Hong Kong Researchers Have Developed A Coronavirus Vaccine, There Is Just One Catch

With scientists from around the world scrambling to be the first to market with a vaccine for the Chinese coronavirus pandemic, Hong Kong researchers said today they have already developed a vaccine for the deadly Wuhan diseases, although there is a catch: the vaccine will not be commercially available for months, if not a year, as it would “take months” to test the vaccine on animals and at least another year to conduct clinical trials on humans before it was fit for use.

That’s a problem, because at the current exponential rate of propagation, the virus may have infected several billion people by then.

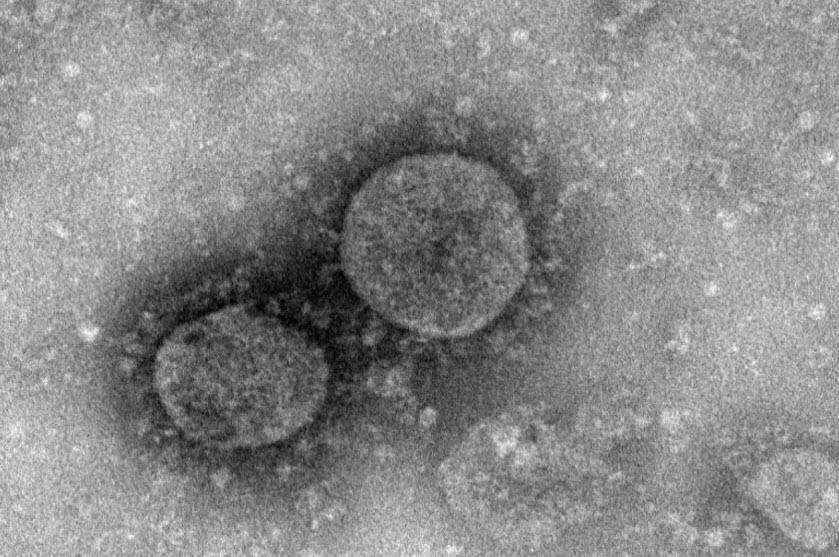

According to SCMP, as scientists in mainland China and the United States were racing to produce a vaccine for the new coronavirus, infectious diseases expert Professor Yuen Kwok-yung, chair of infectious diseases at the University of Hong Kong, revealed that his team was working on the vaccine and had isolated the previously unknown virus from the city’s first imported case.

“We have already produced the vaccine, but it will take a long time to test on animals,” Yuen said, without giving a specific time frame on when it would be ready for patients.

Professor Yuen Kwok-yung did not give a time frame on when the vaccine would be ready. Photo: SCMP

Meanwhile, with the virus having already mutated once becoming “more easily spreadable” among humans according to Chinese officials, by the time the virus is finally tested, the prevalent phenotype will likely be vastly different from the one the HK researcher is currently operating on.

How did the HK team come up with such a quick vaccine? HKU researchers based it on a nasal spray influenza vaccine previously invented by Yuen’s team. Researchers modified the flu vaccine with part of the surface antigen of the coronavirus, meaning it could prevent influenza viruses as well as the new coronavirus, which causes pneumonia.

Could Yuen’s team be just a tad optimistic about the relevance of their product? Most likely: on Monday Chinese mainland media quoted Chinese infectious diseases expert Li Lanjuan who said saying a vaccine targeting the coronavirus was only now being developed and could be made in around a month at the earliest; testing would then lead to further months of delays.

“If the vaccine appears effective and safe in a number of animal species, it will go into clinical trials on humans. This takes at least one year even if expedited,” Yuen said, adding that the approach taken by the mainland side to develop a vaccine would lead to a major complication, in which people who were vaccinated might develop a more severe disease if exposed to the virus. He said such a reaction for coronavirus had been recorded in reports.

Coronaviruses are a large family of viruses causing illnesses ranging from the common cold to more severe diseases such as Middle East respiratory syndrome (Mers) and severe acute respiratory syndrome (Sars). Meanwhile, Xinhua reported that Shanghai East Hospital of Tongji University had urgently approved a project for the development of a vaccine targeting the novel virus.

The vaccine would be co-developed by the hospital and Stemirna Therapeutics, a Shanghai-based biotechnology company. Company CEO Li Hangwen said no more than 40 days would be needed to manufacture vaccine samples, which would then be sent for tests and brought to clinics “as soon as possible.” Here’s the problem: assuming the number of infected people continues to roughly double every day… well, we leave it to readers to calculate how many will be sick in over a month if we start with today’s 4,500 infected baseline.

Impeachment Moves Into Q&A Phase; Here’s What To Expect

With President Trump’s defense team set to wrap up their third and final day of opening arguments in his Senate impeachment trial, and a debate over witnesses raging outside the chamber, Senators are preparing to move into the next phase of the proceeding where they will spend 16 hours asking questions of both the Democratic House impeachment managers and President Trump’s defense team.

And as noted by The Hill, the Q&A round will “lead to plenty of tea-leaf reading as observers scrutinize what the questions reveal about the senators considering the merits of the case.”

There won’t be many limits on what can be asked, as a resolution passed last week on guidelines merely states “Upon the conclusion of the president’s presentation, senators may question the parties for a period of time not to exceed 16 hours.” That said, the questions will be filtered through party leadership, which will then send the questions to Chief Justice John Roberts, will read them. Senate Majority Leader Chuck Schumer (D-NY) says that he’ll take a hands-off approach to narrowing down questions, though be may combine similar submissions.

“The only thing we might try to do is make sure that the questions — if 10 people want the same question, that we ask it once, OK, in the name of the 10,” said Schumer, adding that there would be “all kinds of different questions” and a “whole lot” of them.

Republicans will have their questions processed by Majority Leader Mitch McConnell (R-KY).

Close attention will be paid to Democrats who might vote against impeachment, such as Sen. Joe Manchin (D-WV), who has not revealed which direction he’s leaning in.

“I’m working with my staff right now [based on] things we have heard,” said Manchin.

Similarly, Sen. Doug Jones (D-AK) – another potential “no” vote, says he has a ton of questions for both sides, and would “try to pair them down.”

“You know, there’s 100 of us [and] everybody’s got questions, so we’ll see how it goes,” he said.

Senators filed more than 150 questions during the 1999 Clinton impeachment trial, using two days to work through the pile. Only one question in that trial came from a bipartisan pair of senators: Sens. Susan Collins (R-Maine) and Russ Feingold (D-Wis.).

It’s unclear if there will be a bipartisan question submitted during Trump’s trial.

Manchin opened the door to submitting a bipartisan question this week, noting that “if there was going to be a bipartisan question, I’m more than open to that.”

“I’m happy to work with my Republican colleagues,” he added.

Jones, however, appeared to shoot down working on questions with his colleagues.

“No,” he said, asked about the possibility. “These are my questions … and I consider myself pretty bipartisan.” –The Hill

“I’ve taken a lot of notes — it takes me back to law school,” said Sen. Lisa Murkowski (R-AK), adding “Along the way I made little asterisks and notations about what I want to see, what questions I still have.”

Or, maybe she’ll just ask whatever Dianne Feinstein wants her to ask.

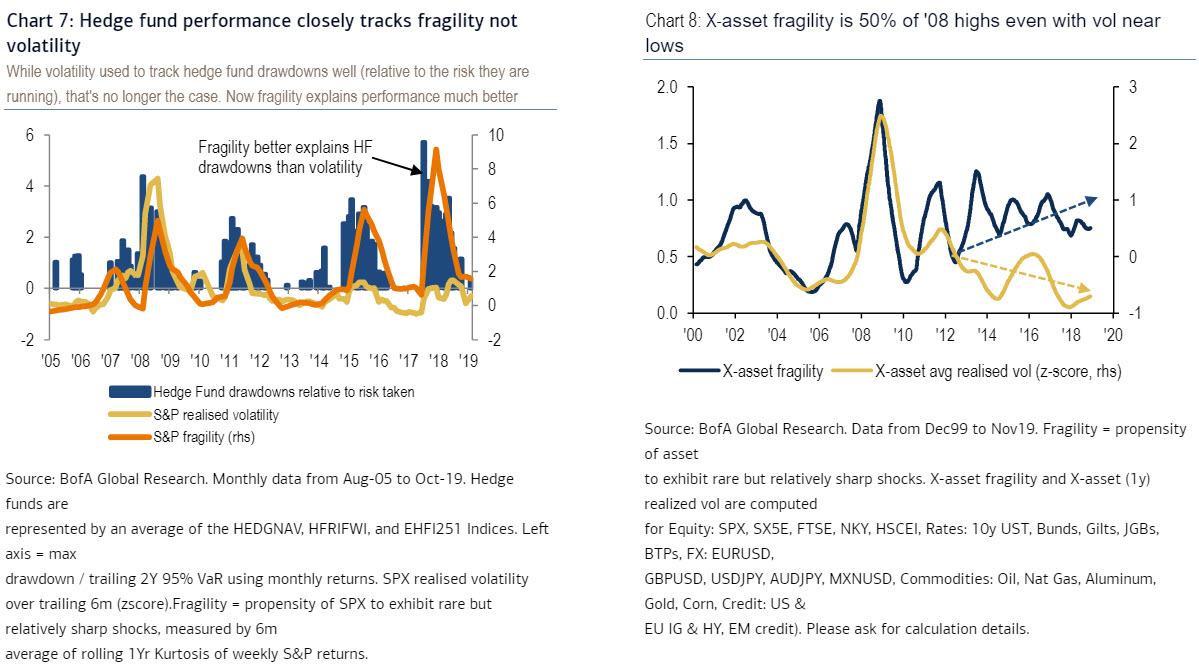

Central Banks Have Made Markets So Fragile, Liquidity Premiums Are Now Negative

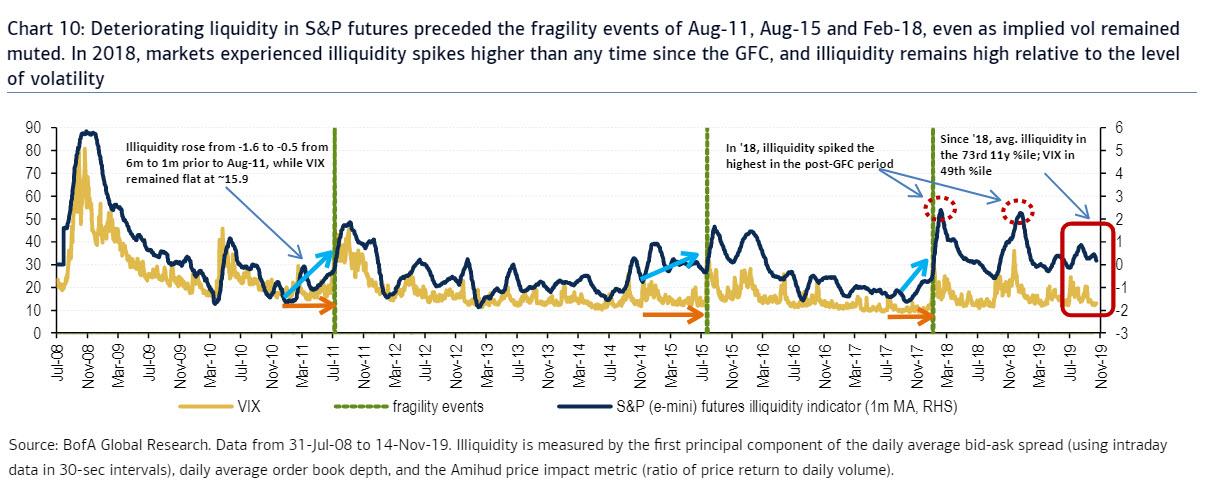

Back in late December, when the market was melting up every single day with zero regard for economic data or newsflow, we pointed out something ominous: the world’s most liquid stock market, the S&P500, was now as (il)liquid as it was during the 2008 financial crisis.

As BofA’s Benjamin Bowler wrote, while market liquidity generally correlated with volatility, in recent years, it was progressively deteriorating despite near record low levels on the VIX. According to BofA calculations, average “illiquidity” for S&P e-mini futures since 2018 has been in its 73rd% since 2008. Historically, the period when markets were less liquid was primarily during the ’08 crisis when the VIX was north of 40.

It is also noteworthy that illiquidity rose ahead of the sharp fragility events of Aug-2011, Aug-2015, and Feb-2018, while implied vol remained muted until very near the selloffs, suggesting that VIX no longer reflects prevailing market stress, and confirms what Morgan Stanley said in late 2019, namely that Fed actions now directly seek to lower marketwide volatility.

Why does this matter?

Because as BofA summarized one month ago, the fact that liquidity seems to be progressively deteriorating over time suggests that market fragility is getting worse, particularly as long as crowding remains a problem and liquidity providers are incentivized to pull back from liquidity provision in times of stress.

Wait, what fragility?

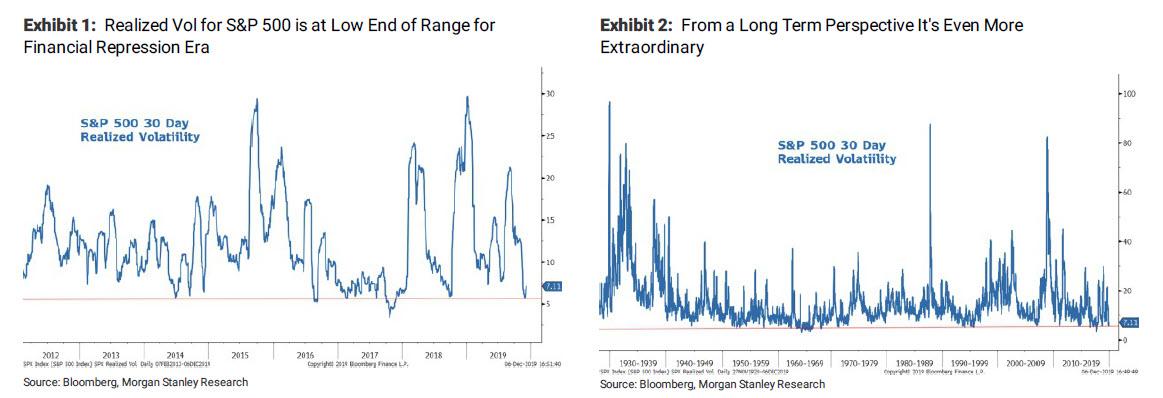

While we have extensively discussed the growing fragility of the market, manifesting itself in ever more frequent liquidity “air pockets” and “flash crashes”, here is a quick reminder, once again courtesy of Bank of America, which writes that despite the direct suppression of volatility by central banks, “markets have remained highly fragile in recent years.”

The left chart below shows that BofA’s fragility measure for the S&P 500 exceeded global financial crisis (GFC) levels during 2018 despite volatility remaining at or below its longer-run average. In fact, as the chart on the right shows, fragility across 25 markets covering five asset classes has been historically elevated vs. volatility in recent years.

This matters because as Bowler notes, it is fragility – not volatility – that is a better measure of the risk that active managers are exposed to. In this vein, BofA believes that high market fragility in the past few years (which corresponded to relatively large hedge fund drawdowns) “is driven by a combination of investor crowding in an alpha starved market and the increasingly fickle liquidity provision from high frequency traders (HFTs).“

Fast forward to the end of January when we got a very clear example of what happens when fragility and black swan (or perhaps black bat) events collide.

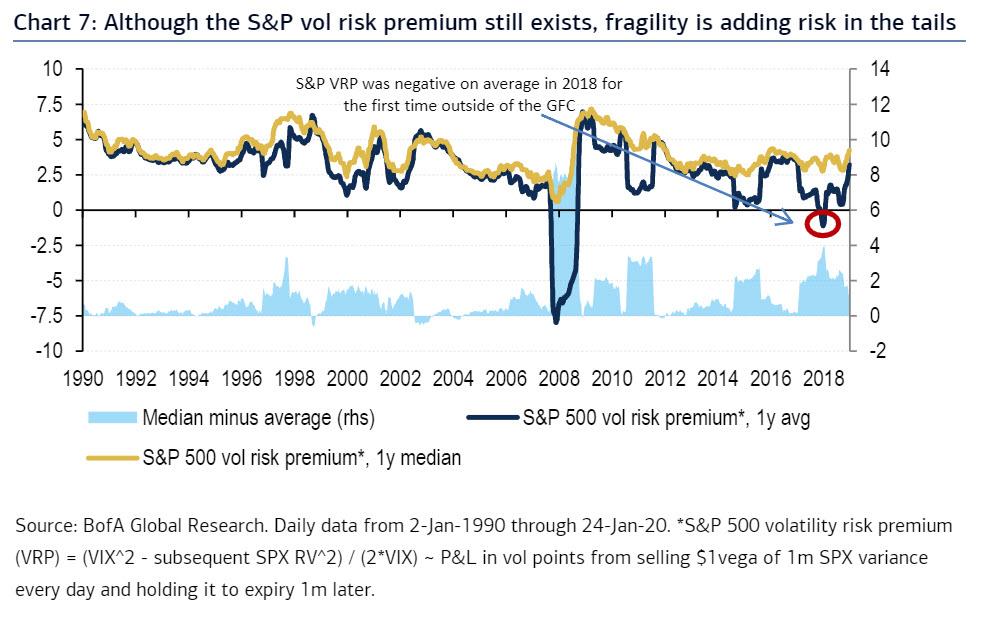

As Bowler writes today, “fragility risk remains real – as seen from the -3.2 stdev drop in the S&P on 27-Jan following a near-record Sharpe of 6.3 over the prior 3m” and is driving a paradigm shift in harvesting the equity volatility risk premium (VRP).

The S&P volatility risk premium – long one of the most persistent across derivatives markets – has been especially hard hit, turning negative on average in 2018 for the first time outside of the GFC and struggling to revive itself in 2019.

BofA attributes this to:

(i) a supply-demand shift in S&P options usage (towards more robust supply from yield-starved investors and weaker hedging demand from under-positioned equity investors), as well as

(ii) high market fragility (i.e., large dislocations in price relative to the prevailing level of volatility), which has altered the distribution of the SPX VRP in recent years by pulling its average well below its median

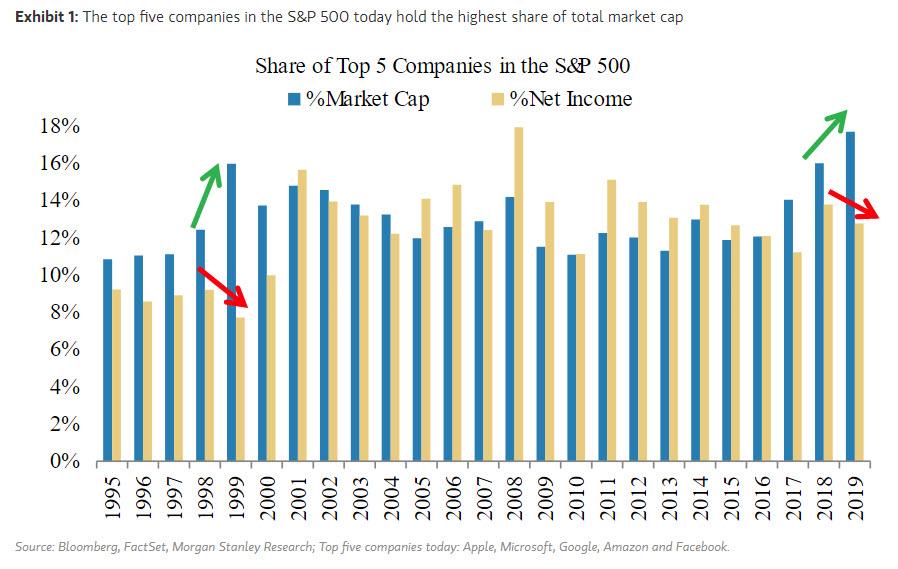

Looking to 2020, more bullish US equity positioning (as the Fed increasingly pulled investors back into the recent rally where there wasn’t a single +/-1% market swing in 70 days ) could restore healthier demand for S&P hedges in sell-offs, according to Bowler. However, in yet another irony, more liquid markets now tend to perversely experience more acute fragility events, as they attract a broader array of trading activity. In other words, superior liquidity equates to higher crowding risk, which translates to greater realized fragility in markets today. One needs to only recall the “other 1%”, namely that the top 5 companies in the S&P500 make up a record 18% of total market cap, more than the dot com era, to get a sense of what’s going on.

Alas, with the S&P being the most liquid equity market in the world, “and to the extent that central bank-induced financial repression continues to incentivize yield-starved investors to sell short-dated S&P options/vol for income, headwinds to the SPX VRP likely remain”, according to BofA.

What’s the remedy?

According to BofA’s chief derivatives strategist, beyond adopting more defensive approaches to VRP harvesting, investors should look to diversify away fragility risk. Sizing is also critical to the risk management of short volatility positions, and applying more conservative sizing schemes to assets prone to fragility shocks can help limit the contribution of such assets to broader cross-asset risk premia portfolios.

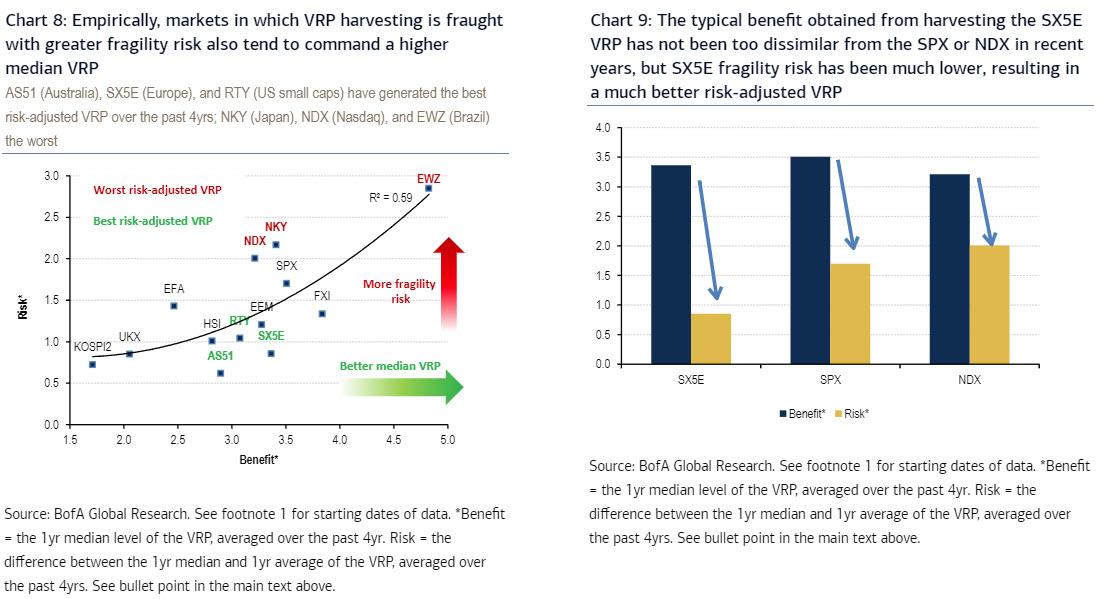

What does this mean in practical terms? While the S&P does not rank at the very bottom of the screen, it still ranks among the worst (and sits above the regression line in Chart 8). Importantly, what makes the S&P/Nasdaq rank so poorly vs. SX5E is not the benefit side of the equation, but instead the fragility risk (see Chart 9). Indeed, the Stoxx 50 has the second-lowest fragility risk metric among the markets considered (i.e., selling vol on SX5E has been one of the safest opportunities for vol sellers among popular global equity indices over the past 4 years; see Chart 10). Hence, it is ironic that selling vol in markets which some would consider as having better fundamentals (e.g., US large caps or US Tech) has become a worse investment proposition than selling vol on markets with the some of the worst fundamentals (e.g., European equities or US small caps).

In conclusion, and consistent with the notion of a negative liquidity premium, whereby more liquid markets like the S&P are ironically more vulnerable to fragility shocks, BofA finds that selling volatility on markets with worse fundamentals – e.g., European equities (SX5E) – has perversely become a better investment proposition than selling volatility on US large caps. Paradoxically, VRP “harvesting” on the Stoxx 50 has never been safer vs. the S&P or Nasdaq over the past 20 years. This leads BofA to conclude that “S&P vol sellers should efficiently diversify away fragility risk.”

Of course, they won’t and instead the crowding will continue until one day the market crashes and the Fed is unable to spark the BTFD rebound, resulting in what will likely be the first ever market-wide halt that will last for a long time until clearing prices based on fundamentals and not liquidity are rediscovered far, far lower.

Watch Live: Trump Unveils ‘Deal Of The Century’ Mideast Peace Plan With Netanyahu

President Trump and Israeli Prime Minister Benjamin Netanyahu will be delivering joint remarks from the White House, scheduled for noon EST on Tuesday.

TRUMP PEACE PLAN CALLS FOR 2 STATES, ISRAEL AND PALESTINE: AP

Trump:

“I was not elected to do small things or shy away from big problems”

“This vision for peace is fundamentally different from past proposals”

80 pages are the “most detailed proposal every put forward by far”

Trump touted his experience as a “Deal-maker” and that what’s being proposed is a win-win “two-state solution”

Both Netanyahu and Gantz willing to endorse vision as basis for direct negotiations with Palestinians. A joint US-Israeli committee will work on implementing conceptual map.

US will work toward recognizing contiguous territory within the Palestinian state “when conditions for statehood are met”

“Jerusalem will remain Israel’s undivided capital”… “But that’s no big deal because I’ve already done that for you…”

“We will not allow a return to… relentless bloodshed… we will never allow Israel to compromise its security.”

“I want this deal to be a great deal for the Palestinians. After 70 years this could be the last opportunity” for Palestinians to have their own state.

Palestinian capital in East Jerusalem where the US “will proudly open a US Embassy”…

No Israelis or Palestinians will be displaced from their homes. Palestinians’ GDP will triple over next decade if peace plan conditions implemented.

Yesterday the president met with both Israeli Prime Minister Benjamin Netanyahu and Blue and White party rival Benny Gantz separately at the White House. Both have briefly paused campaigning ahead of Israel’s March 2 elections.

Trump had sought to assure the press that the Palestinians would “ultimately” come around to giving their support, though statements of Palestinian leadership have made this highly doubtful.

“I think it might have a chance,” he said Monday. Trump touted that both Netanyahu and Gantz “like very much” what they’ve heard of the plan thus far. President Trump described the plan has having been “many, many years in the making”.

The administrations last big move, albeit deeply controversial, was to relocate the US Embassy in Tel Aviv to Jerusalem in recognition of it as the official Israeli capital in 2018.

Netanyahu’s arrival at the White House yesterday, via Washington Post.

“We’ll see what happens,” Trump said. “We have something that makes a lot of sense for everybody,” the president added after describing that most people think of the prospect for Israeli-Palestinian peace as something impossible.

Despite Trump’s measured optimism, Palestinian Authority leaders as well as Hamas have previously repeatedly said the plan would be dead on arrival.

For its part the Palestinian side has not been invited to Washington, and even threatened over the weekend to withdraw from key provisions of the 1993 Oslo Accords.

Lockdowns are for those with no money, not the wealthy.

Beijing Departures

25 flights on a page

5 pages for the 00:00-06:00 departures

26 pages for 06:00-12:00 departures

22 pages for the 12:00-18:00 Beijing departures

20 pages for the 18:00-00:00 departures

That’s about 1825 flights out of Beijing.

Wuhan Departures Today

How easy is it to escape Wuhan?

You can still catch a flight from Wuhan to Anchorage, Tokyo, Seoul, Bangkok, Singapore, Taipei and countless cities in China including Beijing and Shanghai.

There are 8 pages of flights out of Wuhan today. That’s about 200 flights. Most of the flights are within China, but that hardly stops containment.

In the 00:00-06:00 slot one flight left for Anchorage. Another left for Bangkok, Thailand and another went to Tokyo.

In the 06:00-12:00 slot, two planes left for Tokyo and three to Hong Kong.

In the 12:00-18:00 slot, three planes left for Seoul, South Korea and two went to Taipei, Taiwan.

In the 18:00-00:00 slot, one plane went to Bangkok , three went to Taipei, three went to Hong Kong,

Wuhan Departures Tomorrow

Tomorrow, there are four flights from Wuhan to Singapore, three to Taipei, two to Bangkok, three to Tokyo, three to Paris, and six to Hong Kong, three to San Francisco,

The rest headed for other parts of China including Beijing. Then where? Here are international possibilities from Beijing.

US and Canada Destinations From Beijing Today

New York, Boston, Los Angeles, San Francisco, Detroit, Anchorage, Newark, Vancouver

European Destinations From Beijing Today

Amsterdam, Istanbul, Paris, Prague, Milan, Moscow, Frankfort, Munich, Athens, Barcelona, Warsaw, Rome, Stockholm, London

Other International Destinations From Beijing Today

Sydney, Singapore, Melbourne, Abu Dahabi, Manila, Auckland, Hong Kong, Seoul, Macau, Osaka, Bangkok, Ho Chi Minh, Taipei.

WHO is the World Health Organization. Add to that list, the Center for Disease Control (CDC), Chinese officials, and other US health officials.

The sane thing to do was ban all flights from China days ago.

But more landed today and far more are scheduled for tomorrow. And that’s just from two cities. I did not check departures from Shanghai or other large Chinese cities.

Many of you know Chris Martenson from his economic website, Peak Prosperity.

But even those who do know him, may not be aware that his background includes a PhD in pathology.

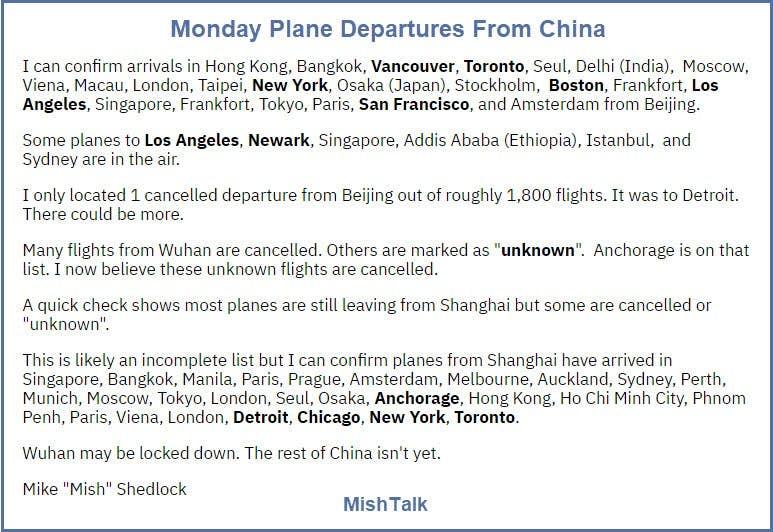

I can confirm arrivals in Hong Kong, Bangkok, Vancouver, Toronto, Seul, Delhi (India), Moscow, Viena, Macau, London, Taipei, New York, Osaka (Japan), Stockholm, Boston, Frankfort, Los Angeles, Singapore, Frankfort, Tokyo, Paris, San Francisco, and Amsterdam from Beijing.

Some planes to Los Angeles, Newark, Singapore, Addis Ababa (Ethiopia), Istanbul, and Sydney are in the air.

I only located 1 cancelled departure from Beijing out of roughly 1,800 flights. It was to Detroit. There could be more.

Many flights from Wuhan are cancelled. Others are marked as “unknown“. I now believe these unknown flights are cancelled.

I can confirm planes from Shanghai have arrived in Singapore, Bangkok, Manila, Paris, Prague, Amsterdam, Melbourne, Auckland, Sydney, Perth, Munich, Moscow, Tokyo, London, Seul, Osaka, Anchorage, Hong Kong, Ho Chi Minh City, Phnom Penh, Paris, Viena, London, Detroit, Chicago, New York, Toronto.

Wuhan may be locked down. The rest of China isn’t yet.

Avenatti Googled “Insider Trading” And “Nike Puts” Before Attempting To Shake Down Sneaker Giant

No, this is not from the Onion.

Somehow, before driving his firm and himself into near bankruptcy due to his insatiable lifestyle addiction, Michael Avenatti was once a respected California lawyer.

A respected California lawyer who clearly had no qualms googling things like “Insider trading” and “Nike puts” before allegedly attempting to extort the world’s biggest manufacturer of athletic shoes. Even if he wasn’t arrested for the threats, the SEC would have almost certainly nailed him if he tried to trade on his own press conference.

With Avenatti’s trial set to begin next week, prosecutors are arguing that the judge should admit a history of Avenatti’s google searches, which they argued offer critical insights into Avenatti’s state of mind while he was concocting the so-called extortion plot (Avenatti originally partnered with another celebrity lawyer, Mark Geragos, according to media reports. However, Geragos was never charged in the scheme).

According to Bloomberg, prosecutors informed US District Judge Paul Gardephe about the emails on Monday, and are now trying to convince the judge to let the jury see the evidence. However, the judge has raised some hackles with their argument, pointing out that Avenatti is not being tried for insider-trading related charges.

Despite being re-arrested two weeks ago for violating his bail terms by – what else? – trying to conceal money from the government, Avenatti appeared in court Monday wearing a real suit (instead of an orange jumpsuit) for his pre-trial hearing. Opening statements in the trial could start as soon as Tuesday.

We’re certain Avenatti’s lawyers will use every trick in the book to try to redirect the jury’s focus to Nike’s misdeeds, rather than Avenatti’s allegedly illegal behavior. They’ve already leaked information about texts showing Nike lawyers mocking the FBI to the press, suggesting that the company’s wrongdoing will be a cornerstone of their defense.

But judge Gardephe said Monday he won’t allow the trial to “involve an exploration” of whether Nike sought to corrupt youth basketball. But the lawyers can argue to the jury that Nike’s intentions when they approached the FBI about Avenatti were less than pure.

Nike argued in a filing that Avenatti was simply trying to “put the government’s and Nike’s conduct on trial” because he can’t dodge the video and audio evidence of his demands on the company.

“He intends to misdirect the jury – pointing their attention anywhere but on his own conduct – in the hope that at least one of them will be confused by evidence that is legally irrelevant and factually inaccurate,” Nike said.

Responding to this, the “creepy porn lawyer’s” legal team described the google searches mentioned above as a “red herring.”

“The obvious implication is that Mr. Avenatti illegally traded in Nike stock based upon information obtained from Coach Franklin,” the defense lawyers said in a Jan. 24 court filing. “That did not happen, the government has no evidence that it did, and Mr. Avenatti is not charged with insider trading.”

Sure, he didn’t trade on his information. But we’d off an analogy to illustrate what these google searches represent: It’d be like if a man accused of attempted murderer had googled “best strategies for disposing of a body” before the assault.

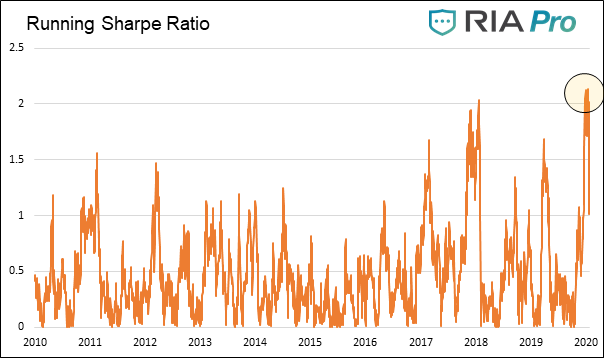

Over the last few weeks, we have discussed the outsize market advance driven by the Fed’s massive liquidity injections into the market. As we discussed with our RIAPRO subscribers (30-day RISK FREE Trial) we stated:

“If it appears to you that the recent rally is an anomaly, your thoughts do not deceive you. The graph below shows that recent returns divided by annualized volatility (risk) have been running higher than at any time since the financial crisis.

This standard calculation of return per unit of risk is technically called the Sharpe Ratio. The ratio has been sitting around 2.0 for most of January. To put that into context, the current reading is about 4 sigma (standard deviations) from the norm, an event that should statistically occur in one day out of every 43 years. Since January first, there have been 5 daily readings that were greater than 4 sigmas!”

Not surprisingly, due to that extreme reading the correction on Monday was the largest we have seen since the Federal Reserve started intervening into the financial market in mid-October of last year.

This analysis, along with several other posts over the last couple of weeks, detailed our concerns about inherent market risk and why we reduced portfolio exposure a couple of weeks ago. To wit:

“On Friday, we began the orderly process of reducing exposure in our portfolios to take in profits, reduce portfolio risk, and raise cash levels.

In the Equity Portfolios, we reduced our weightings in some of our more extended holdings such as Apple (AAPL,) Microsoft (MSFT), United Healthcare (UNH), Johnson & Johnson (JNJ), and Micron (MU.)

In the ETF Sector Rotation Portfolio, we reduced our overweight positions in Technology (XLK), Healthcare (XLV), Mortgage Real Estate (REM), Communications (XLC), Discretionary (XLY) back to portfolio weightings for now.

The Dynamic Portfolio was allocated to a market neutral position by shorting the S&P index itself.

Let me state clearly, we did not ‘sell everything’ and go to cash. We simply reduced our holdings to raise cash, and capture some of the gains we made in 2019. When the market corrects we will use our cash holdings to either add back to our current positions, or add new ones.”

While I received a lot of emails and comments questioning why would we“sell out of the market” and “go to cash,” such was NOT the case. We did raise our cash position from 5% to 12%. Just prior to increasing cash, we had previously added defensive exposure in fixed income, gold, gold miners, and REIT’s. However, we still maintain the majority of our long equity exposures currently.

You Can’t Time Market Corrections

At the time we made these changes, it appeared we were clearly wrong as the market continued to grind higher. As Howard Marks once quipped:

“Being early, even if you are right, is the same as being wrong.”

However, from a portfolio management, and more particularly, a “risk mitigation” view, our job isn’t necessarily to hit the exact tops or bottoms, just to provide a cushion against losses.

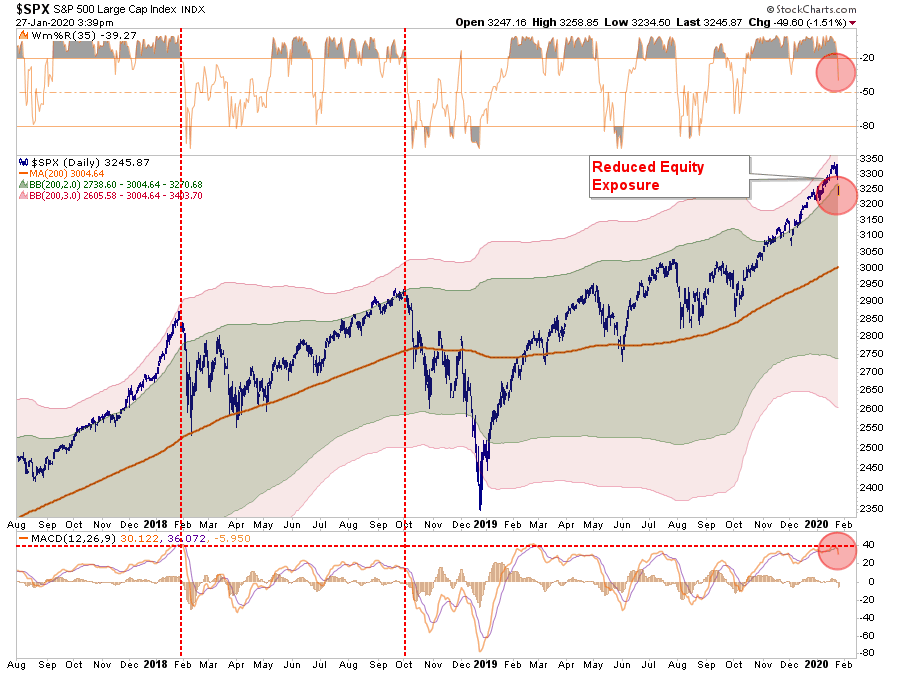

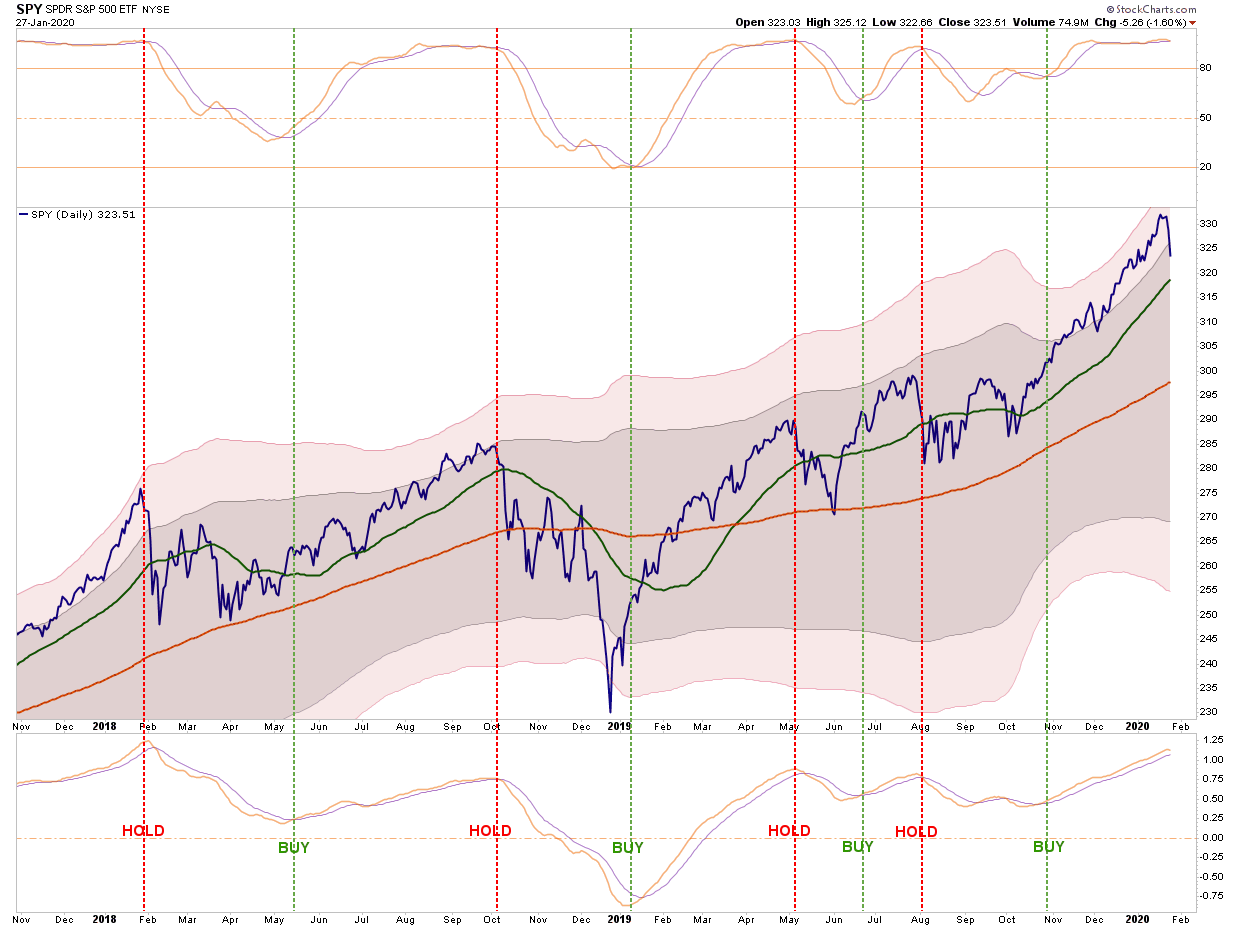

During the last couple of weeks, we have noted the extreme overbought, overly bullish, and over complacent conditions of the market. Here is an updated chart of the S&P 500 from two weeks ago when we discussed taking profits.

With the markets pushing into 3-standard deviations above the 200-day moving average, it was only a function of time before a correction occurred. Therefore, while we were early taking profits, the end result is it reduced portfolio risk against a pending correction. As I wrote then:

“While the markets could certainly see a push higher in the short-term from the Fed’s ongoing liquidity injections, the gains for 2020 could very well be front-loaded for investors.

Taking profits and reducing risks now may lead to a short-term underperformance in portfolios, but you will likely appreciate the reduced volatility if, and when, the current optimism fades.”

When discussing portfolio management, it is often suggested that you can’t “time the market.”

That statement is correct.

You can not effectively, and repetitively, get “in” and “out” of the market on a timely fashion. I have never suggested that an investor should try and do this. However,I have discussed managing risk by adjusting market exposure at times when “risk” outweighs the potential for further “reward.”

While our actions are almost always misunderstood, and labeled as “bearish,” I am actually neither bullish or bearish. In our practice, we follow a very simple set of rules, which forms the core of our portfolio management philosophy which focuses on capital preservation and long-term “risk-adjusted” returns.

As long-term investors, we don’t worry about short-term rallies, we only need to worry about the direction of overall market trends, and focus on capturing more of the positive and less of the negative. This philosophy stems from Baron Nathan Rothschild’s view:

“You can have the top 20% and the bottom 20%, I will take the 80% in the middle.”

While our assessment of the market two-weeks ago was that risk versus reward was unbalanced, such can remain the case for extended periods of time.

The problem with an economy being propped up by artificially appreciated assets is that this pendulum swings both ways. At some point, prices eventually decline. No one knows what will cause the decline;

Higher interest rates like in 2018,

A presidential tweet, when he launched the “trade war” with China.

The ongoing implosion of the Chinese economy is still a threat.

It could just be the realization by the markets that asset prices don’t grow to the sky.

Or, it could be triggered by an unexpected, exogenous event, which results inthe markets “repricing” risk.

The “coronavirus” was the exogenous event the markets had not priced into its view.

Is It Time To “Buy The Dip?”

With the “sell off” on Monday, the immediate reaction by investors is to jump in and “buy the dip.” This would seem to be the logical action given the Federal Reserve is still supplying liquidity to the market currently.

Maybe not.

The chart below is part of the analysis we use to “onboard” new client portfolios. The purpose of this measure is to avoid transitioning a new client into our portfolio models near a short-term peak of the market. The vertical red lines suggest we avoid adding equity risk to portfolios and vice versa.

There are a few important points to denote in the chart above.

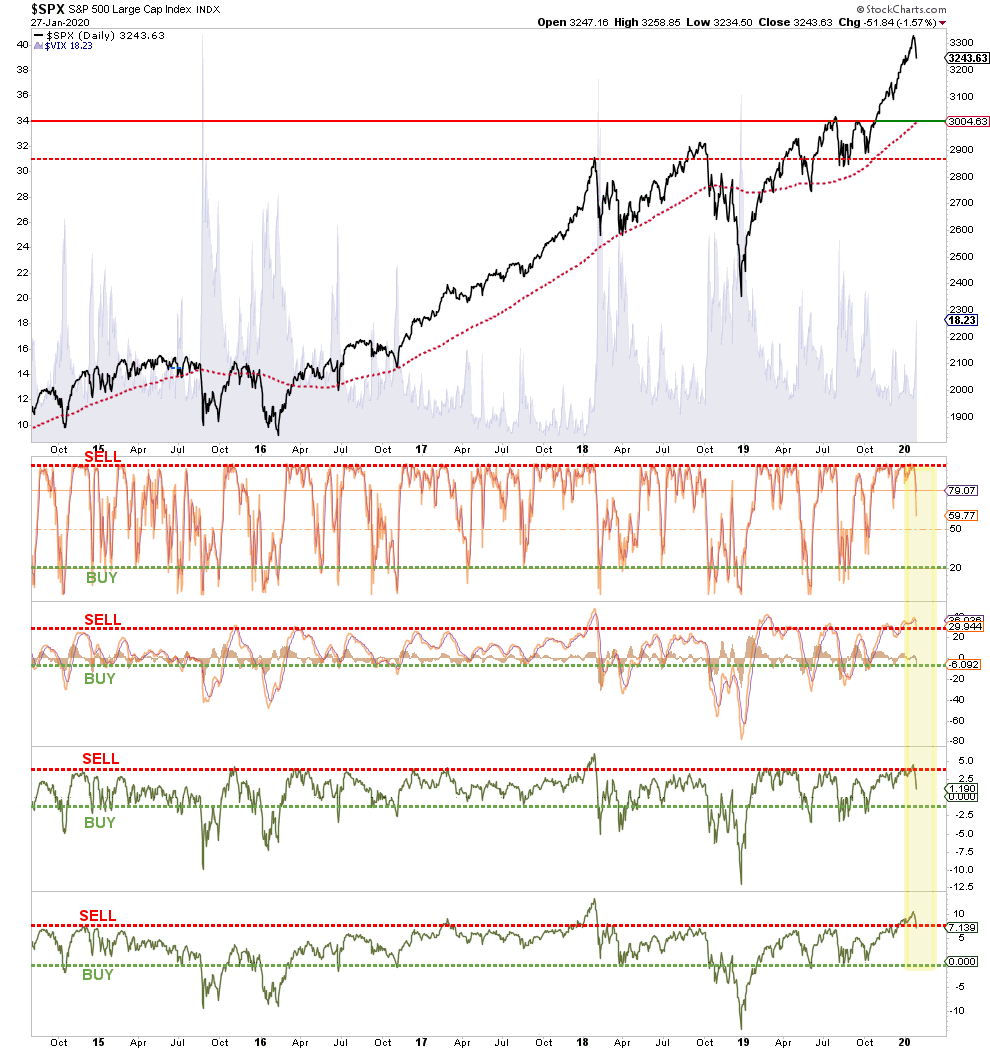

The top and bottom signals are essentially relative strength and momentum measures. Both are currently still on “buy” signals and the current “sell off” has not reversed those signals as of yet.

With the market still very deviated above the longer-term 200-dma, and just clearing out of 3-standard deviation territory, there is currently more downside risk, than upside reward.

Note that corrections, once the “sell signals” are triggered can last from several weeks, to several months. During the correction process there are often multiple opportunities to reduce risk and raise cash accordingly.

The last two times the market pushed into 3-standard deviation territory, the resulting corrections were fairly sharp and lasted for several months.

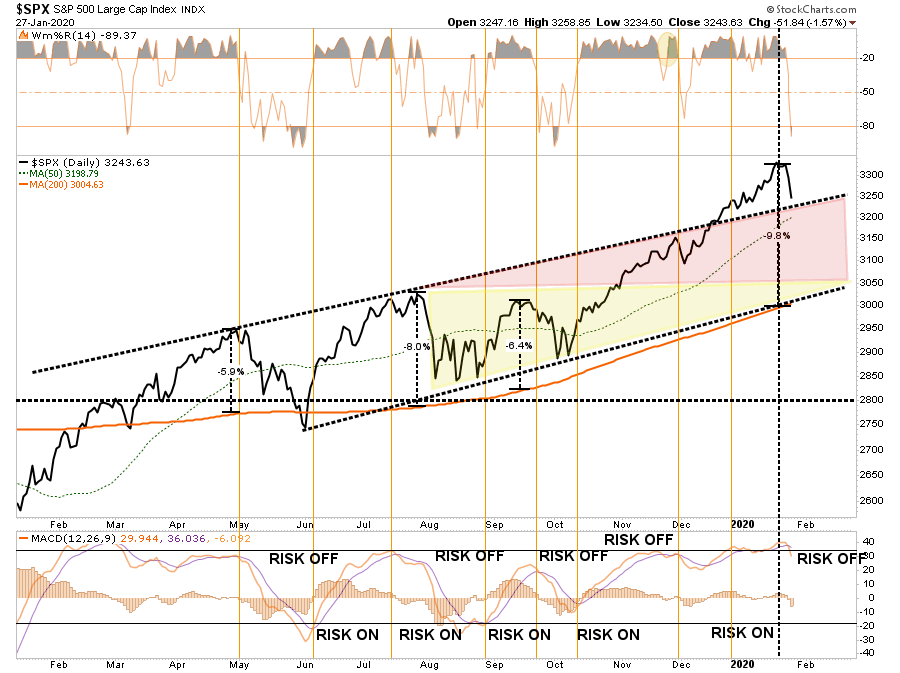

However, on a VERY short-term basis the market is indeed oversold, and is testing the breakout of the upward trending trading range from last year. Given the MACD has registered a “sell signal” from a fairly high level, investors must consider the risk of further downside even if the market rallies over the next couple of days.

Don’t be fooled that a short-term reflexive rally is an “all-clear” for the bull market to resume. With the bulk of our momentum, relative strength, and overbought/sold indicators just starting to correct from recent highs, it is likely short-term rallies will be “selling opportunities” over the next couple of weeks as the market either corrects further or consolidates recent gains.

As we have detailed over the last few missives, due to the rather extreme extension of the market, this is likely the beginning of a correction which could encompass a 5-10% decline in totality before it is complete.

The problem for investors is they tend to make to critical mistakes in managing portfolios.

Investors are slow to react to new information (they anchor), which initially leads to under-reaction but eventually shifts to over-reaction during late-cycle stages.

Investors are ultimately driven by the “herding” effect. A rising market leads to “justifications” to explain over-valued holdings. In other words, buying begets more buying.

Lastly, as the markets turn, the “disposition” effect takes hold and winners are sold to protect gains, but losers are held in the hopes of better prices later.

With the Federal Reserve reducing slowing its torrid pace of liquidity, still weak economic growth, and potential for weaker than expected earnings growth, the risk remains to the downside currently.

From that perspective, we are continuing to maintain our higher levels of cash, and we will use reflexive rallies in the short-term to rebalance portfolio risk as needed according to our investment discipline.

Tighten up stop-loss levels to current support levels for each position.

Hedge portfolios against major market declines.

Take profits in positions that have been big winners

Sell laggards and losers

Raise cash and rebalance portfolios to target weightings.

Notice, nothing in there says, “sell everything and go to cash.”

“The point being made here is essential; risk management is generous. Based on the past 100 years of market data, there is no evidence that long-term returns are penalized by taking a defensive investment posture at high valuations. Investors today do not need to ‘buy and hold’ stocks and remain heavily invested when expected returns are paltry. The historical record, though imprecise, affords an excellent map for navigating and managing risk.”

By having reduced risk, we can afford to remain patient and wait for the next opportunity. Much like a professional baseball player, by reducing risk we create an environment that is “emotionally” controllable and we can exercise patience until a “fat pitch” comes along.

One thing is for certain, swinging at every pitch, won’t get you into the “hall of fame.”

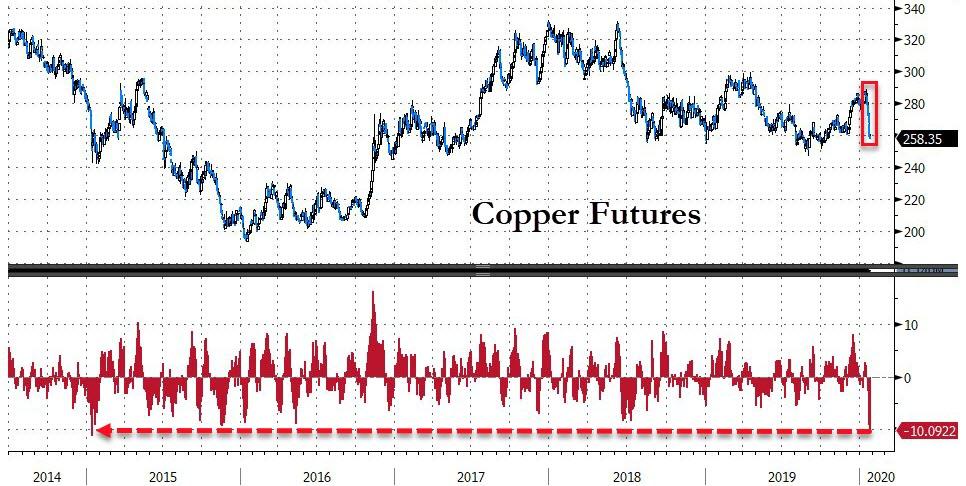

Doctor Copper Catches Coronavirus With Worst Performance In 34 Years

Copper prices are down 10 straight days – the longest streak of losses for the commodity with an economics PhD since 1986!

And as stocks rebound – for no reason whatsoever – copper continues to fall…

Source: Bloomberg

This is the worst 9-day drop since early 2015’s global growth scare…

Source: Bloomberg

And, it appears that other lifeblood of the global economy is also not buying what stocks are selling…

Source: Bloomberg

And bonds continue to disagree with stocks’ exuberance…

Source: Bloomberg

Still – if Powell promises to save the world by printing more money – potentially to use as homemade masks – then why not keep buying stocks? What could go wrong?

Bernie Sanders Staffer Admits Campaign Attracts “Marxists, Leninists And Anarchists”

Two more Bernie Sanders staffers have been caught on tape speaking passionately about ‘the revolution’ they’re fighting, they type of people the Sanders campaign attracts, and the need to take direct, violent action against their enemies.

“I’ve Canvassed with Someone Who’s an Anarchist, and with Someone Who’s a Marxist/Leninist. So, We Attract Radical, Truly Radical People in the Campaign…Obviously That’s Not Outward Facing,” said South Carolina field organizer, Mason Baird, who told a Project Veritasundercover operative “We would need a federal government and a labor movement that is working together to strip power away from capitalists and preferably directing that violence towards property.”

“A lot of those people (on the campaign) who do that kind of work, they’re Marxist-Leninists, they’re anarchists…They have more of a mind for direct action…engaging in politics outside of the electoral system,” says Baird.

BREAKING: @BernieSanders Field Organizer Mason Baird “A lot of those people(on the campaign) who do that kind of work…they’re Marxist-Leninists, they’re Anarchists…They have more of a mind for direct action…engaging in politics outside of the electoral system”#Expose2020pic.twitter.com/pF31MBsTsm

Another South Carolina field organizer, Daniel Taylor, said that not everybody is ready for the “crazy stuff,” when it comes to direct action.

“We don’t want to scare people off, so you kinda have to feel it out before you get into the crazy stuff…more, more extreme organizations and stuff like Antifa, you know you were talking about the Yellow Vests and all that; but, you know we’re kinda keeping that, keeping that on the back-burner for right now.“

“It’s unfortunate that we have to make plans for extreme action, but like I said, they’re not going to give it to us, even if Bernie is elected.“

BREAKING: “I have no problem going all in on the campaign stuff because you’re planting a seed…The whole socialist thing four years ago was a lot more toxic than it is today…” – @BernieSanders Field Organizer Daniel Taylor #Expose2020pic.twitter.com/kWcqXOaYuy

Earlier this month, Veritas caught two other Sanders staffers extolling the virtues of throwing capitalists in literal gulags, and fighting in the revolution.

In short, Sanders is getting the Antifa vote, assuming they vote.

As O’Keefe notes at the end of the latest montage, will Bernie disavow these radicals within his campaign, or does he welcome them?

Coronavirus isn’t the issue. It’s an unexpected event – a No-see-Um that caught the market by surprise. It’s its effect that matters. It’s refocusing markets on to the things they do know. It’s bound to have some rebalancing effects on stocks directly impacted, and on policy. The reaction in terms of the dip and increased VIX vol is what we expected on unknowable news.

Strip it out, and the critical factor for general prices remains the absolute disconnect between high stock prices relative to corporate earnings (lacklustre), oil prices (tumbling), commodity prices (low) and growth (anaemic). The IMF may have raised its global GDP expectations to “still breathing”, but its only central banks remaining accommodative, and the market relying on them to keep juicing the party – that’s been keeping this market where it is.

How much longer will the Central Banks play along? They will be watching the virus for signs of “economic drag”. But, soon to be ex-BOE Governor Mark Carney could throw a completely unnecessary ease in the UK as a final Remainer pout. The market reckons the US Fed will remain on hold till Q3, if not longer.

Even the ECB may be waking up to the reality – a Luxemblurg member noting with typical clarity how Europe’s Central Bank might just have contributed to “very elevated” asset prices. Oops. “These unusual times call for heightened vigilance regarding the financial-stability consequences of our monetary policy actions.” Congratulations the Yves Mersch who gets a gold star for stating the downright blinking obvious. Heaven help us if the ECB’s promised policy review actually acknowledges just how they’ve progressed the Japanification of Europe through zero rates, austerity, QE and pig-headedness (particularly in acknowledging the weakness of European banking and achieving little to alleviate it). But the ECB is a story for another day – and after Friday’s divorce is finalised I don’t suppose we Brits will ever hear from Yoorp again….

If even the ECB knows the current market levels are built on a sand of loose policy and inflated financial asset prices.. who doesn’t?

Going back to the Coronavirus – it’s having real damaging effects on the regional and global economy. The immediate losers include the airlines, luxury good makers and miners. But it’s interesting how Tech stocks have also wobbled. The government mandated policy responses have triggered real and significant effect. If they set the world a wondering about how the specific virus damage to stocks has morphed into a knee-jerk falls in indexes – does it mean it’s time to take cover, or look for buying opportunities.

If it’s so clear stocks are overvalued, then could this be the sell-off moment? Is it time to dump stocks? Don’t be silly!

Its time to get selective – keep the diamonds, and dump the dross while the market remains this frothy and overpriced.

Why would you sell high dividend stocks to buy bonds at record low yields? Makes much more sense to sell the speculative stuff at current valuations where they aren’t paying returns. (That will trigger a host of comments from the Rude-American’s about how I don’t understand its all about stock prices, not profits!) Although there may still be some upside in bond prices from a further round of global easing if we get renewed weakness – that certainly isn’t nailed on, and it will be limited.

What is far more likely to happen is a refocus on what stocks to own and at what price. Do the Tech giants justify their high valuations? The cornerstone of my own PA portfolio has been Apple and the news sounding increased orders all sounds positive. But do the successful companies like Facebook, Amazon, Google etc justify the high multiples? Why not? Do the questionable multi-unicorns still in expansion mode justify expectations – do the competitive threats to Uber and Netflix justify lower prices. And what about Tesla’s extraordinary valuation? Keep the former, I have doubts on the latter.

This is not a run for the hills moment, nor is it a buy the dip opportunity. But it might be time to make some rational choices on what to keep and spring clean portfolios of over-optimistic crud.

Boeing

Interesting to see Boeing easily raise a $12 bln 2-year L+100 bank loan to cover the grounding delays in B-737 Max deliveries. Its described in the press as a vote of confidence in the plane-maker. A few weeks ago I almost made a speculative call to buy Boeing, expecting a sudden uptick on the stock on rumours the MAX might get approved for flight. Now Boeing say it will be H2, although the FAA say it might be sooner if Boeing continue to hit milestones.

Now I am beginning to think the bank loan looks… “Courageous”. The odds continue to stack up against Boeing. New orders for the B-787 Dreamliners have dried up and production has been slowed. The new B-777x finally flew last weekend, but is generally considered to the wrong plane, at the wrong time and appeals pretty much exclusively to lead order Emirates. Pilots and passengers are united against the B-737 Max – even if does get back into service it’s going to be interesting to see if orders are cancelled.

All of which leaves nothing on the Boeing production line any airline particularly wants. There is nothing in the development shed like a new super-efficient smaller regional work horse. Instead of a promising new product, Boeing executives can proudly point to the fact they squandered all the 737 revenues on a stock buyback programme that made executives richer through their stock options, and happy shareholders till the B-737 Max started crashing. The stock has performed dismally since. It could get far worse if the expected 737 Max cancellations kick in and its recertification is further delayed. It will get much worse when investors wake up and smell the coffee… and discover where the company value went.

{kind=link}

{kind=link}