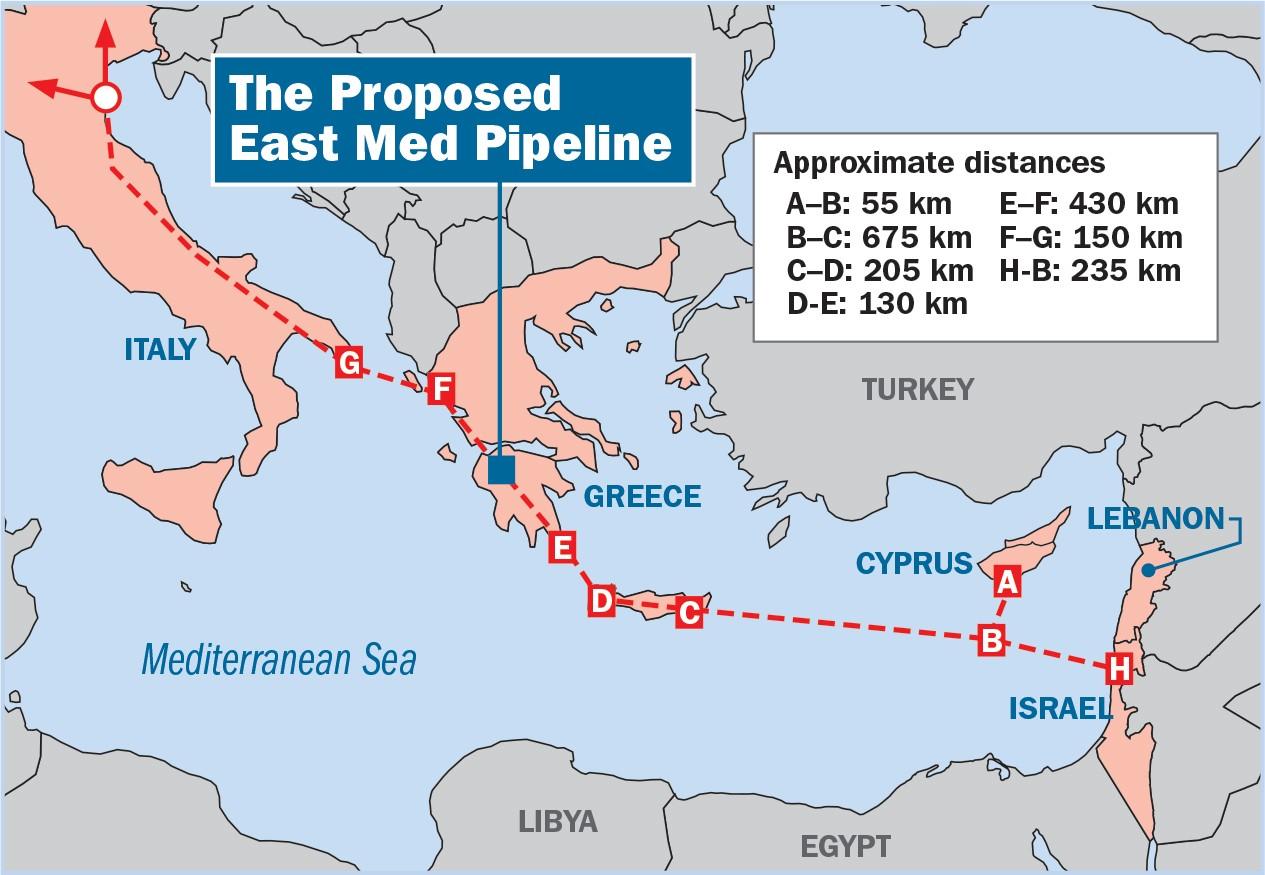

Greece, Israel & Cyprus Sign Landmark EastMed Gas Pipeline Deal Despite Turkey’s Wrath

Long in the works, but coming at a geopolitically sensitive moment for the region given expanding Turkish maritime claims, the East Med gas pipeline deal was signed this week between the countries of Greece, Cyprus and Israel.

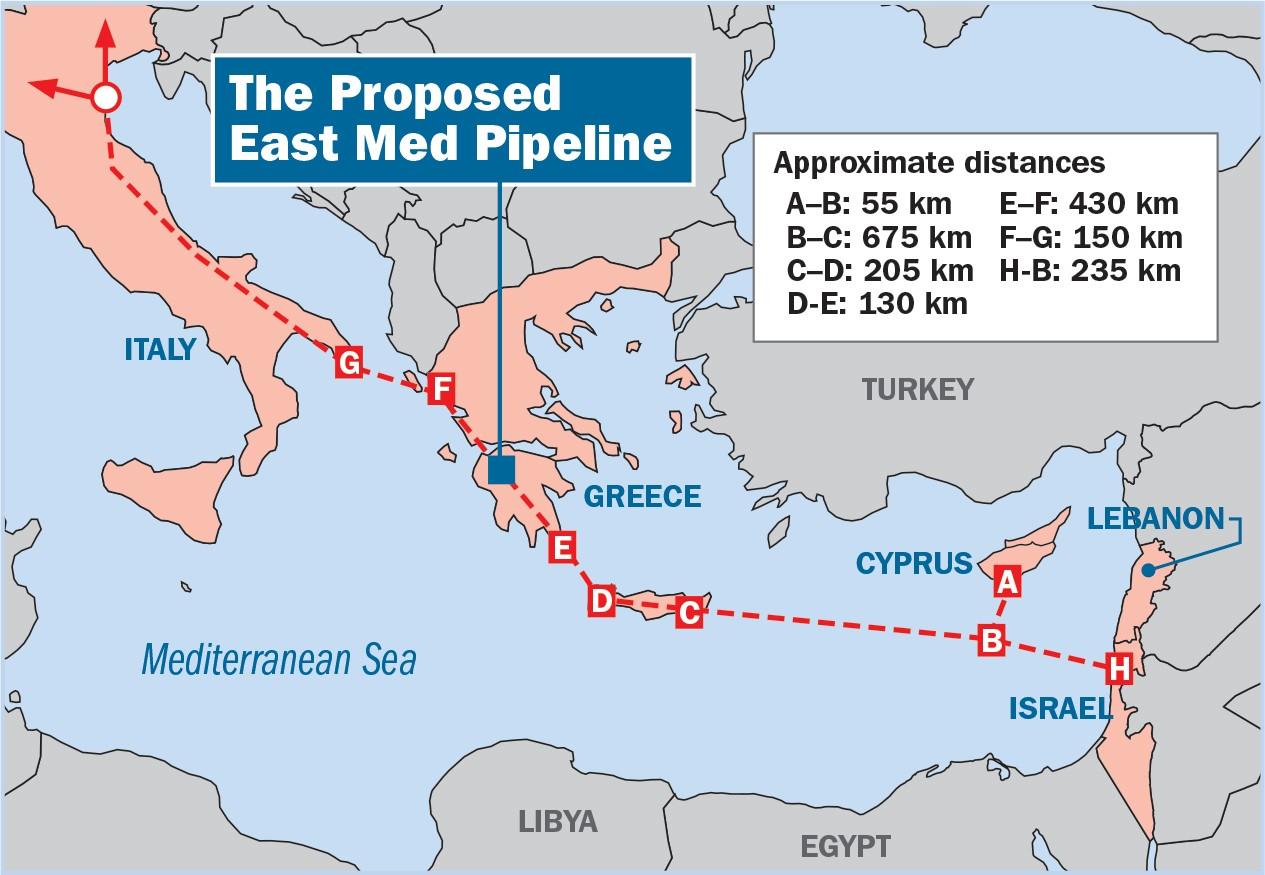

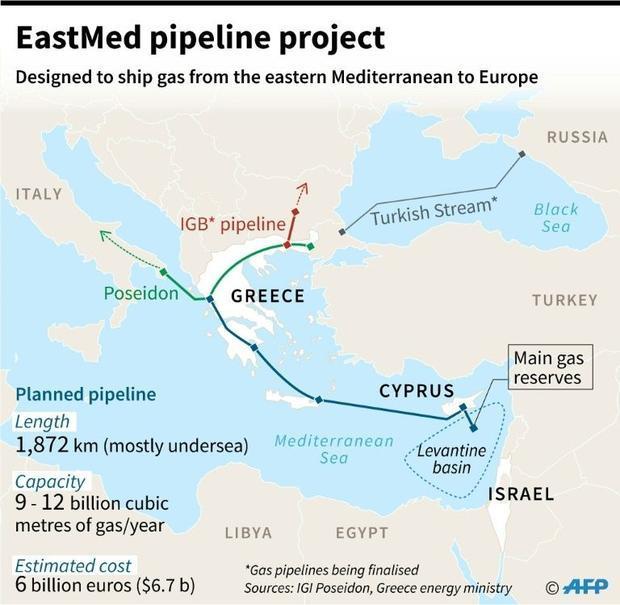

The three signed the deal on Thursday to build a 1,900 km (1,180 mile) subsea pipeline to transport supplies from the rapidly advancing gas fields of the eastern Mediterranean to Europe.

A massive undertaking tosupply energy-hungry Europe, the East Med pipeline project was first proposed by Greek energy minister Yannis Maniatis in 2014, and has since been hailed as “the longest and deepest gas pipeline in the world”. At an initial estimated cost of $6-7 billion, it will be financed by “private companies and institutional lenders,” according to prior Israeli Energy Ministry statements.

The energy ministers of Greece, Israel and Cyprus – Kostis Hatzidakis, Yuval Steinitz and Yiorgos Lakkotrypis – attending the signing ceremony on Thursday. Image source: Reuters.

The underground, sub-sea pipeline is proposed to connect Israel, via Cyprus, to Greece and Italy, in a massive construction project estimated to take five or six years to complete, and which once online is expected initially pump 10 billion cubic meters of gas per year.

The energy ministers of Greece, Israel and Cyprus – Kostis Hatzidakis, Yuval Steinitz and Yiorgos Lakkotrypis – attended a signing ceremony in Athens which finalized the project’s moving forward, according to Reuters.

Predictably, Turkey is actively opposing the project, given its own expanding oil and gas exploration claims which have now completely surrounded Cyprus (using the excuse of “rights” based on the contested so-called Turkish Republic of Northern Cyprus) and have even cut into Greece’s Exclusive Economic Zone as well. Per Reuters:

Although Turkey opposes the project, the countries aim to reach a final investment decision by 2022 and have the pipeline completed by 2025 to help Europe diversify its energy resources.

Last month a Turkish official said there was no need to build the EastMed pipeline because the trans-Anatolian pipeline already existed.

Turkey’s Foreign Ministry complained this week that the East Med pipeline “ignored the rights of Turkey and Turkish Cypriots” and thus would be doomed to failure.

Via The Weekly Standard

“The most economical and secure route to utilize the natural resources in the eastern Mediterranean and deliver them to consumption markets in Europe, including our country, is Turkey,” Turkish Foreign Ministry spokesman Hami Aksoy said Thursday, just as the deal was being signed in Athens.

Turkey has lately angered countries like Egypt, Greece and Cyprus over its disputed maritime boundary agreement with Libya, which many see as a big and illegal maritime grab for drilling rights in the southern Mediterranean.

Cypriot President Nicos Anastasiades shot back, however, saying “It (the agreement) … supports a common aim for peace, security and stability in the particularly vulnerable region of the Eastern Mediterranean,” underscoring that it’s actually good for the region’s security in a historically restive area where neighboring countries rarely get along.

Map via the AFP

The transformation of the eastern Mediterranean into an “energy hotspot” could have huge global geopolitical implications, especially given that currently the EU relies on Russia for a third of its gas.

It’s especially southeast Europe that’s been entirely reliant on Russian gas, given its lack of infrastructure. Thus Europe has greeted the project as part of a broader push for “energy diversity” that such other projects as the Nord Stream 2 Russia-Germany pipeline is meant to satisfy as well.

NBC News anchor Chuck Todd is under fire for an openly derisive comment about Trump supporters as effectively delusional drones who want to be lied to. He even added a dig at belief in biblical accounts like Noah’s Ark. It is the latest example of how open bias has become the norm on mainstream media. Imagine if Todd said Obama supporters are ignorant voters who just want to be lied to. This is precisely why the media is now driving some voters to Trump and reinforcing echo-journalism on both sides.

On Sunday’s “Meet the Press,” Todd criticized “misinformation” in the media and referenced a “fascinating” letter to the editor of the Lexington Herald Leader from last January. The letter read, “[W]hy do people support Trump? It’s because people have been trained from childhood to believe in fairy tales… This set their minds up to accept things that make them feel good… The more fairy tales and lies he tells the better they feel . . . Show me a person who believes in Noah’s ark and I will show you a Trump voter.”

Todd used the letter to say to New York Times executive editor Dean Baquet “This gets at something, Dean, that my executive producer likes to say, ‘Hey, voters want to be lied to sometimes.’ They don’t always love being told hard truths.”

Baquet was not sold on the theory and responded “I’m not quite sure I buy that. I’m not convinced that people want to be lied to. I think people want to be comforted, and I think bad politicians sometimes say comforting things to them.”

My first reaction was to recoil at the transparent use of a letter to say indirectly what Todd did not want to say directly. The point however was abundantly clear as was the inherent bias. The fact that Todd and Baquet would have a pseudo intellectual discussion of whether Trump voters are mindless zombies only magnifies the concerns. The issue was presented as whether this is now a clear fact or a developing fact. The question itself however is treated as mainstream and obvious.

Half of this country opposes impeachment and over 40 percent Trump. Are they all mindless drones seeking to be lied to? Stay tuned to NBC for the developing answer.

And now, a new study may indicate why people across the political spectrum tend to ignore opposing views and rest comfortably with echo-journalism.

Researchers at Ohio State University found that people tend to misremember numbers to match their own beliefs. They think that they are basing their views on hard data when they are actually subconsciously tailoring that data to fit their biases.

In the study,participants were given factual numerical information on four different societal issues. The researchers matched the results of two tests to support the views of the subjects and two to contradict those views.

For example, one study showed that there were 12.8 million Mexican immigrants in the United States in 2007 but fewer (11.7 million) in 2014. On the divergent studies, the subjects routinely misremembered the numbers. Thus, for people on the immigration issue, the subjects were most likely to misremember the lower figure in 2014 if they opposed current immigration levels.

This explains a lot, but I still insist that the Chicago Cubs have won 9 out of 10 of the last World Series championships.

Times Of London Names Iranian General To List Of “2020 Rising Stars” Day Before Assassination

How’s this for bad timing?

In a list consisting mostly of foreign dignitaries that are known to only a handful of people in the UK, US and the rest of the English-speaking world, the Times of London named now-deceased Iranian General Qassem Suleimani to its list of “Twenty faces to look out for in 2020.”

The list, published on the Times’ website early Thursday morning, just hours before Suleimani was killed during a drone strike in Baghdad, also included Princess Leonor of Spain, Nigerian Afrobeat star David Adedeji (better known by his stage name Davido) and Italian politician Giorgia Meloni.

But the highlight (at least, in hindsight) will likely be Suleimani, who is included as the list’s final entry. In the description, Times’ writer Richard Spencer claims that 2020 could be the year that the long-serving general finally “cement[s] his reputation as the Machiavelli of the Middle East – or prove that even the smartest operators can suffer hubris”.

Moving on, Spencer writes that the Iranian general was already well-known to intelligence agencies as “the guiding force of Iran’s cross-border operations.”

Offering a massive dose of irony, the Times noted how Suleimani’s movements are “well-signalled” due to his status as a celebrity general, who “even poses for selfies” with militia leaders across the region.

Spencer noted that Suleiman had succeeded in making Iran’s long-held dream of a “land corridor from Tehran to the Mediterranean” a reality (such a stretch is apparently controlled by Iran-backed militias, from Iraq, to Lebanon, and everywhere in between (Syria).

Finally, it was noted that Suleimani’s popularity had taken a dive in the months and years before his death, evidenced by the protests in Iraq and Lebanon over Iran’s growing influence.

The piece concluded by claiming that “if General Soleimani can hold the line, he will have shown he deserves the trust of Iran’s Supreme Leader.”

Since his death, the general has been cited by pundits as a potential successor to the Ayatollah.

Interested parties can read the entire entry below:

This will be the year in which a slight, grey-haired general will cement his reputation as the Machiavelli of the Middle East — or prove that even the smartest operators can suffer hubris (Richard Spencer writes).

A decade ago, Qassem Soleimani was already known to intelligence agencies as the guiding force of Iran’s cross-border operations. He was the link man to Hezbollah in Lebanon and it was he who masterminded the strategy whereby a “resistance” movement based on Shia militias bombed and shot British and American troops out of Iraq.

Now his movements are well-signalled. As head of the al-Quds Force, the overseas arm of the Revolutionary Guard, he backs militia leaders across the Levant and Yemen, and even poses for selfies with them.

Deftly reacting to the Syrian war, American uncertainty and the conflict against Isis, he has established Iran’s long-held dream of a land corridor from Tehran to the Mediterranean, controlled by loyal militias.

But he is experiencing resistance. Popular protests in Lebanon and Iraq may not have been hostile to Iran when they began but, seeing them as a threat, Major-General Soleimani has taken action. He has been to Baghdad at least twice, summoned militia leaders and pro-Iran politicians, and ordered them to stand firm. In Lebanon, where Iran’s ally Hezbollah has tried to market itself as a nationalist force, he has been more subtle.

A recent opinion poll, though, suggested that Hezbollah had lost support rapidly from the Christian and Sunni communities, even as more of Iraq’s Shia population turn against Iran.

If General Soleimani can hold the line, he will have shown he deserves the trust of Iran’s Supreme Leader, Ayatollah Ali Khamenei.

The general’s inclusion on the list is just another reason to doubt claims that the assassination was planned to distract from Trump’s upcoming trial or the release of unflattering government documents

…’Cause I’ve had the time of my life..and I owe it all to you..

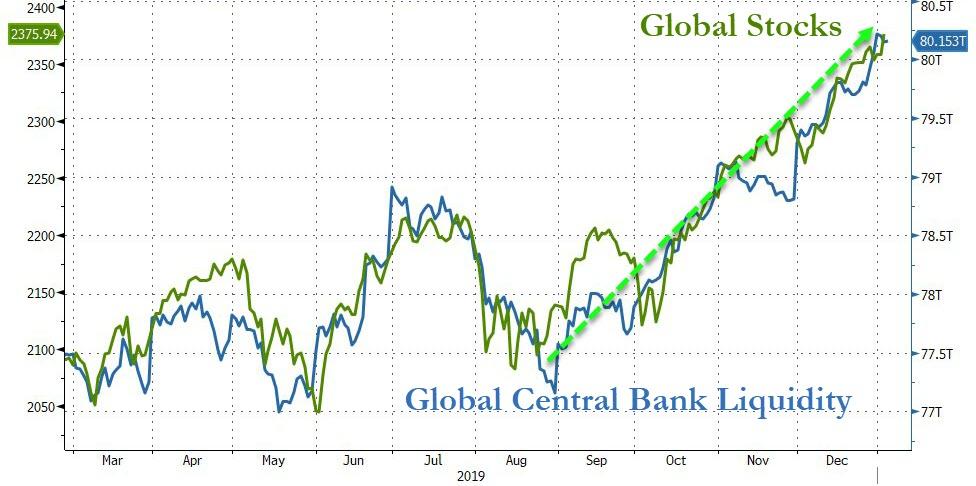

The original song from Dirty Dancing is one of my all time favourites and somehow reminds me of the Global Markets performance this year.Every conceivable asset class (except cash) posted positive returns ,thanks to the LIQUIDITY provided by global central banks. The Fed, in my view, moved to implement the “ high pressure economy” regime outlined in former chair Janet Yellen’s 2014 speech at the Boston Fed Reserve bank.

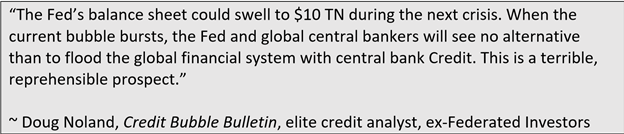

Indirecly this document suggest the US central Bank has returned to the Greenspan approach to bubbles- they will deal with the consequences once it pops.

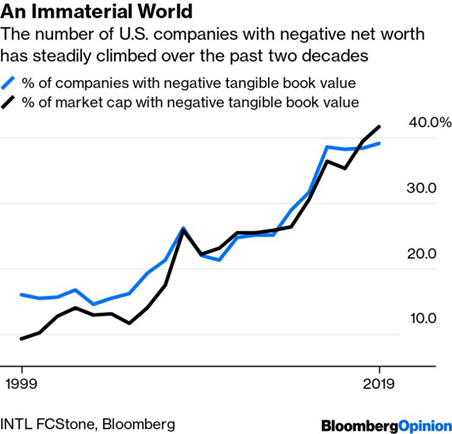

The chart below explains the LIQUIDITY story.

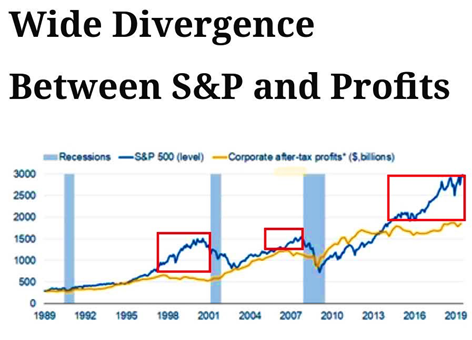

Gone are the good old days when Earnings used to be tailwind for market valuations.

The polarising performance of US markets.

The two stocks, Apple and Microsoft, each having a market cap of USD 1 trillion have contributed the most to 2019’s total stock-market returns and also hold that position for the entire decade.

The number of Zombie companies continue to rise along with their market caps.

The above charts were examples of distortion created by excess pumping of money.

Jerome Powell raised the bar for raising rates significantly whereas the bar for lowering rates has gone down. More evidence that Central Bankers will tolerate higher inflation and low or negative real rates.

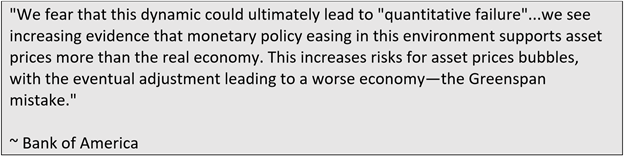

BOFA has a crystal ball and they see the endgame approaching .

The global economy has entered a period called ‘slowbalization,’ which is the result of geopolitical shifts and secular trends that have slowed down globalization or, in some cases, completely reversed it. A global manufacturing recession was sparked by changes in consumer preferences that have roiled manufacturing hubs and complex supply chains in developed and emerging markets. Almost every major central bank across the world is easing at the moment in hopes of generating a mini-cycle trough to rebound growth in 2020.

(Ben Hunt via The Eplison Theory)

Neel Kashkari has just become the voting member of FOMC for the year 2020 and he wants to redistribute wealth in the society.

The farce is complete.

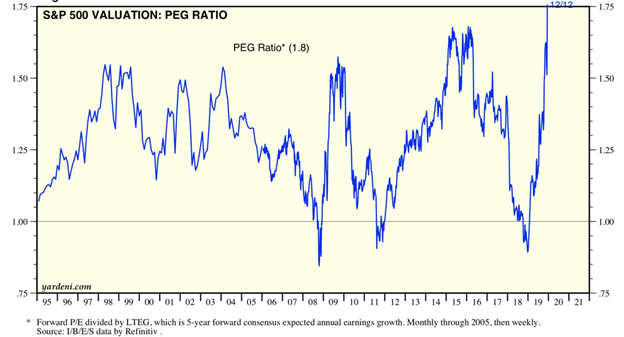

When markets run on nothing but multiple expansion the PEG ratio (price earnings growth) may just skyrocket higher. In this case: Through the historic roof. Don’t let anyone tell you this market is cheap. It’s not, it’s the most expensive in our lifetimes on a PEG basis.

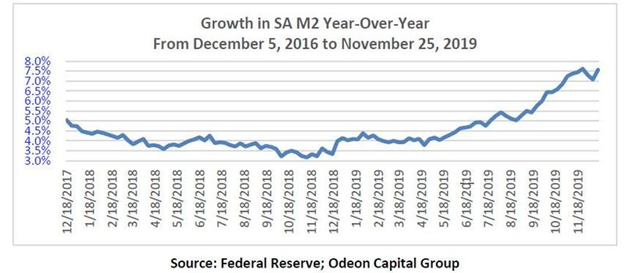

US M2 growth y-o-y which was growing at 3.2% in November 2018, is now growing at 7.6% y-o-y. The economy is not growing rapidly enough to absorb this growth and the competition from the money and bond markets, domestically and overseas, is not compelling.

Money supply is expanding at above average rates and share growth is not. Consequently, share values are expanding — not likely to stop soon.

Winter is coming

Market Outlook

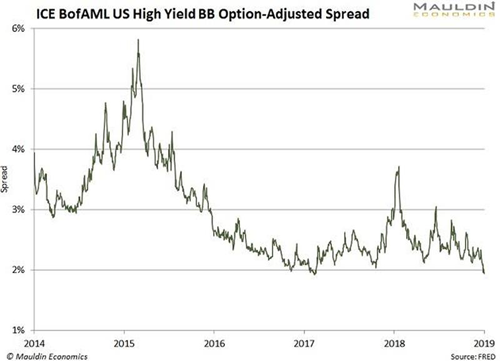

Sure, a lot of things could pop the bubble, if you think it’s a bubble. Inflation fears could do it, lots more of Treasury supply, etc. And the flows just keep on coming. High-yield spreads have dropped to historic lows and I give more credence to signals from credit spreads than equity markets.

But the inflection point in my view was the collapse of WeWork which changed the sentiment away from loss making enterprises in the hopes of dominating market share, to more efficient operations focused on at least attempting to generate profits. Second, the hike by the RiskBank this month to Zero is a sign that negative rates have lost their allure. I couldn’t help but put this photo of Germans standing in line at Cologne outside Degussa showroom to buy precious metals since their hard-earned money lying in bank deposits is now earning negative interest rates.

Finally, the Dollar index (DXY), which was in a rising trend for some time and was supported by a strong US GDP growth is in the process of rolling over and making lower highs and lower lows. Trump and Fed would be happy at this achievement but who knows what a falling dollar bring with it.

Overall, these developments would appear to support some whiff of reflation and higher inflationary expectations,

1). Shift away from buying cash- burning market share to buying profits.

2). Weaker dollar raises the prices of imports and create domestic pricing power.

What are the possibilities regarding a potential “normalization of repo liquidity post-run? In the year 1999-2000 Fed had similarly flooded the system with massive liquidity to tide over Y2K related issues and when it went to withdraw that liquidity there was sharp negative reaction by stock market. I guess we will see the same towards the end of first quarter 2020. Emerging markets will be bid till the time Dollar index is soft. In terms of bonds, the prospect of less certain funding and higher deficits might also stifle some enthusiasm. Commodities could outperform stocks as a class.

What if the Fed finds that it can’t step back from repo operations due to fear of financial dislocations? In this case, stocks could see a more aggressive “melt-up” helped by tsunami of Fed liquidity, but the dollar will fall more, and GOLD will benefit.

The Irish Spend More On Eating-Out Than Any Other European Nation

According to new data from Eurostat, households across the European Union spend more than €600 billion on catering services such as restaurants, cafes and canteens.

Ireland devoted the largest share of household expenditure to eating out in 2018 at 14.4 percent, followed by Spain with 13 percent and Malta’s 12.6 percent.

Romania was at the very bottom of the eating out spending league at just 1.9 percent household income in 2018. Romania’s spending is decreasing and it stood at 2.9 percent back in 2008.

The ruling Establishment has learnt a profound lesson from the debacle over Iraqi Weapons of Mass Destruction. The lesson they have learnt is not that it is wrong to attack and destroy an entire country on the basis of lies. They have not learnt that lesson despite the fact the western powers are now busily attacking the Iraqi Shia majority government they themselves installed, for the crime of being a Shia majority government.

No, the lesson they have learnt is never to admit they lied, never to admit they were wrong. They see the ghost-like waxen visage of Tony Blair wandering around, stinking rich but less popular than an Epstein birthday party, and realise that being widely recognised as a lying mass murderer is not a good career choice. They have learnt that the mistake is for the Establishment ever to admit the lies.

The Establishment had to do a certain amount of collective self-flagellation over the non-existent Iraqi weapons of mass destruction, over which they precipitated the death and maiming of millions of people. Only a very few outliers, like the strange Melanie Phillips, still claimed the WMD really did exist, and her motive was so obviously that she supported any excuse to kill Muslims that nobody paid any attention. Her permanent pass to appear on the BBC was upgraded. But by and large everyone accepted the Iraqi WMD had been a fiction. The mainstream media Blair/Bush acolytes like Cohen, Kamm and Aaronovitch switched to arguing that even if WMD did not exist, Iraq was in any case better off for having so many people killed and its infrastructure destroyed.

These situations are now avoided by the realisation of the security services that in future they just have to brazen it out. The simple truth of the matter – and it is a truth – is this. If the Iraq WMD situation occurred today, and the security services decided to brazen it out and claim that WMD had indeed been found, there is not a mainstream media outlet that would contradict them.

The security services outlet Bellingcat would publish some photos of big missiles planted in the sand. The Washington Post, Guardian, New York Times, BBC and CNN would republish and amplify these pictures and copy and paste the official statements from government spokesmen. Robert Fisk would get to the scene and interview a few eye witnesses who saw the missiles being planted, and he would be derided as a senile old has-been. Seymour Hersh and Peter Hitchens would interview whistleblowers and be shunned by their colleagues and left off the airwaves. Bloggers like myself would be derided as mad conspiracy theorists or paid Russian agents if we cast any doubt on the Bellingcat “evidence”. Wikipedia would ruthlessly expunge any alternative narrative as being from unreliable sources. The Integrity Initiative, 77th Brigade, GCHQ and their US equivalents would be pumping out the “Iraqi WMD found” narrative all over social media. Mad Ben Nimmo of the Atlantic Council would be banning dissenting accounts all over the place in his role as Facebook Witchfinder-General.

Does anybody seriously wish to dispute this is how the absence of Iraqi WMD would be handled today, 16 years on?

If you do wish to doubt this could happen, look at the obviously fake narrative of the Syrian government chemical weapons attacks on Douma. The pictures published on Bellingcat of improvised chlorine gas missiles were always obviously fake. Remember this missile was supposed to have smashed through ten inches of solid, steel rebar reinforced concrete.

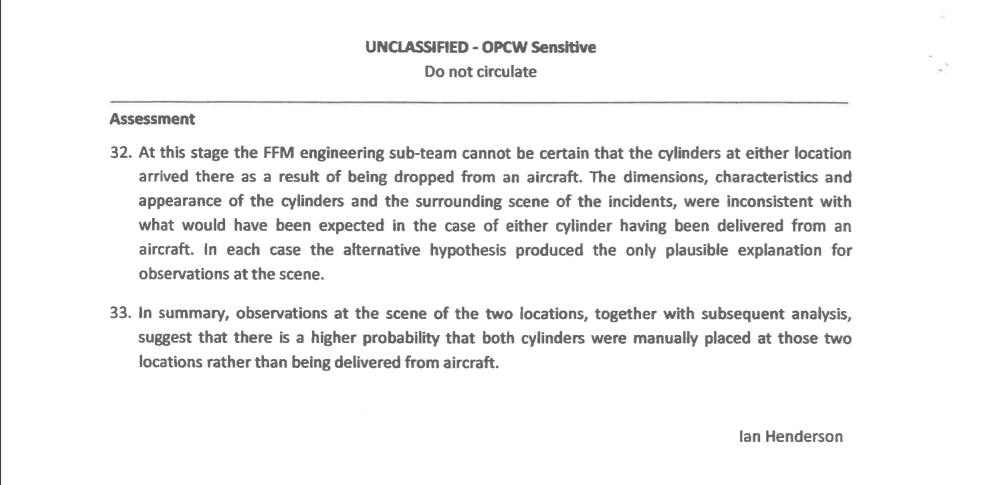

As I reported back in May last year, that the expert engineers sent to investigate by the Organisation for the Prohibition of Chemical Weapons (OPCW) did not buy into this is hardly surprising.

That their findings were deliberately omitted from the OPCW report is very worrying indeed. What became still more worrying was the undeniable evidence that started to emerge from whistleblowers in the OPCW that the toxicology experts had unanimously agreed that those killed had not died from chlorine gas attack. The minutes of the OPCW toxicology meeting really do need to be read in full.

“No nerve agents had been detected in environmental or bio samples”

“The experts were conclusive in their statements that there was no correlation between symptoms and chlorine exposure”

I really do urge you to click on the above link and read the entire minute. In particular, it is impossible to read that minute and not understand that the toxicology experts believed that the corpses had been brought and placed in position.

“The experts were also of the opinion that the victims were highly unlikely to have gathered in piles at the centre of the respective apartments, at such a short distance from an escape from any toxic chlorine gas to much cleaner air”.

So the toxicology experts plainly believed the corpse piles had been staged, and the engineering experts plainly believed the cylinder bombs had been staged. Yet, against the direct evidence of its own experts, the OPCW published a report managing to convey the opposite impression – or at least capable of being portrayed by the media as giving the opposite impression.

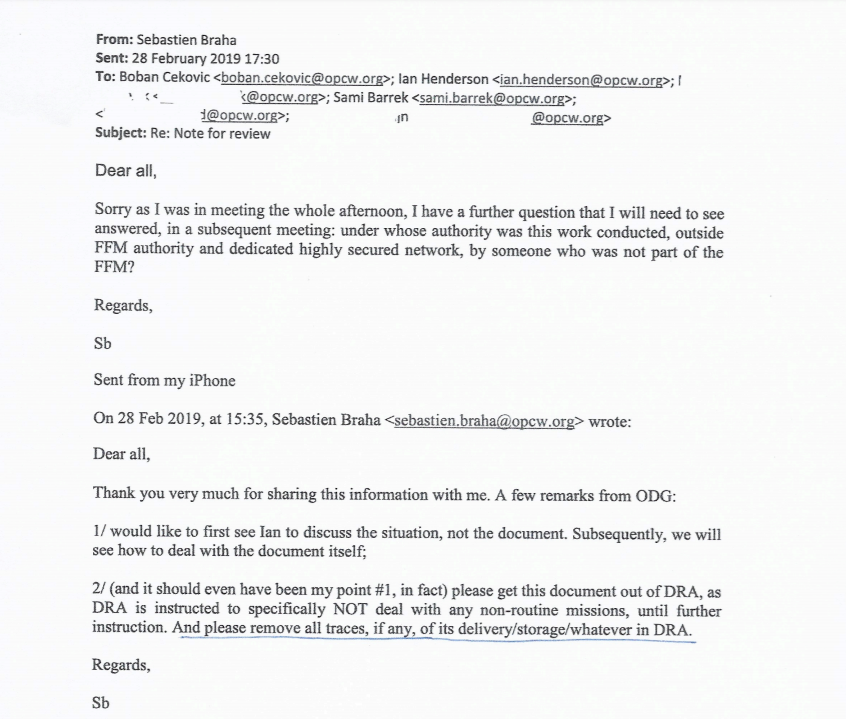

How then did the OPCW come to do this? Rather unusually for an international organisation, the OPCW Secretariat is firmly captured by the Western states, largely because it covers an area of activity which is not of enormous interest to the political elites of developing world states, and many positions require a high level of technical qualification. It was also undergoing a change of Director General at the time of the Douma investigation, with the firmly Francoist Spanish diplomat Fernando Arias taking over as Director General and the French diplomat Sebastian Braha effectively running the operation as the Director-General’s chef de cabinet, working in close conjunction with the US security services. Braha simply ordered the excision of the expert opinions on engineering and toxicology, and his high-handedness worked, at least until whistleblowers started to reveal the truth about Braha as a slimy, corrupt, lying war hawk.

FFM here stands for Fact Finding Mission and ODG for Office of the Director General. After a great deal of personal experience dealing with French diplomats, I would say that the obnoxious arrogance revealed in Braha’s instructions here is precisely what you would expect. French diplomats as a class are a remarkably horrible and entitled bunch. Braha has no compunction about simply throwing around the weight of the Office of the Director General and attempting to browbeat Henderson.

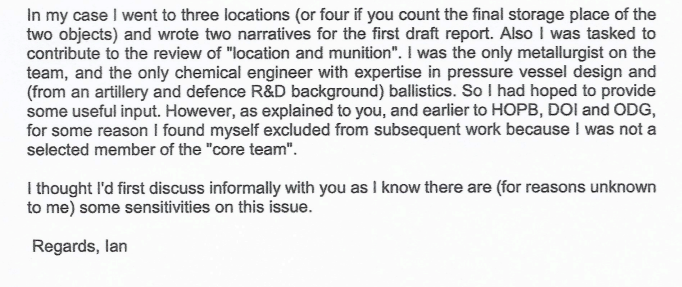

We see now how the OPCW managed to produce a report which was the opposite of the truth. Ian Henderson, the OPCW engineer who had visited the site and concluded that the “cylinder bombs” were fakes, had suddenly become excluded from the “fact finding mission” when it had been whittled down to a “core group” – excluding any engineers (and presumably toxicologists) who would seek to insert inconvenient facts into the report.

France of course participated, alongside the US and UK, in missile strikes against Syrian government positions in response to the non-existent chlorine gas attacks on Douma. I was amongst those who had argued from day one that the western Douma narrative was inherently improbable. The Douma enclave held by extreme jihadist, western and Saudi backed forces allied to ISIL, was about to fall anyway. The Syrian government had no possible military advantage to gain by attacking it with two small improvised chemical weapons, and a great deal to lose in terms of provoking international retaliation.

That the consequences of the fake Douma incident were much less far-reaching than they might have been, is entirely due (and I am sorry if you dislike this but it is true) to the good sense of Donald Trump. Trump is inclined to isolationism and the fake “Russiagate” narrative promoted by senior echelons of his security services had led him to be heavily sceptical of them. He therefore refused, against the united persuasion of the hawks, to respond to the Douma “attack” by more than quick and limited missile strikes. I have no doubt that the object of the false flag was to push the US into a full regime change operation, by falsifying a demonstration that a declared red line on chemical weapon use had been crossed.

There is no doubt that Douma was a false flag. The documentary and whistleblower evidence from the OPCW is overwhelming and irrefutable. In addition to the two whistleblowers reported extensively by Wikileaks and the Courage Foundation, the redoubtable Peter Hitchens has his own whistleblowers inside OPCW who may well be different persons. It is also great entertainment as well as enlightening to read Hitchens’ takedown of Bellingcat on the issue.

But there are much deeper questions about the Douma false flag. Did the jihadists themselves kill the “chlorine victims” for display or were these just bodies from the general fighting? The White Helmets were co-located with the jihadist headquarters in Douma, and involved in producing and spreading the fake evidence. How far were the UK and US governments, instrumental in preparing the false flag? That western governments, including through the White Helmets and their men at the OPCW, were plainly seeking to propagate this false flag, to massively publicise and to and make war capital out of it, is beyond dispute. But were they involved in the actual creation of the fake scene? Did MI6 or the CIA initiate this false flag through the White Helmets or the Saudi backed jihadists? That is unproven but seems to me very probable. It is also worth noting the coincidence in time of the revelation of the proof of the Douma false flag and the death of James Le Mesurier.

Now let me return to where I started. None of the New York Times, the Washington Post, the BBC, the Guardian nor CNN – all of which reported the Douma chemical attack very extensively as a real Syrian government atrocity, and used it to editorialise for western military intervention in Syria – none of them has admitted they were wrong. None has issued any substantive retraction or correction. None has reported in detail and without bias on the overwhelming evidence of foul play within the OPCW.

Those sources who do publish the truth – including the few outliers in mainstream media such as Peter Hitchens and Robert Fisk – continue to be further marginalised, attacked as at best eccentric and at worse Russian agents. Others like Wikileaks and myself are pariahs excluded from any mainstream exposure. The official UK, US, French and Spanish government line, and the line of the billionaire and state owned media, continues to be that Douma was a Syrian government chemical weapons attack on civilians. They intend, aided and abetted by their vast online propaganda operations, to brazen out the lie.

What we are seeing is the terrifying rise of the zombie state narrative in Western culture. It does not matter how definitively we can prove that something is a lie, the full spectrum dominance of the Establishment in media resources is such that the lie is impossible to kill off, and the state manages to implant that lie as the truth in the minds of a sufficient majority of the populace to ride roughshod over objective truth with great success. It follows in the state narrative that anybody who challenges the state’s version of truth is themselves dishonest or mad, and the state manages also to implant that notion into a sufficient majority of the populace.

These are truly chilling times.

In the next instalment I shall consider how the Establishment is brazening out similar lies on the Russophobe agenda, and sticking to factually debunked narratives on the DNC and Podesta emails, on the Steele Dossier and on the Skripals.

* * *

Unlike his adversaries including the Integrity Initiative, the 77th Brigade, Bellingcat, the Atlantic Council and hundreds of other warmongering propaganda operations, Craig’s blog has no source of state, corporate or institutional finance whatsoever. It runs entirely on voluntary subscriptions from its readers – many of whom do not necessarily agree with the every article, but welcome the alternative voice, insider information and debate. Subscriptions to keep Craig’s blog going are gratefully received.

There are a multitude of false assumptions out there on what the collapse of a nation or “empire” looks like. Modern day Americans have never experienced this type of event, only peripheral crises and crashes. Thanks to Hollywood, many in the public are under the delusion that a collapse is an overnight affair. They think that such a thing is impossible in their lifetimes, and if it did happen, it would happen as it does in the movies – They would simply wake up one morning and find the world on fire. Historically speaking, this is not how it works. The collapse of an empire is a process, not an event.

This is not to say that there are not moments of shock and awe; there certainly are. As we witnessed during the Great Depression, or in 2008, the system can only be propped up artificially for so long before the bubble pops. In past instances of central bank intervention, the window for manipulation is around ten years between events, give or take a couple of years. For the average person, a decade might seem like a long time. For the banking elites behind the degradation of our society and economy, a decade is a blink of an eye.

In the meantime, danger signals abound as those analysts aware of the situation try to warn the populace of the underlying decay of the system and where it will inevitably lead. Economists like Ludwig Von Mises foresaw the collapse of the German Mark and predicted the Great Depression; almost no one listened until it was too late. Multiple alternative economists predicted the credit crisis and derivatives crash of 2008; and almost no one listened until it was too late. People refused to listen because their normalcy bias took control of their ability to reason and accept the facts in front of them.

There are a number factors that cause mass blindness to economic and social reality. First and foremost, establishment elites deliberately create the illusion of prosperity by rigging economic data to the upside. In almost every case of economic crisis or geopolitical disaster, the public is conditioned to believe they are in the midst of a financial “boom” or era of “peace”. They are encouraged to ignore fundamental warning signs in favor of foolish faith in the system. Those people that try to break the apathy and expose the truth are called “chicken little” and “doom monger”.

In the minds of the cheerful lemmings a “collapse” is something very obvious; they think they would know it when they saw it. It’s like trying to teach a blind person about colors; it’s not impossible, but it’s very difficult to get all these Helen Kellers to understand that what they perceive is not the whole reality. There’s a vast world hidden from them and they have no concept of how to observe it.

Crash events are like stages in the process of collapse; they create moments of clarity for the blind. However, they are also often engineered to benefit the establishment. There’s a reason why the elites put so much energy into hiding the real data on the state of the economy, and it’s not because they are trying to keep the system from faltering by using sheer public ignorance. Rather, a crash event is a tool, a means to an end. As Congressman Charles Lindbergh Sr. warned after the panic of 1920:

“Under the Federal Reserve Act, panics are scientifically created; the present panic is the first scientifically created one, worked out as we figure a mathematical problem…”

Central bankers and their cohorts manipulate economic data and promote the false notion of a boom before almost every major crash because they WANT to ambush the populace. They WANT to create panic, and then use it to their advantage as they rebuild and mutate the system into something unrecognizable only decades ago. Each consecutive crash contributes to the collapse of the whole, until eventually the society we once had is barely a distant memory.

This process can take decades, and the US has been subject to it for quite some time now. Once again in 2019 we are seeing the lie of an “economic boom” being perpetuated in the mainstream. The public was growing too aware of the danger and had to be subdued. More specifically, conservatives were growing too aware. The sad thing is that the boom propaganda is most prominent today among conservatives, who are desperately trying to ignore the fundamentals in an attempt to defend the Trump Administration.

The same people who were pointing out the economic bubble under Obama are now denying its existence under Trump. Trump himself argued that the markets were a dangerous economic fraud created by the Federal Reserve during his campaign, yet once he was in office he flip-flopped and started taking full credit for the bubble. What is mind boggling to me is that many people, even in the liberty movement, still choose to dismiss this behavior in favor of worshiping Trump as some kind of hero on a white horse.

This only reinforces my theory that the system is due for another major engineered crash event, and that the ongoing collapse of the US is soon to accelerate. Each case of economic calamity in modern history was preceded by peak delusional optimism and peak greed. When the people traditionally most vigilant against crisis suddenly capitulate and claim victory, this is when reality strikes hardest. This is when the establishment triggers yet another controlled demolition.

In order to determine how long an empire will last, one has to take into account the agenda of the elites that control its institutions. As long as they are in key positions of power within the system and as long as they can inject their own puppet politicians, they will have the ability to influence the collapse timeline of that system.

Can they prolong and stave off crisis? Yes, for a short while. However, once the machine of a crash has been set in motion the best they can do is slow down the Titanic; they cannot change its path towards the iceberg. And frankly, at this point why would they? I hear it argued often that the elites are going to “keep the plates spinning” on the economy and that they don’t want to lose their “golden goose” in the US economy. This reveals an naivety among skeptics of the true agenda.

Firstly, the elites have a highly useful political puppet in the form of Donald Trump; he is useful in that he inspires sharp national division, and, he is a self proclaimed conservative champion and nationalist. If the elites did not trigger a crash under Trump, then this would give the public the impression that conservative ideals and national sovereignty works. This is the opposite of what they want. Why would globalists that want the erasure of nation states and the creation of a centralized socialist “Utopia” seek to make conservatives and nationalists look good? Well, they wouldn’t.

The only concern of the banks is that they do not take the blame as their engineered collapse of the old world order hits the public with increasingly painful consequences. These consequences are already becoming visible.

The next major crash has begun in the form of plunging fundamentals, and far too many conservatives are placing their heads in the sand for the selfish sake of proving the political left wrong. Declines in US manufacturing, US freight, global exports and imports, mass closures in US retail, as well as all time highs in consumer debt, corporate debt and national debt are being shrugged off and rationalized as nothing more than “hiccups” in an otherwise booming economy. The Fed’s repo market purchases, barely keeping up with demand from liquidity starved corporations are also not being taken seriously.

Conservatives and analysts are going to have to forget about supporting Trump, a Rothschild owned proxy, and start acknowledging reality once again. The only question now is, will the elites allow the crash to spread further into mainstreet and strike markets before or after the 2020 election?

As noted above, to predict the timing of a collapse in a nation or empire, one has to examine the agendas of the elites that dominate its institutions. We can gain some sense of timing from the public admissions of globalist organizations like the IMF and the UN. Each has announced the year 2030 as a target date for the finalization of globalization, a cashless society and sustainability goals. This means that the elites have around ten years to create a crisis and then “solve” that crisis with globalism.

Ten years is a narrow window, and if the elites intend for conservatives to take the blame for the next crash, they will have to initiate it soon. They may not have a choice anyway, as the chain of dominoes was already been set in motion by the Fed in 2018 with its liquidity tightening policies.

We can also gauge timing of a collapse to a point by understanding the common tactics the establishment uses to hide what they are doing. Generally, when a collapse is about to accelerate the elites use crisis events as cover to distract the public and produce scapegoats. In my article ‘Globalists Only Need One More Major Event To Finish Sabotaging The Economy’, I outlined three potential distractions that could be used in the near term, and if any of these events took place, then people should watch for the collapse to move faster. Two of these events now appear imminent: The first being a war with Iran, and the second being a ‘No Deal’ Brexit.

Finally, we can take into account the globalist need for a scapegoat, and it appears that conservatives and nationalists are their target for blame. This leaves less than one year for a crisis event if Trump is intended to leave the White House in 2020, or less than four years if he is intended to stay in for a second term. Keep in mind that A LOT can happen in a single year, and a second Trump term is certainly not guaranteed yet.

But why create a collapse in the first place? Crash events allow the establishment to consolidate control over hard assets as poverty forces the population to sell what they have to survive. This poverty also creates fear, which makes the public malleable and easier to control. Each new crisis opens doors to political and social changes, changes which end in less freedom and more centralization. Collapse is a succession of crashes leading to a complete erasure of the original society. It’s not a Mad Max event, it’s a hidden and insidious cancer that takes over the national body and warps it into a wretched form. The collapse is complete when the nation either breaks apart, or is so damaged for so long that no one can remember what it used to look like.

What we are witnessing today is the beginning of a new crash, and the final phases of a collapse of our way of life. The economic boom narrative among conservatives is a farce designed to trick us into complacency. The bubble that we warned about under the Obama Administration has been popped under the Trump Administration. Nothing has changed in the ten years since the 2008 crash except that the motivation for keeping the crash hidden is quickly disappearing.

Crashes are inevitable, but collapse is only possible when the public remains unprepared. Our civilization and its values are under attack, but they can only be destroyed if we stay apathetic to the threat and refuse to prepare for their defense. We must adopt a philosophy of decentralization. We need localized and self sufficient economies, as well as a return to localized production. Beyond that, we have to prepare for the eventuality of a fight. The fate of the US economy has already been sealed, but the people who are destroying it can still be stopped before they use the collapse to force society into subservience. We have to offer security, we have to offer alternatives to the “new world order” and we have to remove the globalist threat permanently.

Make no mistake, we are living in the midst of an epoch moment; the outcome of collapse depends on us and our reactions. This is not the task of the next generation, it is a task for our generation. We do not have another couple of decades to take the danger seriously. The plates are not spinning, they have already dropped.

* * *

If you would like to support the work that Alt-Market does while also receiving content on advanced tactics for defeating the globalist agenda, subscribe to our exclusive newsletter The Wild Bunch Dispatch. Learn more about it HERE.

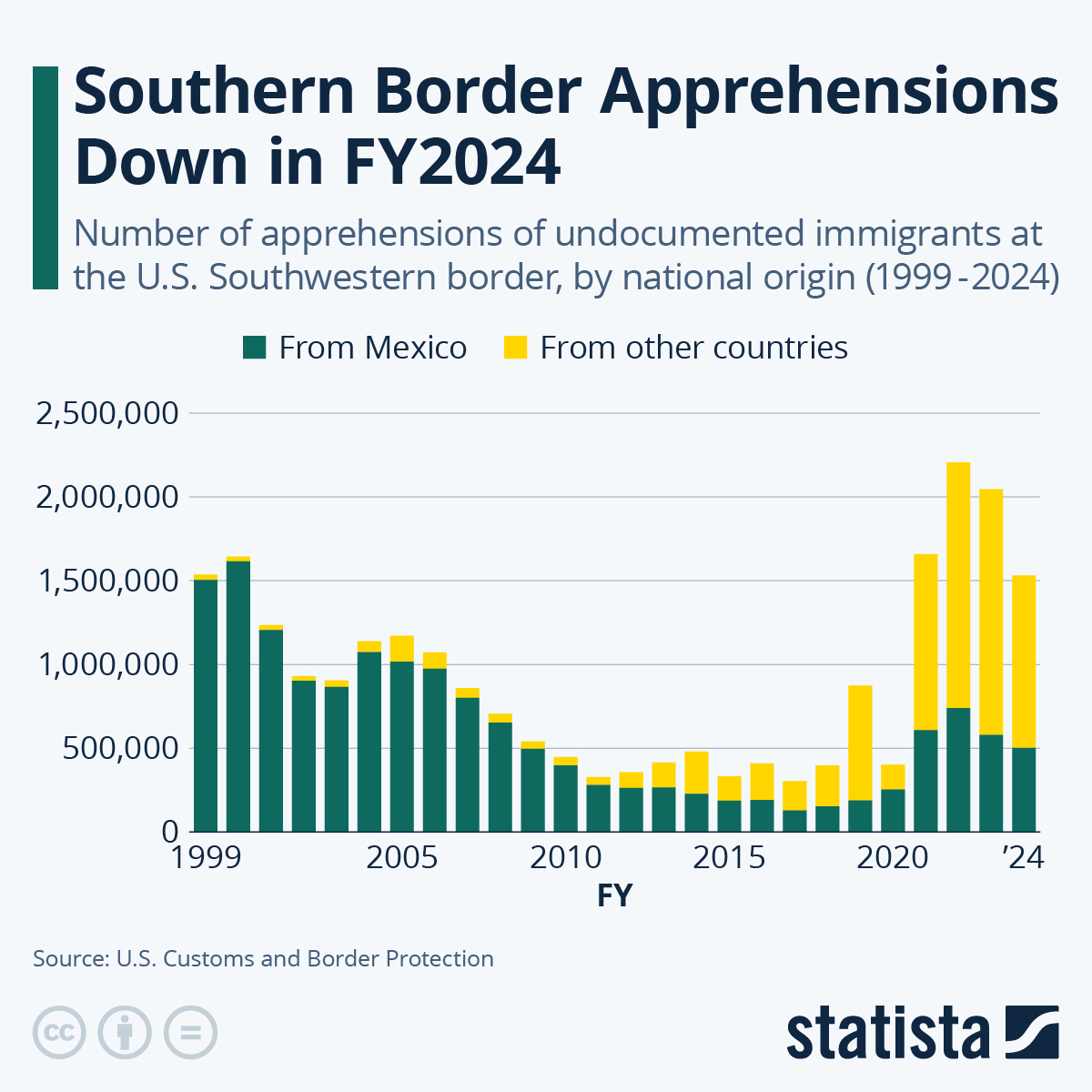

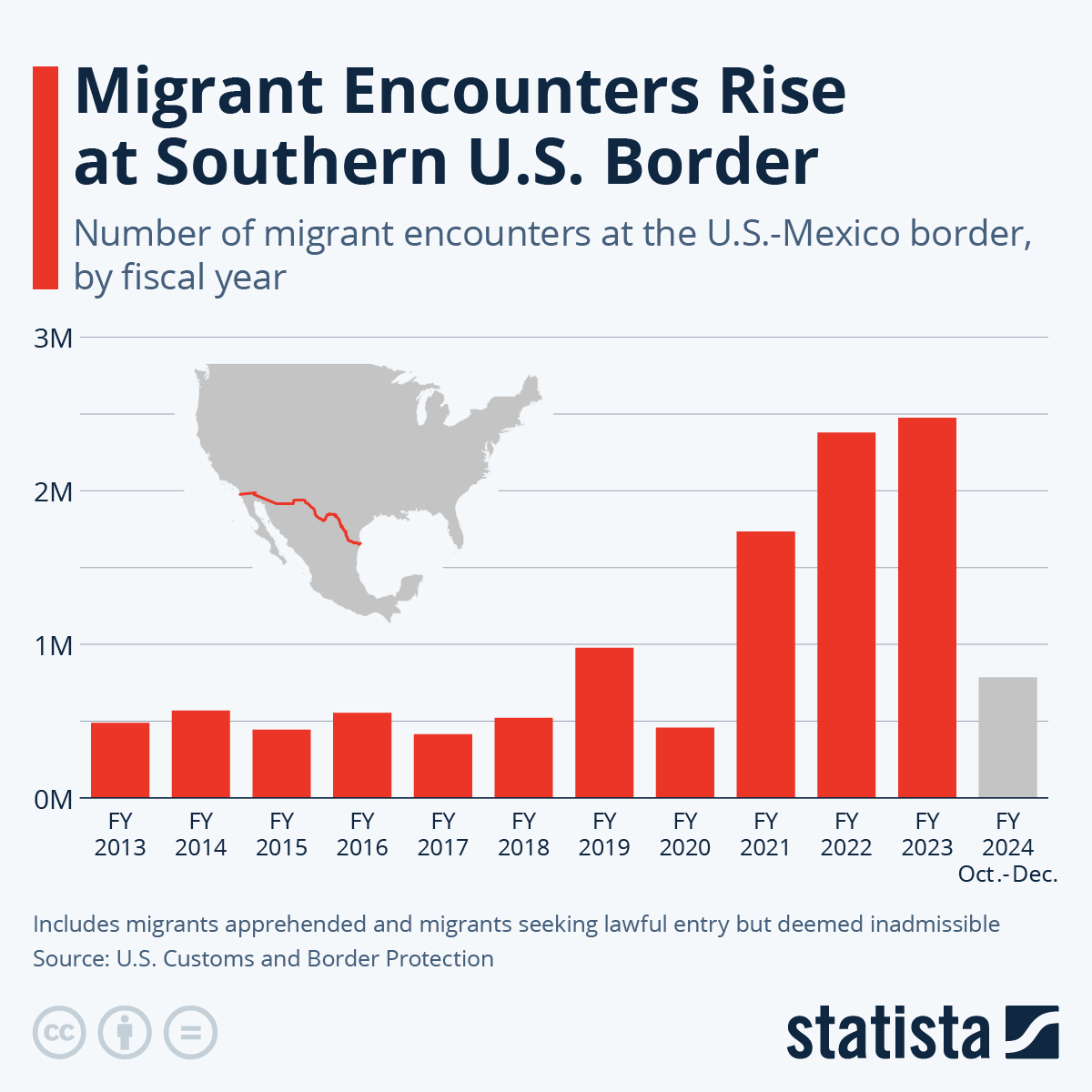

2019 was a year that changed the face of migration on the U.S. Southwestern border. Not only did many more immigrants try to cross it, but a majority – almost 56 percent – arrived together with their families, fleeing violence in Central America. As a result of this fundamental change in who is seeking to immigrate to the United States, Non-Mexicans outnumbered Mexicans 4:1 at the Southern border in the fiscal year of 2019. These numbers are inferred from arrest records of Customs and Border Protection.

The number of undocumented immigrants reached its peak in May 2019, when more than 132,000 people were apprehended. In November 2019 (FY2020) was back down to approximately 33,500.

Because many of the new arrivals are applying for asylum, the Trump administration has overhauled its application process, making many asylum seekers wait in camps on the Mexican side without much assistance. These changes were implemented after another system overhaul – the separation of families in U.S. custody and the tendency to release fewer immigration detainees on bail – had caused chaotic scenes at detention centers and an international outcry.

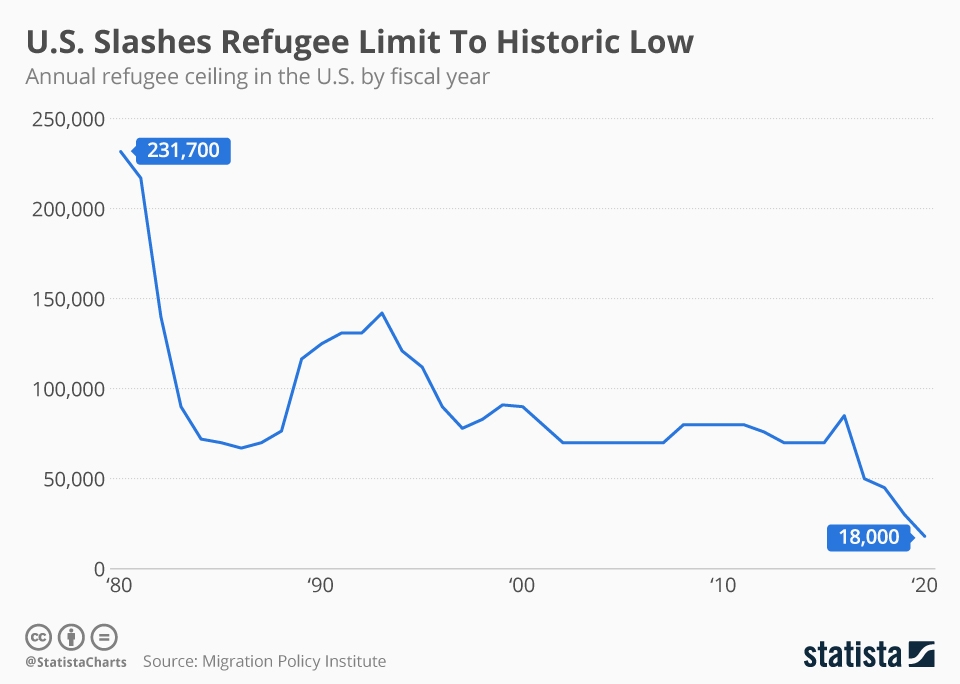

Historically, Mexicans made up the largest share of undocumented immigrants to the U.S. but have been more successful at finding work in Mexico, where the economy is improving and workers are more sought after as the country’s population ages. As more asylum seekers and less work migrants arrive, the U.S. has also slashed the number of refugees it accepts annually to the historic low of 18,000 for 2020.

A remarkably non-propagandistic news-report, in the New York Times, by Eric Lipton, Maggie Haberman and Mark Mazzetti, included powerful evidence that the impeachment-effort against US President Donald Trump is motivated, in part if not totally, by a desire by US Senators and Representatives – as well as by career employees of the US Departments of Defense, State Department, and other agencies regarding national defense – to increase the sales-volumes of US-made weapons to foreign countries.

Whereas almost all of the contents of that article merely repeat what has already been reported, this article in the Times states repeatedly that boosting corporations such as Lockheed Martin, General Dynamics, Boeing, and Northrop-Grumman, has been a major — if not the very top — motivation driving US international relations, and that at least regarding Ukraine, Trump has not been supporting, but has instead been trying to block, those weapons-sales — and creating massive enemies in the US Government as a direct consequence.

In an Oval Office meeting on May 23, with Mr. Sondland, Mr. Mulvaney and Mr. Blair in attendance, Mr. Trump batted away assurances that [Ukraine’s current President] Mr. Zelensky was committed to confronting corruption. “They are all corrupt, they are all terrible people,” Mr. Trump said, according to testimony in the impeachment inquiry.

In other words, Trump, allegedly, said that he didn’t want “terrible people” to be buying, and to receive, US-made weapons (especially not as US aid — free of charge, a gift from America’s taxpayers).

The article simply assumes that Trump was wrong that “they are all terrible people.”

Indeed, Trump himself has sold hundreds of billions of dollars worth of US-made weapons to the Royal Saud family who own Saudi Arabia, and he refuses to back down about those sales on account of that family’s having been behind the widely-reported torture-murder of Washington Post journalist Jamal Khashoggi, and on account of their effort since 2015 to starve into submission — by bombing the food-supplies to — the Houthis in adjoining Yemen, and on account of their using US weapons in order to achieve that mass-murdering goal. Consequently, even if Trump is correct about Ukraine’s Government, he would still have a lot of explaining to do, in order to cancel congressionally authorized US weapons-sales to Ukraine but not to Saudi Arabia.

For the New York Times, in its ’news’-report — even this article that’s less prejudiced than most of mainstream US ’news’-reporting is — to simply presume that Trump had no valid reason for asserting what he did against Ukraine’s present (the Obama-installed) Government of Ukraine, constitutes merely anti-Trump (and pro-Obama) propaganda, on their part, and it would be more appropriate in an editorial or op-ed from them than in an alleged news-article, such as here. However, the actual news-value in that article is real. They quoted from “a piece in the conservative Washington Examiner saying that the Pentagon would pay for weapons and other military equipment for Ukraine, bringing American security aid to the country to $1.5 billion since 2014.” This was an anti-Democrat, pro-Republican, newspaper and article, saying:

Kurt Volker, the US special representative for Ukraine, told the Senate Foreign Relations Committee at a Tuesday hearing. “I think it’s also important that Ukraine reciprocate with foreign military purchases from us as well, and I know that they intend to do so.” The assistance comes at a pivotal moment for Ukraine’s newly minted president, Volodymyr Zelensky, a popular comedian who won a landslide victory in April. Zelensky has made ending the Russian-backed insurrection in Ukraine’s eastern Donbas region his top political priority.

The Times, in order to appear nonpartisan, was there citing, as authority, the anti-Trump appointee by Trump, Kurt Volker, who said “it’s also important that Ukraine reciprocate with foreign military purchases from us as well, and I know that they intend to do so.” In other words: Volker was saying that Ukraine’s Government would follow through with America’s war against Russia, next door to Ukraine, and that therefore, US taxpayers should pay for Ukraine’s purchases of US-made weapons, such as from Lockheed Martin and Raytheon. He was saying that milking US taxpayers to boost those US corporations’ profits is good, not bad. He was saying that Ukraine is on US taxpayers’ dole, as if the Obama-installed, rabidly anti-Russian, Ukrainian Government is a charity-case which is the US Government’s business (and not merely those private stockholders’ business), and that therefore, Trump should continue Obama’s policy toward Ukraine, of using Ukraine in order ultimately to place on Ukraine’s border with Russia, missiles against Moscow, right across that border. This is what the New York Times is presenting in a favorable light.

Then, the New York Times ‘news’-report said:

For a full month, the fact that Mr. Trump wanted to halt the aid remained confined primarily to a small group of officials.

That ended on July 18, when a group of top administration officials meeting on Ukraine policy — including some calling in from Kyiv — learned from a midlevel budget office official that the president had ordered the aid frozen.

“I and the others on the call sat in astonishment,” William B. Taylor Jr., the top United States diplomat in Ukraine, testified to House investigators. “In an instant, I realized that one of the key pillars of our strong support for Ukraine was threatened.”

In other words: the Times’s further attack against Trump’s intention not to provide this US taxpayer boondoggle to Lockheed Martin, Raytheon, United Technologies, and other US weapons-making corporations — a boondoggle so as to continue free supply to the Obama-installed Ukrainian regime of US-made weapons against Russia — is that career US national-security personnel support and want to continue Obama’s war against Russia.

Then, the Times reported further:

“This is in America’s interest,” Mr. Bolton argued, according to one official briefed on the gathering.

“This defense relationship, we have gotten some really good benefits from it,” Mr. Esper added, noting that most of the money was being spent on military equipment made in the United States.

America’s war against Russia is designed to enrich investors in US ‘Defense’-contractors.

Isn’t it clear, then, what was actually behind 9/11, and behind America’s invasion of (instead of merely Special-Forces operation regarding) Afghanistan in 2001, and invasions of Iraq in 2003, and of Libya in 2011, and of Syria in 2012-now, etc., and coup against Ukraine in 2014?

The Times article closes with this impeach-Trump line:

But then, just as suddenly as the hold was imposed, it was lifted. Mr. Trump, apparently unwilling to wage a public battle, told Mr. Portman he would let the money go.

White House aides rushed to notify their counterparts at the Pentagon and elsewhere. The freeze had been lifted. The money could be spent. Get it out the door, they were told.

The debate would now begin as to why the hold was lifted, with Democrats confident they knew the answer.

“I have no doubt about why the president allowed the assistance to go forward,” said Representative Eliot L. Engel, Democrat of New York and the chairman of the House Foreign Affairs Committee. “He got caught.”

In other words: Trump yielded to the threat of being impeached. Trump, the sales-person who had sold the Saud family hundreds of billions of dollars worth of US weaponry, recognized that unless Russia is going to be the main target of US weaponry, Trump’s own Presidency will be in jeopardy.

US foreign policies are a vast sales-promotion scheme, for America’s billionaires, who crave to control Russia, above all. Trump won’t buck them. Instead, he’s continuing Obama’s policy on Ukraine.

This Is The Top Job For Americans Hoping To Make Six Figures With No Experience

Given the insane cost of college in the US, who can blame prospective students for trying to game out which career paths have the highest short-term payouts immediately after graduation?

To that end, the two men behind the website theinterviewguys.com (h/t to MarketWatch’s Quentin Fottrell) analyzed some data from the BLS’s Occupational Requirements Survey to glean some insights on which jobs offer the highest salaries to those who are just starting their careers post-graduation.

They found that in 2019, the highest-paying job for college graduates that required no previous work experience was being a pharmacist.

Roughly 64% of pharmacist job postings required no previous work experience in the field, while also carrying a median starting salary of $126,000 a year, more than twice the average wage in the US. Next up was another position in the health-care field: Nurse practitioner. 60% of job postings for nurse practitioners required no prior work experience, while advertising a median salary of $114,000.

Of course, the high median salaries in these fields aren’t an accident, or some kind of happy coincidence. Rather, students face a difficult curriculum during their undergrad years, plus at least some grad school. Pharmacy students must obtain a doctoral degree in pharmacy just to be eligible to enter the workforce, and they must also pass the Pharmacy College Admission Test.

Looking further down the income distribution, the pair found that high school teachers and special education teachers most often required no previous work experience (According to their research, the interview guys found that more than 91% of postings in those fields stipulated that no prior experience in the field was necessary).

However, median salaries for these teaching jobs came in at just over $60,000. Police patrol officers also ranked high on the list of jobs requiring no prior experience in the field (something that the SJWs will surely latch on to as an example of the rank injustices permeating the law-enforcement community). The median salary for patrol officer jobs came in at just over $65,400.

For college graduates, jobs offering high starting salaries with little required experience fall into a category that the study’s authors have dubbed “the sweet spot.” After all, one of the most infuriating struggles that recent grads face is surmounting the ‘experience’ barrier. Every year, hundreds of thousands of American students embark on unpaid or for-credit internships in the hopes of gaining precious work experience.

Some employers, in turn, have been castigated for taking advantage of this situation by relying on unpaid interns or “perma-interns” who receive pay, but no other benefits, for their work.

In many professional-class fields, jobs with low starting wages often lead to higher-paying positions after three or four years in the workforce.

And more often than not, jobs with a low barrier to entry pay much less than other positions. But with unemployment at 50-year lows, some jobs that were traditionally seen as menial or blue-collar labor are seeing upward pressure on wages as jobs like long-haul trucker and fast-food cook become increasingly difficult to fill.

{kind=link}

{kind=link}

{kind=link}