containment efforts for the COVID-19 coronavirus. We expect Ford’s EBITDA margin to remain below 6% on a sustained basis and believe that its free operating cash flow to debt is unlikely to exceed 15% on a consistent basis.

Ford has drawn $13.4 billion on its corporate credit facility and $2 billion on its supplemental credit facility. We believe the company’s current cash position stands at about $36 billion.

We are downgrading our long-term issuer credit rating to ‘BB+’ from ‘BBB-‘. At the same time, we are assigning issue-level ratings of ‘BB+’ on Ford’s unsecured debt.

We are also placing the ratings on CreditWatch with negative implications, which reflects at least a 50% chance that we could lower the ratings depending on factors such as the duration of the plant shutdowns, the rate of cash burn, and the adequacy of Ford’s liquidity position.

This S&P move follows Moody’s cutting Ford’s long-term corporate family rating to Ba2 from Ba1 earlier in the day.

With a total amount of public bonds & loans outstanding around $95.8 billion, according to data compiled by Bloomberg, Ford has just become one of the largest fallen angels yet.

Will this sudden large fallen angel lead to further repricing in the junk bond market, just as the market is dead-cat-bouncing on Fed intervention?

You could go out for groceries and prescription drugs and dog walking. You could go out if you performed an “essential service.” You could go out for a walk or a run or a bike ride so long as you kept 6 feet between you and other human beings. Instantly many more people than usual in Berkeley took to the streets and, instantly, you could see that no one was quite sure how to behave. No one had ever tried to estimate 6 feet every time they passed another person, and people had different ideas of how much it was. Basically everyone avoided eye contact and small talk — as if any human interaction, no matter how remote, might cause a coronavirus infection.

If you ranked all American towns and cities by the likelihood that passing strangers would acknowledge each other’s existence, Berkeley would fall some place in the middle. Ahead of New York City, behind any place in Mississippi. (New Orleans would rank first.)

The first day of the lockdown, people on the streets of Berkeley became New Yorkers. But it felt less like indifference than some combination of guilt and uncertainty. Here was a new social situation for which the etiquette manual had yet to be written.

By the second day, behavior on our streets changed, radically. People kept their physical distance but now made more of an effort with each other than I’d ever seen here. Everywhere you turned you saw total strangers not only saying hello but also stopping to chat. All of a sudden we all had something in common! (Aside from our left-wing views.) We were all in lockdown! And we were all outside! The streets of Berkeley for a moment felt almost like the streets of New Orleans.

Within a few days the novelty mostly wore off, and people went back to treating each other with the same old indifference. Except the old people. The old people are still making eye contact.

There’d been only a couple of reported Covid-19 cases in town, both contracted someplace else. So far as anyone could tell, no one in Berkeley had caught the virus from someone else in Berkeley. And so we’re still waiting, for an answer to a question. Italy or Germany: Which will we be? Italy has only twice as many cases as Germany but almost 50 times the deaths. Maybe the Italians are especially old or vulnerable, but it’s more likely the Germans have tested huge numbers of people and the Italians have tested only people with serious symptoms. That is, some vast number of Italians have had the virus but were never tested, either because their symptoms never sent them running to the hospital or they never even knew they had it. We in the U.S. have tested far fewer people than the Italians. We’ve tested fewer people than basically every advanced country — which raises another question? Are we still one?

The nation that led the data revolution, that invented the job title of “data scientist,” that has held up better data analysis as the key to smartening up everything from political campaigns to baseball teams is now, at its moment of greatest peril, without data.

This is a problem.

If you don’t know who has the virus, you can’t see where it is and where it isn’t. If you can’t see where it is, you don’t know how to fight it, except by shutting everything down and telling people to stay away from each other. On the one hand, there are probably a lot of data geeks here who don’t mind being told they can’t go out; on the other, it’s a little odd that the corner of California that gave birth to the data geek was the first in the country to be told it had to take extreme measures to prevent people from killing each other — because there is no data.

* * * * *

It seemed like a good time to call Bill James. James is in some ways the father of the data revolution – or at least the idea that people who have good data, and know how to use it, have a huge advantage over people who don’t. In the early 1970s, he began to marshal data about baseball players, and to argue that Major League Baseball teams didn’t understand the value of their own players, or the wisdom of their strategies. His ideas reached the Oakland A’s, who used them to win lots more games than they should have, given how little money they had to spend on baseball players. I wound up writing a book about this, called “Moneyball,” and James wound up being hired by the Boston Red Sox – who in short order won their first World Series in nearly a century. Now James’s idea has infected every corner of American life, except, oddly, the corner in which this virus is meant to be fought. A kind way to view President Donald Trump’s administration is to think of it as being run about as well as the 1970 Cleveland Indians.

It’s interesting how people are spending the pandemic. James, 70, is staying more or less locked inside his home in Lawrence, Kansas.

“There’s nobody on the streets here,” he said.

“Nobody. The only time I go out is to walk the dog in the morning.”

He’d recently left his job with the Red Sox but thought he might join another team. The virus put a hold on that ambition. Instead he’s using the time he now has on his hands to rethink how to measure the value of a baseball player’s defense, as he thinks the baseball establishment has it wrong. Former Atlanta Braves outfielder Andruw Jones is on the ballot for the Hall of Fame and that fact alone troubles James. Jones was more famous for his defense than James thinks he should have been, because the data on baseball defense, and the ability to analyze it, is inadequate. James is busy building a new metric that will reveal more truth. Thus one consequence of the pandemic is to make it a bit more difficult for Andruw Jones to enter the Hall of Fame.

I asked James a question I’ve been asking lots of people: What are the three things that he’s saddest to have lost?

“The NCAA tournament,” he said, without missing a beat.

“My Jayhawks were the consensus No. 1 team.”

After that he mourned the delay to the start of the baseball season. “That’s going to tear a huge hole in my daily life.”

He rattled off the years that MLB’s season was shortened, by war or strike: 1918, 1919, 1972, 1981, 1994, 1995. A few days earlier he’d put a poll up on Twitter, asking people to predict this year’s Opening Day. He had his own prediction: May 15. More than a thousand people took his poll. All but one thought he was being wildly optimistic.

James has no privileged information about the virus. He reads the news like everyone else.

“It’s hard to distinguish between what is being said responsibly and what’s just being said,” he told me.

But he also has a history of looking at data and deciding to think one thing, even when everyone else is thinking another, and being proved right.

“I have four reasons for thinking what I think,” he said.

First, warm weather might deaden the virus’s spread.

Second, the global medical research community might prove surprisingly resourceful.

“I believe we will find medicine that will combat this more quickly than most people seem to believe,” he said.

“I think most people have the sense not to pay attention to the rules that don’t make sense to pay attention to, and so doctors will be doing more freelancing and we’re going to start hearing people say, ‘I’ve got a medicine that works.’”

Third, he thought that the country with the best testing data had the most accurate view of the disease. And that it was possible that a huge number of Americans have it now, or have had it, without really knowing it.

“If 30% of the population has already been exposed to this then that number will go to 70% in two weeks,” James said.

Assuming that having the disease left you with immunity to it, the crisis would then be as good as over, and baseball could begin.

“What’s the fourth reason to your argument?” I asked.

“Yes,” he said. “There’s another reason, but being an old person I can’t remember what it was.”

“What’s the third thing you are saddest about having lost?” I asked.

“I had a goal of going to lunch with a friend 100 times this year. That’s not going to happen.”

I said goodbye to Bill James and checked our local news site. Berkeleyside, it is called, and it is suddenly the go-to place for the news that matters most. An hour earlier, the site reported, an 80-year-old Berkeley man had tested positive for the virus. His girlfriend (!) said that the man hadn’t gone anywhere for a long time. But he had, a few days earlier, shopped for his groceries at our local Safeway.

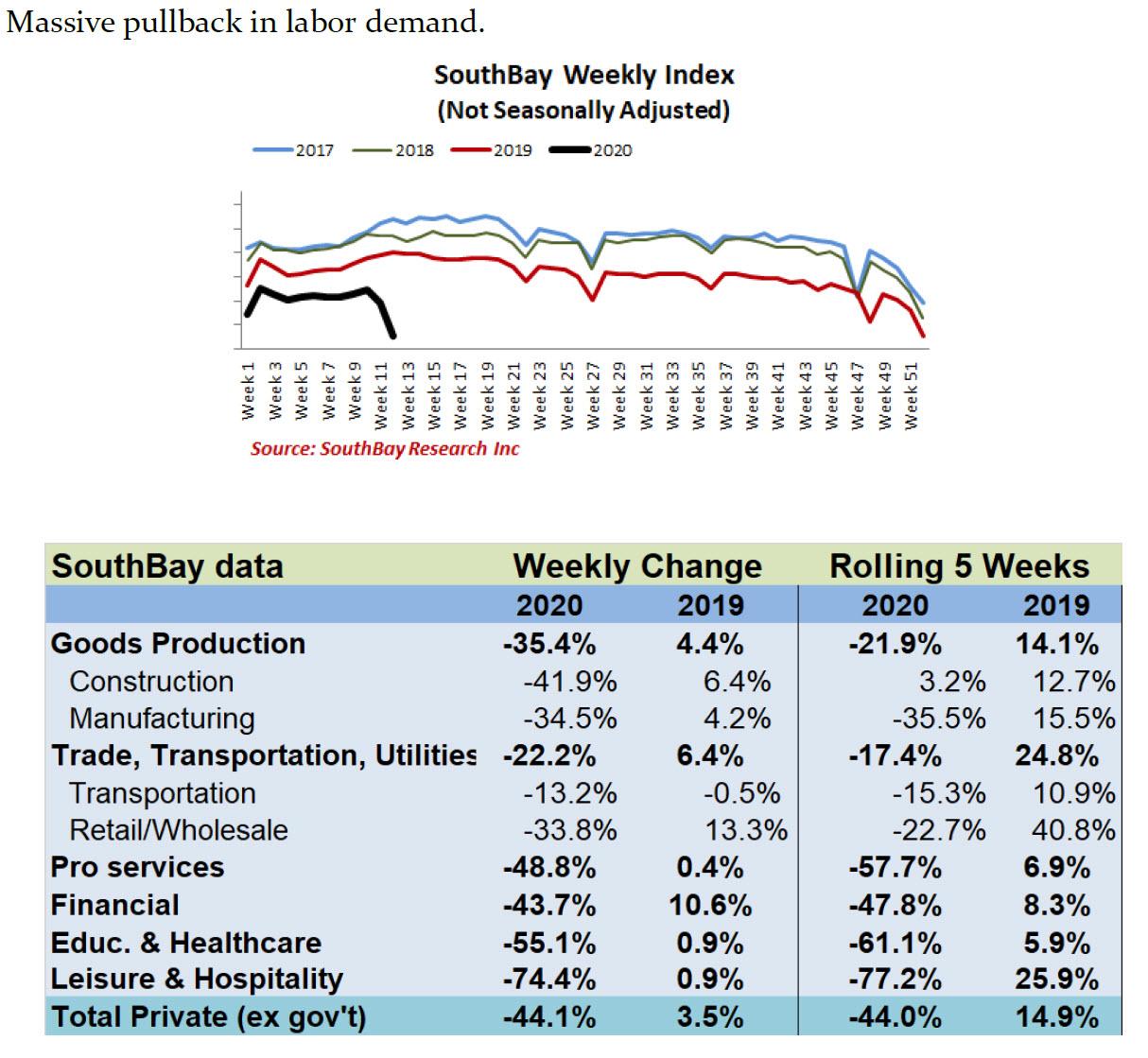

Last week’s initial claims print, which surged to 281K from a recent baseline of about 220K, while bad was nowhere near the apocalyptic prints some strategists had predicted in light of the massive closures of restaurants, retailers, lodgings, and virtually all other service establishments which have shuttered for the duration of the coronavirus pandemic.

Indeed, many now think that last week’s print was “low” only because the real hit was deferred to tomorrow due to processing delays and other logistical issues (countless labor department websites are only sporadically online amid the surge in traffic).

And while looking at tomorrow’s initial claims report reveals a historic surge in Wall Street expectations, with consensus now expecting up to 750K newly laid-off workers seeking benefits, according to Southbay, historically one of the most accurate labor market forecasters, tomorrow’s print will be a whopper at no less than 2.5 million!

Prior Week Initial Claims (Actual): 281K

Current Week Claims Forecast (Consensus): 750K

Current Week Claims Forecast (SouthBay): 2,351K

Here is SouthBay Research answering the question “How many people have been laid off?“

Consider theme parks: Disneyland shut last week and they employ ~25K. Disney World the same.

Or restaurants: There are 660K restaurants in the US. Of which 300K+ are full service restaurants (FSR): wait staff, host staff, bussers, dishwashers. According to the BLS, FSRs employ ~5.5M workers.

Basically it’s hard not to see 1M+ layoffs in dining & drinking establishments. (Barely 8% of the total Food & Drinking labor base). If each FSR lays off 1 waiter and 1 support staff, that alone is 600K.

Michigan reported 55k claims in the 1st 3 days of the week; that’s 15x the normal week total.

SouthBay’s Model

The SouthBay data shows a 66% y/y drop in hiring (-44% week-over-week), with the heaviest concentration in…restaurants. In 2009, when Jobless Claims were surging at a comparable rate, they were running at 600K Initial Claims per week. But we didn’t have complete shutdowns then.

The number will be slightly lower than actual because of late filings and government processing (the scale will be more than can be handled).

And visually:

This is what the initial claims chart will look like if SouthBay is right.

Confirming that tomorrow will be a bloodbath, is the latest commentary from Larry Kudlow who just said on Fox News that the upcoming jobs report will show a “large increase” in unemployment claims.

“It’s going to be a very big increase, everybody in the market knows that.”

Of course, the question is how large.

Finally, if not this week, the next will certainly be a shocker, and here’s why:

CA GOV: 1 MILLION IN STATE HAVE FILED JOBLESS CLAIMS THIS MONTH

Yesterday the Chair of the FDIC released an astonishing video asking Americans to keep their money in the bank.

Accompanied by soft piano music playing in the background, the official said:

“Your money is safe at the banks. The last thing you should be doing is pulling your money out of the banks thinking it’s going to be safer somewhere else.”

Amazing. I was half expecting her to waive her hand and say, “These aren’t the droids you’re looking for…”

As I’ve written before, there’s $250 TRILLION worth of debt in the world right now: student debt, housing debt, credit card debt, government debt, corporate debt, etc.

And let’s be honest, some of that debt is simply not going to be paid.

Millions of people have already lost their jobs. Millions more (like the 10 million waiters and bartenders across America) are barely earning anything right now because their businesses are closed.

A lot of those folks have no emergency savings to fall back on during times of crisis, so they’re going to be forced to choose: pay the rent, or buy food.

The government has already suspended evictions and foreclosures, which is a green light for people to stop paying the rent or mortgage.

And that means banks will take it in the teeth.

This is what happened back in 2008– millions of people across the country stopped paying their mortgages, and the banking system nearly collapsed as a result.

Today it’s a similar situation; a lot of people are going to stop paying their mortgages, credit cards, auto loans, etc. And that directly impacts the banks.

Businesses are in deep financial trouble too.

According to the Wall Street Journal, the median small business in the United States has a cash balance that will last them just 27 days.

And many are operating with an even smaller safety net; the median restaurant, for example, has a cash balance of just 16 days.

These businesses have been told to close down due to the Corona Virus. And it’s likely that many of them will never re-open.

A lot of these companies also have debt. And if they close, those debts will never be repaid.

Even big businesses are susceptible to failure.

Every airline, cruise ship operator, hotel, retail chain, etc. is on the ropes, and each of these companies has borrowed billions of dollars.

This pandemic could easily push several big companies into bankruptcy.

You probably know that old saying– if you owe the bank a million dollars and can’t pay, you have a problem. If you owe the bank a billion dollars and can’t pay, the bank has a problem.

That’s what we’re seeing now.

Countless unemployed individuals, millions of shuttered small businesses, and bankrupt big companies collectively owe the banks trillions of dollars. And many of them can’t pay… which means the entire banking system has a problem.

How much money will the banks lose because of this pandemic?

It could easily end up being hundreds of billions of dollars, even several trillion dollars.

No one knows. But it’s not going to be zero. It’s silly to think that banks are immune to the Corona virus, or to assume that not a single bank is going to run into problems.

Don’t get me wrong– I’m not saying that the banking system is about to collapse. There are stronger banks and weaker banks. Many of them will survive, others will fail.

What I am saying is that there are enormous and obvious risks that threaten the banking system.

As I’ve written several times over the past few weeks: Anyone who says, “No, that’s impossible,” clearly doesn’t have a grasp of what’s happening right now. EVERY scenario is on the table, including severe problems in the banking system.

But the FDIC insists that there’s nothing to worry about.

That’s ridiculous. The FDIC only has $109 billion to insure the entire $13 trillion US banking system. That’s less than 1%!

The FDIC also insists that they’ve always been able to prevent depositors from losing money. “Not a single depositor has lost money since 1933.” And that’s true.

But they’ve never had to deal with this before. Neither the FDIC, nor any bank, has ever had to deal with a complete shutdown of the economy… or potential losses of this magnitude.

The Covid-19 impact on the banking system could be 10x bigger than the housing meltdown in 2008.

If the pandemic ends up causing trillions of dollars of loan losses, the FDIC won’t have enough ammunition to fix it… and that doesn’t even consider trillions of dollars more in potentially toxic derivatives exposure.

So to casually brush off these risks and claim that everything is 100% safe seems incomprehensible.

It also raises an interesting point: why is the FDIC asking us to NOT withdraw our savings?

If the financial system is so safe, it shouldn’t matter to them whether or not people keep their money in the banks.

Yet they still felt the need to specifically ask people to NOT withdraw their money… and tell us that we shouldn’t keep cash at home.

I’ll reiterate a point that we’ve made again and again at Sovereign Man over the years: it makes sense to have some physical cash in an at-home safe.

I’m not suggesting you keep your life’s savings in physical cash. But a month or two worth of expenses won’t hurt.

There’s very little downside– your bank probably only pays you 0.01% anyhow, so it’s not like you will be giving up a ton of interest income.

And given that the FDIC is specifically saying that you shouldn’t do this, a prudent person might wonder what’s really going on.

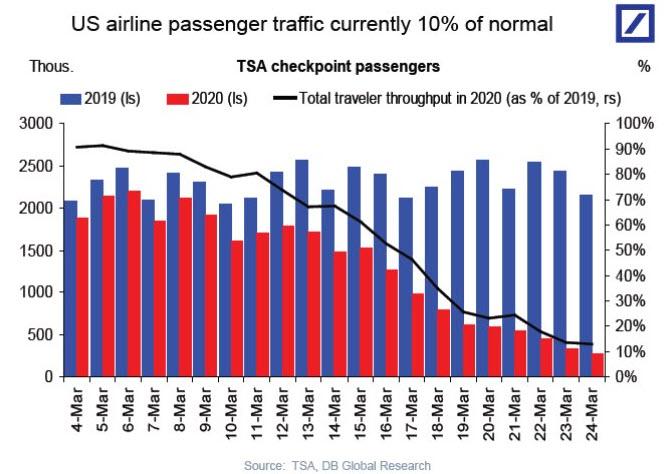

Unprecedented Collapse: US Airline Traffic Currently Just 10% Of Normal

Previously we reported that the US restaurant and retail industries have all but shut down. We can now add airlines.

According to this stunning chart from Deutsche Bank’s Torsten Slok, US airline passenger traffic is currently just 10% of normal. As Slok explains, “on a normal day in March, over 2 million people travel by air in the United States. Yesterday that number was 279,018.”

And somehow Boeing hopes to have the 737 MAX flying in May…

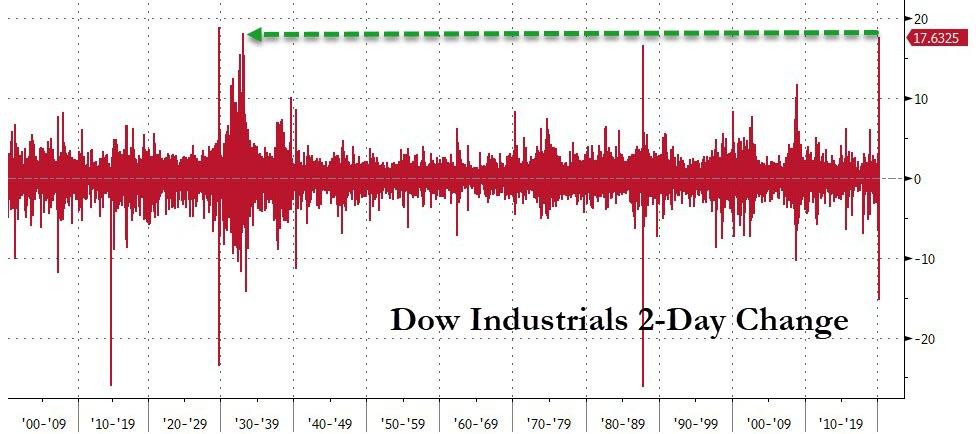

Stocks Scream Higher On Greatest Short-Squeeze In History, Bonds & Bullion Shrug

“Fear” is almost over according to the market’s “Virus Fear” trade…

Source: Bloomberg

The Dow is up by almost 18% in the last 2 days – the biggest 2-day surge since March 1933…

Source: Bloomberg

And Dow futures are up a stunning 20% from the limit-down lows on Sunday night…

But bonds ain’t buying it…

Source: Bloomberg

So, with stocks roaring higher once again, this seemed appropriate…

“Most Shorted” stocks are up a stunning 21% in the last two days – the greatest short-squeeze in history…

Source: Bloomberg

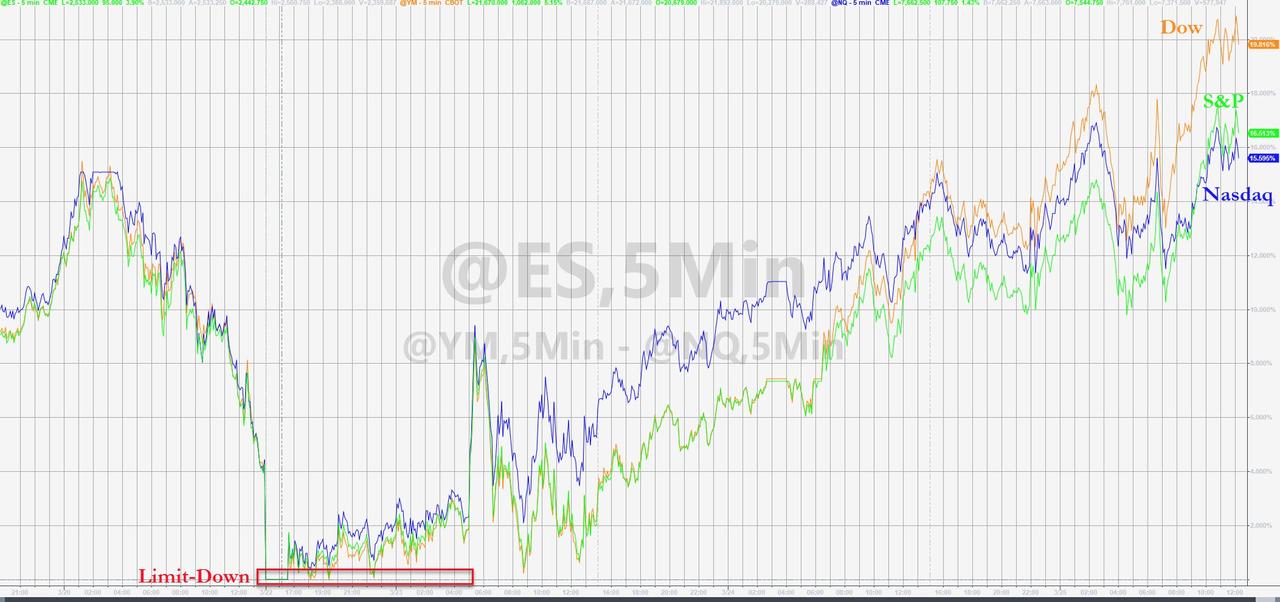

Dow futures show the insane scale of today’s moves best – a 1000 point surge into yesterday’s close, a failed 1000 point surge overnight (on the “deal”), another failed 1000 point surge into and through the cash open, and then a 1500 points surge that held into the close…

BUT – Things “went a little bit slightly turbo” into the close as Bernie Sanders spoiled the party by threatening to hold up the vote on the bill…

Knocking stocks lower and sending Nasdaq red on the day…

AAPL also did not help as reports came out that it may delay its 5G phone…

However, on the last two days, stocks are up strong…

Airlines, Cruise operators, and restaurants all soared massively today again…

Source: Bloomberg

Boeing was the most ridiculous of all stocks…

Source: Bloomberg

There’s nothing like a government handout to make everything better! What a farce!

VIX and stocks have decoupled (are people seriously buying calls to lever-up into this rebound? Or is this hedgers?). VIX was unchanged today as stocks soared…

Source: Bloomberg

Treasury yields were mixed today – short-end bid (less than 5Y -2bps), long-end offered (30Y +2bps), belly flat but relative to stocks huge moves, bonds basically shrugged…

Source: Bloomberg

Starting at around 1400ET, someone decided to dump the long-bond hard…

Source: Bloomberg

US T-Bills have negative yields out to the end of the year…

Source: Bloomberg

Both HY and IG bonds rallied today (thogh HYG rolled over late on as LQD was bid into the close)…

Source: Bloomberg

Before we leave bond-land, it is worth pointing out that the number of bonds trading at a spread over 1,000 bps (the barometer of distress) neared 1,900 this week – the highest since 2009, data compiled by Bloomberg show. It was less than 300 at the start of March.

Source: Bloomberg

As Bloomberg noted, the spread on the entire junk bond index flipped above 1,000 bps on Friday, and strategists expect it to exceed 1,200 bps soon. In addition, there’s a whole world of grief in the $1 trillion leveraged-loan market, which is trading on average below 80 cents on the dollar, a level typically associated with distress.

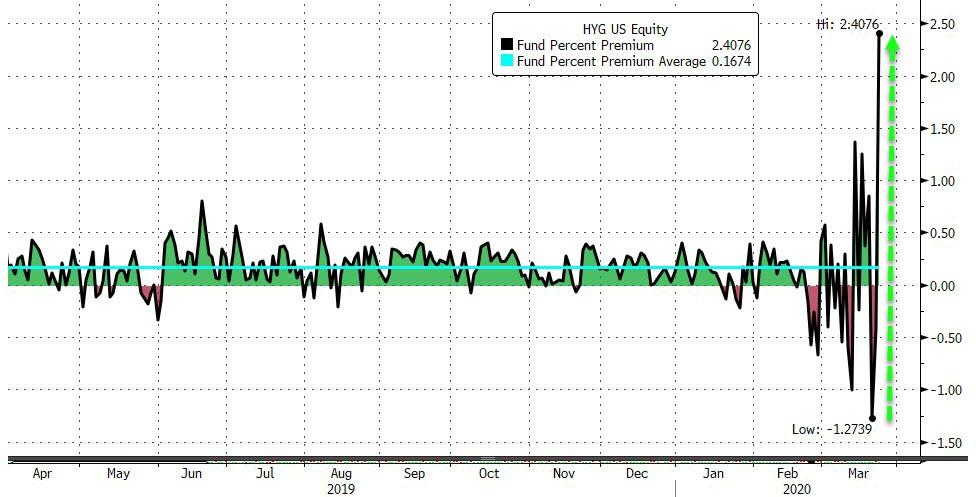

But, HYG – the HY Bond ETF – has screamed higher today, back into a huge premium to underlying NAV…

Source: Bloomberg

The Dollar tumbled for the second day in a row (after 11 days straight up)…

Source: Bloomberg

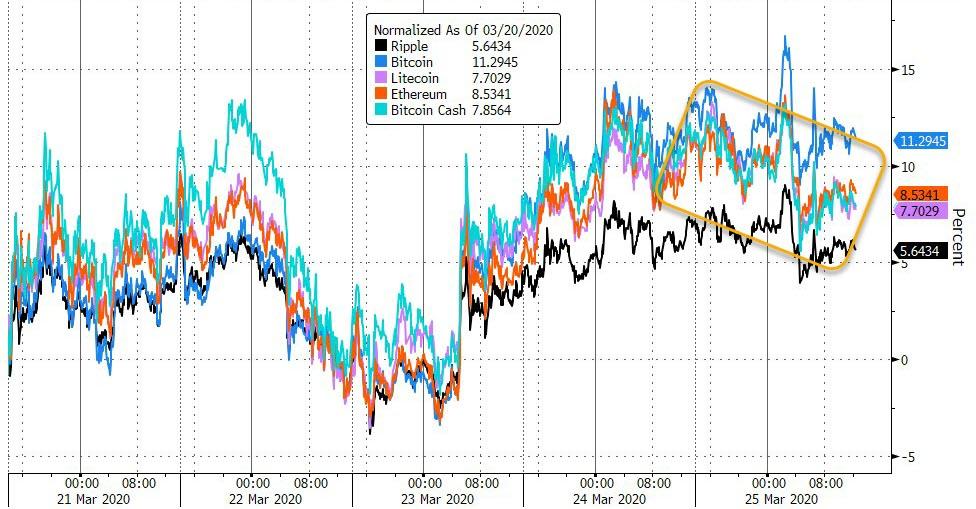

Cryptos broadly slipped lower today…

Source: Bloomberg

Someone was bidding oil again during the US session…

Source: Bloomberg

Spot Gold and futures remain decoupled though the spread did compress from their extremes yesterday…

Source: Bloomberg

Palladium exploded higher today (though all PMs are notably higher since The Fed went “all-in”)…

Source: Bloomberg

After surging Tuesday, Palladium futures in New York skyrocketed 26% Wednesday, the biggest gain in records dating back to 1986.

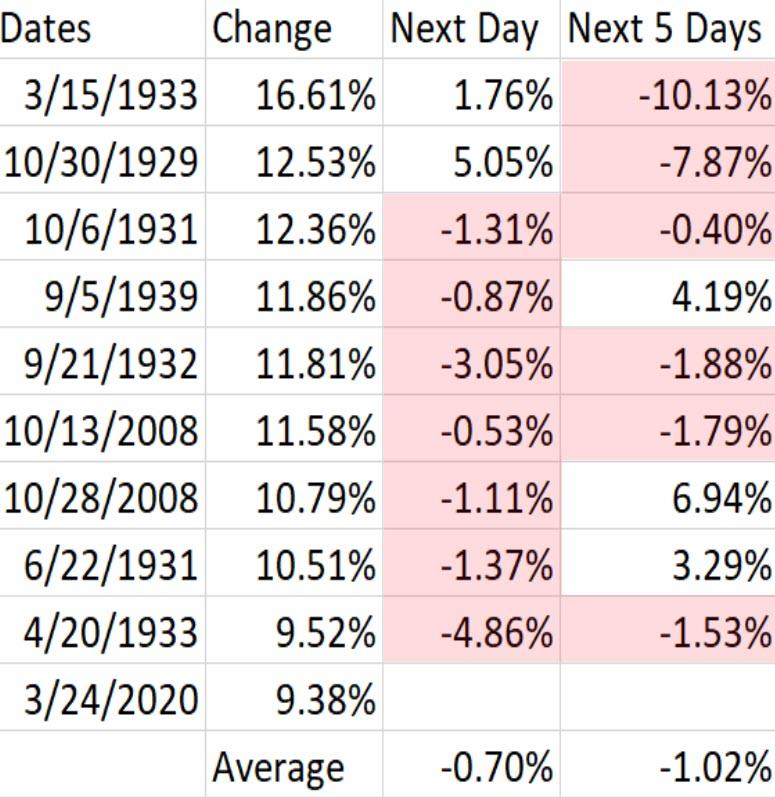

Finally, we’ve seen this all before… As Bloomberg details, historically expectations are low after a big rally. The 9.4% jump in the S&P 500 yesterday was the 10th largest in history. The benchmark S&P fell seven of the previous nine times with an average loss of 0.7%.

While the most intense sell-off may be behind us, there’s still room for the markets to fall. For one, the current drawdown is 34%. It is less than the peak-to-trough falls in the previous crises, including the 57% slump in 2008-2009, the 49% drop after the burst of the dot.com bubble and the 48% retreat during the 1973 oil crisis.

And for now, it appears the 1929 analog is holding up…

Source: Bloomberg

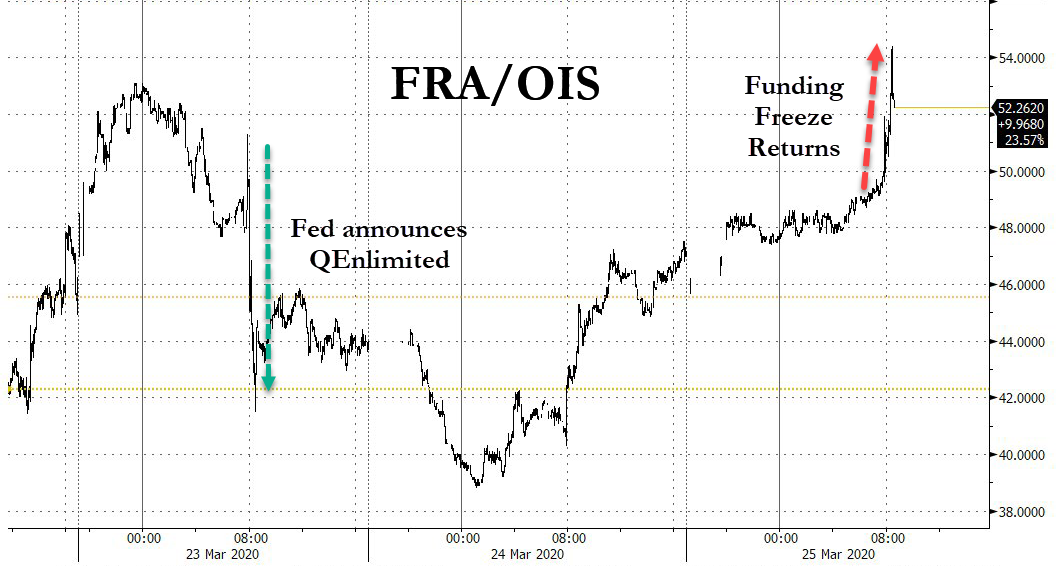

It’s certainly good news that the fiscal stimulus of more than $2 trillion is on the verge of getting passed in Congress. But the stimulus and various Fed actions are necessary but insufficient conditions for the market to bottom, and worse still, the dollar funding crisis is rapidly re-accelerating as month-end looms… having erased all of the ‘improvement’ offered by The Fed…

Source: Bloomberg

And don’t forget – tomorrow is jobless claims and it’s going to be a doozy!

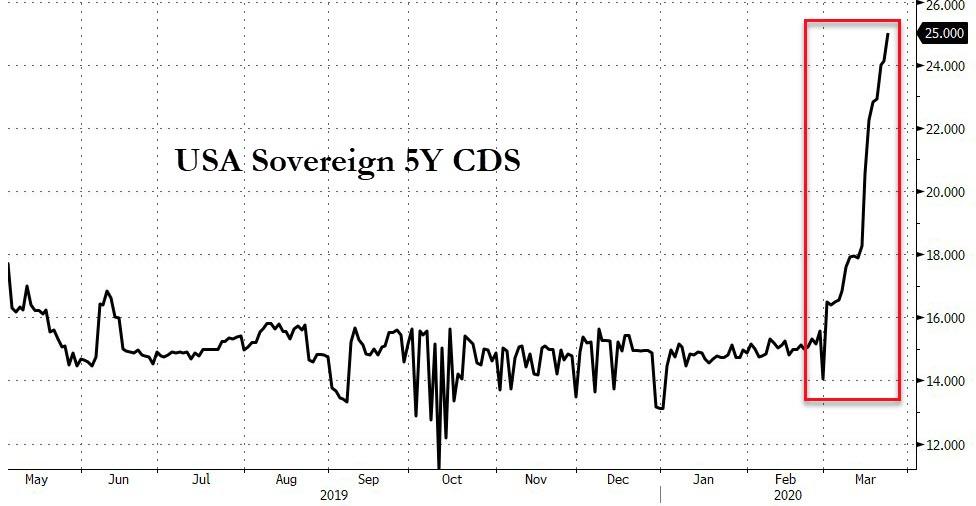

If all of that doesn’t scare you – this should – the sovereign credit risk of the USA is surging higher since helicopter money began to creep into reality…

Apple Tumbles After Report Says 5G iPhone Could Be Delayed To 2021

A new report from Nikkei Asian Review states that Apple could delay the launch of its 5G iPhone over supply chain disruptions in China and new fears of demand issues as the global economy crashes.

Sources told Nikkei that Apple has “held internal discussions on the possibility of delaying the launch by months, three people familiar with the matter said, while supply chain sources say practical hurdles could push back the release, originally scheduled for September.”

“Supply chain constraint aside, Apple is concerned that the current situation would significantly lower consumer appetite to upgrade their phones, which could lead to a tame reception of the first 5G iPhone,” said the source. “They need the first 5G iPhone to be a hit.”

None of this should be surprising considering our March 6 report that specified, “the iPhone 5G launch in the fall could see a month of delay.”

Another source told Nikkei that a final decision on the 5G iPhone delay could arrive in May.

“The discussion is still at an early stage, and the fall launch is not completely off the table,” the source said. “But the 5G iPhone could be postponed to 2021 in the worst-case scenario.”

Just like the Olympics, it seems that Apple could delay its latest and greatest 5G iPhone to 2021.

So was the Nikkei report of possible 5G iPhone delays the reason why Apple shares tumbled in late session?

China Lifts Lockdown On Hubei Province Despite COVID-19 Resurgence

People flooded onto trains and buses in Hubei province on Wednesday after China lifted a two-month lockdown on the epicenter of the coronavirus outbreak, which began in the eastern city of Wuhan (roughly 900 feet from a laboratory where they were experimenting on bat coronavirus that’s 96% genetically identical to COVID-19).

At a railway station in the city of Macheng, there were long queues of people lugging suitcases in the rain as they queued for trains.

Children in masks were among those waiting, while guards directed the crowds and station announcements offered details of trains to destinations across the country.

Footage from Xinhua News Agency showed migrant workers in Huanggang — one of the cities worst-hit by the coronavirus outbreak — queuing for long-distance coaches. –RTHK.hk

“I have been at home in Hubei for more than two months,” said one unnamed worker returning to Wenzhou in Zhejiang province.

While trains and buses are not yet operating in Wuhan, 30 highways leading into the city were re-opened on Wednesday according to state media, which showed jam-packed roads.

According to state broadcaster CCTV, a state police traffic officer said that people are allowed to travel in and out of Hubei as long as they have a “green” health code issued by authorities, according to RTHK.

It’s not over, however

While CCP officials claim there have been no new local infections in Wuhan over the last few days, RTHK sources say that’s “simply not the case,” and that people are being turned away from hospitals without being tested in order to back the official data.

A member of a volunteer group said his mother, who is in hospital with a heart problem, had seen coronavirus patients being turned away by staff.

Zhang Yi said it is a political need that is making mainland authorities claim there have been no new local infections.

He said he had received messages from officials which showed there were still people coming down with the disease in Wuhan.

“Whether the official figure is accurate or not, I think you will know. This is a political treatment, not medical treatment,” he said. –RTHK

Meanwhile, one of China’s own top experts, professor Li Lanjuan- who has been handling the medical aspect of the Wuhan outbreak – says she is “very worried that imported cases could trigger another large-scale epidemic” in the country.

Her comment came after health officials reported the country’s first case of someone who is believed to have contracted the disease, known as COVID-19, from another person returning from abroad.

It also came as life in former epicentre Wuhan is slowly returning to normal following a two-month draconian lockdown. –Daily Mail

“The mission in Wuhan has not been accomplished, and there are still many critical patients,” said Li, adding “I think the current situation in our country is very tough.”

Cuomo: Stimulus Deal “Terrible” – Would Leave NY With “Drop In The Bucket”

New York Governor Andrew Cuomo (D) criticized the impending COVID-19 stimulus deal as “terrible,” and would allocate a “drop in the bucket” to the worst-hit state in the nation, according to The Hill.

“The Senate is considering a $2 trillion bill, which is quote-unquote ‘relief’ for business, individuals and governments,” said Cuomo during his daily briefing, adding. “It would really be terrible for the state of New York.”

“What does it mean for New York state?” the governor asked. “It means $3.8 billion. $3.8 billion sounds like a lot of money, but we’re looking at a revenue shortfall of [as much as] $15 billion. This response to this virus has probably already cost us $1 billion, and it will probably cost us several billion dollars when we’re done.”

New York City, specifically, Cuomo said, will only receive $1.3 billion in the stimulus deal, which he called “a drop in the bucket, as to need.”

“I spoke to our House congressional delegation this morning, I said to them ‘this doesn’t do it.’ I understand the Senate theory and the Republican theory but we need the House to make adjustments,” Cuomo said, noting that the House’s bill, in contrast, gave the state $17 billion. –The Hill

“We’re not a big-spending state. I cut taxes every year,” Cuomo continued. “I have the lowest growth rate of the state budget in modern political history. We are frugal and we are efficient. I’m telling you these numbers don’t work and I told the House members that we really need their help.“

New York has 30,811 registered cases and 285 deaths from COVID-19 as of this writing.

In February, the general consensus among large investment banks and supranational entities was that there would be a one-time impact on GDP in the first quarter due to the impact of the coronavirus, followed by a stronger recovery in the form of V.

The IMF anticipated a modest correction to world GDP of 0.1%, and the biggest cut in growth estimates for 2020 was 0.4%.

Those days are over.

The latest round of world growth reviews includes a reduction in growth estimates for the first and second quarters and a very modest recovery in the third and fourth quarters. Estimates of average GDP are now down 0.7%, and JP Morgan expects the eurozone to enter a deep recession in the next two quarters (-1.8% and -3.3% in the first and second quarters), followed by a very poor recovery that would still leave the estimate for the entire year 2020 in contraction.

The investment bank also assumes that the United States will fall by 2% and 3% respectively, but with modest growth throughout the year (considerably more than consensus)…

Capital Economics estimates a year-long blow to the US economy that would cut 0.8% from previous estimates, although it continues to predict growth, but a greater impact in the euro area, with growth throughout the year 2020 to an average of -1.2%, led by a prediction of -2% for Italy. This, unfortunately, seems only the beginning of a cycle of decline that adds to the problem of an economy that was already slowing down in 2019.

The decision to close air travel and to close all non-essential business is now a reality in the world’s major economies. The United States has banned all European flights, while Italy enters a complete blockade, Spain declares a state of emergency and Franceclose all public places and nonessential businesses. These decisions are key to containing the spread of the virus and trying to prevent the collapse of health systems, and our thoughts are with all those infected. Closing travel and business has a negative domino effect on the economy. It is an important measure to prevent a rapid spread of the disease and there will be more cancellations of events and activities.

By now, at least we have a clearer picture of the severity of the pandemic, and we can discuss the economic consequences, so I think it’s important to remind readers of some important factors:

We cannot assume that the above estimates are too pessimistic. If we have learned anything from the history of world growth estimates, it is that most of us tend to be more optimistic than realists even in periods of crisis. Most analysts did not see a crisis in 2008 and, most importantly, most did not see it in 2009, when it was evident. It is true that 80 percent of the estimates at the beginning of any year have to be revised, but it is not because they are too pessimistic, but rather the opposite.

Calls for large tax packages to offset the pandemic may be futile. Allen-Reynolds of Capital Economics warned that “even if governments agreed to a broader fiscal and spending package, the economic impact would be much less than in the past, particularly if the fiscal stimulus was concentrated in Germany,” because the production gaps are almost non-existent. This is not a demand problem, but a supply shock, and supply shocks with bricks, mortar, and deficit spending are not addressed.

A quick recovery in the third quarter is now virtually impossible. The collapse of the developed economies is already guaranteed and will probably take us more than a couple of weeks. The collapse of emerging economies is likely to start in May and affect estimates for 2020 and 2021. All the analyzes we’ve seen so far only take into account the factors of a recession in 2020, not a crisis, let alone a major impact on the economy in 2021, but the financial implications of an already over-leveraged world add a series of credit events to an economic collapse.

The latest wave of downgrades is already a large-scale stimulus, rate cuts, and quantitative easing. The diminishing returns of monetary easing were already evident in 2018 and especially in 2019, with global manufacturing purchasing managers (PMI) indices contracting and growth estimates dropping significantly throughout the year. Average downward growth reviews by country averaged 20% between January and December, amid a coordinated and massive injection operation by the central bank that injected up to $ 170 billion a month into the economy (considering the Banco Popular de China (PBOC), the Bank of Japan (BOJ), the European Central Bank (ECB) and the Federal Reserve) and saw widespread cuts in rates.

The economic implications of a pandemic will not be resolved with a massive increase in spending. Governments will implement large demand policies that are the wrong response to a collapse of the economy. Most companies will experience a collapse in sales and the consequent accumulation of working capital, and none of this will be resolved by deficit spending. A supply shock cannot be mitigated with demand policies, which increase debt and excess capacity in sectors already in debt and swollen and do not help sectors that are experiencing an abrupt collapse in activity.

A forced temporary collapse must also include the collapse of the tax collection system. Governments already finance themselves at negative rates. They must eliminate (not defer) the payment of taxes to companies in the crisis period to avoid a massive increase in unemployment and a domination of bankruptcies, and facilitate working capital lines with zero rates to allow companies and self-employed workers circumvent a closure. Governments that make the mistake of maintaining the current fiscal structure or simply extend the payment period for six months will see the huge negative consequences of a closure in the next nine months.

If, as expected, the collapse spreads to more countries every week, the negative effects on the economy will be longer and exponential, and the mirage of a recovery in the third quarter will be even less likely.

It is very likely that the closure of the main developed economies will be followed by a closure of the emerging markets, creating a shock to supply that has not been seen in decades. The adoption of massive inflationary and demand-driven measures in a shock to supply is not only a mistake, but is the recipe for stagflation and guarantees a multi-year negative impact generated by the increase in debt, the weakening of productivity, the increase in inflation in non-reproducible goods while deflation is making headlines and economic stagnation.

{kind=link}