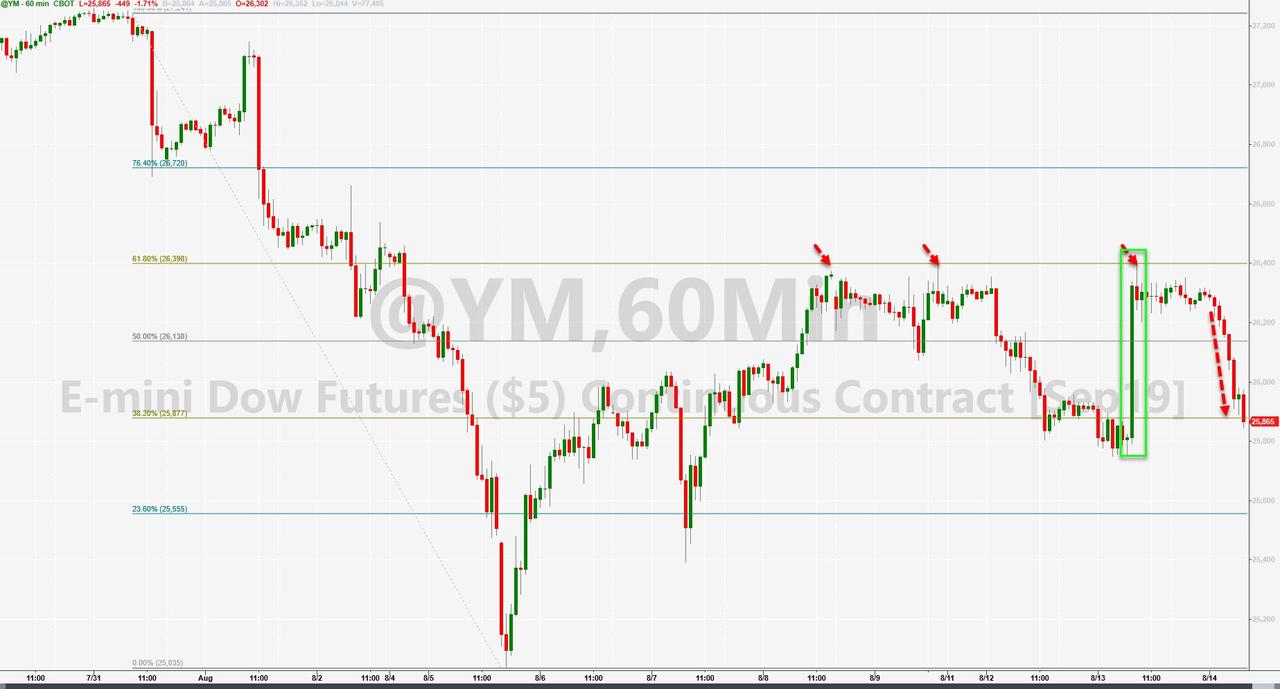

Well that de-escalated quickly…

Dow futures are down over 450 points this morning…

Seems like critical resistance held after all…

From hope to nope.

via ZeroHedge News https://ift.tt/2KyyVTb Tyler Durden

another site

Well that de-escalated quickly…

Dow futures are down over 450 points this morning…

Seems like critical resistance held after all…

From hope to nope.

via ZeroHedge News https://ift.tt/2KyyVTb Tyler Durden

Authored by Mike Shedlock via MishTalk,

Negative yields? Who cares says Greenspan. It’s meaningless.

Former Fed Chair Alan Greenspan sees No Barriers to Prevent Negative Treasury Yields.

Former Federal Reserve Chairman Alan Greenspan says he wouldn’t be surprised if U.S. bond yields turn negative. And if they do, it’s not that big of a deal.

“There is international arbitrage going on in the bond market that is helping drive long-term Treasury yields lower,” Greenspan, who led the central bank from 1987 to 2006, said in a phone interview. “There is no barrier for U.S. Treasury yields going below zero. Zero has no meaning, beside being a certain level.”

Joachim Fels, global economic adviser at Pacific Investment Management Co., detailed earlier this month a view that there’s been a change in the fundamental economic theory of time preference that helps explain why people are buying debt with negative yields. He postulated that extended life expectancy and an aging population have caused people to value future consumption more than current spending.

Greenspan, 93, said he views Fels’s thesis as very plausible and also a reason why more debt has a yield below zero. He doesn’t think it will last forever.

Please consider Bubblicious Debate: Greenspan Says “Bond Bubble About to Break”, No Stock Market Bubble

In a CNBC interview, the longtime central bank chief said the prolonged period of low interest rates is about to end and, with it, a bull market in fixed income that has lasted more than three decades.

“The current level of interest rates is abnormally low and there’s only one direction in which they can go, and when they start they will be rather rapid,” Greenspan said on “Squawk Box.”

Alan Greenspan told Bloomberg TV : “By any measure, real long-term interest rates are much too low and therefore unsustainable. When they move higher they are likely to move reasonably fast. We are experiencing a bubble, not in stock prices but in bond prices. This is not discounted in the marketplace.”

Now it’s “No Big Deal”.

On December 5, 1996 the Maestro warned of “Irrational Exuberance“.

Click on the link for an amusing video.

By the year 2000 Alan Greenspan embraced the “productivity miracle” of technology and no longer saw any bubbles.

That’s precisely when the technology bust started.

As noted above, Joachim Fels, global economic adviser at Pacific Investment Management Co, suggests “there’s been a change in the fundamental economic theory of time preference that helps explain why people are buying debt with negative yields.“

Time preference can never be negative. Never.

To believe in negative time preference is to believe things such as “It’s better to have 90 cents ten years from now than a dollar today”.

Yields are negative only because central banks manipulated yields negative. They would never be negative on their own accord.

Investors buy negative yielding debt firmly convinced central banks will manipulate yields even more negative.

Alan Greenspan is wrong. Zero is very meaningful with negative being even more meaningful.

It means central banks have hit a brick wall. They cannot cram any more debt into the system. There is no tolerance for paying interest.

That’s the meaning, and the evidence is overwhelming.

More Currency Wars: Swiss Central Bank Poised to Cut Interest Rate to -1.0%

Inverted Negative Yields in Germany and Negative Rate Mortgages.

As Gold Blasts Through $1500 the implied message is that central banks are out of control.

Gold has the meaning of zero correct even if central bank clowns and analysts don’t.

via ZeroHedge News https://ift.tt/301P6O8 Tyler Durden

A$AP Rocky and two associates were found guilty of assault on Wednesday, after a Swedish court ruled that they were “not in a situation where they were entitled to use violence in self-defense,” according to the Washington Post.

The 30-year-old rapper whose arrest led to a minor diplomatic spat was not sentenced to any prison time because the “assault has not been of such a serious nature that a prison sentence must be chosen,” according to a Stockholm district court press release.

Rocky and two of his associates faced up to two years in jail for allegedly assaulting a man in Stockholm at the end of June, but their temporary release on Aug. 2 was seen as a possible indication of a not-guilty verdict or a sentence shorter than the time already served during more than four weeks of pretrial detention. –Washington Post

Rocky, who was released on bail two weeks ago and returned to the United States on August 2, was arrested along with associates Bladimir Emilio Corniel and David Tyrone Rispers in early July, stemming from a June 30 street fight with a 19-year-old man, Mustafa Jafari.

On the last day of Rocky’s trial, a key witness changed her testimony to say that she never saw Rocky hit the alleged victim with a bottle – which resulted in the presiding judge, Senior Judge Per Lennerbrant, saying in a written statement that “the prosecutor has not been able to prove that the victim was struck in the back of the head with a bottle or that he was in any other way assaulted with bottles. This has affected the assessment of the seriousness of the crime.“

A$AP Rocky released from prison and on his way home to the United States from Sweden. It was a Rocky Week, get home ASAP A$AP!

— Donald J. Trump (@realDonaldTrump) August 2, 2019

Last month President Trump urged Sweden’s prime minister to release Rocky, which Swedish leaders criticized as an attempt to interfere with their country’s independent legal system. Trump had called on the Swedish government to focus on its “real crime problem” instead of Rocky – implying that they should do something about crime committed by migrants.

Sweden’s justice system is ranked among the world’s most respected, but the rapper’s arrest and weeks-long detention without charges sparked an outcry in the United States. Kim Kardashian West, Kanye West and Justin Bieber called for his release, as did several Democratic members of Congress. –Washington Post

Earlier this month, CNN released a diplomatic letter warning of “negative consequences” in US-Swedish relations, if the American rapper’s hearing on assault charges was not resolved quickly. The letter included what appeared to be a veiled threat against the Swedish government, to either release Rocky, or risk damaging the bilateral relationship.

CNN has obtained the full text of a letter written by the US Special Presidential Envoy for Hostage Affairs Robert C. O’Brien and leaked earlier on Twitter. Addressed to the Swedish Prosecution Authority on July 31 – before the rapper’s trial had concluded – the letter said the US was eager “to resolve this case as soon as possible to avoid potentially negative consequences to the US-Swedish bilateral relationship.”

US ‘hostage affairs envoy,’ Robert C. Obrien was also dispatched to Stockholm to attend the trial, which Swedes widely mocked.

via ZeroHedge News https://ift.tt/2KP7UK7 Tyler Durden

Blain’s Morning Porridge, submitted by Bill Blain of Shard Capital

“My heart will never break… but it will stop beating..”

So much noise out there this morning!

Someone must have told Trump his electoral chances would not be enhanced by a miserable Christmas on Main Street USA, so he held back some selected consumer-good tariffs till December. Effectively this confirms a stark reality – its US consumers who are paying the costs of Trump’s tariffs on China. Its not de-escalation, its just more policy on the hoof. Anyone betting the US and China are about to kiss and make up is in La-La Land.

Meanwhile, I’ve appended a graph showing the performance of the Argentina Century Bond vs the Austrian Century Bond. You are unlikely the two bonds mixed up – although I’m told it’s happened… One of them yields nothing for 98 years. The other yields lots… Do you care if you don’t get your money back? Probably not.. but you are equally unlikely to get any coupon… Zeros?

There is one very important secondary observation to make on the Argentina melt-down: one of main reasons we saw such a dramatic crash in bonds and the near 50% tumble in the stock market was the complete absence of serious market makers or broking. This isn’t due to investment banks and traders not seeing opportunity in over-sold Argentina, but more a result of how capital regulations and trading rules have made it utterly non-economic to trade smaller, illiquid, risk markets. The market was opportunistic. We saw bid/offers wide enough to turn a supertanker thru – and it proved very difficult to execute any client orders.

The Implications are serious – if we see a breakdown, then the collapse of liquidity across markets like High-Yield (now officially defined as anything yielding anything) and corporate bonds will be crushing. Wide bid/offers and chronic illiquidity will massively exaggerate losses and deepen any sell-off. It’s going to hit less liquid equity markets also – look how wide Burford whipsawed last week, and it’s the biggest AIM stock on the London market. Sell-off’s are a bargain hunting opportunity… but who is prepared to take Argie risk..? (If you are interested, let me know if you are a buyer.. we may be able to help..)

Watching the Hong Kong situation I can’t think there is a screaming, massive obvious short out there. Who? Sorry, but its HSBC. They have apparently attracted the ire of the Chinese Government over the accusation they gave confidential info on Huawei to the US investigators. If/when China clamps down on the protests, they stand to see 90% of the current profit base disrupted. Worst case scenario is they are effectively chased out. Best case is they still find themselves in a position of weakness. Its down 7.5% since it sacked its CEO. How much lower will it go if the People’s Army marches in? If there are reasons to be positive please share

Inversion Recession?

Where do we go next? The US 2s/10s yield curve inversion looks a very real threat (currently 2s yield 1.63% and 10s yield 1.65%). The conventional wisdom is any inversion where Bonds yield less than short-bills screams recession. The joke is inversions have predicted 10 of the last 3 recessions. (The truth is, an inversion is usually correct.)

But a 2s/10s reversion is a serious deflationary signal. T-Bills (short-dated obligations of the government) say little about inflation and are usually bought by money market and short-term funds. 2-year Notes do factor future inflation and are bought by institutional investors as part of long-term investment strategies. It means the real money market has serious doubts on the future.

For investors predicting a stronger economy and rising bond yields, then 2-year T-Notes would be the place to play the pivot towards higher yields. What an inversion says when 2-year yields more than longer bonds is a massive recessionary signal and a strong indicator of long-term deflation – it suggests investors think rates are going lower for longer, hence looking to lock in 10-year plus returns now! That is frightening… suggesting the market thinks this lasts for a decade or more!

No wonder folk are thinking about Gold, while some idiots still think BitCoins are the answer. If you think so, be my guest. There is no positive question to which BotCoin is ever the answer.

Were you aware one of the top performing markets this year has been Carbon Credits? Its been a strange and curious market – subject to all kinds of shenanigans and difficulties in the past. The market now looks more established. European governments have been handing carbon credits to industrial producers for years. Since 2017 European governments have been slashing the supply of credits. Supply is being cut by 24% per annum for the next 5 years! This year the sweltering July drove up power demand, pushing prices higher!

US Carbon offset credits are also rising – especially in California which has managed to reduce Co2 emissions below 1990 levels, largely by hitting transport sources via emission taxes. While the state posted 3.7% growth in 2017, Co2 emissions actually dropped! New Californian “Low Carbon Fuel Standard” laws demand transport sector reduce Co2 emissions. As a result Californian Carbon Offset prices are going through the ceiling. It’s becoming a multi-billion dollar market.

Young Greta Thunberg sets off today on her 2 week voyage across the Atlantic to save the Carbon a 8 hour flight would have generated. I admire her for doing it. Listening the Generation Z on BrekDrek this morning – they absolutely believe. Carbon Nuetral politics is not only here to stay, but is going to become more and more influential. I do feel sorry for Greta. She is not a sailor, and the weather pattern she is sailing into means a massive storm and high winds will hit tomorrow, making her first day on the boat miserable. The problem with sea-sickness is that on the first day you are scared you are going to die. On the second day, you are scared you are not!

Carbon pricing is here to stay, and its going to be massive. One of the alternative asset deals we’re currently marketing produces CO2 Carbon Offset by extracting CO2 out of carbon fuels which can then be buried (sequestered) in old gas and oil fields and saline aquifers. Give me a shout and I will tell you all about it.

Blain’s Brexit Watch

We still have no idea on what Europe might be prepared to discuss, or even if they will. In London lots of angry noise from Remainer Parliamentarians determined to thwart a No-deal. There is a massive game being played. Boris would like to call an election – the polls now say he could win, but he can’t unless he recalls parliament, and force a no-confidence vote. He still might lose. So he waits. And Waits. Nothing is apparently happening except lots of squawking ducks… while Boris paddles furiously beneath the surface.

Brexit.. what a laf!

via ZeroHedge News https://ift.tt/2Z5AsEi Tyler Durden

Despite China’s exported deflation reaching a 12-year highs…

US Import and Export prices surprisingly rose MoM (Imports +0.2% vs -0.1% exp and Exports +0.2% vs -0.1% exp), but, both import and export prices have deflated YoY for three straight months…

Good news for Powell – another well selected item to use as ammo for rate cuts.

But where are the tariff-driven surges in prices?

via ZeroHedge News https://ift.tt/2TtFOb2 Tyler Durden

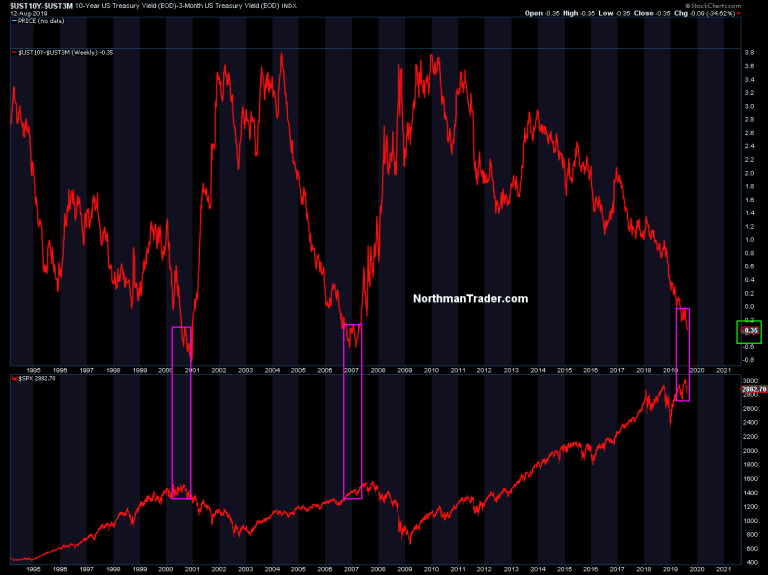

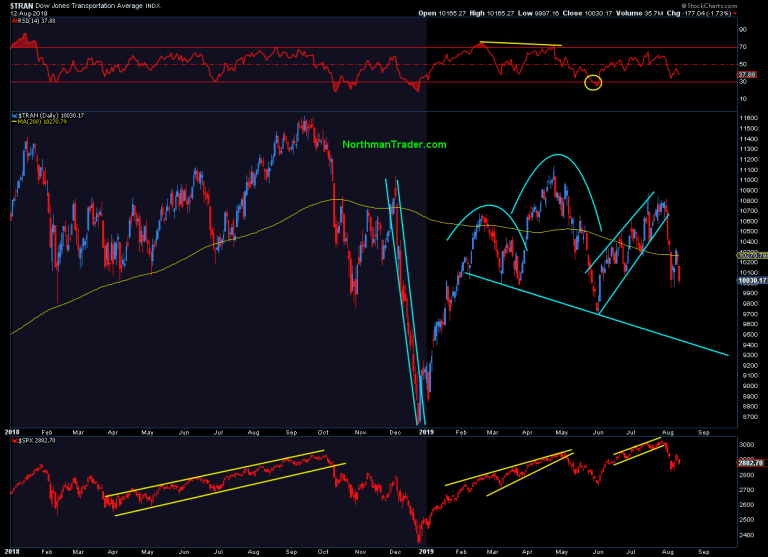

Authored by Sven Henrich via NorthmanTrader.com,

Bulls are walking a tight rope here.

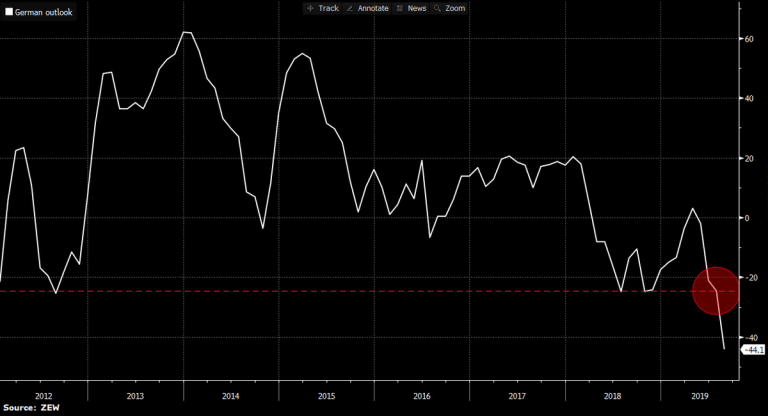

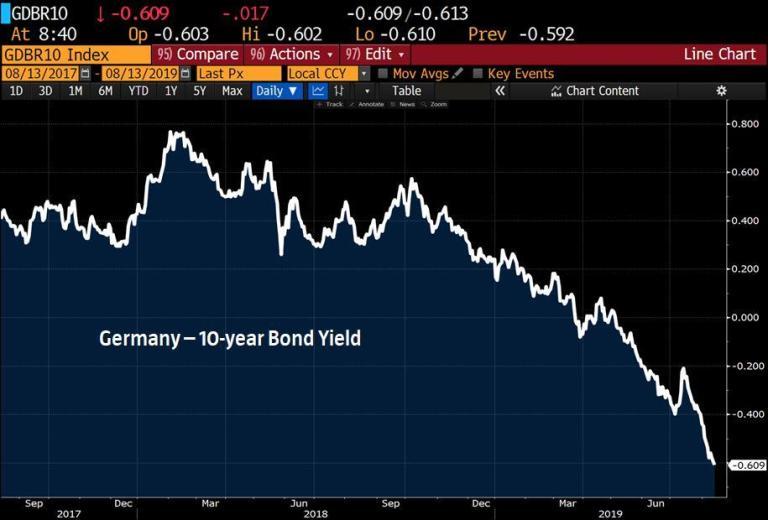

There are smoldering fires burning everywhere. Almost too many to list, all of which have the potential to unleash a major forest fire. Europe data is getting more lousy by the minute, as is Asia’s. European bank levels are freaking everyone out, and we look one bank shoe drop away from a major support break. Last week it was the UK that announced a negative quarterly GDP print, today it was Singapore that showed dismal figures and dropped GDP growth projections to zero. Yield curves keep inverting and yields keep dropping like flies all around the stench of a global economy struggling. Argentina’s sudden blow-up yesterday adds to global contagion stress and unrest in Hong Kong is rightfully adding to angst in that region. Add plummeting German ZEW data:

and yields:

..and the global bear case is getting ever more obvious and perhaps this should worry bears the most in this environment, as any of these things can also be sources of futures relief rallies if things calm down a bit.

After all, in this climate, all it would take is for President Trump to tweet “tariffs delayed” and you have a rip your face off relief rally.

But that all being said concerns are widening.

The 10 year 3 month curve keeps in inverting to a troubling zone:

And now all eyes are on the 10/2:

The macro wheels are turning big time and it’s coming at a critical point of market valuations versus GDP, a point I’ve been beating the drum on in recent days to raise awareness as I haven’t seen it discussed anywhere.

I made the point yesterday on CNBC:

And also on CNN:

“The biggest bubbles in most of our lifetimes were the 2000 tech bubble, the 2007 real estate bubble and the monstrosity we are witnessing now: the cheap money bubble,” writes Sven Henrich https://t.co/MZtegWWGAG

— CNN Business (@CNNBusiness) August 13, 2019

The cheap money bubble, the low interest bubble, the one that makes record expansion in debt possible and sustainable in the here and now. But none of that changes the valuation reality and it’s a critical point hence my effort to raise awareness.

From my perch the only way the Fed can avoid a recession is to blow an even bigger valuation bubble versus the size of the underlying economy, a larger one than what we saw during the tech bubble or the housing bubble.

US stocks have held relatively well in so far. We’re currently in the middle of another smaller correction greatly aided by buybacks and consumer confidence still high. High confidence equals spending. And look, in the world of passive investing and still high market prices and 50 year lows in unemployment consumer confidence can remain high until 2 things happen: Stocks drop hard and/or unemployment turns which it invariable will do at some point. In December retail sales stunk up the joint as stocks tanked. Confidence is a prickly thing and can change quickly. See a major market drop again and confidence will wane quickly.

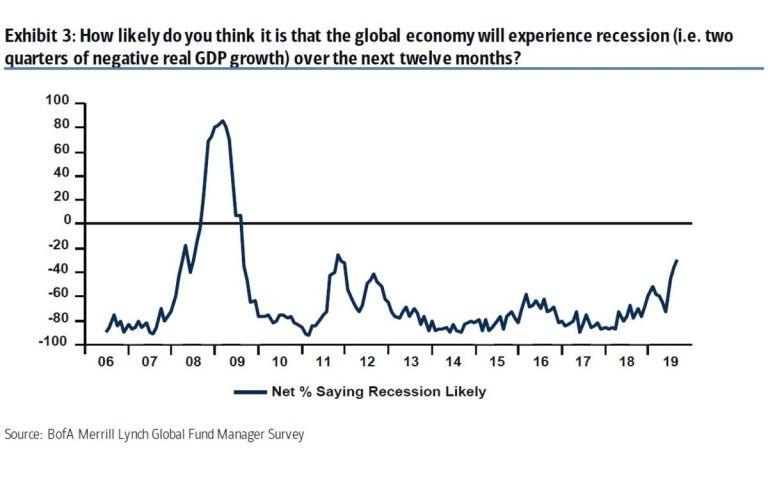

Right now we’re still in a period of recession risk denial. Every central banker insists in denying there is recession risk. They always do. They have to. Central banks can’t warn of recessions or they themselves would cause confidence to wane. And hence recession risk denial is a well established thing. After all recession risk denial was all the rage even at the end of 2007 when the recession already started in December of that year:

Now fund managers are sensing recession risk is on the increase on a level similar to 2011 and in 2008. In 2011 the Fed responded by announcing operation Twist & ultimately with QE3. In 2008 they dropped rates by over 300bp in just that year for an ultimate total off over 500bps. So far we only have a 25bp rate cut with with only 200bp to work with before hitting zero again.

But forget yields and yield curve inversions for a moment. There’s another subtle signal floating about: Transports:

Correlation may not imply causation, but, fwiw, when $TRAN makes new all time highs and prints a negative divergence on these new highs a recession has unfolded thereafter. pic.twitter.com/dHFB7AdaZE

— Sven Henrich (@NorthmanTrader) August 13, 2019

Transport have been the canary in the coal mine for a while as you can see if you expand the tweet ahead above.

Just because there’s recession denial doesn’t mean a recession isn’t coming. The only question remains the when and were. With all the global uncertainty it’s hard to imagine companies committing to large scale hiring programs, but so far jobs are hanging in there and that’s a piece of comfort for bulls.

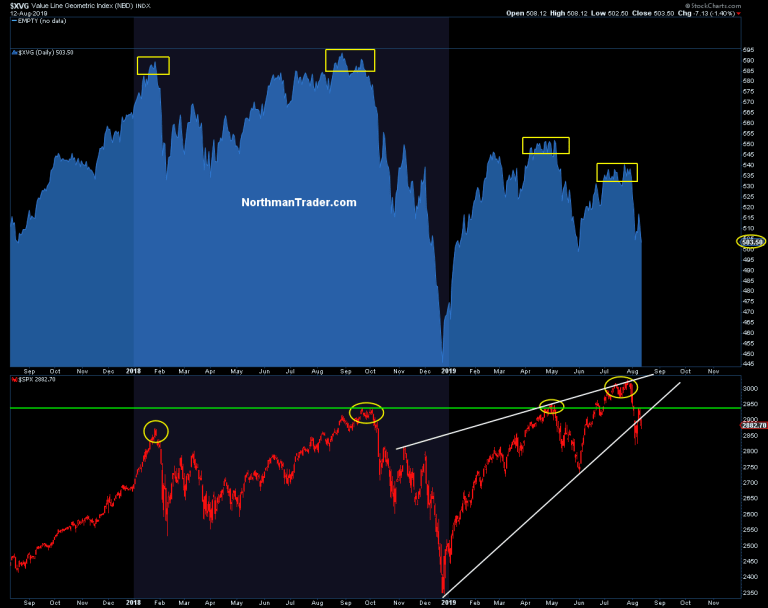

But be sure they’re walking a tight rope and are one larger sell-off away from facing a different reality, a reality that has already been unfolding in the value line geometric index that keeps printing lower highs and lower highs:

And now $SPX is overtly at risk of breaking its 2019 trend. Last week’s save has been sold this week so far.

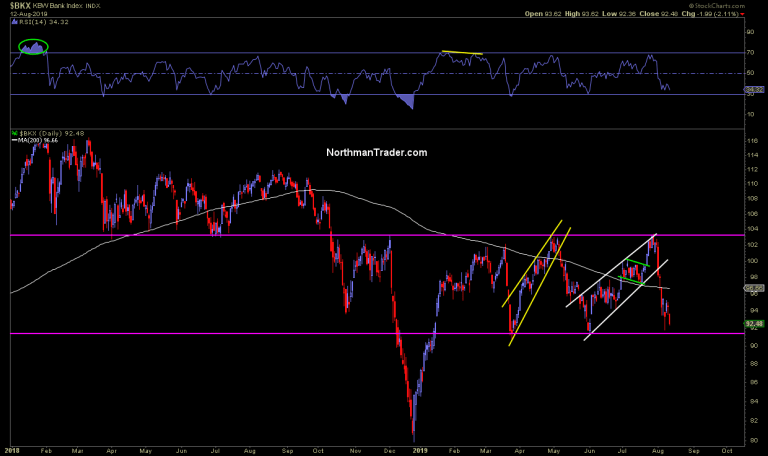

And for banks this support line is critical to maintain:

A break below and things could get ugly fast. The same message sent by transports as they sport a potential topping pattern that could target the December lows:

Nothing’s confirmed broken yet and markets are becoming oversold. But bulls are walking a tight rope here and sure could use a magic tweet or headline to avert a breakdown.

But will a headline or tweet rally be enough to change the larger picture? Depends on what it is I suppose. At this point sentiment is so bad President Trump could probably inspire a global rally by simply folding on his trade war, declare victory and end it. No trade deal required. Word is he’s now on his own and is ignoring his advisers.

As of now there’s no apparent end in sight to the trade war or stress in currency and bond markets nor the slowdown in growth while US stock markets remain historically highly elevated versus underlying GDP while earnings estimates are dropping hard:

But let’s keep raising price targets https://t.co/ixoAO7ow4K

— Sven Henrich (@NorthmanTrader) August 12, 2019

Bottomline: Both bulls and bears are on notice all the time in this headline driven market, but bulls have a lot to lose if they lose balance.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2YWqn0v Tyler Durden

Macy’s shares are down 14% in the pre-market – the lowest since Feb 2010 – after missing Q2 expectations and cutting its full-year guidance for earnings, blaming weather, fashion, inventory and markdown issues.

Macy’s said diluted earnings for the three months ending in July came in at 28 cents per share, down 47.2% from the same period last year and well shy of the Street consensus forecast of 45 cents per share.

But it gets worse, as the company looks into 2019, Macy’s said it now sees diluted earnings in the region of $2.85 to $3.05 per share, down from a prior forecast of $3.05 to $3.25 per share.

“We had a slow start to the quarter and finished below our expectations. Rising inventory levels became a challenge based on a combination of factors: a fashion miss in our key women’s sportswear private brands, slow sell-through of warm weather apparel and the accelerated decline in international tourism,” said CEO Jeff Gennette.

“We took markdowns to clear the excess Spring inventory and are entering the Fall season with the right inventory to meet anticipated customer demand.”

“Our 2019 strategic initiatives are on track to contribute to sales growth in the back half of the year, and we have plans to drive productivity and improve gross margins,” Gennette added.

“Our team has responded quickly to the external environment, course corrected when needed and we remain confident”

Investors are unhappy

Cue the tweet from the president blasting Jeff Bezos (will Amazon take over the parade?)

via ZeroHedge News https://ift.tt/2MZkMQm Tyler Durden

As expected, WeWork – or “the We Company”, as its struggling to rebrand itself – published on Wednesday the prospectus for its hotly anticipated IPO, which it confidentially submitted to the SEC months ago.

Of all the ‘tech’ darlings that have either recently IPO’d, or are expected to in the near future, WeWork’s business so far has involved burning ever-more cash (roughly in line with revenue growth) while its CEO, Adam Neumann, shares his grandiose, expansive vision to build an office-space leasing company, that’s also a provider of adult dorms, and a private school, and generalized lifestyle company.

To back up that vision with numbers, Neumann’s company listed its Total Addressable Market in its S-1 as $3 trillion, equivalent to roughly 15% of the US economy. Meanwhile, the company generated $1.54 billion in revenue in the first six months of 2019 and posted a net loss of $689.7 million. Astonishingly, the company has been valued at $47 thanks to VC investments by Soft Bank and other large institutional investors.

According to WeWork, its potential market size is 15% of US GDP. Thanks @federalreserve this is all your doing pic.twitter.com/s5YyX7iS5x

— zerohedge (@zerohedge) August 14, 2019

The IPO will leave WeWork with three classes of common stock, adding to its already complicated structure, which is set up to provide tax benefits to Neumann and other early investors.

This is almost as straightforward as Alibaba’s org chart pic.twitter.com/73vrNotjZd

— zerohedge (@zerohedge) August 14, 2019

In the filing, WeWork said it’s “reinventing” the way people work and “relate to the workplace” (admittedly, an appealing turn of phrase).

“We are reinventing the way people work and transforming the way individuals and organizations relate to the workplace,” the company said in the filing. “When we started, it was obvious to us that the solutions available in the market were not meeting the needs of the modern workforce.”

The listing is being finalized as WeWork hopes to sow up another $6 billion asset-backed financing package. That package is reportedly contingent on WeWork raising at least $3 billion from its IPO, which it’s expected to do.

via ZeroHedge News https://ift.tt/31DWsHS Tyler Durden

Authored by Charles Hugh Smith via OfTwoMinds blog,

Or perhaps “Epstein was an intelligence asset” is just a tissue-thin cover for a much more destructive reality: those at the top of the American state have no moral compass at all.

Let’s start by stipulating that the Jeffrey Epstein story is so sordid and outlandish that it’s like a made-for-TV movie about the evil proprietor of a nightmarish enclave of private perversion and sexual exploitation, Lolita Island.

For Epstein’s victims, the nightmare was all too real.

Next, let’s stipulate that in a nation with a functioning system of justice, every individual who knew about Epstein’s degenerate empire and did nothing to stop it should be ushered into a Federal prison cell to ponder their sins against the exploited girls and against the nation.

Yes, as in treason, as in “throw them in prison and let them rot” treason. As I have explained, corruption and debauchery undermine the legitimacy of the state, and so doing nothing while Epstein et al. gratified the desires of the rich and powerful for degenerate debauchery was treasonous: the American state will collapse not from military conflict but from moral decay, and every individual who enabled (or made use of) that moral decay is guilty of treason.

Which leads us to the basic questions of the case: who protected Epstein for decades, and why? There are several explanations floating around for the why: those in power enjoyed their diabolically exploitive visits to Lolita Island and wanted to continue their criminal gratifications.

The second explanation is that Epstein was a spy for a “friendly” foreign intelligence agency and therefore off-limits. (“Friendly” is in quotes because when it comes to intelligence, one’s “friends” can do more damage than one’s worst enemies.)

Let’s say this turns out to be true. Wouldn’t the NSA, CIA and FBI know of Epstein’s activities and connections to a foreign intelligence service? Of course they would. So at a minimum, we can infer the NSA, CIA and FBI enabled Epstein’s operation to continue for some benefit, perhaps relating to “honeypot” blackmail and control of “assets,” unwilling or willing.

This narrative is the “explanation” for Epstein’s wrist-slap conviction a decade ago: he was supposedly an “asset” of US intelligence.

So exploiting vulnerable girls served the “national interests” and therefore it’s all OK. If we’re supposed to believe this is the heart of the matter, how is America any different from a corrupt developing-world kleptocracy organized to gratify a handful of oligarchs and their cronies?

Or perhaps the “he was an intelligence asset” is just a tissue-thin cover for a much more destructive reality: those at the top of the American state have no moral compass at all. That honeypots and blackmail are standard-issue tools of spycraft targeting individuals in the employee of other nations is a given, but presumably the CIA doesn’t recruit 14-year girls as bait (although nothing should surprise us at this point).

But Lolita island (a.k.a. Orgy Island) was not spycraft; it was a privately operated wholesale exploitation of underage girls for the gratification of the Western world’s male elites. That some enterprising agency recruited (or blackmailed) Jeffrey Epstein was predictable, as the treasure trove of compromising videos could yield all sorts of useful leverage on highly placed individuals.

Many of us sense an existential crisis is close at hand, and the U.S. is ill-prepared for such a crisis. Possibilities broached by others include a global war, a break-up of the U.S. into regional states, or a civil war of some sort.

My bet is on a moral and financial crisis in which the ruling elites and the federal state lose their legitimacy, i.e. the consent of the governed. As their Federal Reserve “money” loses value and the corruption of the ruling elites and the government they control reaches extremes, the citizenry will no longer heed their corrupt, self-serving “leaders.”

If America’s ruling elites will not let justice be done, then they guarantee a revolt against the elites that could track a very grim path if that is the only option left open to the citizenry.

Once again I turn to The Second Coming by William Butler Yeats for a poetic evocation of the coming crisis:

Turning and turning in the widening gyre

The falcon cannot hear the falconer;

Things fall apart; the centre cannot hold;

Mere anarchy is loosed upon the world,

The blood-dimmed tide is loosed, and everywhere

The ceremony of innocence is drowned;

The best lack all conviction, while the worst

Are full of passionate intensity.

* * *

Pathfinding our Destiny: Preventing the Final Fall of Our Democratic Republic ($6.95 ebook, $12 print, $13.08 audiobook): Read the first section for free in PDF format. My new mystery The Adventures of the Consulting Philosopher: The Disappearance of Drake is a ridiculously affordable $1.29 (Kindle) or $8.95 (print); read the first chapters for free (PDF). My book Money and Work Unchained is now $6.95 for the Kindle ebook and $15 for the print edition. Read the first section for free in PDF format. If you found value in this content, please join me in seeking solutions by becoming a $1/month patron of my work via patreon.com. New benefit for subscribers/patrons: a monthly Q&A where I respond to your questions/topics.

via ZeroHedge News https://ift.tt/33BsdmH Tyler Durden

For the third day in a row, global markets started off the session with some bullish enthusiasm – this time on hopes of a trade deal with China following Trump’s delay to some key tariffs – only to see it all fade, as global stocks were flushed down the red drain thanks to dismal economic news first from China, whose key economic indicators all missed overnight and factory output tumbled to a 17 year low, then from Germany where GDP contracted for the 2nd time in 4 quarters sending the country to the verge of recession, and culminating with the inversion of both the UK and US 2s10s yield curve as the 30Y Treasury yield dropped to a record low, sliding below the effective fed funds rate for the first time ever.

US equity futures slumped to session lows, dropping alongside European stocks as weak data from two of the world’s biggest economies overshadowed an apparent de-escalation in the trade war. Treasuries and European bonds rallied, with key parts of both the U.S. and U.K. yield curves inverting.

European stocks fell on poor industrial production data and as Germany’s economy went into reverse, reviving fears of global recession and tempering a rally for equities after Washington delayed tariffs on some Chinese imports. Germany shrank 0.1% in the second quarter as the trade war and weak demand dragged on German manufacturers. The euro zone as a whole reported gross domestic product grew just 0.2% in the same quarter.

The Euro Stoxx 600 fell 0.4%, with markets in London, Frankfurt and Paris losing from 0.2% to 0.6%, tracking U.S. futures lower, as all but two of the 19 industry groups decline. Carmakers, banks and miners are the worst performers, while food-and-beverage shares temper the benchmark’s decline. Cyclical shares are retracing some of Tuesday’s gains after data from China and Germany flag a worsening economic outlook.

Earlier in the session, Asian stocks advanced, led by technology firms, as easing trade tensions between the U.S. and China spurred a relief rally around the world. Almost all markets in the region were up, with India and Japan leading gains. The Topix climbed 0.9%, supported by electronic and telecommunication firms, as Japanese traders looked beyond the worst earnings in three years and bet on a turnaround. The Shanghai Composite Index added 0.4%, with Kweichow Moutai advancing to a new record, even though China’s economy slowed more than expected in July, posting the weakest industrial output growth since 2002. The 4.8% growth was the lowest in 17 years.

The German figures, along with data showing the slowest growth for Chinese industrial output in 17 years stoking recession worries, knocked the wind out the sails for stocks.

Sure enough, this quickly manifested itself in the bond market, with the U.K. yield curve inverting for the first time since the financial crisis and the pound strengthened after inflation unexpectedly rose above the Bank of England’s 2% target in July. The US Treasury yield curve also inverted as the spread between US two-year and 10-year Treasury yields – a closely watched metric for signs of a slowdown and a famous recession predictor – finally turned negative after 12 years.

“The bond market is saying central banks are behind the curve,” said Marc Ostwald, global strategist at ADM Investor Services in London. “It’s all doom and gloom on the global economy.”

Earlier in the session, investors had cheered earlier when U.S. President Donald Trump pushed back a Sept. 1 deadline for new tariffs on remaining Chinese imports. The S&P 500 which had fallen 1% on Monday, rose 1.5% on Tuesday, sending Asian stocks outside Japan up 0.6%. Benchmarks in Shanghai, Hong Kong and Tokyo all mirrored the surge in U.S. stocks. But the momentum ebbed in Europe, as optimism faded that Trump’s move meant tensions were easing and Germany’s slowdown showed the damage already done by the trade war.

“The trade war and the dispute between U.S. and China has already had an impact – especially when you look at countries most sensitive to global trade like Germany and even Italy,” said Christophe Barraud, chief economist and strategist at Market Securities in Paris.

Meanwhile, Hong Kong’s airport resumed normal operations after a chaotic night of protest in which demonstrators beat and detained two suspected infiltrators and Trump warned of Chinese troops massing on the border.

In FX, the safe haven Japanese yen gained 0.3% to 106.42 per dollar as the Chinese data signaled that any resolution to the trade war was a long way off. Mirroring that view, the offshore Chinese yuan fell 0.4% against the dollar to 7.0337, erasing gains made the day before and remaining weaker than the 7 to the dollar it reached last week. The Australian dollar fell after the China economic data, including retail sales and industrial output, missed estimates. Swedish inflation data comes in stronger than forecast yet the krona fails to sustain knee-jerk reaction gains. The pound gained after U.K. inflation unexpectedly accelerated above the Bank of England’s target.

In commodity markets, oil prices fell after the Chinese data from China and a rise in U.S. crude inventories, erasing some of the gains made after Trump’s tariff delay. Brent crude was down 54 cents, or 0.9%, at $60.76 a barrel after rising 4.7% on Tuesday, its biggest percentage gain since December.

Expected data include mortgage applications. Canada Goose, Macy’s, Agilent, Canopy Growth and Cisco are among companies reporting earnings.

Market Snapshot

Top Overnight News

Asian equity markets traded higher across the board with global risk appetite spurred by a de-escalation in the US-China trade war after the US announced to delay the 10% tariffs on some items from China until December 15th, although stocks are off the day’s best levels on disappointing Chinese data in which Industrial Production grew at the slowest pace in 17 years. ASX 200 (+0.4%) and Nikkei 225 (+1.0%) gained from the open but with upside in Australia capped by weakness in financials after NAB reported tepid profit growth for Q3 and as gold miners suffered from a pullback in the precious metal, while Tokyo sentiment was boosted by encouraging data after Machinery Orders showed the largest M/M increase on record. Hang Seng (+0.1%) and Shanghai Comp. (+0.4%) were buoyed at the open after the tariff delay announcement which President Trump noted was for the Christmas season in case it had an impact on shopping and suggested that he had a very productive call with China, while a continued PBoC liquidity effort and firmer CNY fix added to the optimism before weaker than expected Industrial Production and Retail Sales data from China saw stocks give back some of the gains. 10yr JGBs are lower after the US tariff delay triggered safe haven outflows and amid a continued lack of BoJ buying with the central bank only in the market today for Treasury Bills.

Top US News

European equities are lower across the board [Eurostoxx 50 -1.3%] as the global risk appetite seen yesterday and overnight waned in earlier European trade. Major bourses are posting broad-based losses although Italy’s FTSE MIB (-1.9%) is underperforming, as the ongoing political angst sees almost all Italian stocks in the red. Meanwhile, DAX 30 (-1.4%) breached the key 11,600 support level on which the index turned-around during the May rout. Sectors are all in negative territory, although defensive sectors are somewhat more resilient, i.e. utilities, consumer staples and healthcare. In terms of individual movers, Commerzbank (-4.0%) fell to a new record low of EUR 5/shr as the German banking rout deepens following a Germany GDP Q/Q contraction and as the bank tracks German yields. Meanwhile, Balfour Beatty (+9.0%) and RWE (+1.9%) rose to the top of the Stoxx 600 after earnings, with the latter raising its interim dividend.

Top European News

In FX, the traditional safe-haven currencies and their commodity compatriot Gold have regained some composure after yesterday’s sharp/abrupt fall from grace on the resumption of US-China trade talks and decision to defer/waiver certain items from the list of Chinese imports that were due for 10% tariffs on September 1. Subsequent comments from President Trump indicate that the concessions are not in response to any progress in negotiations or reciprocity from Beijing, but an effort to avoid US consumers feeling the pinch over the festive period. Meanwhile, latest Chinese data has also dampened spirits with ip and retail sales both falling short of expectations, though the PBoC has stalled the measured Yuan depreciation and Usd/Cny ended on-shore trade below the official fix. Usd/Jpy back down around 106.00 and Usd/Chf is pivoting 0.9730 as Xau/Usd returns to justy above 1500/oz mark amidst faltering risk sentiment.

In commodities, WTI and Brent prices have held onto the bulk of their trade-driven gains in which the benchmarks soared around USD 3/bbl after the USTR decided to delay tariffs on some Chinese goods until December 15th. Sentiment drove yesterday’s gains, although ultimately, the demand outlook remains unchanged unless material progress can be made in dialogue, i.e. if the nations overcome sticking points which broke down talks last time. The relief rally had begun to peter out in Asia-Pac and European trade, with some aid from a surprise build in API stockpiles (+3.7mln vs. Exp. -2.8mln). WTI residing around its 50 DMAs at 56.08/bbl whilst its Brent counterpart remains around 60.50/bbl. PVM notes that if Brent fails to hold its 13 DMA (60.55/bbl), then it’ll likely cause a 5-day gap narrowing dip to around the 5 DMA at 59.29/bbl. Traders will now be looking ahead to the weekly DoE data for confirmation of the API numbers. ING notes that last week’s release saw a surprise build driven mainly by a fall in crude oil exports. “The relative strength in WTI vs. Brent, means we could see another week of poor exports”, analysts say. Elsewhere, gold has made some gains above the 1500/oz mark after finding a base at 1480/oz yesterday from the trade-driven unwind of safe-haven positions. Meanwhile, copper prices are on the backfoot as yesterday’s optimism wanes in EU trade and disappointing Chinese IP prints exacerbated the downside, with some additional pressure after exports of the red metal from Peruvian port of Matarani have now resumed following a three-week suspension due to protests.

US Event Calendar

DB’s Craig Nicol concludes the overnight wrap

Just when you thought we were getting away with a rare period of calm from trade headlines, yesterday afternoon’s announcement that the Trump administration was to delay 10% tariffs on some Chinese products until mid-December quickly put an end to any hope of that. Risk-on was back in force, however the inherent problem for markets with these trade headlines is the predictability of how unpredictable they are, both with regards to timing and substance so it makes it incredibly difficult to take short term views while things remain so fluid.

That didn’t bother risk assets though, with the S&P 500 gaining +1.50% to more than retrace Monday’s decline. The benchmark index has now traded +/-1% in five of the last seven sessions, the longest such streak since December. Tech shares outperformed, with the NASDAQ, FANG, and Philly semiconductor indexes rallying +1.95%, +2.53%, and +2.95%, respectively, as several broad categories of high-tech imports from China were in the basket of goods which will not be tariffed on 1 September. Apple (+4.23%), Qualcomm (+3.41%), and Micron (+4.84%) paced gains. In Europe, the STOXX 600 reversed losses of as much as -0.87% to ultimately close +0.54% higher.

The moves in rates were sharp as well, with two-year treasuries retracing yesterday’s rally to end +8.3bps higher. The rise in 10-year yields was more muted, up only +5.9bps. Both were affected by the risk-on sentiment and flows out of safe havens, but the front-end also had to deal with the strong CPI inflation print (more below). As a result, the market is now pricing 57bps of Fed cuts this year, from 66bps as of Monday. Those reduced fed odds contributed to a flatter yield curve, with the 2y10y spread down -2.5bps to just 3.3bps, having touched a low of 0.8bps in the New York afternoon. As we’ve highlighted many time the 2y10y is our favourite recession indicator and as it flirts with inversion we’ve become more concerned about the downside risks.

In other markets, oil was boosted by the trade de-escalation, with WTI advancing +3.95% to $57.10/bbl. The US cash HY energy index rallied -16bps, helping the overall HY index to tighten -13bps, The VIX index fell -3.6pts to 17.5, which is actually relatively elevated from its 6-month average of 15.0. Meanwhile, EM currencies gained +0.48%, despite another bloodbath for the Argentine peso, which weakened a further -5.00% versus the dollar. The biggest EM mover was the offshore yuan, which gained +1.29% during US trading on trade optimism.

As for the actual details of the tariff announcement, the most substantive news was the decision to delay tariffs on around $150bn of imports until at least 15 December. Around $100bn of imports will face the 10% tariff effective on 1 September. That leaves several tens of billions of goods unaccounted for, though they could just be the result of rounding, other exemptions, or errors. The USTR’s press release said that some items would be removed for “health, safety, national security and other factors.” As for the goods which will see delayed tariffs, the list includes cell phones, laptops, video games, toys, and computer monitors, which explains the tech outperformance mentioned above. President Trump later confirmed that he decided to delay the tariffs to avoid impacting the Christmas shopping season, which may be taken as a tacit admission that tariffs result in higher prices for US consumers, as our economists have argued. Fittingly, “art for nativity scenes” was also among the items be delayed beyond the Christmas season.

The trade headlines came not long after a much more risk unfriendly CPI report in the US. Indeed the July core CPI reading of +0.3% mom was ahead of consensus for +0.2% and in doing so it pushed up the annual reading to +2.2% yoy and thus matching the highs from January. Amazingly, that is the first time since 2001 that we’ve had two rounded readings of at least +0.3% mom for the core. The 3m annualized rate is also now at +2.83% which is the second highest during the current cycle. On top of that, there were no obvious outliers in the details which is another indication of the broadness in strength in the data. So, however you cut and slice it this was a strong reading. That being said the moves in rates were quickly overtaken by the tariff story headlines.

Overnight, Asian markets are following Wall Street’s lead with the Nikkei (+0.63%), Hang Seng (+0.55%), Shanghai Comp (+0.75%) and Kospi (+0.75%) all up. That being said, most markets are off their intraday highs following weak Chinese data overnight (more on that below). As for FX, the CNY is trading at 7.0234 (+0.28%) while other Asian currencies are also trading up with the South Korean won (+0.79%), Indian rupee (+0.75%) and Indonesian rupiah (+0.70%) all making gains. Elsewhere, S&P 500 futures are flat.

Just on the China data, industrial production in July was confirmed at 4.8% yoy which was well below expectations for 6.0% yoy and also the weakest reading since 2002 while retail sales also came in at +7.6% yoy (vs. +8.6% expected). There was a smaller miss for fixed asset investment which came in one tenth lower than expectations at 5.7% yoy while the surveyed jobless rate rose two tenths versus last month to 5.3% and thus matching the recent highs from February. So, a weak slew of data and one which begs the question how long is China willing to tolerate weaker growth and higher joblessness. Needless to say that the downside risks to growth are now on the rise.

In other news, the Telegraph is reporting that House of Commons Speaker John Bercow said that he will refuse to allow PM Johnson to suspend U.K. Parliament to secure Brexit. He said, “We cannot have a situation in which Parliament is shut down – we are a democratic society. And Parliament will be heard and nobody is going to get away as far as I am concerned with stopping that happening.” Meanwhile, in Italy lawmakers have summoned PM Conte to appear before the Senate on August 20, with Bloomberg suggesting that this could lead to a confidence vote in the upper house, or possibly even his resignation of further delays.

The other highlight of the data yesterday and which ultimately got overshadowed was a shocking August ZEW survey in Germany. The -44.1 expectations reading was not only well below consensus for -28.0 but marked a monthly decline of -19.6pts which was the most since July 2016 and second most since 2012. Staying with Germany, the final July CPI revisions threw up no surprises with the +0.4% mom reading unrevised versus the flash. The data in the UK was also broadly in line with earnings printing at +3.9% 3m/yoy while the unemployment nudged up one-tenth to 3.9%. The other data release worth flagging was the July NFIB small business optimism reading in the US which rose 1.4pts to 104.7 (vs. 104.0 expected).

To the day ahead now, where the main focus of the data this morning will be Germany’s Q2 GDP release where expectations are for a -0.1% qoq print. We’ll also get Q2 employment data in France, and July CPI readings in France and the UK. We’ll then round off the data in Europe with the preliminary Q2 GDP print for the Euro Area. In the US this afternoon it’s a bit quieter for data with the July import price index reading the only data of note.

via ZeroHedge News https://ift.tt/300hb8B Tyler Durden