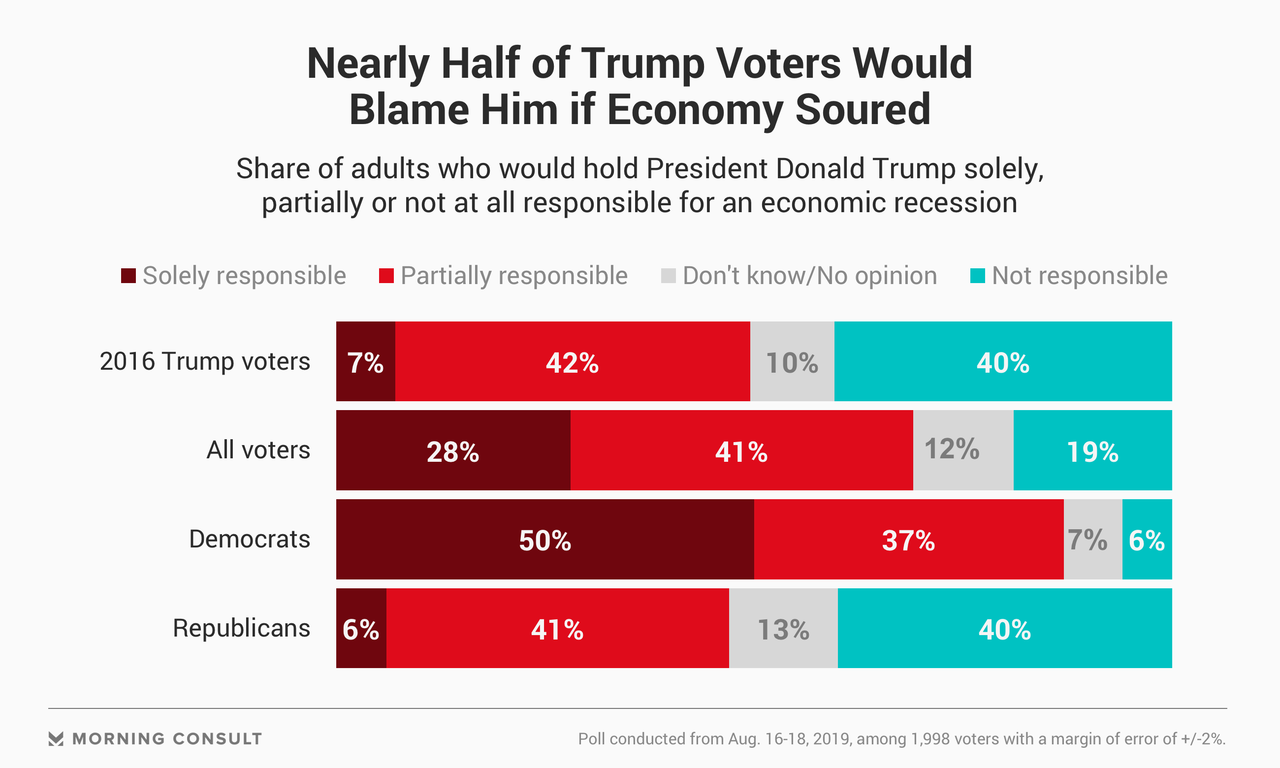

While President Trump continues to tout the strength of the US economy – and take credit for it, he is no doubt keenly aware that a recession before the 2020 election would put a dent in his chances for reelection.

To that end, a new poll by Morning Consult found that 42% of Trump voters would hold him at least partially responsible for an economic downturn, while 7% say it would be all his fault. Meanwhile, the poll revealed that Trump has a 48% approval rating on the economy.

Perhaps that’s why he’s continued to push for rate cuts and tax cuts; an attempt to avoid the economic chaos which liberal HBO host Bill Maher is praying for in the hopes of ushering in a Democratic president in the next election.

Still, Trump appears confident that the wheels won’t fall off the economy anytime soon.

“I don’t think we’re having a recession,” he said on Sunday. “We’re doing tremendously well.”

That said, Trump also floated an idea during Oval Office comments this week that he may temporarily cut payroll taxes to temporarily boost the economy, while also slamming the Federal Reserve for abdicating its duties by not approving a large interest rate cut.

“So Germany is paying Zero interest and is actually being paid to borrow money, while the U.S., a far stronger and more important credit, is paying interest and just stopped (I hope!) Quantitative Tightening,” he tweeted on Wednesday.

So Germany is paying Zero interest and is actually being paid to borrow money, while the U.S., a far stronger and more important credit, is paying interest and just stopped (I hope!) Quantitative Tightening. Strongest Dollar in History, very tough on exports. No Inflation!…..

Meanwhile, as Morning Consult notes, “Data is starting to pile up that an economic downturn could be coming sooner rather than later. Economists surveyed by the National Association for Business Economics expect a recession in 2020 or 2021.”

via ZeroHedge News https://ift.tt/2PbGCms Tyler Durden

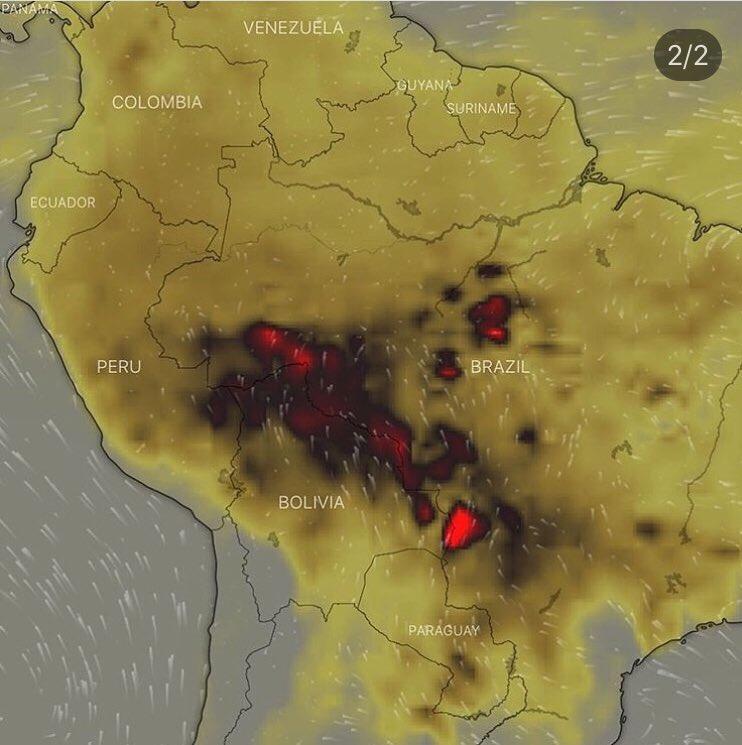

This week the skies above Brazil’s largest city turned black in the middle of the afternoon due to the massive wildfires that are currently raging in that country. But the wildfires aren’t actually happening anywhere near São Paulo. In fact, the smoke that turned the skies black actually came from fires that were happening more than 1,000 miles away. Can you imagine how powerful the fires have to be in order to do that?

And it isn’t just Brazil – right now horrific fires are scorching vast stretches of our planet from South America all the way up to the Arctic. Some of the fires are producing so much smoke that you can actually see it from space. And in the process, irreversible damage is being done to our ecosystems.

I know that this number is hard to believe, but there have been more than 72,000 wildfires in Brazil so far in 2019, and most of those fires are happening in the Amazon rainforest. I understand that many of you may not care what happens in Brazil, but you should. Approximately 60 percent of the entire Amazon rainforest is in Brazilian territory, and that rainforest produces approximately 20 percent of all the oxygen in our atmosphere. So essentially the “lungs of the Earth” are being burned away right in front of our eyes…

The fires are burning at the highest rate since the country’s space research center, the National Institute for Space Research (known by the abbreviation INPE), began tracking them in 2013, the center said Tuesday.

There have been 72,843 fires in Brazil this year, with more than half in the Amazon region, INPE said. That’s more than an 80% increase compared with the same period last year.

The Amazon is often referred to as the planet’s lungs, producing 20% of the oxygen in the Earth’s atmosphere.

Every minute of every single day, an average of 1½ soccer fields of Amazon rainforest are being wiped out. This is an ongoing crisis that hasn’t been getting nearly the attention that it deserves in the United States.

But when the skies above Sao Paulo suddenly turned completely black at three in the afternoon on Monday, that set off a social media frenzy…

São Paulo’s skies were blackened for roughly an hour at around 3 p.m. Monday due to raging fires throughout the region and weather conditions that pushed particulate matter over the city, setting off intense speculation on social networks about the reason why the day was seemingly transformed into night.

Videos and images posted by local residents depicted disturbing scenes of pedestrians walking under black skies and cars driving in the mid-afternoon with their headlights on as the continued fires throughout the Amazon rainforest drove the hashtags #PrayforAmazonia and #PrayforAmazonas to worldwide viral status.

Sadly, these fires are not going to end any time soon. It is being reported that more than 9,000 fires are raging at the moment, and it is being estimated that 640 million acres have been affected by those fires.

Multiple fires are burning near the state’s biggest city, and firefighters have called in assistance from the Lower 48. More than 400,000 acres are currently burning, and one of the biggest concerns is the McKinley Fire, which has destroyed at least 50 structures about 100 miles north of Anchorage. Officials with the Matanuska-Susitna Borough declared a state of emergency, and firefighters hoped that calmer weather predicted for Wednesday could permit evacuees to return.

When I think of Alaska, I think of a place that is bitterly cold. But apparently it is hot enough this year for wildfires to sweep across hundreds of thousands of acres.

And we are also witnessing highly unusual wildfires in the Arctic in 2019…

The Arctic as a whole has seen unusually high wildfire activity this summer, Parrington said, including areas such as Greenland that typically don’t see fires. One estimate found that the amount of carbon dioxide emitted from fires burning within the Arctic Circle in in June 2019 was greater than all of the CO2 released in the same month from 2010 through to 2018 put together.

To me, it is very strange to be talking about “wildfires in the Arctic”, but we have entered a period of time when our entire definition of “normal” is going to change. Last winter we experienced one of the coldest winters in ages, during the first half of this year the middle of the U.S. experienced unprecedented rainfall and flooding, and now we are being told that last month was the hottest July ever recorded…

The average global temperature in July was 1.71 degrees F above the 20th-century average of 60.4 degrees, making it the hottest July in the 140-year record, according to scientists at NOAA’s National Centers for Environmental Information.

The previous hottest month on record was July 2016. Nine of the 10 hottest recorded Julys have occurred since 2005; the last five years have ranked as the five hottest. Last month was also the 43rd consecutive July and 415th consecutive month with above-average global temperatures.

Unfortunately, many believe that this is just the beginning. Global weather patterns are going haywire, and so the extremes that we have seen so far may just be the tip of the iceberg.

The environment that we depend upon for life every moment of every day is being shaken, and many are deeply alarmed about what is happening to the Earth. Each day it is being destroyed a little bit more, and the clock is ticking…

via ZeroHedge News https://ift.tt/2TThYG4 Tyler Durden

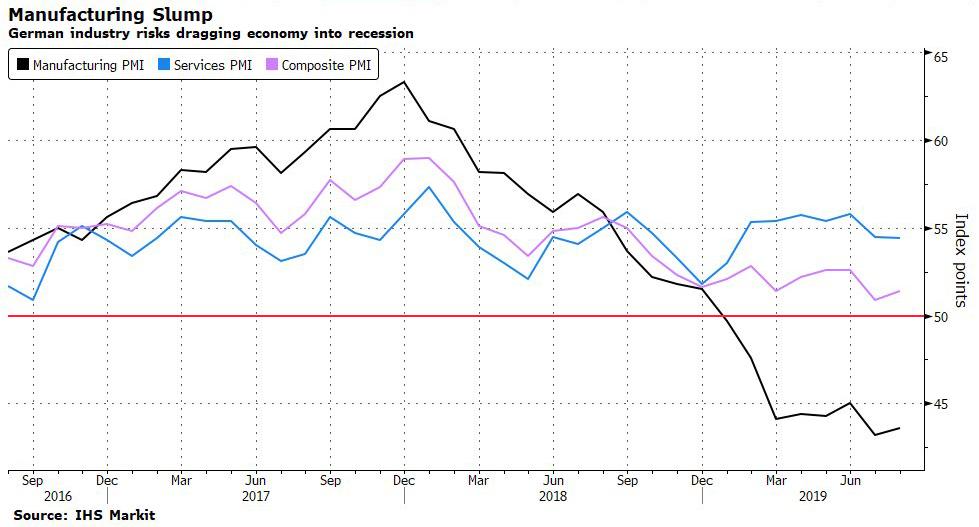

There was some good and some not so good news in today’s German PMI data.

First, the good: the composite PMI rose 0.5pt to 51.4, beating expectations of another decline, and led by modest gains in the manufacturing output subcomponent even as the services PMI showed a marginal decline.

However, the underlying indices were more subdued, with new orders and employment falling more. The press release also noted a sharp fall in business expectations in the services sector. Backlogs of work across both sectors fell for a 10th month and the pace of hiring slowed, with employment in manufacturing declining at the fastest pace in seven years.

Perhaps more concerning was the outlook, which is now outright recessionary as for the first time since 2014, more companies now expect output to fall than rise over the next 12 months.

The problem for Germany is that with its manufacturing sector contracting at a dismal rate, Europe’s most powerful economy has no buffer left – as a reminder, last week we learned that the economy shrank in the second quarter and real-time sentiment indicators confirm that another contraction in Q3 is virtually inevitable, guaranteeing a technical recession.

The persistent German weakness, driven in particular by mounting global trade tensions, car industry woes and slowing demand in China, certainly doesn’t bode well for the broader euro area. The silver lining: whereas European manufacturing is now screaming recession, at least services remain well in expansionary territory. However, with the spread now at all time highs, it is only a matter of time before services tumble.

Indeed, while the headline German composite PMI unexpectedly rebounded modestly in August to 51.4 from 50.9, the manufacturing index remained far below 50, signaling a seventh month of contraction.

Meanwhile, analysts continue to clamor for Merkel to do something besides lip service to the coming recession, and unleash fiscal stimulus: “Somehow they are not looking at this data,” said ING economist Carsten Brzeski. “The German government should react. We have this stagnation of the entire economy now and we really need some fiscal stimulus.”

Well, the German government said it will react – we just need a deep recession first, and one is clearly approaching right on schedule. One reason Germany may ignore the issue is because the ECB is already “on top” of it, with the central bank widely expected to add monetary stimulus as soon as next month by cutting rates and/or restarting QE.

Commenting on the latest dismal data out of German, Bloomberg’s chief European economist showed a trace of optimis, saying “there’s a little light at the end of the tunnel for Germany’s economy. The PMI — a trusted gauge of economic activity — picked up a little in August. The big risk is that a fresh blow to manufacturing materializes — the U.S. goes ahead with tariffs on EU car exports, for example — or that weakness in the industrial sector spreads to services.”

Others, however, were far more pessimistic: “Germany remains a two-speed economy, with ongoing growth of services just about compensating for the sustained weakness in manufacturing,” according to Markit’s Phil Smith. “Although improving slightly, the survey’s output data haven’t changed enough to dispel the threat of another slight contraction in gross domestic product in the third quarter.”

via ZeroHedge News https://ift.tt/30qE1X5 Tyler Durden

The European PMIs that were released earlier today beat forecasts. And it felt positively quaint when the euro and bund yields rose to their respective highs of the day. If that is all it takes to change the mood, then economists should be enlisted to keep low-balling any economic estimates. Algorithms can be forgiven for reacting to the prints. No human trader should have been doing anything else besides fading the move for better intraday trade location.

That’s harsh. But it reflects two realities.

The market fully expects central banks to be dovish.

And the market is relying on that fact for its investing thesis.

Yet deep down inside, investors worry, probably even know, that further monetary policy stimulus will be of dubious value in actually getting the global economy moving at a quicker pace. Expensive money is not what ails us.

Trading volumes remain, understandably, very low. Earlier in the week, that didn’t mean there weren’t things to be learned from the price action. Whatever today brings should probably be taken with a little bit more wariness. Traders have a tendency to talk themselves into all sorts of notions when the event they have been preparing for suddenly looms.

A few days ago, everyone was sure exactly what Fed Chairman Jerome Powell was going to say and what the central banks were going to do. Today will be about traders torturing themselves by questioning those assumptions. Whether they have been right or wrong in formulating their expectations, nothing in Wednesday’s Fed minutes nor this morning’s PMIs will change what ends up happening in September.

Having said that, the short end of the Treasury curve is probably right in being just a little bit more circumspect about pricing beyond next month. Emphasis on the word “just.” There has been a lot built into expectations that go well beyond data-dependence. And there are plenty of domestic and international challenges that are very much known unknowns. Some of which, it would seem, can change on a whim or political expediency.

Whatever path markets take to get there, they have confidently assumed that the central banks are very focused on asset prices and will try to maintain their buoyancy. That will get harder to accomplish over time. But timing is everything.

The euro is the most interesting currency trade of the day. It needs to start holding up for more than short bursts of time or risks taking a new look at year-to-date lows. I guess it will wait until after the G-7 to decide what it is going to do. But it is really just hanging on. It seems even more in play than the dollar, which refuses to break out higher but also doesn’t back off. It’s becoming a frustrating exercise to trade. The yen is also worth keeping a close eye on. It’s hard to find anyone who isn’t bullish on it, which raises the question, why isn’t USD/JPY lower? Maybe it, rather than the euro, will decide which way the dollar indexes end up going.

If looking for a canary in the coal mine, given all of the interest-rate assumptions that current market pricing is based on, watch gold.

It keeps looking longingly at its support zone, which isn’t something one would normally expect with everything else going on.

via ZeroHedge News https://ift.tt/31RO47G Tyler Durden

Most Americans could be forgiven for thinking that the ‘trade war’ is really only impacting the US and (maybe) China. After all, it was President Trump’s belligerent rhetoric about holding China accountable that helped him win in 2016 in the first place. But what is less known, is that Trump’s angry trade rhetoric aggravated a bunch of other longstanding trade spats, most notably, the now-emergent trade spat between Japan and South Korea, which is threatening to seriously disrupt trade throughout the Pacific Rim region.

Now, according to the Nikkei Asian Review, in the latest sign of how the relationship between the two countries has deteriorated, South Korea has decided not to extend an intelligence-sharing agreement with Japan.

The decision was reportedly made at a National Security Council meeting on Thursday at South Korea’s “Blue House.” South Korea said it no longer believes the agreement is “in its national interest” after Japan excluded South Korea from the “so-called” “White Countries’ list”.

Kim Yu-keun, the National Security Office’s deputy director, said: “We thought that it is not in our national interest to maintain the agreement,” adding that, “We will inform the Japanese government through diplomatic channels by the deadline of the extension, according to the agreement.”

Kim said: “The government estimated that the Japanese government caused a critical change in the circumstances of security cooperation between the two countries by excluding our country from the so-called white countries’ list…with no clear evidence, on Aug. 2.”

The timing of the pact’s termination is also interesting because of North Korea resuming its short-range missile tests, as well as its threats to call off peace talks with the South and the US.

Yoshihide Suga, Japan’s chief cabinet secretary, late last month said that Tokyo wanted to maintain the pact, known as the General Security of Military Information Agreement.

The neighbors signed the agreement in 2016 out of a desire to cooperate in the face of an increasing threat from North Korea. The agreement stipulates how the countries can share military intelligence.

SK’s decision not to extend the pact follows a meeting between the two countries foreign ministers in Beijing, where South Korean Foreign Minister Kang Kyung-wha demanded that Japan rescind its decision.

The decision came one day after South Korean Foreign Minister Kang Kyung-wha met with her Japanese counterpart, Taro Kono, in Beijing. South Korea’s foreign ministry said Kang had expressed regret in regard to Japanese Prime Minister Shinzo Abe’s decision to exclude South Korea from its “whitelist” of trusted trading partners earlier this month. She urged Tokyo to withdraw the decision that makes it more cumbersome for South Korean companies to import certain materials from Japan.

Unsurprisingly (since NAR is a Tokyo-based business newspaper), most of the analysts quoted in the piece seem to think South Korea’s decision is a bad idea.

Analysts say Seoul should be careful about escalating the feud to include the intelligence agreement, which benefits both countries.

“We had better keep the agreement,” Lee Su-hoon, a professor at Kyungnam University and a former ambassador to Japan, said at a forum. “We need military information. However, sharing high-class information should be based on trust.”

Leif-Eric Easley, a professor at Ewha University in Seoul said in the report: “The Moon government may see this decision as domestically popular and as a symbolic, low-cost way of signaling resolve to Tokyo. However, this move will raise international concerns that Seoul misreads the regional security situation and is presently unwilling to shoulder its responsibility for improving Korea-Japan relations.”

The relationship between the two countries has been deteriorating since even before a South Korean court ruled that Japanese companies must pay reparations to Koreans forced to work in Japan during WWII, which Japan has claimed goes against a treaty signed in 1965, that supposedly settled the issue of war reparations.

via ZeroHedge News https://ift.tt/2ZluhMv Tyler Durden

Elon Musk may have finally secured some of that precious financing he once claimed to have secured (roughly one year ago), though, according to a report in German business magazine Manager, things didn’t turn out quite like he had hoped.

Per the magazine, Tesla is getting ready for a takeover, perhaps by Volkswagen, as carmakers scramble to roll out rival electric cars.

Of course, given Musk’s track record, it’s important to take this news with a grain of salt – but Tesla shares are ripping higher in the premarket.

via ZeroHedge News https://ift.tt/2P77NPr Tyler Durden

US equity futures drifted lower, tracking European and Asian stocks in the red as uncertainty over the outlook for interest rate cuts following the release of the FOMC minutes kept investors on edge, while few traders were willing to trade in size with the Jackson Hole meeting set to begin. The yen and dollar jumped as the euro dropped and the yuan tumbled, while Treasuries edged higher with oil, while gold dipped.

The euro and German yields initially nudged initially higher after better-than-expected PMI readings in the euro area helped offset some fears of an imminent European recession. The moves were modest, however, and gains quickly faded as the manufacturing readings remain challenging (especially in Germany).

Some details on the latest PMI report from Goldman:

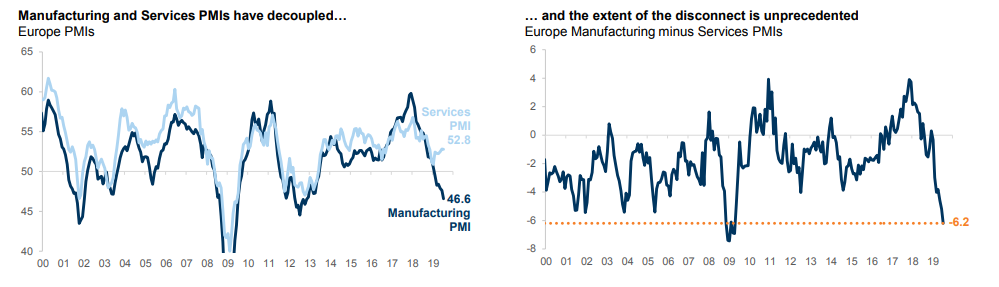

The Euro area Flash composite PMI was up three-tenths in August, against expectations of a decline. The gain only partially offset the decline in July. The breakdown of the Euro area PMI showed a small increase in the services PMI (+0.2pt to 53.4) and a larger one in the manufacturing PMI (+0.5pt to 47.0). Within the manufacturing PMI, employment, new orders and output were higher than their July levels, but remain in contractionary territory.

At the country level, the French PMIs recorded gains across all subcomponents, helping to push the composite PMI up 0.8pt to 52.7. New orders increased in both the service and manufacturing sectors. In Germany, the composite PMI rose 0.5pt to 51.4, led by modest gains in the manufacturing output subcomponent. The German services PMI showed a marginal decline; however, the underlying indices were more subdued, with new orders and employment falling more. The press release also noted a sharp fall in business expectations in the services sector.

And visually:

As a result, after the glow faded from euro-area PMIs, investors again sought safer assets, pushing Treasuries higher while the yen hit a fresh daily high amid a flight to safe havens. The moves came after South Korea said it would withdraw from an intelligence-sharing agreement with Japan and a senior EU official says discussions with U.K. Prime Minister Boris Johnson suggest a no-deal Brexit is likely. Italy’s FTSE MIB (+0.4%) was kept afloat as Italian President Mattarella holds a barrage of talks with party leaders in search of a coalition to fill the country’s political void in order to pass the 2020 budget later this year. Meanwhile, UK’s FTSE 100 (-0.5%) marginally lags its peers as heavyweight tobacco stocks (Imperial Brands -1.0%, British American Tobacco -1.4%) weigh on the index amid news that the US House Energy and Commerce Committee launched a probe into four e-cigarette companies, British American Tobacco, Atria Group (MO), Japan Tobacco (2914 JT) and Reynolds American; seeking information on Cos’ research into public heath impacts, marketing practices and promotion of e-cigarette use by adolescents.

As a result, Europe’s STOXX 600 index fell 0.1% in choppy trade, following a 0.5% drop in MSCI’s broadest index of Asia-Pacific shares outside Japan. The MSCI world equity index was down 0.1%.

Earlier in the session, Asian stocks dropped for a second day, led by energy and utility firms, as traders awaited a Friday address by Federal Reserve Chairman Jerome Powell. Markets in the region were mixed, with India retreating and Malaysia climbing. The Topix closed little changed, as chemical producers advanced and electronic companies slipped. The Shanghai Composite Index edged up 0.1%, supported by Kweichow Moutai Co. and China International Travel Service Corp. The Hang Seng Index fell 0.8%, with Hong Kong-listed stocks facing their worst earnings decline since 2008. India’s Sensex fell for a third day, dragged down by Reliance Industries Ltd. and HDFC Bank Ltd. The country needs a “significant” fiscal package, a gradual decline in the rupee and more liquidity for the shadow-banking system to ease tight financial conditions, according to Bank of America Merrill Lynch.

While it didn’t impact markets on Wednesday, when US equities posted notable gains, minutes of the Fed’s July meeting showed deep splits among policymakers over whether to cut interest rates last month, though there was some unity in wanting to signal it was not on a preset path to looser policy. The Fed cut rates by 0.25% in July. While a “couple” of Fed members supported a deeper cut of half a percentage point, “several” favored no change at all. That reluctance to loosen policy seems at odds with the expectations for a cut of over 100 basis points by the end of 2020 that are already priced into markets.

Strategists said that the minutes reflected a dissonance between expectations for cuts – fueled by geopolitical concerns such as U.S.-China trade tensions and economic weakness in major economies such as Germany – and the apparently solid fundamentals of the U.S. economy.

“The update last night was a bit of a reality check – maybe don’t get ahead of yourself on what the Fed is going to do,” said David Madden, market analyst at CMC Markets. “If you forget about the geopolitical headlines, forget about what the bond markets are doing, and look at the underlying indicators of the U.S. … people are in jobs, earning decent money, and more importantly spending money.”

But beyond the United States, worries about the fragility of the global economy were evident in data from Europe on Thursday. Germany’s private sector continued to struggle in August, suggesting further that Europe’s largest economy is heading for a recession after its economy shrunk between April-June. Euro zone business growth expectations also fell to their weakest in more than six years on trade war fears, even as the expansion picked up a touch in August.

In FX, the slump in the yuan dragged it to an 11-year low, which also sapped appetite for risk, with dealers saying state-owned banks were seen selling dollars to support the yuan.

The Fed minutes also raised the stakes for Chairman Jerome Powell’s speech on Friday at the Fed’s annual policy retreat in Jackson Hole, Wyoming – an event that investors are waiting for with bated breath hoping for some clarity on the Fed’s intentions. U.S. President Donald Trump has been urging larger rate reductions, with proponents of looser policy pointing to the need to lift inflation toward the Fed’s target and thwart fallout from global trade tensions. And those trade worries played out again in currency markets, where the fall in onshore China’s yuan to 7.0752 per dollar, its lowest since March 2008, promoted a rush to perceived safe-haven assets such as the Japanese yen. The yen advanced by 0.2% to 106.41 yen, nearing last week’s eight-month low of 105.05 yen. The euro slipped to a daily lows as commodity and Scandinavian currencies deepened losses.

Currency traders said that while the Chinese economy’s slowing growth meant pressure had been building on the renminbi from long before, the new fall suggested Beijing was prepared to use the currency as leverage as trade tensions simmer.

“This indicates that this is an instrument of the Chinese government in the trade war. It is allowing for renminbi weaknesses,” said Thu Lan Nguyen, FX strategist with Commerzbank in Frankfurt. “It is an indication that they are expecting the trade war to continue, to last longer than they anticipated last year.”

In geopolitics, North Korea carried out live fire drills by bombing replicas of South Korea’s F-15K fighter jets, surface to air missiles and a radar. Across the border, South Korea stated they will not be renewing their intelligence accord with Japan, according to the Blue House. Iran displayed a new locally built mobile missile defence system, reported via Iranian news agencies. Iranian Foreign Minister Zarif says he is prepared to work on France’s proposals regarding a nuclear deal.

In commodities, oil prices dipped on worries about the global economy and bigger-than-expected buildups in oil product inventories in the United States, the world’s biggest oil consumer. Brent crude futures rose 0.3%, or 18 cents, to $60.48, while U.S. crude gained 23 cents to $55.91 a barrel.

Expected data include jobless claims and PMIs. Gap, Intuit, Salesforce, and VMware are among companies reporting earnings.

Market Snapshot

S&P 500 futures unchanged at 2,929

STOXX Europe 600 down 0.4% to 374.24

MXAP down 0.3% to 152.02

MXAPJ down 0.5% to 492.13

Nikkei up 0.05% to 20,628.01

Topix up 0.04% to 1,498.06

Hang Seng Index down 0.8% to 26,048.72

Shanghai Composite up 0.1% to 2,883.44

Sensex down 1.1% to 36,660.18

Australia S&P/ASX 200 up 0.3% to 6,501.81

Kospi down 0.7% to 1,951.01

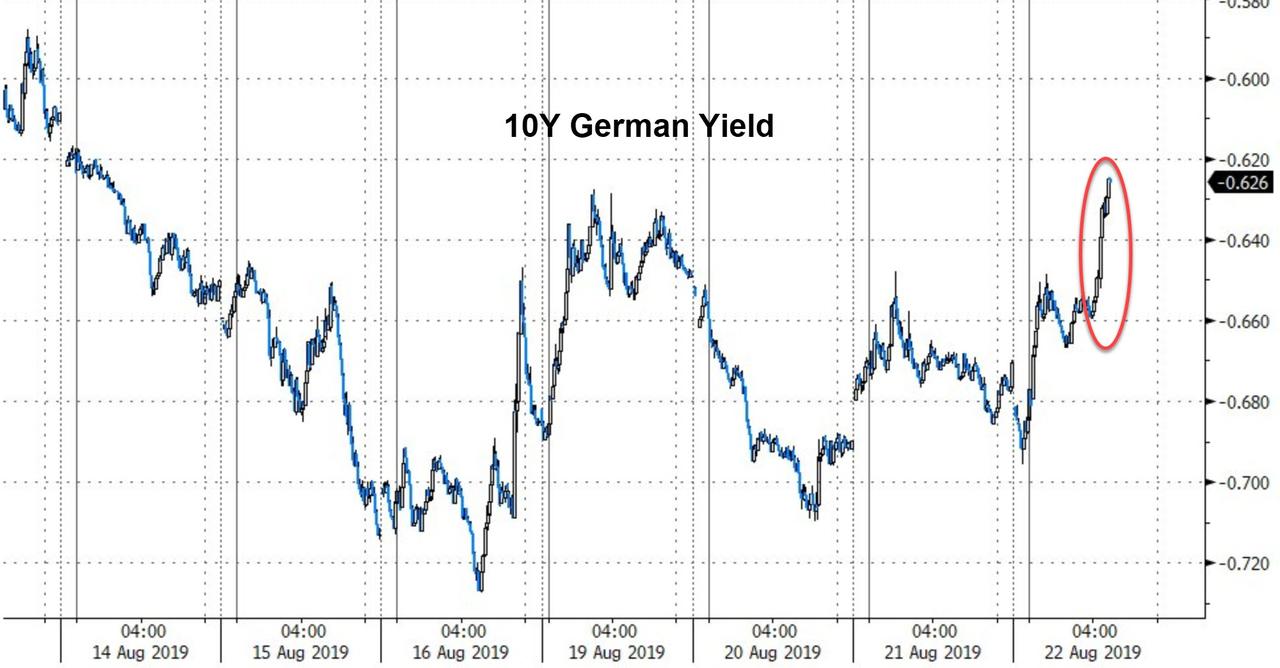

German 10Y yield rose 1.3 bps to -0.657%

Euro up 0.2% to $1.1102

Italian 10Y yield fell 3.9 bps to 0.985%

Spanish 10Y yield rose 1.2 bps to 0.109%

Brent futures up 0.2% to $60.44/bbl

Gold spot down 0.2% to $1,499.52

U.S. Dollar Index little changed at 98.24

Top Overnight News

German manufacturers are reinforcing concern that Europe’s largest economy is headed into a recession. A nationwide gauge showed orders at factories and services companies dropping at the fastest pace in six years, and more companies now expect output to fall than rise over the next 12 months. That’s the first time that’s happened since 2014, according to the Purchasing Managers’ Index from IHS Markit

Federal Reserve officials viewed their interest-rate cut last month as insurance against too-low inflation and the risk of a deeper slump in business investment stemming from uncertainty over President Donald Trump’s trade war.

Angela Merkel’s challenge to Boris Johnson to find a Brexit solution in the next 30 days sounds impossible. But while both sides are talking tough, officials in private say there’s still time to salvage a deal

The prospects for forming a new coalition in Italy improved after the first day of consultations as most of the smaller parties and independent lawmakers told Mattarella they’re against a snap election and would eventually favor a new government.

The French government expects the U.K. to leave the European Union without a withdrawal agreement, an official in President Emmanuel Macron’s office said, meaning the immediate imposition of border controls after Brexit at the end of October

The IMF executive board recommended removing the age- limit for the fund’s managing director, paving the way for Kristalina Georgieva the European Union-backed candidate to replace Christine Lagarde

Oil climbed as attention turned from expanding American fuel stockpiles to the prospects for monetary easing as the world’s top central bankers gather in Jackson Hole, Wyoming

South Korea said it would withdraw from an intelligence-sharing agreement with Japan, extending their feud over trade measures and historical grievances into security cooperation.

Italy’s President Sergio Mattarella will meet with the country’s main political leaders on Thursday in an effort to carve out a viable governing coalition after Rome’s government – – an alliance between the hard-right League and the anti- establishment Five Star Movement — collapsed earlier this week

Asian equity markets traded mixed as the region failed to sustain the early momentum from Wall St where sentiment was underpinned by strong retailer earnings and after the FOMC minutes did little to alter the landscape as they showed a divide among officials on rate cuts. ASX 200 (+0.3%) and Nikkei 225 (U/C) were both higher at the open with tech and energy the outperformers on the busiest day of the earnings season in Australia, while Tokyo trade was less decisive as price action eventually reflected a choppy currency and after a lack of progress in talks between Japanese and South Korean Foreign Ministers to resolve the ongoing spat. Hang Seng (-0.8%) and Shanghai Comp. (+0.1%) were subdued amid CNY weakness and as Hong Kong’s property sector suffered the brunt of the Hong Kong protests with developers said to be reducing prices to support sales, although losses in the mainland have been cushioned by the PBoC’s liquidity efforts. Finally, 10yr JGBs were initially unchanged amid similar uneventful trade in T-notes, but later saw mild support after firmer demand at the enhanced liquidity auction for long end JGBs and as risk tone began to deteriorate.

Top Asian News

Hong Kong Faces Worst Earnings Recession Since 2008 Crisis

Indonesia Surprises With Second Rate Cut to Support Growth

Hedge Fund Outflows of $55.9 Billion Make Dismal 2018 Look Good

European stocks have given up the earlier PMI-induced gains [Eurostoxx 50 -0.1%] as the sentiment seen from firmer EZ metrics across the board failed to persist, and amid little follow-through from FOMC Minutes. Italy’s FTSE MIB (+0.4%) is kept afloat as Italian President Mattarella holds a barrage of talks with party leaders in search of a coalition to fill the country’s political void in order to pass the 2020 budget later this year. Meanwhile, UK’s FTSE 100 (-0.5%) marginally lags its peers as heavyweight tobacco stocks (Imperial Brands -1.0%, British American Tobacco -1.4%) weigh on the index amid news that the US House Energy and Commerce Committee launched a probe into four e-cigarette companies, British American Tobacco, Atria Group (MO), Japan Tobacco (2914 JT) and Reynolds American; seeking information on Cos’ research into public heath impacts, marketing practices and promotion of e-cigarette use by adolescents. Moreover, broker downgrades for BHP (-1.7%), Anglo American (-2.0%) and Rio Tinto (-0.4%) adds further pressure on the index. Sectors are almost all in the red with cyclical stocks faring worse than defensives, in-fitting with the current risk tone. In terms of individual movers, Thyssenkrupp (+5.4%) shares jumped to the top of the Stoxx 600 amid reports that parties interested in Co’s elevator unit include Advent, Apollo, CVC, Carlyle, KKR and possibly EQT, according to Manager Magazin. Meanwhile, BBVA (+1.3%) and Caixabank (+1.7%) benefit from broker upgrades at HSBC

Top European News

Italy’s President Enters High-Stakes Talks in Bid to End Crisis

Osram Board Agrees AMS Can Make Offer to Rival Bain- Carlyle

Distressed-Debt Hedge Fund Mudrick Starts Expanding Into Europe

In FX, the euro was Not the strongest G10 currency, but the Euro perked up in wake of the flash Eurozone PMI surveys that were firmer than forecast across the board. Eur/Usd started to climb after the French preliminary prints and then crossed 1.1100 and beyond when German and pan headlines maintained the recovery trend, but faded again before testing offers reportedly waiting at 1.1120. Note also, hefty option expiries between 1.1095 and the big figure may be exerting a gravitational pull given 1.65 bn rolling off at the NY cut.

GBP/JPY – The other major outperformers as the Dollar continues to drift post-FOMC minutes that failed to provide any further or clearer insight on guidance for the September policy meeting. Indeed, the DXY remains tightly bound just above the 98.000 handle and inside relatively narrow confines for the week so far (between 98.451-115), awaiting Fed chair Powell for clearer pointers (hopefully) at Jackson Hole on Friday. Meanwhile, Sterling is still seemingly taking the positive view that there is time left (albeit limited and decaying) to resolve the Irish backstop stalemate and reach some sort of Brexit deal before October 31, with Cable keeping its head above 1.2100, but capped by the 21 DMA circa 1.2154 and Eur/Gbp pivoting 0.9150 even though the single currency is underpinned as noted above. Elsewhere, the safe-haven Yen retains an underlying bid around 106.50 amidst ongoing global trade and geopolitical tensions after tough talks between the US and Japan failed to produce a breakthrough and SK not renewing its intelligence sharing agreement with Japan.

NZD/AUD/CAD – All on the backfoot vs their US counterpart as the Kiwi loses more ground after failing to sustain recovery momentum above 0.6400 and the Aussie likewise following fleeting bounces over 0.6800, but also undermined by CBA PMIs overnight showing sub-50 manufacturing and composite readings. The Loonie is holding up a bit better after Wednesday’s frothy Canadian CPI, but unable to rally too far beyond 1.3300 ahead of wholesale trade data later today.

SEK/NOK – Also weaker, partly on fundamentals and technically as Swedish unemployed jumped in SA terms and Norway trimmed its Q3 oil investment estimate, with Eur/Sek back up above 10.7000 and Eur/Nok hovering nearer the top of 9.9550-9145 trading parameters against the backdrop of faltering risk appetite.

EM – Widespread losses against the Greenback, but Cnh and Try depreciation looks particularly eye-catching as the offshore Yuan teeters around 7.1000 amidst more warnings from China that retaliation is in the pipeline if the US presses ahead with extra tariffs on September 1st. Meanwhile, the Lira continues to list and tested 100 DMA support circa 5.7922 even though Turkish consumer sentiment picked up in August.

In commodities, WTI and Brent futures are modestly firmer on the day with the former around the 56/bbl mark, whilst the latter remains near the 60.50/bbl level having found a base at 60/bbl. News flow has been light thus far for the complex with price action likely to be dictated by macro developments/sentiment heading into Fed Chair Powell’s speech tomorrow. Meanwhile, the WTI/Brent Arb widened to around USD 4.60/bbl vs. USD 3.60 earlier in the week. ING notes that “it does appear that the relative strength in WTI is starting to raise concerns over how it may impact demand for US oil from overseas buyers”. Elsewhere, gold is marginally softer and pivots on either side of 1500/oz ahead of ECB Minutes and as the Jackson Hole Symposium goes on underway, with Fed Chair Powell due to speak tomorrow. Copper prices declined further below the 2.6/lb mark as risk appetite somewhat waned.

US Event Calendar

8:30am: Initial Jobless Claims, est. 216,000, prior 220,000; Continuing Claims, est. 1.71m, prior 1.73m

9:45am: Markit US Manufacturing PMI, est. 50.5, prior 50.4; Markit US Services PMI, est. 52.8, prior 53

10am: Leading Index, est. 0.3%, prior -0.3%

11am: Kansas City Fed Manf. Activity, est. 1.2, prior -1

DB’s Craig Nicol concludes the overnight wrap

So there we have it, another one of those ‘where were you when…’ moments in the era of crazy low bond yields with the world’s first-ever zero coupon 30-year bond issued yesterday. Indeed, the 30y Bund ended up pricing at -0.11%; however, the big talking point was the anaemic demand at the auction with less than half of the offering being taken up by investors, meaning the Bundesbank had to retain the balance. The real subscription rate as a result was just 0.43x, which compares with 0.86x at the July auction. A lot was made of this being a very weak auction although it’s still hard to ignore the fact that €824m of the negative yielding ultra-long bonds were taken up by investors.

That auction came on a day when bond markets were a bit weaker. The whole Bund curve is still negative; however, yields were up a couple of basis points while Treasury yields also closed higher after the release of the FOMC minutes. Two-year yields rose +6.3bps, while 10-year yields rose +3.4bps.That sent the curve back down to just 1.0bp – a level it’s holding this morning – and dangerously close to inversion again.

The most immediately-relevant takeaway from the minutes was that there is minimal support for a 50bps cut in September, and markets moved to price in only a 12% chance of the bigger cut. That’s down from 20% before the minutes and from as high as 50% last week, though a 25bps cut remains fully priced. The minutes also suggested that policymakers were attentive to the trade war risks and were not caught off guard by the recent escalation, saying that “participants were mindful that trade tensions were far from settled.” As for the Fed’s longer-term policy review, there were several indications that the discussions are accelerating, as policymakers reportedly discussed using QE “more aggressively” and also analyzed “makeup strategies.” The latter “could be designed to promote a 2 percent inflation rate, on average, over some period,” which would have dovish implications for rates. While we’re on the Fed, President Trump continued his relentless attack on twitter, calling Powell “a golfer who can’t putt, has no touch”. To be fair, the same could be said for 99% of amateur golfers.

The moves in bond markets reflected a generally more upbeat tone across markets more broadly. That was certainly the case in equities where last night the S&P 500 closed +0.82%. The NASDAQ and DOW also finished +0.90% and +0.93%, respectively, with cyclical sectors generally leading gains. Favourably-viewed corporate earnings results in the retail sector from Target (+20.55%) and Lowe’s (+10.35%) helped. Nevertheless, the reality is that equities have just chopped around in a range since the plunge early in August and sit roughly where they were two weeks ago. HY credit spreads also had a strong day, with cash spreads trading -11bps and -10bps tighter in the US and Europe, respectively.

Overnight, Asian markets are quickly losing momentum although it’s not entirely obvious what’s driving the reversal from the highs. The Nikkei (-0.04%), Hang Seng (-0.87%), Shanghai Comp (-0.18%) and Kospi (-0.38%) are all lower having opened with decent gains. Futures on the S&P 500 (-0.03%) are also back to flat as we go to print.

Moving on. While markets have had very little to feed on the way of economic data this week, the good news is that we’ve got the global flash August PMIs today, which will give us a fresh opportunity to test the global growth pulse. We’ve already had the data out in Japan this morning where the composite rose half a point to 51.7, helped by a 1.6pt increase in the services reading to 53.4 while the manufacturing reading remained in contractionary territory at 49.5, albeit up 0.1pt from July. We’ll get the data for France, Germany and the Euro Area shortly and the consensus expects the composite reading for the Euro Area to have deteriorated slightly from 51.5 to 51.2, with the manufacturing and services readings expected to print at 46.2 and 53.0, respectively. A reminder that the July numbers confirmed a reversal of the improvement seen in June with the composite reading roughly consistent with a low +0.2% qoq rate of growth. This data of course will be the single biggest growth data point ahead of the ECB meeting in 3 weeks’ time. We should note that we’ll also get the data in the US where expectations are for a 50.5 manufacturing and 52.8 services print.

In other news, Italian assets continue to perform well despite persistent political uncertainty. Prime Minister Conte is scheduled to meet with leaders from the League and Five Star today, to see if he can find a prospective government and avoid fresh elections. Italian assets outperformed their European counterparts yesterday with the FTSE MIB finishing +1.77% versus +1.21% for the STOXX 600 while BTPs rallied -4.0bps and now sit at the lowest since October 2016.

Elsewhere, the CBO updated their US economic and budget forecasts. They now expect the fiscal deficit to widen to $960bn this year, up from their prior estimate of $896bn from May. That will be worth around 4.5% of GDP, worse than their prior forecast for 3.9%. The worse outlook will also result in trillion-dollar deficits beginning in 2020, two years earlier than before. On the bright side, the CBO raised their 2020 GDP growth forecast by 0.4pp to 2.1%, though they left 2019 at 2.3%.

Finally, the economic data didn’t add much but for completeness, US existing home sales rose to 5.42mn for July, marginally beating expectations for 5.40mn. That took the trend to 2.5% mom, and the prior month was revised upward slightly. Mortgage applications, a more forward-looking metric, fell -0.9%.

Looking at the day ahead now, outside of the PMIs the other data scheduled for release is August CBI survey data in the UK and August consumer confidence data for Euro Area, before jobless claims, July leading index and August Kansas Fed manufacturing survey is released in the US. We’ll also get the ECB minutes and of course the Fed’s Jackson Hole symposium kicks off tonight but with Powell not due to speak until tomorrow.

via ZeroHedge News https://ift.tt/2NqGywE Tyler Durden

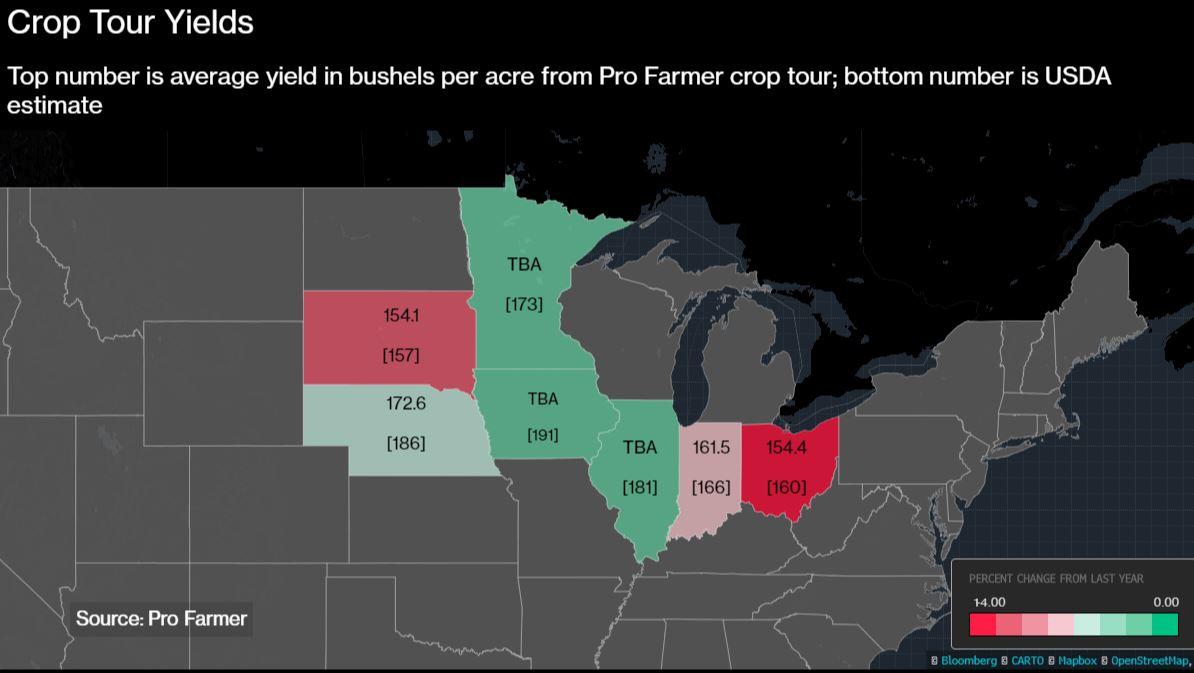

Apparently, President Trump’s hint that the Department of Agriculture might authorize another tranche of bailout funds for America’s farmers wasn’t enough to quell their anger. Because in what Bloombergdescribed as a “sign of rising tensions with the farm community,” staffers from the USDA’s Statistical Service was pulled from a popular but privately run Midwestern crop tour after a government employee was reportedly threatened.

The threat didn’t come from somebody involved in the Crop Tour, but the USDA decided to pull all staff as a precaution.

Lance Honig, crops chief at the USDA’s National Agricultural Statistics Service, was scheduled to address the tour in Nebraska City Tuesday night, but a video interview with him was screened instead.

“Federal Protective Services were contacted and are investigating the incident,” NASS Administrator Hubert Hamer said Wednesday, without giving details on the threat. “The safety of our employees is our top priority.”

The animosity toward the USDA might be inspired by the fact that the USDA has been criticized for publishing crop estimates that were larger than anticipated, weighing on the price of agricultural commodities at an already difficult time for American farmers, who have been struggling with the fallout from Trump’s trade war with China. Beijing recently revealed that it would scrap plans to buy more soybeans and other American agricultural goods.

The USDA had already been criticized for its June estimates, and decided to take the rare step of re-surveying farmers to test the accuracy of their information.

The USDA’s decision to withdraw from the crop tour comes about two weeks after farmers leveled criticism at Agriculture Secretary Sonny Perdue at a fair in Minnesota over the trade war with China.

In a statement Wednesday, Pro Farmer parent company Farm Journal said it took the threat seriously and has also taken care to ensure the safety of participants.

“For 27 years the Pro Farmer Crop Tour has been a public service for the benefit of agriculture, in good times and bad,” it said. “And it’s clearly a stressful time right now.”

During recent stops in Indiana, Illinois and Nebraska, farmers asked government officials and employees of Pro Farmer about the government’s methods for determining corn planted area and yields after a swift swing in prices left many farmers in the lurch. The USDA said yield estimates were based largely on input from pro farmers as well as satellite imagery.

One farmer interviewed by BBG stressed that most farmers likely wouldn’t condone the threats.

“We had a great time with the USDA guys yesterday,” said Jim Putnam, a Minnesota farmer, who traveled with two USDA staff on the tour Tuesday. “I’m sorry this happened. It makes us all look stupid.”

But, if nothing else, the animosity that the USDA is struggling hints at just how contentious the 2020 race could be for farmers who have largely suffered under President Trump’s policies, despite supporting him during the election.

via ZeroHedge News https://ift.tt/2zjSTKJ Tyler Durden

With the resignation of Prime Minister Giuseppe Conte the future of Italy is now up in the air. There are many things that come into play with Conte resigning before the No-Confidence vote tabled by Lega Leader Matteo Salvini could take place.

The euro popped 40 pips, back above support at $1.11 on the news. The forex markets realize this was a Brussels-friendly move.

Conte didn’t want to chance getting voted out of office. That makes it difficult for President Sergei Mattarella to call for a new government without snap elections. The Italian Senate would have formally rebuked Mattarella’s compromise pick for Prime Minister, Conte.

Conte was there to effectively keep the children in line – Euroskeptics Lega and Five Star Movement (M5S). So, Conte used his time to take the bully pulpit and excoriate Salvini for twenty minutes. This gives the U.S. and European media plenty of chum to make their case against Salvini.

You will hear a lot about how non-partisan Conte did this for the sake of Italy to stop the mad, selfish and unprofessional Salvini from taking power.

It’s good political theater but it’s as disingenuous as the day is long and very much the truth. No one in power in Brussels wants what Salvini is selling. Not many in Rome do either.

Because had he not resigned Mattarella could have faced impeachment for not going to elections. He only relented to let M5S and Lega take power under that threat last year.

So Conte has set the stage for Mattarella to take charge again. They will put the veneer of legitimacy on this process to protect Italy from Salvini. In reality, the only people they are protecting are in Brussels.

Remember, Salvini wants to circumvent EU budget controls through issuing the mini-BOT parallel currency. And current polling puts him at just below the threshold to take power outright.

The downstream effects of this are myriad but there is one big fulcrum on which this hinges.

M5S Leader Luigi Di Maio is now placed to play kingmaker. He can either do a deal with Matteo Renzi and the Democrats (PD), who M5S was formed to oust from power, or he can drag things out to attack Salvini for putting Italy in turmoil and hope for the best in an election.

Mattarella will push for a caretaker government to keep Salvini from power and marginalize M5S as much as possible. The goal is to forestall elections for as long as possible.

That latter path leads to Di Maio trying to shift opinion polls back on his side. Not likely, but hey, deluded people try to manipulate events against the trend all the time.

Salvini forced this crisis because of his persuading the Italian people that not only his future plans are better but so would be his leadership. The coalition has been stymied by both Conte and M5S and M5S’s poll numbers reflect their mission creep.

When that fails, Di Maio will have to make a deal with PD or face elections which will see M5S out of power.

But Di Maio is now in the same position that another reformer turned toady was in after he betrayed his country in 2015, Greece’s Alexis Tsipras.

To remind everyone, Tsipras is now out of a job and one of the most hated people in Greece. So complete was his sell out of the Greek people, he ushered back into power a center-right government in July.

Five Star was born out of the disgust Italians had for its leadership in Rome and the technocratic overthrow of Silvio Berlusconi’s government back in 2011.

It was a pure protest party, especially when Beppe Grillo was its figurehead. Now, it’s making deals to stay in power with those same technocrats.

Di Maio has to think very carefully about where things go from here.

Salvini is still in the driver’s seat because a betrayal by M5S of that nature will see Italy ground into a paste. Look no farther than the English Channel to see what Brussels wants to to do the Brits over Brexit. IF you think Italy will be spared after their dalliance with insurrection you are terminally naive.

And Salvini not being a part of that works to his advantage going forward. Sometimes the best way to win a battle is to retreat and let your enemies over-extend themselves.

Di Maio wasn’t a strong enough leader to keep the disparate factions within M5S on mission. He will now pay the price for his lack of vision.

* * *

Join my Patreon and Install Brave if you want to keep reading independent analysis and make the bastards sweat just a little bit.

via ZeroHedge News https://ift.tt/2Zecw5K Tyler Durden

At a moment that Iran and the US/UK are effectively already at war on the open seas in an ongoing “tanker war,” Tehran is set to unveil a new Iran-manufactured long range air-defense missile system which could rival Russia’s S-300 system.

Citing state media, the Associated Press described “the Bavar-373 is a long-range surface-to-air missile system able to recognize up to 100 targets at a same time and confront them with six different weapons.”

Screengrab of new state media footage published this week.

Iran’s semi-official Fars news agency indicated the system will be fully unveiled in a ceremony on Thursday, on the occasion of the country’s “Defense Industries day”.

The Iranian military has been increasingly reliant on its burgeoning domestic defense manufacturing industry in the face of crippling US sanctions. Since the early 1990’s it’s been able to develop tanks, submarines, and light and heavy munitions, and more recently touted an Iran-build stealth warship.

State media called the soon to be revealed Bavar-373 system a “deterrence against threats” uniquely produced domestically due to the “continuous sanctions imposed by the enemies” of the Islamic Republic. The first footage of the system was released Tuesday through state sources ahead of Thursday’s unveiling ceremony.

Russian aviation publication Avia.Pro claimed early this week that the Iranian system is “superior” to the S-300. It’s reportedly been undergoing testing since 2017, but it’s unclear how quickly it will actually be deployed into operation.

“The Iranian Bavar-373 radars can detect air targets at distances of up to 300 kilometers, and, in addition to aircraft, the radar is able to detect cruise and ballistic missiles, as well as small drones,” the publication stated, according to a translation.

“According to unconfirmed data, the radar is also capable of detecting stealth aircraft, which makes it an effective means of combating F-22 and F-35 fighters, which, incidentally, were recently discovered near the Iranian borders,” the report said further.

The system could be a competitor to Russia’s S-300 missile system.

No doubt the timing of this week’s unveiling is calculated as a message to Washington, and as a warning that sanctions will only increase Iran’s domestic-produced defense capabilities.

via ZeroHedge News https://ift.tt/2KL9M7Q Tyler Durden

{kind=link}