Are you ready for this week’s absurdity? Here’s our weekend roll-up of the most ridiculous stories from around the world that are threats to your liberty, your finances, and your prosperity.

Professor Blames Private Property for California Wildfires

A public takeover of utility companies is not enough, according to Kian Goh, Professor of Urban Development at UCLA.

In order to combat California wildfires, we need to abandon “aspirations of home ownership, and belief in the importance of private property.”

Fueled by cheap energy– and of course the ever-present racism of the white middle-class– people expanded beyond cities, building little tinder-box neighborhoods into the forests.

Goh says that, “Expansionist, individualist, and exclusionary patterns of housing became synonymous with freedom and self-sufficiency.”

Ah yes, it’s not so hard to link the desire for freedom and self-sufficiency with every known evil on earth. You’re even responsible for burning down California.

But Urban Planners like Kian Goh would be happy to step in, and tell us how our lives should be designed.

For the greater good, we must collectivize and live on communal (i.e. government controlled) land.

Just a reminder– parents across the country pay top dollar each year so people like Professor Goh can teach their children.

In Early November, Oren Levy had his shipment of legal hemp confiscated by the New York Police. They even bragged about the “drug bust” on social media.

Too bad it was perfectly legal. Levy even had the documentation to prove it, included in every box of the shipment.

But police still lured Levy’s brother to the department under the guise that he could pick up the shipment, and arrested him.

After almost two months, and nearly destroying Levy’s perfectly legal CBD oil business, charges were dropped. The shipment was returned– though in a dry and deteriorated condition.

Levy is now suing the NYPD, the City of New York, and possibly FedEx for alerting the authorities in the first place.

Congress has a New Year’s Resolution: Destroy Facebook’s Libra Token

Two bills that the US Congress will consider this year seem aimed specifically at preventing Facebook from rolling out it’s digital token Libra.

One is called the “Keep Big Tech Out Of Finance Act.” It would ban “large platform utilities” from being, or being affiliated with, a financial institution.

It would also not allow large platforms to create or “operate a digital asset that is intended to be widely used as medium of exchange, unit of account, store of value, or any other similar function.”

Violators would be fined $1 million per day.

The other bill is called the “Managed Stable Coins are Securities Act.”

Libra is intended to be a “stable coin” which is a digital currency tied to the value of existing currencies.

This bill would make it law that Libra would be considered a security, like a stock or bond, as opposed to a currency, like the dollar or Swiss franc.

Sounds like the US government doesn’t want any competition with their Federal Reserve Notes.

In September 2019, the media company Vox ran the headline, Gig workers’ win in California is a victory for workers everywhere.

They were referring to a new law in California which classified gig workers and contractors as employees.

The story was that by classifying workers as contractors instead of employees, companies like Uber and Lyft got away with not providing employee benefits required under California law.

Then, just before Christmas, Vox showed us what the law really meant when it fired 200 California-based freelance writers.

Vox helped sell the public the lie that laws like these force companies to absorb freelancers as employees. But in reality, it means they get fired.

US Officials Say Soleimani Was Planning Attacks On Diplomatic Targets In Syria, Lebanon

Top Iranian commander Qassem Soleimani was plotting to attack American military, diplomatic and financial targets in Syria and Lebanon, and comprised the imminent threat used to justify Soleimani’s killing, according to NBC News, citing multiple US officials.

“When we start seeing extensive and very solid intelligence that [Soleimani] is plotting imminent attacks against the United States, the president as commander in chief has a duty to take decisive action,” said a senior State Department official, adding “If we had not taken this action, and hundreds of Americans were dead, you would be asking me why didn’t you take out Soleimani when you have the chance.”

Gen. Mark Milley, chairman of the Joint Chiefs, said he is confident Soleimani was actively planning attacks against the U.S. in the Middle East and those attacks were imminent.

“We had clear, compelling, unambiguous intelligence to indicate Qassem Soleimani was planning, coordinating, and directing a significant campaign of violence against the United States in the coming days,” said Gen. Milley. –NBC News

Soleimani’s targets are said to include US military outposts in eastern Syria, and diplomatic and financial targets in Lebanon. According to Gen. Milley, the US is confident that the “size, scale and scope” of the planned attacks constituted an imminent threat.

“By the way, it still might happen,” he added.

A Syrian boy looks at a U.S. convoy patrolling near the Turkish border on Oct. 31, 2019. (Delil Souleiman / AFP)

Should Lebanon come under attack, the 173rd Airborne Brigade Combat team is on alert and prepared to deploy, should they come under attack. The deployment would consist of somewhere between 130 and 750 total troops.

A senior U.S. official said Soleimani had traveled to Syria, Lebanon and then to Iraq Thursday, and U.S. intelligence officials believe he was approving final plans for attacks in each location.

Milley said Soleimani had been directing attacks against the U.S. inside Iraq, including a Dec. 27 attack near Kirtkuk that killed an American contractor and wounded four U.S. service members.

“He approved it,” said Milley. “I know that. One hundred percent.” –NBC News

According to a senior Congressional aide briefed on the intelligence, however, lawmakers saw nothing linking Soleimani to an imminent attack – rather, what they saw was “exactly the sort of planning and coordination he has been doing for years,” according to NBC. The aide added that while nobody doubts Soleimani was a threat to the United States, the case for acting on an imminent threat was not made.

Sen. Mark Warner (D-VA), ranking member of the Senate Intelligence Committe, said “I have real questions and want to get a full briefing from the intelligence community about the decision on this time and place.”

Today, as we step into the New Year, we reach down to turn over a new leaf. We want to make a fresh start. We want to leave 2019’s bugaboos behind. But, alas, lying beneath the fallen leaf, like rotting food waste, is last year’s fake money. We can’t escape it. But we refuse to believe in its permanence.

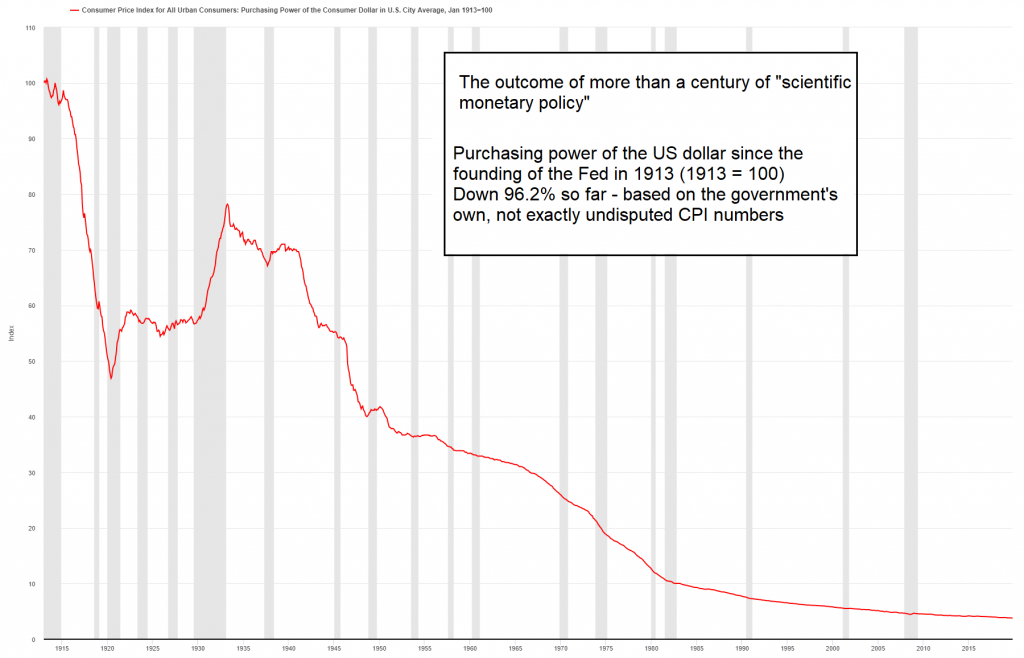

This is what “monetary stability in the Fed-administered fiat money regime looks like: in the year the Fed was established it took $3.80 to buy what $100 buy today – provided the government’s CPI data are actually a valid gauge of the dollar’s purchasing power. [PT]

Victorian economist William Stanley Jevons, in his 1875 work, Money and the Mechanism of Exchange, stated that money has four functions. It is a medium of exchange, a common measure of value, a standard of value, and a store of value.

No doubt, today’s fake money, including the U.S. dollar, falls well short of Jevons’ four functions of money. Certainly, it comes up short in its function as a store of value.

Hence, today’s money is not real money. Rather, it is fake money. And this fake money has heinous implications on how people earn, save, invest, and pay their way in the world we live in. Practically all aspects of everything have been distorted and disfigured by it.

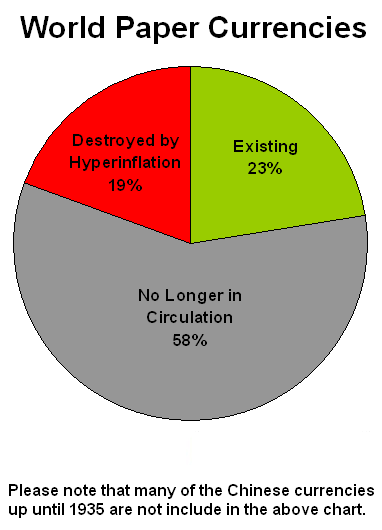

Take the dollar, for instance. Over the last 100 years, it has lost over 96 percent of its value. Yet, even with this poor performance, the dollar has one of the better track records going. In fact, many currencies that were around just a short century ago have vanished from the face of the earth. They have been debased to bird cage liner.

This graphic is slightly dated by now (we downloaded it almost 20 years ago), i.e., a few more fiat currencies have joined the expired contingent by now. It also excludes a number of historical paper currency experiments in China, which failed without exception. Still, it can be estimated that no more than 20% of the paper currencies created so far still exist – and the strongest one of them has lost “only” 96% of its value! [PT]

Who Will Buy All this Debt?

The failings of today’s dollar are complex and multifaceted. But they generally stem from the unsatisfactory fact that the dollar is debt based fiat that is issued at will by the Federal Reserve. How can money function as a store of value when a committee of unelected bureaucrats can conjure it from thin air?

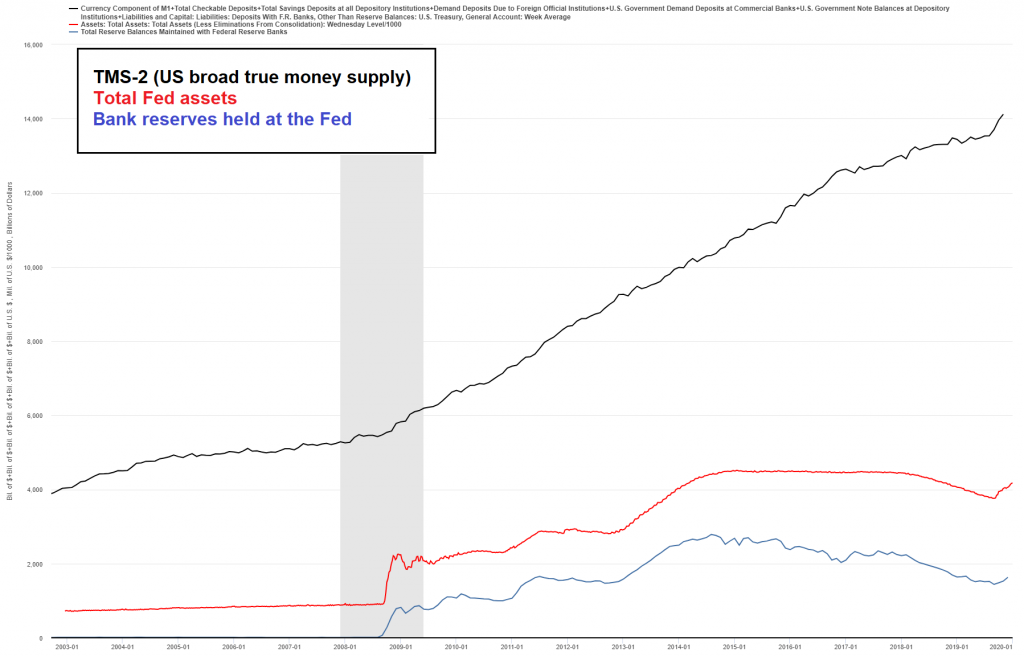

After President Nixon “temporarily” suspended the Bretton Woods Agreement in 1971, the future was written. The money supply has expanded without technical limitations. This includes expanding the Fed’s balance sheet to buy Treasury debt. In a practical sense, Fed purchases of U.S. Treasury notes are now needed to fund government spending above and beyond tax receipts (i.e., fiscal deficits).

As an aside, the Fed’s charter prohibits it from directly purchasing bills issued by the U.S. Treasury. So to bypass this restriction, dealers – i.e. preferred big banks – purchase Treasury bills upon issuance and then several days later these same Dealers sell them to the Fed. What’s more, for providing this laundering service the Dealers pocket an unspecified markup. These indirect money printing operations have been going on for well over a decade, and last occurred about a week before Christmas – to the tune of nearly $23.7 billion.

Unbridled monetary inflation: TMS-2 (US broad true money supply), Fed assets and bank reserves. [PT]

According to the Congressional Budget Office, the federal budget deficit for the first two months of fiscal year 2020 is $342 billion. At this rate, Washington is going to add over $2 trillion to the national debt in FY 2020. Who will buy all this debt?

Not China. Not Japan. Not Saudi Arabia. Not American citizens. Instead, the Fed will buy it via balance sheet expansion. Of course, there are natural consequences for these underhanded practices – and you will pay for them, you already are…

Thank God we have this bearded Nobel Prize winner to remind us we are completely wrong about fiscal deficits…[PT]

Subjective Evaluation

About a decade before Jevons outlined the four functions of money, he elaborated the idea of marginal utility. That the utility – the satisfaction or benefit – derived by consuming a good or service changes from an increase in the consumption of that good or service. This change in utility influences how goods and services are priced within the economy.

Stanley Jevons, Carl Menger and Leon Walras worked out the law of marginal utility independently from each other at roughly the same time. It revolutionized price and value theory, but evidently many people fail to grasp it to this day. For instance, the Wikipedia article on marginal utility is chock-full of arrant nonsense and has proved utterly resilient to correction since we first laid eyes on it ten years ago (here is an example illustrating that the author of the article simply does not know what he or she is talking about. Listing alleged “exceptions” to the law of diminishing marginal utility they write: “[…]marginal utility of a good or service might be increasing as well. For example: bed sheets, which up to some number may only provide warmth, but after that point may be useful to allow one to effect an escape by being tied together into a rope.” This is incorrect, for the simple reason that “bed sheets tied together into a rope” are a different good than bed sheets. As soon as they are tied together into a rope, they are no longer bed sheets, but a rope. The concept of marginal utility then applies to similar ropes. The rope’s previous incarnation as bed sheets is irrelevant. One would think this is obvious, but apparently it isn’t on Wikipedia, which one should definitely not rely on as a source for anything). [PT]

Yet Jevons went down the rabbit hole of simultaneous determination, which included modeling complex relationships as systems of simultaneous equations in which no variable “causes” another. The flaw in Jevons’ approach is that it relied on creating artificial, modeled representations of reality. Unfortunately, much of popular economics followed him down the rabbit hole where they still reside to this day… enamored with technical nonsense.

However, at the same time as Jevons, Austrian economist Carl Menger, from the University of Vienna, independently developed the concept of marginal utility. Menger, in contrast to Jevons, applied these principles through deduction and logic to explain the real world actions of real people. For Menger, the role of subjective evaluation was critical to the principle of marginal utility.

Menger, in Principles of Economics, published in 1871, explained prices as the outcome of the purposeful, voluntary interactions of buyers and sellers, each guided by their own subjective evaluations of the usefulness of various goods and services. Menger elaborated that the exact quantities of goods exchanged, and their prices, are determined by the values individuals attach to marginal units of these goods.

Menger also recognized that the first unit of consumption of a good or service yields more utility than the second and subsequent units, with a continuing reduction for greater amounts. Hence, the fall in marginal utility as consumption increases is known as diminishing marginal utility, and is commonly expressed as the law of diminishing marginal utility.

Money, like any other good, is subject to the law of diminishing marginal utility. Specifically, an increase in the quantity of money by an additional unit leads to a reduction in purchasing power per monetary unit. As people exchange the increased money against other goods, prices rise. Or, more aptly, the purchasing power of money falls.

How the Fed Robs You of Your Life

The inflation of the money supply, in effect, distorts the prices of goods and services. Subsequent units of a good or service may have a reduced utility, though, over time, their nominal cost increases. This also undermines individual savings… and robs savers – that is you – of their lives…

Highway robbers not only lurk at Epsom… these days they lurk in the Eccles building too. [PT]

When the Fed introduces new money to the economy to finance deficits it debases the dollar. Similarly, when the Fed provokes the over-issuance of credit by artificially suppressing interest rates, it further inflates the money supply and debases the dollar. This has the effect of reducing the dollar’s purchasing power. What does all this have to do with you?

Think of all the days you would have rather stayed home with your family than schlepping and slogging the day away for money. Think of all the time you spent on the road getting dumped on by clients while your kids were growing up. Think of all the sunny days you missed because you were at the office all day estimating and bidding on ridiculous jobs.

For what? So that after paying taxes on it all, what is left over is inflated away from your bank account? Remember, money, in addition to being property, also represents time and the sacrifices made to earn it.

When the Fed inflates your money away it not only robs you of your money. It robs you of your life.

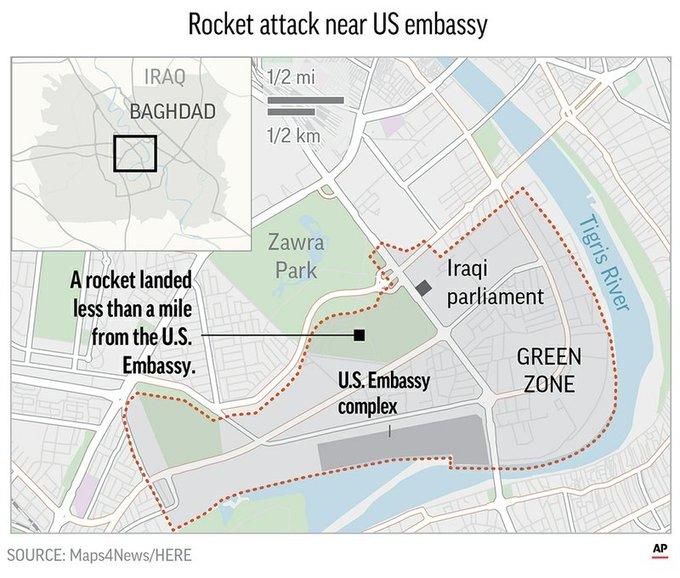

As 1000s march in the streets of Baghdad to moutn the death of Soleimani, Al-Arabiya (and other local news sources) report rockets have landed in the heavily fortified Green Zone in Baghdad, where the US Embassy (among other things) is located.

Witnesses told Reuters that an explosion was heard in the Iraqi capital, Baghdad

شهود لرويترز: سماع دوي انفجار في العاصمة العراقية بغداد

Air Force Releases Video Of B-2 Stealth Bomber In Action

Several days after Iranian militia attacked the US embassy in Baghdad and about 12 hours after US airstrikes killed a top Iranian general near Baghdad International Airport, the US Air Force released a video of the Northrop Grumman B-2 Spirit bomber in action.

The video, according to Defense Blog, displays the aircraft’s mission at Whiteman Air Force Base.

About a year ago, we detailed how the 509th Bomb Wing, assigned to the Eighth Air Force of the Air Force Global Strike Command, operates a fleet of Northrop Grumman B-2 Spirit stealth bombers out of Whiteman AFB, released a video showing one of its planes dropping two 14 ton GBU-57 Massive Ordnance Penetrators (MOP) in a test flight.

The short video, uploaded to YouTube by The Aviationist blog, shows the stealth bomber with the tail number 82-1066. The video first starts with the plane in a hanger, being prepped for flight, then takes off from Whiteman AFB under cover of night. About a third into the clip, the bomber is over an unidentifiable mountain range receiving fuel from an aerial refueling tanker. Moments later, the plane releases two MOPS. Land-based cameras capture the incredible moment when the bombs slam into an unidentifiable missile test range producing a massive explosion.

The clip is short, so prepare yourself for an exhilarating 55 seconds of American firepower, weapon bays open at 00:37:

America could be nearing a period of wartime considering last week’s developments in the Middle East. The Air Force’s video of the stealth bomber should be seen as wartime propaganda.

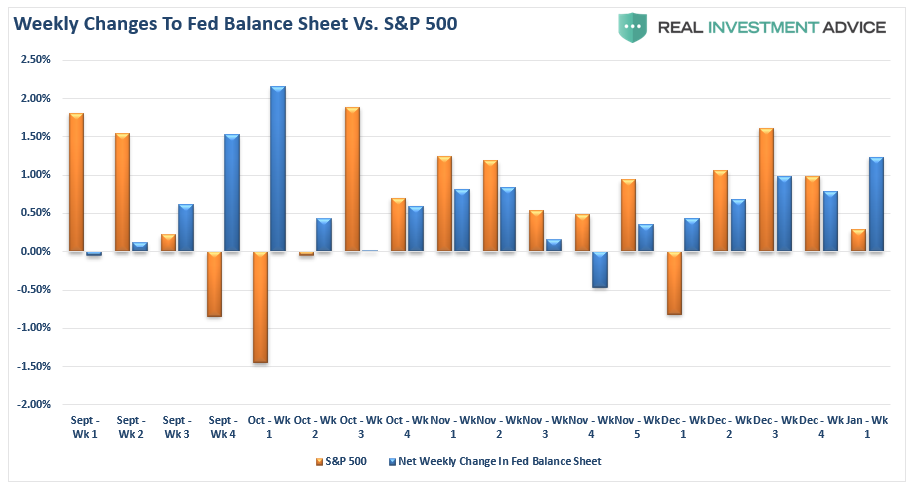

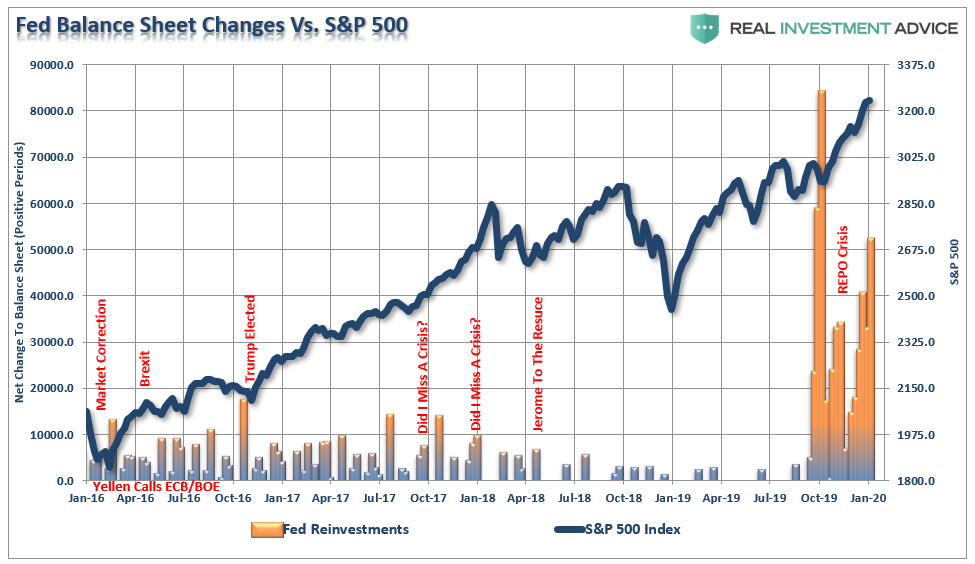

That is the current mantra of the market as we begin 2020, and it certainly seems to be the right call. Over the last few months, the Federal Reserve has continued its “QE-Not QE” operations, which has dramatically expanded its balance sheet. Many argue, rightly, the current monetary interventions by the Fed are technically “Not QE” because they are purchasing Treasury Bills rather than longer-term Treasury Notes.

However, “Mr. Market” doesn’t see it that way. As the old saying goes, “if it looks, walks, and quacks like a duck…it’s a duck.”

Those liquidity flows most notably have been chasing the largest of large caps – namely Apple (AAPL) and Microsoft (MSFT). As Ed Dowd noted, there are many similarities between now and the last time the Fed was fighting a perceived liquidity shortage before the “turn of the century” over concerns of “Y2K.”

But here is what jumped out at me.

Going back to 2016, as the world faced a “Brexit” crisis, the Fed, ECB, and the BOE all joined forces to provide liquidity to the markets. Then, just before the 2016 election, as the world was concerned a “Trump Election” would crash the market, the Fed provided a huge boost of liquidity. All along the way, each dip in the market was met by liquidity support.

Currently, we are being told there is “nothing to worry about” with respect to the financial system. Maybe, but the amount of liquidity being injected dwarfs all previous injections by massive proportions.

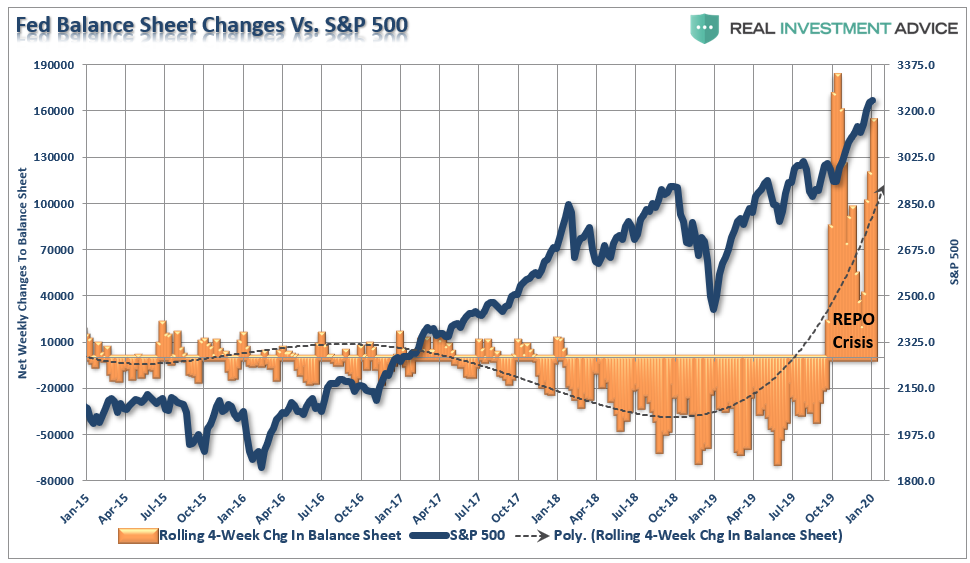

You can see the issue more clearly looking at a rolling 4-week change to the Federal Reserve’s balance sheet.

So, despite commentary to the contrary, there are only two conclusions to draw from the data:

There is something functionally “broken” in the financial system which is requiring massive injections of liquidity to try and rectify, and;

The surge in liquidity, whether you want to call it a “duck,” or not, is finding its way into the equity markets.

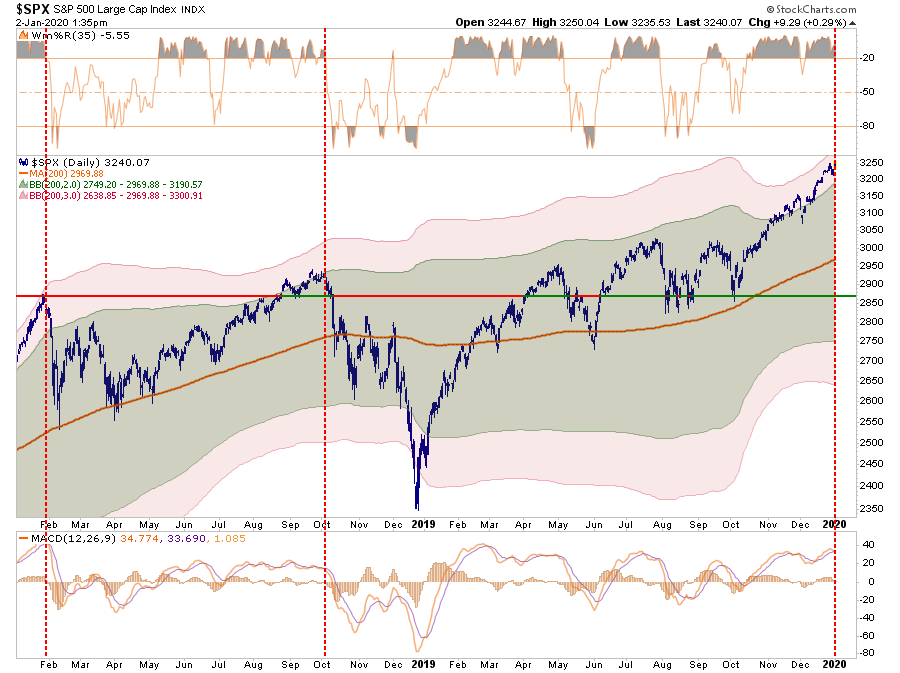

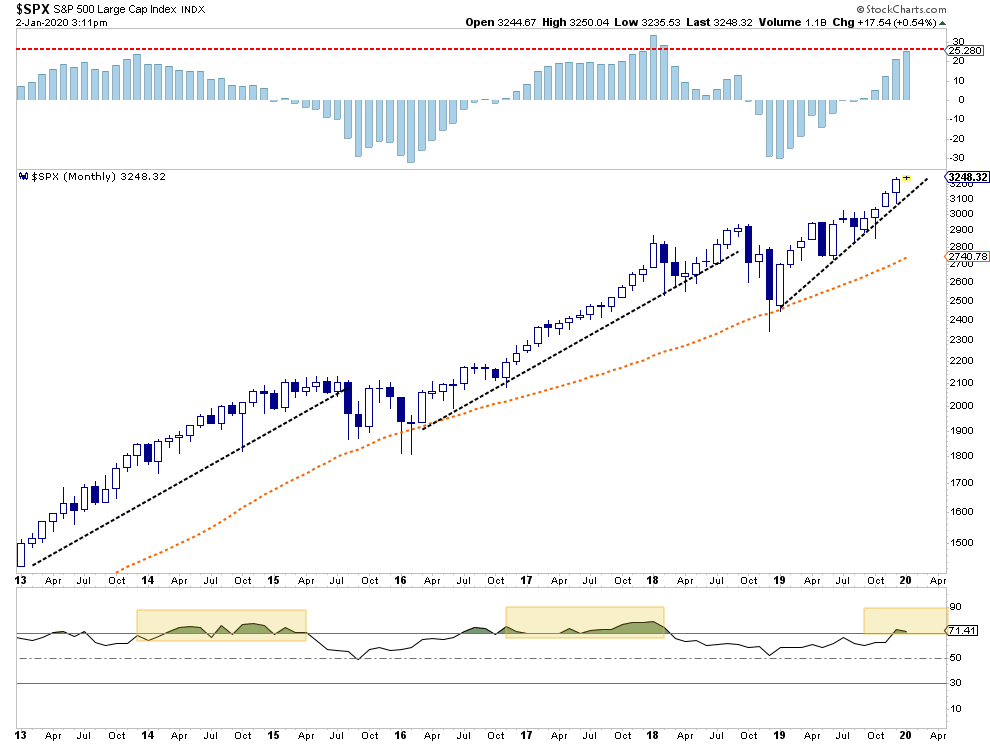

January 2018 Redux

“The exuberance that surrounded the markets going into the end of last year, as fund managers ramped up allocations for end of the year reporting, spilled over into the start of the new with S&P hitting new record highs.

Of course, this is just a continuation of the advance that has been ongoing since the Trump election. The difference this time is the extreme push into 3-standard deviation territory above the moving average which is concerning.” – Real Investment Report Jan, 5th 2018

At the beginning of 2018, following the passage of “tax reform,” the market was pushing 3-standard deviations of the 50-dma. It eventually pushed 3-standard deviations above the 200-dma before it came crashing back to earth. The second time it pushed the same deviation was in October of 2018, which was again followed by a marked decline.

Currently, that push into a 3-standard deviation extreme is once again present. Does that mean a sharp correction is coming? Not necessarily. However, it does suggest gains are likely limited in the short-term.

As I stated in 2018:

“That extension, combined with extreme overbought conditions multiple levels, has historically not been met with the most optimistic of outcomes. But, as I will discuss next, “exuberance” of this type is not uncommon during a market ‘melt-up’ phase.”

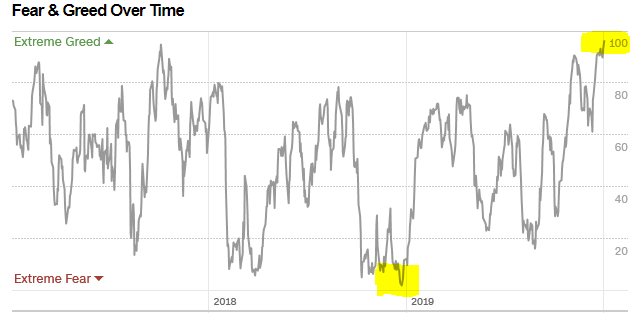

Currently, “exuberance” has returned with a vengeance, as noted by my friend and colleague Doug Kass:

“2019 ended in an entirely dissimilar manner compared to the way that 2018 ended. (As an example the CNN Fear & Greed Index was under 10 a year ago, its at 90 this week).

Despite a continued manufacturing recession, ongoing weakness in many global economies, political discord (and a Presidential impeachment), little resolution of the U.S./China trade differences and a flat year for S&P profits – valuations exploded (from 14.5x to nearly 19x) as confidence in an extended domestic economic recovery was heightened.”

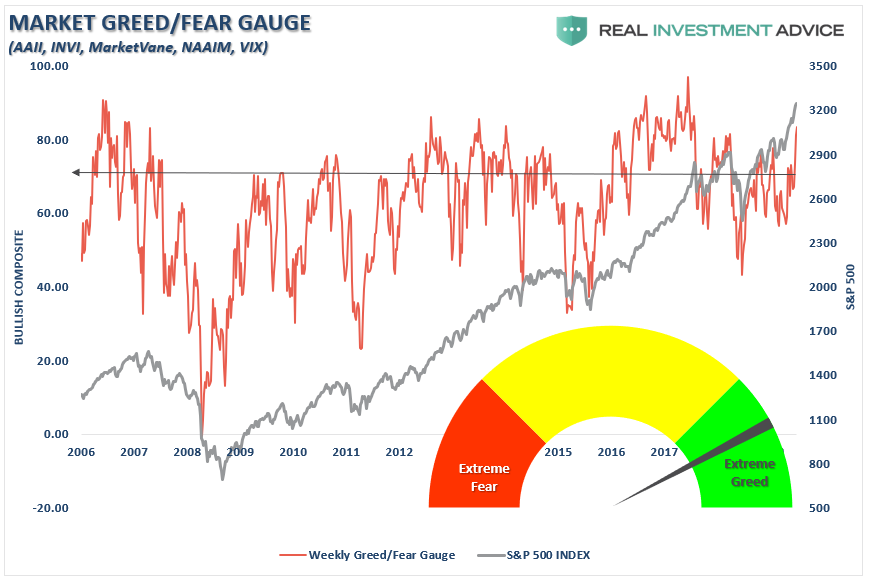

But it isn’t just sentiment which has gotten extraordinarily extended, but also investor positioning on many levels both individual and professional.

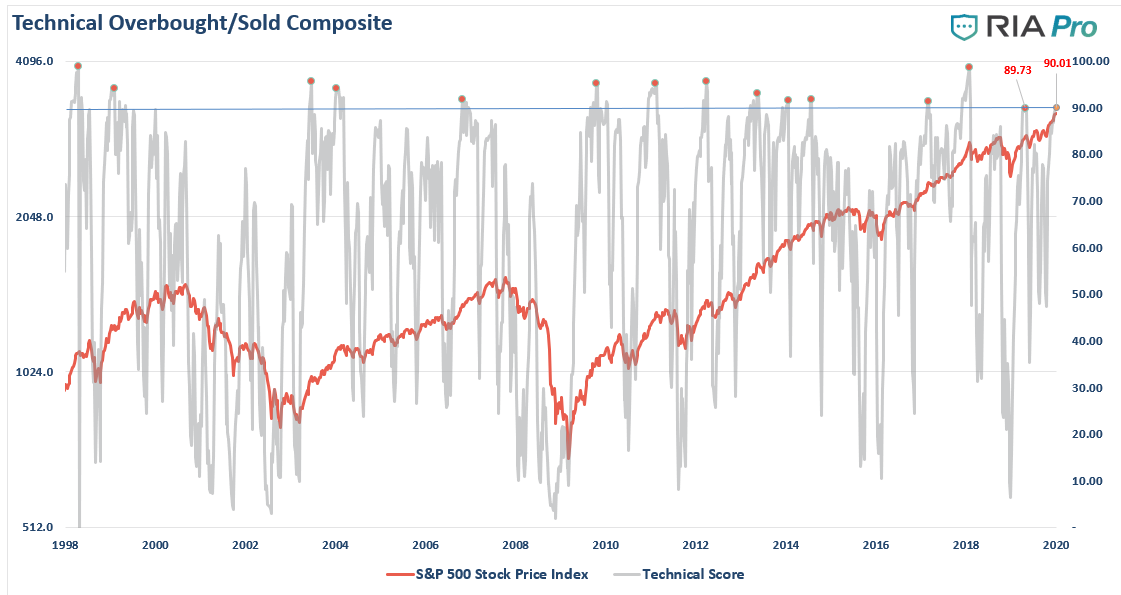

Lastly, our composite technical overbought/oversold gauge has also hit extremes.

In other words, “everyone is in the pool,” including the “life guards.”

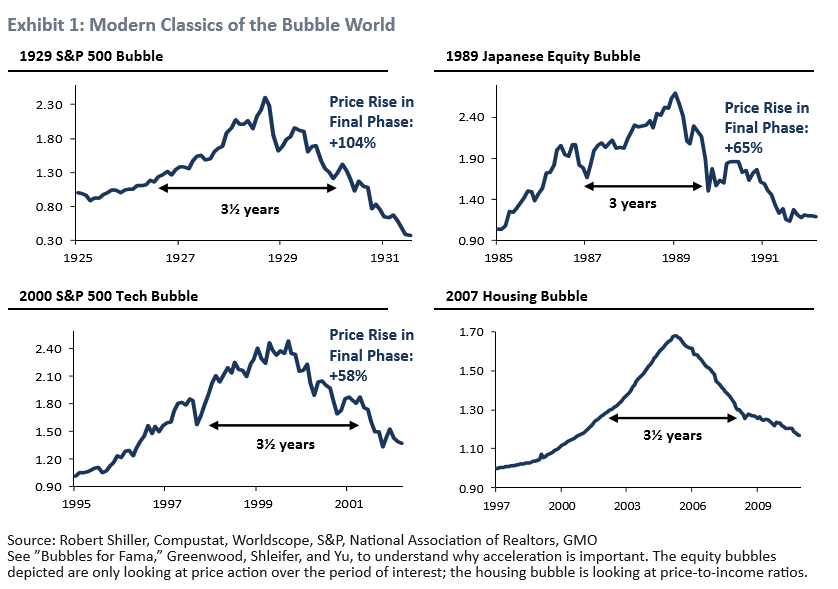

While the levels of exuberance are quite astonishing, it certainly isn’t surprising. This is what has been witnessed during previous market “melt-ups” throughout history. Jeremy Grantham of GMO previously wrote an excellent piece on market “melt-ups” and potential outcomes. To wit:

“As a historian of the great equity bubbles, I also recognize that we are currently showing signs of entering the blow-off or melt-up phase of this very long bull market.

The classic examples are not just characterized by higher-than-average prices. Price alone seems to me now to be by no means a sufficient sign of an impending bubble break. Among other factors, indicators of extremes of euphoria seem much more important than price.

Let’s look at what is missing in the way of psychological and technical signs of a late-stage bubble and what is beginning to fall into place. On the topic of classic bubbles, I have long shown Exhibits 1 and 2. They recognize the importance of a true psychological event of momentum increasing to a frenzy. That is to say, acceleration of price.”

Grantham is certainly very correct in his analysis. As shown in the chart below, the reversion of oversold, to extreme overbought (top panel in blue) has been extremely rapid. Historically speaking, such extreme overbought, overconfident, and extended markets tend not to stay that way for long.

From S&P 3300 to 3500, & Back Again

While we penned our initial target for the bull cycle at 3300 in July, given the extreme level of Federal Reserve monetary interventions, I certainly WOULD NOT rule out the possibility of a further melt up to 3500.

It is a possibility which must be considered. However, you must also balance that possibility with the probability of an eventual reversion. As noted by George Soros’ “Theory of Reflexivity:”

Typically bubbles have an asymmetric shape. The boom is long and slow to start. It accelerates gradually until it flattens out again during the twilight period. The bust is short and steep because it involves the forced liquidation of unsound positions.”

In the latter stages of the advance, money simply chases price. This is the point in the cycle where everything rises regardless of fundamental underpinnings or value.

2019 was such a year.

“According to Jeffrey Kleintop (Charles Schwab), “in 2019, all major asset classes produced above-average returns. That’s never happened before.” – WSJ

…

This needs no comment. pic.twitter.com/H0jtZQ7Bou

“It’s a marshmallow world for capital markets as we enter 2020. Name the asset class, and it had a stellar year in 2019. U.S. stocks? Up over +30%. Stocks across the rest of the world? Higher by more than +20%. Investment grade corporate bonds? Up nearly +20%. High yield bonds? +14%. Long-Term US Treasuries? +15%. Gold and silver? +16% each. Even long struggling commodities posted high single-digit returns this year. If you were allocated to risk assets in 2019, you likely enjoyed a good year.”

However, as Eric notes, when everything is “as good as it can get,” that only leaves one other option.

“Past performance can present future challenges. Most significantly, such universally good returns are difficult to maintain. Typically, capital markets assign winners and losers even when the % stimulus is pumping full throttle as it is today. So whether such good times can continue in 2020 across all asset classes remains to be seen, but investors are well served to consider what categories may be best positioned to continue to climb and those that may be set to take a breather in the year ahead.”

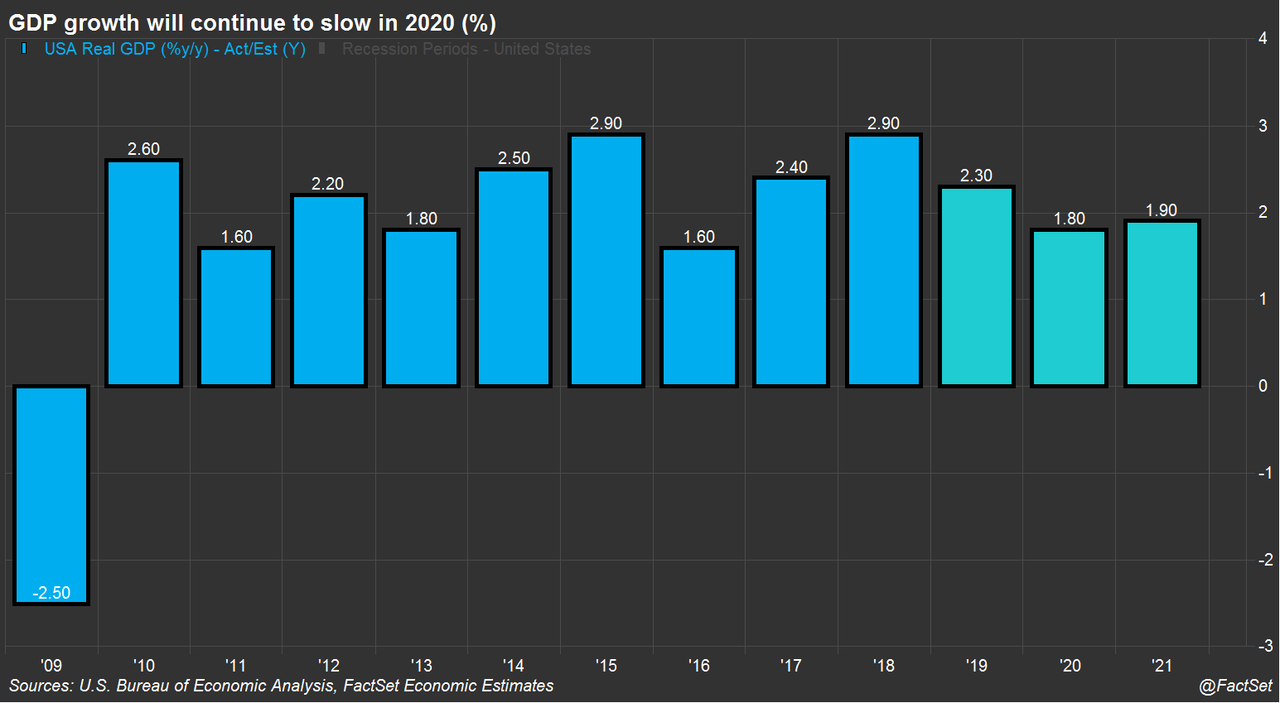

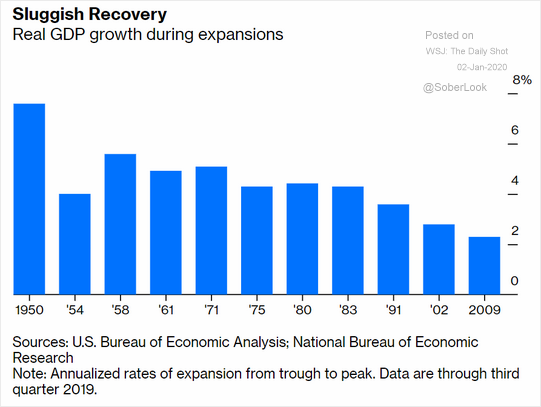

In particular, stocks are facing increasingly challenging headwinds from sluggish economic growth, to weaker earnings growth. Currently, economists are predicting economic growth below 2% in 2020, as noted by FactSet:

“While the odds of a near-term recession appear to have diminished, growth is projected to slow in the coming quarters due to a weaker global outlook and reduced global trade flows. U.S. economic growth is expected to continue to slow into 2020, with analysts surveyed by FactSet projecting 2.3% annual growth in 2019 followed by 1.8% in 2020.”

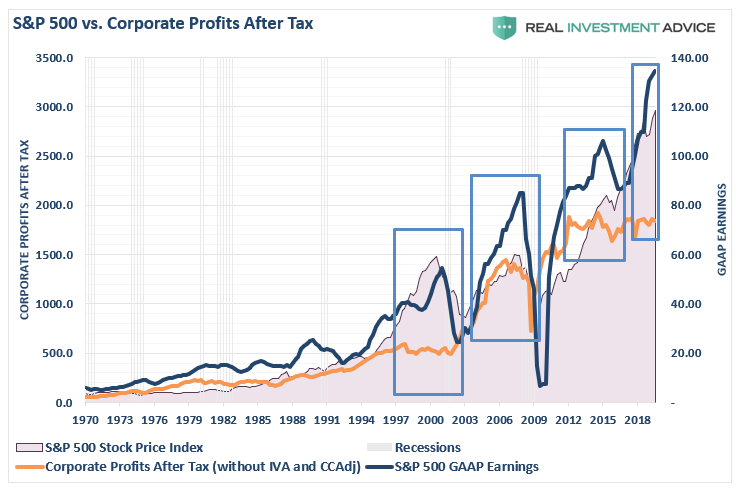

Despite the S&P 500 being up 353% (total return since January 1st, 2009), economic growth has been the weakest in history.

This is why the differential between GAAP earnings and corporate profits is going to be a major challenge for investors going forward.

This was a point Eric noted:

“Stocks are facing a slowing corporate earnings problem in 2020. Quarterly GAAP earnings on the S&P 500 declined by more than -6% on a year-over-year basis in 2019 Q3. This marked the first quarterly year-over-year decline since 2015 Q4 and 2016 Q1 when oil prices were cascading to the downside and the U.S. economy appeared headed toward recession were it not for a major monetary policy intervention stick save.

Thus, corporate earnings growth is not only slowing, but it may be set up to disappoint in the coming quarters.”

As such, stocks will likely once again be reliant on both multiple expansion and share buybacks for further gains in 2020. However, there are limits to just how many shares a company can repurchase given balance sheet constraints of both liquid cash and debt levels.

The bullish case does remain as both fiscal and monetary stimulus remains excessively abundant. Given the recent passage of another $1.4 trillion continue resolution to increase spending without the constraint of a “debt ceiling,” and the Fed continuing with monetary interventions, the amount of money sloshing around the system has to go somewhere.

This is why, despite excessive technical deviations, extraordinary complacency, and extreme bullishness, we remain allocated toward equity risk in portfolios currently.

But, these words were the same as 2018 opened for trading. Just a few weeks later, as Trump launched the “trade war,” exuberance was replaced with pessimism as stocks wiped out all the gains for the month.

Red Flag Of Jihad Raised As 1000s Mourn Death Of Suleimani In Baghdad

In what many middle east experts are calling an “ominous” signal to the west following the assassination of the commander of IRGC’s Quds Force General Qassem Soleimani, a red flag has been hoisted over the holy mosque of Jamkaran in Qom, Iran’s holiest city.

The flag is almost always blue, but according to old Iranian traditions in ancient wars red flags were raised when the enemy commits murder and will remain red until revenge is complete.

Al Manar TV reports that the red flag was raised as speakers in the mosque called: “O Allah, hasten your custodian reappearance,” referring to the reappearance of Imam Al-Mahdi.

The flying of the so-called “flag of jidah” is particularly noteworthy given Leader of the Islamic Revolution in Iran Imam Sayyed Ali Khamenei comments that Soleimani was now a “worldwide resistance icon,” and Hezbollah Secretary General Sayyed Hasan Nasrallah described Soleimani as the “master of Resistance Axis martyrs,” stressing that avenging him and the other martyrs is a duty of all resistance mujahidin around the world.

Meanwhile, AP reports that thousands of mourners chanting “America is the Great Satan” marched in a funeral procession Saturday through Baghdad, a day before the top Iranian commander will be laid to rest in Iran.

The mourners, mostly men in black military fatigues, carried Iraqi flags and the flags of Iran-backed militias that are fiercely loyal to Soleimani. They were also mourning Abu Mahdi al-Muhandis, a senior Iraqi militia commander who was killed in the same strike.

The mourners, many of them in tears, chanted:

“No, No, America,” and “Death to America, death to Israel.”

Mohammed Fadl, a mourner dressed in black, said the funeral is an expression of loyalty to the slain leaders.

“It is a painful strike, but it will not shake us,” he said.

Hadi al-Amiri, who heads a large parliamentary bloc and is expected to replace al-Muhandis as deputy commander of the Popular Mobilization Forces, an umbrella group of mostly Iran-backed militias, was among those paying their final respects.

“Rest assured,” he said before al-Muhandis’ coffin in a video circulated on social media.

“The price of your pure blood will be the exit of U.S. forces from Iraq forever.”

The gates to Baghdad’s Green Zone, which houses government offices and foreign embassies, including the U.S. Embassy, were closed. The U.S. has ordered all citizens to leave Iraq and closed its embassy in Baghdad. Britain and France also warned their citizens to avoid or strictly limit travel in Iraq.

Predicting what happens next is near impossible but this thread from Politico’s Rym Momtaz is as good as we have seen…

1/ Why did Iran militarily escalate in the Gulf lately? Shooting down a US drone, seizing tankers, bombing Saudi oil infrastructure? It wanted to internationalise the conflict. The Strait of Hormuz is where most of the world’s shipping transits. The US chose not to go there.

2/ US also held its own line: a US person killed meant retaliation. It targeted the militia that did the attack. It was reciprocal, but also punitive to send a message. Iran-backed militia escalated against US embassy. US managed the attack, didn’t blow everything up.

3/ US responded to embassy attack, and many lower level attacks by Iranian-backed militias in run-up, by killing, in Iraq, the head of all Iranian-backed anything #Soleimani. US may have just restored some escalation dominance. Whether it’s part of cogent strategy is different Qu

4/ Real US reckless action or declaration of war wld have been attacking Iranian soil. This admin determined that the cost of tolerating Soleimani alive had now exceeded the benefits of not killing him. We must wait and see whether that was the right call, no one knows today.

5/ The most important part of Soleimani’s killing, isn’t his killing (as big as that is), it is the deep US intelligence penetration around Iran’s most important military leader that it revealed. Signals and human intel. This is what is going to spook the Iranian camp the longest.

6/ Why did US claim the #Soleimani kill, instead of following the Israeli ambiguity playbook? US and Israel have different roles and capacities. The US is the mightiest military power around, owning attacks cld be part of deterrence, showing force, restoring escalation dominance.

7/ What happens next: let’s be clear, no one knows for sure, even those who will decide some of the next steps.

The Iranian regime is not suicidal, it is strategic, calculating (even if it miscalculates sometimes), so likelihood of an all-out direct US-Iran war is low.

8/ Khamenei promised response, it must be strong enough to save face internally, for a regime already strained + facing popular dissent, and also be calibrated to avoid provoking a US response inside Iran. Iran response will show whether deterrence restored.

9/ The myth of invincibility that Iran built around Soleimani was a huge recruitment tool, it may also now turn out to be a double-edged sword. How does its most valiant warrior, its most effective US challenger, get picked off so precisely by the US?

10/ Concern for US military, diplo personnel, and citizens, in the region is legit. But allowing it to dictate policy plays into Iran’s hands which weaponises Western sensitivity to human loss, and war weariness, to further destabilise the region unchecked.

11/ There are many so-called anti-imperialists who always criticise Western intervention but justify Iranian/Russian intervention. Iran is not a legit actor in Iraq/Syria/Leb/Yemen. Its crimes there are no less reprehensible than those by the US or colonialists.

12/ Iran is set to announce its next violations of the JCPOA in next few days. That’s another thing to look out for, other than a military retaliation, in wake of today’s #Soleimani kill. Will it escalate to the point of affecting break-out time or not?

Understanding the keys to power…will be a survival requirement for the coming decade.

The past decade was undoubtedly shaped by the policy adopted by the global central banking cartel to flood the world with massive amounts of liquidity (over $15 trillion) to “rescue” markets following the Great Financial Crisis.

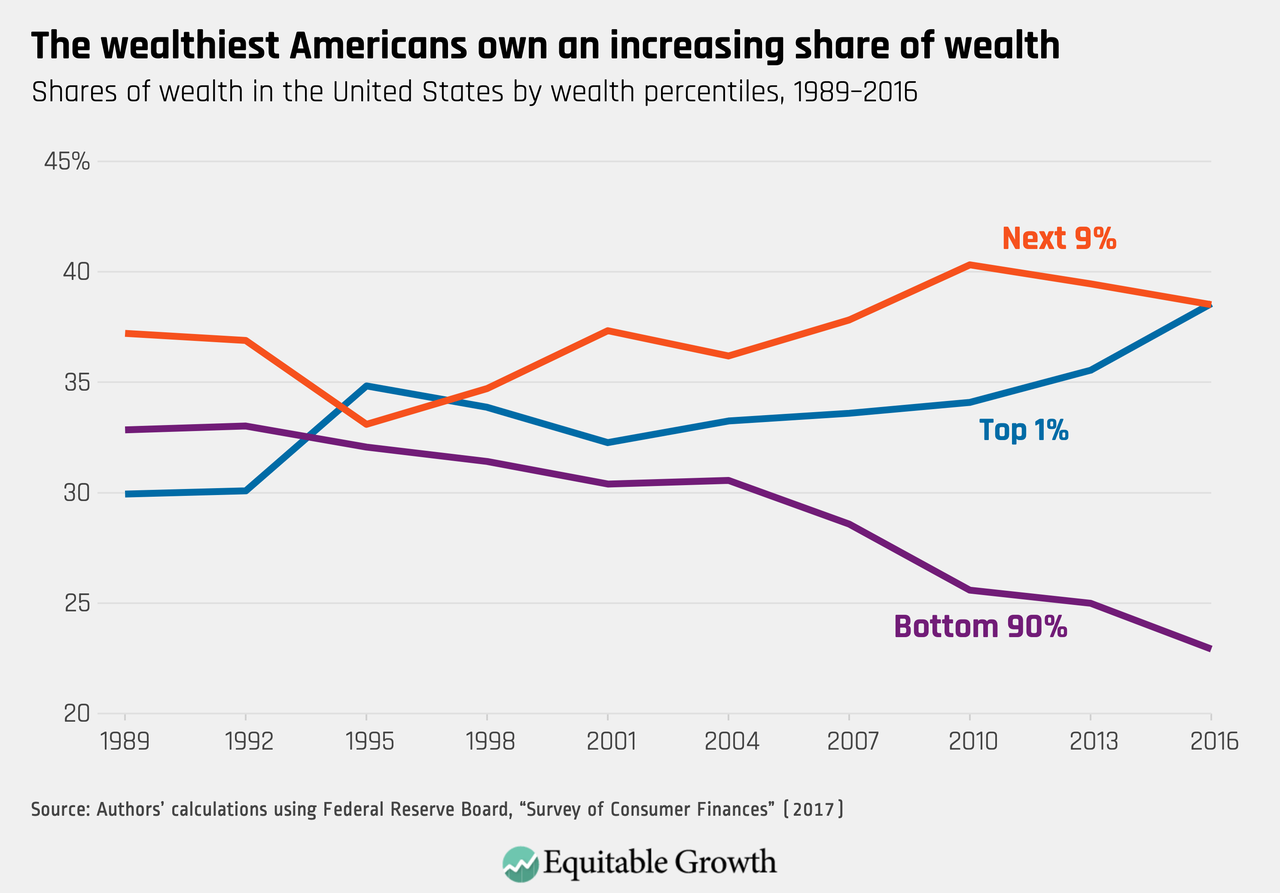

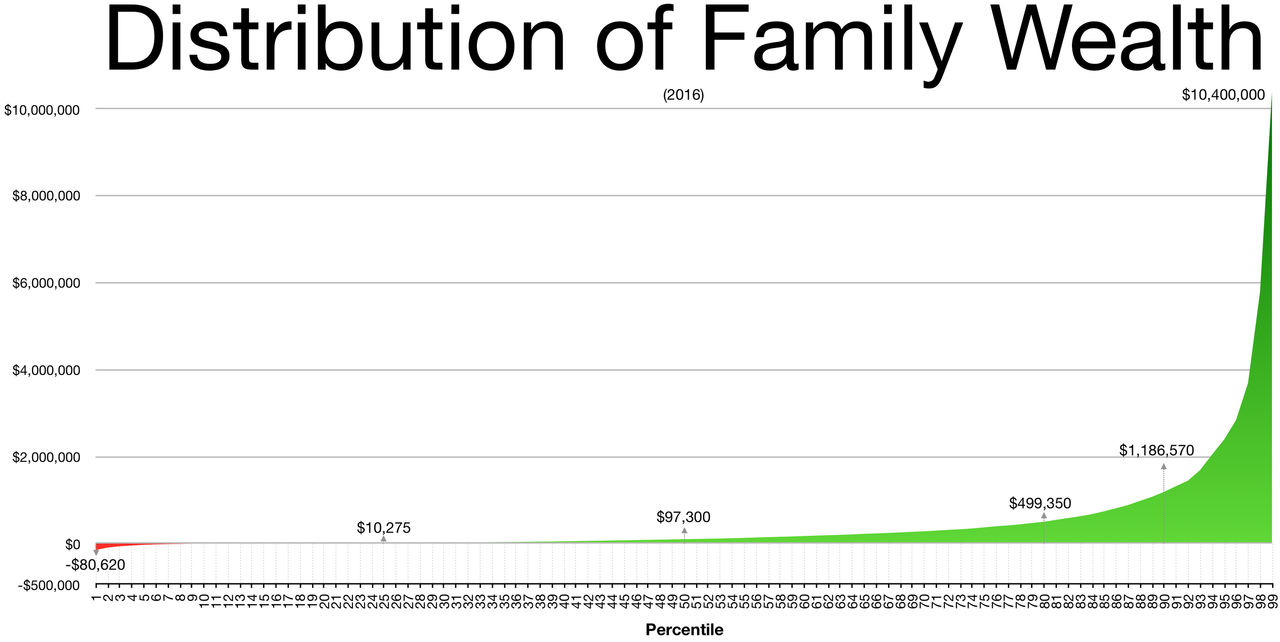

It’s becoming increasingly clear who benefitted most from this: the ultra-rich

As $trillions flowed into financial assets pushing them higher every year throughout the twenty-teens, those who owned those assets — disproportionately the very rich — saw their wealth soar.

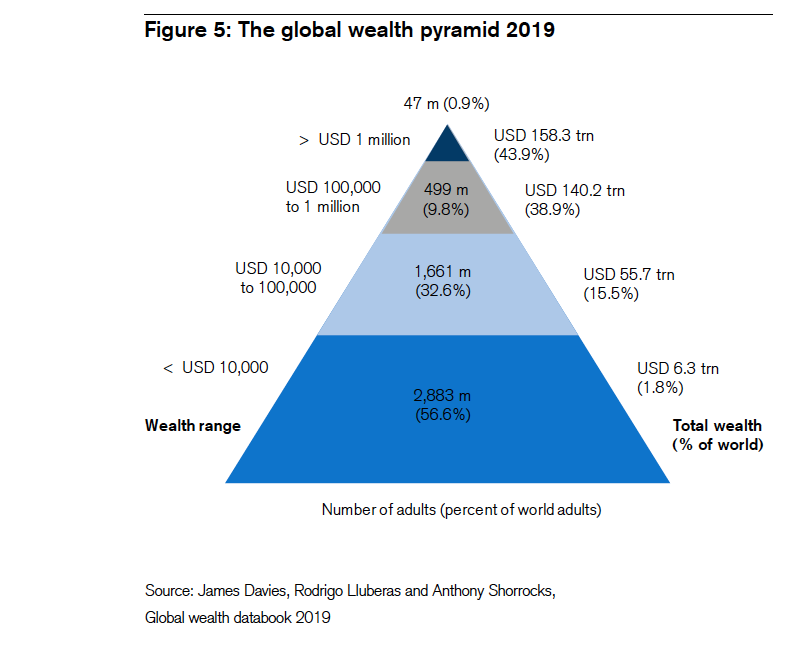

We’re now at the point where the richest 1% owns nearly half of the world’s assets, while the bottom 60% have (often much) less than $10,000 to their name:

How has the distribution of wealth become this distorted?

The harsh simple truth is that those who run the system manipulate it to their benefit.

This is true in both government and industry. Those in power do ‘whatever it takes’ to remain in power and enjoy the fruits of their advantage. Any sort of social ‘duty’ is secondary (at best), and will be sacrificed if necessary.

Perhaps one of the best analyses and explanations of this is put forth by the book The Dictator’s Handbook, by Bruce Bueno de Mesquita and Alastair Smith. For politicians and CEOs alike, maintaining control of the “keys to power” — those who support and enable your rule — is essential.

This is why we’ve ended up with the bastardized crony form of capitalism now in place. Those running the system work hard to reward/punish anyone who aids/threatens their power base.

Like it or not, this is the world in which we live. And it’s critical to understand its nature if we want to avoid becoming unwitting serfs to it.

The most important tenets to be aware of are laid out very effectively in this short video called The Rules For Rulers, created under the supervision of Bueno de Mesquita and Smith:

The above video has very powerful explanatory power when seeking to understand why our leaders act as they do. And its ‘rules’ are tremendously useful in helping us predict how they will act in the future.

As we enter a new decade, one likely to be filled with much more adversity — e.g., economic slowdown, financial turmoil, resource scarcity, social unrest, geopolitical competition, military conflict — we may very well see much more radical responses from our leaders as they act to protect their keys to power.

* * *

Which brings me to an important update: we’ve just secured Bruce Bueno de Mesquita as the keynote speaker for day one of this year’s Peak Prosperity seminar, being held in Sebastopol, CA on May 1-3, 2020. We’re extremely excited about this. We have drawn value from Bruce’s framework for years, and are eager to hear what he foresees ahead in the coming decade.

And speaking of the seminar, we’ve just opened it up for registration to the public. If you’re planning to come, register soon in order to lock in the Early Bird price discount. It’s a 38% savings off of the general admission price. And if you register now, before midnight tomorrow (Thurs, Jan 2), you’ll receive an additional savings of $30 if you use the discount code EB2020.

In addition to Bruce, you’ll also learn from and have the chance to mingle socially with other great minds like Mike Maloney, Charles Hugh Smith, Wolf Richter, Axel Merk, John Rubino, Richard Heinberg, Jeff Clark, and Joe Stumpf. This year’s seminar is already set to be our best ever. And the line-up of speakers keeps getting stronger as the weeks go by.

Chris and I can’t wait to see you there in May. But first, lock in your seat!

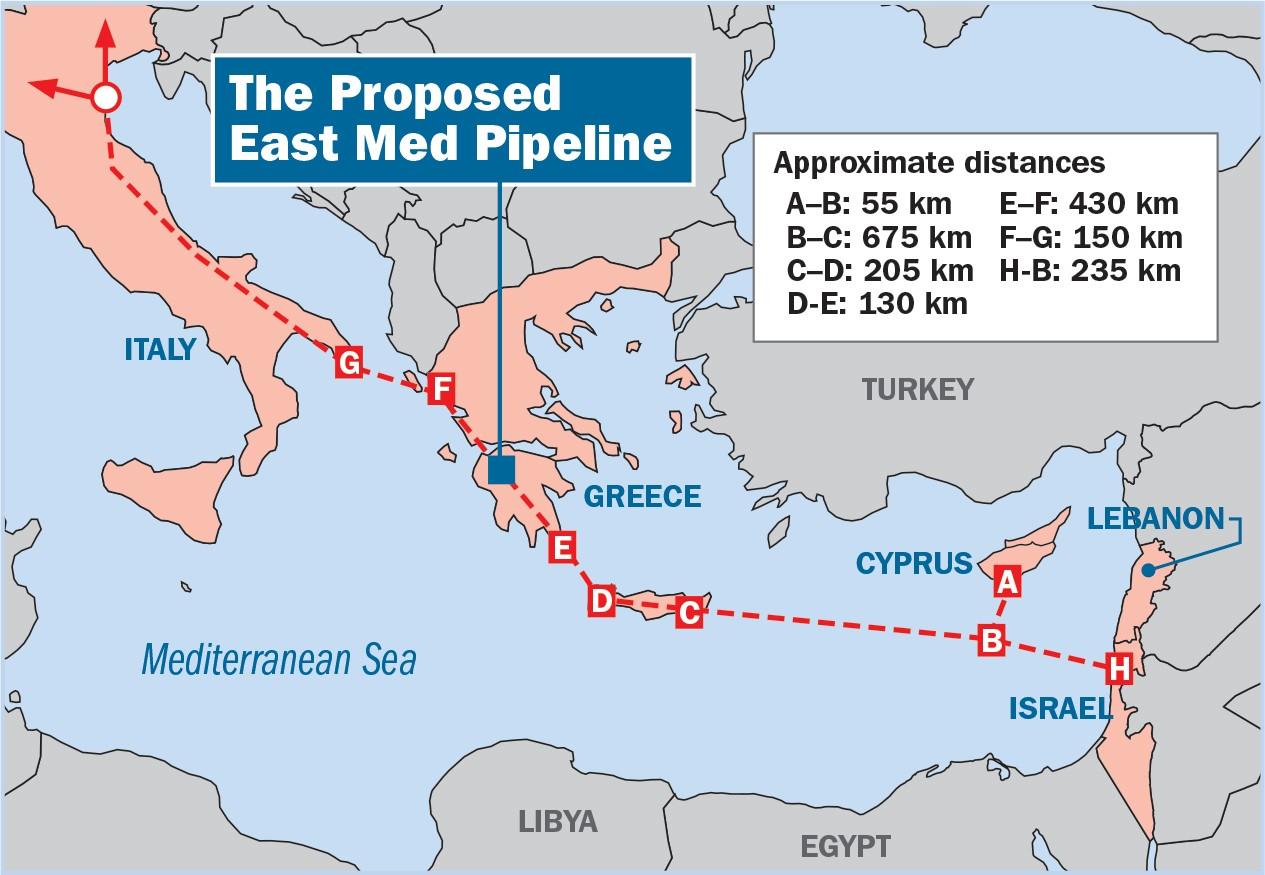

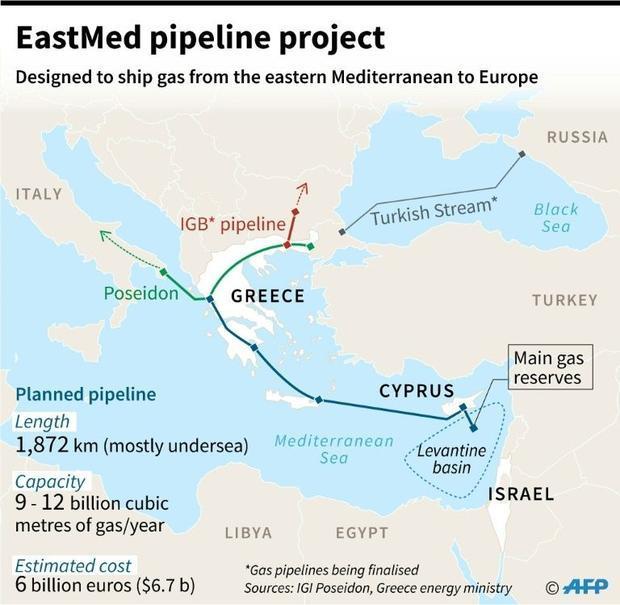

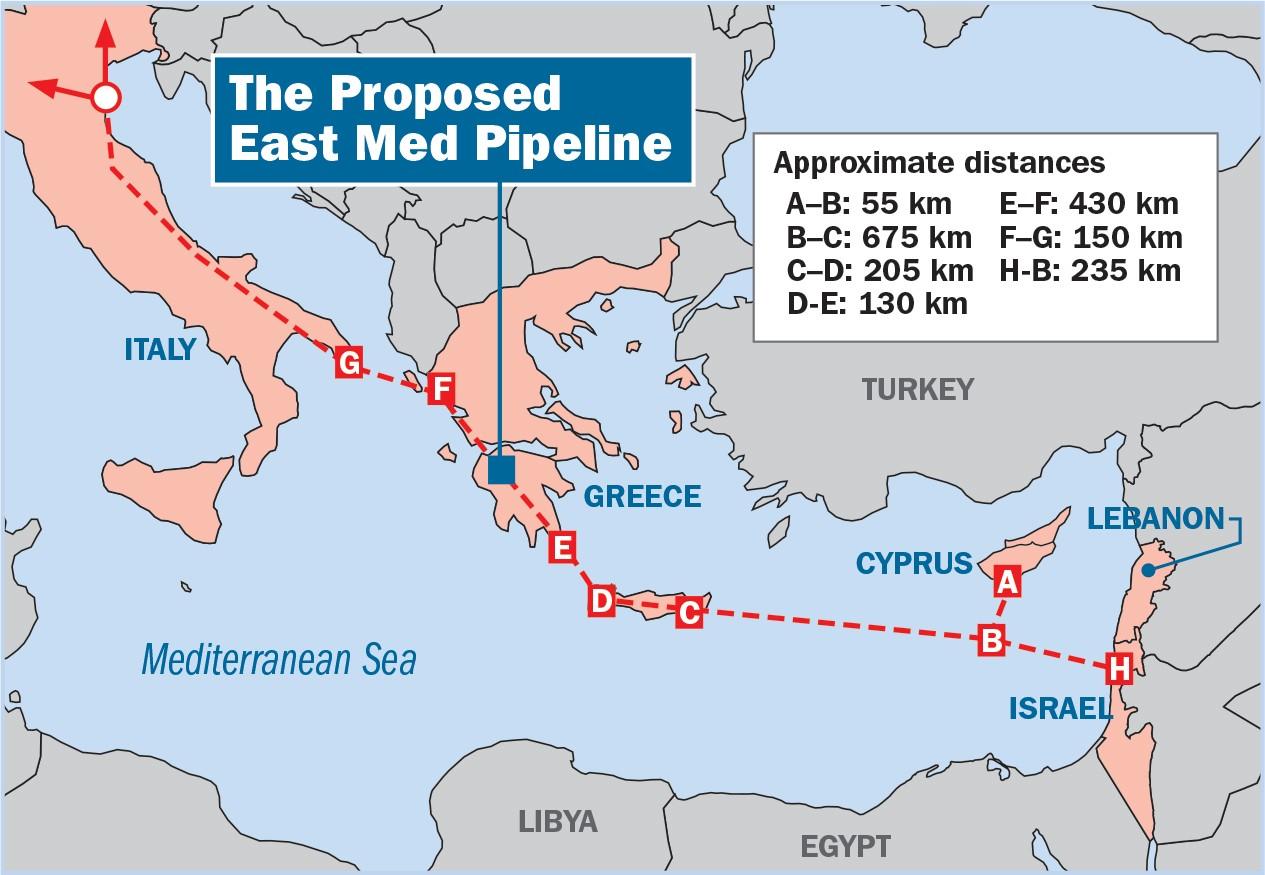

Greece, Israel & Cyprus Sign Landmark EastMed Gas Pipeline Deal Despite Turkey’s Wrath

Long in the works, but coming at a geopolitically sensitive moment for the region given expanding Turkish maritime claims, the East Med gas pipeline deal was signed this week between the countries of Greece, Cyprus and Israel.

The three signed the deal on Thursday to build a 1,900 km (1,180 mile) subsea pipeline to transport supplies from the rapidly advancing gas fields of the eastern Mediterranean to Europe.

A massive undertaking tosupply energy-hungry Europe, the East Med pipeline project was first proposed by Greek energy minister Yannis Maniatis in 2014, and has since been hailed as “the longest and deepest gas pipeline in the world”. At an initial estimated cost of $6-7 billion, it will be financed by “private companies and institutional lenders,” according to prior Israeli Energy Ministry statements.

The energy ministers of Greece, Israel and Cyprus – Kostis Hatzidakis, Yuval Steinitz and Yiorgos Lakkotrypis – attending the signing ceremony on Thursday. Image source: Reuters.

The underground, sub-sea pipeline is proposed to connect Israel, via Cyprus, to Greece and Italy, in a massive construction project estimated to take five or six years to complete, and which once online is expected initially pump 10 billion cubic meters of gas per year.

The energy ministers of Greece, Israel and Cyprus – Kostis Hatzidakis, Yuval Steinitz and Yiorgos Lakkotrypis – attended a signing ceremony in Athens which finalized the project’s moving forward, according to Reuters.

Predictably, Turkey is actively opposing the project, given its own expanding oil and gas exploration claims which have now completely surrounded Cyprus (using the excuse of “rights” based on the contested so-called Turkish Republic of Northern Cyprus) and have even cut into Greece’s Exclusive Economic Zone as well. Per Reuters:

Although Turkey opposes the project, the countries aim to reach a final investment decision by 2022 and have the pipeline completed by 2025 to help Europe diversify its energy resources.

Last month a Turkish official said there was no need to build the EastMed pipeline because the trans-Anatolian pipeline already existed.

Turkey’s Foreign Ministry complained this week that the East Med pipeline “ignored the rights of Turkey and Turkish Cypriots” and thus would be doomed to failure.

Via The Weekly Standard

“The most economical and secure route to utilize the natural resources in the eastern Mediterranean and deliver them to consumption markets in Europe, including our country, is Turkey,” Turkish Foreign Ministry spokesman Hami Aksoy said Thursday, just as the deal was being signed in Athens.

Turkey has lately angered countries like Egypt, Greece and Cyprus over its disputed maritime boundary agreement with Libya, which many see as a big and illegal maritime grab for drilling rights in the southern Mediterranean.

Cypriot President Nicos Anastasiades shot back, however, saying “It (the agreement) … supports a common aim for peace, security and stability in the particularly vulnerable region of the Eastern Mediterranean,” underscoring that it’s actually good for the region’s security in a historically restive area where neighboring countries rarely get along.

Map via the AFP

The transformation of the eastern Mediterranean into an “energy hotspot” could have huge global geopolitical implications, especially given that currently the EU relies on Russia for a third of its gas.

It’s especially southeast Europe that’s been entirely reliant on Russian gas, given its lack of infrastructure. Thus Europe has greeted the project as part of a broader push for “energy diversity” that such other projects as the Nord Stream 2 Russia-Germany pipeline is meant to satisfy as well.

NBC News anchor Chuck Todd is under fire for an openly derisive comment about Trump supporters as effectively delusional drones who want to be lied to. He even added a dig at belief in biblical accounts like Noah’s Ark. It is the latest example of how open bias has become the norm on mainstream media. Imagine if Todd said Obama supporters are ignorant voters who just want to be lied to. This is precisely why the media is now driving some voters to Trump and reinforcing echo-journalism on both sides.

On Sunday’s “Meet the Press,” Todd criticized “misinformation” in the media and referenced a “fascinating” letter to the editor of the Lexington Herald Leader from last January. The letter read, “[W]hy do people support Trump? It’s because people have been trained from childhood to believe in fairy tales… This set their minds up to accept things that make them feel good… The more fairy tales and lies he tells the better they feel . . . Show me a person who believes in Noah’s ark and I will show you a Trump voter.”

Todd used the letter to say to New York Times executive editor Dean Baquet “This gets at something, Dean, that my executive producer likes to say, ‘Hey, voters want to be lied to sometimes.’ They don’t always love being told hard truths.”

Baquet was not sold on the theory and responded “I’m not quite sure I buy that. I’m not convinced that people want to be lied to. I think people want to be comforted, and I think bad politicians sometimes say comforting things to them.”

My first reaction was to recoil at the transparent use of a letter to say indirectly what Todd did not want to say directly. The point however was abundantly clear as was the inherent bias. The fact that Todd and Baquet would have a pseudo intellectual discussion of whether Trump voters are mindless zombies only magnifies the concerns. The issue was presented as whether this is now a clear fact or a developing fact. The question itself however is treated as mainstream and obvious.

Half of this country opposes impeachment and over 40 percent Trump. Are they all mindless drones seeking to be lied to? Stay tuned to NBC for the developing answer.

And now, a new study may indicate why people across the political spectrum tend to ignore opposing views and rest comfortably with echo-journalism.

Researchers at Ohio State University found that people tend to misremember numbers to match their own beliefs. They think that they are basing their views on hard data when they are actually subconsciously tailoring that data to fit their biases.

In the study,participants were given factual numerical information on four different societal issues. The researchers matched the results of two tests to support the views of the subjects and two to contradict those views.

For example, one study showed that there were 12.8 million Mexican immigrants in the United States in 2007 but fewer (11.7 million) in 2014. On the divergent studies, the subjects routinely misremembered the numbers. Thus, for people on the immigration issue, the subjects were most likely to misremember the lower figure in 2014 if they opposed current immigration levels.

This explains a lot, but I still insist that the Chicago Cubs have won 9 out of 10 of the last World Series championships.

{kind=link}

{kind=link}

{kind=link}

{kind=link}