Today, President Trump signed an executive order placing significant restrictions on the issuance of new work visas through 2020. The ban covers:

(a) an H-1B or H-2B visa, and any alien accompanying or following to join such alien;

(b) a J visa, to the extent the alien is participating in an intern, trainee, teacher, camp counselor, au pair, or summer work travel program, and any alien accompanying or following to join such alien; and

(c) an L visa, and any alien accompanying or following to join such alien.

The executive order also extends the prohibition on issuing most new green cards that was originally supposed to last 60 days and expire today. Many commentators saw it coming from the start that this extension would happen.

The restrictions were made known under the sinister headline of a “Proclamation Suspending Entry of Aliens Who Present a Risk to the U.S. Labor Market Following the Coronavirus Outbreak”. The trope of scary foreigners coming and “taking away” jobs from Americans reigns supreme. When it comes to immigration law, the Trump administration has certainly not let any good crisis go to waste.

from Latest – Reason.com https://ift.tt/319TNZw

via IFTTT

This is the week when the movement to reform Section 230 of the Communications Decency Act got serious. The Justice Department released a substantive report suggesting multiple reforms. I was positive about many of them (my views here). Meanwhile, Sen. Josh Hawley (R-MO) has proposed a somewhat similar set of changes in his bill, introduced this week. Nate Jones and I dig into the provisions, and both of us expect interest from Democrats as well as Republicans.

The National Security Agency has launched a pilot program to provide secure DNS resolver services for US defense contractors. If that’s such a good idea, I ask, why doesn’t everybody do it, and Nick Weaver tells us they can. Phil Reitinger’s Global Cyberalliance offers Quad9 for this purpose.

Hackers used LinkedIn’s private messaging feature to send documents containing malicious code which defense contractor employees were tricked into opening. Nick points out just what a boon LinkedIn is for cyberespionage (including his own), and I caution listeners not to display their tats on LinkedIn.

Speaking of fools who kind of have it coming, Nick tells the story of the now former eBay executives who have been charged with sustained and imaginatively-over-the-top harassment of the owners of a newsletter that had not been deferential to eBay. (Wired, DOJ)

It’s hard to like the defendants in that case, I argue, but the law they’ve been charged under is remarkably sweeping. Apparently it’s a felony to intentionally use the internet to cause substantial emotional distress. Who knew? Most of us who use Twitter thought that was its main purpose. I also discover that special protections under the law are extended not only to prevent internet threats and harassment of service animals but also horses of any kind. Other livestock are apparently left unprotected. PETA, call your office.

Child abusers cheered when Zoom buckled to criticism of its limits on end-to-end encryption, but Nick insists that the new policy offers safeguards for policing misuse of the platform. (Ars Technica, Zoom)

I take a minute to roast Republicans in Congress who have announced that no FISA reauthorization will be adopted until John Durham’s investigation of FISA abuses is done, which makes sense until you realize that the FISA provisions up for reauthorization have nothing to do with the abuses Durham is investigating. So we’re giving international terrorists a break from scrutiny simply because the President can’t keep the difference straight.

Nate notes that a story previewed in April has now been confirmed: Team Telecom is recommending the blocking of a Hong Kong-US undersea cable over national security concerns.

Gus reminds us that a bitter trade fight between the US and Europe over taxes on Silicon Valley services is coming. (Politico, Ars Technica)

Nick and I mourn the complete meltdown of mobile phone contact tracing. I argue that from here on out, some portion of coronavirus deaths should be classified as mechanogenic (caused by engineering malpractice). Nick proposes instead a naming convention built around the Therac-25.

And we close with a quick look at the latest data dump from Distributed Denial of Secrets. Nick thinks it’s strikingly contemporaneous but also surprisingly unscandalizing.

You can subscribe to The Cyberlaw Podcast using iTunes, Google Play, Spotify, Pocket Casts, or our RSS feed. As always, The Cyberlaw Podcast is open to feedback. Be sure to engage with @stewartbaker on Twitter. Send your questions, comments, and suggestions for topics or interviewees to CyberlawPodcast@steptoe.com. Remember: If your suggested guest appears on the show, we will send you a highly coveted Cyberlaw Podcast mug!

The views expressed in this podcast are those of the speakers and do not reflect the opinions of their institutions, clients, friends, families, or pets.

from Latest – Reason.com https://ift.tt/2YXZdnV

via IFTTT

There is room for debate over when it is appropriate to rename institutions or remove or relocate statutes and memorials to disgraced public figures. For myself, I think the burden on those calling for such changes should be rather high, and I generally prefer supplementing such memorials or displays–such as by adding statues or memorials of other, more deserving figures–over removal. History is important, including (perhaps especially) when it concerns our shortcomings as a nation.

The one context in which I think such historical effacement is justified concerns memorials to leaders of the Confederacy. While I think it is perfectly appropriate, indeed important, to have such historical artifacts in museums and appropriate venues, I think it is appropriate to remove the names and visages of Confederate leaders from places of honor. There is no good reason to have such statutes in public squares or the names of Confederate generals on U.S. military bases.

My reasons are quite simple: The Confederacy was a traitorous uprising expressly inspired by a desire to maintain slavery as a racial institution.

While the true causes of secession have not always been adequately covered in history books (some of which repeat the fable that southern states seceded over tariffs or suggest it was a “war of Northern aggression), the historical record is abundantly clear. The South seceded over slavery, preemptively seeking to leave the Union after their preferred candidate lost the Presidential election.

The relevant original documents speak for themselves. As southern states seceded, they identified the need to protect slavery as their cause, expressly repudiated the principles of the Declaration of Independence, and were more-than-willing to trample the rights of free citizens in the service of protecting slavery (as well as to prohibit any of the confederate states from seceding).

In his infamous “Cornerstone Speech”, Confederate vice president Alexander Stephens declared:

The constitution, it is true, secured every essential guarantee to the institution while it should last, and hence no argument can be justly urged against the constitutional guarantees thus secured, because of the common sentiment of the day. Those ideas, however, were fundamentally wrong. They rested upon the assumption of the equality of races. This was an error. It was a sandy foundation, and the government built upon it fell when the “storm came and the wind blew.”

Our new government is founded upon exactly the opposite idea; its foundations are laid, its corner-stone rests, upon the great truth that the negro is not equal to the white man; that slavery subordination to the superior race is his natural and normal condition. This, our new government, is the first, in the history of the world, based upon this great physical, philosophical, and moral truth.

The Confederate states seceded from the Union, and started a war, to protect the institution of slavery. (And, yes, the Confederacy started the war—announcing secession before Abraham Lincoln had been inaugurated, and firing the first shots Fort Sumter.)

And they lost, too.

This history is something to remember, but neither the secessionist cause, nor its leaders, are something to commemorate.

from Latest – Reason.com https://ift.tt/3fLJZJk

via IFTTT

China Kicks Off 10 Day Dog Meat Festival Tyler Durden

Mon, 06/22/2020 – 20:30

You’d think eating random animals – not to mention pets – in China would be frowned upon at this point. But a little global pandemic hasn’t stopped organizers from kicking off a 10 day dog meat festival, despite pushback from activists and government, according to the South China Morning Post. This despite earlier reports that China would no longer market dogs as livestock.

The festival is known to attract “thousands of visitors” who buy dogs “for the pot” that are on display. Animal rights activists are trying diligently to get the festival disbanded permanently.

Animal rights activist Peter Li said: “I do hope Yulin will change, not only for the sake of the animals but also for the health and safety of its people. Allowing mass gatherings to trade in and consume dog meat in crowded markets and restaurants in the name of a festival poses a significant public health risk.”

The article claims that the coronavirus has forced China to “reassess its relationship with animals”, although with an event like, well, a 10 day dog meat festival, it appears to us the country has a lot more reassessing to do.

Back in April, Shenzhen banned the consumption of dogs and other provinces are expected to follow suit. The agriculture ministry also decided to classify dogs as pets instead of livestock, SCMP noted. That did not last long.

Another activist, Zhang Qianqian, said: “From what we understand from our conversations with meat sellers, leaders have said the consumption of dog meat won’t be allowed in future. But banning dog-meat consumption is going to be hard and will take some time.”

via ZeroHedge News https://ift.tt/3drJcf9 Tyler Durden

22 Market Observations From Goldman’s Head Of Hedge Fund Sales Tyler Durden

Mon, 06/22/2020 – 20:10

By Tony Pasquariello, global head of HF Sales at Goldman

For the financial markets, the period since late February has been a watershed – a genuinely epic sequence of action and reaction.

In tactical terms, there’s no shortage of stories to recount. there was the day when S&P closed down … 12% (and, thereafter, the VIX touched 85). or, the time when the US long bond rallied 40bps … in 24 hours. and, to be sure, no greatest hits list would be complete without reference to the futures expiry when WTI sold off, ahem, 305%.

Jumping off those points, below is a simple layout of 22 line items that stuck out to me over the course of the past several months.

This sequence wasn’t constructed to represent a cohesive theme or directional bias, but I think we can agree on the following: this period has been epochal. we’re passing the early chapters. and, perhaps most importantly, the interplay between the financial markets and policy has been truly enormous and without precedent; the undeniable fact that government has been an overwhelming force in markets is shot through the list below:

1. 2020 has likely featured the sharpest — but, the shortest — recession in US history (certainly since the 1850s for the US, and since WWII on a global scale). credit: Jan Hatzius, GIR.

2. in turn, we’ve just seen the strongest rally out of a bear market since … 1932. credit: Ben Snider, GIR.

3. the US alone had conducted $2.3tr of QE in the past three months (Treasuries + mortgages). for those keeping score at home, that’s an average of around $35bn of bond buying per business day since mid-March. credit: David Mericle, GIR.

4. GIR expects zero interest rates in the US for several more years — until the economy reaches 2% inflation and full employment — which is perhaps not until 2025 (link).

5. GIR expects another $1.5tr of US fiscal support to come this summer (link).

6. largely thanks to fiscal support, GIR expects US disposable income to grow 4.0% in 2020 (link).

7. the US Treasury planned to borrow $3tr in Q2 alone (link); despite that supply glut, we’re just off the all-time low yields in US 2yr notes and 5yr notes.

8. in that same general context, US 30yr mortgage rates are down to all-time lows (link).

9. the past six weeks have seen the largest amount of global equity issuance on record, at $205bn (link).

10. March saw record outflows from corporate bond funds (-$42bn); we’re now witnessing record inflows to corporate bond funds (+$85bn since the start of April); link.

11. it’s not just that we’re witnessing record new issue in the credit markets, it’s that we’re also seeing record low corporate financing costs (e.g. AMZN raised $10bn of capital at the lowest 3/5/7/10 and 40yr yields ever; link).

12. March saw record outflows from equity mutual funds and ETFs; one can argue we’re now seeing legitimate signs of retail investor euphoria (e.g. a record # of account openings at US retail brokers; link).

13. buybacks: GS executed repurchase is down ~ 50% YTD (link). that said, it wouldn’t be surprising to see AAPL + MSFT + GOOG collectively buy back $75bn this year.

14. subject to your interpretation: the market cap of MSFT is larger than the entire US High Yield market (link).

15. Michele Della Vigna, GIR: “we estimate that clean tech can drive $1-2tr pa of green infrastructure investments and create 15-20mm jobs worldwide, mostly through public-private collaboration, low financing costs and a supportive regulatory framework … renewable power will become the largest area of spending in the energy industry in 2021” (link).

16. related: ESG funds comprised 31% of all YTD flows to global passive equity funds (link).

17. randomly found in a comment section on the world wide web: “does not capitalizing the first word in a paragraph make a writer appear to be cool or is it simply that Tony Pasquariello is an idiot.” I’m not bolding any part of this sentence.

Finally, these were some of the more striking charts from H1’20:

18. for better or for worse, this clearly illustrates the top heavy nature of S&P 500 returns YTD (credit to Cole Hunter, GIR):

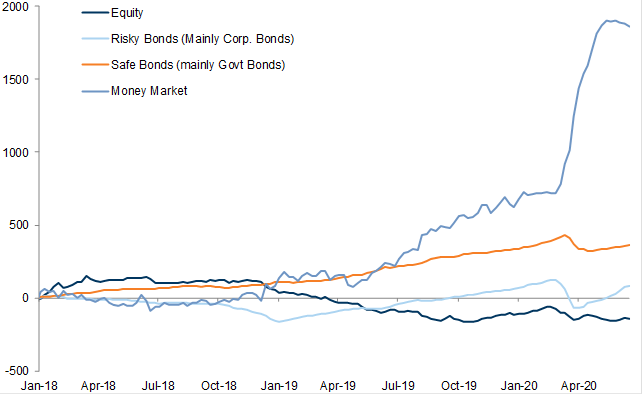

19. despite an absence of available yield, we live in a world of record inflows to money market funds (link). I find it a little interesting that we’re seeing a tentative inflection lower here:

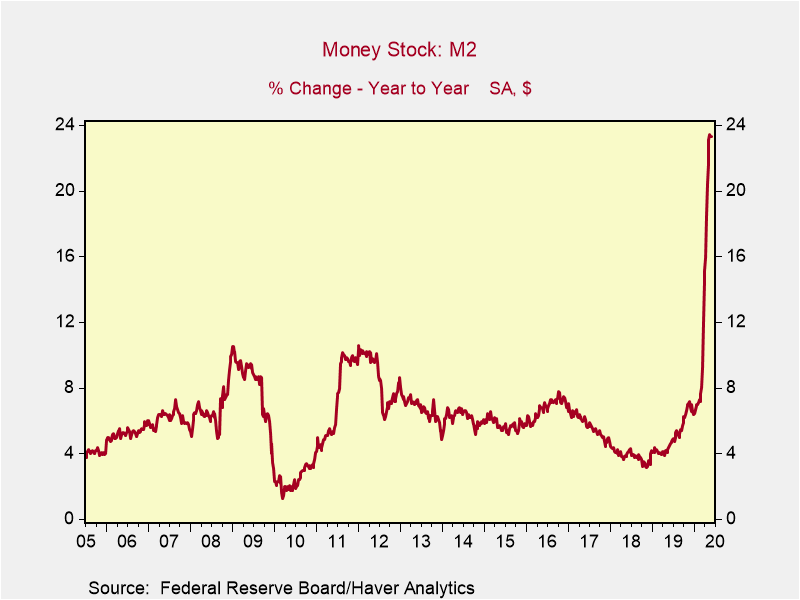

20. an updated chart of the y/y % change in US money supply (credit William Marshall in GIR. your interpretation of this chart may hinge on whether you’re a first or second derivative kind of person:

21. yes, there’s been some significant rotation of late in things like leaders vs laggards. for example, you can see there was some recent retracement in names were hit hard by the health crisis (see white line below, which is a ratio vs S&P). that said, note that the stocks most leveraged to the stay-at-home theme continue to outpace most everything else in the market (blue line):

22. last but not least, through thick and thin, the big S&P bull trend line still holds:

via ZeroHedge News https://ift.tt/2Z1YamD Tyler Durden

NYC Sees 400% Jump In Shootings As Undercover Unit Disbanded Tyler Durden

Mon, 06/22/2020 – 19:50

As the NYPD disbands its undercover investigations unit, taking hundreds of crime-spotting undercover officers off the streets (a decision that will almost certainly lead to fewer low level arrests, but also leaves an opening for more serious crime to make a comeback), it appears one of the most closely followed crime metrics in NYC has skyrocketed compared with the same period last year.

According to stats released by the department, the number of shootings reported in NYC over the past week hit 55, compared with just 12 during the same period last year. That’s a nearly 5-fold rise.

Commissioner Dermot Shea officially disbanded the plainclothes unit a week ago. The results since then have been startling.

Meanwhile, the hundreds of “journalists” who live in NYC have been obsessed with a bogus ‘conspiracy theory’ about the surfeit of fireworks heard around the city is part of a ‘conspiracy’ to stop black and brown people from getting enough sleep, in order to fomet more unrest.

Even Commissioner Shea acknowledges that the rank and file are “demoralized” after weeks of sometimes deadly interactions with protesters and looters and rioters. On Sunday, video of an officer applying a chokehold while detaining a suspect in Rockaway Beach, Queens led to his suspension without pay, further rankling the rank and file after Shea limply defended the decision to foster more “accountability in policing.”

The city council last week passed a new law requiring cops who use chokeholds to be charged with a misdemeanor, regardless of whether the subject is injured.

Venting to the New York Post, one law enforcement source claimed that this is what the politicians want, they want an increase in crime so they can further demonize police, while letting “non violent” offenders out of Rikers by the hundreds. “This is what the politicians wanted – no bail, nobody in Rikers, cops not arresting anyone,” one angry law enforcement source said Friday. “All those things equal people walking around on the street with guns, shooting each other.”

I’d like to address some aspects of the Greater Depression in this essay.

I’m here to tell you that the inevitable became reality in 2008. We’ve had an interlude over the last few years financed by trillions of new currency units.

However, the economic clock on the wall is reading the same time as it was in 2007, and the Black Horsemen of your worst financial nightmares are about to again crash through the doors and end the party. And this time, they won’t be riding children’s ponies, but armored Percherons.

To refresh your memory, let me recount what a depression is.

The best general definition is: A period of time when most people’s standard of living drops significantly. By that definition, the Greater Depression started in 2008, although historians may someday say it began in 1971, when real wages started falling.

It’s also a period of time when distortions and misallocations of capital are liquidated, and when the business cycle, which is caused exclusively by currency debasement (also known as inflation), climaxes. That results in high unemployment, business failures, uncompleted construction, bond defaults, stock market crashes, and the like.

Fortunately, for those who benefit from the status quo, and members of something called the Deep State, the trillions of new currency units delayed the liquidation. But they also ensured it will now happen on a much grander scale.

The Deep State is an extremely powerful network that controls nearly everything around you. You won’t read about it in the news because it controls the news. Politicians won’t talk about it publicly. That would be like a mobster discussing murder and robbery on the six o’clock news. You could say the Deep State is hidden, but it’s only hidden in plain sight.

The Deep State is the source of every negative thing that’s happening right now. To survive the coming rough times, it’s essential for you to know what it’s all about.

The State

Now, what causes economic problems? With the exception of natural events like fires, floods, and earthquakes, they’re all caused directly and indirectly by the State, through its wars, taxes, regulations, and inflation.

Yes, yes, I know this is an oversimplification, that human nature is really at fault, and the institution of the State is only a mass dramatization of the psychological aberrations and demons that lie within us all.

But we don’t have time to go all the way down the rabbit hole, so let’s just talk about the proximate rather than the ultimate causes of the Greater Depression. And here, I want to talk about the nature of the State, in general, and then something called the Deep State, in particular.

A key takeaway (and I emphasize that because I expect it to otherwise bounce off the programmed psyches of most people) is that the very idea of the State itself is poisonous, evil, and intrinsically destructive. But, like so many bad ideas, people have come to assume it’s part of the cosmic firmament, when it’s really just a monstrous scam.

It’s a fraud, like your belief that you have a right to free speech because of the First Amendment, or a right to be armed because of the Second Amendment. No, you don’t. The U.S. Constitution is just an arbitrary piece of paper… entirely apart from the fact the whole thing is now just a dead letter. You have a right to free speech and to be armed because they’re necessary parts of being a free person, not because of what a political document says.

Even though the essence of the State is coercion, people have been taught to love and respect it. Most people think of the State in the quaint light of a grade school civics book. They think it has something to do with “We the People” electing a Jimmy Stewart character to represent them.

That ideal has always been a pernicious fiction, because it idealizes, sanitizes, and legitimizes an intrinsically evil and destructive institution, which is based on force. As Mao once said, political power comes out of the barrel of a gun. But things have gone far beyond that. We’re now in the Deep State.

The Deep State

The concept of the Deep State originated in Turkey, which is appropriate, since it’s the heir to the totally corrupt Byzantine and Ottoman empires. And in the best Byzantine manner, the Deep State has insinuated itself throughout the fabric of what once was America. Its tendrils reach from Washington down to every part of civil society. Like a metastasized cancer, it can no longer be easily eradicated.

I used to joke that there was nothing wrong with Washington that 10 megatons on the capital couldn’t cure. But I don’t say that anymore. Partially because it’s too dangerous, but mainly because it’s now untrue. What’s now needed is 10 megatons on the capital, and four more bursts in a quadrant 10 miles out.

In many ways, Washington models itself after another city with a Deep State, ancient Rome. Here’s how a Victorian freethinker, Winwood Reade, accurately described it:

“Rome lived upon its principal till ruin stared it in the face. Industry is the only true source of wealth, and there was no industry in Rome. By day the Ostia road was crowded with carts and muleteers, carrying to the great city the silks and spices of the East, the marble of Asia Minor, the timber of the Atlas, the grain of Africa and Egypt; and the carts brought out nothing but loads of dung. That was their return cargo.”

The Deep State controls the political and economic essence of the U.S. This is much more than observing that there’s no real difference between the left and right wings of the Demopublican Party.

It’s well known by anyone with any sense (that is, by everybody except the average voter) that although the Republicans say they believe in economic freedom (but don’t), they definitely don’t believe in social freedom. And the Democrats say they believe in social freedom (but don’t), but they definitely don’t believe in economic freedom.

Who Is Part of the Deep State?

The American Deep State is a real, but informal, structure that has arisen to not just profit from, but control, the State.

The Deep State has a life of its own, like the government itself. It’s composed of top-echelon employees of a dozen Praetorian agencies, like the FBI, CIA, and NSA… top generals, admirals, and other military operatives… long-term congressmen and senators… and directors of important regulatory agencies.

But the Deep State is much broader than just the government. It includes the heads of major corporations, all of whom are heavily involved in selling to the State and enabling it. That absolutely includes Silicon Valley, although those guys at least have a sense of humor, evidenced by their “Don’t Be Evil” motto.

It also includes all the top people in the Fed, and the heads of all the major banks, brokers, and insurers. Add the presidents and many professors at top universities, which act as Deep State recruiting centers… all the top media figures, of course… and many regulars at things like Bohemian Grove and the Council on Foreign Relations. They epitomize the status quo, held together by power, money, and propaganda.

Altogether, I’ll guess these people number 1,000 or so. You might analogize the structure of the Deep State with a huge pack of dogs. The people I’ve just described are the top dogs.

But there are hundreds of thousands more who aren’t at the nexus, but who directly depend on them, have considerable clout, and support the Deep State because it supports them.

This includes many of the wealthy, especially those who got that way thanks to their State connections… the more than 1.5 million people who have top secret clearances (that’s a shocking, but accurate, number)… plus top players in organized crime, especially the illegal drug business, little of which would exist without the State. Plus, mid-level types in the police and military, corporations, and non-governmental organizations.

These are what you might call the running dogs.

Beyond that are the scores and scores of millions who depend on things remaining the way they are. Like the 50%-plus of Americans who are net recipients of benefits from the State… the 60 million on Social Security… the 66 million on Medicaid… the 50 million on food stamps… the many millions on hundreds of other programs… the 23 million government employees and most of their families. In fact, let’s include the many millions of average Joes and Janes who are just getting by.

You might call this level of people, the vast majority of the population, whipped dogs. They both love and fear their master, they’ll do as they’re told, and they’ll roll over on their backs and wet themselves if confronted by a top dog or running dog who feels they’re out of line.

These three types of dogs make up the vast majority of the U.S. population. I trust you aren’t among them. I consider myself a Lone Wolf in this context and hope you are, too. Unfortunately, however, dogs are enemies of wolves, and tend to hunt them down.

The Deep State is destructive, but it’s great for the people in it. And, like any living organism, its prime directive is: Survive! It survives by indoctrinating the fiction that it’s both good and necessary. However, it’s a parasite that promotes the ridiculous notion that everyone can live at the expense of society.

Is it a conspiracy, headed by a man stroking a white cat? I think not. I find it’s hard enough to get a bunch of friends to agree on what movie to see, much less a bunch of power-hungry miscreants bent on running everyone’s lives. But, on the other hand, the top dogs all know each other, went to the same schools, belong to the same clubs, socialize, and, most important, have common interests, values, and philosophies.

The American Deep State rotates around the Washington Beltway. It imports America’s wealth as tax revenue. A lot of that wealth is consumed there by useless mouths. And then, it exports things that reinforce the Deep State, including wars, fiat currency, and destructive policies. This is unsustainable simply because nothing of value comes out of the city.

via ZeroHedge News https://ift.tt/3dwfplC Tyler Durden

Specifically, Goldman believes inflation will need to move above the Fed’s 2% target and this move to be met with a muted policy response.

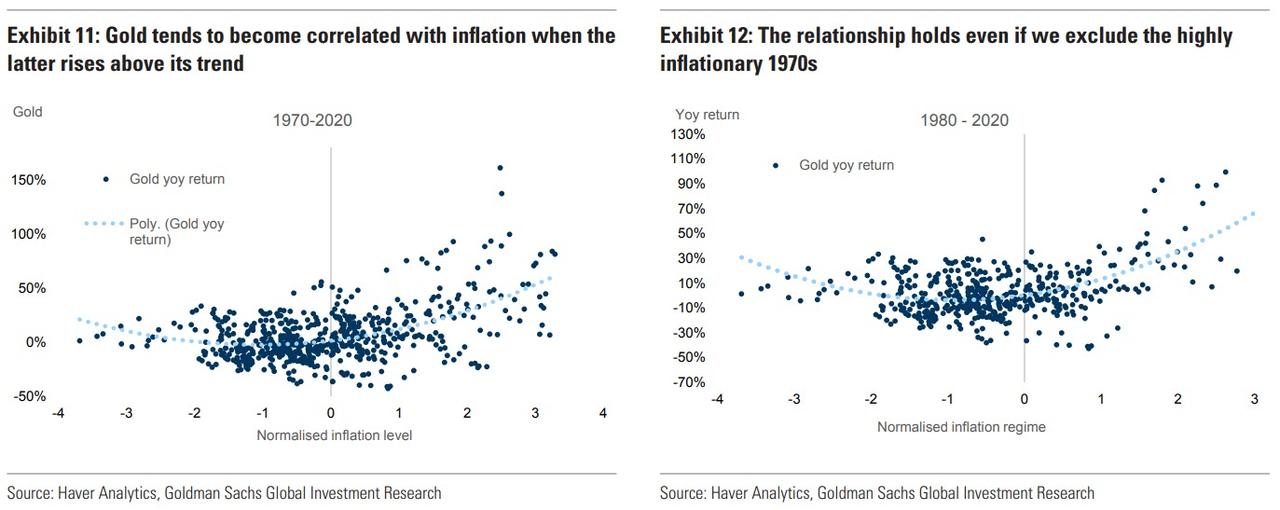

Historically, gold’s relationship with inflation is non-linear. Gold does not display a strong correlation with inflation while the latter is moderate but becomes strongly correlated when inflation gets above a certain threshold. Gold also tends to go up moderately in deflationary environments.

In fact, we find that what matters most is the deviation of inflation from its trend, rather than its absolute level (see Exhibit 11 and Exhibit 12).

This is understandable – investor expectations of future inflation changes through time. For example, while a 5% inflation rate in the early 1980’s may have been perceived as relatively low, today it would represent a large upward surprise to the market. The relationship between gold and inflation gets stronger when we adjust inflation for its trend. The relationship holds in the post-Volcker period that excludes the extremely high inflation of the 1970’s.

Using this relationship between gold and inflation deviations from trend we find that to get to $3000/toz we would need to have inflation exceed its average over the past 10 years of 1.75% by about 3 standard deviations (approx 4.5%). Alternatively, gold could reach $3000/toz if the move in inflation is smaller but more persistent. For example, an inflation rate of 3.5% maintained for several years would achieve a similar target. Persistently high inflation rates would lead to concerns over the commitment of central banks to meet their inflation targets, amplifying fears of inflation further.

But, an increase in interest rates in excess of the level of inflation, akin to Volcker’s 1980 policy, would remove any tail risks of inflation, reducing gold’s appeal.

Additionally, Goldman finds that gold is a useful addition to any portfolio in periods of high inflation.

Specifically, we looked at gold and equity’s performance over previous inflationary environments. We divide the inflationary regimes by looking at deviation of YoY inflation rates vs. its 10 year rolling average.

We find that gold tends to outperform equities in high inflation regimes as well as in deflationary environments, whereas equities do better when inflation is moderate.

There is another shoe that needs to drop – a breakdown in the US dollar. Several people in the mainstream have warned about this in recent weeks. Yale economist Stephen Roach’s warned that “the era of the US dollar’s ‘exorbitant privilege’ as the world’s primary reserve currency is coming to an end.” Meanwhile, Guggenheim Investments Chief Investment Officer Scott Minerd said that while “there are no signs the world is questioning the value of the US dollar” right now, it’s clear that the greenback is “slowly losing market share as the world’s reserve currency.”

via ZeroHedge News https://ift.tt/2V8awIW Tyler Durden

The single biggest threat against President Donald Trump’s reelection in November isn’t unhinged liberals out for blood, a hostile media or even a politicized U.S. Supreme Court; it’s Dr. Anthony Fauci, the top infectious disease adviser on the White House Coronavirus Task Force.

If he’s not reined in, then he may succeed in making Trump a one-term president.

Here’s why.

One of the most important things an incumbent needs to secure reelection is a strong economy, but due to the radical lockdown and months-long national quarantine Fauci championed in March to mitigate the pandemic, the U.S. economy was dealt a devastating blow, resulting in 46 million Americans losing their jobs. So, now, instead of the president galloping into the November election leading one of the hottest economies on record, he’s trudging to the ballot box hoping the economy will recover quickly enough.

Strike 1.

In hindsight, advisers like Fauci, the director of the National Institute of Allergy and Infectious Diseases, should’ve recommended a partial lockdown and a quarantine only for our nation’s most vulnerable citizens — the elderly and those with underlying medical conditions — not the entire country. But that moderate and reasonable approach didn’t happen. Instead, the president adopted the questionable advice of Fauci and others who favored a national lockdown — which many voters consider Draconian — kneecapping the economy and our collective rights and now jeopardizing the president’s reelection chances.

Strike 2.

Fauci has also sowed skepticism about kids going back to school in the fall, radically influencing, if not forever altering, our entire U.S. education system. Since March, when schools were closed nationwide, approximately 57 million American children were forced into isolation at home, cut off from friends, socialization, sports and normal activities. Scores have been denied a quality education and have suffered detrimental effects to their mental and physical health — unnecessarily — as it’s well-known that children are a low-risk group for getting the coronavirus and dying from it. For reference, in Massachusetts, a hotspot for coronavirus, not a single child ages 0-19 has died from coronavirus according to the mass.gov website.

But that’s not all Fauci is radically altering in the name of public health. Turns out, he wants to cancel football, too. During a recent interview, Fauci told CNN’s Chief Medical Correspondent Dr. Sanjay Gupta:

“Unless players are essentially in a bubble — insulated from the community and they are tested nearly every day — it would be very hard to see how football is able to be played this fall. If there is a second wave, which is certainly a possibility and which would be complicated by the predictable flu season, football may not happen this year.”

Strike 3.

Americans are not going to accept a beloved American pastime like football — or other pro sports — being canceled indefinitely because Fauci, an unelected bureaucrat with an opinion, says so.

Bottom line:If the president doesn’t bench Fauci soon and reject his endless calls for extreme mitigation measures, he’s likely to join 46 million on the unemployment line come November.

via ZeroHedge News https://ift.tt/2AZjbXj Tyler Durden

There is room for debate over when it is appropriate to rename institutions or remove or relocate statutes and memorials to disgraced public figures. For myself, I think the burden on those calling for such changes should be rather high, and I generally prefer supplementing such memorials or displays, such as by adding statues or memorials to other, more deserving figures, over removal. History is important, including (perhaps especially) when it concerns our shortcomings as a nation.

The one context in which I think such historical effacement is justified concerns memorials to leaders of the Confederacy, particularly in this . While I think it is perfectly appropriate, in deed important, to have such things in museums and appropriate venues, I think it is appropriate to remove the names and visages of Confederate leaders from places of honor. There is no good reason to have such statutes in public squares or the names of Confederate generals on U.S. military bases.

My reasons are quite simple: The Confederacy was a traitorous uprising expressly inspire by a desire to maintain slavery as a racial institution.

While the true causes of secession have not always been adequately covered in history books (some of which repeat the fable that southern states seceded over tariffs or suggest it was a “war of Northern aggression), the historical record is abundantly clear. The South seceded over slavery, preemptively seeking to leave the Union after their preferred candidate lost the Presidential election.

The relevant original documents speak for themselves. As southern states seceded, they identified the need to protect slavery as their cause, expressly repudiated the principles of the Declaration of Independence, and were more-than-willing to trample the rights of free citizens in the service of protecting slavery (as well as to prohibit any of the confederate states from seceding).

In his infamous “Cornerstone Speech”, Confederate vice president Alexander Stephens declared:

The constitution, it is true, secured every essential guarantee to the institution while it should last, and hence no argument can be justly urged against the constitutional guarantees thus secured, because of the common sentiment of the day. Those ideas, however, were fundamentally wrong. They rested upon the assumption of the equality of races. This was an error. It was a sandy foundation, and the government built upon it fell when the “storm came and the wind blew.”

Our new government is founded upon exactly the opposite idea; its foundations are laid, its corner-stone rests, upon the great truth that the negro is not equal to the white man; that slavery subordination to the superior race is his natural and normal condition. This, our new government, is the first, in the history of the world, based upon this great physical, philosophical, and moral truth.

The Confederate states seceded from the Union, and started a war, to protect the institution of slavery. (And, yes, the Confederacy started the war—announcing secession before Abraham Lincoln had been inaugurated, and firing the first shots Fort Sumter.)

This history is something to remember, but neither the secessionist cause, nor its leaders, are something to commemorate.

from Latest – Reason.com https://ift.tt/3fLJZJk

via IFTTT