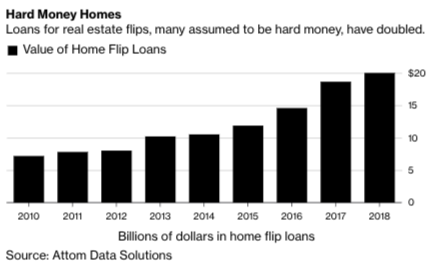

The American Association of Private Lenders says the number of hard money lenders is approximately 8,300, up 40% since 2016, reported Bloomberg.

A hard money loan is an asset-based loan financing through which a borrower receives capital secured by the property. The volume of these loans to house flippers last year rose to $20 billion. That’s up 37% from 2016 and about double the figure from 2014. ATTOM Data Solutions believes hard money is a significant source of lending for house flippers.

“There’s a lot of activity. Every time I turn around there’s new entrants,” said Glen Weinberg of Fairview Commercial Lending in Evergreen, Colorado.

While Weinberg usually loans up to 60% of a property’s value, some newer lenders will go up to 90%, he said.

Blackstone Group LP and Goldman Sachs Group Inc. recently dove into the hard money lending space, drawn by interest rates of 8% to 12%.

About ten years from the real estate trough in 2009, the outlook is starting to seem worrisome for flippers and their hard money financiers.

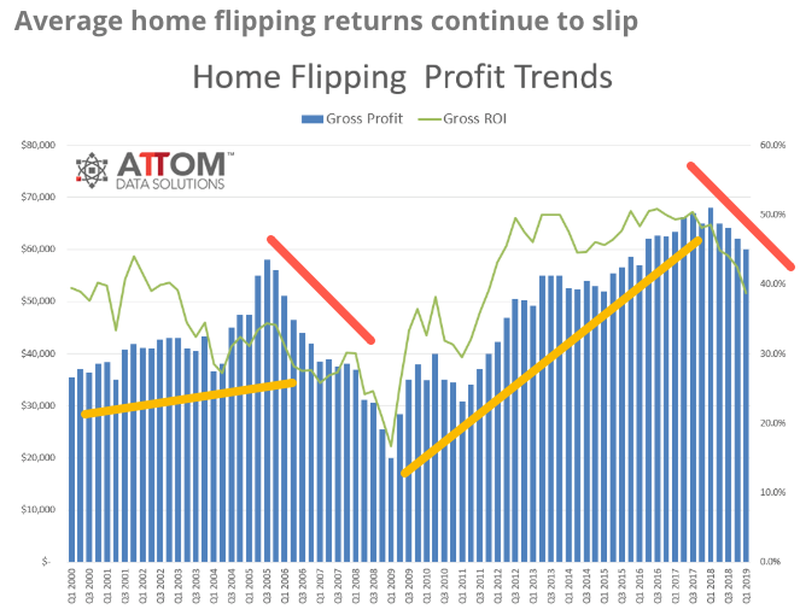

ATTOM Data Solutions published a new report earlier this month called Q1 2019 US Home Flipping Report, which shows house-flipping volume rebounded across the country earlier this year as gross profits and return on investment fell.

In Atlanta, house flippers want to put up smaller down payments than ever before, said Michael Braswell, a broker who works with hard money lenders.

“I would say, probably more than half the deals that come across my desk are not viable deals,” Braswell said.

Nationwide, 49,000 homes flipped in 1Q19, represented 7.2% of all home sales last quarter, up from 5.9% MoM and up 6.7% YoY, the highest home flipping rate since 1Q10. While this could be interpreted as a sign of continued progress, it also may suggest that investors are unloading their homes while they still can, Attom’s Todd Teta told Bloomberg this month.

The West Coast has seen some of the most significant house flipping declines in the country.

Bloomberg said hard money lenders aren’t forecasting a downturn in the real estate market just yet, but as we have mentioned before, many have overlooked the economy cycling down into 2H19.

As Zerohedge readers would know, any disruption in hard money lending and or a downturn in the house flipping market would be a ‘canary in the coal mine’ that could suggest the overall housing market will continue to deteriorate into 2020.

via ZeroHedge News http://bit.ly/2IRYjBb Tyler Durden

For months now the markets have been in denial that ECB President Mario Draghi has any answers to the Euro-zone’s problems. Today’s statement confirms what anyone with eyes to see has been saying.

There is no Plan B.

Draghi started the year saying he would end his various QE programs and by June he’s not only put them back on the table (New TLTRO in September) but has now opened up the possibility of taking rates lower.

Draghi told an ECB conference in Sintra, Portugal, that “further cuts in policy rates… remain part of our tools.” He added that there was “considerable headroom” to re-start bond purchases, which inject newly created money into the financial system in the hope of boosting lending and economic activity.

Draghi has been exposed as swimming naked, as Warren Buffet would put it.

The fun part is that Draghi used the cover of Trump’s trade war with everyone to justify a policy that was inevitable anyway.

In response, President Trump piled on accusing Draghi of being a currency manipulator. And then announced his upcoming meeting with Chinese Premier Xi Jinping to hammer out a trade deal.

Trump backed himself into a corner with China, essentially demanding it give the U.S. ultimate say over its fiscal, monetary and trade policy.

The Chinese aren’t going to agree to that any more than the Palestinians are going to agree to a Palestinian State in name only, administered like a Native American reservation by Israel.

Lebanon is not going to accede to Pompeo’s demands to remove Hezbollah from its government. North Korea isn’t going to give up its nukes so the U.S. will allow it to trade with dollars. Negotiations with Trump are nothing of the sort.

They are terms of surrender.

And Trump, in full re-election mode, is running around telling his MAGApede followers, “China broke the deal.”

There never was any deal. There was a draft agreement China took back to Beijing and altered to suit the demands of any sovereign nation. And Trump threw a temper tantrum which is creating massive uncertainty all across the capital markets.

So don’t have any hopes of seeing a deal with China that is substantively different than the one we currently have. Because Xi is no more going to cave to Trump’s idiotic demands than Draghi will admit central banking is a failure.

I’ve warned readers time and again that Trump is an economic ignoramus. Draghi’s dovishness is a response to the very policies Trump has implemented. Sanctions and tariffs on everyone that looks at him sideways creates uncertainty.

Uncertainty creates fear. And fear means deflation. In a confidence-based system a lack of it leads to hoarding of the currency most needed by everyone to do business.

This isn’t rocket science folks, but it is beyond the ken of His Orangeness.

So, while markets soared on the news that the ECB would commit hari kiri gold pumped and then dumped just as quickly as Trump took hold of the algorithms for a Warhol-like fifteen minutes.

Gold continues to struggle to find a perch above $1350 getting rebuffed every time it gets there by the flimsiest of excuses. Today it was Trump’s tweet about meeting with Xi.

Gold was up on the news of the ECB loosening things up even more. Then it was sold on the idea that China and the U.S. would kiss and make up, freeing up trade. At this point there is little rhyme or reason as to what’s happening in the gold market.

So the day-to-day movements can be hard to parse. After an explosive couple of weeks gold moved to briefly touch $1,360 to end the week before pulling back hard to $1,340. At the same time the euro and the British pound reversed their short-term rallies to continue sinking into oblivion on Brexit-anxiety as Boris Johnson handily won the opening round of the Tory leadership struggle.

On Friday a weak euro sent gold down. Today it rose until Trump got his mitts on it. It is interesting to note that intraday volatility is rising as the bulls keep pushing it up against the massive overhead resistance in place since the high put in just after the original Brexit vote in July of 2016.

The fight for this level is intensifying as bulls keep pressing but the demand for immediate dollars is strong enough that we see violent dumps into strength.

Remember, no one important wants to see gold rise through the cap currently in place. When it does it will be the biggest tell of all that Draghi, Jerome Powell at the Fed and the rest of the central bankers don’t have any answers for what is happening.

And we’re going to find out tomorrow just how few answers they have. I’m still of the opinion that Powell will hold off on a rate cut here to keep the Fed’s reputation and independence intact, as least nominally. The more Trump screams, the less likely the Fed will cut until it looks like their idea.

Trump will bitch but it won’t matter. The Fed will hold off here as long as possible even though the yield curve inversion gets deeper. The stock markets are still near record highs, hated on poor fundamentals, so the Fed doesn’t have to act here.

There is something else that has the markets spooked. The U.S. Dollar LIBOR curve is now also inverted, signaling short-term funding worries.

The announcement earlier in the week that Deutsche Bank is looking at spinning off a “Bad Bank” may be part of what we’re looking at here. As Jeff Snider wrote about on Monday, if DB bet wrong on a global reflation for 2018-19 which failed in a big big way last year then it would account for why there has been such a rush out into sovereign debt as DB is sitting on a mountain of bad bets which need to be cordoned off.

And that’s probably why Draghi’s position has so thoroughly shifted in the past two meetings. Trump is irrelevant in this mess, except that his misunderstanding of the situation can and will lead him to pour gasoline on an already roaring fire while he rails about trade theft.

But look carefully at what’s happening. I reiterate what I’ve been saying for months. Gold is strong alongside the a rising dollar. Equities continue levitating and safe-haven sovereign bonds continue to defy gravity right alongside them.

This isn’t a recession that has the markets spooked. It’s something far larger. Draghi’s admitted defeat, joining Kuroda at the Bank of Japan. All that’s left is Powell. If he surprises with a rate cut expect gold to explode and the dollar to briefly sell off before turning higher as the smart money understands what it really means.

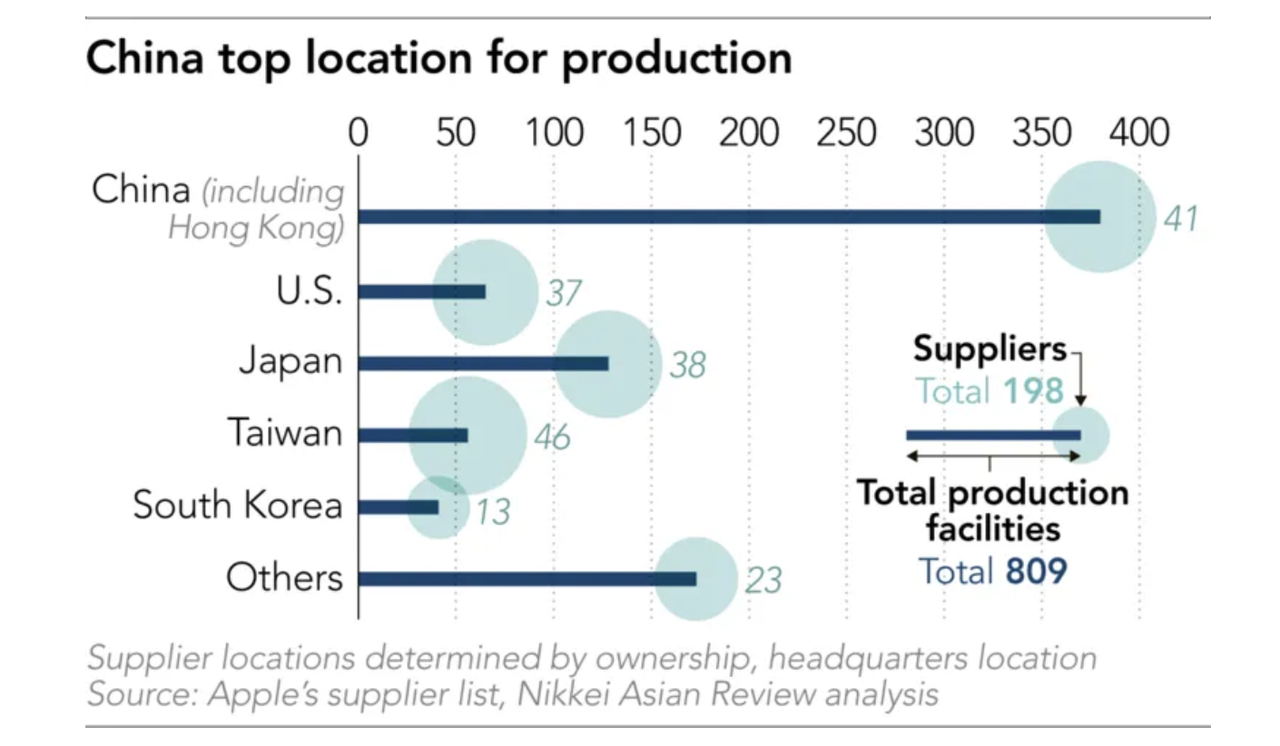

Since the trade war began last year, analysts have been closely parsing every production-related decision by Apple and its suppliers, seeing them as bellwethers of the global consumer-tech industry: Will the American tariffs permanently restructure the global supply chain? Increasingly it’s looking that way. Because not long after a Foxconn executive warned that the largest manufacturer of iPhones in mainland China was ready to help Apple shift production elsewhere, Nikkei reports that suppliers for iPhones, iPads, MacBooks and Apple Ear Pods have all drawn up plans to move 15%-30% of production outside of the mainland, with India, Vietnam, Mexico and Malaysia looking like the top alternatives.

At this point, even if Washington doesn’t follow through with plans to slap tariffs on another $300 billion in goods, companies, including Foxconn, Pegatron, Wistron, Quanta Computer, iPad maker, Compal Electronics, and AirPods makers Inventec, Luxshare-ICT and Goertek have all been asked by Apple to evaluate options outside of China.

Other suppliers are watching these companies, and monitoring where they go.

“We need to know where those big assemblers are heading to so that we can initiate our plan too,” an executive at an Apple component supplier told Nikkei.

Apple supplier Wistron has assembled cheaper iPhones in India since 2017, and Foxconn started assembling more iPhones there this year, but volumes have been very small. More than 90% of Apple’s products are still assembled in China. And last year, the number of mainland Chinese and Hong Kong-based suppliers surpassed the number from the US and Japan for the first time, accounting for 41 of the top 200 suppliers.

This is the biggest reason why Apple needs its suppliers to write up plans for long-term “diversification” of production. But trade tensions aren’t the only issue with China: Apple also raised demographic issues like lower birth rates. Ultimately, millions of jobs in China are at risk.

The California-based tech giant’s request was triggered by the protracted trade tensions between Washington and Beijing, but multiple sources say that even if the spat is resolved there will be no turning back. Apple has decided the risks of relying so heavily on manufacturing in China, as it has done for decades, are too great and even rising, several people told Nikkei.

“A lower birthrate, higher labor costs and the risk of overly centralizing its production in one country. These adverse factors are not going anywhere,” said one executive with knowledge of the situation. “With or without the final round of the $300 billion tariff, Apple is following the big trend [to diversify production],” giving itself more flexibility, the person added.

China has been the production base on which Apple’s global success has been built over the past two decades. The country has not only been able to rally hundreds of thousands of skilled workers at short notice to fill rapidly rising orders as the company grew, but an extensive and complex ecosystem of components, logistics and talent has built up in and around Apple manufacturing sites.

Some 5 million Chinese jobs rely on Apple’s presence in the country, including those of more than 1.8 million software and iOS App developers, according to a study available on the company’s website. Apple itself employs 10,000 staff in China, the company said.

If Apple and its suppliers decide to follow through, the changes won’t happen right away: In any case, Apple moving 15% of its iPhone production out of China would be a “gargantuan endeavor,” laden with risks like supply-chain disruption and higher costs according to Wedbush. The Wedbush team estimates it would take two-to-three years to pull off. Suppliers appear to agree.

Suppliers admit that replicating this network elsewhere will take time, and China is likely to remain Apple’s most important manufacturing base for the foreseeable future. “It’s really a long-term effort and might see some results two or three years from now,” said one supplier.

“It’s painful and difficult, but that’s something we have to deal with.”

But the trade war has prompted Apple to seriously consider meaningful diversification for the first time, say several sources. At the end of last year, the company began to expand its so-called capital expense studies team, according to sources familiar with the matter.

The team of more than 30 people is discussing production plans with suppliers and negotiating with governments over financial incentives they might be willing to offer to attract Apple manufacturing, as well as regulations and the local business environment.

But at this point, it looks like nothing short of the complete reversal of trade war tensions would stop Apple from directing suppliers to move at least some production elsewhere on a permanent or semi-permanent basis. Which means that whatever Trump and Xi decide in Osaka, best case scenario, it will be too little too late for China, leaving China’s dominance of the tech components and assembly business in jeopardy.

As often as Beijing insists that Washington will feel the greater sting from the trade tensions, this is a major area of vulnerability for China.

via ZeroHedge News http://bit.ly/2ISDcyB Tyler Durden

After yesterday’s torrid, euphoric surge on the back of Draghi’s dovish deluge and Trump’s announcement of a G-20 meeting with Xi, world stocks were rather muted, holding near two-week highs on Wednesday, and in the case of the S&P500 just shy of all time highs as investors bet on a worldwide wave of central bank stimulus…

… amid growing expectations that the United States and the euro zone may deliver interest rate cuts as early as July.

Which of course has put Powell in a very difficult position: with Trump demanding by the day, if not hour, that the Fed cur rates, just how does the Fed Chair pull it off without looking political when since the March FOMC meeting: i) stock prices are higher; ii) the unemployment rate fell to a 50-year low; iii) growth forecasts have improved; iv) the tariffs on Mexico that prompted the latest calls for rate cuts have been taken off the table. We’ll find out in just over 6 hours.

Meanwhile, Draghi already capitulated “pre-emptively” on Tuesday, frontrunning the Fed, when in one of the biggest policy reversals of his eight-year tenure, Draghi flagged more easing if inflation failed to pick up, firing up markets and resulting in one of the biggest one-day moves in global stocks of 2019.

But, as Reuters notes, some caution seeped in after the previous day’s frenzy. German and U.S. bond yields, which hit record lows and two-year lows respectively after Draghi’s comments, inched higher to trade just off those levels.

European shares slipped off six-week highs in early trading (although they have since rebounded) and Wall Street futures indicated a slightly weaker opening on Wednesday. Most of the concern is down to the U.S. Federal Reserve’s meeting, the decision of which is due at 1800 GMT. It is widely expected to follow the lead of the European Central Bank and open the door to future rate cuts.

“It should be really clear to absolutely everyone that this is a monetary policy turning point … Those rate cut expectations have now shifted much closer,” said Ulrich Leuchtmann, head of currency and emerging markets research at Commerzbank, quoted by Reuters. “Of course the other question is: What is the Fed doing? If the Fed takes the fundamental risk of political pressure seriously, they cannot do anything today,” he said, noting that Trump’s strident calls for lower interest rates posed a dilemma for the Fed.

Meanwhile, futures are almost fully priced for a quarter-point easing in July and imply more than 60 basis points of cuts by Christmas. As for Europe, markets have almost fully priced a cut in September, though some analysts, such as those at Germany’s Commerzbank, now say rates will be cut in July, rather than in the last quarter of the year as they had predicted earlier.

The risk is that for all the clamor for easing creates risks that policymakers will disappoint.

“Market expectations for a dovish shift are nearly universal, the only question seems to be the degree,” said Blake Gwinn, head of front-end rates at NatWest Markets, referring to the Fed. “Markets will be looking for validation of this pricing. We think this represents a fairly high bar for the Fed to deliver a dovish surprise.”

It wasn’t just central banks though: Bullish market sentiment was reinforced by news that Trump will meet Chinese leader Xi Jinping at the G20 summit this month, even though many doubt the two men can reach a breakthrough on ending their trade dispute.

MSCI’s global equity index rose 0.4%, adding to Tuesday’s 1% gain, as Asian shares excluding Japan followed the lead of their European and U.S. counterparts to jump almost 2% — their biggest one-day rally since January as investors bet on a possible easing of U.S.-China trade tensions. Technology shares led the rally after President Donald Trump said he would meet Chinese counterpart Xi Jinping at the G-20 summit next week. All markets in the region were up, with Hong Kong and Taiwan leading gains, while Australian stocks hit an 11-year high. The Topix gauge climbed 1.7%, as Keyence and SoftBank provided the biggest boosts. Construction stocks rose after a magnitude 6.7 earthquake struck off the northwest coast of Japan.

Over in China, the Shanghai Composite Index closed 1% higher, as brokerage shares jumped on a media report that China encouraged banks to boost liquidity support for securities firms. The S&P BSE Sensex Index fluctuated, with Kotak Mahindra Bank rising and Mahindra & Mahindra declining. India’s second-biggest life insurer said it was time to take money out of the nation’s equities.

In rates, the yield on 10-year Treasuries pared some of the drop from a day earlier, after reaching the lowest level since September 2017 at 2.016%, a world away from the 3.25% top touched in November last year. The yield rose slightly from those lows but is down some 60 bps since January, while that of Japan’s benchmark sank to the lowest since August 2016 at -0.145%. German yields were close to the minus 0.33% record low hit on Tuesday, while Japanese yields

The fallout in currencies has been significantly less, mostly because it is hard for one to gain when all the major central banks are under pressure to ease. The euro did pull back after Draghi’s comments, but at $1.118 it touched only a two-week low. The dollar eased slightly on the yen to 108.3, but was flat versus a basket of currencies. The yuan touched three-week highs versus the dollar on the trade news. The pound gained for a second day.

In commodities, the rate-cut buzz kept gold just off 14-month highs at $1,345.16 per ounce. Brent crude futures however slipped 0.6% to $61.75 a barrel, pressured by economic growth worries.

Expected data include mortgage applications. Oracle and Steelcase are reporting earnings

Market Snapshot

S&P 500 futures little changed at 2,924.50

STOXX Europe 600 little changed at 384.68

MXAP up 1.8% to 157.98

MXAPJ up 1.8% to 518.37

Nikkei up 1.7% to 21,333.87

Topix up 1.7% to 1,555.27

Hang Seng Index up 2.6% to 28,202.14

Shanghai Composite up 1% to 2,917.80

Sensex up 0.1% to 39,086.68

Australia S&P/ASX 200 up 1.2% to 6,648.13

Kospi up 1.2% to 2,124.78

German 10Y yield rose 2.2 bps to -0.298%

Euro up 0.09% to $1.1204

Italian 10Y yield fell 18.0 bps to 1.753%

Spanish 10Y yield rose 4.2 bps to 0.435%

Brent futures down 0.5% to $61.82/bbl

Gold spot down 0.3% to $1,342.61

U.S. Dollar Index little changed at 97.60

Top Headline News from Bloomberg

Facing pressure from Wall Street and President Trump, Fed Chairman Powell and his colleagues may be running out of patience

President Trump said he had a “very good” phone conversation with Chinese counterpart Xi. The two will hold an extended meeting at the G-20 summit on June 28-29, Trump said on Twitter

Boris Johnson extended his lead over his rivals in the race to become Britain’s next prime minister and looked poised to pick up more votes as the hardest Brexiteer in the contest was eliminated

Trump administration is weighing three sanctions packages to punish Turkey for its purchases of the Russian S-400 missile-defense system, according to people familiar

Japan’s exports fell for a sixth month as U.S.-China trade tensions add to concerns about global demand and economic growth

President Trump asked White House lawyers earlier this year to explore his options forremoving Jerome Powell as Fed chairman, according to people familiar

Trump officially announced his campaign for re-election, delivering a speech thick with grievance in which he warned of a dark future for America if his opponents win in 2020

An OPEC committee sees global oil inventories contracting by almost 500,000 barrels a day if the group continues restraining supply in the second half of the year, a delegate said

China is stepping up efforts to avert a funding squeeze among the nation’s banks and securities companies after a rare government seizure of a small lender triggered concerns about a vital part of the nation’s financial plumbing.

Wednesday’s Federal Reserve rate decision carries more wild cards than most. While market participants don’t expect a rate cut this time around, they do see lower rates this year

The Trump administration is weighing three sanctions packages to punish Turkey over its purchases of the Russian S-400 missile- defense system, according to people familiar with the matter. The most severe package under discussion between officials would all but cripple the already troubled Turkish economy

Asian equity markets rallied across the board as the region followed suit from the heightened global risk appetite due to a double dosage of optimism from ECB President Draghi’s hints of potential easing and after US President Trump confirmed a meeting with his Chinese counterpart at the G20. ASX 200 (+1.2%) and Nikkei 225 (+1.8%) were higher with Australia led by energy names after a surge in oil prices and with outperformance also seen in the trade sensitive industries such as tech, materials and miners, while the Japanese benchmark gapped above the 21K level fuelled by favourable currency flows and strength in commodity-related sectors. Hang Seng (+2.5%) and Shanghai Comp. (+1.0%) were buoyed after US President Trump announced the resumption of US-China trade talks and that he will be conducting an extended meeting with Chinese President Xi at the G20 following “a very good” telephone conversation between the 2 leaders, while the PBoC were also supportive with the announcement of liquidity injections through reverse repos and its medium-term lending facility. Finally, 10yr JGBs were higher after the dovish comments from ECB’s Draghi added to the declining global yields narrative which saw a drop in 10yr JGB yields to their lowest since August 2016, while the BoJ also kick starts its 2-day policy meeting where they are expected to maintain current policy settings and reaffirm guidance of keeping rates at very low interest rate levels for an extended period of time at least through around Spring 2020.

Top Asian News

Agung Jumps as Jakarta Issues Permit for Reclamation Projects

Nomura Jumps on $1.4b Buyback, Governance Tweaks

Boutique Firm Led by Ex-UBS Banker Said to Bid for Abraaj Funds

KKR Is Said to Near Partial Exit From $2b Helicopter Firm

European equities are tentative [Eurostoxx 50 Unch] as the region gears up for the FOMC rate decision later today (Full preview available in the Research Suite). Sectors are mixed, underperformance is seen in defensive stocks with healthcare, utilities and consumer staples all lower. In terms of movers, STMicroelectronics (+3.2%) and Infineon (+2.7%) shares gained following a broker move at Morgan Stanley and Bernstein respectively. On the flip side, Steinhoff (-6.5%) opened at the foot of the Stoxx 600 after the Co.’s delayed 2018 results posted losses, whilst Belgian retailer Colruyt (-12.2%) plunged on disappointing earnings.

Top European News

Airline Shares Fall as HSBC Sees More Profit Warnings Ahead

Piraeus Tests Risk-Hungry Market With CCC Rated Greek Bank Debt

U.K. Inflation Returns to BOE Target on Air Fares, Car Prices

German Property Stocks Fall on Fears of Rent Regulation Ahead

In FX, relatively tight lines are being drawn ahead of the FOMC in G10 land, as is often the case, but the Greenback has clawed back some losses against EMs after Tuesday’s euphoria over the US and China reopening lines of communication on the trade front. However, the index is braced for the Fed within a confined 97.683-553 range, and seemingly reluctant to breach chart/psychological resistance or support around 97.639 (61.8% Fib retracement of pull-back from 98.373 ytd peak to recent 96.451 low) and 97.500 respectively in the run up – see the Ransquawk Research Suite for a full preview.

GBP/CHF – Bucking the overall muted trend, Cable has continued its recovery towards 1.2600 after broadly in line with forecast UK CPI and PPI data and ahead of the BoE tomorrow, while Eur/Gbp has also retraced further to test 0.8900 compared to circa 0.8975 before ECB President Draghi’s apparent dovish Sintra revelations. Similarly, the Franc is consolidating back above parity and over 1.1200 vs the single currency as markets tread more cautiously in wake of yesterday’s risk-on session.

EUR/JPY/CAD/AUD/NZD – All narrowly mixed vs the Buck, as noted above, with the Euro licking wounds inflicted by latest dovish ECB vibes and back on the 1.1200 handle where extremely heavy option expiry interest is anchored (5.2 bn 10 pips either side of the big figure). The Yen is also wary of BoJ guidance skewed towards ongoing or even more stimulus, and bound by hefty expiries as 2.95 bn rolls off at the 108.00 strike and 1.3 bn between 108.30-40 vs the 108.25-61 range so far. Elsewhere, the Loonie awaits Canadian CPI data and is holding above 1.3400 with decent expiries from 1.3350-70 (1.2 bn) in close proximity, while the Aussie and Kiwi are both maintaining their recovery momentum over 0.6850 and 0.6500 respectively ahead of RBA Governor Lowe and NZ Q1 GDP, with the former not unduly ruffled by the latest in a growing list of calls for more rate cuts.

EM – The Lira is back on the rack and underperforming amidst the general retracement noted above, and the renewed threat of US sanctions against Turkey has lifted Usd/Try off recent lows to 5.9150+ at one stage. Elsewhere, the Rand has unwound some of its Eskom-related outsize gains despite firmer the forecast SA CPI, with Usd/Zar rebounding through 14.5000.

In commodities, WTI and Brent futures are marginally lower on the day as yesterday’s upbeat sentiment in the complex somewhat wanes ahead of today’s DoE release. Last night’s API numbers showed a slightly narrower-than-forecast draw in crude stocks (-0.81mln vs. Exp. -1.1mln) . Traders will be keeping an eye on the more widely followed DoE numbers for any short term direction (crude stocks expected to draw by 1.077mln barrels), ahead of tonight’s FOMC meeting. On the OPEC front, the oil producers have decided to hold the OPEC meeting on July 1st and the OPEC+ meeting on the 2nd following weeks of indecisiveness. Elsewhere, gold is unwinding some of its risk premium amid President Trump and his Chinese counterpart showed willingness to reignite US-Sino trade talks at the G20, albeit the yellow metal is certain to be swayed by tonight’s Fed meeting and presser. Meanwhile, copper is little changed but holds onto most of its trade-driven gains. Finally, Dalian iron ore futures spiked higher by almost 6% as the base metal followed the broad rally across assets.

US Event Calendar

7am: MBA Mortgage Applications -3.4%, prior 26.8%

2pm: FOMC Rate Decision

DB’s Jim Reid concludes the overnight wrap

Wherever you’re reading this, get comfortable as this is a long one today after probably the biggest day of the year for market moving news. We’ll start by recycling the famous quote, “When the facts change, I change my mind. What do you do?”.

After yesterday’s huge day in financial markets it no longer feels appropriate to be tactically underweight credit. To recap, we decided to move to this position in May as the trade escalation left us feeling that weak markets or poor economic data were needed to push the US and China into meaningful talks. To be fair we did initially see weak markets and slipping economic data but then came a huge change in market pricing of central bank activity, first in terms of the Fed and then the ECB, culminating in Draghi’s extremely dovish signal yesterday. If that wasn’t enough, our weekend sources in Washington which we detailed on Monday were proved correct as Mr Trump tweeted just after the US open that he will meet with China’s President Xi at next week’s G-20. So the balance of risks (and there still are a lot of risks) have become more balanced and more supportive of the carry trade of which credit is a key one. So the path of least resistance now seems tighter for credit, with European credit likely to be additionally propped up by expectations that CSPP is a step closer after yesterday (see this note from last week for more on how to assess the probabilities of this). The risks to the view is that the events of the last month are already leading to a global slowdown that central banks can’t do much about and/or that the Trump/Xi G20 talks end up going nowhere and we get the final round of tariffs applied very soon after and then further escalations. The next hurdle is today’s FOMC which is another much anticipated moment. The market and Mr Trump have put a lot of pressure on the Fed. It’s hard to imagine that they’ll disappoint given all that’s going on but we should note that under Mr Powell, nine out of ten FOMC meeting days have seen equities down. We’ll preview in full below.

Before we go through the details of Mr Draghi and Mr Trump’s significant comments, respectively, it’s worth starting with markets where we can now list new all-time yield lows for 10y bonds. Germany, Denmark, Netherlands, Austria, Finland, Sweden, France, Belgium, Slovakia, Ireland, Slovenia, Latvia, Spain, Portugal, Cyprus and Croatia all experienced this yesterday. Indeed it wouldn’t be a surprise if we missed one or two. Bunds rallied -7.6bps to close at the eye wateringly low level of -0.322%, OATs hit an intraday low of -0.004% – the first time they have been below 0% – while yields in Sweden and Austria closed at -0.027% and -0.052%, both below 0% for the first time too. BTPs also rallied -18.5bps which is the biggest one-day move since October. If you want a scary example of just how extreme the rates move was, then Austria’s 100y bond rose 5.5pts yesterday, taking it to a cash price of 156.9. That means it has jumped nearly 40pts YTD already, equivalent to a -61.2bp fall in yield so far in 2019. The coupon on that bond is 2.1% and the yield is now just 1.14%. Oh, and it has a duration of 51.8! You’d be hard to pressed to find many fixed income assets which have delivered a bigger return YTD. Yesterday’s moves were even more remarkable since they were driven by collapsing real yields as inflation expectations perked up. The European five year-five year inflation swap rate popped up 8.9bps to 1.23%, which is still extremely low by historical standards but was the biggest rise since March 2012.

The move for European rates reverberated throughout the US too. Indeed 10y Treasuries rallied -3.5bps (though they were down -7.9bps before the Trump tweet) and are now down to 2.060%, the lowest level since September 2017. They have held that level overnight also. The 2s10s curve also dipped to 19.15bps (-2.8bps on the day). The amount of negative yielding debt in the world now is around $12.5tn and the most ever. Oh, and the Bund curve is now negative out to 18 years. The other side of the coin for markets was a big rally for risk. The STOXX 600 (+1.67%) had its best day since January. The DAX, CAC and FTSE MIB also all closed up more than 2% while in the US the S&P 500, NASDAQ and DOW ended +0.97%, +1.39% and +1.35%, respectively. Despite the yield move, banks rose +1.54% in Europe (possibly on hints of tiering alongside rate cuts) and +1.79% in the US. EM equities also finished +2.44%, their best session since January, while HY credit spreads were -10bps and -6bps tighter in Europe and the US, respectively. Oil also rallied +3.79%, helped by the improved risk sentiment but also by news that the OPEC+ group will meet to discuss a possible extension to their supply cuts. Finally the euro finished down -0.21% – a fairly modest move all things considered, though -0.43% from its pre-Draghi level.

Overnight in Asia markets are following Wall Street’s lead with the Nikkei (+1.71%), Hang Seng (+2.37%), Shanghai Comp (+1.50%) and Kospi (+1.11%) all posting decent gains. In rates, yields on 10y JGBs are down -2.1bps to -0.158%, thereby hitting the lowest yield since July 2016 and testing the limits of the BoJ’s target range. In other news, here in the UK, the Times reported overnight that the Labour Party leader Jeremy Corbyn will today back a move to change the party’s Brexit policy and support a second referendum in all circumstances. This supposedly follows rising internal pressure from his own MPs. Meanwhile, as we go into the print, Bloomberg is reporting that the Trump administration is weighing three sanctions packages to punish Turkey over its purchases of the Russian S-400 missile-defense system. The Turkish lira is trading down -0.71% on the news.

Back to Draghi, where the most significant statement was “in the absence of improvement, such that the sustained return of inflation to our aim is threatened, additional stimulus will be required”. He added “in the coming weeks, the Governing Council will deliberate how our instruments can be adapted commensurate to the severity of the risk to price stability” and that “further cuts in policy interest rates” remain part of the ECB’s toolkit. The plural “cuts” didn’t go unnoticed, and nor did the reference to “how” instruments can be changed, rather than “if.” Draghi went on to say that the “APP still has considerable headroom,” possibly signaling a relaxation in the 33% country limit on purchases. Peter Praet, former ECB Chief Economist whose term ended 3 weeks ago, also added to Draghi’s comments by saying that the ECB will look at tiering if a rate cut moves onto the agenda. There’s little doubt that this counts as a u-turn compared to the June meeting, as evidenced by markets yesterday. The ECB has joined the Fed and the question is how much easing is there to come. Markets are now pricing in around 9bps of cuts by the September meeting, plus another 5bps between September and December. So fully pricing at least one 10bps cut before the year is out. We should also note that overnight, anonymously sourced articles (per Bloomberg) said both that rates will the primary tool before restarting QE and that the options are still being considered.

Beyond the immediate implications for rates, the shift by the ECB will have reverberations throughout and beyond the euro area. It will likely become increasingly difficult for other major central banks, like the BoE, BoJ, and BoC, to tighten policy in the face of European easing. Perhaps more interestingly, there will likely be increased focus on the fiscal authorities to act in concert with the central bank. Draghi devoted a section of his speech to discussing fiscal policy. He said it “should play its role” and that monetary easing works best “if fiscal policies are aligned with it.” He also criticised the fiscal response post-crisis, where he argued that the countries with fiscal space should have made better use of their position by pursuing more expansionary policy, rather than the several percentage points of GDP of tightening that we ultimately got in the event. So the ECB this week have definitely stepped up pressure on governments to do more. Ironically by doing more themselves they actually take pressure off governments to some degree!

Trump had his own say on the ECB, tweeting that “Mario Draghi just announced more stimulus could come, which immediately dropped the Euro against the Dollar, making it unfairly easy for them to compete against the US. They have been getting away with this for years, along with China and others” and that “German DAX way up due to stimulus remarks from Mario Draghi. Very unfair to the United States!” Later in day, news broke that the White House legal office had considered the potential for Trump to demote Fed Chair Powell, to take his chairmanship away but not fire him. It is not clear if that would be legal, but in any event White House economic advisor Kudlow told reporters that Trump is not currently considering that option. However, when reporters asked the President directly about Powell after markets had closed, Trump responded “let’s see what he does.”

It was Trump’s tweet about a “very good telephone conversation” with President Xi of China that was more significant for markets though. Trump confirmed that the two would have an “extended meeting” at the G-20 meeting and that the respective teams of both would begin talks prior to this. Chinese state media confirmed that Xi and Trump had spoken by phone and that Xi had agreed to meet at the G-20. Significantly, Xi also said that the two had agreed that “trade teams should keep talking to solve issues”. While it’s still hard to predict, at the very least this feels like the timeline for any escalation has been pushed back, while the prospect for an agreement has risen. So it was unsurprising to see risk do so well on the back of the headlines.

One final note to add on yesterday’s trade and political news. USTR Lighthizer testified for the Senate and discussed the administration’s trade policy. He didn’t provide much new information, but did say that the apparent deal to avert tariffs with Mexico makes it “more likely” that the administration reaches a deal with China. He also said that tariffs have proven to be a useful negotiating tool, and talked up the odds of trade deals with Japan and Europe, though legislators indicated that many roadblocks remain.

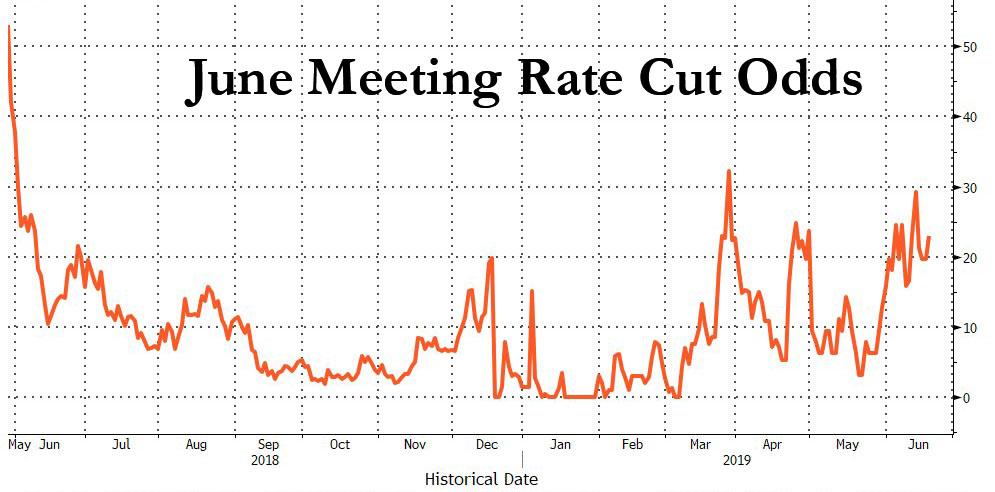

What a time to have a Fed meeting then. The market is pricing in a fairly small chance of a rate cut today – 20% to be precise – and it does feel like the big question is how much the Fed swings to endorsing market pricing which is still for 83bps of cuts over the next 12 months. Our US economists expect the statement to drop its “patient” narrative and adopt language similar to Powell’s recent statement that the Committee will “act as appropriate to sustain the expansion.” This shift should signal that downside risks are building and that the Committee stands ready to lower rates in the coming months if the macro and markets environment justify it. The dots should show some movement in this direction, with the median dot likely to be flat in the coming years and some individual dots calling for cuts this year, but the SEP should stop short of having the median dot imply cuts. Powell’s press conference is likely more important than the dots and this is his chance to reinforce the dovish tilt. More from our US economists can be found here .

Turning quickly to yesterday’s economic data, which was understandably overshadowed by the other news. The highlight was Germany’s ZEW survey. The expectations measure fell -19pts to -21.1, the sharpest drop since July 2016 and the lowest level since November. On the other hand, the current situation measure fell only -0.4pts to 7.8, slightly better than expected. Euro area core CPI was confirmed at 0.8% yoy. In the US, housing starts fell -0.9% mom in May, worse than expected, but the prior month was revised 1.1pp higher to 6.8, leaving the trend steady. Building permits rose 0.3% mom, a touch better than the 0.1% expected.

To the day ahead, where the obvious highlight is the aforementioned Fed meeting. Away from that we’ve got May PPI data due out of Germany this morning, and the May inflation data docket from the UK along with the June CBI survey. Sintra also continues so expect more headlines there. Finally the Tory party leadership debate will see another round of voting.

If you’ve got this far well done…… and thank you!!!

via ZeroHedge News http://bit.ly/2IoZ9q6 Tyler Durden

Blackadder II is one of the best ever British TV comedies: forget Mr Bean and watch Rowan Atkinson as Edmund Blackadder try to connive his way through the dangerous medieval court of Queen Elizabeth I. Episode 5 (Beer) is of particular relevance today. In it, Blackadder entertains his elderly aunt and uncle, both puritans, in the hope of charming a huge inheritance from them. Yet due to a scheduling mix-up, just down the corridor courtiers have come for an evening of debauched drinking with the alcohol-intolerant Blackadder, and the first to pass out has to pay a fine of 10,000 florins – which Edmund doesn’t have. Our anti-hero sits at the dining table to entertain his tedious relatives…

Edmund: So, how are we all going, then?

Aunt: Not well. Let us discuss your inheritance.

Edmund: Ah, yes, good. Erm, a little drink, first?

Aunt: [stands] Drink?! [slaps him twice] Wicked child!!! Drink is urine for the last leper in Hell!

Edmund: Oh, no, no–this is only water. This is a house of simple purity.

[Drunk monk enters in convulsions. He rushes to the fireplace and vomits, then turns and begins to leave.]

Monk: Great booze-up, Edmund!

[very awkward, long pause]

Aunt: Do you know that man?

Edmund: [looks behind himself as though he didn’t really see] No…

Aunt: He called you `Edmund’…

Edmund: Oh, *know* *him*…oh, yes, I do.

Aunt: Then can you explain what he meant by `great booze-up’?

Edmund: [thinks … thinks … thinks … thinks … thinks … thinks … thinks] Yes, I can… My friend…is…a missionary… and… on his last visit abroad… brought back with him…the chief of a famous tribe… *His* name is Great Bu… He’s been suffering from sleeping sickness…and he has obviously just woken…because, as you heard, “Great Bu’s up”.

What, is the relevance of all this? Yesterday we heard the ECB’s Draghi explain why six months after ending QE and talking of rates going up, he is now open to rate cuts and more QE, and never mind rules that say he can’t buy more bonds. The reason for the complete U-turn? “Great Bu’s up”, basically. Yes, there was technobabble about forward guidance being enhanced by “adjust[ing] its bias and its conditionality to account for variations in the adjustment path of inflation,” which was enough to make anyone suffer from sleeping sickness. But basically, inflation is as down as ‘Bu’ is up, and so are bond yields, to below zero in fact, in new European countries at longer maturities than ever been experienced before. Mr. Draghi – you win a negative-yielding inheritance from those elderly relatives….and an attack from President Trump for allowing too much policy stimulus! This is a “Great Bu’s-t up” that drags us into even weirder places.

Of course, the ECB follow the RBA, who are not even funny because we can see the punchline coming. Their “Great Bu’s up” for another rate cut promised “sooner rather than later” is that unemployment now conveniently needs to be below 4.5%…just as the housing market slumps.

Today we are all going to hear the Fed tell their own “Great Bu’s up” to explain why they are about to cut rates when unemployment is so low; job gains are still reasonable for this stage in the cycle; key data is far from dire on the surface; and equities are close to all-time highs. Yes, they can point to the bond market. However, what “Great Bu” can the Fed offer to explain why for the past 18 months it is *them* who have been suffering from sleeping sickness? And how do they explain it was President Trump–who “twists and turns like a twisty-turny thing” to quote Edmund’s drinking opponent Lord Melchett–who was right about rates when all their models and experts were wrong? Surely it’s all coincidence that yesterday we got a news report that the White House had considered “demoting” Fed Chair Powell in February(?) In short, expect lots of po-faced technobabble, and po-faced copy-and-paste analysts will write up how reasonable it all sounds. Yet the long and the short of it is that this is, like Blackadder II, a classic farce.

It’s even more farcical when one considers Trump is twisty-turny enough that now he will be having an extended meeting Xi at the G20 after a phone call with him. Perhaps Xi, who as we are endlessly told “wants a trade deal”, is visiting North Korea’s Kim tomorrow: will he be putting in a good word on the nuclear front for Trump as a quid pro quo or co-ordinating positions vs. the US? We shall see. (NB, We still deeply remain sceptical of any real trade breakthroughs.)

Trump also managed to twist and turn enough yesterday that recent Iranian attacks on oil tankers aren’t important enough for a US counter-attack on Tehran, only holding nukes is according to Trump – you know, the things that Kim already has. So no bombing in the Middle East today at least, thankfully; but a further sign that Trump, often called dangerous by his critics, is actually more war averse than many past US presidents. (Which will no doubt be noted for future reference by those choking on US sanctions and tariffs, as we mentioned earlier this week).

In short, it’s mainly reasons for optimism in terms of key news–trade, Iran, and even the moderate Rory Stewart is the most likely challenger to Boris Johnson after the second round of the Tory leadership contest!–but nonetheless the backdrop right now is of an underlying central-bank promise of lower, and negative, rates for ever…and a race to who gets there fastest.

Perhaps central banks hope that if they promise markets enough liquidity we won’t ask probing questions about if they really know what they are doing or not or, as Blackadder does when sozzled, to point an accusatory finger saying “*I* know who you are! You are Merlin the Happy Pig!!!” Instead, they hope we will all get completely sloshed, as at the end of “Beer”, and end up in a pile singing “See the little goblin, see his little feet / And his little nosy-wose — isn’t the goblin sweet?”

The equity markets already are!

via ZeroHedge News http://bit.ly/2XipM8x Tyler Durden

With Turkey’s purchase of the Russia S-400 missile-defense system looking like a done deal, the Trump Administration, which claims it already made Ankara its ‘best offer’ on the US Patriot missile-defense system, is trading the carrot for the stick and, in a non-too-subtle message to Erdogan and his senior advisors, warned that, if Turkey goes ahead with the purchase, the US will drive Turkey’s nascent defense industry into ruin with CAATSA.

Just days after Turkish officials warned that the S-400 purchase was as good as done, Bloomberg reported on Wednesday that Trump is feeling ‘bipartisan’ pressure from Congressional leaders to impose CAATSA sanctions against Turkey, and the administration has devised three plans for retaliation.

Since technically any country that buys defense equipment from Russia is eligible for American sanctions, Congressional leaders are reportedly arguing that there’s no legal reason to excuse Turkey from the sanctions (which appear to be applied on an ad hoc basis, seeing as America’s idle threats haven’t stopped India and others).

The last time Trump took an aggressive tack with Turkey, he came away with the win: everybody who insists that punitive tariffs don’t work should first remember Turkey’s decision to release pastor Andrew Brunson, made after Washington doubled metal tariffs on the country in August and slapped sanctions on two senior government officials. The result? Brunson was released shortly afterward.

And Trump is hoping the strategy will work again, though, so far at least, Turkey has shown no indication that it plans to back down.

The US has been considering possible sanctions for well over a year as it became clear Turkey wasn’t going to back down. A leading proponent was Wess Mitchell, the assistant secretary of State for European affairs who stepped down earlier this year.

“This has the potential to spike the punch,” Mitchell said of the S-400 purchase in Senate testimony in June 2018. “We can’t be any clearer than saying that both privately and publicly, that a decision on S-400 will qualitatively change the U.S.-Turkish relationship in a way that would be very difficult to repair.”

Yet Turkey has so far refused to back down. Part of the country’s calculation, according to people familiar with the matter and outside experts, is that Erdogan believes he can split Trump off from the rest of his administration and persuade him that buying the S-400 isn’t a big problem.

Which is why Trump has developed his three plans, all of which would involve using CAATSA to impose sanctions, and the most serious of which would ‘cripple the Turkish economy’. At the very least, Washington will likely cut off sales of any new F-35s to the NATO ally.

The Trump administration is weighing three sanctions packages to punish Turkey over its purchases of the Russian S-400 missile-defense system, according to people familiar with the matter.

The most severe package under discussion between officials at the National Security Council and the State and Treasury departments would all but cripple the already troubled Turkish economy, according to three people familiar with the matter, who asked not to be identified discussing internal deliberations.

Any of the options would come on top of the months-old U.S. pledge to cut off sales of the F-35 jet to Turkey if President Recep Tayyip Erdogan keeps his vow to buy the Russian system.

The idea with the most support for now is to target several companies in Turkey’s key defense sector under the Countering America’s Adversaries Through Sanctions Act, or CAATSA, which targets entities doing business with Russia. Such sanctions would effectively sever those companies from the U.S. financial system, making it almost impossible for them to buy American components or sell their products in the U.S.

But there’s still the G-20 summit in Osaka, where it’s believed Trump and Xi will have an opportunity to meet. It’s not clear how BBG knows this, but Erdogan is reportedly hoping he can speak to Trump alone in Osaka, and split him off from the rest of his advisors, like he did when he convinced Trump to pull American troops from Syria.

via ZeroHedge News http://bit.ly/2Fj0UDi Tyler Durden

A crisis is brewing in the Eurozone and it’s not even on mainstream media radar. Italy is at the center of the crisis.

BOT stands for Buoni Ordinari del Tesoro (Ordinary Treasury Bonds).

Mini means the denomination is smaller than the lowest denomination of regular treasury bonds, which is €1,000, thus “Mini-BOT”.

Il minibot da 100 euro fronte/retro come l’abbiamo immaginato qui, su twitter, alla luce del sole. Con una votazione che ha visto Enrico Mattei e la sua Urbino prevalere su Camillo e Adriano Olivetti, Pietro Ferrero e Giovanni Agnelli. pic.twitter.com/iO19W0LkRN

— Claudio Borghi A. (@borghi_claudio) June 9, 2019

The Italian government, led unofficially by deputy prime ministers Matteo Salvini (League) and Luigi Di Maio (Five Star Movement) both support the idea of a parallel currency.

The technocrat prime minister, Giuseppe Cont, is not calling the shots and threatened to resign over this issue.

ECB president, Mario Draghi, proclaimed “Mini-BOTs are either money and then they are illegal, or they are debt and then the stock of debt goes up. I don’t think there is a third possibility.”

The two parties that make up the fractious governing alliance – the hard-Right League and the Five Star Movement – want to introduce a new type of government bond that would be used to pay off the state’s debts to companies and individuals.

Both the League and Five Star are deeply eurosceptic and have in the past mooted the idea of abandoning the common currency, with Matteo Salvini, the League’s combative leader, last year calling the euro “a mistaken experiment that has damaged jobs and the Italian economy“.

The idea of introducing mini-BOTs has alarmed Europe, with Mario Draghi, the head of the European Central Bank, saying on Thursday that they would either amount to a parallel currency, in which case they would be illegal, or they would simply add to Italy’s towering debt.

He received support a day later from Vincenzo Boccia, the president of Confindustria, Italy’s employers’ federation, who said: “We are on the same wavelength as Draghi about the mini-bots because it would just mean more public debt.”

“There’s a complicated game going on between the League, Five Star, the Quirinale (the residence of the president of Italy, Sergio Mattarella), ministers and the prime minister,” said Prof Giovanni Orsina, a professor of politics at Luiss University in Rome.

Showdown Coming Soon

A showdown is certain.

The timing is unknown, but it is sooner rather than later.

At the moment, France is also in breach of economic rules and there is this “little” thing called Brexit on the ECB and EU’s mind.

So the EU will do what it always does, pretend there is no crisis and hope it goes away. But it won’t.

Meanwhile, Italy wants to do this and will do this, but it would rather the EU trigger the event.

Path Set

Italy’s budget is not close to meeting EU rules.The EU has threatened Excessive Deficit Procedures against Italy.

The EU will bush this aside debt targets for as long as it can, but the fate is sealed. The EU will either have to abandon its rules or fine Italy.

The upcoming fine and a spike in Italian bond yields will be the trigger for Italy to escalate the crisis with Mini-BOTs.

The longer the EU waits, the more time Italy has to prepare for the Mini-BOT launch.

I expect this to trigger within a year, and possibly months.

Italy is set to leave the Eurozone. The Mini-BOT is the transition mechanism. Few see it coming.

via ZeroHedge News http://bit.ly/2WRmSD8 Tyler Durden

Following yet more tense intercepts involving Russian and US jets which reportedly occurred over the Black and Baltic Seas on Monday, Russia’s Ministry of Defense (MoD) has released new video showing one of these latest incidents.

International media reports cited that at least two encounters between US and Russian planes took place early this week, with one of them possibly over or at least near Crimea.

“The crews of Russian Su-27 fighter jets… have intercepted US Air Force B-52H strategic bombers, that approached Russian state border from the Black and Baltic seas,” the MoD said in a statement.

The US Air Force also confirmed the incident, saying that multiple nuclear capable B-52 long-range bombers had conducted missions in support of the annual NATO-led Baltic Operations (BALTOPS) hosted out of Romania.

The newly released footage is from the cockpit of one of the Su-27 jets sent to intercept a B-52 flying from the West.

The MoD further said that no violations of Russia’s borders took place; however, one report based on US military sources and radar said that one US B-52 made a flight path “straight at Crimea” in what “could have been a mock strike run”.

Russia says that it sent Su-27 Flankers to intercept multiple U.S. Air Force B-52 Stratofortresses flying over both the Baltic Sea and Black Sea regions today. In one of the encounters, one of the bombers was flying directly toward the Crimean Peninsula, which the Kremlin occupies, in what could have been a mock strike run. Another one of the B-52s subsequently made an emergency landing at RAF Mildenhall in the United Kingdom following an unrelated in-flight emergency. — The Drive

There’s been a dramatic uptick in such incidents of the past few years, with Pentagon officials routinely condemning the Russian pilots’ “unprofessional behavior”.

Meanwhile Moscow has repeatedly condemned expansion and the extent of NATO military games in Baltic and East European states.

The MoD has in multiple incidents over the past months warned against US and NATO planes coming “dangerously close to the border” – which has made it necessary to intercept the aircraft.

via ZeroHedge News http://bit.ly/2IOkOac Tyler Durden

“The cultural level of a nation is mirrored by its rate of interest: the higher a people’s intelligence and moral strength, the lower the rate of interest.” Thus declared economist Eugen von Böhm Bawerk, according to Richard Sylla and Sidney Homer’s classic tome A History of Interest Rates. By that logic, Europe is the domain of superhumans, as the overnight deposit rate has resided below zero since June 2014 and at negative 40 basis points since March 2016.

The M.D. overseeing Europe’s monetary affairs has his own version of the Hippocratic Oath. Speaking at the ECB’s annual forum at the resort town of Sintra, Portugal today, ECB president Mario Draghi made waves by suggesting the central bank will impose still lower interest rates:

Further cuts in policy interest rates and mitigating measures to contain any side effects remain part of our tools. . . Negative rates have proven to be a very important tool in the euro area.

In the absence of improvement, such that the sustained return of inflation to our aim is threatened, additional stimulus will be required.

The implications are clear. Claus Vistesen, chief eurozone economist at Pantheon Macroeconomics, told Bloomberg: “Draghi is going to finish his tenure [set to end on Oct. 31] with a cut. The door is now open and I don’t see how they can not walk through it.” Mike Riddell, fund manager at Allianz Global Investors, noted: “The ECB has just handed the bond bulls an ammunition dump.”

Five years and counting into the negative rate era, the ECB’s increasingly radical policies designed to hot up inflation simply haven’t worked. Eurozone CPI rose just 1.2% year-over-year in May, the lowest figure in over a year. Likewise, the “five year, five year inflation swap rate,” Draghi’s preferred metric for the future inflation expectations that the central bank is so eager to manipulate, fell to a record low 1.14% on Friday, since rebounding to 1.23% but still well below the five-year average of 1.48%, let alone the ECB’s now-symmetrical, “close to 2%” bogey.

While inflation stubbornly refuses to follow the playbook, the bond market has been more easily cowed. Following Draghi’s remarks today, the French 10-year yield temporarily broke below zero for the first time ever, while Sweden (which resides outside of the eurozone currency bloc but is an E.U. member state) also saw its 10-year borrowing costs make their first ever foray into negative territory.

More broadly, the worldwide sum of negative-yielding debt instruments rose to $11.8 trillion as of yesterday, up from less than $6 trillion as recently as last fall and within range of the record $12.2 trillion seen in July 2016 (when the 10-year Treasury yielded less than 1.4%, compared to 2.06% today). Never in the 4,000 years of human history, per Sylla, were negative rates seen in substantial size prior to this cycle. The upside-down policy rate extends to the less-creditworthy members of the E.U., as Baa3/triple-B-rated Italy and B1/double-B-minus-rated Greece saw their 10-year yields fall to 2.12% and 2.51%, respectively, not far above the split-rated (triple-A at Moody’s, double-A-plus at S&P) United States.

Bloomberg’s global negative rate index by market capitalization since January 2010

The peculiar state of affairs has not seemed to help the Old Continent’s frail banking system, which lags far behind global peers in terms of profitability and valuation (Almost Daily Grant’s, May 28). As the banks list, one of the shakiest institutions continues to search for answers. Bloomberg reports today that Deutsche Bank A.G. (which has seen shares fall 84% in the last nine years to less than 21% of its year-end 2018 book value) CEO Christian Sewing is set to “purge” a number of top executives and is also “zeroing in on another round of deep trading cuts that may result in the shuttering of the U.S. equities” division.

Others take a different tack. Speaking on a conference panel this morning, Cornelius Riese, co-CEO of Frankfurt-based DZ Bank A.G. (Germany’s second-largest by assets), observed that negative rates indeed “have a huge impact on banks.” Riese ventured to offer some gentle criticism of Draghi & Co.’s grand policy experiment: “Maybe at the end of the story, in three to five years, we will notice it was a historical mistake.”

Not everyone was so circumspect. This morning, Donald Trump took to Twitter to complain:

Mario Draghi just announced more stimulus could come, which immediately dropped the Euro against the Dollar, making it unfairly easier for them to compete against the USA. They have been getting away with this for years, along with China and others.

Sad!

via ZeroHedge News http://bit.ly/2KZpb51 Tyler Durden

Depending on who you are in the United States, trust in the news has either sky-rocketed or nose-dived, according to Reuters Digital News Report.

As Statista’s Sarah Feldman notes, about half of people on the left trust the news most of the time, while merely 9 percent of people on the right trust the news most of the time. Looking at the data, President Trump’s entrance into the presidential election certainly acted as an inflection point, driving the public’s perception of news trust worthiness to either side of the political spectrum.

As a point of comparison, the United Kingdom has seen the opposite trend. Back in 2015, there was about a 10-percentage point gap in the trust worthiness of news between people on the opposite side of the political spectrum. During that time, the U.S. had a similar spread in trust between partisans. After 2015, the UK had its own inflection point: Brexit. Instead of being further driven apart, that trust gap has narrowed, though overall both sides trust the news less than they did in 2015.

{kind=link}