After the 4th biggest point drop in US stock market history, this is all equity dip-buyers could manage? This won’t end well…

China was mysteriously panic-bid overnight after plunging at the open after US stocks crashed…

Source: Bloomberg

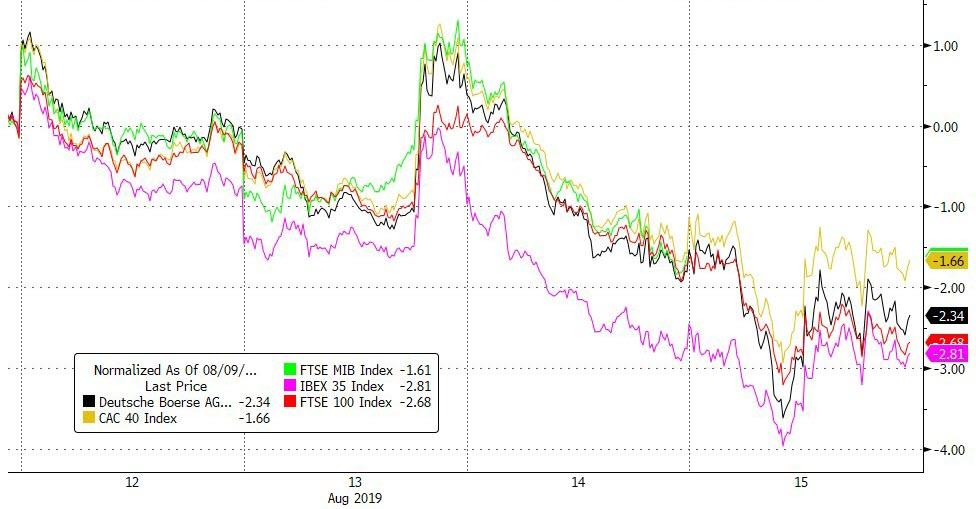

More stimulus promises did nothing to help European stocks…

Source: Bloomberg

EU banks broke to a new cycle low…

Source: Bloomberg

After ECB promised more stimulus, Bund yields crashed to a stunning record low of -71bps (down 21 of last 24 days)…

Source: Bloomberg

Also of note, in the crazy world of negative rates, the 50Y EU Swap rate has dropped below zero for the first time ever…

Source: Bloomberg

US equities whipsawed by headline-reading algos early on as China threatened retaliation, WMT surged, and China offered some hope for a deal before Trump confirmed on his terms…

An afternoon buying spree (paging Steve Mnuchin) lifted The Dow, S&P, and Nasdaq into the green for the day

On the week, Trannies are the biggest losers

The Dow bounced back above its 200DMA…

Small Caps tumbled to May lows and bounced a smidge, dramatically below the 200DMA…

The Dow was rescued by WalMart’s big gains…

But GE crashed on Markopolous exposures…

Defensives dominated the days…

Source: Bloomberg

Source: Bloomberg

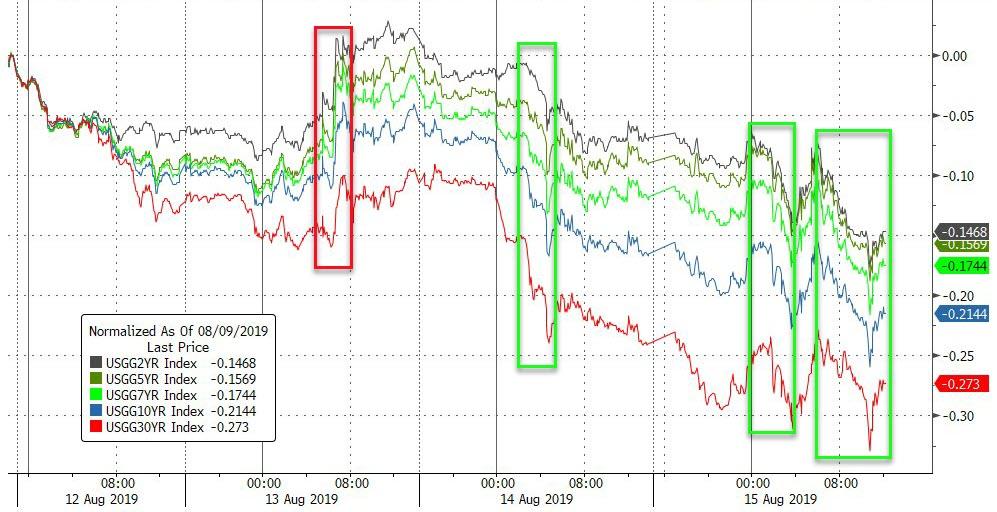

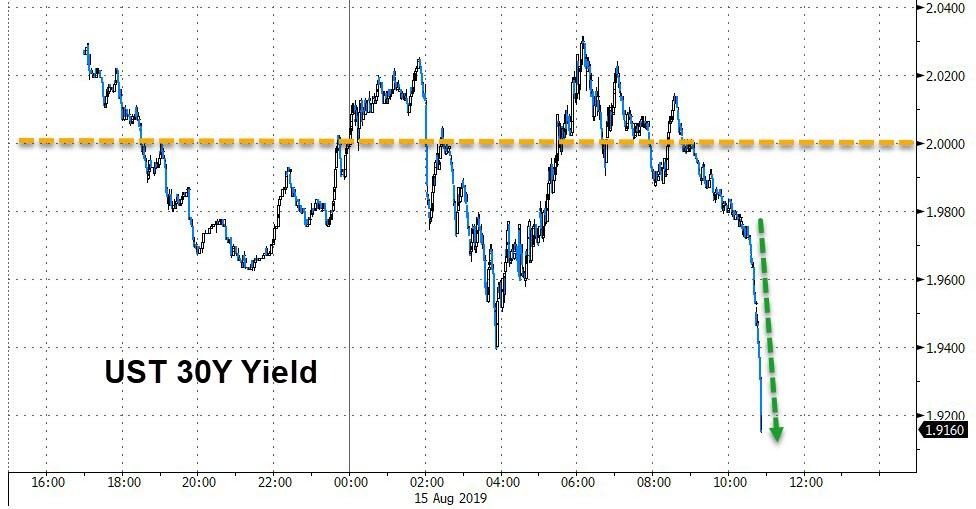

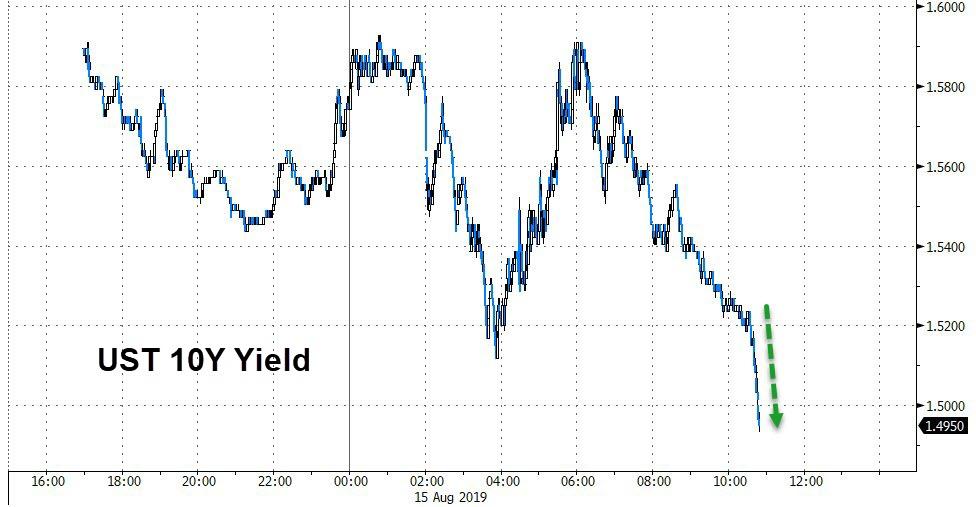

Treasury yields tumbled on the day (again) with the short-end outperforming this time (2Y -7bps, 30Y -3bps)…

Source: Bloomberg

30Y broke below 2.00% for the first time ever (and 2Y broke below 1.50% for the first time since 2007 as did 10Y)…

Source: Bloomberg

And the 10Y Yield is testing back towards record lows…

Source: Bloomberg

The yield curve story was mixed – 2s10s rose back from inversion…

Source: Bloomberg

BUT remember the 3m10Y – which is the most accurate recession indicator – remains deeply inverted…

Source: Bloomberg

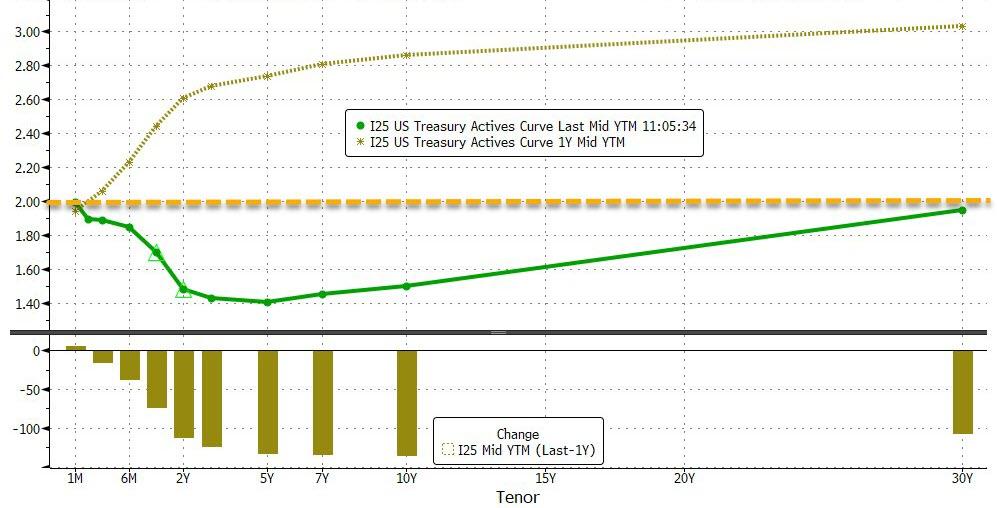

What a difference a year makes – entire curve now below 2.00% but entire curve was above 2.00% exactly one year ago…

Source: Bloomberg

And TIPS markets are pricing in a deflationary future…

Source: Bloomberg

Overnight weakness in the dollar ramped higher once again today (starting to see a pattern here)…

Source: Bloomberg

Yuan weakened modestly overnight (even as the PBOC fixed it stronger again)…

Source: Bloomberg

Which is notable as China appeared to start trying to squeeze the shorts with a liquidity squeeze overnight…

Source: Bloomberg

And it appears Hong Kong authorities intervened to keep the HKD away from the low-end of the USD peg…

Source: Bloomberg

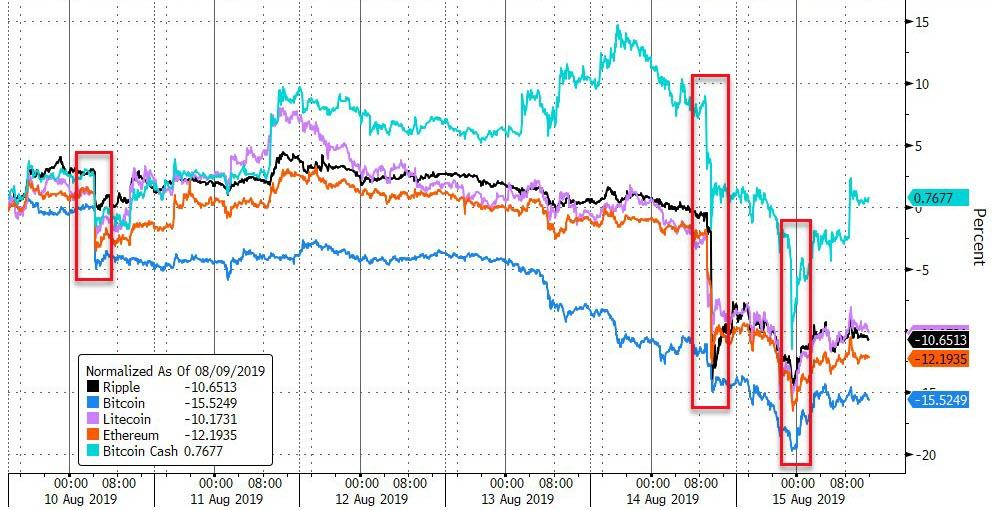

Cryptos got hit hard overnight but bounced back as Europe opened…

Source: Bloomberg

But Bitcoin bounced back above $10k by the end…

Source: Bloomberg

Oil and gold diverged once again today as did copper (lower) and silver (higher)…

Source: Bloomberg

WTI is back below $55…

Gold futures’ bounce off $1500 continues…

Global Negative-yielding debt topped $16 trilion for the fiorst time ever, and gold tracked it perfectly (but bitcoin appears to have decoupled for now)…

Source: Bloomberg

Treasury yields imply gold should be higher or copper lower…

Source: Bloomberg

Finally, we have seen the emergence of another ominous Hindenburg Omen…

Source: Bloomberg

We all know who to blame… right Mr. Trump?

“The Fake News Media is doing everything they can to crash the economy because they think that will be bad for me and my re-election. The problem they have is that the economy is way too strong and we will soon be winning big on Trade, and everyone knows that, including China! “

At least The Fed wasn’t immediately blamed this time.

via ZeroHedge News https://ift.tt/2KBYJxN Tyler Durden

An adjunct professor from City University of New York says the “ideology of racialized terrorism” is the responsibility of all white people in the United States.

In an interview with WBGO radio (which was taken offline shortly after being posted; the archived link is here), political science instructor Josie Gonsalves said that she has “seen enough” and proceeded to tie America’s racist and capitalist past to the current mass shootings of the present.

Gonsalves claims she left her island nation (she doesn’t identify it) — “a parliamentary democracy with vigorous intellectual discourse and robust civic engagement” — and upon arrival in the US was “assigned” the designation of “immigrant, non-white, and ‘other.’”

That “other” is key, Gonsalves says, as white America has a history of engaging in the ethnic cleansing of “others,” starting with Native Americans.

The professor also has an interesting way to describe the Civil War: “So fierce, the fight for ownership of human beings as chattel, America waged a Civil War from 1861-65 to maintain, property rights over Black bodies.”

This political ideology of racialized terrorism rests with every white designated person in this country. White neoliberals cloak themselves in a fantasy that the race war exploding on the streets of America rests discreetly in the hands of “crazies,” “far-right wingers,” “outliers” and even more mythic characterizations. So, America builds clinics and mental health hospital beds for White home-grown terrorists, but concentration camps and high-level security prisons for Black, and Black and Brown immigrants.

The killings in El Paso and Dayton this past weekend demonstrate, again, that the ugly of America is as mainstream as apple pie. This country’s history and praxis rest comfortably in the mythology of white superiority. In choosing to “other” fellow citizens [undocumented and documented Black and Brown immigrants; Brown and Black; Muslim and Jew], white America has damned this democracy into the hands of White terrorists. White America has laid the burden of the debt incurred by white supremacy on the bodies and psyches of the “other.”

Gonsalves goes on to wonder why we pay tribute every September 11 to “the once pillars of American capitalism,” but never to “the young Black and Brown” victims of domestic terror. She also claims a race war “is being thrust upon us.”

“White America,” she concludes, “can no longer expect to pay for life, liberty, and the pursuit of happiness with the red blood of those they want to Other, criminalize, dehumanize, disenfranchise, and marginalize.”

The College Fix asked WBGO why Gonsalves’s original commentary was removed, but did not receive a response.

According to her LinkedIn page, Gonsalves is a “sort-after [sic] public speaker and moderator on racial and social justice, and implicit bias” whose post-graduate studies at Rutgers included “reparative justice.”

via ZeroHedge News https://ift.tt/2KPxKNY Tyler Durden

When stocks rise – usually because the Fed made some guttural, dovish noise and promised even more monetary Kool-Aid – the bulls are delighted, and go to great lengths to mock the bears and short sellers who are “obviously wrong.” However, when stocks plunge – as they did yesterday – there is an utmost urgency to i) explain that the sellers are clueless/have no idea that stocks are massively undervalued, ii) find the sellers, and iii) failing that, blame the selloff on the algos (and in some very specific cases – like Goldman and oil for example – blame negative gamma).

That’s precisely what happened following yesterday’s 800 point Dow plunge, which the bulls and other liquidity addicts quickly accused the algos, quants and various other machines who – the narrative goes – of mindlessly latching on to the plunge in bonds yields, sending stocks tumbling.

Only that’s not true, and as Nomura’s quant team writes today, the magnitude of yesterday’s sell-off suggests that panic-selling by longer-term investors was the driving force, rather than trading by algo players, to wit:

When a sell-off like yesterday’s happens, commentators scanning the supply/demand landscape in a hunt for the principal culprit tend to single out algorithmic traders, but we think they would be wrong to do so in yesterday’s case.

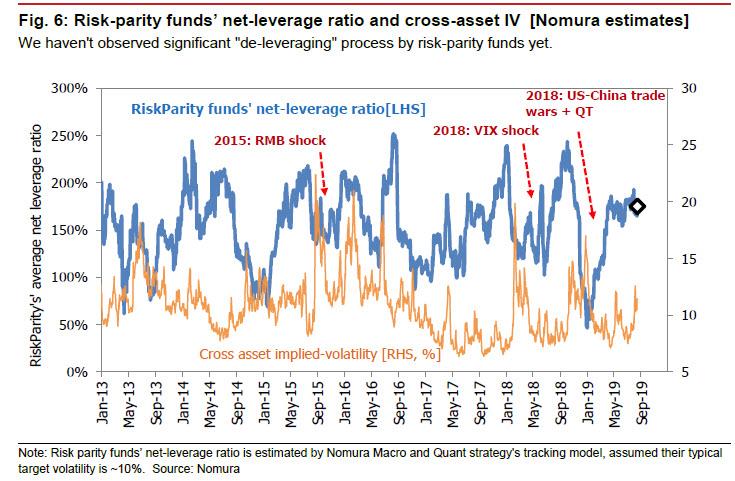

And while Nomura concedes that both CTAs and risk-parity funds participated in the selling, the Japanese bank sees no signs that they exited longs or deleveraged “on the sort of scale that could make for a sell-off of yesterday’s magnitude.” Furthermore, while it is plausible to think that some anti-momentum algorithmic traders momentarily dumped stocks in response to the signal sent by the inversion of the 10yr-2yr yield curve, Takada thinks that the large and continuous sell-off that progressed from that point on was in all likelihood led by panic-selling on the part of longer-term investors. Indeed, recall that in December 2018, algos were treated as a convenient scapegoat for longer-term investors’ shift away from stocks and into bonds as other segments of the yield curve started to invert.

Some more details:

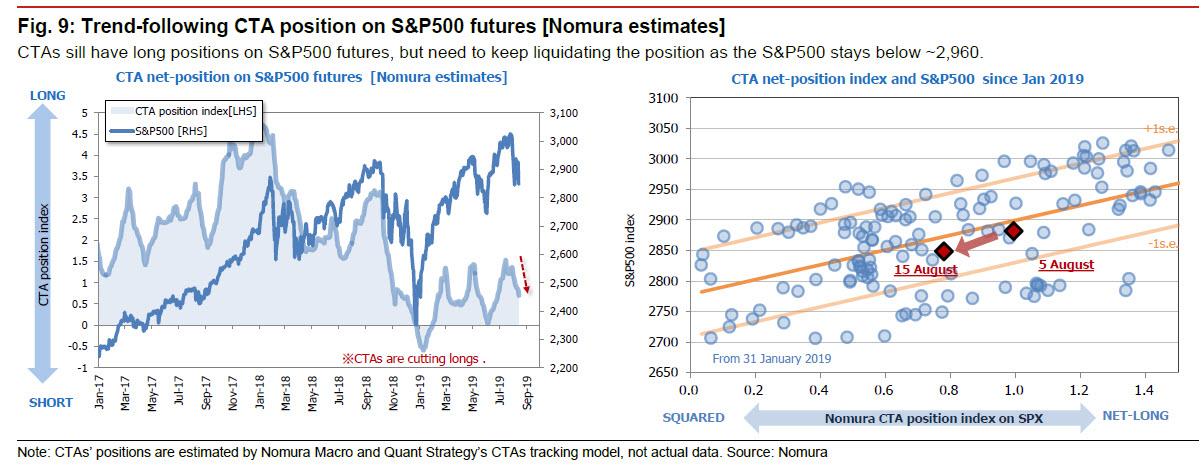

Trend-chasing CTAs were net sellers of equity futures in major markets. With the S&P 500 stuck below 2,960 (which is the average break-even line for CTAs’ net buying since June), CTAs have continued closing out longs. As of now, CTAs have only closed out 54% of the net long position they held on 16 July (the recent peak in that position), so they still have quite a way to go. CTAs are also still selling China A50 futures at index readings below 13,440 (representing their average cost of net buying since June). Meanwhile, CTAs continue to accumulate short positions in Nikkei 225 futures and DAX futures. We estimate that CTAs’ existing short positions break even at 21,200 (for the Nikkei 225) and 11,630 (for the DAX). In each of these markets, selling by CTAs looks merely steady, not frantic.

Little evidence of much market activity by risk-parity funds. Some funds may have moved to rebalance their portfolios in response to the rise in stock market volatility, but most are probably waiting until their regular month-end portfolio rebalancing comes around. Cross-asset volatility has not increased all that dramatically, and risk-parity funds’ portfolio leverage has held steady at around 170%; we see no evidence of significant deleveraging.

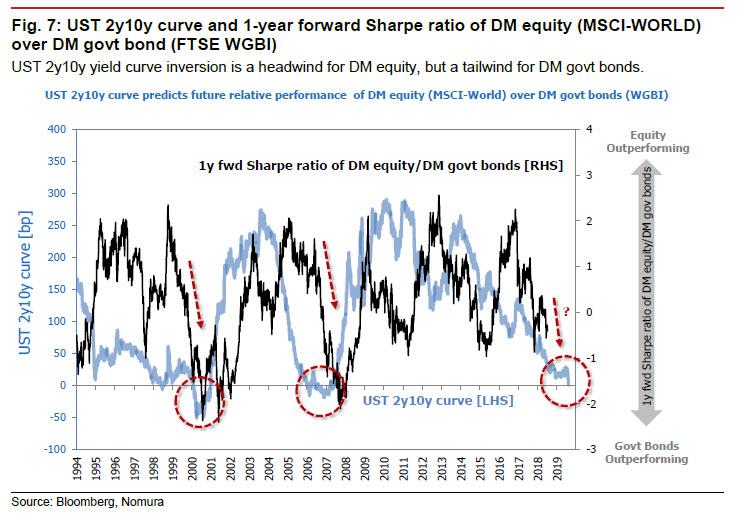

But while yesterday’s selling may have been all humans, the real question is whether it will continue – regardless if human or machine-driven. To this point, Nomura makes one final, ominous observation: with the 10yr-2yr UST yield curve having briefly inverted yesterday, an interesting phenomenon that tends to occur after such inversions is that stocks tend to consistently underperform bonds over the subsequent 12 months (measured using one-year forward rolling Sharpe ratios).

Here, Nomura’s quant team argues that the historical underperformance of stocks in these circumstances is powered by an undercurrent of longer-term investors quietly executing an allocation shift away from stocks and into bonds, upon reading the inversion of the yield curve as a signal of a coming recession.

This is also why yesterday’s symbolically-loaded inversion of the 10-2 spread did much to induce panicky behavior (stock-selling and bond-buying) among longer-term investors, be they man or machine.

via ZeroHedge News https://ift.tt/2Z9SNEa Tyler Durden

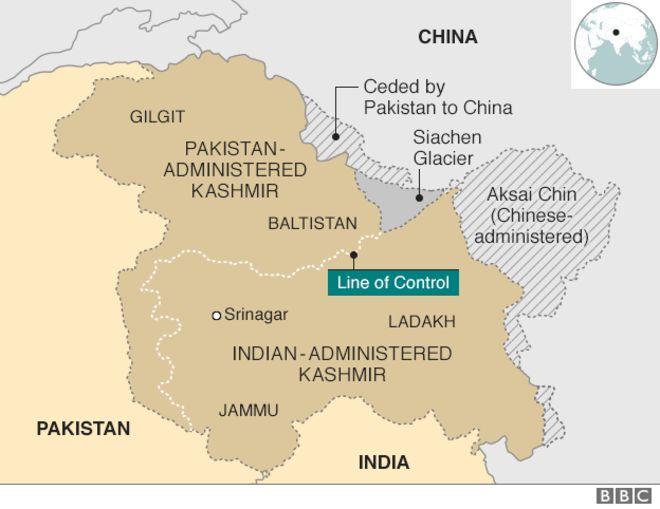

A major exchange of fire has erupted along the contested Kashmir border separating India and Pakistan known as the Line of Control (LoC). Pakistan’s army says at lease three Pakistani and five Indian soldiers were killed during the cross-border fighting on Thursday.

However, India is denying the Pakistani army’s account of the “ceasefire violations,” calling it “fictitious”. According to India Today “unprovoked fire” from the Pakistani side deliberately timed during India’s 73rd Independence Day forced a response. India claims there were no casualties on its side, while affirming that three Pakistani troops were killed.

File image: Indian troops along the Line of Control

The incident was first revealed when chief spokesman of the Pakistan armed forces, Major General Asif Ghafoor, announced on Twitter that Indian forces had fired at the LoC, and that “Intermittent exchange of fire continues”.

In efforts to divert attention from precarious situation in IOJ&K,Indian Army increases firing along LOC.

3 Pakistani soldiers embraced shahadat. Pakistan Army responded effectively. 5 Indian soldiers killed, many injured, bunkers damaged. Intermittent exchange of fire continues. pic.twitter.com/wx1RoYdiKE

In response to Pakistan’s claim of 5 Indian soldiers killed, a senior Indian Army official told national media, “The claim made by Pakistan’s military is fictitious.”

Sporadic shelling has continued along the LoC as a major Indian military crackdown on Jammu and Kashmir (J&K) continues after early last week New Delhi voted to revoke the Muslim majority region’s autonomous status.

A complete communications blackout and state of martial law has continued in the restive region. Recently Pakistan’s Prime Minister Imran Khan has vowed to support Kashmir amid the Indian crackdown “with all possible options”.

Analysts have predicted that India revoking J&K’s status could send it hurtling towards war with its nuclear-armed Muslim neighbor Pakistan.

via ZeroHedge News https://ift.tt/2KCgkpe Tyler Durden

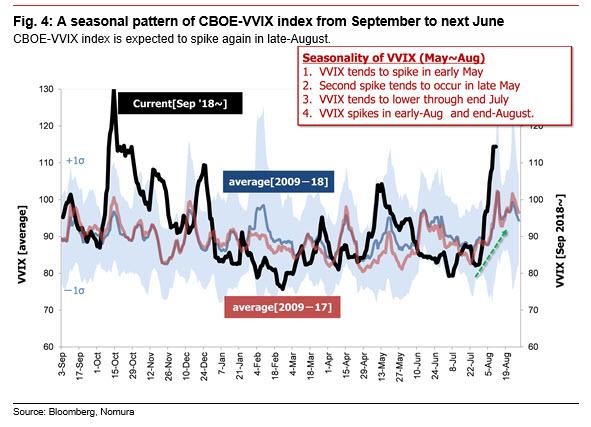

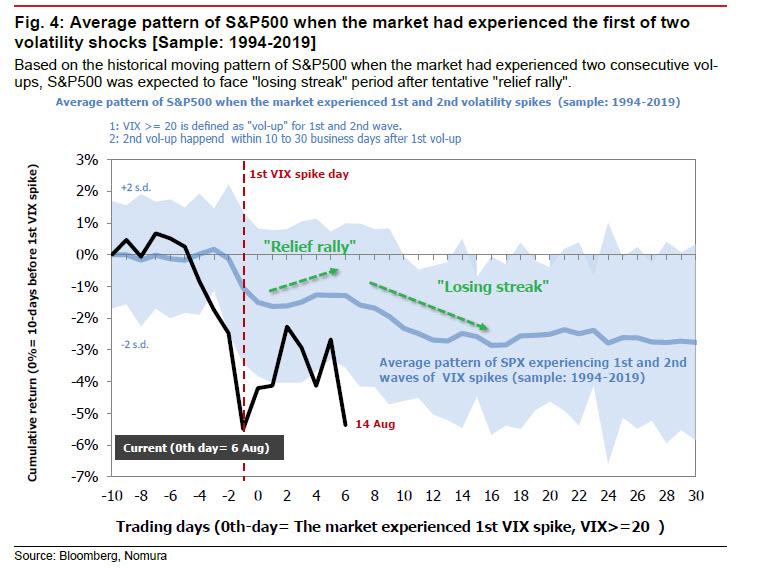

One week ago, and just days before Wednesday’s market plunge and curve inversion, Nomura’s quant team – correctly – predicted that the early August rally was a head fake, and warned that any such rally “should be best treated as an opportunity to sell in preparation for the second wave of volatility” that the bank expects will arrive in late August or early September. Worse, as Nomura quant Masanari Takada said, “the second wave may well hit harder than the first, like an aftershock that eclipses the initial earthquake. At this point, we think it would be a mistake to dismiss the possibility of a Lehman-like shock as a mere tail risk.”

Since then a lot of things happened, but none more memorable than the inversion of the 2s10s curve – the most respected leading recession indicator – for the first time since 2007 following dismal economic data from both China and Germany. And, as Nomura’s quant team points out, “the trauma in global bond markets worked its way into equity markets as well, such that stock markets in the West—and especially in the US—underwent a massive sell-off.”

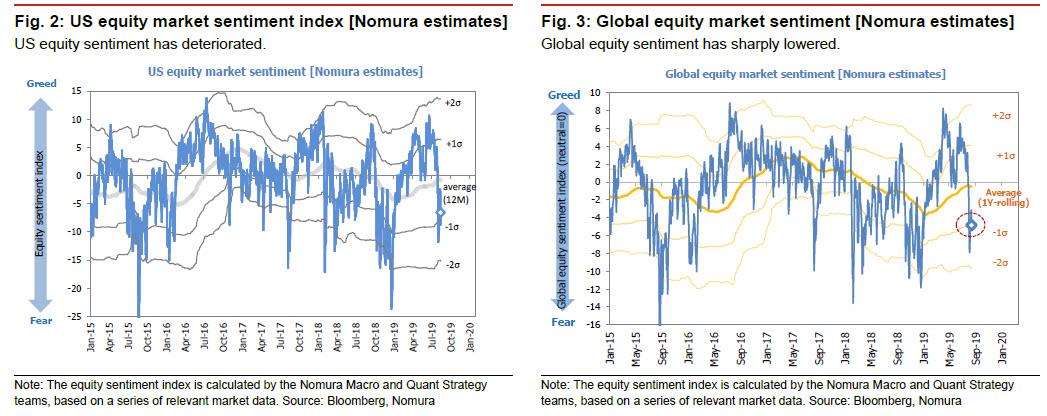

The result was that Nomura’s composite measure of US stock market sentiment swiftly dropped from -2.6 on 13 August to -6.5 on 14 August, while its measure of global stock market sentiment similarly fell from -3.1 to -4.8, both levels not seen since December’s mini bear market.

The other immediate result: the boost the market got on the previous day (13 August) from the postponement of a portion of the fourth round of US tariffs on Chinese goods evaporated almost immediately, putting a quick end to the relief rally in US stocks, and as Takada argued in his Wednesday note, sustaining the rally would depend on

the S&P 500 regaining the 2,960 line,

the VVIX settling down to around 90, and

a 10yr-2yr UST yield curve that resists becoming inverted.

By all three measures, yesterday’s developments were a complete rout, as the S&P 500 was sold down to 2,840, the VVIX rose to 113, and the 10-2 spread inverted, according to Takada. All of this is to say that the market seems to be experiencing just the sort of tense summer Nomura had anticipated, “raising the likelihood of the second “vol-up” wave that we have been warning may arrive in late August or early September.”

* * *

So if a vol explosion and/or a “Lehman shock” is indeed coming, how should one be positioned?

First of all, according to Nomura, there is little in the way of developments on the horizon that could help solidly reestablish a normal 10yr-2yr UST yield curve, so the bank thinks it makes sense for now to stay bearish on global equities and bullish on global bonds (sovereign debt).

Additionally, the bank’s quants see a high risk of the market unwittingly launching itself into a pattern of trades that make a recession essentially self-fulfilling, barring the emergence (by the end of August) of some positive news powerful enough to turn the tide, such as

the withdrawal of the fourth round of tariffs on Chinese goods,

an emergency rate cut by the Fed on the order of 50-100bp (or an implicit promise to make such a cut), or

reports to the effect that a coordinated fiscal response is on the way.

Absent these highly unlikely events, Nomura warns investors not to be swayed by day-to-day headlines that do not add up to one of these three things, and should consider strategies built around the assumption that a second “vol-up” wave is coming. In that context, Nomura has 4 key trade recommendations:

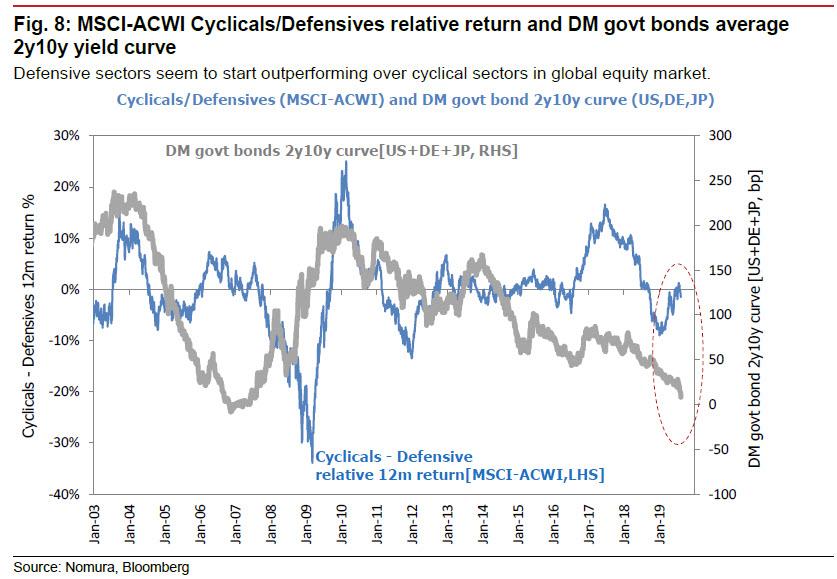

1. Buy low-beta & defensive stocks, sell high-beta & cyclical stocks: There is a loose correlation between the inversion of the 10-2 spread in DM bond markets and the relative performance of defensives vs. cyclicals in global equity markets (MSCI ACWI). The bond market’s track record in predicting recessions is somewhat less than perfect, but it makes sense to conservatively shift into low-beta & defensive stocks on the assumption that stock market players as well will become more fearful of a recession

2. Too soon to start contrarian buying in the hope of riding a bear squeeze rally in equity futures: CTAs and other speculative players are still net long US equities. Buying in now would mean trying to catch a falling knife, according to Takada; instead, a better opportunity may come in perhaps two weeks’ time. As the Nomura quant notes, “the right time to consider taking out contrarian long positions with the aim of capturing a bear squeeze rally would be when CTAs have cleared away their outstanding longs and have started taking on shorts.”

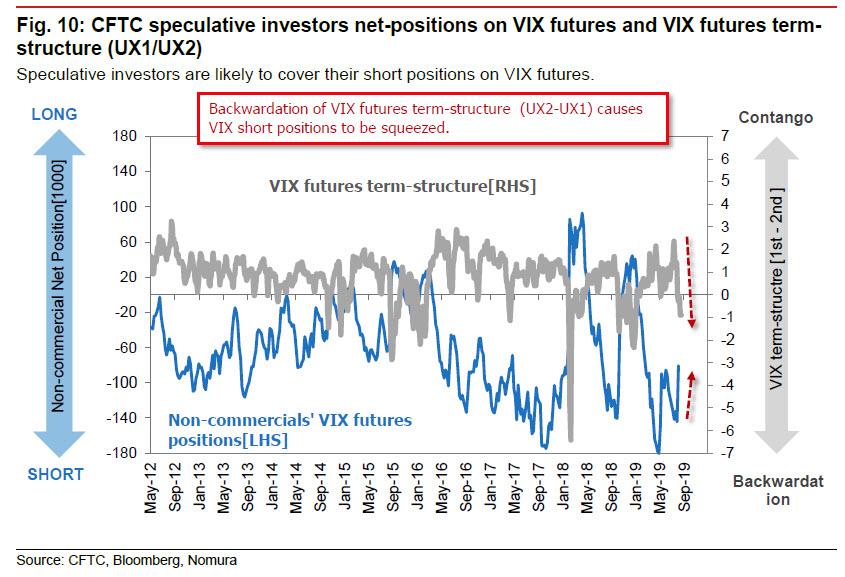

3. Still favoring long positions in the VIX and other measures of implied equity volatility, as the time for going short would be after the second “vol up” wave: CFTC data shows speculative players (non-commercial traders) to still have a net short position in VIX futures, to the tune of 80,000 contracts as of 6 August. Given the backwardation of the VIX futures curve between UX1 and UX2, speculators are likely to continue buying VIX futures to cover shorts.

4. Contrarian trades on indicators of fundamentals: Global markets are likely to increasingly press the Fed to cut interest rates substantially. Therefore expect stock market players to apply the “good news is bad news” reading to incoming US macroeconomic data.

Last but not least, beware of a self-fulfilling recession.

The inversion of the 10yr-2yr UST yield curve put a quick end to the relief rally in US stocks, and thereby seems to have pushed US stock market sentiment into a pattern that suggests further, significant deterioration ahead.

As Nomura concludes, “the inauspicious pattern in US stock market sentiment could well be signaling that a self-fulfilling recession is on the way.”

via ZeroHedge News https://ift.tt/31IrS00 Tyler Durden

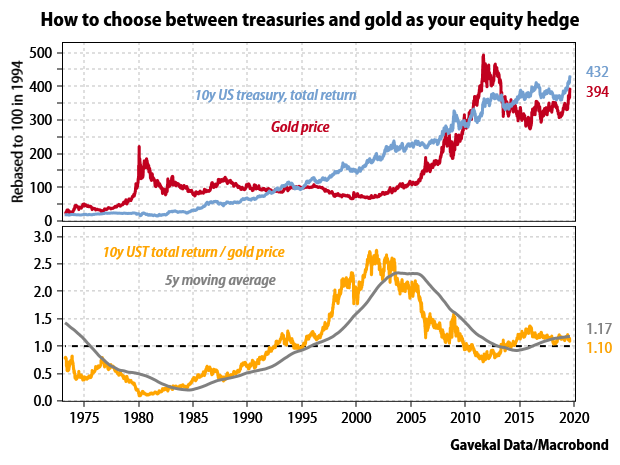

I always try to be a rules-driven investor. And when the US stock market is down -3% in a day, taking it to -6% from its peak in three weeks, when 10-year US treasury yields have halved in nine months to just 1.55%, and when gold is up 20% in three months, it is a good time to review those rules to see what they can tell me. The answer is: quite a lot.

One of the core tenets of my approach to portfolio construction is that to hedge the equity portion of my portfolio, I know I can use gold if the economy is in an inflationary period, and long-dated US treasury bonds if it is in a disinflationary interlude.

The trick is to determine whether the economy is in an inflationary period or not. I tend to look at the markets. If gold has outperformed the 10-year US treasury over the previous five years, I can stop asking questions and hedge with gold. Conversely, if the bond market has outperformed, I can go ahead and hedge with long bonds, providing its valuation is not too demanding.

Now please take a look at the chart below. The upper pane shows the price of gold plotted against the total return index of the 10-year treasury. The lower pane shows the ratio of the two series. Looking at the ratio, it is clear that from 1971 to 1984, investors should have used gold as their hedge. From 1985 to 2002 they should have chosen US long bonds; then from 2003 to 2012 gold, and from 2014 to May 2019 US long bonds once again.

Since May 2019, when the treasury total return/gold ratio fell below its five-year moving average, I have been recommending that investors switch from overvalued bonds to gold as the preferred hedge for their equity exposure (see The Inflation Shift And Portfolio Construction).

Usually, these two assets—long-dated US treasuries and gold—tend to be negatively correlated. When treasuries are going up, gold tends to go down, and vice versa.

But in the last few months, both have powered ahead at the same time. This left me scratching my head, and as usual when puzzled, I reached for the history books to see when in the past both treasuries and gold have looked overbought at the same time. Specifically, I looked for other occasions when the three-month rate of change for each asset was above its respective standard deviation at the same time. The conclusion is striking: we are in a panic.

There were plenty of market panics in the 1970s, when real rates were negative. Then from 1980 to 2007, when short rates were “normal”, they were almost non-existent. However since 2007, there have been several occasions when—unusually—both treasuries and gold went up at the same time.

Here they are:

The beginning of the global financial crisis.

The end of the global financial crisis.

The bond market meltdown in peripheral Europe which prompted Mario Draghi’s “whatever it takes” put.

The slowdown in China which led to the G20 “Shanghai agreement”.

The latest panic.

Each previous panic was dealt with by governments and—more importantly —central banks, including the Chinese central bank, ganging up to stop the rout. However, given the current chill in relations between Washington and Beijing over trade and technology, it is hard to believe that the latest episode will be halted thanks to a cozy cooperation deal between Donald Trump and Xi Jinping.

So what should investors do? My immediate advice would be to do very little right now. Acting in the middle of a panic is seldom a good idea. I would just continue selling bonds, and so raising cash.

Structurally, I maintain my call to hedge the equity risk in a portfolio with gold, since bondholders are most likely to be the victims of the next crisis. Indeed, I believe that in the next crisis, trading in some bond markets may be discontinuous, as in Argentina in recent days (see Lessons From The Argentine Shock). In the coming crisis, I fear there may be very little to choose between some European bond markets and Argentina.

Investors who believe the Hong Kong situation will not deteriorate further (see Hong Kong Q&A (Part II)) should hold on to their Chinese bonds (over the last 12 months, the 10-year Chinese government bond is up 7% in US dollar terms, handsomely outperforming the total returns on both one-year US T-bills and the S&P 500). And they should concentrate their equity holdings in high quality stocks relatively immune from the vagaries of governments, and hedge them with gold.

Praying might also help.

via ZeroHedge News https://ift.tt/33BSbGY Tyler Durden

Jeffrey Epstein’s former bodyguard and driver has backpedaled over 2015 comments he made to former Daily Beast reporter M.L. Nestel, at one point sugesting he drop the story and stop asking questions about Epstein’s pedophilia.

Nestel, now with New York Magazine, was able to reach the former UFC fighter, Igor Zinoviev, who was happy to answer questions about shuttling Epstein around Palm Beach and training the ‘pretend billionaire’ via workouts and light martial arts, the Russian MMA competitor clammed up when the topic shifted to Epstein’s crimes.

You were Jeffrey Epstein’s driver? You weren’t just his bodyguard and trainer?

Yep.

You drove him in all three places?

In New York, I didn’t drive him. In New York, he had a driver, whatever his name was. He was like old family. I was just training with him in New York and travel with him. And I just drove him here in Palm Beach. Because other places he had different drivers. They’re just personnel, you know, who just drive him. Somebody drive him in New Mexico. Somebody drive him in Virgin Islands, actually. I just drove him here in Palm Beach.

You went with him to all the other properties? Did you go with him to New Mexico also?

Yeah.

You worked with him and traveled with him 24/7 — so that means you were on his plane with him, correct?

Yeah.

You lived in his guest house?

Yeah.

***

Now things get uncomfortable as Zinoviev backpedals on statements he made in 2015.

***

In our conversation in 2015, you described his relationship with teenage girlfriends: “So many time I tried to stop him. I try to tell tell him my opinion about that. He don’t listen to me. That’s the reason why I’m not working for him no more. I make him do that — to let me go.” Do you remember saying that?

It’s not the teenage girls. I never see the teenage girls. I tell you I never see teenage girls.

Plenty of times when I work for him I never see anything unproper or teenage girls around him.

That’s what I say.

So now you say you only saw him with women? Older than 18? 20?

All what I say he has always been with girlfriends and therewas a couple girls — I don’t remember their names. She was 25 and worked for him as assistant. Maybe 25 or 23 — whatever, I don’t know the age.

Okay. But you definitely told me that last time we talked.

No, no. It’s not that. He working like work-release on other stuff. And I just tell him, you know, he would order his girlfriends around, and I told him, “Calm down.” It’s not just teenage girls.

I never see teenage girls in my life at his house. That’s what it is. That’s a misunderstanding. Completely. That’s because — that’s what I’m saying. Most of the time with reporters they give me that kind of questions. “Who told you I see the teenage girls?” I never see the teenage girls in my life. And they said I was —

Here’s another thing you said last time about Epstein and the girls you saw at his house — specifically about moments when you were trying to offer him advice about his conduct: “Sometimes he tries to make a joke. He’d say, ‘Thank you, Grandma. I don’t need your opinion.’ So when you tried to do something good, he would try to make a joke in front of his girls. I never give anyone any questions. It’s one of my rules actually. I be honest with you. I never ask any of my clients what they do for a living or how they do whatever they do. I just do my job, and that’s it.”Do you remember saying that?

Yes, that’s what I say. I feel like the cops watching me whenever he’s on work release — I tell him, “Don’t do stupid stuff.” Like, “[Don’t] put your girlfriend in the car and drive together.

Don’t! Watch it out — all the extra attention.”

Epstein made fun of you in front of the girls, right?

Yeah. Yeah, that was his thing, yeah.

You said you never ask your employers questions.

Yeah. That’s normal answer. People like him just do whatever he wants to do. Because like people talking and just — they already have some release and I understand and just read some papers about his like, whatever, “teenage girls.” But that was [how] he answers. That’s it. So I don’t know.

Here’s another quote from our last interview:“He had a couple girlfriends. They have no idea the degree of what they are doing. But you can’t tell nothing to them. Because they support him kind of. For the while, this one girl can be more attached to him, he just fire her. Fire them and keep them away. For example, I give you some idea: You have private plane and you have three girlfriends and one girl can be more attached to him. And next week — he don’t take that girl. He takes another one, and he just switch them. He brings them on a couple trips and then get different girls. That’s what he doing.”Remember that?

Kind of not!

Igor.

Wait a minute. Wait a minute.

I understand this is sensitive —

It’s not sensitive — it’s just — kind of a little uncorrect.

It’s exactly what you said. I can send it to you. Here’s something else you said: “It could be tricky you know. Normally he always checks his newspapers — ‘Nothing about me?’ I say, ‘No!’ He say, ‘They forget about me?’” And when I mentioned Epstein was being exposed for messing with teenage girls, you said: “I’m not surprised at all. I’m just surprised how low he can be outside the real world. Someday is going to call him and it will be real jail. He have so much money he can pay it off. Me personally, if I caught him with my daughter or something do that — I’m not going to go to police. I do something else. Much worse. That guy could try to sue me and manipulate the situation with his money. That’s the American way. I know he screwed up a lot of fashion girls also. That’s a different story. [Laughs.]”Do you remember saying that?

I remember one thing: I say like, “If I be the father and somebody screw up my daughter, I don’t give shit with how much money he have. I definitely do some bad thing.” That’s what I said. Before that stuff, I don’t know. I’m just really like —

Igor, I’m not making stuff up. I was very careful.

I’m really careful, too.

It was four years ago. You may not remember what you told me. I kept very good notes of what you and I said. It must come across as very harsh. But it’s the truth. I’m happy to understand a little better. He’s not alive. You don’t have anything to be afraid of anymore.

I’m not afraid. Beyond that just he is dead. I don’t want anything to be uncorrect. There’s too much shit in here, you know, already. He’s dead and just like, freaking people, just leave him alone.

Hold on. When did you find out he died?

Saturday or Sunday or whenever.

What did you think when you found that out?

What did I think?

Yeah.

Are you sure you want to hear what I am going to think?

Yeah.

Somebody helped him to do that.

You think somebody helped him kill himself?

Yeah.

Okay. Why?

Listen, you know, that’s going a little too deep.

I mean, I’m just trying to understand that maybe you’d be happy he was dead or you would be upset. I don’t know. Are you even feeling anything?

I’m not sad. I mean, I didn’t have anything against him, like a bad thing, you know? I don’t care about his life completely. I don’t give a, let’s say, like, crap about how he die, how he live, or how he’s managed.

How many years did you live at his house?

Five or six years. In Palm Beach.

That’s a long time.

Yeah.

You don’t have any emotion after learning he’s dead?

No.

Did you think that would happen to him?

It’s unexpectable. Well —

***

One thing you told me, for instance — okay, one thing you told me is he got a heads up when the authorities were going to come to his house the night before.

Listen, what you say is between you and me —

You told me he would get phone calls the night before and eight o’clock the police are going to come. He would get a heads up from local police.

[Silence.]

You told me that, Igor. Want me to read the quote?

Well, you can read whatever you want right now. Don’t just — you can put yourself in big trouble.

You said: “He always do something wrong. There was some nights in question. There was at home arrest and police, before they come to the house, they call him and tell him they coming in at eight o’clock in the morning. It’s all corruption you know. It’s all bullshit.”

Listen, don’t put yourself in trouble. Seriously.

We talked about this.

I understand we got this.

I’m telling you to give you a chance to remember because we talked about this stuff. I know it’s hard. I don’t know what you mean about “put myself in trouble.”

Let that go. Seriously. Let that go.

Why is it so important? Are you worried about the local cops?

Listen, you’re really smart and I’m not going to offer that over the phone right now, okay? You’re really smart. You have no idea. Please!

What do you mean by that?

I can’t explain you. I can’t explain you over the phone any of this.

You said that last time. And we didn’t talk for years. You can tell the world who this guy was. You were with him for a long time. You know what I mean?

[Silence.]

I totally understand that you think he could have had help committing suicide.

First of all, I have to go right now. I have another client.

Still training people?

Yes. But just be careful. I’m not kidding.

What’s your email so I can send you —

Don’t do any kind of that stuff. Just don’t play it. Seriously.

Can you tell me why?

I can’t. I can’t.

May I ask you one more question?

Go ahead.

Have you been talking to anyone in the government, the FBI? Have they come to you?

[Long pause] Um. Great talking to you. Seriously. We talk later.

Really?

Bye.

All right.

Bye.

via ZeroHedge News https://ift.tt/2KPxGh7 Tyler Durden

Once upon a time, the quarterly publication of hedge fund 13F statements was a momentous event, more important even than corporate earnings, creating a frenzy of activity within the buyside community as hedge funds scrambled to figure out who is buying – or selling – what, and what such activity telegraphed about the bigger picture.

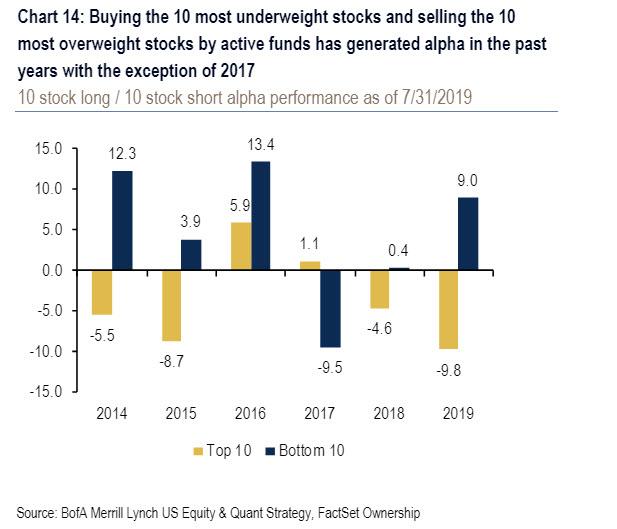

Alas, over the past decade – ever since SAC’s egregious use of “expert networks” made the legal use of inside information impossible and as central banks took over markets – hedge fund returns collapsed, and so did interest in their holdings. In fact, as we showed time after time, the best strategy since 2013 was not going with the crowd but against it, and as noted two weeks ago, going long the most shorted names and shorting the most popular ones has continued to be not only the most consistently profitable, alpha-generating strategy, but in 2019 YTD, the top 10 crowded stocks underperformed the 10 most neglected stocks by 19% YTD, a 5-year record!

Still, whether one uses it to bet with it or – more likely – against it, a list of what hedge funds buy and sell any given quarter is still informative, if for no other reason than to indicate what the prevailing groupthink regurgitates at various idea dinners across Manhattan.

So, courtesy of Bloomberg, the latest batch of 13-Fs revealed that the recent red-hot IPOs were quite popular among the 2 and 20 crowd, as Coatue, Tiger Global, and Viking Global all disclosed the value of their positions in struggling-IPO Uber Technologies while its rival Lyft tried to attract big hedge funds.

In what may have been the biggest surprise, billionaire activist investor Bill Ackman unveiled a new big new bet on Warren Buffett’s Berkshire Hathaway, prompting questions among his investors if they should be paying him… or Buffett? Meanwhile, Berkshire itself boosted its bets on Bank of America and Amazon.com.

Elsewhere, BlueMountain disclosed that it converted most of its stake in the bankrupt utility owner PG&E from common shares to swaps, while David Tepper’s Appaloosa bought some Intelsat and sold its entire Alibaba stake.

Also during the quarter, activist giant Elliott Management added a chunk of Marathon Petroleum to its holdings while exiting Sempra Energy. Casino stocks went out of favor last quarter as D1 Capital Partners and Melvin Capital Management were among funds that trimmed their positions in Wynn Resorts Ltd.

Courtesy of Bloomberg, here are the notable holdings changes for the most prominent money managers as of June 30. Top new buys may include IPOs in which hedge funds may have invested prior to their debut:

ADAGE CAPITAL PARTNERS GP

Top new buys: RTN, DUK, ABBV, CF, TEL, COMM, MDU, GRA, COP, SAP

Top exits: IFRX, EXP, BRKMY, LNG, BLD, TAK, WMB, CE, BMY, CMI

As Henry Markopolos readily admits, GE has reportedly been playing fast and loose with its revenues for decades, which is why thousands of analysts were shocked to see the dogged Madoff whistleblower publish a report Thursday morning warning about ‘Accounting Irregularities’ at the once-mighty industrial conglomerate, which amounted to almost $40 billion.

Markopolos continued that the fraud growing inside GE was “bigger than Enron and Worldcom combined” (which is difficult to imagine given GE’s relatively puny market cap), and that most of the dirt could be found within its insurance unit, which will need to bolster its reserves by $18.5 billion in cash, and faulted the way the company is accounting for its oil-and-gas business. All told, he said, the accounting problems amount to $38 billion, or 40% of the conglomerate’s market value.

But in a tough interview with CNBC Thursday morning, Markopolos defended his findings, all while repeatedly refusing to disclose with whom he is working (It’s reportedly a US-based mid-sized hedge fund)

“Years ago, I would sit down at analyst luncheons and everybody would joke about GE and how they were cooking their earnings under Jack Welch then of course again under Immelt…GE took off like a rocket under take numbers (that is, until the crisis).”

Everybody said, “it’s 3% of the S&P 500, we should benchmark it because if we only have 1%, then we’d be short 2% after it took off like a rocket under fake numbers.

But what is Markopolos seeing right now that the rest of Wall Street has missed?

“The numbers are missing. They report top line revenues, bottom line profits, and nothing in between, expenses, research and development, selling, general administration costs – including cash flows, they don’t provide working capital, in fact GE is the only company in its industry that doesn’t provide working capital, in fact, GE’s working capital is minus $23 billion, if you search for current ratio in their annual ratio it doesn’t appear – name another company that does that…it’s accounting 101,” he said.

How severe is the problem? Serious enough to push it into bankruptcy? Yes, Markopolos says.

“They took a $15 billion reserve hit in Jan 2018 for long term care they have another $18.5 billion in immediate cash needs for reserves, they also have a $10.5 billion non-cash reserve hit they need to take on their GAAP books that’s going to be a loss and destroy their equity ratios and it needs to be done before Q1 2021 when new accounting rules take place.

He also explained how he went through the statutory filings for 8 GE reinsurance counterparties for long term care and pulled the regulatory filings for the years 2013-2018 and saw “all the losses falling onto GE’s books.” “GE is losing $5.27 for each dollar of premium they’re taking in.”

“Those losses are unsustainable and they’re growing at an exponential rate. That’s not going away…and it’s probably going to make this company file for bankruptcy.”

But if GE’s insurance liabilities take place over several decades, why take a charge for that now?

“Usually you reserve in advance so you can invest the money in the bond market and earn returns on it so you have the money to pay claims when they come due…and if you want to compare it to Unum…Unum’s loss ratio for 2018 was 90%, which means they took in $1 of premiums and paid out 90 cents so they were profitable…for Prudential, 81%…for GE, 527% – many times greater. It’s unsustainable and it’s growing.”

A lot has changed since the Enron and Worldcom scandals…what about the auditors, and boards…were all of these people missing the mark here?

“Yes, the gatekeepers have consistently failed…look at the Ratings Agencies during the financial crisis.” Markopolos also didn’t speak with the company before publishing his report so they wouldn’t start destroying evidence.

Markopolos said he’s pursuing GE because the shareholders deserve to know…but also because he needs to get paid. “I have a family to support.”

Finally, as the interview wound down to a close, Markopolos offered a bizarre explanation for his decision to go after GE: It’s recent move of its headquarters near Boston from Fairfield, Conn. “When you move to my home town, and you’re running a scam, I’m going to come after you.” And while Markopolos’s ‘nobody commits accounting fraud in my backyard’ sounds convincing, we’d certainly feel better knowing for whom Markopolos is working, and what their angle is, considering that betting against GE is nothing knew.

via ZeroHedge News https://ift.tt/2H8vEb3 Tyler Durden

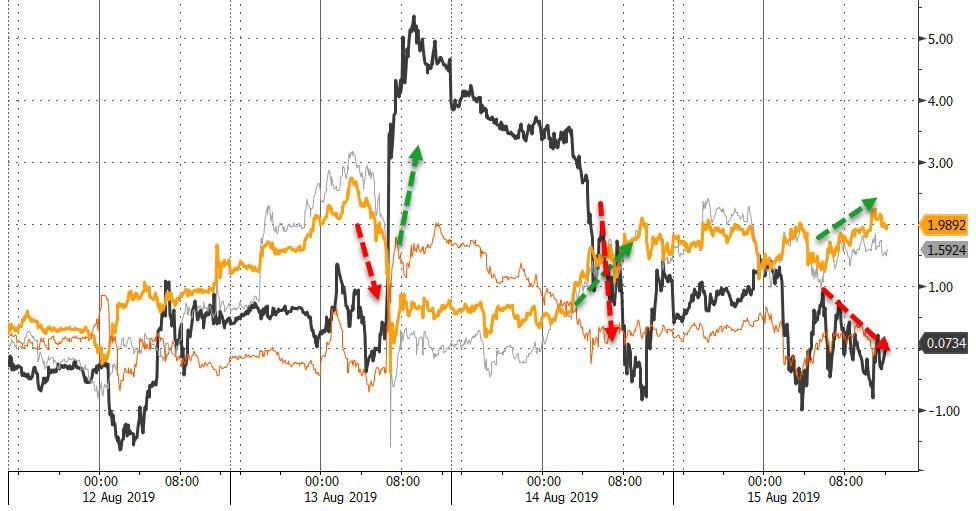

10Y Yield just plunged back below 1.50%, and 30Y yields are pushing new record lows at 1.93% as stocks give up early gains dumping into the red… no immediate catalyst but the combined move suggests a major delevering in risk-parity.

It’s a bond bear bloodbath…

Source: Bloomberg

And stocks are also puking their gains…

Pushing VIX above 23…

Paging Steven Mnuchin…

via ZeroHedge News https://ift.tt/2Zagk3D Tyler Durden

{kind=link}