China First Capital Continues Epic Crash In Hong Kong As Chairman Offloads More Shares

Last week we reported how China First Capital Group, an investment holding company, saw its equity trading on the Hong Kong exchange crash in minutes.

The epic implosion continued into the new week, shares are down -23% on Monday as a new report from Bloomberg specifies the chairman of the company unloaded half his stake.

Exchange filing published Saturday show Wealth Max Holdings Ltd. dumped 326.57 million shares of China First Capital on Nov. 28, one day after the stock plummeted 78%.

Wealth Max is controlled by chairman Wilson Sea, who held a 16.1% stake in China First Capital as of last December.

We noted that the abrupt stock slump, wiping out billions of dollars in shareholder value, has once again put the spotlight on corporate governance of Hong Kong stocks.

The forced selling by the chairman was likely due to a margin call on a loan that had collateral as stock. This dangerous business practice can act as a domino effect when companies are connected by investors or business lines.

The next significant risk for investors in Hong Kong and or Chinese stocks are sliding prices because of a decelerating regional economy. As a result, this would lead to additional margin calls and force a vicious circle of panic selling.

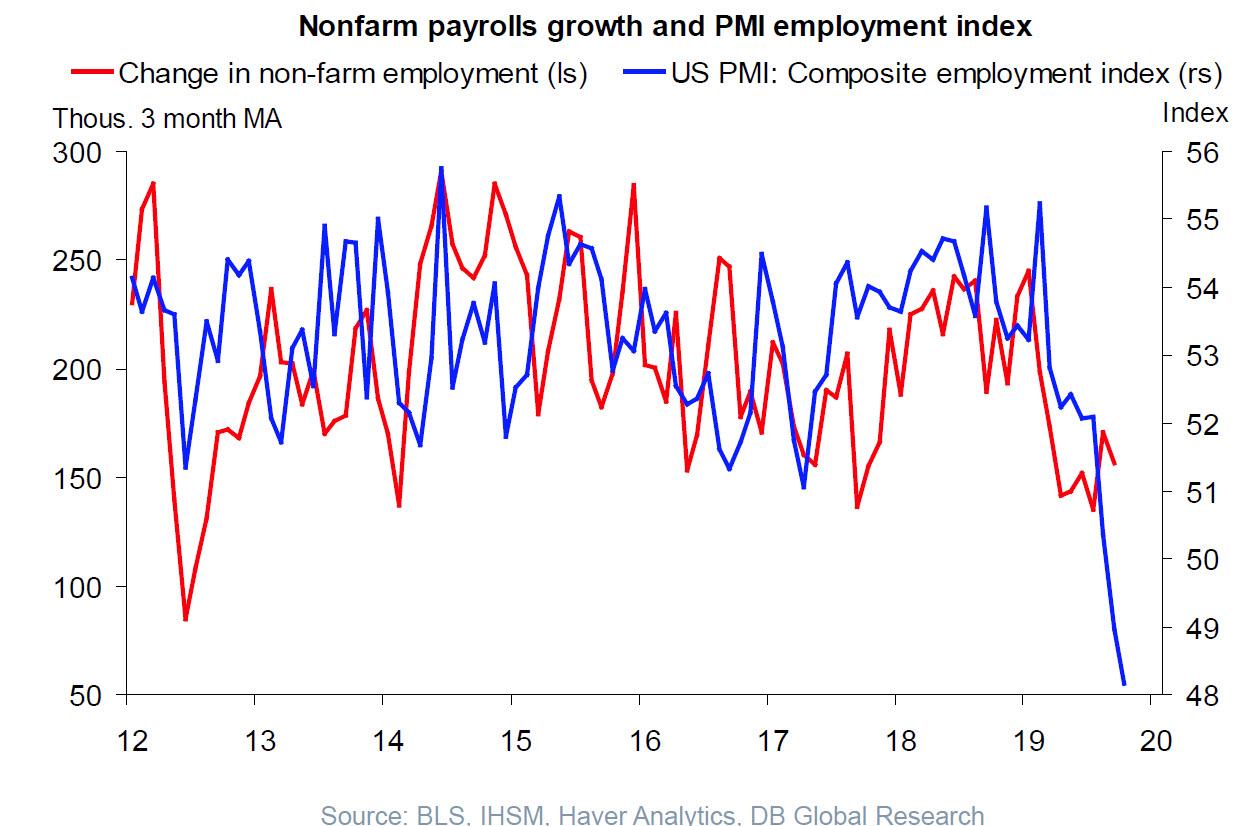

Every month, and quarter, economists, analysts, the media, and investors pour over a variety of mainstream economic indicators from GDP, to employment, to inflation to determine what the markets are likely to do next.

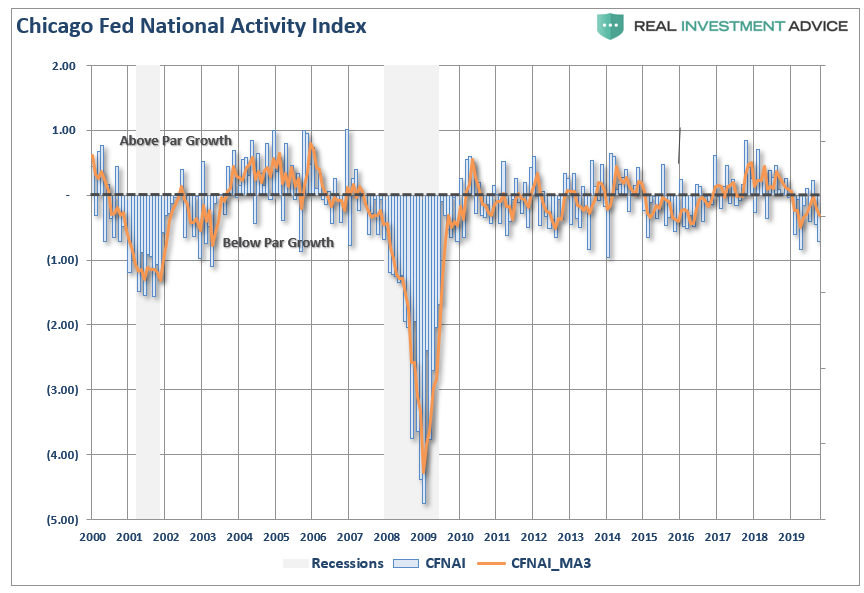

While economic numbers like GDP, or the monthly non-farm payroll report, typically garner the headlines, the most useful statistic, in my opinion, is the Chicago Fed National Activity Index (CFNAI). It often goes ignored by investors and the press, but the CFNAI is a composite index made up of 85 sub-components which gives a broad overview of overall economic activity in the U.S.

The markets have run up sharply over the last couple of months due to the Federal Reserve once again intervening into the markets. However, the hopes are that US economic growth is going to accelerate going into 2020 which should translate into a resurgence of corporate earnings. However, if recent CFNAI readings are any indication, investors may want to alter their growth assumptions heading into next year.

While most economic data points are backward-looking statistics, like GDP, the CFNAI is a forward-looking metric that gives some indication of how the economy is likely to look in the coming months.

Importantly, understanding the message that the index is designed to deliver is critical. From the Chicago Fed website:

“The Chicago Fed National Activity Index (CFNAI) is a monthly index designed to gauge overall economic activity and related inflationary pressure. A zero value for the index indicates that the national economy is expanding at its historical trend rate of growth; negative values indicate below-average growth; and positive values indicate above-average growth.“

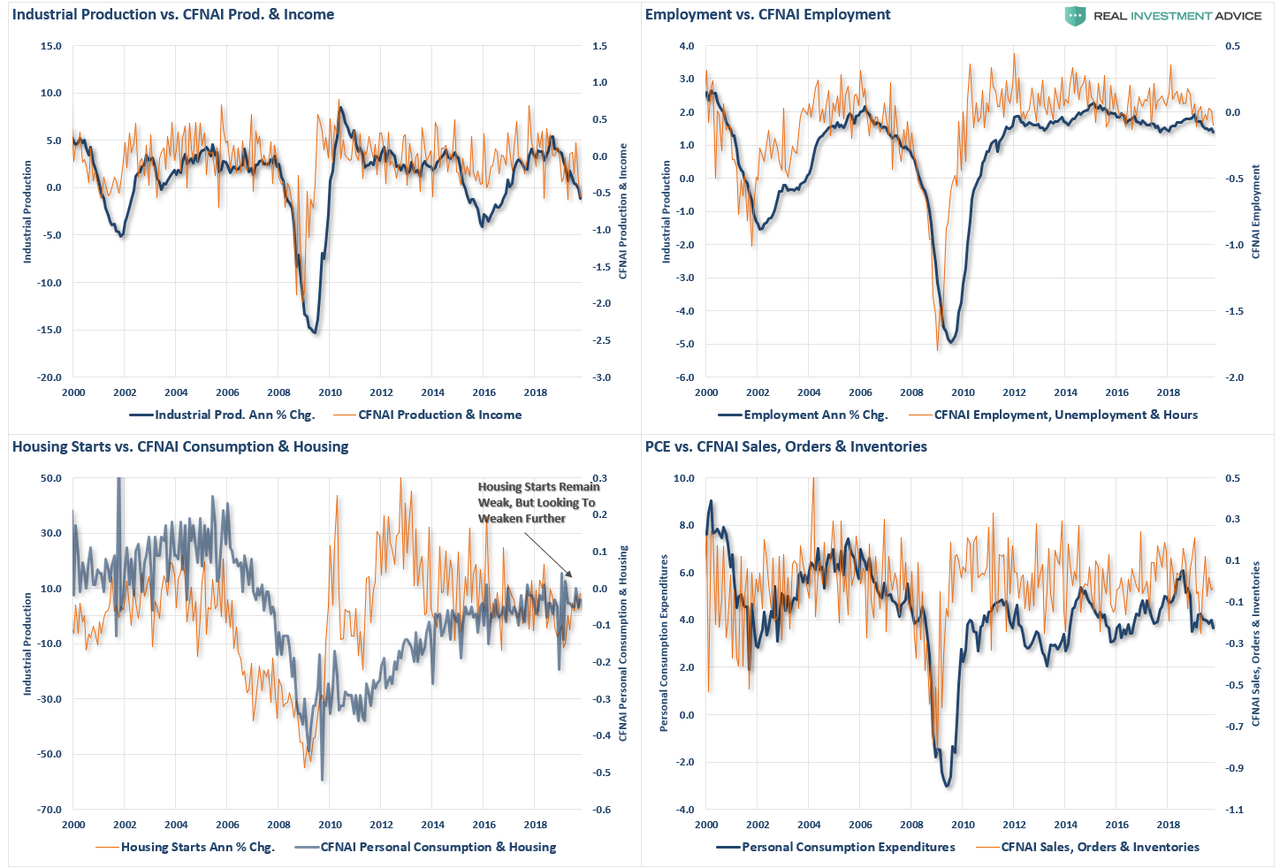

The overall index is broken down into four major sub-categories which cover:

Production & Income

Employment, Unemployment & Hours

Personal Consumption & Housing

Sales, Orders & Inventories

To get a better grasp of these four major sub-components, and their predictive capability, I have constructed a 4-panel chart showing each of the four CFNAI sub-components compared to the four most common economic reports of Industrial Production, Employment, Housing Starts and Personal Consumption Expenditures. To provide a more comparative base to the construction of the CFNAI, I have used an annual percentage change for these four components.

The correlation between the CFNAI sub-components and the underlying major economic reports do show some very high correlations. This is why, even though this indicator gets very little attention, it is very representative of the broader economy. Currently, the CFNAI is not confirming the mainstream view of an “economic soft patch” that will give way to a stronger recovery by next year.

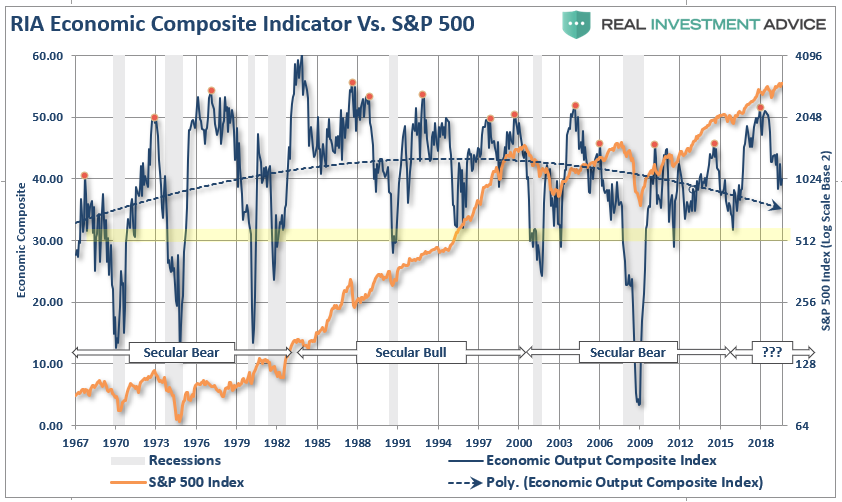

The CFNAI is also a component of our RIA Economic Output Composite Index (EOCI) which is even a broader composition of data points including Federal Reserve regional activity indices, the Chicago PMI, ISM, National Federation of Independent Business Surveys, and the Leading Economic Index. Currently, the EOCI further confirms that “hopes” of an immediate rebound in economic activity is unlikely. To wit:

“The problem is there is not a ‘major shift’ coming for the economy, at least not yet, as shown by the readings from our Economic Output Composite Index (EOCI).”

“There are a couple of important points to note in this very long-term chart.

Economic contractions tend to reverse fairly frequently from high peaks and those contractions tend to revert towards the 30-reading on the chart. Recessions are always present with sustained readings below the 30-level.

The financial markets generally correct in price as weaker economic data weighs on market outlooks.

Currently, the EOCI index suggests there is more contraction to come in the coming months, which will likely weigh on asset prices as earnings estimates and outlooks are ratcheted down heading into 2020.”

It’s In The Diffusion

The Chicago Fed also provides a breakdown of the change in the underlying 85-components in a “diffusion” index. As opposed to just the index itself, the “diffusion” of the components give us a better understanding of the broader changes inside the index itself.

There two important points of consideration:

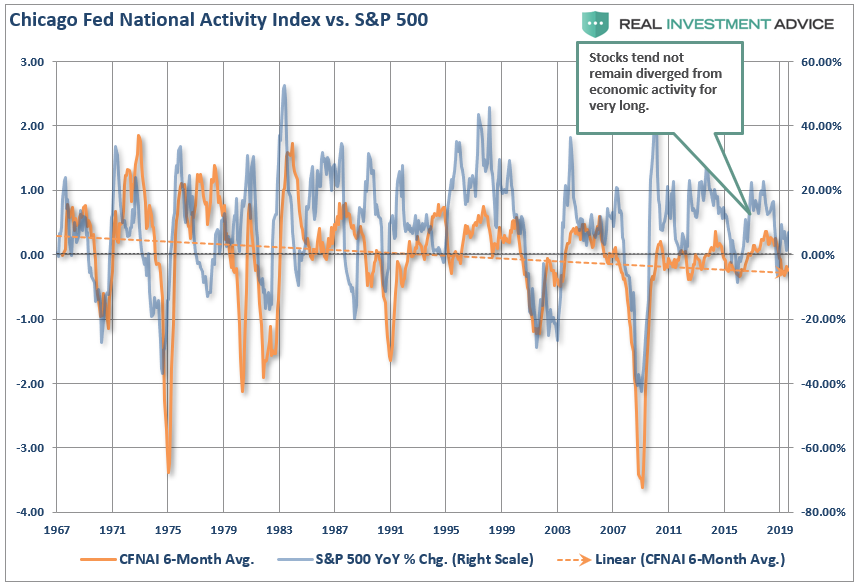

When the diffusion index dips below zero have coincided with weak economic growth and outright recessions.

The S&P 500 has a history of corrections, and outright bear markets, which correspond with negative reading in the diffusion index.

The second point should not be surprising since the stock market is ultimately a reflection of economic growth. The chart below simply compares the annual rate of change in the S&P 500 and the CFNAI index. Again, the correlation should not be surprising.

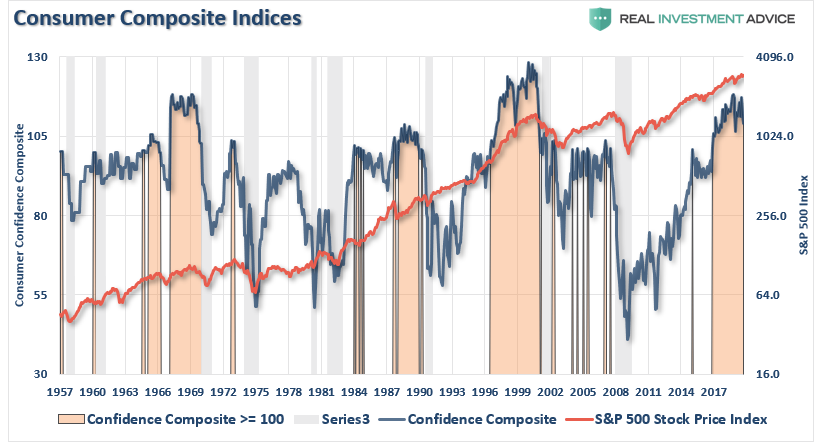

Investors should also be concerned about the high level of consumer confidence readings. There have been numerous headlines touting the “strength of consumer” as support for the ongoing “bull market.”

“The chart below shows our composite confidence index, which combines both the University of Michigan and Conference Board measures. The chart compares the composite index to the S&P 500 index with the shaded areas representing when the composite index was above a reading of 100.

On the surface, this is bullish for investors. High levels of consumer confidence (above 100) have correlated with positive returns from the S&P 500.”

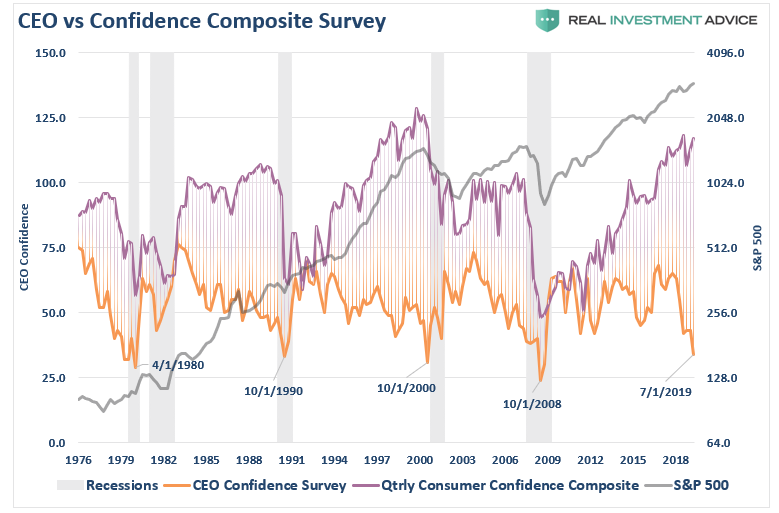

The issue is the divergence between “consumer” confidence and that of “CEO’s.”

“Is it the consumer cranking out work hours, raising a family, and trying to make ends meet? Or the CEO of a company who is watching sales, prices, managing inventory, dealing with collections, paying bills, and managing changes to the economic landscape on a daily basis?”

Notice that CEO confidence leads consumer confidence by a wide margin. This lures bullish investors, and the media, into believing that CEO’s really don’t know what they are doing. Unfortunately, consumer confidence tends to crash as it catches up with what CEO’s were already telling them.

What were CEO’s telling consumers that crushed their confidence?

“I’m sorry, we think you are really great, but I have to let you go.”

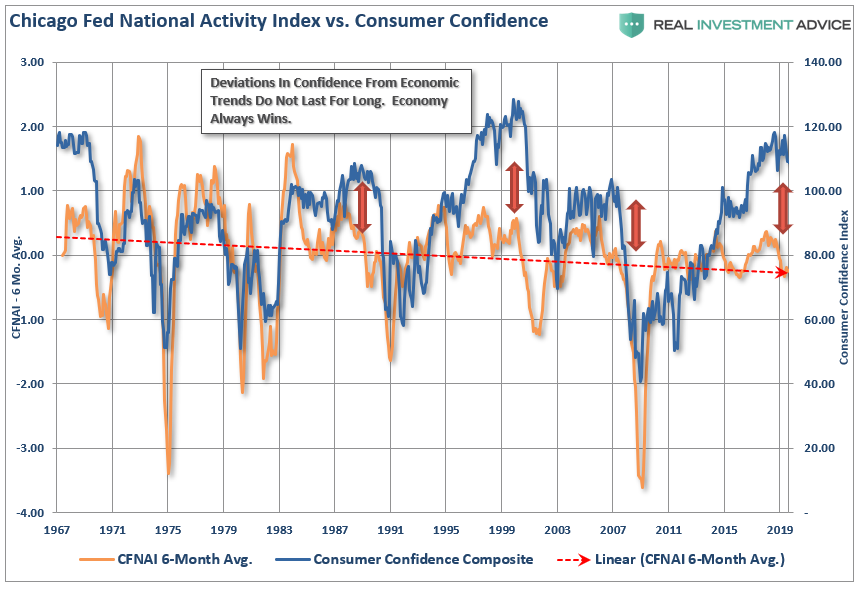

The CFNAI also tells the same story with large divergences in consumer confidence eventually “catching down” to the underlying index.

This chart suggests that we will begin seeing weaker employment number and rising layoffs in the months ahead if history is any guide to the future.

This last statement is key to our ongoing premise of weaker than anticipated economic growth despite the Federal Reserve’s ongoing liquidity operations. The current trend of the various economic data points on a broad scale are not showing indications of stronger economic growth but rather a continuation of a sub-par “muddle through” scenario of the last decade.

While this is not the end of the world, economically speaking, such weak levels of economic growth do not support stronger employment, higher wages, or justify the markets rapidly rising valuations. The weaker level of economic growth will continue to weigh on corporate earnings which, like the economic data, appear to have reached their peak for this current cycle.

The CFNAI, if it is indeed predicting weaker economic growth over the next couple of quarters, also doesn’t support the recent rotation out of defensive positions into cyclical stocks that are more closely tied to the economic cycle. The current rotation is based on the premise that economic recovery is here, however, the data hasn’t confirmed it as of yet.

Either the economic data is about to take a sharp turn higher, orthe market is set up for a rather large disappointment when the expected earnings growth in the coming quarters doesn’t appear. From all of the research we have done lately, the latter point seems most likely as a driver for the former seems lacking.

Maybe the real question is why we aren’t paying closer attention to what this indicator has to tell us?

Futures Fade China PMI Euphoria After Trump Restarts Trade War With Brazil, Argentina

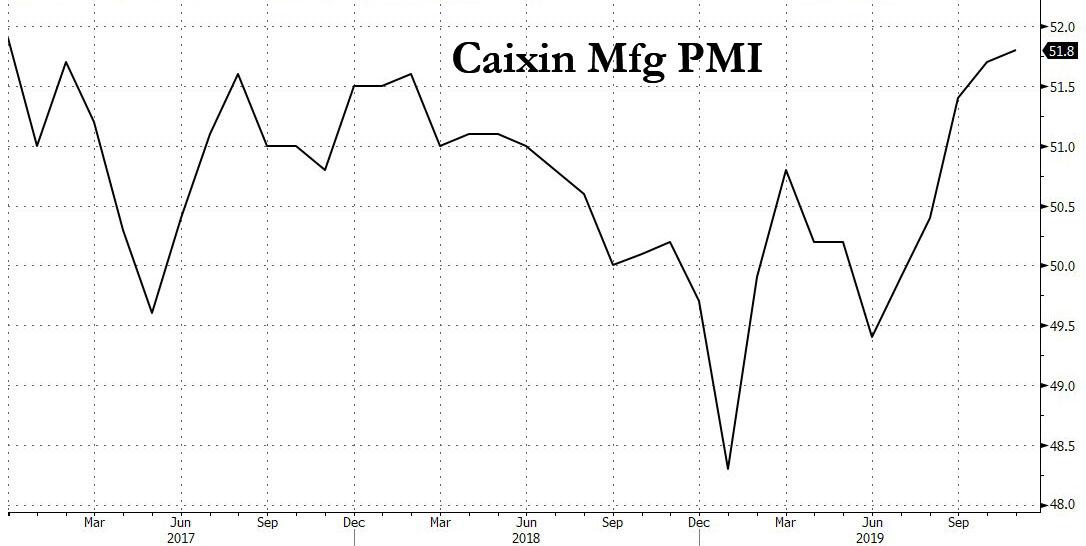

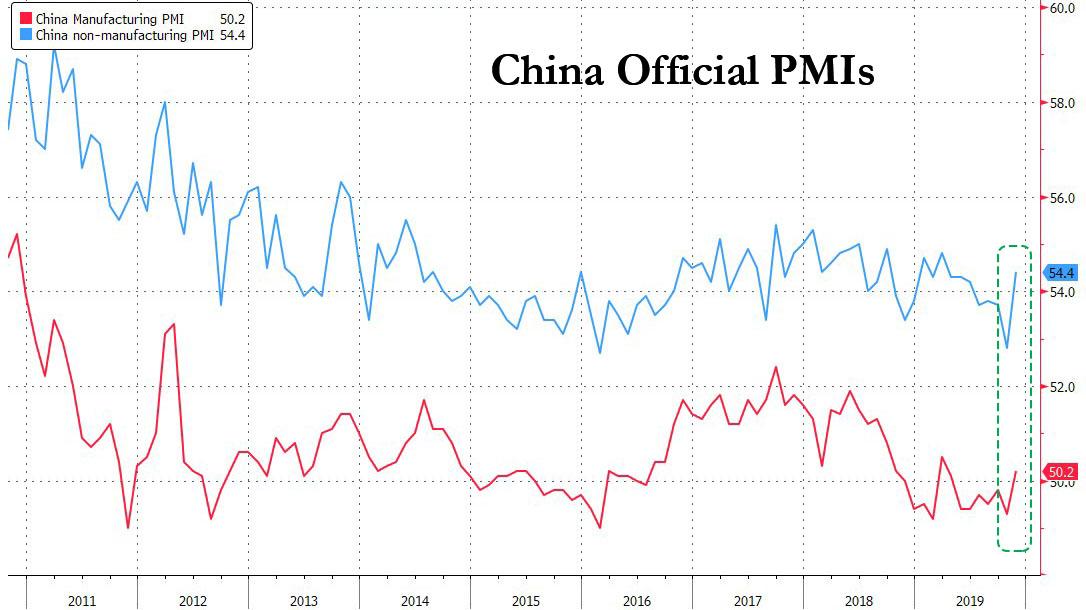

Markets started off the week in full-blown euphoria mode, despite another lukewarm Black Friday (as Amazon continues to cannibalizes the entire bricks and mortar retail industry) disappointing Korean exports, Japanese industrial data and a report out of China that only a full rollback on existing tariffs will lead to a “Phase 1” trade deal, with traders instead choosing to focus on this weekend’s NBS and Caixin manufacturing PMI data out of China, of which the former unexpectedly moved into expansion in November, while the latter jumped to a near three-year high, which reinforced market confidence that the worst may be over for China (of course, this is merely a soft survey; China’s actual hard data has been an absolute disaster) and the world economy.

Not even an Axios report late on Sunday that the US-China trade deal had stalled because of Hong Kong legislation and the the phase one deal would probably happen year-end at the earliest, managed to dent optimism.

However after rising as high as 3,158 shortly after the European open, S&P futures pared much of their gain and Europe stocks briefly turned lower after President Trump tweeted on Monday that he will immediately restore tariffs on U.S. steel and aluminum imports from Brazil and Argentina, in the process reminding investors of lingering trade risks and overshadowed solid factory data.

“Brazil and Argentina have been presiding over a massive devaluation of their currencies, which is not good for our farmers. Therefore, effective immediately, I will restore the Tariffs on all Steel & Aluminum that is shipped into the U.S. from those countries,” Trump said in a tweet.

…..Reserve should likewise act so that countries, of which there are many, no longer take advantage of our strong dollar by further devaluing their currencies. This makes it very hard for our manufactures & farmers to fairly export their goods. Lower Rates & Loosen – Fed!

Trump also urged the Federal Reserve to prevent countries from gaining an economic advantage by devaluing their currencies: “The Federal Reserve should likewise act so that countries, of which there are many, no longer take advantage of our strong dollar,” Trump tweeted. “Lower Rates & Loosen – Fed!”, he said, perhaps unaware that the Fed did just that in three of the past five months.

The latest tariff twist threatened to overshadow promising data out of China and Europe along with a record $7.4 billion in U.S. online sales for Black Friday, if somewhat below expectations. Investors will also be looking for new reasons to be bullish in American factory and employment numbers due this week, although as we showed on Sunday, they may end up disappointed.

Despite the modest Trump tweet glitch, US futures remained solidly higher thanks to the Chinese PMI data, which coming from a country best known for fabricating all of its economic data, is certainly beyond reproach and is absolutely accurate.

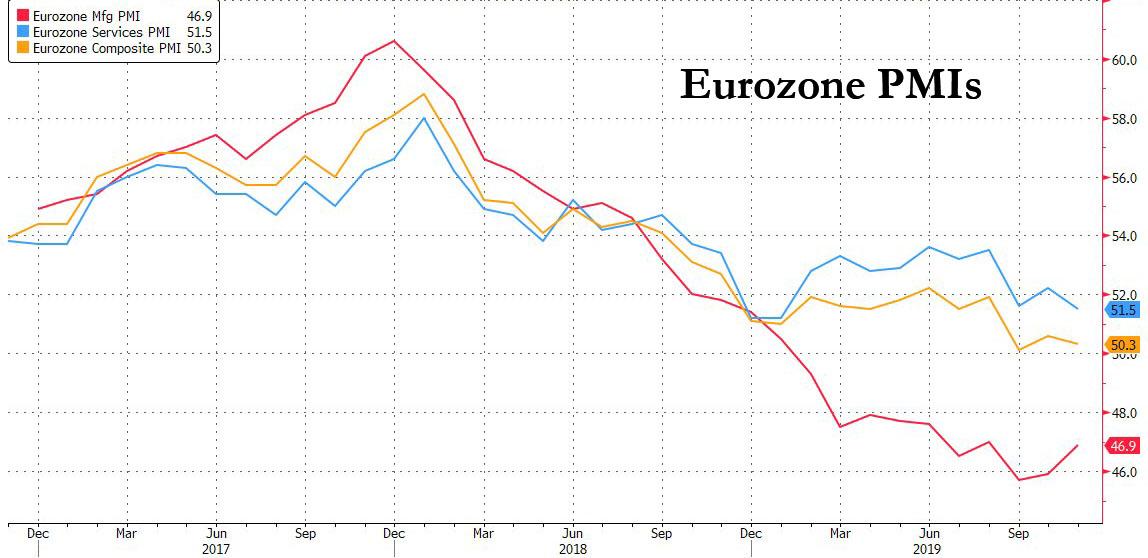

In Europe, the Stoxx Europe 600 Index erased erases an early gain of as much as 0.6% and traded slightly lower as defensive bond proxies utilities, telecoms and real estate led declines. The STOXX 600 Utilities Index extends drop, down 1.4%, the most since Nov. 7. Markets were also keeping track of the latest Eurozone PMI reports which indicated manufacturing activity contracted for a 10th straight month in November although the bloc’s battered factories may have turned a corner as forward-looking indicators in Monday’s survey appear to have passed a nadir.

IHS Markit’s final manufacturing Purchasing Managers’ Index (PMI) has been below the 50 mark separating growth from contraction since February, but at 46.9 it was above October’s 45.9 and higher than a preliminary estimate of 46.6.

The index for output, which feeds into a composite PMI due on Wednesday that is seen as a good gauge of economic health, rose to 47.4 from 46.6. “Although still signaling a steep rate of decline, the manufacturing PMI nonetheless brings some encouraging signals which will fuel speculation that the worst is over for euro area producers,” said Chris Williamson, chief business economist at IHS Markit.

New orders, employment, raw materials purchases and backlogs of work all declined at a shallower rate, while optimism staged its biggest one-month bounce in over six years. The future output index leapt to 55.3 from 51.9.

“Perhaps most promising is a marked upturn in business sentiment, particularly in Germany,” Williamson said. Germany is going through a soft patch but is on track to grow 0.2% this quarter, the Ifo economic institute said last week. Its export-dependent manufacturing sector contracted at a slower pace for the second month in a row in November, the German factory PMI showed earlier. The country’s mfg PMI printed at 44.1, above the 43.8 expected.

In another key weekend development, Germany’s Finance Minister Scholtz lost his bid to become leader of the SPD after suffering defeat at the hands of the left-leaning Norbert Walter-Borjans and Saskia Esken, who have been highly critical of the coalition between their party and the CDU/CSU. The Chief economist at the Centre for European Reform noted that Walter-Borjans and Esken have been critical of the debt brake but accept that it probably cannot be changed, adding that it is unlikely the coalition will collapse but the SPD will likely make the GroKo more painful for the CDU.

Earlier, Japanese stocks led gains in Asia, while Hong Kong shares managed to climb even after clashes between protesters and police resumed over the weekend. Asian stocks advanced, led by health-care firms, after China posted stronger-than-expected manufacturing surveys. Most markets in the region were up, with Japan and the Philippines leading gains. The Topix climbed, driven by electronic companies and automakers, as the yen stabilized near a six-month low against the U.S. dollar. The Shanghai Composite Index edged higher, snapping a three-day losing streak, with Will Semiconductor and Foxconn Industrial Internet driving gains. India’s Sensex fluctuated after retreating from Thursday’s record-high close in the previous session. Reliance Industries climbed while Tata Consultancy Services, slid.

As a reminder, on Saturday China rpeorted that its official, NBS Manufacturing PMI rose to 50.2 vs. Exp. 49.5 (Prev. 49.3), its first expansion in 7 months, while the Chinese Non-Manufacturing PMI also rose to 54.4 vs. Exp. 52.0 (Prev. 52.8), resulting in a Composite PMI (Nov) 53.7 (Prev. 52.0) Chinese Caixin Manufacturing PMI (Nov) 51.8 vs. Exp. 51.4 (Prev. 51.7).

“This improvement in the manufacturing PMI is important because we can say with more certainty, than at the beginning of the year, that China’s macro outlook is indeed stabilizing,” said Aninda Mitra, senior sovereign analyst at BNY Mellon Investment Management.

Meanwhile, better-than-expected manufacturing data from China and the euro area failed to ignite demand for emerging-market assets as risks including a lack of progress in U.S.-Sino trade talks and protests in Hong Kong weighed on investor sentiment. While MSCI’s emerging-market stock index eked out a modest gain on Monday, the currency gauge extended a decline after posting its first down month in three in November. The Philippine peso led declines as the nation braces for Typhoon Kammuri, while Turkey’s lira edged lower amid concern soft economic growth will push the central bank to ease policy further. The zloty strengthened after the manufacturing PMI climbed. “Markets see the glass half full,” Guillaume Tresca, a Paris-based strategist for Credit Agricole, said in a client note. While the Chinese manufacturing data improve the outlook for global growth, “it could get more complicated to get a trade deal” as China’s government insists on a tariff rollback.

In FX, the U.S. dollar rose to a six-month high versus the Japanese yen and New Zealand’s currency jumped to near four-month peaks on Monday on a rebound in global economic optimism. The U.S. dollar rallied to 109.73 yen, the highest since May, and was last up a quarter of a percent against the safe-haven Japanese currency at 109.63 yen. The euro was steady ahead of a testimony by the European Central Bank’s new president, Christine Lagarde, to the European parliament later in the day. A tightening British election race knocked the pound lower. Riskier currencies also rallied after the Chinese data, with New Zealand’s dollar jumping to its highest in almost four months at $0.6475. It was up 0.75% on the day, while the Australian dollar rallied 0.4% at $0.6789.

In rates, global bonds retreated as equities traded in a sea of green and commodity currencies advanced. US 10Y Tsy yields jumped as high as 1.86% before fading half of their gains following the Trump tweet.

In commodities, oil rallied following its more than 5% sell-off on Friday, while gold retreated. Crude oil firmed on dual tailwinds in the form of better than expected PMIs out of China and talk of OPEC+ producers considering a 400k deepening of existing cuts acting as a tailwind for the complex. Front month WTI and Brent futures have managed to recover nearly half of Friday’s steep losses, the former eclipsing USD 56.50/bbl to the upside (vs. lows of USD 55.00/bbl), the latter briefly topping the USD 62.00/bbl mark (vs. USD 60.40/bbl lows). Weekend comments from Iraqi Oil Minister Ghadhba hinted the cartel will mull deepening existing oil output cuts by about 400k bpd to 1.6mln bpd, comments which further corroborated by sources this morning; the touted a cut of at least 400k BPD which could last until at least June.

Following a barrage of PMI reports from around the world, we also get PMIs and construction spending data from the US.

Market Snapshot

S&P 500 futures up 0.2% to 3,148.25

STOXX Europe 600 up 0.5% to 409.44

MXAP up 0.4% to 164.47

MXAPJ up 0.2% to 524.78

Nikkei up 1% to 23,529.50

Topix up 0.9% to 1,714.49

Hang Seng Index up 0.4% to 26,444.72

Shanghai Composite up 0.1% to 2,875.81

Sensex unchanged at 40,794.04

Australia S&P/ASX 200 up 0.2% to 6,862.27

Kospi up 0.2% to 2,091.92

German 10Y yield rose 7.9 bps to -0.281%

Euro down 0.01% to $1.1017

Italian 10Y yield fell 0.3 bps to 0.885%

Spanish 10Y yield rose 6.9 bps to 0.485%

Brent futures up 2.4% to $61.94/bbl

Gold spot down 0.5% to $1,456.67

U.S. Dollar Index little changed at 98.34

Top Overnight News from Bloomberg

The House this week begins the solemn task of deciding whether to bring impeachment articles against President Donald Trump, faced with a sharply divided American public, a compressed timetable and doubts about how and if the White House will participate

Peter Navarro, the self-described “bad cop” of Trump administration economic policy, wants to shake up the World Trade Organization

Chancellor Angela Merkel’s government was thrown into crisis after Germany’s Social Democrats redrew the country’s political map by electing a new leadership seen as a threat to the survival of their coalition; Chancellor Angela Merkel’s party told the new leadership that there will be no renegotiation of the terms of their alliance

The Labour Party gained on the ruling Conservatives in four of five polls with two weeks until the U.K. election, with one of them signaling a possible hung parliament

First it was India and South Korea. Now Japan and New Zealand are joining Asia Pacific’s fiscal stimulus bandwagon, raising concerns for bond investors who will be asked to fund the attempt to re-ignite growth

For years, OPEC ignored the rise of the U.S. shale industry and came to regret its mistake. Now, the group is making another bold gamble on America’s oil revolution: that its golden age is over

Asian equity markets kick-started December on the front-foot with risk appetite stimulated by a flurry of better than expected Chinese data including official Manufacturing PMI which expanded for the first time in 7-months. ASX 200 (+0.2%) and Nikkei 225 (+1.0%) were higher with Australia led by outperformance in the defensive and financial sectors but with upside capped by energy following the recent slump in oil prices after Russian Energy Minister Novak triggered doubts for a deal extension at this week’s OPEC+ meeting, while the advances in Tokyo were mainly fuelled by a weaker currency. Hang Seng (+0.4%) and Shanghai Comp. (+0.1%) welcomed the encouraging PMI data which aside from the headline beat, also showed Non-Manufacturing PMI and Caixin Manufacturing PMI topped estimates, although gains were limited by continued PBoC inaction, the resumption of violence in Hong Kong protests over the weekend and ongoing trade uncertainty with Beijing said to be insistent on a tariff rollback and as other reports suggested Hong Kong legislation may have stalled the US-China agreement but that a phase one deal would still probably occur by year-end at the soonest. Finally, JGBs were lower amid similar pressure in T-notes and with demand for bonds sapped by the mostly upbeat sentiment, while the BoJ’s presence for a respectable JPY 890bln of JGBs did little to help 10yr JGB prices after having slipped through prior support at the 153.00 level.

Top Asian News

PBOC Signals Policy to Stay Cautious Amid Uncertain Data

Slowdown Fuels Fears Turkey to Push Stimulus It Can’t Afford

Better than expected PMI data out of China overnight followed by slight revisions higher to manufacturing PMIs across Europe have somewhat spurred risk appetite; subsequently, major European bourses (Euro Stoxx 50 +0.1%), but has pared back a bulk of its gains in recent trade. Sectors are mostly in the green, led by Energy (+0.7%), in-line with rallying crude prices, while the defensive Utilities (-1.3%) sector is the laggard. In terms of individual mover, Tullow Oil (+4.3%) is the top Stoxx 600 gainer, as reports circulate alleging the Co. has agreed to sell a stake in its Ugandan oil fields. Lufthansa (+1.5%) received a boost on the news that Qatar Airways may be interested in taking a stake in the Co., which could lead to a partnership, although the Co. pushed back on the news stating that the Co. was not privatised in Germany to be nationalised in Qatar. Elsewhere, positive broker moves for Rio Tinto (+0.7%) and EDF (+2.4%) sees the Co.’s shares supported. In terms of the laggards, Hiscox (-3.4%) is set to receive the boot from the FTSE 100 in its quarterly reshuffle on Wednesday, while Fresnillo (-3.7%) and Kingfisher (+1.5%) are also reportedly at risk. easyJet (-0.1%), Just Eat (Unch) and GVC (+1.0%) could be promoted, according to Elsewhere, at the bottom of the FTSE 100 is Ocado (-8.6%), whose shares sunk on the news that the Co. is to issues GBP 500mln worth of bonds which will be convertible into shares as it seeks cash to fund its tech arm’s commitments.

Top European News

Johnson Bolsters Security Message After London Knife Attack

Euro- Area Manufacturing Slump Eases But Job Losses Continue

U.K. Factory Downturn Was Less Severe Than Feared in November

UniCredit Sells Stake in Turkey Unit as Mustier Readies Targets

Merkel’s Party Plays Hardball With Coalition Future in Doubt

In FX, the Kiwi has made a flying start to December on the back of significantly stronger than forecast NZ terms of trade for Q3 that has lifted Nzd/Usd over the 0.6450 mark to test early November resistance (around 0.6466) and nudged the Aud/Nzd cross down through 1.0500 to test Fib support even though the Aussie is also doing well in the G10 arena in wake of encouraging Chinese PMIs, with Aud/Usd climbing above 0.6775 and rebounding towards 0.6800.

EUR/CHF/CAD/GBP/JPY – All softer vs a generally solid Greenback, bar the aforementioned Antipodean Dollar outperformance, as the DXY meanders between 98.272-368 awaiting the full return of US markets/participants from Thanksgiving. Eur/Usd is just maintaining 1.1000+ status with the aid of better than flash or forecast Eurozone PMIs that have offset some of the investor qualms over German politics due to the failed attempt by Finance Minister Scholz to become SPD chief over the weekend. However, more hefty option expiry interest may keep the single currency supressed, as 1.2 bn runs off from 1.0995-1.1000 and a further 1.1 bn between 1.0005-20. Elsewhere, the Franc is pivoting parity after Swiss retail sales and the manufacturing PMI both beat consensus, but slowed from previous levels and the Loonie is hovering just above 1.3300 Canada’s manufacturing survey amidst a firm rebound in oil prices that is also helping the NOK pare some of its recent declines. Indeed, Eur/Nok has eased back from around 10.1600 vs a more elevated Eur/SEK following falls in Norwegian and Swedish manufacturing PMIs (albeit the former still growth vs the latter contracting faster). Meanwhile, Cable continues to labour on the 1.2900 handle, with weekend polls indicating a tighter UK election race and an upward revision to the manufacturing PMI not really providing the Pound with any momentum due to weak sub-components. Similarly, the Yen did not derive much impetus from Japan’s manufacturing headline rebounding closer to 50.0 as Usd/Jpy hovers near the middle of a 109.49-72 range and stays technically bullish after a 3rd close above a key chart level (109.37 Fib).

EM – Depreciation against the Buck almost across the board, with Usd/Cnh hovering around 7.0400 after China’s retaliatory moves in response to the US bill in favour of HK protestors and Usd/Try skirting 5.7600 following scant reaction to a rebound in Turkish GDP or upturn in manufacturing PMI.

In commodities, crude oil prices are firmer during Monday morning trade, with dual tailwinds in the form of better than expected PMIs out of China and talk of OPEC+ producers considering a 400k deepening of existing cuts acting as a tailwind for the complex. Front month WTI and Brent futures have managed to recover nearly half of Friday’s steep losses, the former eclipsing USD 56.50/bbl to the upside (vs. lows of USD 55.00/bbl), the latter briefly topping the USD 62.00/bbl mark (vs. USD 60.40/bbl lows). Weekend comments from Iraqi Oil Minister Ghadhba hinted the cartel will mull deepening existing oil output cuts by about 400k bpd to 1.6mln bpd, comments which further corroborated by sources this morning; the touted a cut of at least 400k BPD which could last until at least June. Moreover, the latest analysis from OPEC sees a significant oil glut and inventory build in H1 2020 in the absence of further cuts, said multiple sources. In terms of the metals; gold is well off last Friday’s highs of around USD 1467/oz, as lack of haven demand on better global PMI data puts the precious metal under pressure. Copper, meanwhile, received a fleeting overnight boost on better Chinese PMIs but has since retreated from highs and is fairly flat on the day as the red metal balances trade implications from China’s action against the Hong Kong bill which passed into law in Washington.

US Event Calendar

9:45am: Markit US Manufacturing PMI, est. 52.2, prior 52.2

10am: ISM Manufacturing, est. 49.2, prior 48.3

ISM Employment, est. 48.3, prior 47.7

ISM Prices Paid, est. 47, prior 45.5

ISM New Orders, prior 49.1

10am: Construction Spending MoM, est. 0.3%, prior 0.5%

DB’s Jim Reid concludes the overnight wrap

As we welcome in December, Craig has already published our monthly performance review (link here ).The penultimate month of the year proved to be another good one for risk assets as tentative signs of progress towards a “Phase One” trade deal and slightly better data helped. As such of the 16 equity markets in our sample, 13 closed with a positive total return in local currency terms. That of course included fresh new highs for the major US equity markets. YTD, all 38 assets in our sample across all asset classes are now up. Impressive stuff. See the link for more.

It always feels that getting past Thanksgiving marks the start of the official Christmas season. The tree went up at home yesterday, Bronte has already eaten 5 tree decorations, the twins have pulled off several more and Maisie has demanded that she opens more than one advent calendar door each day. Meanwhile my wife drops more Xmas present hints than a taxi driver does passengers on New Year’s Eve. It’s going to be a long month.

This first week of December has a number of critical events that will set the agenda for markets running up to Christmas. Data releases include global PMIs (today and Wednesday), the US jobs report (Friday) and the US ISM figures (today and Wednesday). We’ll hear from ECB President Lagarde (today), and get policy decisions from central banks in Canada (Wednesday), Australia (Tuesday) and India (Thursday), while there’ll be another UK election debate between the two main party leaders (Friday) and a NATO leaders summit in London (Tuesday-Wednesday). With only just over a week to the U.K. election all eyes on whether Trump’s visit to London (starting today ahead of NATO) creates political capital for the opposition parties keen to link Mr Trump to Mr Johnson. Finally the German SPD 3-day party conference starting on Friday is now a must watch given the shock leadership results over the weekend that we’ll discuss below.

Today is global manufacturing PMI day before the services and composite PMIs come out on Wednesday. China has given the world a boost by seeing the official manufacturing gauge at 50.2 (49.5 expected), the first 50+ print since April and up from 49.3 in October. Non-manufacturing rose to 54.4 (consensus 53.1) from 52.8 last month. There is some chatter about strong seasonal helping but overall this will be seen as positive news. Meanwhile, China’s November Caixin manufacturing PMI also came in higher than consensus at 51.8 (vs. 51.5 expected). Asian equity markets have subsequently started the week on the front foot with the Nikkei (+0.99%), Hang Seng (+0.34%), Shanghai Comp (+0.30%) and Kospi (+0.13%) all up. Elsewhere, futures on the S&P 500 are up +0.28% while yields on 10y USTs are up +3.8bps. In other news, China’s Global Times tweeted yesterday that the Chinese government wants tariffs to be rolled back as part of the phase one trade deal with the US, citing unidentified people in Beijing. As for other overnight data releases Japan’s final November PMI came in 0.3pts above the preliminary read at 48.9.

As for the rest of the weekend news, the surprise SPD leadership victory for Norbert Walter-Borjans and Saskia Esken who are very much on the left wing of the party will likely have short and longer term implications. Walter-Borjans has already suggested that they don’t need to leave the coalition with Mrs Merkel’s CDU but that “we must improve the policies and perhaps loosen the black zero”. Whatever actually happens from here this news will likely get markets excited about an easier path to more German fiscal policy in the future. It makes the probability of the Groko breaking up higher and increases the chance of fresh elections in H1 next year. With the Greens riding high in the polls (Forsa) this hope of more fiscal will be further boosted by this. However their policies are not market friendly so what happens next in Germany is very complicated. It could well be that nothing actually happens and the Groko stays together. The SPD are low enough in the polls to make them vulnerable in early elections but staying in the coalition isn’t helping their polling. So a catch-22. Makes me happy I live in an easy to predict country in terms of politics (a joke by the way!). Maybe we’ll have a lot more to report this time next week after the 3-day SPD conference starting on Friday. The Euro is trading flattish this morning at 1.1020 after the news. See our FX strategist full round up of this German political earthquake and implications for the Euro here .

In terms of the U.K. election polls, the Tory lead over Labour in the weekend polls were 6, 10, 15, 9, 13 and 9 points with a bigger range than of late. This still averages 10 points but it’s clear that Labour are eroding the lead in enough polls to make this a little more “interesting” than a couple of weeks ago even if the aggregated lead isn’t that much different. A reminder that a lead of less than 6-7 points might start to push us towards hung parliament territory. Sterling is trading a shade weaker overnight at $1.2917 on the back of these polls.

Moving forward and as for the rest of the global PMIs, the flash numbers mean we do have some initial indications of how the global economy performed into November but if momentum is improving this can be picked up between the flash and final numbers. The flash Euro Area services PMI fell to 51.5 while the manufacturing reading rose to 46.6, and the consensus is expecting the final Euro Area PMI readings to remain in line with the flash ones.

In the US, we’ve also got the ISM releases, with the manufacturing report today before the non-manufacturing index comes out on Wednesday. The manufacturing reading has been below 50 since August (49.2 expected, 48.3 last month), although the non-manufacturing index has held up better, at 54.7 last month.

The other big highlight of the week comes with the US jobs report on Friday. In October, the +128k increase in nonfarm payrolls was the slowest pace of job growth since May but was better than expected with upward revisions to earlier months. The consensus is looking for a rebound to +190k in November. Meanwhile the unemployment rate and average hourly earnings yoy growth are expected to remain at 3.6% and +3.0% respectively. Other US data on factory orders, the trade balance and durable goods orders on Thursday will also help set the tone through December.

In Europe, slightly less is happening in terms of data aside from the PMIs, but we will see German factory orders and industrial production figures released for October on Thursday and Friday respectively. With the German economy having avoided a technical recession in Q3 with +0.1% qoq growth, attention will focus on whether the data heading into Q4 has shown further signs of stabilisation. Finally, for the Euro Area as a whole, Thursday sees the October retail sales figures coming out, along with the final reading for Q3 employment and GDP.

Turning to central banks, with the Fed in their blackout period, the main event this week is likely to be ECB President Lagarde’s appearance before the Economic and Monetary Affairs Committee of the European Parliament today. This is the first Monetary Dialogue with the committee since Lagarde became ECB President, and it’ll be worth keeping an eye on whether she talks about the upcoming strategic review of monetary policy.

Other political events to watch out for include the annual UN climate change conference in Madrid from today, which will be taking place over the next two weeks. Then here in London we have a summit of NATO leaders on Tuesday and Wednesday. And finally, ahead of the UK general election on December 12, there’ll be the second head-to-head debate between Prime Minister Johnson and Labour leader Corbyn on Friday.

A quick recap of last week and equity markets ended on a negative foot amid thin post-US holiday liquidity, but were still higher on the week thanks in large part to better US data from earlier in the week. The S&P 500 ended +0.99% on the week (-0.40% Friday), with the NASDAQ outperforming, up +1.71% (-0.46% Friday). The STOXX 600 moved a similar amount, up +0.85% (-0.44% Friday). Bank stocked lagged in both regions, with the S&P 500 banks index up +0.43% (-0.28% Friday) and the STOXX bank index -1.08% (-0.49% Friday). Fixed income markets were calm, with yields on treasuries up +0.5bps (+1.0bps Friday) and on bunds down -0.1bps (+0.1bps Friday). Gilts saw a relatively larger move on Friday, ending the week -0.8bps lower despite a +2.1bps selloff on Friday, as confidence increased that the Conservative party will win the upcoming election even with a slight narrowing in the polls.

Market Spooked After Trump Threatens To Restore Steel And Aluminum Tariffs On South American Countries

Not surprising whatsoever that President Trump is starting the new week on the wrong foot by threatening several South American countries with a return of steel and aluminum tariffs.

Trump alleges that Brazil and Argentina have been conducting “massive devaluation of their currencies,” which are harming US farmers.

Brazil and Argentina have been presiding over a massive devaluation of their currencies. which is not good for our farmers. Therefore, effective immediately, I will restore the Tariffs on all Steel & Aluminum that is shipped into the U.S. from those countries. The Federal….

Trump then scapegoats Powell for this mess and demands “Lower Rates & Lossen – Fed!”

…..Reserve should likewise act so that countries, of which there are many, no longer take advantage of our strong dollar by further devaluing their currencies. This makes it very hard for our manufactures & farmers to fairly export their goods. Lower Rates & Loosen – Fed!

China is signing trade deals with Brazil and Argentina for agriculture products. We’ve noted this on several occasions. Trump is troubled with these developments and is willing to deepen the trade war as China is buying agriculture products elsewhere.

Nevertheless, overnight, AXIOS reported that the US-China trade deal was now “stalled because of the Hong Kong legislation.” Likely, a phase one deal might not be seen until next year.

E-mini S&P500, Nasdaq, and Rusell 2000 futures are sliding on Trump’s tweets.

House Intelligence Committee ranking member Rep. Devin Nunes told Fox News host Judge Jeanine Pirro Saturday, that phase two of the impeachment hearings will start this week with Chairman Jerrold Nadler who will deliberate on the constitutionality of impeachment.

Nunes said he doesn’t expect anything new from the House Judiciary Committee’s Democrat led investigation.

“Jerry Nadler has been in the witness protection program for several months after he botched the (Robert) Mueller probe. We’re going to see how this goes supposedly they’re going to talk about the constitutionality of impeachment,” said Nunes.

So far the Democrats have not been able to show any evidence that President Donald Trump withheld any aid from Ukraine in exchange for an investigation into former Vice President Joe Biden’s son, Hunter Biden. In fact, Office of Management and Budget Mark Sandy told lawmakers during Schiff’s hearing that the only reason the money was held up for a short period of time was Trump’s concern that other “countries were not contributing more to Ukraine.

The controversy surrounds questionable actions around Hunter Biden’s paid position on the board of Ukrainian energy company Burisma Holdings. His firm Rosemont Seneca Partners LLC, “received regular transfers into one of its accounts — usually more than $166,000 a month — from Burisma from spring 2014 through fall 2015, during a period when Vice President Biden was the main U.S. official dealing with Ukraine and its tense relations with Russia,” according to reports.

No Evidence For Trump Impeachment

Nunes added, “during the (President Richard) Nixon impeachment hearings you had an actual break in – you knew what the crime was. During the (President Bill) Clinton impeachment you knew that he had lied to a grand jury. I think for two weeks one of the things we were able to expose is that not only did they not have a quid pro quo, they actually had to change quid pro quo to bribery until John Ratcliff had to pointed out that the only person ever accused of bribery in Adam Schiff’s star basement down in the capital is Hunter Biden.”

The White House until Dec. 6, to decide whether to participate in the House Judiciary Committee’s impeachment proceedings, Nadler said. The committee will hold it’s first hearing Wednesday, and offered President Donald Trump the option to send someone to represent him.

It is highly unlikely that the White House will send anyone to represent the president at the Wednesday hearing, according to reports.

Four Key Pieces of Evidence Against Democratic Narrative (Republican Memo)

The July 25 call summary – the best evidence of the conversation – shows no conditionality or evidence of pressure;

President Zelensky and President Trump have both said there was no pressure on the call;

The Ukrainian government was not aware of a hold on U.S. Security assistance at the time of the July 25 call; and

President Trump met Ukrainian President and assistance flowed to Ukraine in September 2019. These occurred without Ukraine investigating President Trump’s political rivals.

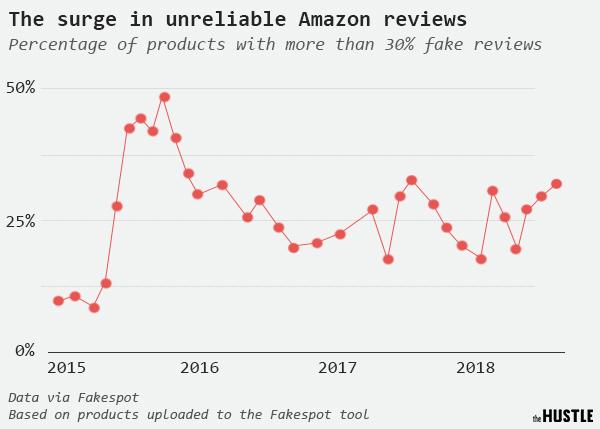

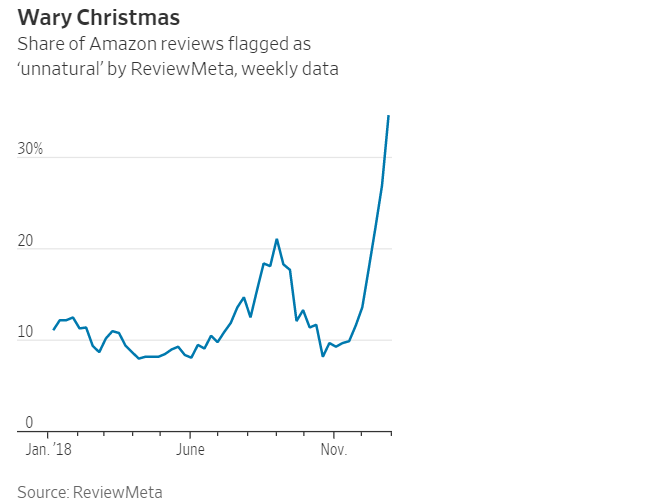

As Black Friday slides into Cyber Monday, you may want to really sift through online product reviews instead of blindly trusting those 5-star reviews.

According to review monitor Fakespot, over 1/3 of online reviews on all major websites – including Amazon, Walmart and Sephora, are fake – meaning they are generated by either bots or people paid to write them, according to the Wall Street Journal. The companies have disputed Fakespot’s findings, but promise they’re doing more to make their reviews more reliable.

In Amazon’s case, it said it has spent more than $400 million to protect customers from review abuse and other fraud or misconduct in the past year, and that it prevented more than 13 million attempts last year to leave inauthentic reviews on its website.

An Amazon spokeswoman said that in the past month more than 99% of the reviews read by customers on its site were authentic. She added that Fakespot can’t determine the authenticity of Amazon reviews, because it doesn’t have access to Amazon’s proprietary data. –WSJ

Online sales are expected to increase by as much as 14% in November and December – now accounting for a whopping 23% of all retail sales excluding automobiles, gasoline and restaurants according to the National Retail Foundation.

“I really rely on reviews, but now I feel like I can’t trust them,” said 40-year-old financial services manager, Jessica Shanmac, who says she was recently ripped off by fake reviews on Amazon – including 5-star rated Christmas tree decorations that were total crap.

“Don’t tell me it’s an amazing product when it’s crappy,” she added.

In April, a two-week investigation by The Hustle‘s Zachary Crockett irevealed rampant fraud within online reviews – primarily from shady Chinese sellers bribing buyers for positive feedback.

Fake reviews have been an issue for Amazon since its inception, but the problem appears to have intensified in 2015, when Amazon.com began to court Chinese sellers.

The decision has led to a flood of new products — a 33% increase, by some accounts — sold by hundreds of thousands of new sellers. Rooted in manufacturing hubs like Guangzhou and Shenzhen, they use Amazon’s fulfillment program, FBA, to send large shipments of electronic goods directly to Amazon warehouses in the US.

This rapid influx has spawned thousands of indistinguishable goods (chargers, cables, batteries, etc.). And it has prompted sellers to game the system. –The Hustle

“The way Amazon presents reviews to you is a form of hypnosis,” says Saoud Khalifah of Fakespot. “They put a glowing 5-star review right in your face. They program you to trust these stars.”

“It’s a lot harder to sell on Amazon than it was 2 or 3 years ago” said ex-Amazon manager Fahim Naim earlier this year. “So a lot of sellers are trying to find shortcuts.”

Los Angeles-based vendor Steve Lee says “You have to play the game to sell now,” adding “And that game is cheating and breaking the law.“

Fakespot uses algorithms and AI to filter reviews and identify ‘problematic’ ones.

They look at whether reviews are spaced evenly over time, or clustered around particular days, as well as how many are written by verified purchasers—those identified as having bought the item directly from the retailer or brand. They also analyze the language, looking for repetition of themes or words that would suggest the posts were written off a script.

One sign that the problem of fake reviews is widespread is the overwhelming number of positive ratings that most products receive. Tommy Noonan, founder of ReviewMeta, which analyzes reviews on Amazon, said his firm noticed a spike in unverified purchase reviews on Amazon’s website in the first three months of 2019, and 98% of them were five-star ratings. Less than 1% were one-star reviews. Amazon removed most of the reviews flagged by ReviewMeta. –WSJ

“The majority of online reviews are positive,” says cybersecurity expert David Décary-Hétu of Flare Systems. “It’s impossible to have that many happy people.“

Greta Thunberg is being taught to Swedish children as part of a course about “religious knowledge,” with kids being asked to mock her opponents.

News outlet Samhällsnytt reported that the 16-year-old climate activist is now included in the school curriculum and is being portrayed in an overtly sympathetic light, with the course describing her as an “alarm clock” that “allows us to discuss, talk, and reflect on what is happening to our world.”

According to one student, “Greta is practically painted as a saint.”

Students are tasked with making memes about Greta that mock her opponents and disprove criticism that has been leveled at her.

“In one task, they are asked to find a picture to illustrate the sentence “One simply doesn’t mess with Greta,” a nod to an outdated Boromir meme from “Lord of the Rings,” reports Sputnik.

According to education publisher Liber, including Greta in lessons is “important to constantly offer materials and teaching materials that reflect the contemporary.”

To the left, Greta has been exalted as some kind of religious figure but given her recent ominous appearance on a looming mural in San Francisco, others view her as a cult leader.

Churches in Sweden are now ringing bells in her honor, while last year the Church of Sweden proclaimed Greta to be “Jesus’s Successor.”

Last month, another mural of Thunberg was defaced in Edmonton, Alberta, with the vandal telling Greta to stop lecturing him on how to live his life.

As I document in the video below, Greta is just another massive hypocrite being used to push an alarmist, hysterical global warming narrative that has been disproved time and time again.

* * *

My voice is being silenced by free speech-hating Silicon Valley behemoths who want me disappeared forever. It is CRUCIAL that you support me. Please sign up for the free newsletter here. Donate to me on SubscribeStar here. Support my sponsor – Turbo Force – a supercharged boost of clean energy without the comedown.

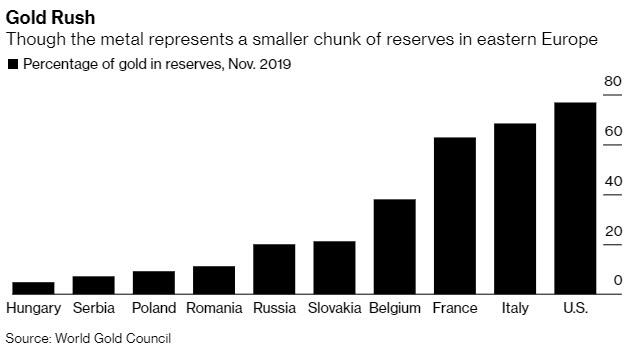

Serbia, Slovakia Join Sudden Eastern European Gold Repatriation Push

The gold rush continues…

Just a few short days after Poland’s government touted its economic might after completing the repatriation of 100 tons of the barbarous relic; and with Hungary‘s anti-immigrant Prime Minister Viktor Orban also ramping up holdings of the safe-haven asset to boost the security of his reserves, more Eastern European nationalist leaders are demanding their country’s gold back on home soil.

As Bloomberg reports, former Slovak Premier Robert Fico, whose odds of returning to power are rising quickly, urged parliament to compel the central bank into repatriating the nation’s gold stocks, which are currently stored in the U.K..

His reason?

Perhaps most vocally reflecting what many other nations also believe – sometimes your international partners can betray you.

Citing a 1938 pact by France, Britain, Italy and Germany allowing Adolf Hitler to annex a chunk what was then Czechoslovakia, Fico told reporters:

“You can hardly trust even the closest allies after the Munich Agreement.

I guarantee that if something happens, we won’t see a single gram of this gold. Let’s do it as quickly as possible.”

Additionally, Serbia’s strongman leader Aleksandar Vucic took note, ordering the central bank to boost reserves and prompting the purchase of nine tons in October.

Vucic said last week that more should be bought because “we see in which direction the crisis in the world is moving.”

The various leaders have a recent example to prove their fears right as the Bank of England refused to return Venezuela’s gold stock over political differences.

“Gold is a symbol,” said Vuk Vukovic, a political economist in Zagreb.

“When states purchase it, people everywhere see it as a sign of economic sovereignty.”

The gold rush mirrors steps by Russia and China to diversify reserves exceeding $3 trillion away from the dollar amid flaring geopolitical tensions with the U.S.

The Secret War in Africa (part 1) covered the overall strategic predominance of US military/ NATO bases – some secret – in Africa, and the expansion by private military contractors (PMC) there in aid of corporate and national interests according to the major powers.

In Part 2 we examine the geopolitical associations in Africa which vary by nation, where major powers have a vested interest in a particular resource causing that major power to assume an aggressive posture to ‘protect’ its national interest by dominating or subverting the African state, in possession of that resource.

Typically those resources include natural gas, oil, gold, diamonds, silver, uranium, coal, rare earth elements and minerals, etc. Thus the major powers have their ‘client states’ in pursuance of the extraction of those resources, where that extraction may result in corruption, confrontation, armed aggression, and even support for terrorist organizations in those states.

In this post-Colonial era the extraction of resources by the major powers in a region where the indigenous people are exhorted to have their own right to self-determination is a significant challenge to global corporations, and former colonial occupiers in Africa like Britain, Belgium, France, Germany, Italy, etc.

When corporate interests either collide or collude with state interests the local insurrection may be severe as mining giant Rio Tinto discovered in Bougainville. Other examples include coal and natural gas in Mozambique; uranium and gold in Niger and Mali; oil in Sudan; diamonds in the Central African Republic, and so on.

France in Africa

Perhaps the most notable component for NATO – specifically for France – is the uranium needed to run its nuclear operations. Most of that uranium originates in Africa even though France has reduced its capacity for nuclear power. Even so, France still receives in excess of two-thirds of its electricity from nuclear power via the former Areva Corporation, now called Framatome.

The uranium mined for Framatome’s nuclear reactors is commonly found in the Sahel region of Africa where most of France’s uranium comes from, primarily northern Niger and Mali. Chad** and Mauritania also possess enormous reserves of the dangerous material. Mali is the fourth-largest supplier of gold too, and with falling registered gold reserves and the already accomplished confiscation of gold by the west from its failed states Mali makes an especially attractive target… particularly for the EU’s struggling banks.

After the indigenous people of the Sahel suffered serious illness from the effect of uranium mining – where drinking water is frequently contaminated – activist leader Almoustapha Alhacen and NGO Aghirin cooperated to oppose France’s corrupt mining giant Areva in Niger and Mali after 2001.

By 2006-2009 the protests and strikes in Agadez and Mali became effective versus Areva. And by 2011 – surprisingly coincident with Hillary Clinton’s “Arab Spring” – mysterious new terror cells appeared in the Sahel subsequent to the NATO destruction of Gaddafi’s government, including:

Movement for Oneness Jihad in West Africa (MUJAO) funded by France/Morocco Intel

Ansar Dine funded by France/Morocco Intelligence Services

Al-Qaeda in the Islamic Maghreb (AQIM) funded by the United States of America CIA

Prior to 2011, a Tuareg rebellion led by the Movement for the Liberation of Azawad (MNLA) had some success versus the Malian government and versus Areva. The MNLA is a legitimate secular rebel group and is not funded by any western intelligence service. MNLA’s success eventually led to air and ground assaults by France in Mali in Operation Serval (with bases in Bamako and N’Djamena) by 2014.

Under the guise of striking al Qaeda and ISIL in Africa – a continent where those groups did not exist prior to 2010 – France invoked air strikes and ground assaults versus the indigenous people who have been most effective in their resistance to Areva.

France’s military uses Bamako airport in Mali (which hosts the MINUSMA mission) and N’Djamena in Chad where these facilities certainly do not provide ideal bases for striking the rebellious indigenous population of the region. * Unfortunately for Macron’s ultra-high-tech world order, Bomako and N’Djamena air strips are ill-equipped for modern military aircraft.

Now, with the commissioning of the US Niger Air Base 201 as of November 1st, 2019, the question arises as to whether Macron will be allowed to use this base to bomb Tuareg protestors. That’s because NATO and the US military will not reveal whether Niger Base 201 may be jointly used, where all such communications appear to be classified. However, Base 201 may be considered a defacto ‘secret’ NATO air base.

Note that the United States imports less than 3% of its uranium from Niger whereas France imports more than ten times that much (in percentage terms). While the United States imports very little oil from Africa, France by contrast imports large amounts. France imports oil from Nigeria, from Angola, Libya and Algeria — comprising one-quarter of France’s oil imports overall.

These ‘divergent goals’ and the rift between the United States and France has recently come to light. France’s position in Africa has been modified by the ascendance of Donald Trump because under the Obama regime the United States and France had been marching in goose-step… or, lockstep.. but not anymore — at least for now.

The United States has asked France and all other NATO nations to contribute more funding to the construction and operation of bases – including Air Base 201 and other NATO bases. But even if France does have the use of Niger Base 201 it is clear that Macron prefers to see such a base owned and controlled by the European Union. Overall, the foregoing may lend some insight about Macron’s drastic words ie that NATO is ‘brain dead’.

France is evidently wheeling for a predominant position in the EU as a major power which has escaped France so far and (perhaps) resulted in NATO keeping quiet about its bases in Africa. At present all such NATO bases in Africa are used secretly or covertly by NATO because NATO does not fund any US military base.

United States Bases in Africa

The United States has its own agenda of course for the thirty-four military bases it operates in Africa (with many more under construction). One can only surmise about the rapid growth of bases there since 2016. It appears that this rapid growth is not based on a particular goal to cull resources in Africa at present; instead the US intends to maintain its role as global hegemon, to manage its Empire by Terror in the region, and to resist any nascent exploitation of African resources or expansion by Russia or China.

The United States is of course forward-looking in its role as unilateral global hegemonic and understands that it will not always be self-sufficient in oil. At some point shale and fracking will be done where Oilprice touts that shale is already in trouble with fracking to follow by 2024.

In that event — and since the United States has already destroyed most of the Middle East — Africa will become important to the US as a source for oil going forward. Meanwhile US plans to expand its designs on natural gas from Mozambique and elsewhere in Africa continue apace.

In summary US bases in Africa serve these purposes:

Beheading anyone by drone as seen fit

A gateway to African resources if and when they are needed (generally corporate)

To prevent and discourage Russia and China from exploiting resources in Africa

Use of bases by NATO should that interest coincide with US interest

Reinforcement of the US global hegemonic

Russian Base in Eritrea

Russia has only one base in Africa. Russia’s Eritrea Logistics Centre is a recent development and the intended purpose for this site is presently unclear and it may not be a military base. However the Russian leadership has publicly expressed its interest in developing resources in Africa especially to provide safe nuclear power on the continent, and this site may bear some relation.

As covered in part 1 , private military contractors from Russia have been active providing security in the following African states:

Central African Republic, Resources: gold, timber, diamonds

Libya: Oil, natural gas, iron ore

Mozambique: Russian giant Gazprom was in competition with US Exxon for a large natural gas contract in a lawless region of Mozambique which was awarded to Exxon

Angola: iron ore, diamonds, petroleum, bauxite, uranium, feldspar and petroleum

The relevant resources are listed because PMC contractors are generally hired to protect these resources on behalf of their private clients — no Russian Federation bases in Africa or Russian governmental ambitions are involved. PMC contractors support either Russian corporate interests or the local interests of their hosts and clients in Africa.

Regardless, the presence of private military contractors in Africa with connections to any Russian private business bears no relation – not even a remote comparison — to the massive and bloated US military presence in Africa.

China’s PLA Military Support Base in Djibouti

China’s military base in Djibouti was established in 2017 perhaps to counter the growing threat of US unilateralism. Since the base opened, a number of alarming reports have appeared in the US major media including the idea that the US could ‘lose its only base in Africa’ due to China’s presence when in fact Washington supports a vast number of bases in Africa.

China states that its purpose in Djibouti is to maintain peace in the region and to support humanitarian operations in Africa. That China appreciates African resources and their potential for development is just as relevant as saying that all other major powers appreciate the same.

China has a specific vested interest in patrolling the Gulf of Aden to ensure that piracy versus its shipping is kept in check.

Summary

There is a trite saying that the last frontier is space, but for those of us on earth it’s clear that Africa is the last frontier. Africa is a continent of resources and promise that could be responsibly developed and thrive if there were only any will in the world to do so.

Climate change and a declining world order make the prospect for Africa look bleak, as well as the resurgence in western colonial thought which sees Africa not as a treasure chest for promise, but for greed.

There are tiny rays of hope for Africa in the form of Algeria, Tunisia, and even Eritrea… but the colliding world disorder of west versus east and ever-deepening corruption in the ever-decaying west may not spare Africa. The ‘secret war’ in Africa is just that – secret, and shall remain so, so long as the new world disorder — primarily engendered by the west – continues in its apparent death spiral.

On November 11th, the very disturbing but clearly true “Lessons To Learn From The Coup In Bolivia” was posted to the Web. That anonymous author (a German intelligence analyst) documented the evilness of the overthrow of Evo Morales in Bolivia, and the threat now clearly posed to the world by the US regime — a spreading cancer of expansionist fascism, led from Washington. But, even more than this, he indicated that unless the individuals who are responsible for the advancing fascism are executed, there won’t be any real hope for democracy anywhere in the world.

Either this impunity will stop, or else the spread of the US international dictatorship — not only by CIA coups such as this, but by illegal international invasions such as of Iraq 2003, Libya 2011, Syria 2012-, and Yemen 2015-, — will continue and will engulf in misery ultimately the entire world. He makes clear the complicity of US ‘news’-media in the lies that ‘justify’ this coup (and ‘justified’ those invasions). It’s, by now, clearly the way the US regime functions. Of course, none of those media will publish any such truth; they all cover-up constantly for the regime, because they actually are an essential part of it. (All of these invasions and coups are based on nothing but lies, and the media are a necessary part of that.) Censorship in America is thus actually extreme, and constant.

Will the CIA and generals, and Bolivia’s oligarchs, be executed for that? Of course, they should be. If they aren’t, then how can democracy ever be restored there? It’s one, or the other — it’s continuation of the dictatorship, or else it will be restoration of the democracy — at this stage. There can be no ‘reconciliation’, now. This is an irreconcilable state of war that exists between the coupsters and the Bolivian people. There will be bloodshed — and the more so as the coupsters remain in power and Morales not be quickly restored fully to the powers to which he had repeatedly been popularly elected. However, he won’t be able safely to return to his home and his homeland, unless and until the coupsters are executed, because, otherwise, they certainly would execute him first, and he would never be able to feel safe there.

Because of what the coupsters did, this will inevitably be a war to the death — and not only for the principal persons on each side, but for hundreds, or probably thousands, of their followers. What the coupsters did has thus precipitated, inevitably, massive future bloodshed in Bolivia. And yet the US regime’s lying press supports what was done. The truths that they know they hide from the public. This constant lying will be necessary in order for the US regime’s extensions such as the OAS and the IMF to provide the coupsters the public support that will enable the Bolivian coup-regime to be granted international ‘legitimacy’, which will be necessary in order for that regime’s actions to be treated as legally valid and binding in international business.

Unfortunately, the only global solution would be a second American Revolution, but, this time, the news-media are far less honest, and so almost no support exists amongst the US population for doing that.

Consequently, the outlook for the future, worldwide, is grim.

If the warning (hidden by the media as it is), this time from Bolivia, is not heeded, how can this cancer ever be stopped from engulfing the entire world?