Rouhani Willing To Meet With Trump This Week At UN, CNN’s Amanpour Says

Despite the United States vowing it would make its case against Iran at this week’s United Nations Assembly meeting in New York, especially regarding its alleged role in the Saudi Aramco attack, we could see an opening of direct dialogue between Tehran and Washington this week.

This after CNN’s Christiane Amanpour indicated Sunday that President Hassan Rouhani may be willing to meet with President Trump on the sidelines of the assembly. The prominent CNN news host revealed the information in a tweet based on a new interview she did with Iran’s foreign minister Javad Zarif.

Amanpour said, citing Iran FM Zarif’s words, that “President Rouhani is willing to meet with President Trump in New York this week ‘provided that President Trump is ready to do what’s necessary,’ exchanging sanctions relief for ‘permanent monitoring of Iranian nuclear facilities.’”

NEW: Iranian FM @JZarif tells me today that President Rouhani is willing to meet with President Trump in New York this week “provided that President Trump is ready to do what’s necessary,” exchanging sanctions relief for “permanent monitoring of Iranian nuclear facilities.” pic.twitter.com/oozihdsiVN

Amanpour further quoted Zarif as saying in a follow-up tweet:

“The olive branch has always been on the table, but we’re showing it again.”

Over the past month mixed signals have come out of the White House — at times Trump has gone so far as to float ‘no preconditions’ talks, but at others has lambasted “fake news” about face-to-face talks.

Rouhani is actually scheduled to meet with UK Prime Minister Boris Johnson on the sideline of the UN assembly on Tuesday, despite Johnson’s recent statements pointing the finger at Tehran for the Saudi Aramco attack, and his further indicating he’s not ruled out military action against Iran.

But there could be a rapid thawing of tensions given on Monday Iran announced it has freed the 2-month detained British-flagged Stena Impero, in what appears a good will gesture just ahead of the key meeting the PM Johnson.

Whether Rouhani and Trump actually meet could depend on developments in the meeting with PM Johnson, where the Iranian leader will likely be pressed over possible involvement in the Saudi Aramco attack.

Iran announced Monday the British-flagged tanker is “free to go”.

At the UN assembly itself the Iranians are expected to propose a new plan to deescalate regional tensions, which it has called the ‘Hormuz Peace Endeavor’ — and would involve a gulf countries only patrol of the Persian Gulf, presumably led by Iran itself.

Zarif told reporters while in New York that under the plan “all the coastal states of the Persian Gulf are invited to join this coalition to provide and maintain regional security.”

The Iranians are also expected this week to argue vehemently against the US-led “illegal and unjust” sanctions targeting the country. “The cruel actions that have been taken against the Iranian nation and also the difficult and complicated issues that our region faces with them need to be explained to the people and countries of the world,” Zarif said to reporters.

A couple of years ago, I wrote an article discussing the disconnect between the markets and the economy. At that time, the Fed was early into their rate hiking campaign. Talks of tax cuts from a newly elected President filled headlines, corporate earnings were growing, and there was a slew of fiscal stimulus from the Government to deal with the effects of 3-major hurricanes and 2-devastating wildfires. Now, the Fed is cutting rates, so it is time to revisit that analysis.

Previously, the consensus for the rise in capital markets was the tax cuts, and low levels of interest rates made stocks the only investment worth having.

Today, rates have risen, economic growth both domestically and globally has weakened, and corporate profitability has come under pressure. However, since the Fed is cutting rates, hinting at expanding their balance sheet, and a “trade deal” is at hand, stocks are the only investment worth having.

In other words, regardless of the economic or fundamental backdrop, “stocks are the only investment worth having.”

I am not so sure that is the case.

Let’s begin by putting the markets into perspective.

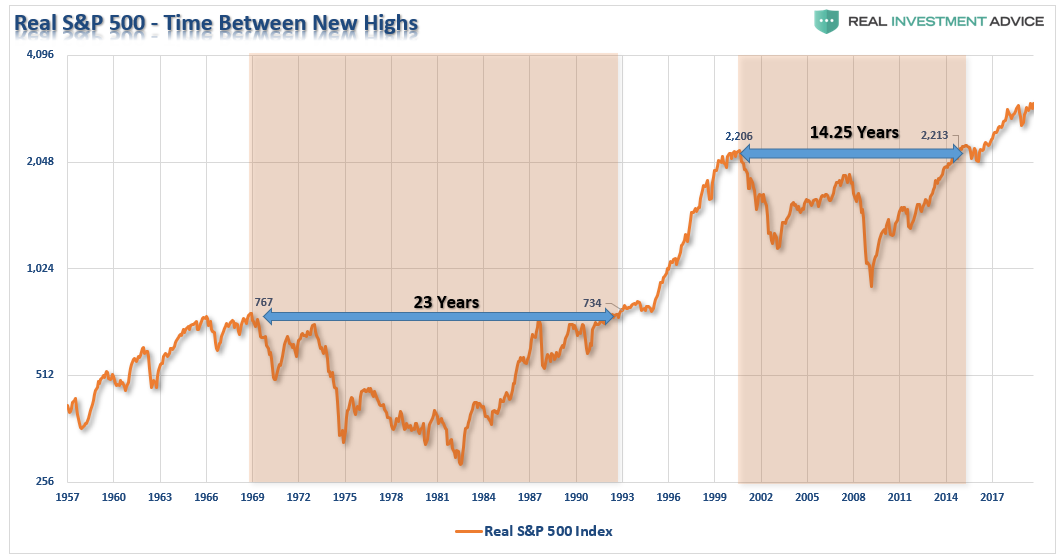

Yes, the markets are flirting with “all-time highs.” While this certainly sounds impressive, for many investors, they have just started making money on their investments from the turn of the century. As we noted in “The Moment You Know You Know, You Know,” what is often forgotten is the massive amount of “time” lost in growing capital to meet retirement goals.

“By the time that most individuals achieve a point in life where incomes and savings rates are great enough to invest excess cash flows, they generally do not have 30 years left to reach their goal. This is why losing 5-7 years of time getting back to “even” is not a viable investment strategy.

The chart below is the inflation-return of $1000 invested in 1995 with $100 added monthly. The blue line represents the impact of the investment using simple dollar-cost averaging. The red line represents a “lump sum” approach. The lump-sum approach utilizes a simple weekly moving average crossover as a signal to either dollar cost average into a portfolio OR moves to cash. The impact of NOT DESTROYING investment capital by buying into a declining market is significant.”

“Importantly, I am not advocating “market timing” by any means. What I am suggesting is that if you are going to invest into the financial markets, arguably the single most complicated game on the planet, then you need to have some measure to protect your investment capital from significant losses.

While the detrimental effect of a bear market can be eventually recovered, the time lost during that process can not. This is a point consistently missed by the ever bullish media parade chastising individuals for not having their money invested in the financial markets.”

However, let’s set aside that point for the moment, and discuss the validity of the argument of the rise of asset prices is simply a reflection of economic strength.

Assuming that individuals are “investing” in companies, versus speculating on price movement, then the investment process is a “bet” on future profitability of the company. Since, companies derive their revenue from consumption of their goods, products, and services; it is only logical that stock price appreciation, over the long-term, has roughly equated to economic growth. However, during shorter time-frames, asset prices are affected by investor psychology which leads to “boom and bust” cycles. This is the situation currently, which can be seenby the large disconnect between current economic growth and asset prices.

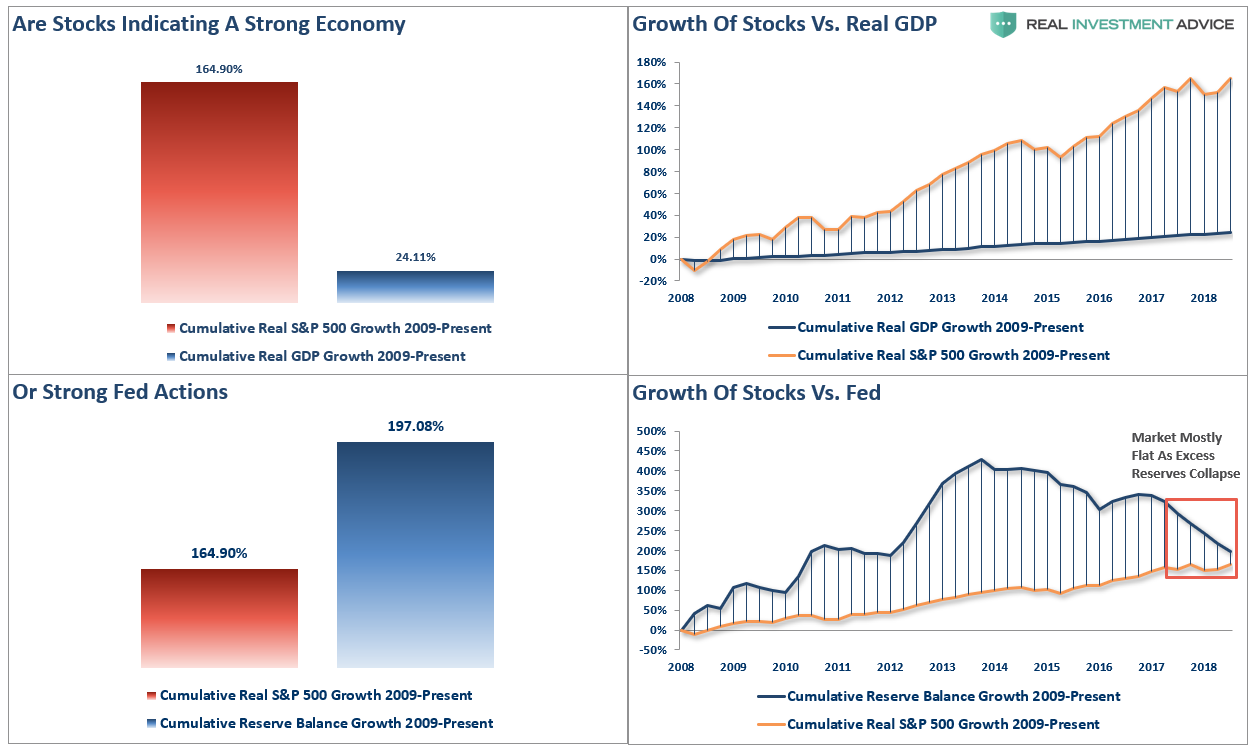

Since January 1st of 2009, through the end of the second quarter of 2019, the stock market has risen by an astounding 164.90% (inflation-adjusted). However, if we measure from the March 9, 2009 lows, the percentage gain explodes to more than 200%. With such a significant gain in the financial markets, we should see a commensurate indication of economic growth.

The reality is that after 3-massive Federal Reserve driven “Quantitative Easing” programs, a maturity extension program, bailouts of TARP, TGLP, TGLF, etc., HAMP, HARP, direct bailouts of Bear Stearns, AIG, GM, bank supports, etc., all of which total more than $33 Trillion, the economy grew by just $3.87 Trillion, or a whopping 24.11% since the beginning of 2009. The ROI equates to $8.53 of interventions for every $1 of economic growth.

Not a very good bargain.

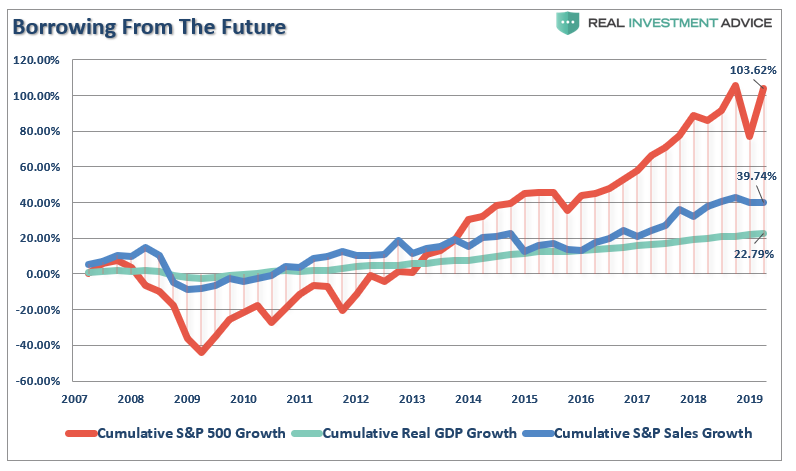

We can look at this another way.

The stock market has returned almost 103.6% since the 2007 peak, which is more than 4-times the growth in GDP and nearly 3-times the increase in corporate revenue. (I have used SALES growth in the chart below as it is what happens at the top line of income statements and is not AS subject to manipulation.)

The all-time highs in the stock market have been driven by the $4 trillion increase in the Fed’s balance sheet, hundreds of billions in stock buybacks, and valuation (PE) expansion. With Price-To-Sales ratios and median stock valuations near the highest in history, one should question the ability to continue borrowing from the future?

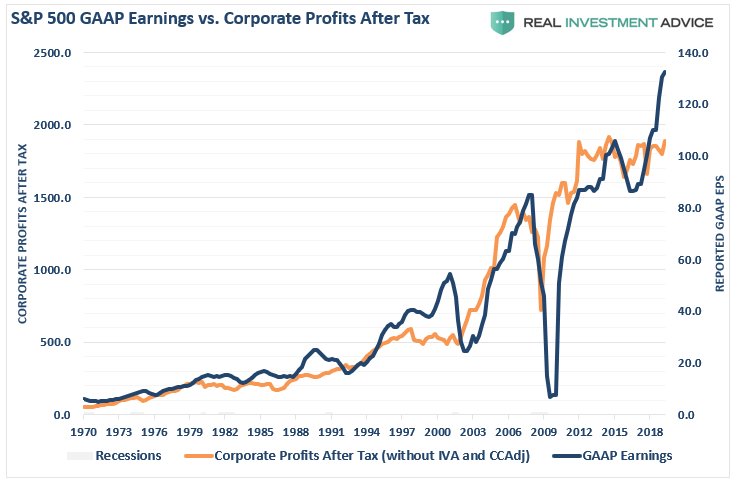

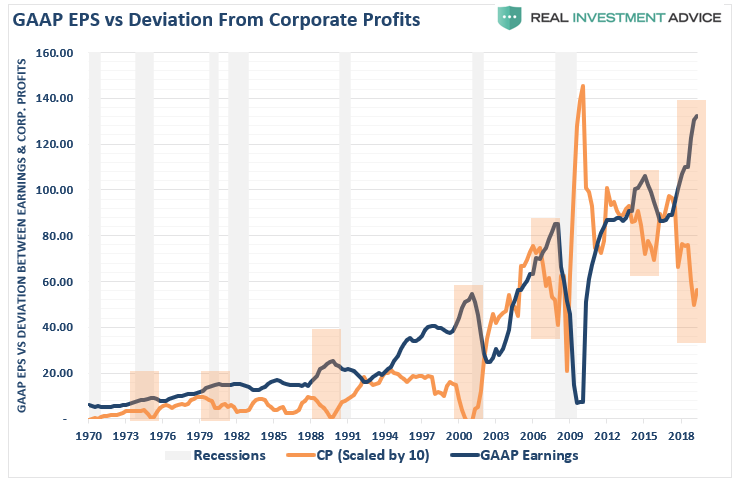

Speaking of rather extreme deviations, another concern for the detachment of the markets from more basic economic realities, the deviation of reported earnings from corporate profits after-tax, is at historical extremes.

These sharp deviations tend to occur in late market cycles when “excess” from speculation has reached extremes. Recessions tend to follow as a “reversion to the mean“ occurs.

While, earnings have surged since the end of the last recession, which has been touted as a definitive reason for higher stock prices, it is not all as it would seem.

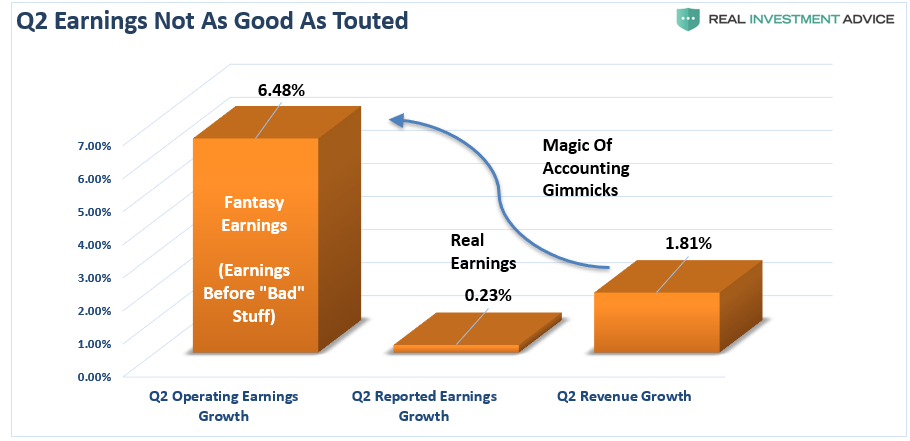

Earnings per share are indeed an important driver of markets over time. However, the increase in profitability has not come strong increases in revenue at the top of the income statement. The chart below shows the deviation between the widely touted OPERATING EARNINGS (earnings before all the “bad” stuff) versus REPORTED EARNINGS which is what all historical valuations are based. I have also included revenue growth, as well.

This is not a new anomaly, but one which has been a consistent “meme” since the end of the financial crisis. As the chart below shows, while earnings per share have risen by over 360% since the beginning of 2009; revenue growth has barely eclipsed 50%.

While suppressed wage growth, layoffs, cost-cutting, productivity increases, accounting gimmickry, and stock buybacks have been the primary factors in surging profitability, these actions have little effect on revenue growth. The problem for investors is all of the gimmicks to win the “beat the estimate game” are finite in nature. Eventually, real rates of revenue growth will matter. However, since suppressed wages and interest rates have cannibalized consumer incomes – there is nowhere left to generate further sales gains from in excess of population growth.

Left Behind

While Wall Street has significantly benefited from the Fed’s interventions, Main Street has not. Over the past few years, as asset prices surged higher, there has been very little translation into actual economic prosperity for a large majority of Americans. This is reflective of weak wage, economic, and inflationary growth which has led to a surge in consumer debt to record levels.

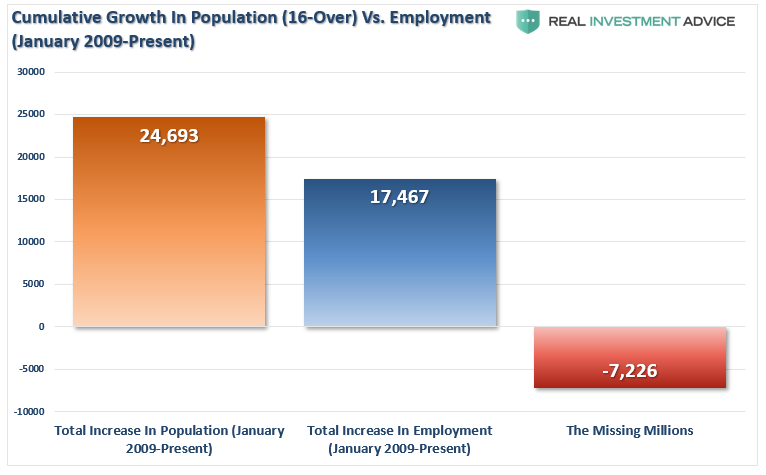

Of course, weak economic growth has led to employment growth that is primarily a function of population growth. As I addressed just recently:

“Employment should increase to accommodate for the increased demand from more participants in the economy. Either that or companies resort to automation, off-shoring, etc. to increase rates of production without increases in labor costs. The chart below shows the total increase in employment versus the growth of the working-age population.”

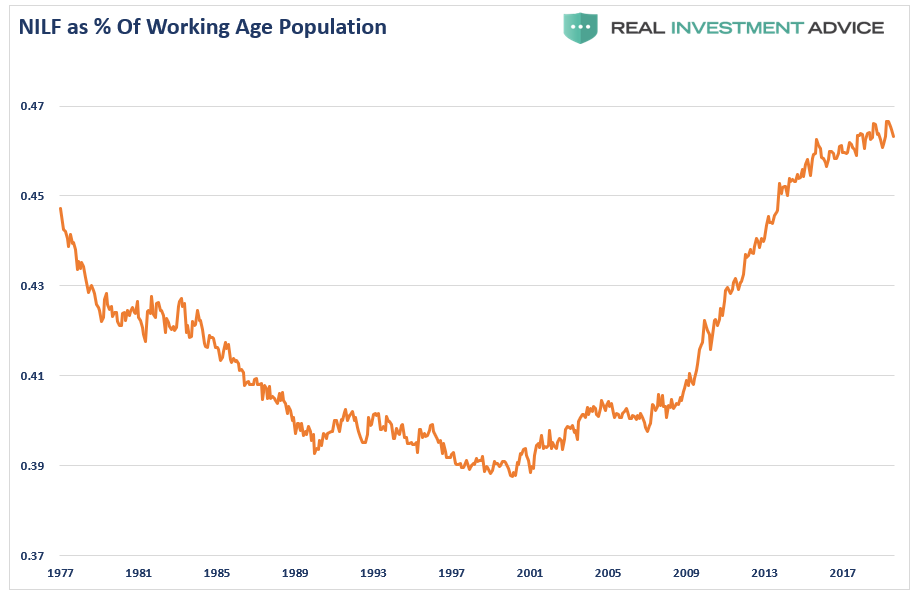

While reported unemployment is hitting historically low levels, there is a swelling mass of uncounted individuals that have either given up looking for work or are working multiple part-time jobs. This can be seen below which shows those “not in labor force,” as a percent of the working-age population, skyrocketing.

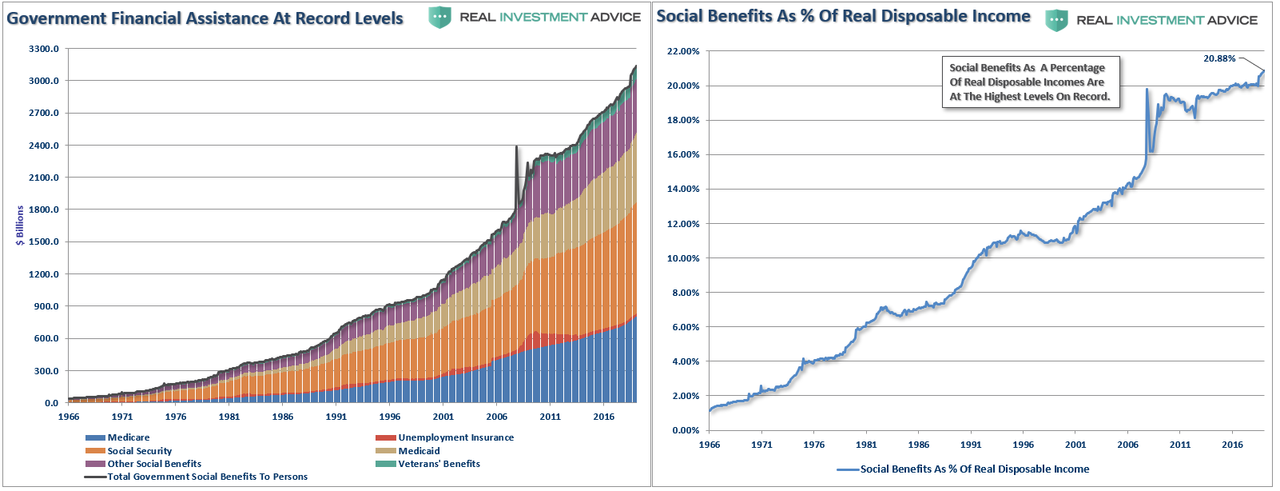

If employment was indeed as strong as reported by government agencies, then social benefits would not be comprising a record high of 22% of real disposable incomes.

Without government largesse, many individuals would literally be living on the street. The chart above shows all the government “welfare” programs and current levels to date. While unemployment insurance has hit record lows following the financial crisis, social security, Medicaid, Veterans’ benefits and other social benefits have continued to rise and have surged sharply over the last few months.

With 1/5 of incomes dependent on government transfers, it is not surprising that the economy continues to struggle as recycled tax dollars used for consumption purposes have virtually no impact on the overall economy.

Conclusion

While financial markets have surged to “all-time highs,” the majority of Americans who have little, or no, vested interest in the financial markets have a markedly different view. While the Fed keeps promising with each passing year the economy will come roaring back to life, the reality has been that all the stimulus and financial support hasn’t been able to put the broken financial transmission system back together again.

Amazingly, more than two-years following the initial writing of this article, the gap between the markets and the economy has grown even wider. Eventually, the current disconnect between the economy and the markets will merge.

I bet such a convergence will likely not be a pleasant one.

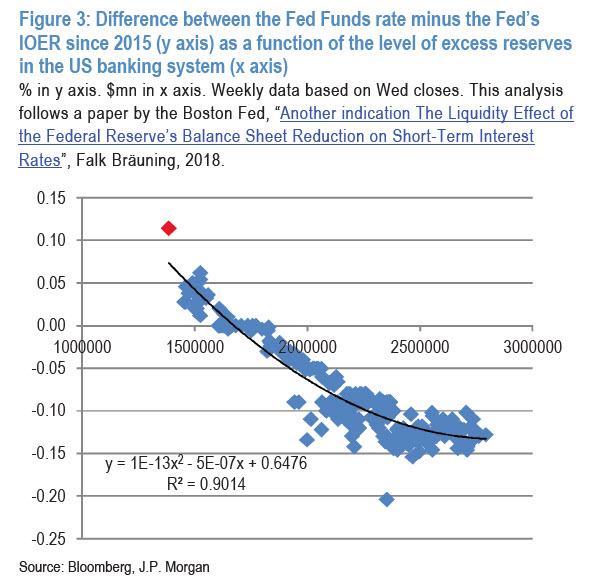

Dollar Shortage Eases But Banks Still Signal $66 Billion Funding Shortfall In Fed Repo Operation

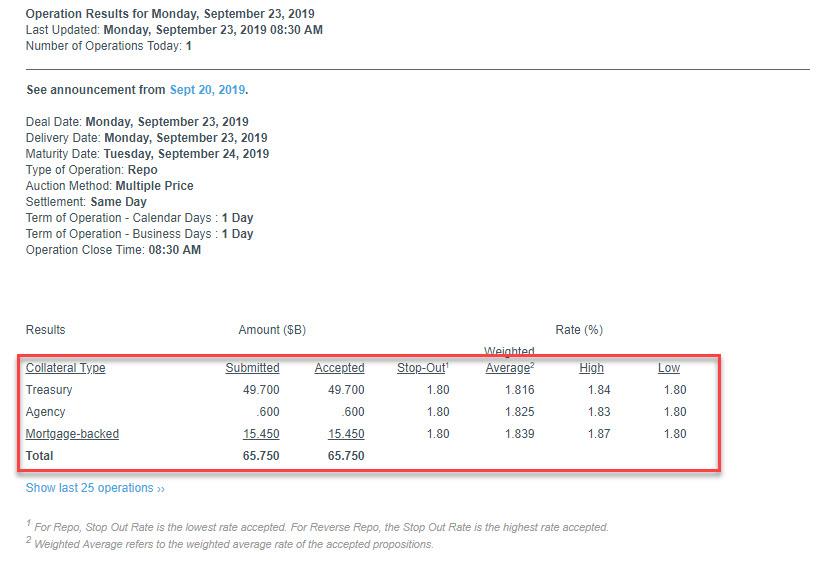

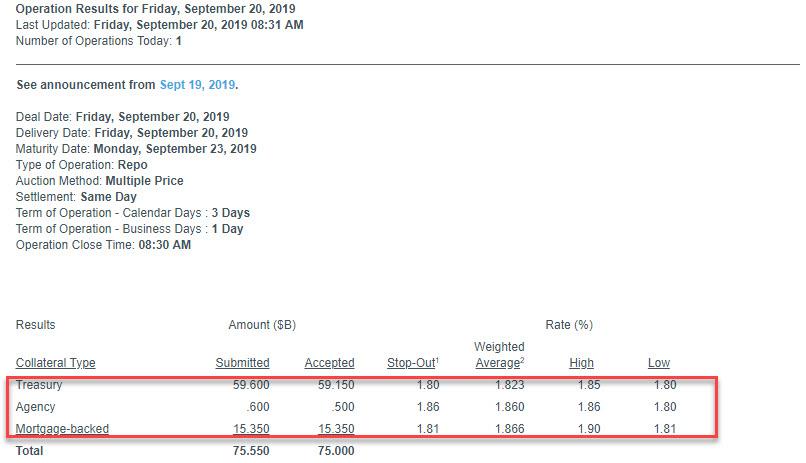

After announcing a barrage of emergency liquidity operations announced by the Fed late on Friday, including daily overnight repo ops, as well as three $30BN term repos to provide funding across quarter end – traditionally a time funding shortages – and into Q4, this morning’s $75BN repo operation showed clear signs of stabilization in the overnight funding market, when “only” $65.75 billion in collateral was accepted by the Fed in exchange for reserves, marking the first non-oversubscribed repo operation since Wednesday.

Specifically, the NY Fed announced that it had accepted $49.7BN in Treasurys, $0.6BN in Agency paper and $15.45BN in MBS all at the 1.80% IOER stop out rate (with the rate however rising as high as 1.84% on TSYs and 1.87% on MBS).

This was just under $10 billion less than Friday’s repo op, driven by a $10 billion drop in Treasury collateral parked at the Fed.

Still, what is worrisome is that almost a week after the widely cited catalyst of tax payments, and with the Treasury’s general account at the Fed already having been boosted to over $300 billion, the liquidity shortage persists even though numerous “experts” said this temporary phenomenon would faded entering this week. This, in turn, suggests that the troubles in the repo market are indeed a function of reserve scarcity, a topic we discussed extensively last night when we suggested that the Fed will need to inject about $400 billion in reserves, pushing the total up to $1.8 trillion, to normalize the Fed Funds -IOER spread.

And while there was no term repo operation scheduled today, one is coming tomorrow, which may indicate that the funding shortage will get worse as dealer will likely anticipate a shortfall of funding exiting the quarter.

Commenting on the ongoing turmoil in the repo market, Citi strategist Steve Kand said in a Friday note that while the Federal Reserve’s open market operations may help to alleviate funding market stress in the near-term, the plan is an “imperfect one” to shield against a rise in repo rates at quarter-end. Similar to our calculations, Citi estimated the in total the repo market needs roughly $200BN to reduce GC volatility over quarter-end and offset the effects of a decline in reserves, Treasury auction settlements and quarter- end netting, reminding that these same three issues were in play in December 2018, when GC rose above 5%.

Looking ahead, Citi expects reserves to decline by around $100BN on Sept. 30, as Treasury’s cash balance will increase by $50b, the Fed’s RRP facility tends to increase by around $40b, and foreign RRP balances have been rising, with Citi estimating another $10b increase. Meanwhile, on Sept 30, the gross Treasury supply is expected to be $113bn.

In short, the quarter-end rate will likely climb, as DTCC GC repo demand rises in lieu of tri-party, given the increase in netting needs.

Finally, Citi joined the bandwagon consensus spearheaded by Bank of America, Nomura, JPMorgan, Goldman and, last but not least, Simon Potter, in concluding that the Fed is likely to transition to permanent open market operations after the October FOMC, which depending on one’s semantic disposition may or may not be defined as QE4; until then, the central bank will experiment with “flexible OMOs” to get a better sense of the amount of “necessary intervention.”

Iran Frees UK-Flagged Stena Impero A Day Before Crucial UN Summit

Iran has indicated it has freed the British-flagged oil tanker Stena Impero on Monday upon the announcement by officials in Tehran that the ship is “free to leave” — though it’s reportedly yet to move out of Iranian waters.

This brings to an end the two-month standoff since the vessel had been captured by the IRGC in the Strait of Hormuz, in what was seen as an immediate retaliatory move responding to the prior July 4 seizure of Iran’s Grace 1, since renamed Adrian Darya 1, off Gibraltar by UK Royal Marines.

British-flagged Stena Impero, via Reuters

Semi-official Fars News Agency said the legal process surrounding the ship’s capture had been concluded, though from the beginning British and Indian negotiators have been involved pressing for its release (given many of the crew were Indian citizens).

However, it’s still unclear as to when the newly freed tanker will commence its voyage out of Iran’s waters.

The ship’s owner, the company Stena Bulk, confirmed Monday the Stena Impero is still in the Persian Gulf port of Bandar Abbas where it’s been for the past two months.

It appears a good will gesture meant to thaw tensions most immediately with the UK, and also the US, given Iranian President Hassan Rouhani is set to meet with UK Prime Minister Boris Johnson on Tuesday on the sidelines of the UN General Assembly in New York.

IRGC forces previously filmed themselves fast roping down to the ship from a helicopter, and subsequently inspecting it.

The crucial UN summit is expected to deal heavily with the recent aerial attacks on Aramco facilities, which knocked out up to half of the kingdom’s daily oil output in the days following the attack.

This even after on Sunday Johnson publicly blamed Iran for overseeing the Sept. 14 attacks on Saudi Aramco facilities.

“‘We think it very likely indeed that Iran was responsible,” said the PM on his way to New York. He agreed with Washington that western allies should “do more to defend Saudi”.

“We will be following that very closely and clearly, if we are asked, either by the Saudis or by the Americans, to have a role, then we will consider in what way we could be useful,” he told reporters, signaling the likelihood that the UK’s military would join any potential US strikes against Iran should the green light be given.

French Officials Doubt Macron Will Hit Goal Of Rebuilding Notre Dame In 5 Years

French President Emmanuel Macron was never more popular than the day that a massive blaze erupted on the roof of the Cathedral of Notre Dame, the most popular tourist attraction in France, and an icon of Catholicism, and of French culture.

Seizing the opportunity to be a “leader,” Macron delivered a fiery speech about the importance of Notre Dame to the spirit of the French people, and vowed to finish restoring the burned-out cathedral as soon as possible.

Caught up in the passion of the moment, Macron delivered what he asserted was an unshakeable vow: He would rebuild Notre Dame in 5 years.

Now, roughly six months in, some French officials are questioning the feasibility of that time frame, according to FT.

The latest to doubt Macron’s 5 year timeline is French culture minister Franck Riester, who said in an interview over the weekend that there had been ‘complications’ at the site during emergency repairs that might delay the project. He hopes now that the cathedral can open to the public within 5 years while restoration continues.

“The most important thing is the quality of the restoration and of the project,” he told the newspaper Le Parisien. “It must be done in a reasonable time.”

He added that “we’re not focused on a timetable.”

“We’re not focused on a timetable.Our aim is five years, but there’s no countdown. The president never asks me when the work will begin. I’m not being put under pressure and there is no obsession.”

Even as some experts warned that it could take decades to finish restoring Notre Dame, Macron declared during his first live television address after the fire: “We Will rebuild the cathedral of Notre-Dame and make it even more beautiful than before and I want this to be completed within five years…we can do it, and we will mobilize to do it.”

Even the architect in charge of the restoration now doubts Macron’s timeline, agreeing instead with Riester, who said that five years might be enough time to reopen the cathedral to the public, but completing the project will likely take even longer.

Philippe Villeneuve, the architect in charge of the restoration, has been more cautious. He said: “In five years, we can rebuild the vaults and the roof, and reopen the church to both worshippers and public. But not much more.”

But not everyone sees the five-year target as impossible.

Not everyone regards the five-target as impossible, however. André Finot, the cathedral’s communications director who once attended services as an altar-boy and was at the building on the night of the fire, said: “It can be done in five years. That’s my point of view.”

“I’m here and I see how the works are going fantastically well. In the first three months workers were here seven days a week, 24 hours a day.”

Still, after passing a law in July limiting the new materials and techniques that can be used during reconstruction, many suspect that management of the restoration is slipping from a presidential priority to something that will be governed by the innerworkings of the French bureaucracy.

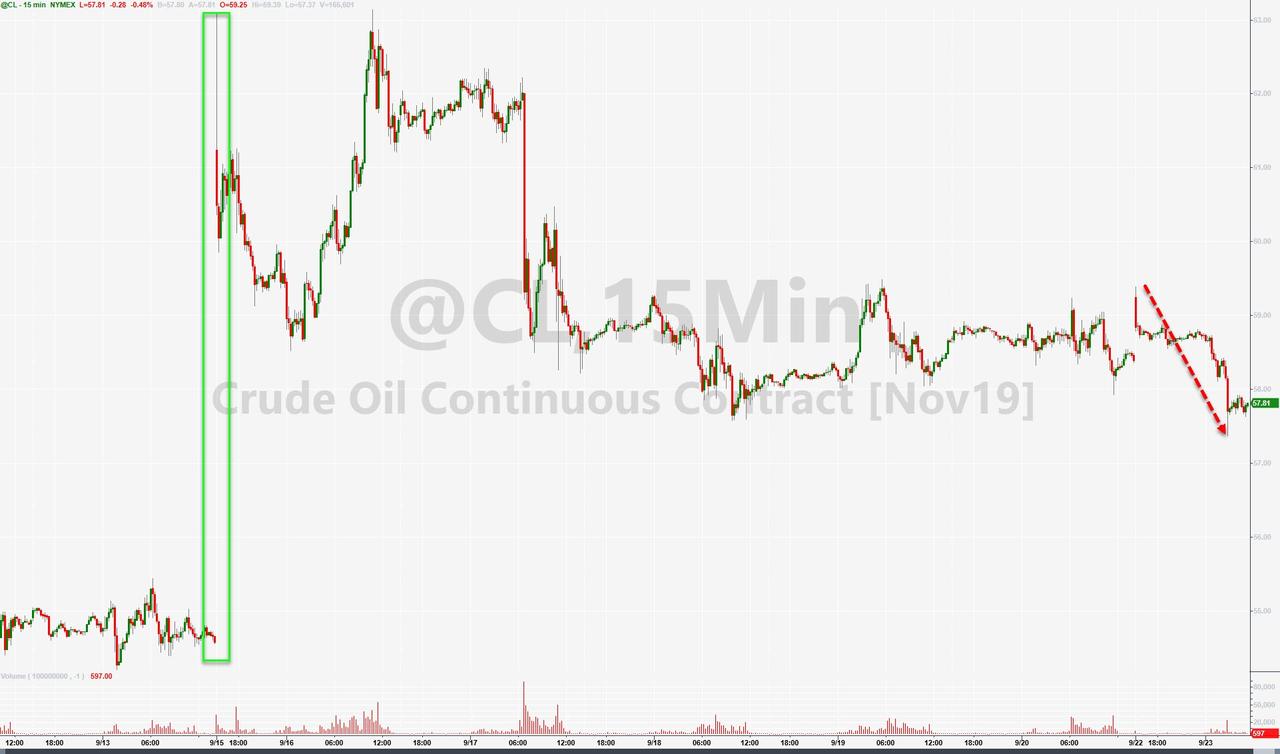

Oil Pumps, Then Dumps After Conflicting Reports Over Saudi Recovery

Crude futures gapped dramatically higher at the open overnight, WTI back above $59, after WSJ headlines over the weekend that Saudi Arabia’s recovery could take “eight months” rather than weeks.

But, prices are tumbling this morning following Reuters reports denying this ‘news’, claiming that Aramco will succeed in restoring its lost production by the end of this month.

However, in context, prices are still significantly higher than before the refinery attack.

Additionally, this morning’s dismal German PMIs did not help matters on the global demand side.

“It’s tug of war between weak demand fundamentals and heightened geopolitical risks,” said Jens Naervig Pedersen, a senior analyst at Danske Bank A/S in Copenhagen.

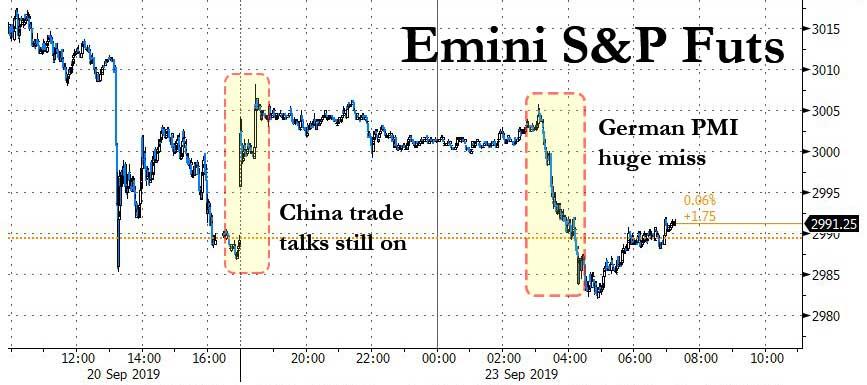

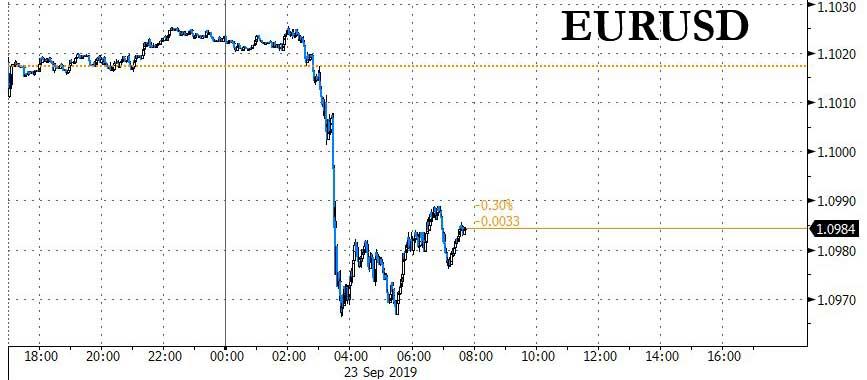

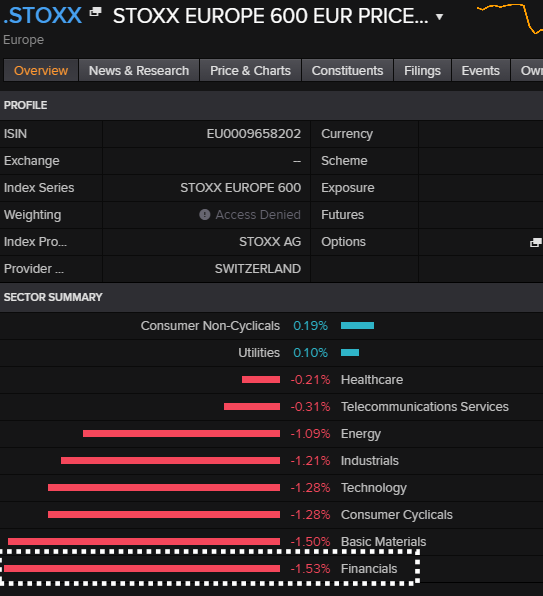

US Futures, Global Markets Slide As Europe Careens Into A Recession

The overnight trading session has been a tale of two halves, with the start of the session marked by sharply higher futures, following this weekend’s news that China’s canceled trip to Montana and Nebraska was made at the request of the US, and not as traders first assumed, by a negative turn in the lower-level discussions held in Washington last week. However, the early optimism quickly crashed after Germany reported the latest PMI data, which missed across the board, printing at 7 year lows, and was – in the words of Phil Smith, Principal Economist at IHS Markit, “simply awful.” (And it’s not just Germany: French PMIs were ugly too, missing across the board).

The result was an instant shift in risk sentiment, as not only is the German manufacturing recession getting worse, but the Services PMI also dropped, dragging the composite below 50 for the first time in seven years…

… slamming US equity futures, which hit session lows shortly after the German print…

… sending most global markets promptly into the red.

… and slamming the EURUSD back under 1.10

The Stoxx Europe 600 Index extended losses and European bonds rallied. Monday’s abrupt sentiment reversal followed the worst session for US equity indexes in about two weeks on Friday – ending a three-week run of gains – after a Chinese agriculture delegation canceled a visit to Montana, dampening optimism about the trade talks. Stock markets had been buoyed earlier in the week by the Federal Reserve’s decision to cut interest rates for the second time in 2019, joining other central banks around the world in easing monetary policy.

The gloomy European data was a stark reminder to investors of the fragility of the global economy. While markets remain on edge ahead of next month’s planned high-level trade talks between the U.S. and China, they’re also fixated on any action or messaging from the world’s major central banks that could support growth. A slew of policy makers will speak this week.

“Global growth risks are rising,” Beverley Morris, director of rates and inflation at QIC Ltd. in Brisbane, told Bloomberg TV. “It’s certainly not panic stations at this stage, but certainly in terms of our portfolio actions, we are being more cautious.”

Asian stocks edged lower, led by technology firms, as investors gauged South Korea’s export slump as well as the twists and turns of China-U.S. trade talks, with Tokyo shut for a holiday. Markets in the region were mixed, with India jumping and China retreating. The Shanghai Composite Index dropped 1%, dragged by large banks and insurers. China’s cancellation of a planned visit to farms in the American heartland was done at the request of the U.S., people familiar with the matter said. Equities in India continued a surge, with the Sensex surging as much as 3.8%, set for its biggest two-day rally in 10 years, amid optimism that the government’s $20 billion company tax cut will revive growth. HDFC Bank and ICICI Bank were among the biggest boosts. The Kospi closed little changed, as South Korean exports headed for a 10th monthly slide amid flagging chip sales

In FX, the Bloomberg Dollar index climbed then pared gains as the U.S. and China continued to engage in discussions to overcome trade differences. The euro fell sharply and global bonds rallied after German manufacturing suffered its worst downturn since the financial crisis. Sterling slipped as U.K. Prime Minister Boris Johnson cautioned against the chances of a Brexit breakthrough when he meets with key European leaders in New York. The onshore yuan fell amid caution in the run-up to next week’s national holidays. The Korean won sank as exports continued to deteriorate.

In rates, U.S. Treasuries advanced for a sixth day with the 10-year yield sliding to its lowest since Sept. 12, dropping to 1.68%.

Oil fluctuated following a report that full repairs to Saudi facilities hit by a drone attack may take many months. Brent fell below $64 a barrel on Monday, reversing an earlier gain, pressured by the prospect of a faster-than-expected full restart of Saudi Arabian oil output and by fresh signs of European economic weakness. It was up earlier in the session, supported by scepticism over how fast output would come back.

“Oil prices are tracking European markets lower this morning, understandably knocked by the woeful manufacturing data from the bloc and the implications for global growth and demand,” said Craig Erlam, analyst at OANDA. Brent has still gained about 18% this year, helped by a supply-limiting pact led by the Organization of the Petroleum Exporting Countries, although concern about slowing economic growth has limited the advance.

Expected economic releases include PMIs. Cantel Medical is reporting earnings. Also on the radar is a speech by Federal Reserve Bank of New York President John Williams at the 2019 U.S. Treasury Market Conference at 9:50 a.m. ET.

Market Snapshot

S&P 500 futures down 0.2% to 2,983.00

MXAP down 0.06% to 159.29

MXAPJ down 0.3% to 509.64

Nikkei up 0.2% to 22,079.09

Topix up 0.04% to 1,616.23

Hang Seng Index down 0.8% to 26,222.40

Shanghai Composite down 1% to 2,977.08

Sensex up 3.1% to 39,197.38

Australia S&P/ASX 200 up 0.3% to 6,749.72

Kospi up 0.01% to 2,091.70

STOXX Europe 600 down 1% to 388.85

German 10Y yield fell 5.9 bps to -0.58%

Euro down 0.3% to $1.0980

Italian 10Y yield rose 3.7 bps to 0.582%

Spanish 10Y yield fell 7.3 bps to 0.163%

Brent futures up 0.4% to $64.51/bbl

Gold spot up 0.2% to $1,519.44

U.S. Dollar Index up 0.2% to 98.74

Top Headline News from Bloomberg

Germany’s private sector is suffering its worst downturn in almost seven years as a manufacturing slump deepens, raising pressure on the government to add fiscal stimulus; a Purchasing Manager’s Index fell to 49.1 in September from 51.7 a month earlier, according to IHS Markit; the reading was worse than economists predicted and the lowest since October 2012

China’s cancellation of a planned visit to farms in America was done at the request of the U.S., people familiar with the matter said, indicating it wasn’t caused by a negative turn in the lower- level discussions held in Washington last week; trade groups from the two nations held “constructive” talks during Sept. 19-20, China’s Ministry of Commerce said Saturday

Thomas Cook Group Plc collapsed under a pile of debt after talks with creditors failed, forcing the British government to charter planes to bring home more than 150,000 of the storied travel provider’s stranded customers; trading in Thomas Cook’s stock was suspended in London and its euro bonds plunged 72%

Deutsche Bank AG completed a deal with BNP Paribas SA to transfer its prime brokerage business to the French bank as part of the German lender’s biggest overhaul in recent history

U.K.’s Johnson will start a week of intense diplomacy on Monday, as he tries to push for a Brexit deal on the sidelines of the United Nations General Assembly in New York

Asian equity markets were mixed following the negative close last Friday on Wall St. amid temperamental US-China trade headlines, while the absence of Japanese markets also contributed to the lacklustre tone. ASX 200 (+0.3%) was positive with the index led higher by the commodity related stocks after gold advanced above the USD 1500/oz level and with oil underpinned by reports it could take 8 months for Saudi output to return to normal, while India’s NIFTY (+2.9%) outperformed again after the recent corporate tax cut announcement. Conversely, weakness in Hang Seng (-0.8%) and Shanghai Comp. (-0.8%) dampened sentiment in the region with underperformance in the mainland as ongoing trade uncertainty overshadowed the liquidity efforts by the PBoC. This followed conflicting reports in which US President Trump stated Chinese agricultural purchases will not be enough and reiterated that he does not need a deal before the 2020 election although it was also reported the US granted temporary tariff exemptions on over 400 types of Chinese products, while China’s delegation cancelled its US farm visit but this was later attributed to concerns it could turn into a media circus or may be misconceived as meddling and was not due to a breakdown in trade talks

Top Asian News

Bond Traders in India Caught Out by Surprise Fiscal Flip Flop

Israel Arabs Back Bid by Netanyahu’s Rival to Unseat Premier

Major European bourses are lower (Euro Stoxx 50 -1.0%), after disappointing PMI data stoked further concerns about the slowdown in Eurozone growth. The DAX (-1.2%) is the notable underperformer, slipping briefly below last week’s low and recent support at 12300, after German manufacturing PMI data pointed to the sector falling further into contractionary territory. Amid the risk off sentiment, utilities (+0.1%), consumer staples (+0.2%) and health care (unch.) sectors are supported, while materials (-1.6%), financials (-1.7%) and tech (-1.4%) are softer. Bucking the general risk tone are European airlines, including TUI (+7.5%), Ryanair (+1.1%) and easyJet (+3.5%), who are higher after rival Thomas Cook ceased trading activities and filed for bankruptcy. In terms of individual movers; William Hill (-4.0%) reversed early gains, despite premarket news that the Co. is looking for US broadcaster deals in an attempt to promote its brand. Elsewhere, K+S (-5.7%) sunk after being downgraded at Pareto Securities. Ocado (+0.2%) managed to reverse losses on triggered by news that the Co’s Chairman stated they “will go to any length” to protect their intellectual property, amid a court battle with a co-founder. Finally, ABN AMRO (-3.5%) is under pressure after being downgraded at Santander.

Top European News

Germany May See No Growth This Year as Manufacturing Slumps

Euro- Area Economy Comes Close to Stalling as Factories Suffer

Vonovia Becomes Sweden’s Biggest Landlord With $1.3 Billion Deal

Has Poland’s Government Become a Threat to Business?

In FX, further concerns about the European economy have weighed on the Euro in early trade as the latest flash PMIs out of the region deteriorated significantly vs. expectations. Germany’s release took EUR/USD below the 1.100 level with IHS noting that on its current trajectory, Germany may not see any growth before year-end, whilst VDMA added further pessimism to the German economic outlook. Further, the EZ release did little to immediately sway asset classes as participants anticipated a softer pan-release, but IHS highlighted that Q3 EZ GDP growth looks set to rise just 0.1%. Analysts at CapEco highlighted concerns regarding manufacturing contagion on the services sector whilst noting that a continuation in the employment component could lead to further easing in wages. Thus, the analysts believe that “there is little reason to think that GDP growth will pick up as the ECB and the consensus forecasts assume”. EUR/USD took out Friday’s low and a Fib level around 1.0995-97 to print a base at 1.0967 ahead of support at 1.0966 and 1.0950 (YTD low at 1.0924). Next up, participants will be eyeing ECB President Draghi’s final testimony to the European Parliament at 1400BST. Meanwhile, the Buck has derived support in light of a weaker Single Currency as DXY extends its gains above 98.50 to a high of 98.84 and ahead of the psychological 99.00 and resistance at 99.10. On the docket State-side, traders will be on the lookout for a few Fed speaks including Williams (voter, neutral) at the US Treasury Market Conference at 1450BST, Bullard (voter, dove, dissenter) on monetary policy at 1800BST and Daly (non-voter, neutral) on supporting US economy in urban & rural communities.

GBP, CAD – Weaker on the day, albeit more on the back of a firmer USD with Brexit-watchers still on the lookout for the Supreme Court’s decision on PM Johnson’s parliament prorogation. If ruled against (as legal experts expect), then the PM could be forced to recall MPs back to parliament. Cable remains marginally softer below the 1.2450 level (vs. high of 1.2490) after finding a base at 1.2424, which marks the lowest since 17th September (although that day saw a low of 1.2393). The Loonie also takes a spot as a G10 laggard, but mostly pressured by a retreat in oil prices as the post-PMI sentiment seeped into the energy complex. USD/CAD hovers around the 1.3300 handle (vs. low of 1.3257) with resistance seen to the upside at 1.3305 (200 DMA), 1.3346 and the psychological 1.3350 levels.

CHF, JPY – Marginally firmer amid a weakening EUR and flights to safety post-EZ PMI with USD/JPY back below the 107.50 level to a low of 107.30 ahead of support at 107.10, whilst EUR/CHF trades flat on the day but fell from an intra-day high of 1.0930 (50 DMA) to a base just above 1.0850 (with support and YTD low at 1.0809). Attention remains on the 1.08 level amid the recent rise in SNB total sights deposits with TD noting that the data suggests the SNB may be defending the level.

AUD, NZD – The antipodeans remain above water with the Kiwi outperforming its Tasman-peer ahead of this week’s RBNZ Monetary Policy Decision amid consensus for an unchanged Cash Rate at 1.00%, following its unexpected rate cut at its prior meeting, whilst the Shadow Board also recommends no change in policy. The currencies seem to have also derived some support from the US-China trade saga with Chinese state media noting that talks are constructive, and that the cancelled China visit to US farms was not a sign of deteriorating talks. NZD/USD hovers near intra-day highs (0.6277) after finding a base at 0.6250 whilst its Aussie counterpart remains above 0.6750, albeit off highs (0.6780).

In commodities, oil prices continued to come off its earlier highs, as focus shifted from the prospect of a more protracted disruption to Saudi Aramco supply than expected (which helped prices over the weekend) to concern over global growth, after more abysmal Eurozone PMI data triggered a bout of selling in the complex. Downside was exacerbated soon thereafter on source reports that Saudi Arabia’s Khuraris and Abqaiaq facilities are to fully restore oil production early next week (form current production levels of around 4.3mln BPD), contrary to WSJ reports over the weekend that repairs could take up to 8 months. WTI Nov’ 19 futures slumped through last week’s lows around the USD 58/bbl handle, before finding a base at USD 57.40/bbl, while Brent Nov’ 19 fell below the USD 64/bbl handle, although last week’s USD 63.06 low is still some way off. Gold prices are higher, despite opening on the back foot (on weekend reports that Chinese agriculture officials didn’t end their US trip early due to trade talk difficulties) and a firmer buck, with negative risk sentiment exacerbated by the aforementioned Eurozone PMIs helping to lift the precious metal; spot gold continues to climb from its recent USD 1500/oz base. On the flip side, global demand concerns are keeping copper prices under pressure.

US Event Calendar

8:30am: Chicago Fed Nat Activity Index, est. 0, prior -0.4

9:45am: Markit US Manufacturing PMI, est. 50.4, prior 50.3

9:45am: Markit US Services PMI, est. 51.5, prior 50.7;

9:45am: Markit US Composite PMI, prior 50.7

DB’s Jim Reid concludes the overnight wrap

As astronomical autumn arrives today in the Northern hemisphere its apt that I got my wellies out yesterday for the first time in a few months after a fair bit of rain. Winter is coming. Also on ordering groceries online last night I got a bit of a shock as they have now started to sell mince pies in time for Xmas. Only 92 days left and just under 8 million seconds. It’ll be here before you know it.

After the central bank frenzy of the last 10 days, the next few days should be somewhat lighter for news flow for markets. Data highlights include the preliminary global September PMIs (today), the German IFO (tomorrow), and the US Conference Board’s consumer confidence reading (tomorrow) and UoM equivalent (Friday) with the spread between the two of notable interest as it has been a lead indicator of the cycle in the past (see below). From central banks, we have ECB President Draghi’s final “Monetary Dialogue” before the European Parliament’s Economic and Monetary Affairs Committee (today), along with a number of other key speakers, especially from the Fed. Finally, we should hear the outcome of the UK Supreme Court Case on the prorogation of Parliament, while world leaders will be gathering at the UN General Assembly.

In a little more detail now, the key data highlight this week will be the preliminary September PMIs today (Japan tomorrow due to a holiday) with the big question continuing to be how and when the divergence between manufacturing and services will end. As an example the Euro manufacturing PMI has been in contractionary territory since February, while the services PMI has shown consistent growth over that period. The consensus expectation is for this divergence to narrow modestly, with the manufacturing Euro PMI rising three-tenths to 47.3, with the services PMI falling two-tenths to 53.3. The German manufacturing PMI will be of particular interest, which last month was at 43.5, and has been below 50 for the entire year so far.

Speaking of Germany, another key highlight will be the Ifo business climate survey tomorrow. In August, the indicator fell to 94.3, its lowest level since November 2012, while the expectations reading fell to 91.3, the lowest since June 2009. Nevertheless, the consensus expectation is for a rebound in both this month, with the business climate indicator expected to rise to 94.6.

With respect to US economic data, Tuesday’s consumer confidence report (132.0 forecast vs. 135.1 previously) and Friday’s University of Michigan consumer sentiment survey (92.0 final vs. 92.0 preliminary) will provide further information on the consumer outlook. As our economists have pointed out, as of August, the spread between the level of the two surveys was at an all-time high, which as their recent research has highlighted, may be sending a concerning signal even though on the surface the levels of both series remain elevated (see ” Yield curve inversion signals recession…(consumer) surveys say? ” ).

Another one to also watch out for is the third estimate of Q2 US GDP, although expectations are for the annualised rate to remain unchanged from the second estimate, at +2.0%. Meanwhile on Friday we’ll also see personal income and personal spending data for August, along with the preliminary durable goods orders reading.

There are a number of central bank speakers this week kicking off today with ECB President Draghi appearing before the European Parliament’s Economic and Monetary Affairs Committee, in his last “Monetary Dialogue” before his eight-year term ends on 31 October Other speakers this week include Bank of Japan Governor Kuroda and Federal Reserve Vice-Chairs Quarles and Clarida, while the Bank of Mexico will be making its latest policy decision. Within the Fed Bullard (voter/dove – wanted 50bps last week) and Daly (nonvoter/dove) will also be making appearances later on today, and Chicago’s Evans (voter/dove) will follow on Wednesday.

Turning to politics, the UK Supreme Court is expected to rule on the case over the prorogation of Parliament early this week according to the Supreme Court President. An update on timing is likely today. It’s also the Labour Party Conference, which is taking place currently until Wednesday, ahead of the Conservative Party Conference the subsequent week. The Labour Party are still fighting over a coherent Brexit strategy which further complicates potential scenarios going forward as it doesn’t seem to be working for them in recent opinion polls. Labour party leader Corbyn said that his party is pledging to hold a second referendum on Brexit if it’s elected to government, pitting ‘Remain’ against a “credible” deal he negotiates with the EU but without saying which side he’d campaign for. Elsewhere in politics, the annual General Debate of the UN General Assembly begins on Tuesday, with a number of world leaders expected to appear.

Overnight we got some fresh trade headlines with Bloomberg reporting that Chinese Vice Premier Liu He plans to visit Washington in the second week of October to meet Lighthizer and Treasury Secretary Steven Mnuchin for high-level negotiations while adding that the two sides are aiming for a high-level meeting around 10th October. Earlier, the USTR’s office said in a statement that the US and Chinese negotiators held “productive” talks on Thursday and Friday in Washington with China’s Ministry of Commerce also calling the meetings “constructive,” and said both sides agreed to continue communications on relevant issues. On Friday, President Trump said he wasn’t interested in “a partial deal” with China based on Beijing increasing its purchases of US agricultural products. Trump added that he wouldn’t relent without reaching a “complete deal” with China.

This morning in Asia markets are largely heading lower with Chinese markets leading the declines – the CSI (-1.49%), Shanghai Comp (-1.31%) and Shenzhen Comp (-1.43%) are all down over 1%. The Hang Seng (-0.86%) and Kospi (-0.15% are also down while Japanese markets are closed for a holiday. Indian stock markets are up another 2% this morning after advancing c.5% on Friday, the largest gain in the last 10 years, as the country lowered the corporate tax rate to 22% from 30%. Elsewhere, futures on the S&P 500 are up +0.38% while oil prices are up c. 1% this morning following WSJ reports that full repairs to Saudi oil fields hit by the drone attack may take many months.

To recap last week, the S&P 500 pared gains on Friday to end the week down -0.51% (-0.49% Friday) after Chinese trade negotiators cancelled a visit to US farmers and President Trump also said he didn’t need a deal before the election next November. Over the weekend there were reports that the cancelled trip to US farm states was not due to trade related issues and that the trip will be rescheduled. That news came too late to rescue markets last week as the trade-sensitive Philadelphia semiconductor index was particularly impacted, ending the week down -2.66% (-1.83% Friday), while Treasuries made gains for a 5th consecutive session following the news to end the week -17.4bps (-6.3bps Friday). The moves come ahead of what the US Trade Representative’s Office describes as “principal-level meetings” planned for October. The news came out after the European close, where the Stoxx 600 had gained +0.30% (+0.29% Friday) to advance for the 5th consecutive week.

Of course the other main market moves of last week came from oil, where further developments came on Friday as the US moved to sanction Iran. New measures were announced on the country’s central bank and its sovereign wealth fund, with President Trump describing them as “the highest sanctions ever imposed”. Brent Crude ended the week +6.74% (-0.19% Friday), the biggest weekly advance since January (even if it was up c.20% at Monday’s Asian open), while WTI Oil ended the week up +5.91% (-0.07% Friday). Energy stocks were the major beneficiaries, with the STOXX Oil & Gas index in Europe ending the week +4.46% (+1.69% Friday), its strongest weekly performance since July 2016.

The flight to safety amidst the geopolitical and trade developments supported safe haven assets, with gold snapping a run of 3 successive weekly declines to close +1.91% (+1.19% Friday), while 10-yr bund yields fell -7.3bps (-1.5bps Friday).

Amidst the stresses in US repo markets last week, which saw the effective federal funds rate move well outside the FOMC’s target range at one point, it was announced on Friday that there will be overnight repo operations daily of at least $75bn through October 10, as well as three 14-day term repo operations of at least $30bn each taking place next week. Two-year dollar swap spreads had hit a record low on Thursday, but widened after the New York Fed announced the operations. If you want to read more on this see DB’s Steven Zeng’s note ” Repo stress: a problem of too many collaterals, not a scarcity of reserves “.

A further interesting development on Friday came from Germany, where the government unveiled a €54bn package of measures to deal with climate change, which includes measures such as a carbon price of €10 per ton in 2021 for the transport and heating sector, rising to €35 per ton in 2025. However, Chancellor Merkel said that Germany would stick with the “black zero” policy of no deficit spending. Our German economists (link here ) write that the net fiscal impact next year will be 0.25% of GDP at best, disappointing those who hoped it would have been a “counter-cyclical package by stealth.”

As for the latest on Brexit, sterling weakened -0.18% against the dollar last week (-0.38% Friday) as negative comments on Friday from the Irish foreign minister, Simon Coveney, undermined hopes that a deal would be reached. Coveney said that “we need to be honest with people and say we’re not close to that deal right now.” Furthermore, Sky News reported that a leaked document from the European Commission said that the UK’s proposals failed to offer “legally operational solutions” to the Irish backstop. All this comes as the UK Supreme Court are going to be publishing their ruling this week in the case on the prorogation of Parliament.

“Simply Awful”: German PMI Plunges To 7-Year Low As Manufacturing Recession Accelerates, Spreads To Services

Weakness in euro-area manufacturing hit a climax this morning as German private sector activity plunged to a seven-year low. The Germany Manufacturing PMI slumped in September, dropping to 41.4, down from 44.7 in August, printing below the lowest sellside estimate (consensus of 44.4); worse, the German manufacturing recession is now spreading to the services sector, where the formerly resilient services PMI also slumped from 54.8 to 52.5, missing the lowest expectation, and resulting in the first composite PMI print below 50, or 49.1 to be precise, since April 2013. The rate of decline was one of the sharpest in seven years.

Key findings of the report indicate business conditions across Germany continue to deteriorate with no end in sight.

Flash Germany PMI Composite Output Index (1) at 49.1 (Aug: 51.7). 83-month low.

Commenting on the flash PMI data, Phil Smith, Principal Economist at IHS Markit said that “The manufacturing numbers are simply awful. All the uncertainty around trade wars, the outlook for the car industry and Brexit are paralyzing order books, with September seeing the worst performance from the sector since the depths of the financial crisis in 2009.

“Another month, another set of gloomy PMI figures for Germany, this time showing the headline Composite Output Index at its lowest since October 2012 and firmly in contraction territory. “The economy is limping towards the final quarter of the year and, on its current trajectory, might not see any growth before the end of 2019.

“With job creation across Germany stalling, the domestic-oriented service sector has lost one of its main pillars of growth. A first fall in services new business for over four-and-a-half years provides evidence that demand across Germany is already starting to deteriorate.”

In kneejerk reaction, global equity futures across the world slumped. European equity futures, from the STXE 600, DAX, CAC 40, FTSE MIB, and IBEX 35 were down over -1%. S&P500 mini tumbled nearly -1%, rejecting the 3,000-handle, and finding a short term bottom around 2982 at the 5 am est. hour.

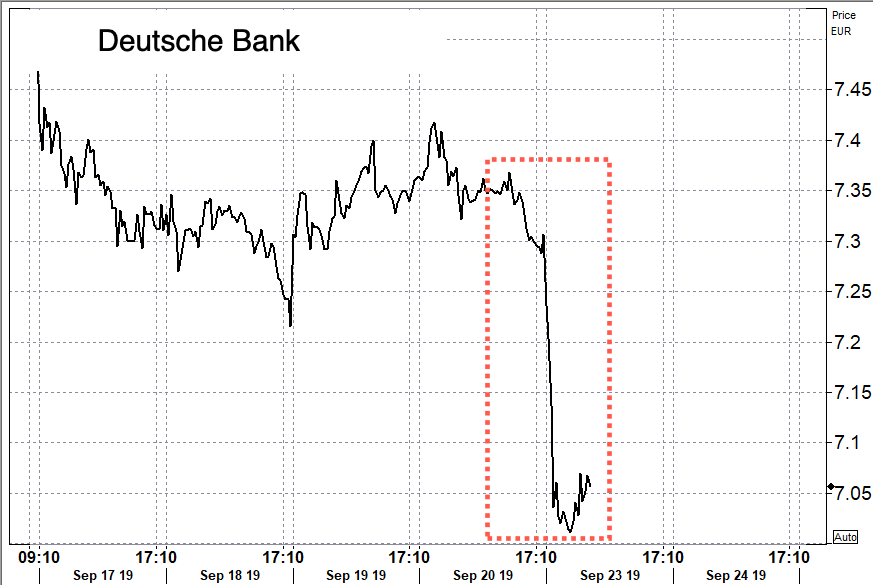

European banks were some of the worst performers of the morning, pulled lower by lenders after PMI figures for Germany were released. Around 5 am est., the Stoxx 600 Bank Index was down -1.6%.

Commerzbank (-5.1%) and Deutsche Bank (-3.6%) lead the declines as the latest PMI figures confirmed Germany is in a technical recession.

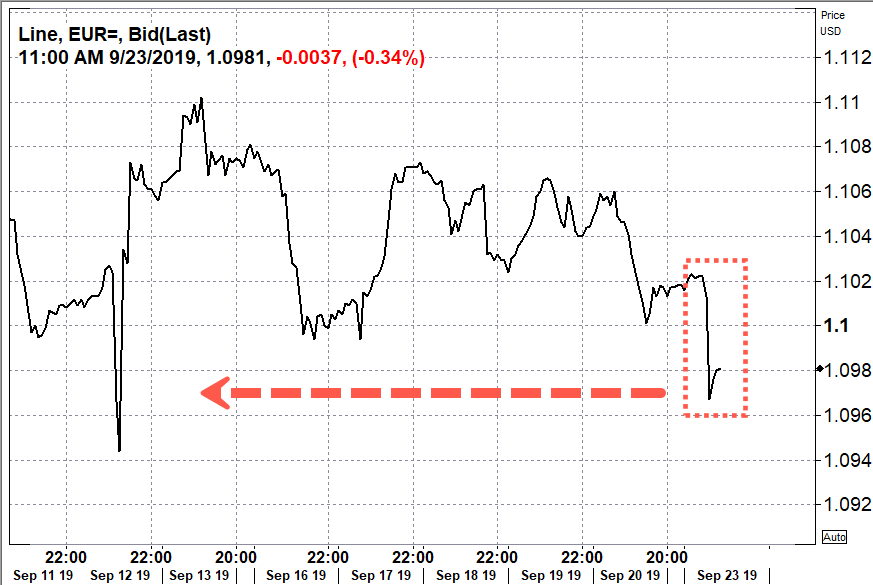

In currencies, the dismal PMI data pressued the common currency, and the EURUSD lost the $1.10 handle, dropping 0.5% to 1.0966, after both Germany and France PMis missed, and what’s worse, now indicate there are spillover effects into the service sector.

“Option-related demand around 1.1000 failed to absorb the selling pressure, with intraday bidding interest below 1.0980 also coming to the test,” traders told Bloomberg.

The weak PMI data from Europe was not a surprise, but the spillover into services shows the consumer is starting to weaken, an indication that the slowdown is broadening.

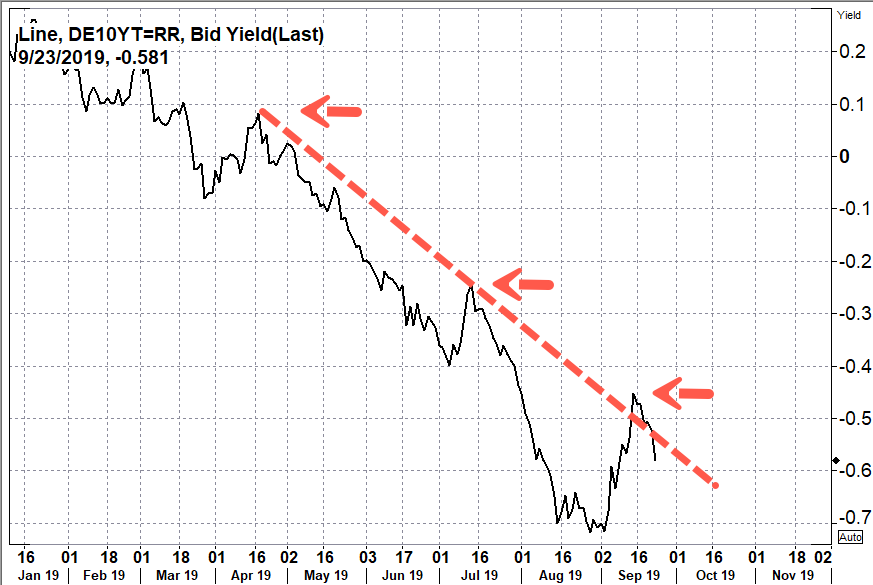

Predictably, Bund yields across the euro area fell in response to PMI figures for Germany, which deepened investors’ recession fears and sparked a rally in government bond markets, where yields declined.

“The bit that will worry markets is that services that have been largely immune now show signs of substantial contagion effect from the slowdown in manufacturing,” said Marc Ostwald, global strategist at ADM Investor Services.

“In terms of today’s price action it will put a big old dent in equities and give the whole spectrum of government bonds a boost.”

Germany’s 10-year bond yield fell to -0.576% — its lowest level since the ECB meeting (Sept. 12) concluded that rate cuts and fresh stimulus were needed to boost weak growth.

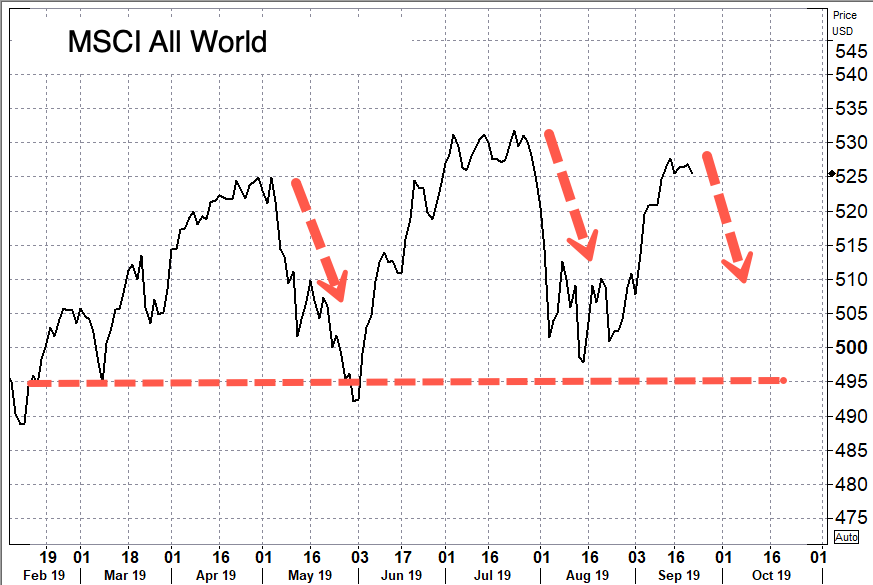

The MSCI All Country World Index, which tracks shares across 47 countries, also dropped on the news of more slowing in Europe.

Brent crude futures jumped on doubts how fast Saudi Arabia can restore its crude output after a drone attack earlier this month crippled one of its largest oil processing facilities.

Brent crude futures climbed to as much as $65.50 per barrel, a gain of over 1%, but have gone red post-PMI data.

“Considering that Germany already contracted in Q2, today’s numbers effectively increase the risk of another negative quarter in Q3, which by definition would constitute a technical recession,” said Marios Hadjikyriacos, investment analyst at XM.

“It seems that the malaise in manufacturing — owed to trade and Brexit worries — has started to spread to the much larger services sector as well.”

Market sentiment was already fragile entering the new week, and it seems that global markets could be returning to macro, scared by the deepening of the German manufacturing recession, and a spillover into services.

UK’s Thomas Cook Collapses After Rescue Talks Fail; 650,000 Travelers Stranded

Becoming the latest European travel company to fail and leave its customers stranded (who can forget about the collapse of Iceland’s Wow Air back in March?), 178-year-old Thomas Cook collapsed after failing to secure a deal with its creditors, leaving the British government to step in and rescue the as many as 600,000 customers who are reportedly now looking for a ride home.

Thomas Cook CEO Peter Fankhauser apologized to customers “following a decision of the board late last night, a British government receiver has been appointed early this morning…we have not been able to secure a deal to save our business...I know that this outcome will cause a lot of anxiety, stress and disruption.”

Fankhauser explained that while a “deal had been largely agreed, an additional facility requested in the last few days of negotiations presented a challenge that ultimately proved insurmountable.” The company, weighed down by debt, said Friday that it was looking for $369 million in financing over the weekend to avoid going under on Monday.

At the time, the company had a debt burden of £1.25 billion and warned that Brexit-related uncertainties had hurt bookings for summer holiday travel. The firm has also struggled with increased competition from online travel-booking websites like Expedia.

Chinese conglomerate Fosun, Thomas Cook’s biggest shareholder, had considered contributing $560 million to bail out the company earlier this year, but ultimately demurred for reasons that aren’t clear.

All bookings made through the company have been invalidated, the company said. It typically runs hotels, resorts, airlines and cruises for 19 million customers a year in 16 countries.

BREAKING: “We have not been able to secure a deal to save our business” – Chief executive of Thomas Cook Group, Peter Fankhauser apologises to the company’s ‘heartbroken’ staff and customers.

Shares in European airlines and tourism-related companies climbed on the news, with the Stoxx 600 Travel & Leisure Index becoming one of 3 sectors gaining as the broader European share gauge declined.

The UK government is now scrambling to get all of its citizens home safely in what some have called “the largest peacetime repatriation effort in British history,” according to the Sydney Morning Herald. The UK Civil Aviation Authority said Monday that it would be working with the government to bring more than 150,000 British customers home over the next couple of weeks. The UK government runs an insurance program that ensures travelers can return home if a British tour operator goes under while they’re traveling, which is exactly what’s happening with Thomas Cook.

CAA Chief Richard Moriarty told the FT that it had launched “what is effectively one of the UK’s largest airlines, involving a fleet of aircraft secured from around the world.”

“The nature and scale of the operation means that unfortunately some disruption will be inevitable.”

Though the company was reportedly still selling vacation packages late last night and assuring its customers that all flights would continue as normal, passengers waiting at the airport were the first to learn that all operations would be cancelled.

Set to depart from Gatwick Airport, Thomas Cook flight 508 to Dalaman, Turkey was abruptly cancelled early Monday, the first in a string of cancellations at UK and global airports that will ultimately impact one million vacationers, according to the Independent.

Thomas Cook’s collapse resembles that of UK carrier Monarch two years ago. but Thomas Cook is a much bigger firm, and cleaning up this mess will be a much bigger headache for the CAA. Meanwhile, analysts at Bernstein suspect other tour operators could collapse, which would put the market into a bind.

The modern Thomas Cook Group formed in 2007 when the UK’s MyTravel merged with the privately-held Germany-based Thomas Cook to create a tour-company behemoth and promising to hasten consolidation in the tour operating industry.

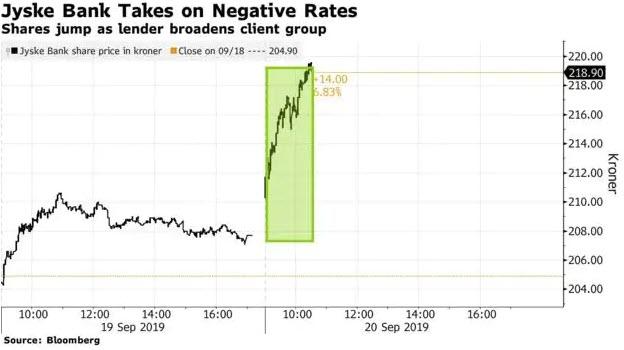

Jyske Bank said on Friday people with more than $111,100 in their bank accounts will be charged more for their deposits as it seeks to pass on some of the costs of recent rate cuts by the European and Danish central bank.

Jyske Bank, Denmark’s second-largest bank, said it would introduce a negative interest rate of 0.75% for all corporate deposits and for private clients depositing more than 750,000 Danish crowns ($111,100) from Dec 1.

Last week, Denmark’s central bank cut its key deposit rate to minus 0.75%, a record low among developed economies. “It is a lot of money and we have to pass on part of this bill to our customers,” he said. “I don’t hope that we will have to go lower but I don’t dare to promise it.”.

Denmark’s largest bank, Danske Bank has said it has no plans to introduce negative interest rates on deposits. Switzerland’s UBS has said it will impose a negative rate of 0.75% on clients who deposit more than 2 million Swiss francs ($2 million). ($1 = 6.7559 Danish crowns)

Simple Question

If you live in Denmark and have a bank account in excess of $100,000 or so, why would you have it at Jyske Bank which charges 0.75% while Danske Bank, the country’s largest bank doesn’t?

Possibilities

There is something seriously wrong at Danske Bank and people don’t trust it.

Danske Bank welcomes deposits and can do something with the money. But if so, at what risk?

Any Danish readers care to answer?

Perhaps we have an answer from Bloomberg in the following discussion.

Shares in Jyske closed more than 5% higher marking their best performance since December 2017, as investors calculated the impact that the new policy will have on the bank’s net interest income.

Jyske has “set the ball rolling,” said Per Hansen, an investment economist at broker Nordnet.

Other Bank Comments

A Danske Bank spokesman said, “We cannot comment on competitors’ prices and have nothing new to add on the matter.” The bank has previously promised to protect retail depositors from negative rates.

Nordea Bank Abp spokeswoman Tenna Schoer said the Danish unit is “monitoring the situation closely.” The bank’s CEO Frank Vang-Jensen has previously said Nordea can’t rule out imposing negative rates on retail depositors.

Sydbank, which has already said it will impose negative rates on retail depositors with over 7.5 million kroner, is monitoring the situation. “We have taken note of developments in the market and have seen that interest rates have fallen further,” said Jan Svarre, deputy CEO at the bank. “We’ll investigate our options and where the limit should be, and then we will return and notify our customers directly.”

Per Hansen commented “imposing such a policy is politically difficult for Danske, given its recent history of financial scandals. The bank is being investigated for a $220 billion money-laundering affair, and has been reported to the police for a separate case in which it overcharged retail investors.”

Bonus Questions

What happens to Danske if all the Danish money flees to Jyske?

What happens if everybody takes their money and runs?

Regardless of the answers, I expect to see an increased demand for gold, the US dollar, US treasuries, and safes as these pass-through policies escalate.

{kind=link}

{kind=link}

{kind=link}