Trump Surprised Staff With Promise Of Tuesday Announcement On Coronavirus Stimulus

President Trump surprised his staff by announcing the details of an economic package set to be unveiled Tuesday in response to chaotic markets that have been rocked by the impacts of coronavirus and an escalating oil price war, according to Bloomberg, citing ‘people familiar with the matter.’

As outlined by Trump in remarks Monday, the proposal will likely include a payroll tax cut and a short-term expansion of paid sick leave, according to the people, who described the proposal on condition of anonymity ahead of its planned release.

Trump’s administration had been working on potential stimulus measures for about 10 days but were unprepared to provide details this quickly, the people said. –Bloomberg

Stocks plunged over 7.5% on Monday, the worst day on Wall Street since the financial crisis (and worst since 1987 intra-day) which saw credit and funding markets start to show signs of extreme stress. This has put Trump under increased pressure to act on concerns that COVID-19 will trigger a recession.

Trump has also been blaming the Federal Reserve – slamming them as “pathetic” and “slow” in Tuesday morning tweets, adding “The Federal Reserve must be a leader, not a very late follower, which it has been!”

Our pathetic, slow moving Federal Reserve, headed by Jay Powell, who raised rates too fast and lowered too late, should get our Fed Rate down to the levels of our competitor nations. They now have as much as a two point advantage, with even bigger currency help. Also, stimulate!

House Democrats, meanwhile, are set to hear from two economists on Wednesday for input as lawmakers consider a fiscal package in response to the coronavirus impact. Both have called for immediate action, with Harvard’s Jason Furman advocating for approximately $350 billion in aid.

Amid all of yesterday’s chaos in bond, commodity, and stock markets, with the yield on the 10-year US Treasury note dropping below 0.5% for the first time in history – a strong indicator that investors are desperately looking for safe harbors – two supposed safe-havens in ‘alternative currencies’ behaved quite differently.

Gold prices remained flat over the day at $1.673 per ounce after reaching a historic high at $1,700 last night. The commodity is up 5.6% in March, displaying a healthy performance during the Coronavirus epidemic which has now spread to nearly every country on the planet.

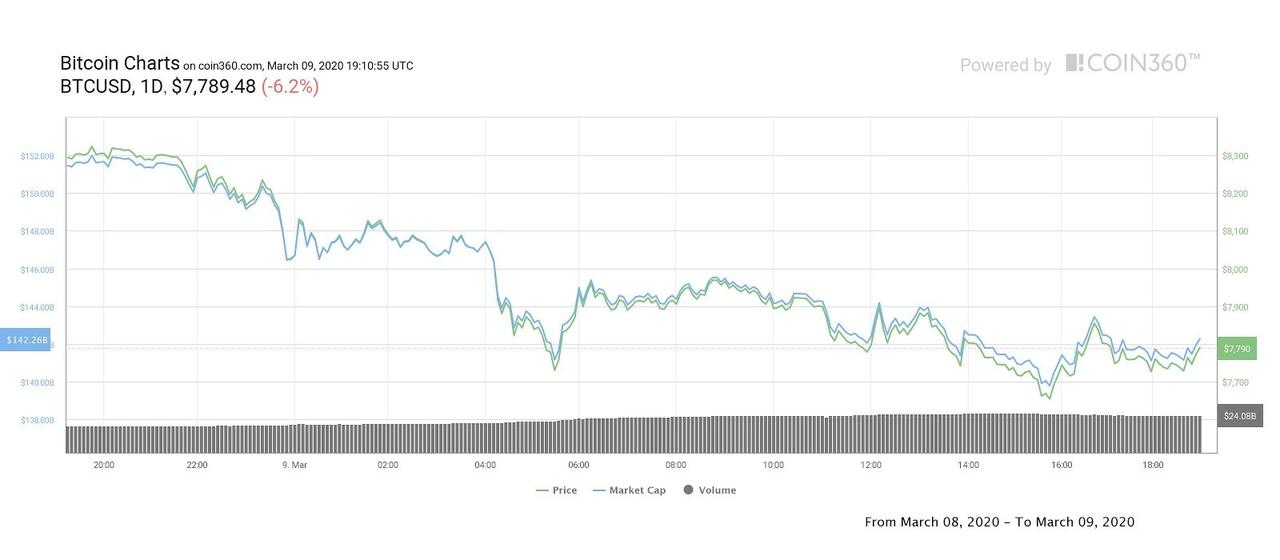

On the other hand, Bitcoin (BTC) is down 13% in 48 hours, testing its lowest level since early January at $7,750.

Brian Armstrong, co-founder and CEO at Coinbase, was caught off guard by the recent price move as expressed by his shock by tweeting:

“Surprised we’re seeing the Bitcoin price fall in this environment, would have expected the opposite.”

BlockTower co-founder Ari David Paul, also tweeted that despite a recent 25% drop in less than 30 days, Bitcoin remains up 7.5% year to date.

Earlier in the day derivatives trader Tony Stewart tweeted that options skew indicator – an important he interprets as a good measure of fear – rose significantly over the past week. According to Stewart, “this skew measures a fear for further downside moves.”

Bitcoin 25d skew. Source: Skew.com

Analysts warn that the financial crisis could deepen

Dennis Dick, head of markets structure and proprietary trader at Bright Trading LLC, raised a red flag on the potential outcome of today’s market reaction. Dick said:

“There is potential that we could be at the start of a financial crisis part two… It’s a possibility right now that wasn’t on the table until we had this oil plunge over the weekend.”

As Bitcoin price corrects, altcoins have also taken on heavy losses. Ether (ETH) has dropped 8.86%, Bitcoin Cash (BCH) is down 7.72% and Litecoin (LTC) lost 10.42% to trade below $50.

The overall cryptocurrency market cap now stands at $222.2 billion and Bitcoin’s dominance rate is 64%.

Stocks Tumble After Trump Claims Pelosi “Won’t Be Ready This Week” To Meet On Fiscal Plans

Markets reacted negatively to a tweet from President Trump claiming that “Do Nothing Democrats” will be unable to meet this week to discuss possible fiscal stimulus plans.

Nancy Pelosi just said, “I don’t know if we can be ready this week.”

In other words, it’s off to vacation for the Do Nothing Democrats. That’s been the story with them for 1 1/2 years!

Nancy Pelosi just said, “I don’t know if we can be ready this week.” In other words, it’s off to vacation for the Do Nothing Democrats. That’s been the story with them for 1 1/2 years!

As Stocks & Oil Surge, Credit Market Carnage Continues

Everything must be awesome again, right? Stocks are up. Oil is up. Bond yields are up… and no one has said the word “bloodbath” on CNBC yet this morning.

However, those pesky kids in the credit markets won’t let stocks get away with it as HY credit spreads continue to scream wider…

Notably shunning the exuberance of this morning’s equity bounce…

For now stocks are fading back rapidly from overnight highs…

Nomura: Today Has The Feel Of A Standard “Bear-Market Rally”

One day after Nomura’s Charlie McElligott deconstructed the various flow and technical drivers behind Monday’s unprecedented VaR shock-cascading plunge in the US stock market, on Tuesday the quant writes that yesterday’s “peak calamity” moment, where shock price gaps triggered “negative-convexity”/“short-gamma”-like trading across VIX, Equities, Rates and Crude, is been meaningfully reversed, with S&P futures briefly surging “limit up” earlier after screaming +4.7% to 2879.

The Pavlovian response that tiggered this move is hardly a secret: whether one uses Michael Hartnett’s favorite phrase whereby “markets stop panicking when policymakers start panicking”, or simply points to the market hope that a “major” fiscal stimulus is about to be unveiled by Trump (even though we now know it probably won’t), as McElligott puts it, “the worse this market-shock gets (thus negatively impacting US financial conditions, particularly at risk of self-fulfilling a corporate credit crunch), the larger the more asymmetric the policy response will likely be; as such, fiscal stimulus measures are beginning to take shape globally, as governments respond to COVID-19.”

Which brings up the question whether either fiscal, or monetary, or a joint stimulus response can do anything to fix a problem that is health/epidemiological in nature. This is how Rabobank’s Michael Every put it:

US President Trump, who is truly worried about those Dow baseball caps, doubly so as the prediction markets concurrently see his odds of retaining the presidency decline, has floated “very substantial measures” via an economic stimulus package: one that includes a payroll-tax cut, to either save or spend on toilet roll; support for hourly wage earners that will allow people to take paid time off if they get sick (presuming they have insurance to cover medical bills); as well as some kind of fiscal support for small businesses, who are about to see demand evaporate anyway.

This is all welcome but is just a plaster on a deep wound unless we see some serious efforts to concurrently fight the virus, not the bear market – and as the “Chug! Chug! Chug!” dynamic at the US sporting event yesterday underline, this is still not being seen on the ground.

Which brings us to the bigger point: was yesterday’s panicked selling the bottom, and is today the start of a new rally? McElligott’s answer won’t please the bulls:“Today has the feel of a standard “bear-market rally”…

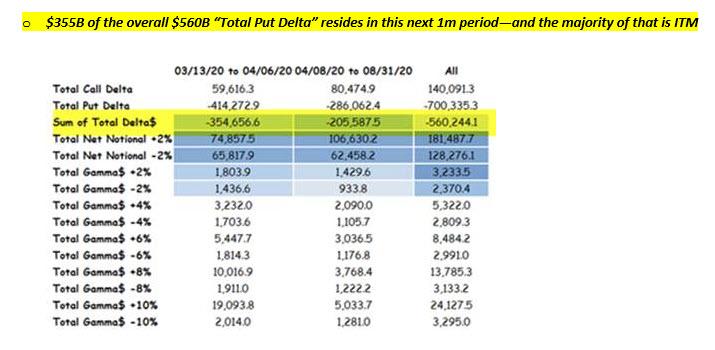

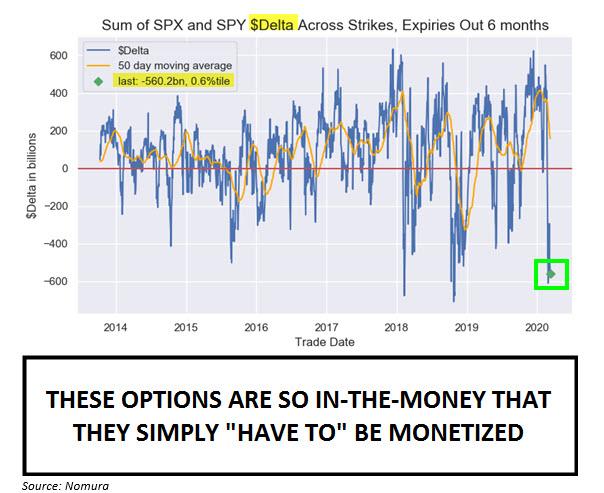

… where selling is increasingly exhausted (see “tgt vol” fund example below), monetization of dynamic hedging in futures shorts turns into a rather violent “squeeze”; as stated repeatedly here, the enormous “Short Delta” via SPX / SPY options (-$560B, 0.6 %Ile since ’13) will continue to act as a “core” catalyst for these raging UP trades (despite still-horrible sentiment and outlook from clients) as these options “have to” be monetized when they’re this in-the-money, especially as they’re expensive to roll.”

Here the biggest factor for reflexive, “technical” buying is the massive notional ($355BN) of put delta that is currently deep in the money over the next month…

… rising to a gargantuan $560BN over the next six months.

Another point made by Charlie is that yesterday we saw equity futures and ETF volumes (ex-XLE in light of the absurd Energy move) shrink relative to single-name flows for the first time in this down-trade, which to him “indicates that there was a local high in de-grossing flows of underlying L/S book exposures, as funds went into risk-management “VaR-down” mode, something we discussed extensively yesterday.

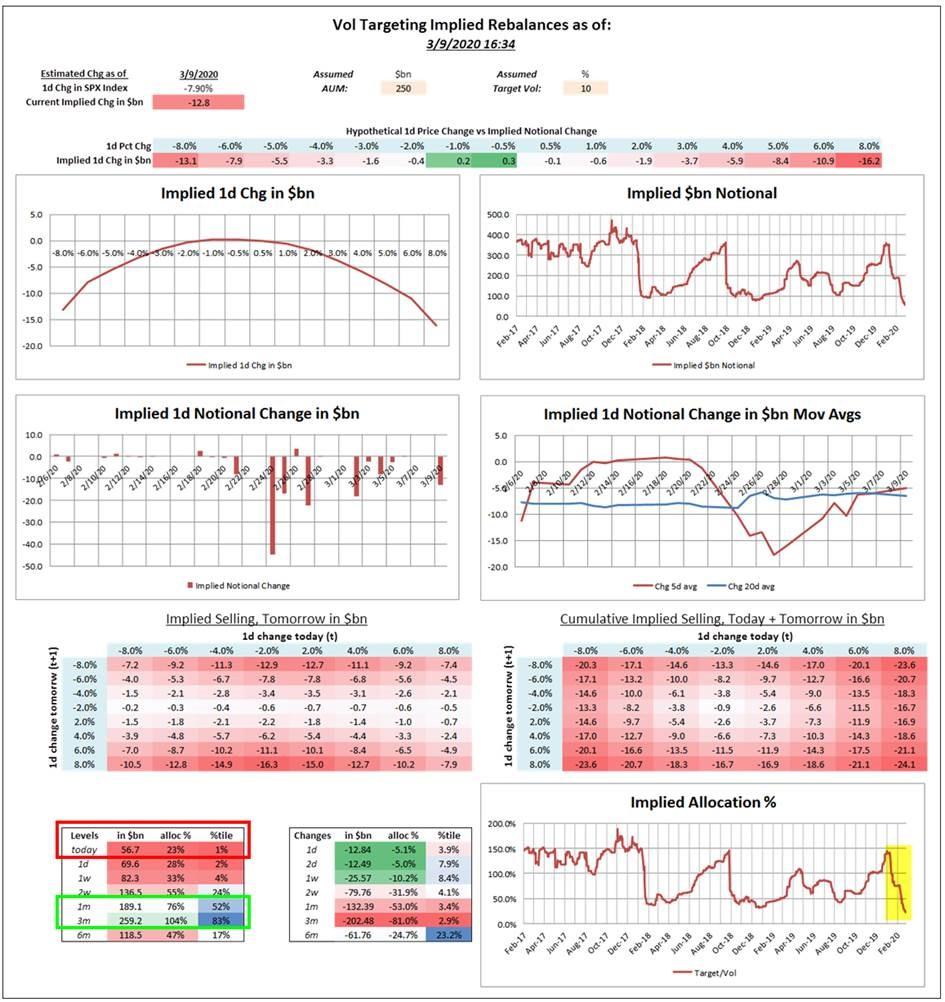

Another example of this increasing “exhaustion” of sell flows, is that Nomura’s “Target Vol” fund implied rebalancing model estimates that the $130B of Equities selling over the past 1 month has shrunk to just $56.7BN, or 23% allocation left, which is a 1st %ile since 2010: “this simply tells us that there is increasingly little left to sell and the greater risk is incremental reallocation to BUY in the coming weeks.“

Yet whether this is merely a bear-market rally, or just seller exhaustion, the key for a “sticky” bounce according to McElligott will be the ability for Vol to reset lower, “but which, for now, remains a challenge most likely until after the March 20th expiration, when the majority of the two prolific legacy hedges in the market we have discussed for months on account of their impact on term-structure (the mega S&P put-wing trades from 2500-2700 strikes and the high-profile VIX call wing lottery tickets) are largely set to expire, and should help release this massive tension in the market that keeps S&P trading so “crash-y.”

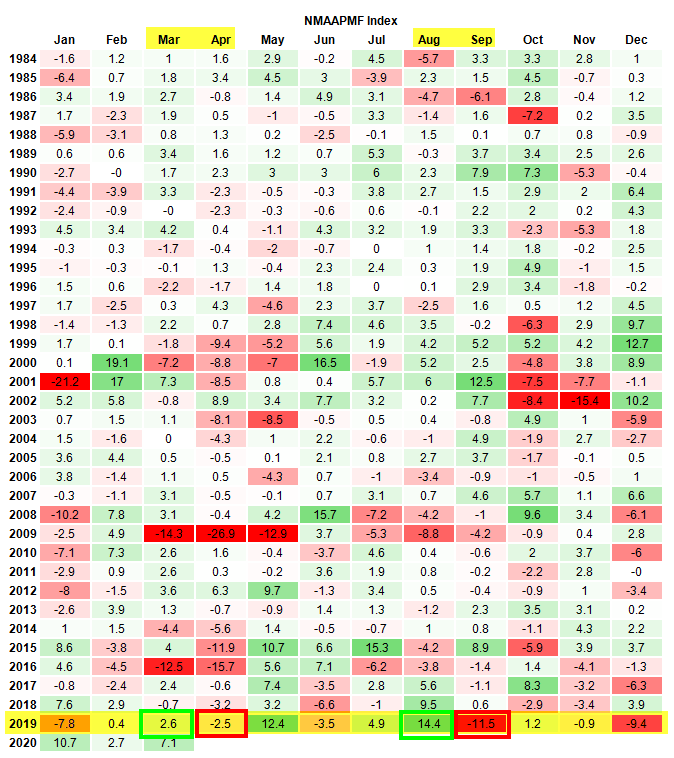

There is another risk: as Charlie writes, “if we see an extension of the UST/Rates selloff on Risk-Asset relief and increased FISCAL stimulus (coming after front-loaded monetary policy “easing”), it is in scope of aligning dangerously with the April U.S. Equities “Peak Momentum Unwind” seasonal month (since 1984).”

This dynamic risks looking like the dual Mar/Apr and Aug/Sep “rally then shock reversal” trades last year in US factors, whereas “Price Momentum” saw enormous performance in Mar and Aug on the back of the factor being a “pure” expression of the “Everything Duration” trade, rallying tremendously with USTs / Rates—but in the month after each Bond rally “overshoot” (largely on account of the “Negative Convexity” events in March ’19 due to Dealer Vol Desks and the August ’19 kind being a function of the Mortgage / ALM / Bank Portfolio hedging / forced buying of Duration), we then saw crashing “Momentum Unwinds” in US Equities

In conclusion, if volatility indeed resets lower after the March expiry, and if TSYs/Rates also re-price lower thereafter into April’s “Peak Momentum Unwind” monthly seasonal, “we can then see a forced re-risking from Vol Target / Risk Control strategies via potentially massive releveraging and in-turn creating a powerful “UP-trade” in Equities…April has the makings for something special from the “Reversal” side…”

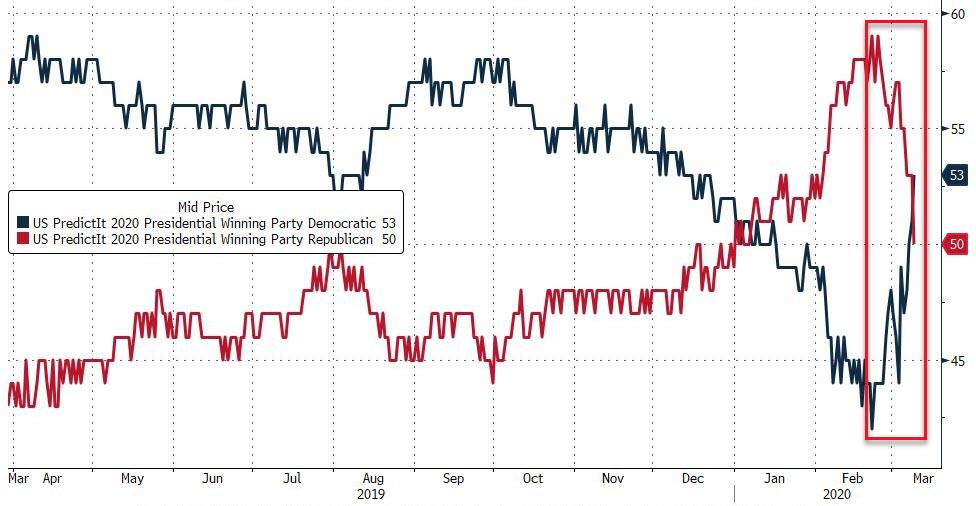

Trump Slams “Pathetic, Slow” Fed As Democrats Take Lead In 2020 Election Odds

It would appear that two things have sparked fear in President Trump’s heart this morning:

1) The prediction markets are now betting on a Democrat win in November…

2) And Trump knows that any meaningful fiscal policy juice to rescue stocks (oh yeah and the economy) will take weeks if not months if ever to achieve (and as we noted previously, may corner Trump into rolling back his corporate tax cuts for funding and thus hurt the markets further).

Both of which are hurting stocks… and thus Trump’s odds of a win.

Which is why he has fallen back on The Fed to save the world this morning with two ‘aggressive’ tweets, slamming Powell and his pals…

Our pathetic, slow moving Federal Reserve, headed by Jay Powell, who raised rates too fast and lowered too late, should get our Fed Rate down to the levels of our competitor nations.

They now have as much as a two point advantage, with even bigger currency help. Also, stimulate!

The Federal Reserve must be a leader, not a very late follower, which it has been!

Our pathetic, slow moving Federal Reserve, headed by Jay Powell, who raised rates too fast and lowered too late, should get our Fed Rate down to the levels of our competitor nations. They now have as much as a two point advantage, with even bigger currency help. Also, stimulate!

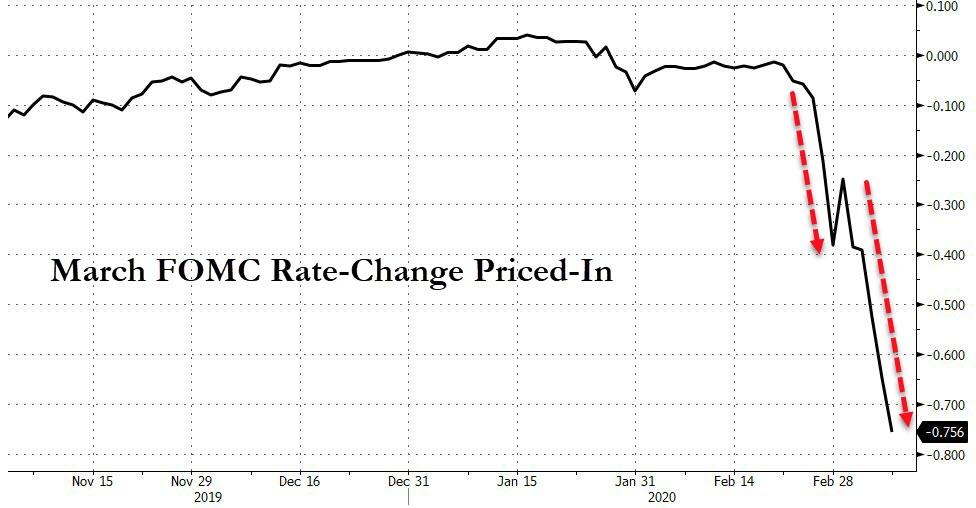

However, Trump is not alone in demanding more drastic actions – the market is screaming for 3 more rate-cuts next week when The Fed meets…

Will The Fed deliver? It would certainly be extremely unusual for The Fed to disappoint markets at this level of extreme… or to launch a huge jawbone program to ratchet down market’s expectations.

The impact of the “coronavirus,” and the shutdown of the global supply chain, will impact exports (which make up 40-50% of corporate profits) and economic growth.

The collapse in oil prices is deflationary and can spark a wave of credit defaults in the energy complex.

European growth, already weak, continues to weaken, and most of the EU will likely be in recession in the next 2-quarters.

Valuations remain at expensive levels.

Long-term technical signals have become negative.

The collapse in equity prices, and coronavirus fears, will weigh on consumer confidence.

Rising loan delinquency rates.

Auto sales are signaling economic stress.

The yield curve is sending a clear message that something is wrong with the economy.

Rising stress on the consumption side of the equation from retail sales and personal consumption.

I could go on, but you get the idea.

In that time, these issues have gone unaddressed, and worse dismissed, because of the ongoing interventions of Central Banks.

However, as we have stated many times in the past, there would eventually be an unexpected, exogenous event, or rather a “Black Swan,” which would “light the fuse” of a bear market reversion.

Over the last few weeks, the market was hit with not one, but two, “black swans” as the “coronavirus” shutdown the global supply chain, and Saudi Arabia pulled the plug on oil price support. Amazingly, we went from “no recessionin sight”, to full-blown “recession fears,” in less than month.

“Given that U.S. exporters have already been under pressure from the impact of the “trade war,” the current outbreak could lead to further deterioration of exports to and from China, South Korea, and Japan. This is not inconsequential as exports make up about 40% of corporate profits in the U.S. With economic growth already struggling to maintain 2% growth currently, the virus could shave between 1-1.5% off that number.

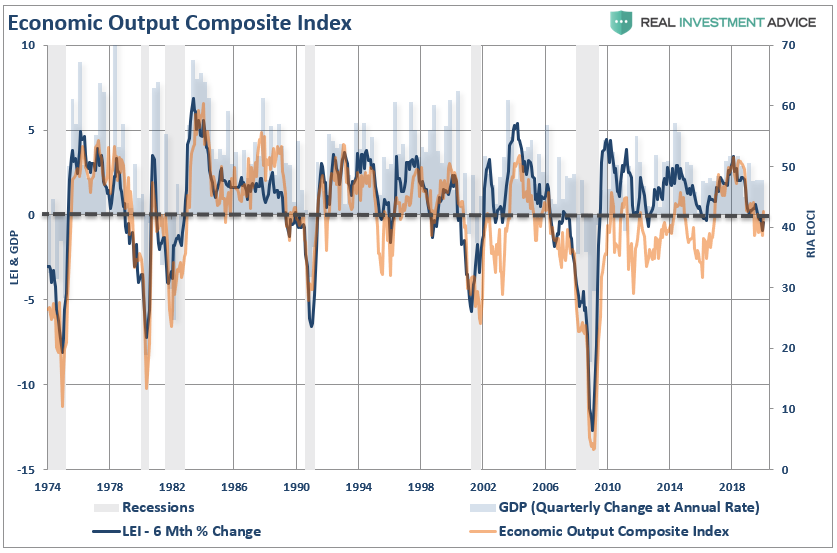

With our Economic Output Composite Indicator (EOCI) already at levels which has previously denoted recessions, the “timing” of the virus could have more serious consequences than currently expected by overzealous market investors.”

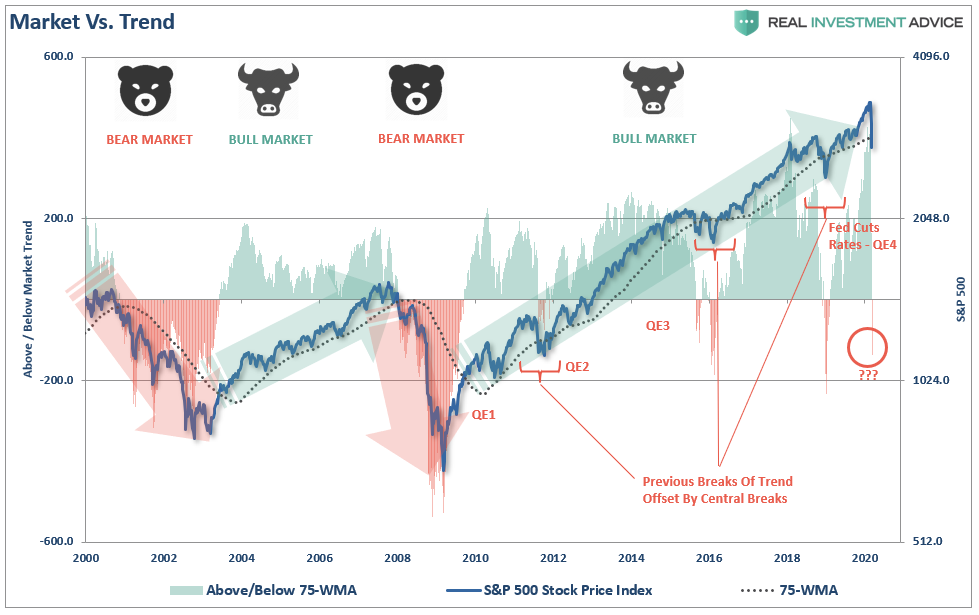

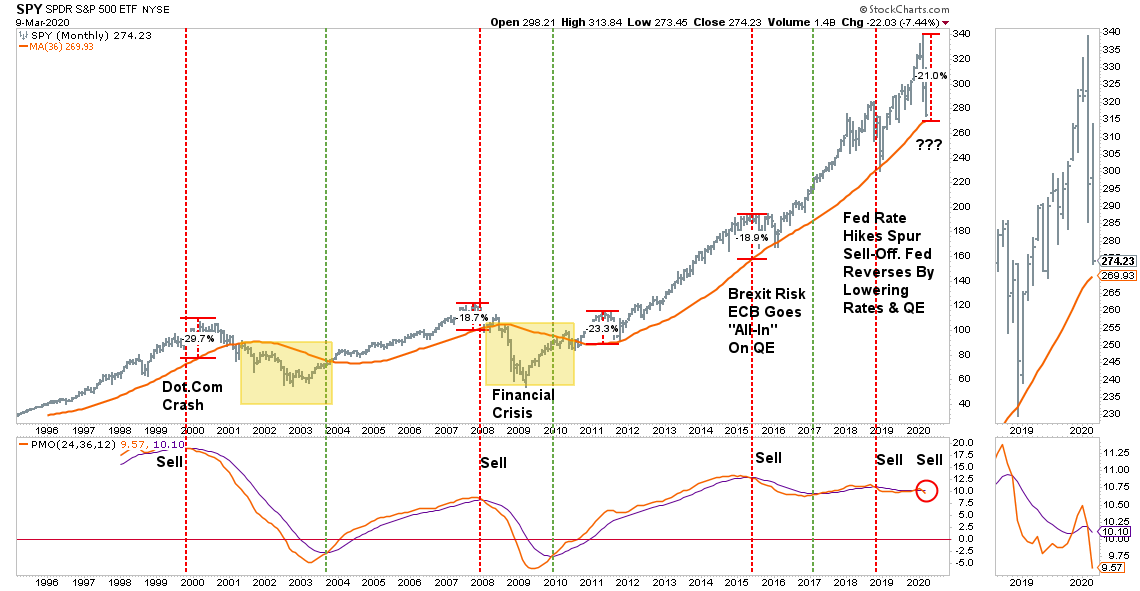

On The Cusp Of A Bear Market

Let me start by making a point.

“Bull and bear markets are NOT defined by a 20% move. They are defined by a change of direction in the trend of prices.”

There was a point in history where a 20% move was significant enough to achieve that change in overall price trends. However, today that is no longer the case.

Bull and bear markets today are better defined as:

“During a bull market, prices trade above the long-term moving average. However, when the trend changes to a bear market prices trade below that moving average.”

This is shown in the chart below, which compares the market to the 75-week moving average. During “bullish trends,” the market tends to trade above the long-term moving average and below it during “bearish trends.”

In the last decade, there have been three previous occasions where the long-term moving average was violated but did not lead to a longer-term change in the trend.

The first was in 2011, as the U.S. was dealing with a potential debt-ceiling and threat of a downgrade of the U.S. debt rating. Then Fed Chairman Ben Bernanke came to the rescue with the second round of quantitative easing (QE), which flooded the financial markets with liquidity.

The second came in late-2015 and early-2016 as the market dealt with a Federal Reserve, which had started lifting interest rates combined with the threat of the economic fallout from Britain leaving the European Union (Brexit). Given the U.S. Federal Reserve had already committed to hiking interest rates, and a process to begin unwinding their $4-Trillion balance sheet, the ECB stepped in with their own version of QE to pick up the slack.

The latest event was in December 2018 as the markets fell due to the Fed’s hiking of interest rates and reduction of their balance sheet. Of course, the decline was cut short by the Fed reversal of policy and subsequently, a reduction in interest rates and a re-expansion of their balance sheet.

Had it not been for these artificial influences, it is highly likely the markets would have experienced deeper corrections than what occurred.

On Monday, we have once again violated that long-term moving average. However, Central Banks globally have been mostly quiet. Yes, there have been promises of support, but as of yet, there have not been any substantive actions.

However, the good news is that the bullish trend support of the 3-Year moving average (orange line) remains intact for now. That line is the “last line of defense” of the bull market. The only two periods where that moving average was breached was during the “Dot.com Crash” and the “Financial Crisis.”

(One important note is that the “monthly sell trigger,” (lower panel) was initiated at the end of February which suggested there was more downside risk at the time.)

None of this should have been surprising, as I have written previously, prices can only move so far in one direction before the laws of physics take over. To wit”

“Like a rubber band that has been stretched too far – it must be relaxed before it can be stretched again. This is exactly the same for stock prices that are anchored to their moving averages. Trends that get overextended in one direction, or another, always return to their long-term average. Even during a strong uptrend or strong downtrend, prices often move back (revert) to a long-term moving average.”

With the markets previously more than 20% of their long-term mean, the correction was inevitable, it just lacked the right catalyst.

The difference between a “bull market” and a “bear market” is when the deviations begin to occur BELOW the long-term moving average on a consistent basis. With the market already trading below the 75-week moving average, a failure to recover in a fairly short period, will most likely facilitate a break below the 3-year average.

If that occurs, the “bear market” will be official and will require substantially lower levels of equity risk exposure in portfolios until a reversal occurs.

Currently, it is still too early to know for sure whether this is just a “correction” or a “change in the trend” of the market. As I noted previously, there are substantial differences, which suggest a more cautious outlook. To wit:

Downside Risk Dwarfs Upside Reward.

Global Growth Is Less Synchronized

Market Structure Is One-Sided and Worrisome.

COVID-19 Impacts To The Global Supply Chain Are Intensifying

Any Semblance of Fiscal Responsibility Has Been Thrown Out the Window

Peak Buybacks

China, Europe, and the Emerging Market Economic Data All Signal a Slowdown

The Democrats Control The House Which Effectively Nullifies Fiscal Policy Agenda.

The Leadership Of The Market (FAANG) Has Faltered.

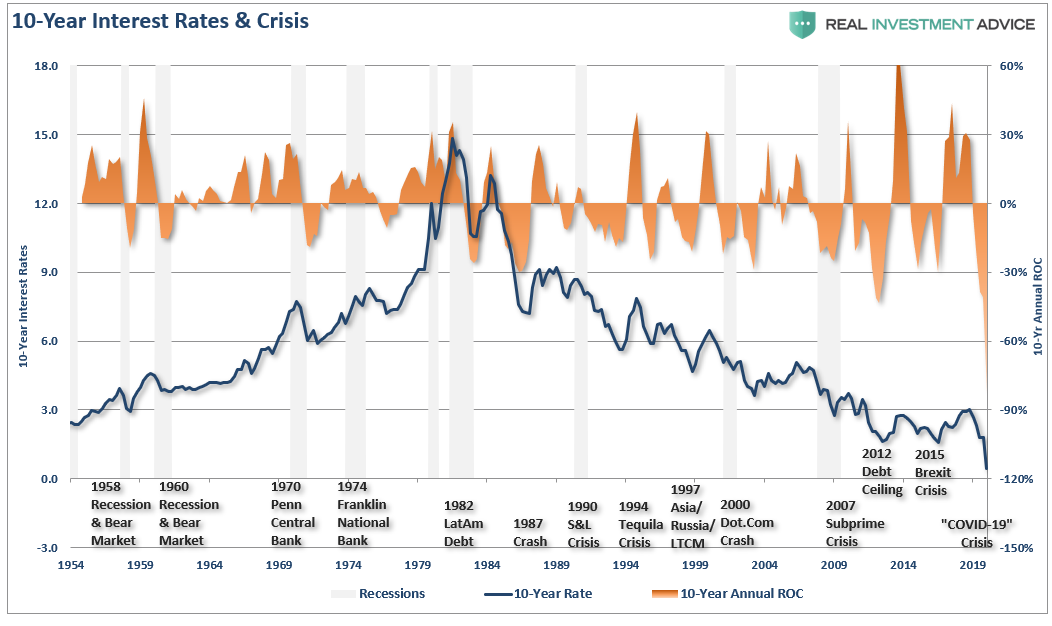

Most importantly, the collapse in interest rates, as well as the annual rate of change in rates, is screaming that something “has broken,” economically speaking.

Here is the important point.

Understanding that a change is occurring, and reacting to it, is what is important. The reason so many investors “get trapped” in bear markets is that by the time they realize what is happening, it has been far too late to do anything about it.

Let me leave you with some important points from the legendary Marty Zweig: (h/t Doug Kass.)

Patience is one of the most valuable attributes in investing.

Big money is made in the stock market by being on the right side of the major moves. The idea is to get in harmony with the market. It’s suicidal to fight trends. They have a higher probability of continuing than not.

Success means making profits and avoiding losses.

Monetary conditions exert an enormous influence on stock prices. Indeed, the monetary climate – primarily the trend in interest rates and Federal Reserve policy – is the dominant factor in determining the stock market’s major decision.

The trend is your friend.

The problem with most people who play the market is that they are not flexible.

Near the top of the market, investors are extraordinarily optimistic because they’ve seen mostly higher prices for a year or two. The sell-offs witnessed during that span were usually brief. Even when they were severe, the market bounced back quickly and always rose to loftier levels. At the top, optimism is king; speculation is running wild, stocks carry high price/earnings ratios, and liquidity has evaporated.

I measure what’s going on, and I adapt to it. I try to get my ego out of the way. The market is smarter than I am, so I bend.

To me, the “tape” is the final arbiter of any investment decision. I have a cardinal rule: Never fight the tape!

The idea is to buy when the probability is greatest that the market is going to advance.

Most importantly, and something that is most applicable to the current market:

“It’s okay to be wrong; it’s just unforgivable to stay wrong.” – Marty Zweig

There action this year is very reminiscent of previous market topping processes. Tops are hard to identify during the process as “change happens slowly.” The mainstream media, economists, and Wall Street will dismiss pickup in volatility as simply a corrective process. But when the topping process completes, it will seem as if the change occurred “all at once.”

The same media which told you “not to worry,” will now tell you, “no one could have seen it coming.”

The market may be telling you something important, if you will only listen.

Employees At Steve Cohen’s Point72 Told To Work From Home After Office Coronavirus Outbreak

If one of your hedge fund’s star portfolio managers catches the coronavirus during a fundraising visit or some other work-related outing (whether to Scores or a classier strip club), that’s one thing.

But if one of the gremlins in the back office exposes the entire floor to an economy-crushing virus, well, let’s just say that employee’s relationship with his coworkers – especially the money-makers (or losers) in the front office – is going to be a lot different once everybody’s back from their wintertime trip to the Hamptons.

According to no less an authority than Page Six editor Emily Smith, a back-office employee at Steve Cohen’s Point72 Asset Management working out of the firm’s NYC office in the newly built Hudson Yards is among the confirmed cases in New York State. Though the circumstances surrounding the exposure are unclear, all Point72 employees who have recently worked out of the 14th floor of the Hudson Yards office building where the mid-sized hedge fund is based have been instructed to work from home and self-quarantine for the next two weeks.

The employee in question is reportedly in “good health”, and has been working from home since early last week.

In a statement to the New York Post, a Point72 spokesperson said “The health and safety of our employees is a top priority, and we are taking the COVID-19 situation seriously.”

“In addition to working closely with state and local health departments, we are taking precautions and preventive measures to protect our employees and maintain a healthy work environment.”

“We have extensive business continuity plans in place to ensure the Firm can continue to operate.”

This comes as more Wall Street banks move their traders and salespeople to back-up sites in New Jersey. The number of confirmed cases in the Greater New York area climbed to more than 150 on Monday, tripling from roughly 50 on Friday.

Fortunately, it appears the firm’s office in Stamford, Conn. is still open.

We can now all look forward to seeing how the writers of “Billions” will spin this during the show’s inevitable seventh season.

There was no word on whether Cohen himself was exposed to the sick employee.

Trader: “Markets Want Proof, Not Promises” Of ‘Substantial’ Policy Relief

Authored by Richard Breslow via Bloomberg,

It is certainly safe to say it has been a day of low-conviction trading. Which certainly hasn’t meant small ranges. No wonder the CME is raising the margin requirements on some of its products. The day has a certain feeling of randomness. Which is odd, because it has become clearly directional.

Equities are up big. Crude is leaping. Bond yields have been moving up. And doing it with gusto. Ten-year Treasury yields opened higher, and then went another 10 basis points. Yet, as cash trading got underway in European government bonds, Treasuries found themselves exactly in the middle of the day’s range, waiting for additional instructions. It seems that when each center opens, traders just aren’t sure what the next group of investors is going to do with things. Or much of anything else, for that matter.

It would be nice to say that today will meaningfully reverse yesterday’s “overreaction.” And, by definition, it has partially done so, if you go by asset prices alone. But it’s still too early to declare victory. And that’s the case, not only from a technical point of view, but because the market, and citizenry for that matter, are now firmly in the “show me and I’ll believe it” camp. That’s both the good news and the bad news. It finally seems to be getting a response.

Japanese equities opened well down from the previous close only to jump higher on comments by Prime Minister Shinzo Abe that his government would be working closely with the BOJ to strengthen the economy. People want to hear fiscal, not monetary, to get sustainably excited. Markets had the expected reaction. The yen weakened almost 2 1/2 big figures. And subsequently gave one of them back. The market now seems unsure what it wants to do from here. It isn’t that it wasn’t welcome news. Frayed nerves were soothed according to one observer. But nothing is going to lastingly change until they come up with the goods.

Forward guidance and promises are only going so far these days.

The BOJ has said all the right things, but has limited room. And what they are likely to try again at their next policy meeting hasn’t exactly kick-started things. The government, itself, isn’t quick to act. The talk overnight was for a stimulus package in April or May. The world isn’t in the mood to consider patience a virtue. And, unilateral currency intervention is unlikely to accomplish much, but should USD/JPY approach 100, expect a lot of talk about it. Which will be fodder for market rumors and jumpy price action. As an aside, the Europeans have little interest in the euro taking off, either.

In the U.S., hopes for fiscal stimulus has been a game changer after Monday’s slide. It did wonders for European markets, as well. We can debate all we want about the best ways to deliver it. A legitimate debate. But too picky for traders. At least for the moment. The powers that be can go micro or macro. Targeted or broad brush. The market, at this point, just wants proof that they are capable of action. Stay tuned. It sounds good, now we’ll see how the politics work.

If you want to get a sense of how desperate the market is to see proactive governments taking action, watch Italy. The news there is terrible. Lock-downs have spread to the entire country. Although, compliance is a bit of an issue. Their country is probably in recession. But the announcement of a possible increase in the already proposed stimulus package got a very favorable reaction.

I’m cherry-picking, but it is the only bond market on my launchpad that is green on the day.

Yesterday, one expert after another warned of recessions and market meltdowns. Serious economists and CIOs talking scary stuff. I seriously doubt that if we brought them back today, they will have changed their analysis. And not out of stubbornness. They, too, need to be convinced. There is a lot at stake. Traders will do what they have to and that is probably going to mean chasing risk assets higher. One day on, the next off. But, at the risk of offending, even a healthy bounce in the S&P 500 doesn’t mean all is yet well with the world. Make them show you.

Vladimir Putin To Stay On As President? MPs Discuss Removal Of Term Limits

In a somewhat surprising turn of events, Russian president Vladimir Putin said this morning that a suggestion by ruling-party lawmakers that would see his presidential tenure reset, thus allowing him to run again in 2024, should be supported by citizens and adopted by the Constitutional Court.

“Putin needs to be there — in case something goes wrong” amid global political and economic turbulence, Valentina Tereshkova, a respected lawmaker who was also the first woman in space, told the State Duma in a speech shown on state TV during debates on a constitutional overhaul put forward by the Kremlin.

“If the situation requires it and, most importantly, if the people want it, to put in law the possibility for the current president to be re-elected to this position is already in accordance with the updated constitution.”

Interfax news service reported that in his address to the State Duma, the parliament’s lower house, Putin said:

“I believe and am deeply convinced that a strong presidential power is absolutely necessary for our country.”

Somewhat ironically, Putin also stressed that the public should have guarantees that elections – including presidential elections – are open and competitive.

As Bloomberg reports, Putin has previously rejected calls to change the presidential term limit, including as recently as last week, and has not indicated any support for early parliamentary elections. While the fact that both proposals came from prominent members of the ruling party suggests they may have Kremlin support, it may also be that the president is using them as trial balloons that are designed to be rejected when he speaks to lawmakers.

Putin has said the plan is aimed at modernizing the basic law and that he plans to observe current term limits, which prevent him from running again. But the overhauls, abruptly announced in January, are widely seen as an effort to create options for Putin to retain control even after he steps down as president.

The removal of term limits and early-vote proposal would require constitutional amendments.

The Kremlin has set a national ballot to approve the constitutional changes for April 22.

Will Vlad join Xi as “Emperor for Life”… and will Trump be jealous?