Uber Helicopter Rides To JFK Cost Less Than Its Car Rides At One Point

Ah, the wonders of city gridlock, and the gifts it showers upon us…

It turns out that Manhattan is so congested and impossible to drive through that, at one point in time, it actually cost less to take an Uber helicopter to JFK airport from downtown than it did to take a car, according to Bloomberg.

The helicopter ride, which takes about 8 minutes, cost $108.98 at one point, which is almost 33% less than the $163.11 charge a rider would have racked up taking an Uber Black and slightly higher than the $100.35 it cost to take an UberX on the same trip.

The pricing of its helicopter rides varies with demand, location and time of day. Still, it was an odd arbitrage given Uber’s new commitment to slashing rider discounts in order to try and achieve profitability.

The chopper rides usually cost between $200 and $225. The discount was called a temporary offer for “a small, random set of riders,” the company said.

The company declined to talk about how many total chopper rides it has given since it introduced the service this past summer. The company is collecting data from its NYC service, which runs Monday through Friday during afternoon rush hour.

Uber will use the data to try and determine whether or not to expand the service.

The company’s Uber Elevate program – a larger aerial ridesharing initiative – is still set to test flights in Dallas, Los Angeles and Melbourne next year. The service is set to become available in 2023.

Uber’s expansion into aerial highlights the company’s ambitions of growing, while at the same time targeting becoming a profitable company.

Chief Executive Officer Dara Khosrowshahi said in November that the company would only focus on businesses and markets where it could establish or defend a top leadership position, putting more focus on the company’s quest to stop burning cash.

From a big picture perspective, the largest rift in American politics is between those willing to admit reality and those clinging to a dishonest perception of a past that never actually existed. Ironically, those who most frequently use “post-truth” to describe our current era tend to be those with the most distorted view of what was really happening during the Clinton/Bush/Obama reign.

Despite massive amounts of evidence to the contrary, such people now enthusiastically whitewash the decades preceding Trump to turn it into a paragon of human liberty, justice and economic wonder. You don’t have to look deep to understand that resistance liberals are now actually conservatives, brimming with nostalgia for the days before significant numbers of people became wise to what’s been happening all along.

They want to forget about the bipartisan coverup of Saudi Arabia’s involvement in 9/11, all the wars based on lies, and the indisputable imperial crimes disclosed by Wikileaks, Snowden and others. They want to pretend Wall Street crooks weren’t bailed out and made even more powerful by the Bush/Obama tag team, despite ostensible ideological differences between the two. They want to forget Epstein Didn’t Kill Himself.

Lying to yourself about history is one of the most dangerous things you can do. If you can’t accept where we’ve been, and that Trump’s election is a symptom of decades of rot as opposed to year zero of a dangerous new world, you’ll never come to any useful conclusions. As such, the most meaningful fracture in American society today is between those who’ve accepted that we’ve been lied to for a very long time, and those who think everything was perfectly fine before Trump. There’s no real room for a productive discussion between such groups because one of them just wants to get rid of orange man, while the other is focused on what’s to come. One side actually believes a liberal world order existed in the recent past, while the other fundamentally recognizes this was mostly propaganda based on myth.

Irrespective of what you think of Bernie Sanders and his policies, you can at least appreciate the fact his supporters focus on policy and real issues. In contrast, resistance liberals just desperately scramble to put up whoever they think can take us back to a make-believe world of the recent past. This distinction is actually everything. It’s the difference between people who’ve at least rejected the status quo and those who want to rewind history and perform a do-over of the past forty years.

A meaningful understanding that unites populists across the ideological spectrum is the basic acceptance that the status quo is pernicious and unsalvageable, while the status quo-promoting opposition focuses on Trump the man while conveniently ignoring the worst of his policies because they’re essentially just a continuation of Bush/Clinton/Obama. It’s the most shortsighted and destructive response to Trump imaginable. It’s also why the Trump-era alliance of corporate, imperialist Democrats and rightwing Bush-era neoconservatives makes perfect sense, as twisted and deranged as it might seem at first. With some minor distinctions, these people share nostalgia for the same thing.

This sort of political environment is extremely unhealthy because it places an intentional and enormous pressure on everyone to choose between dedicating every fiber of your being to removing Trump at all costs or supporting him. This anti-intellectualism promotes an ends justifies the means attitude on all sides. In other words, it turns more and more people into rhinoceroses.

Eugène Ionesco’s masterpiece, Rhinoceros, is about a central European town where the citizens turn, one by one, into rhinoceroses. Once changed, they do what rhinoceroses do, which is rampage through the town, destroying everything in their path. People are a little puzzled at first, what with their fellow citizens just turning into rampaging rhinos out of the blue, but even that slight puzzlement fades quickly enough. Soon it’s just the New Normal. Soon it’s just the way things are … a good thing, even. Only one man resists the siren call of rhinocerosness, and that choice brings nothing but pain and existential doubt, as he is utterly … profoundly … alone.

A political environment where you’re pressured to choose between some ridiculous binary of “we must remove Trump at all costs” or go gung-ho MAGA, is a rhinoceros generating machine. The only thing that happens when you channel your inner rhinoceros to defeat rhinoceroses, is you get more rhinoceroses. And that’s exactly what’s happening.

The truth of the matter is the U.S. is an illiberal democracy in practice, despite various myths to the contrary.

An illiberal democracy, also called a partial democracy, low intensity democracy, empty democracy, hybrid regime or guided democracy, is a governing system in which although elections take place, citizens are cut off from knowledge about the activities of those who exercise real power because of the lack of civil liberties; thus it is not an “open society”. There are many countries “that are categorized as neither ‘free’ nor ‘not free’, but as ‘probably free’, falling somewhere between democratic and nondemocratic regimes”. This may be because a constitution limiting government powers exists, but those in power ignore its liberties, or because an adequate legal constitutional framework of liberties does not exist.

It’s not a new thing by any means, but it’s getting worse by the day. Though many of us remain in denial, the American response to various crises throughout the 21st century was completely illiberal. As devastating as they were, the attacks of September 11, 2001 did limited damage compared to the destruction caused by our insane response to them. Similarly, any direct damage caused by the election and policies of Donald Trump pales in comparison to the damage being done by the intelligence agency-led “resistance” to him.

“Liberal resistance” since 2016:

– Pussy hats

– Russiagate flop

– Let’s beg the tech giants to censor speech we don’t like.

– Hurray for permanent, unelected government. Such smarties!

We don’t have to be. Turning into a rhinoceros happens easily if you’re unaware of what’s happening and not grounded in principles, but ultimately it is a choice. The decision to discard ethics and embrace dishonesty in order to achieve political ends is always a choice. As such, the most daunting challenge we face now and in the chaotic years ahead is to become better as others become worse. A new world is undoubtably on the horizon, but we don’t yet know what sort of world it’ll be. It’s either going to be a major improvement, or it’ll go the other way, but one thing’s for certain — it can’t stay the way it is much longer.

If we embrace an ends justifies the means philosophy, it’s going to be game over for a generation. The moment you accept this tactic is the moment you stoop down to the level of your adversaries and become just like them. It then becomes a free-for-all for tyrants where everything is suddenly on the table and no deed is beyond the pale. It’s happened many times before and it can happen again. It’s what happens when everyone turns into rhinoceroses.

* * *

If you enjoyed this, I suggest you check out the following 2017 posts. It’s never been more important to stay conscious and maintain a strong ethical framework.

Liberty Blitzkrieg is an ad-free website. If you enjoyed this post and my work in general, visit the Support Page where you can donate and contribute to my efforts.

Saudi Arabia Arrests At Least 9 ‘High-Profile’ People Despite Jittery IPO Push

Apparently feeling emboldened by the fact that Saudi Arabia suffered zero repercussions over the Oct.3, 2018 state-ordered murder of Jamal Khashoggi, other than crown Prince Mohammad bin Salman (MbS) briefly being shunned by international elites for a few months, it’s business as usual again in the kingdom of horrors.

In a new breaking report, The Wall Street Journalreveals that “Saudi authorities have arrested several high-profile people in recent days, extending an effort to sideline Crown Prince Mohammed bin Salman’s perceived opponents, despite a push to repair the kingdom’s international image to attract investment.”

Yasser al-Rumayyan, Saudi Aramco’s chairman, via Reuters.

The WSJ counts nine people total arrested in a span of a little more than the past week who are not particularly known for being dissidents or any level of explicitly anti-government activists. They include journalists, intellectuals and businessmen detained since Nov. 16.

What additionally makes these detentions particularly brazen on the part of Riyadh authorities is that it comes just in the final stages of the kingdom preparing for the launch of what most see as the biggest listing in history, Saudi Aramco IPO.

The damning WSJ report hit the same day that Aramco executives met with Abu Dhabi Investment Authority (ADIA) officials in the UAE to discuss investment options and possibilities in the oil giant’s debut share sale, and at a moment the kingdom is desperate to attract a major anchor investor to ensure success.

It appears MbS — no doubt further emboldened by continued support from President Trump even after the Khashoggi affair — realizes a pesky little issue like human rights abuses, including torture of dissidents and continued record pace beheadings and crucifixions, can’t stand in the way.

It also looks as if MbS wants to continue to preempt any future possible criticism from within, given the following:

A person familiar with the matter said all of the people arrested in recent days had been identified by the government for writing or speaking in support of the 2011 Arab Spring uprisings that toppled a series of Middle Eastern governments.

The ‘Arab Spring’ of some eight years ago left little impact in Saudi Arabia, though there were reports of sporadic intense protests among the country’s restive Shia population in the eastern part of the kingdom. The Saudi military did lend support to the allied Bahraini monarchy by sending tanks across the King Fahd Causeway to crush a popular uprising in the streets there.

Interestingly some among the arrested were intellectuals and human rights organization members who themselves had previously voiced support for and participated in initiatives connected with MbS’ reform initiative.

The WSJ reports of others who don’t fit the profile of dissidents in any clear way: “Another, prominent philosopher Sulaiman al-Saikhan al-Nasser, participated in government-sponsored cultural initiatives… Also arrested in recent days were Fuad al-Farhan and Musab Fuada, who both started a company that offers business skills training… Abdulaziz al-Hais, is a former journalist who now owns a carpentry business…. Abdulrahman Alshehri is a journalist who has written for domestic and international outlets.”

One official with Human Rights Watch (HRW) told the WSJ, “It’s all connected to the same campaign of trying to eliminate independent voices in Saudi society, of going after anyone who could be even mildly critical or independent.”

This week, three major winter storms will batter most of the country with ice, snow and bitterly cold temperatures just in time for Thanksgiving. It is being projected that 55 million Americans will be traveling this week, and so this bizarre weather comes at a very bad time. But of course we have already seen a series of blizzards roar across the nation in recent weeks and hundreds of record cold temperatures have already been shattered and we are still about a month away from the official start of winter. Normally, it isn’t supposed to be this cold or this snowy yet, but we don’t live in “normal” times.

Scientists tell us that solar activity becomes very quiet during a “solar minimum”, and when solar activity becomes very quiet we tend to have very cold winters. And in recent months solar activity has been very, very low. In fact, we haven’t seen any sunspots at all “since November 2”…

We have not seen any sunspots since November 2, and at that time they were only visible for two days, and prior to that no sunspots since October 2.

Unless things change, and that is not expected to happen, we should prepare for a very cold and very snowy winter. And this upcoming week is likely to be a preview of coming attractions. According to CNN, holiday travelers will have three major winter storms to deal with…

As Thanksgiving week starts, a record number of travelers will be dealing with three storms nationwide that will add to the holiday stress.

One storm will lash the East and will affect travel through Sunday, another one will batter the Midwest on Tuesday and a third one will move through the West on Wednesday.

Forecasters are telling us that Denver could receive a foot of snow, but it isn’t too unusual for Denver to get a lot of snow.

But it is unusual for Arizona, New Mexico and Texas to get snow this time of the year, and apparently it looks like that could happen on Wednesday…

By Wednesday Arizona could see snow, as could New Mexico, the northern Texas Panhandle, Oklahoma Panhandle.

As that storm moves through the Midwest,“winterlike travel” is expected over large portions of the heartland…

“At this time, enough snow to create winterlike travel is anticipated from central and northeastern Colorado to much of Nebraska, northern Kansas, much of Iowa, northwestern Missouri, northwestern Illinois, southeastern Minnesota, central and eastern Wisconsin and northern Michigan,” AccuWeather Senior Meteorologist Brett Anderson said.

Forecasters expect Tuesday into Wednesday to bring the worst conditions in the Midwest, with strong, gusty winds battering such key airports as Chicago’s O’Hare International Airport.

Shortly thereafter, an absolutely massive winter storm is going to hit California really hard, and we are being told that “travel may be impossible” in certain areas…

Winter storm watches have already been issued for the Sierra and the National Weather Service is saying travel may be impossible as snow levels drop which could lead to numerous road closures Wednesday into Thursday.

Several feet is forecast to snow in the mountains. In the lower elevations and along the coast, it will be rain with the possibility of totals reaching 5 inches.

This definitely is not normal.

In some parts of the country, it feels like winter already arrived more than a month ago. This has had a huge impact on harvest season, and unusually cold temperatures could also make things extremely difficult for farmers that plan to grow crops this winter. The following comes from Martin Armstrong…

The BIG FREEZE is upon us. The volatility in weather that our computer has been forecasting on a long-term basis should result in this winter being colder than the last. In Britain, the snow has hit an already flood-ravaged country as temperatures plunged to -7C. This is part of the problem we face. The ground freezes down and this prevents winter crops. During the late 1700s, the ground froze to a depth of 2 feet according to John Adams.

SCOTLAND is forecast the coldest winter for 10 years – with -13C lows, snow, ice and travel woes, with a weak sun and Arctic chills blamed.

The worst winter since 2009-10 is due as the sun is at the weakest point of its 11-year cycle of strength, said The Weather Company, the world’s biggest commercial forecaster.

The last time the sun’s power was as low as now, Scotland saw the bitter 2009-10 winter, Britain’s coldest winter since the 1970s, and the 2010 Big Freeze, with the coldest December ever recorded.

We are witnessing bizarrely cold weather all over the northern hemisphere, but most people don’t understand why this is happening.

More than anything else, solar activity determines whether conditions are going to be warmer or colder than normal. So this is why the Farmers’ Almanac and the Old Farmer’s Almanac are both telling us that this winter will be bitterly cold and very snowy…

Not long after the Farmers’ Almanac suggested it would be a “freezing, frigid, and frosty” season, the *other* Farmer’s Almanac has released its annual weather forecast—and it’s equally upsetting.

While the first publication focused on the cold temperatures anticipated this winter, the Old Farmer’s Almanac predicts that excessive snowfall will be the most noteworthy part of the season.

The Old Farmer’s Almanac, which was founded in 1792, says that the upcoming winter “will be remembered for strong storms” featuring heavy rain, sleet, and a lot of snow. The periodical actually used the word “snow-verload” to describe the conditions we can expect in the coming months.

Scientists are hoping that solar activity will return to normal soon, but there is no guarantee that will happen. In fact, in a recent article I explained that some experts believe that we may have entered a “grand solar minimum” similar to the Maunder Minimum that created a “mini ice age” in the 17th century. The sunspot cycle virtually vanished from 1645 to 1715, and this resulted in bitterly cold temperatures, disastrous harvests and famines that killed millions upon millions of people all over the globe.

Hopefully things will not get that bad any time soon, but without a doubt we live at a time when global weather patterns are going absolutely haywire. We should be hoping for the best, but we should also be preparing for the worst.

This week, the crazy weather will be a major headache for holiday travelers, but that is just a temporary problem. If solar activity does not return to normal over the next few years, we will soon have far larger issues to deal with.

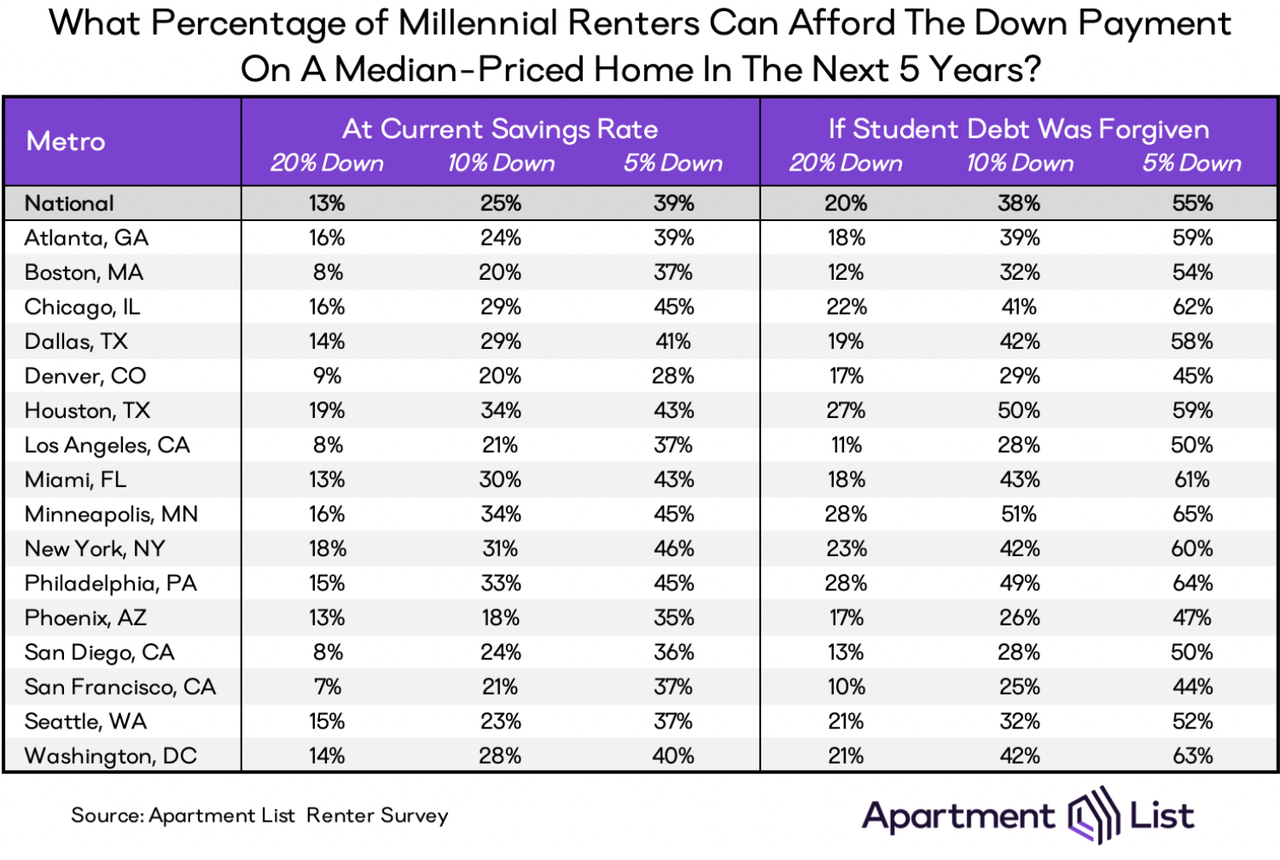

75% Of Millennials May Never Be Able To Afford Owning A House

More so than with Gen X and the Baby Boomers, housing has become indelibly tied up with the millennial identity. That’s largely because economic hardship – or at the very least, stagnation and heavy debt – is perhaps the single defining characteristic of the generation that came or age during or just after the financial crisis nearly destroyed the global economy.

And while many had hoped that millennials would find their footing and their economic prospects would improve with time, sadly, that’s just not the case for many millennials.

And in its latest study of millennial attitudes toward the housing market, Apartment List found that a growing percentage of those surveyed said they fully expected to be renters forever. Unsurprisingly, the percentage of respondents who felt that homeownership would be forever out of reach was higher in expensive urban enclaves like NYC, and many cities across the state of California.

But perhaps the most alarming finding from the study stems from the researchers examination of student debt and how the burden of making their monthly loan payments impacts their ability to save for a down payment. At the current savings rate, just 25% of millennial renters will be ready to put down 10% on a median-priced starter home in the next five years (typically, buyers need 20% down to get a mortgage). That means 75% of millennials likely won’t be able to afford a down payment any time soon.

To better understand the barrier created by student debt, Apartment List tried to simulate Bernie Sanders’ proposal to take all student debt payments and apply them to down payments instead. Apartment List found that the effect would be significant: Across the country the percentage of millennials who would soon be able to afford a 10% down payment on a median condo would rise from 25% to 38%.

After more than a decade of decline, the national homeownership rate is finally climbing again. But the Apartment List study is unfortunately just the latest to show that the situation for millennials hasn’t improved. Half of millennials have nothing saved for a downpayment (despite being dangerous close to – or past – the age of 30). If this keeps up, millennials can ditch that tired sobriquet for something more appropriate: Generation Rent.

The most shocking thing about the House impeachment hearings to this point is not a “smoking gun” witness providing irrefutable evidence of quid pro quo. It’s not that President Trump may or may not have asked the Ukrainians to look into business deals between then-Vice President Biden’s son and a Ukrainian oligarch.

The most shocking thing to come out of the hearings thus far is confirmation that no matter who is elected President of the United States, the permanent government will not allow a change in our aggressive interventionist foreign policy, particularly when it comes to Russia.

Even more shocking is that neither Republicans nor Democrats are bothered in the slightest!

Take Lt. Colonel Vindman, who earned high praise in the mainstream media. He did not come forth with first-hand evidence that President Trump had committed any “high crimes” or “misdemeanors.” He brought a complaint against the President because he was worried that Trump was shifting US policy away from providing offensive weapons to the Ukrainian government!

He didn’t think the US president had the right to suspend aid to Ukraine because he supported providing aid to Ukraine.

According to his testimony, Vindman’s was concerned over “influencers promoting a false narrative of Ukraine inconsistent with the consensus views of the interagency.”

“Consensus views of the interagency” is another word for “deep state.”

Vindman continued, “While my interagency colleagues and I were becoming increasingly optimistic on Ukraine’s prospects, this alternative narrative undermined US government efforts to expand cooperation with Ukraine.”

Let that sink in for a moment:Vindman did not witness any crimes, he just didn’t think the elected President of the United States had any right to change US policy toward Ukraine or Russia!

Likewise, his boss on the National Security Council Staff, Fiona Hill, sounded more like she had just stepped out of the 1950s with her heated Cold War rhetoric. Citing the controversial 2017 “Intelligence Community Assessment” put together by then-CIA director John Brennan’s “hand-picked” analysts, she asserted that, “President Putin and the Russian security services aim to counter US foreign policy objectives in Europe, including in Ukraine.”

And who gets to decide US foreign policy objectives in Europe? Not the US President, according to government bureaucrat Fiona Hill. In fact, Hill told Congress that, “If the President, or anyone else, impedes or subverts the national security of the United States in order to further domestic political or personal interests, that is more than worthy of your attention.”

Who was Fiona Hill’s boss? Former National Security Advisor John Bolton, who no doubt agreed that the president has no right to change US foreign policy. Bolton’s the one who “explained” that when Trump said US troops would come home it actually meant troops would stay put.

One by one, the parade of “witnesses” before House Intelligence Committee Chairman Schiff sang from the same songbook. As US Ambassador to the EU, Gordon Sondland put it, “in July and August 2019, we learned that the White House had also suspended security aid to Ukraine. I was adamantly opposed to any suspension of aid, as the Ukrainians needed those funds to fight against Russian aggression.”

Meanwhile, both Democrats and Republicans in large majority voted to continue spying on the rest of us by extending the unpatriotic Patriot Act. Authoritarianism is the real bipartisan philosophy in Washington.

Triggered: Mayor de Blasio Threatens To Destroy FedEx Robots Running Around New York

FedEx’s new package-delivering robots have been spotted on the streets of New York City, according to dozens of city dwellers who posted pictures and videos of the robots onto social media.

The SameDay Bot is expected to enter commercial service in February 2020, and it uses artificial intelligence, sensors, and stair-climbing wheels to traverse the city’s most challenging terrain.

Twitter user @WhatIsNewYork tweeted last week a short video of the robot rolling down Crosby Street near Houston Street.

Upon the sightings of the robot, Mayor de Blasio was triggered on social media, who tweeted, “First of all, @FedEx, never get a robot to do a New Yorker’s job. We have the finest workers in the world.”

Adding that “Second of all, we didn’t grant permission for these to clog up our streets. If we see ANY of these bots, we’ll send them packing.”

First of all, @FedEx, never get a robot to do a New Yorker’s job. We have the finest workers in the world.

Second of all, we didn’t grant permission for these to clog up our streets. If we see ANY of these bots we’ll send them packing. https://t.co/XxJIrIW9vr

City Hall spokesman Will Baskin-Gerwitz told the New York Post that city employees will remove the robots from city streets.

“These large autonomous robots are not allowed on city streets, and they’re a public safety hazard for New Yorkers. We’ll use appropriate methods to remove them immediately,” Baskin-Gerwitz told The Post.

The de Blasio administration’s violent reaction to robots is a typical ‘Ok Boomer’ response to new technology that will displace millions of jobs by 2030.

Automation in New York City could lead to hundreds of thousands of job losses in the coming years, likely to impact industries such as food service, retail, transportation, and warehousing the hardest.

De Blasio knows that the proliferation of robots on the streets of New York City could lead to a large number of job losses and further push wealth inequality to the extreme. This would destroy the social fabric that has kept everyone complacent in the city; any social unrest could unravel his party’s socialist agenda for the city.

Like so many other glib “Russia experts” with access to Establishment media, Fiona Hill, who testified last week in the impeachment probe, seems three decades out of date…

Fiona Hill’s “Russian-expert” testimony Thursday and her deposition on Oct. 14 to the impeachment inquiry showed that her antennae are acutely tuned to what Russian intelligence services may be up to but, sadly, also displayed a striking naiveté about the machinations of U.S. intelligence.

Hill’s education on Russia came at the knee of the late Professor Richard Pipes, her Harvard mentor and archdeacon of Russophobia. I do not dispute her sincerity in attributing all manner of evil to what President Ronald Reagan called the “Evil Empire.” But, like so many other glib “Russia experts” with access to Establishment media, she seems three decades out of date.

I have been studying the U.S.S.R. and Russia for twice as long as Hill, was chief of CIA’s Soviet Foreign Policy Branch during the 1970s, and watched the “Evil Empire” fall apart. She seems to have missed the falling apart part.

Selective Suspicion

Are the Russian intelligence services still very active? Of course. But there is no evidence — other than Hill’s bias — for her extraordinary claim that they were behind the infamous “Steele Dossier,” for example, or that they were the prime mover of Ukraine-gate in an attempt to shift the blame for Russian “meddling” in the 2016 U.S. election onto Ukraine. In recent weeks U.S. intelligence officials were spreading this same tale, lapped up and faithfully reported Friday by The New York Times.

Hill has been conditioned to believe Russian President Vladimir Putin and especially his security services are capable of anything, and thus sees a Russian under every rock — as we used to say of smart know-nothings like former CIA Director William Casey and the malleable “Soviet experts” who bubbled up to the top during his reign (1981 – 1987). Recall that at the very first meeting of Reagan’s cabinet, Casey openly told the president and other cabinet officials: “We’ll know our disinformation program is complete when everything the American public believes is false.” Were Casey still alive, he would be very pleased and proud of Hill’s performance.

Beyond Dispute?

On Thursday Hill testified:

“The unfortunate truth is that Russia was the foreign power that systematically attacked our democratic institutions in 2016. This is the public conclusion of our intelligence agencies, confirmed in bipartisan Congressional reports. It is beyond dispute, even if some of the underlying details must remain classified.” [Emphasis added.]

Ah, yes. “The public conclusion of our intelligence agencies”: the same ones who reported that the Communist Party of the Soviet Union would never surrender power peaceably; the same ones who told Secretary of State Colin Powell he could assure the UN Security Council that the WMD evidence given him by our intelligence agencies was “irrefutable and undeniable.” Only Richard-Pipeline-type Russophobia can account for the blinders on someone as smart as Hill and prompt her to take as gospel “the public conclusions of our intelligence agencies.”

A modicum of intellectual curiosity and rudimentary due diligence would have prompted her to look into who was in charge of preparing the (misnomered) “Intelligence Community Assessment” published on Jan. 6, 2017, which provided the lusted-after fodder for the “mainstream” media and others wanting to blame Hillary Clinton’s defeat on the Russians.

Jim, Do a Job on the Russians

President Barack Obama gave the task to his National Intelligence Director James Clapper, whom he had allowed to stay in that job for three and a half years after he had to apologize to Congress for what he later admitted was a “clearly erroneous” response, under oath, to a question from Sen. Ron Wyden (D-OR) on NSA surveillance of U.S. citizens. And when Clapper published his memoir last year, Hill would have learned that, as Defense Secretary Donald Rumsfeld’s handpicked appointee to run satellite imagery analysis, Clapper places the blame for the consequential “failure” to find the (non-existent) WMD “where it belongs — squarely on the shoulders of the administration members who were pushing a narrative of a rogue WMD program in Iraq and on the intelligence officers, including me, who were so eager to help that we found what wasn’t really there.” [Emphasis added.]

President Barack Obama with Director of National Intelligence James Clapper, 2011. (White House/ Pete Souza)

But for Hill, Clapper was a kindred soul: Just eight weeks after she joined the National Security Council staff, Clapper, during an NBC interview on May 28, 2017, recalled “the historical practices of the Russians, who typically, are almost genetically driven to co-opt, penetrate, gain favor, whatever, which is a typical Russian technique.” Later he added, “It’s in their DNA.” Clapper has claimed that “what the Russians did had a profound impact on the outcome of the election.”

As for the “Intelligence Community Assessment,” the banner headline atop The New York Times on Jan. 7, 2017 set the tone for the next couple of years: “Putin Led Scheme to Aid Trump, Report Says.” During my career as a CIA analyst, as deputy national intelligence officer chairing National Intelligence Estimates (NIEs), and working on the Intelligence Production Review Board, I had not seen so shabby a piece of faux analysis as the ICA. The writers themselves seemed to be holding their noses. They saw fit to embed in the ICA itself this derriere-covering note: “High confidence in a judgment does not imply that the assessment is a fact or a certainty; such judgments might be wrong.”

Not a Problem

With the help of the Establishment media, Clapper and CIA Director John Brennan, were able to pretend that the ICA had been approved by “all 17 intelligence agencies” (as first claimed by Clinton, with Rep. Jim Himes, D-CT, repeating that canard Thursday, alas “without objection).” Himes, too should do his homework. The bogus “all 17 intelligence agencies” claim lasted only a few months before Clapper decided to fess up. With striking naiveté, Clapper asserted that ICA preparers were “handpicked analysts” from only the FBI, CIA and NSA. The criteria Clapper et al. used are not hard to divine. In government as in industry, when you can handpick the analysts, you can handpick the conclusions.

Maybe a Problem After All

“According to several current and former intelligence officers who must remain anonymous because of the sensitivity of the issue,” as the Times says when it prints made-up stuff, there were only two “handpicked analysts.” Clapper picked Brennan; and Brennan picked Clapper. That would help explain the grossly subpar quality of the ICA.

If U.S. Attorney John Durham is allowed to do his job probing the origins of Russiagate, and succeeds in getting access to the “handpicked analysts” — whether there were just two, or more — Hill’s faith in “our intelligence agencies,” may well be dented if not altogether shattered.

China Central Bank Warns Downward Pressure On Economy Increasing

Several weeks ago, the People’s Bank of China (PBOC) said it would “increase counter-cyclical adjustments” to prevent downward pressure on the economy. Now the PBOC is warning that it might not be able to ward off these downward pressures in the short term, reported Reuters.

The PBOC’s annual financial stability report said China would continue to deploy fiscal and monetary policies to support the economy but warned economic deceleration would continue through year-end.

Policy maneuvering by the PBOC will be limited as it will likely need to cut rates and the amount of money banks put down as reserves to promote credit growth.

The PBOC recognizes the rapid deterioration in the economy, along with the limitations of monetary policy to revive growth.

Likely, credit creation via the PBOC won’t be in magnitude seen in the last ten years used to save the world from escaping several deflationary crashes.

The government will likely stabilize its economy or at least create a softer landing through tax cuts and infrastructure spending, the annual report said.

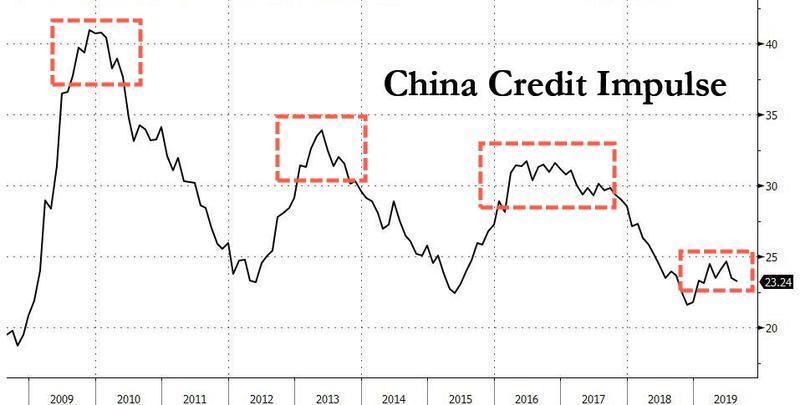

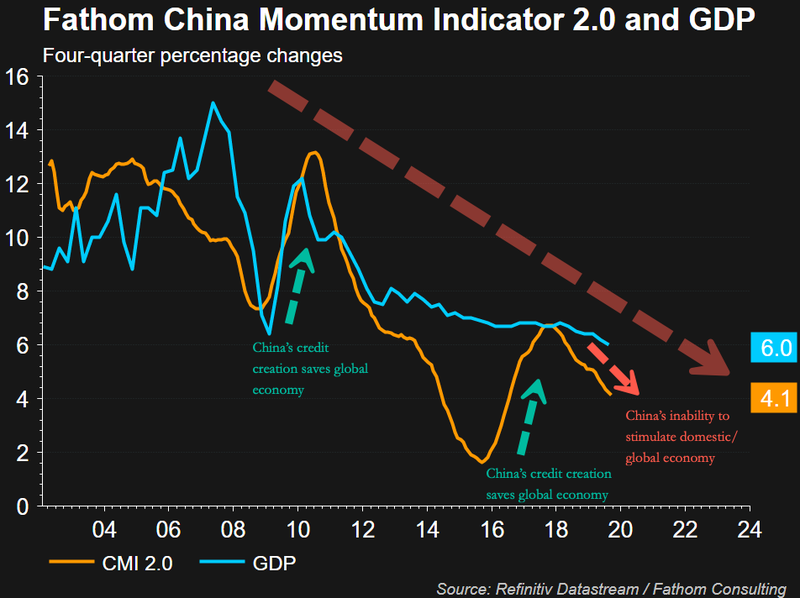

What this all means is that China’s economy isn’t going to save the world as it has done since 2008. China’s credit impulse has rolled over, the probabilities of a massive global economic rebound in the coming quarters are unlikely as China continues slow.

Fathom Consulting’s China Momentum Indicator 2.0 (CMI 2.0) provides a more in-depth view of China’s economic deceleration through alternative data as there’s no evidence at the moment that would suggest a trough in China’s economy.

China’s economy over the last decade has created 60% of all new global debt. This means with China’s economy in freefall, the PBOC powerless over downside, GDP will likely fall to the 5-handle in early 2020. More importantly, this means a global economic rebound of massive proportions is unlikely to happen early next year.

The major forecasters see an oil supply surplus next year, but those bearish outlooks largely depend on the health of U.S. shale growth in 2020, an assumption that is looking increasingly fanciful.

Financial struggles are well-known, but the dominoes continue to fall. As Bloomberg reported, some drillers have recently seen their credit lines reduced, limiting their access to fresh capital. Twice a year in the spring and fall, banks reassess their credit lines to shale drillers, and decide how much they will authorize companies to borrow. This time around is expected to be the first time in roughly three years that lenders tighten up lending capacities.

The curtailment in lending comes at a time when scrutiny on shale finances is increasing. Share prices have fallen sharply this year as investors lose interest. The industry continues to burn cash, and lenders and investors shunning the industry.

Of course, if drillers cannot borrow to cover their financing gaps, they may be forced into bankruptcy. The cutting of the borrowing base “can be a good precursor to potential bankruptcy because as capital markets stay closed off for these companies, the borrowing base serves as the only source of liquidity,” Billy Bailey, Saltstone Capital Management LLC portfolio manager, told Bloomberg.

Not every company is entirely cut off from capital markets. As Liam Denning points out, Diamondback Energy was able to issue $3 billion in new bonds at low interest rates, which highlights the case of “haves and have nots” within the industry.

But the financial stress helps explain the slowdown in U.S. oil production this year. The U.S. added about 2 million barrels per day (mb/d) between January 2018 and the end of last year; but output is only up a few hundred thousand barrels per day in 2019 from January through August.

Confusingly, the IEA still forecasts a substantial increase in U.S. oil production in 2020 at 1.2 mb/d, but not everyone agrees with that optimistic outlook. The credit crunch and financial stress in the shale sector could lead to a disappointment in 2020.

It is against this bewildering backdrop that OPEC+ must decide its next move. The IEA says that OPEC+ is in for some trouble as a supply glut looms – in large part because of shale growth. Others agree, to be sure. Commerzbank said that OPEC’s efforts to focus on laggards such as Iraq and Nigeria will be insufficient. “It is a mystery why OPEC should believe that it can avoid this oversupply by making just a few cosmetic adjustments,” the investment bank said. “By early next year at the latest OPEC thus risks being rudely awakened.”

However, at the same time, the physical market is showing some slightly bullish signs. In the oil futures market, front-month contracts for Brent are trading at a premium to longer-dated ones. The six-month premium rose to $3.50 per barrel recently, up from $1.90 last month, Reuters reports. A large premium is typically associated with a tighter market.

Moreover, there is a chance of a thaw in the U.S.-China trade war, which could provide some tailwinds to the global economy. It’s become impossible to trust the daily rumors coming from Washington and Beijing, but the two sides have shown some desire to at least call a truce and not step up the tariffs.

Still, the economy has slowed. The OECD warned that global GDP will decelerate to just 2.9 percent this year, and remain within a 2.9-3.0 percent range through 2021. This is the weakest rate of growth in a decade, and is down sharply from the 3.8 percent seen last year. “Two years of escalating conflict over tariffs, principally between the US and China, has hit trade, is undermining business investment and is putting jobs at risk,” the OECD said.

The U.S. and China, then, have a great deal of influence over the near-term prospects for oil. As mentioned, there is still a wide range of opinions on the magnitude of the oil supply surplus in 2020, but a breakthrough in the trade war would immediately shift growth projections, oil demand trajectories, and, importantly, sentiment. Even the mere expectation of an economic rebound would send oil prices rising, at least for a little while.

On the other hand, the thaw in the trade war is far from inevitable. The two sides have shown little evidence, if any, that they are actually making progress on some of the structural issues at hand. There is still the possibility that the talks fall apart and the trade war marches on, or even grows worse.

Because it is generally assumed that the oil market has already factored in some degree of optimism around tariff reduction, which has likely added a few dollars to the barrel of oil, a reassessment to the downside would surely send oil prices tumbling.

{kind=link}