US Lawmakers Propose Total Ban On STEM Visas For Chinese Students Tyler Durden

Thu, 05/28/2020 – 10:45

As the White House prepares to eject Chinese graduate students with ties to the PLA, three US lawmakers are taking things a step further – proposing a bill which would ban mainland Chinese students from studying STEM subjects in the United States.

Chinese and other international students wave flags at 2018 Columbia University commencement ceremony.

Two senators and one House member said on Wednesday that the Secure Campus Act would bar Chinese nationals from obtaining visas for graduate or postgraduate studies in science, technology, engineering and mathematics. Students from Taiwan and Hong Kong would be exempt, according to SCMP.

“The Chinese Communist Party has long used American universities to conduct espionage on the United States,” said Sen. Tom Cotton (R-AK), one of the bill’s sponsors, adding “What’s worse is that their efforts exploit gaps in current law. It’s time for that to end.”

“The Secure Campus Act will protect our national security and maintain the integrity of the American research enterprise.”

The proposed legislation comes as diplomatic relations have fractured between the world’s two largest economies. The fissures started to show during a trade war that has been rumbling on for almost two years and have only widened amid accusations about the handling of the Covid-19 disease outbreak , and the treatment of ethnic minority groups in China.

Hong Kong is the latest flashpoint after Beijing drew up a national security law that Washington says tramples on the city’s mini-constitution. The US threatened retaliation over the move. -SCMP

The bill will also tackle China’s efforts to recruit talent overseas through their Thousand Talents Program, an operation launched in 2008 by the CCP which seeks out international experts in scientific research, innovation and entrepreneurship. It proposes that participants in China’s recruitment of foreigners be made to register under the Foreign Agents Registration Act (FARA), and would prohibit Chinese nationals and those participating in China-sponsored programs from receiving federal grants or working on federally funded R&D in STEM fields.

Any university, research institute or laboratory receiving federal funding would be required to attest that they are not knowingly employing participants in China’s recruitment programs – a list of which the US Secretary of State would publish.

US law enforcement and educational agencies have raised red flags about undisclosed ties between federally funded researchers and foreign governments. A crackdown has included indictments and dismissals.

In January, Charles Lieber, 60, chairman of the chemistry and chemical biology department at Harvard University, was arrested and charged for lying about his involvement in the Thousand Talents Programme. -SCMP

Meanwhile, earlier this month a professor at the University of Arkansas who received millions of dollars in research grants, including $500,000 from NASA, was arrested and charged with one count of wire fraud.

According to the FBI, Ang failed to disclose that he was getting paid by a Chinese university and Chinese companies in violation of university policy. He is accused of making false statements while failing to disclose his extensive ties to China as a member of the “Thousand Talents Scholars” program.

63-year-old Simon Saw-Teong Ang is the director of the school’s High Density Electronics Center, which received funding from the National Science Foundation (NSF), Department of Energy (DOE), Department of Defense (DOD) and NASA. Since 2013, Ang has been the primary investigator or co-investigator on US government-funded grants totaling over $5 million, according to the Washington Examiner.

In November, the Senate Permanent Subcommittee on Investigations chaired by Sen. Rob Portman (R-OH) released a 109-page bipartisan report which concluded that foreign nations “seek to exploit America’s openness to advance their own national interests,” the most ambitious of which “has been China,” according to the Examiner. According to the report, Chinese academics involved in their so-called ‘Thousand Talents’ program have been exploiting access to US research labs.

Backlash

According to SCMP, members of the US scientific community see the US as unfairly targeting Chinese colleagues, and that the campaigns will discourage talented individuals from pursuing studies at US universities.

“While we must be vigilant to safeguard research, we must also ensure that the US remains a desirable and welcoming destination for researchers from around the world,” wrote members of 60 groups – including the American Association for the Advancement of Science and the Federation of American Scientists, in a 2019 letter to science policy officials.

The US lawmakers’ proposal follows China’s March decision to revoke the press credentials for US journalists from three major US newspapers – declaring five US media outlets to be foreign government proxies. In February, the Trump administration labeled five Chinese state media groups as “foreign missions” (via SCMP).

via ZeroHedge News https://ift.tt/36F3P5S Tyler Durden

John compares these cases to Noel Canning: these cases lack any controlling precedent, and can be decided without regard to stare decisis.

The cases’ significance for originalism stems from the absence of controlling Court precedent on the question of a presidential elector’s discretion. Most Supreme Court cases have prior cases that arguably dispose of the issue, but these do not. The only case about the obligations imposed on electors, Ray v. Blair, concerned moral pledges that parties required of the electors, not the very different question of whether the electors’ choice can be disciplined by law. In their lack of controlling precedents, these new cases resemble NLRB v. Noel Canning, in which the Court had to address, for the first time in its jurisprudence, certain important questions about the scope of the Recess Appointments Clause.

I analogize Noel Canning to originalism in “precedential open fields, as opposed to deep in the thicket.” There are no institutional constraints to follow some wayward precedent from the Warren Court. Here, the faint-hearted originalists can’t hide behind stare decisis.

Instead, McGinnis warns, they’ll hide behind precedent-by-another name: call it the “chaos” theory of constitutional law:

Unfortunately, if the oral argument for the cases about presidential electors is any indication, the Court may do grave damage to originalism by suggesting that the bad consequences of a constitutional provision or practice subsequent to the time of its enactment can override its original meaning….

And in oral argument, some justices who might be thought to harbor originalist sympathies openly appealed to consequentialist arguments. For instance, Justice Kavanaugh suggested that when it is a “close call” on meaning, the Court might consider avoiding the “chaos” that he implied might follow from a decision allowing electoral discretion.

John explains that the Justices’ concerns for “slipper slopes” will always trump original meaning;

Furthermore, who is to decide how “close” the case must be to permit the consideration of consequences? That is a slippery slope that will allow the original meaning to become merely one consideration among many. For instance, assume that the question of whether the Second Amendment protects an individual right to bear arms is close, even if the better view tips in its favor. Kavanaugh’s approach would authorize judges to decide the case based on their assessment of the consequences of various gun control measures.

At bottom, a ruling against the electors could “bury originalism.”

As Mike Rappaport and I have argued, it is constitutional for judges to follow Court precedent rather than original meaning. It is even warranted in certain, limited circumstances. Originalists need to frame better-reticulated rules about what those circumstances are. But inviting judges to consider the consequences of their decisions or the recent practice of other governmental actors as guides to interpretation threatens to bury originalism.

Seth Barrett Tillman and I had similar concerns after oral arguments. We wrote twoposts about how to properly characterize electors as a matter of original public meaning: we think they hold “public trusts under the United States.” But we acknowledged that some of the Justices worried about that “chaos” that could result in a judgment for the electors. As a result, we offered a middle-ground approach to help reconcile the original public meaning of the Constitution with pragmatic concerns. If the Court is truly motivated by a desire to avoid “chaos,” and cannot rule that electors have discretion, our approach helps to avoid originalism’s burial.

from Latest – Reason.com https://ift.tt/3er2m5B

via IFTTT

Disrespected by Twitter, President Donald Trump is throwing a tantrum in the form of an executive order that declares Twitter and Facebook are the “functional equivalent of a traditional public forum” and should “not infringe on protected speech.” The president seems to have bypassed the typical interagency review process in issuing his new rule. This means the insanely overreaching order (read the leaked draft here) wasn’t written with an eye toward conforming to federal law or constitutional protections of speech and commerce. And make no mistake: the draft order, when it manages to be coherent, is insanely unconstitutional.

But maybe the order having teeth isn’t the point here. Trump’s mandate might not hold up in court, but just by issuing it, Trump sends a not-so-subtle threat to Twitter, Facebook, and other internet companies. Remember, the apparent impetus for this order was Twitter posting a fact check after one of Trump’s tweets.

Should social media companies be getting into the fact-checking game? It’s a bad idea, if you ask me. But it’s a perfectly legal thing for them to do.

The standard Republican talking point on this right now is that affixing fact-checking links to some tweets makes Twitter a “publisher” instead of a “platform” or “forum.” It might make for an interesting semantic distinction, but the legally significant issue is whether Twitter is the speaker or creator of Donald Trump’s tweets. If not, it is not legally liable for them. (The same goes for every other user of Twitter, too.)

If you’re thinking, “But, but, what about when Twitter creates a fact-check link and presents it after a user’s posts?” Courts have routinely ruled that a digital company’s decisions about how to present content (or what content to present at all) do not transform it into the speaker of user content.

But back to Trump’s new order: It’s an Orwellian document, defining federal government regulation of Americans’ speech as “free speech” and private questioning of government authority as “censorship.” In Trump’s formulation, private companies can censor the most powerful person in the country but not the other way around.

This is a bad joke. To put out something like this EO and disingenuously wrap it in the rhetoric of “free speech” is obscene. https://t.co/mH2YArUHAn

Interestingly, after years of downplaying the idea that foreign actors used social media in an attempt to influence the 2016 election, Trump now opportunistically claims that the U.S. government must have power over these platforms to stop the scourge of “disinformation from foreign governments.”

But his biggest complaint is about alleged ideological bias by private companies. Despite previously rallying around the rights of conservative businesses to choose who they do business with and decline to display liberal messages (think florists and bakers), Trump now says that private businesses should have to be totally content-neutral conduits of whatever messages that customers want to broadcast.

To justify his position that the feds can compel companies to display messages from private citizens and government officials alike, Trump turns to a mangled conception of the federal law known as Section 230. This is the 1990s statute stipulating that online platforms and publishers are not to be treated as the speaker of user-generated content (i.e., if I defame someone on Facebook, Facebook isn’t on the hook for defamation).

The order erroneously suggests that Section 230 only applies if online companies moderate content in ways that are explicitly laid out in their terms of service, though nothing in Section 230 comes close to saying this.

It complains that Twitter has been “restricting online content” for reasons other than those laid out as permissible reasons in Section 230(c)(2). This is the part of the statute saying companies don’t become liable for all user content by virtue of moderating content that is “obscene, lewd, lascivious, filthy, excessively violent, harassing or otherwise objectionable.”

But “otherwise objectionable” is a completely discretionary standard and can encompass just about anything.

The legal folks seem to think that this whole thing is both a) legally laughable and nonetheless b) a way of making Twitter and Facebook's life very difficult.

The order relies heavily on conservatives’ victimhood conspiracy du jour: that social media companies are colluding to suppress conservative voices. It’s an objectively untrue viewpoint, as countless booted and suspended liberal, libertarian, and apolitical accounts can tell you. But even if it were true that Twitter or Facebook only takes action against conservatives—or if we take the more believable assertion that current content moderation policies tend to hit some political viewpoints harder than others—it would still not fall outside the bounds of Section 230(c)(2) moderation, which requires only that the moderator find some speech to be “objectionable.”

Somehow, out of Trump’s several paragraphs of paraphrasing Section 230 with random erroneous asides, federal officials are supposed to intuit a new paradigm and “apply section 230(c) according to the interpretation set out in this section.”

The document also instructs the Federal Communications Commission (FCC) to define concepts that Trump just made up for this order and then propose ways to tell if companies are running afoul of them. Trump wants the FCC to determine the conditions under which content moderation will be considered “deceptive, pretextual, or inconsistent with a provider’s terms of service”—but then what? Nothing in Section 230 says a company can’t moderate in ways “inconsistent with” their terms of service. And it’s laughable to think that bureaucrats will be able to tell whether thousands of individual content moderators are making decisions based on the right reasons or on secretly “deceptive” grounds.

The FCC is also tasked with defining this bit of Trumpian gobbledygook: the conditions under which content moderation will be considered “the result of inadequate notice, the product of unreasoned explanation, or having been undertaking without a meaningful opportunity to be heard.”

If you've ever wondered why Internet companies don't follow their own rules, this is it. The one time Twitter attempts to elevate social discourse by experimenting with moderation that goes outside the binary leave up/takedown scheme, it's met with an #executiveorder.

One of the most concrete parts of the executive order, and perhaps the only feasible part, is a bit saying that all federal agencies must review and submit (within 30 days) a report on the amount of money they spend on social media advertising. It comes in a section titled “Prohibition on Spending Federal Taxpayer Dollars on Advertising with Online Platforms That Violate Free Speech Principles.”

Insofar as this order helps keep stupid government propaganda campaigns off social media and reduces what the public pays for those campaigns, great! Alas, Trump doesn’t really have any clue what the criteria for preventing these ads might be and didn’t bother finding out whether he has the statutory authority to require this before writing the order. It actually asks the heads of each executive department and agency to independently review “the viewpoint-based speech restrictions imposed by each online platform” and then tell Trump “the statutory authorities available to restrict advertising dollars to online platforms.”

The second-to-last part of the order is another bit that sounds vaguely weighty but is actually just a bunch of big words sort of strung together in the way that might fool random Trump fans into thinking he’s taking action. He declares that Facebook and Twitter are “the functional equivalent of a traditional public forum”—which would essentially mean that they are the “functional equivalent” of government property.

But of course, Trump has no authority to simply seize these private companies via executive order. And even if he could just declare that Twitter and Facebook were the digital equivalent of the National Mall, this would mean that government actors would face serious hurdles to restricting speech on them. Bottom line: Unless government officials are going to completely take over Twitter and Facebook content moderation, invoking public forums here is just bluster.

Ultimately, the order’s lack of standard review very much shows.

It seems the White House apparently didn’t consult with the Federal Communications Commission about the order, which would mean it did not go through the standard interagency review process.

“Worth remembering that with prior WH attempts to draft an executive order targeting social media companies, the FCC and FTC (which are led by Republican chairmen) privately pushed back on being deputized to police political speech on social platforms,” noted CNN tech reporter Brian Fung on Twitter.

“Much of the order could quickly get bogged down in a thicket of legal and constitutional questions,” Fung added. “Just for example, the FTC reports to Congress, not the WH.”

FREE MINDS

Some positive signs on secret surveillance:

NEWS: The House has postponed the FISA vote expected tonight, Democratic aides tell @nataliewsj, after the bill faced uncertain passage due to a veto threat from President Trump and opposition from some progressive Democrats.

One person was killed and several buildings were set on fire in Minneapolis last night following protests over the police killing of George Floyd.

A man was shot at 9:25 p.m. at Bloomington and Lake. Pronounced dead at hospital, one in custody. Police spokesman would not confirm whether it was a looter. "That is one of the theories we are looking into…" but too early to say, police spokesman said. https://t.co/sttgejZCO6

This doesn’t seem like it will end well for the state:

A Maryland county has banned "consumption of food or beverage of any kind before, during, or after religious services, including food or beverage that would typically be consumed as part of a religious service.” https://t.co/WFOKw9Ib7b via @cnalive

“The average millennial has experienced slower economic growth since entering the workforce than any other generation in U.S. history,” writes Andrew Van Dam at The Washington Post.

Disrespected by Twitter, President Donald Trump is throwing a tantrum in the form of an executive order that declares Twitter and Facebook are the “functional equivalent of a traditional public forum” and should “not infringe on protected speech.” The president seems to have bypassed the typical interagency review process in issuing his new rule. This means the insanely overreaching order (read the leaked draft here) wasn’t written with an eye toward conforming to federal law or constitutional protections of speech and commerce. And make no mistake: the draft order, when it manages to be coherent, is insanely unconstitutional.

But maybe the order having teeth isn’t the point here. Trump’s mandate might not hold up in court, but just by issuing it, Trump sends a not-so-subtle threat to Twitter, Facebook, and other internet companies. Remember, the apparent impetus for this order was Twitter posting a fact check after one of Trump’s tweets.

Should social media companies be getting into the fact-checking game? It’s a bad idea, if you ask me. But it’s a perfectly legal thing for them to do.

The standard Republican talking point on this right now is that affixing fact-checking links to some tweets makes Twitter a “publisher” instead of a “platform” or “forum.” It might make for an interesting semantic distinction, but the legally significant issue is whether Twitter is the speaker or creator of Donald Trump’s tweets. If not, it is not legally liable for them. (The same goes for every other user of Twitter, too.)

If you’re thinking, “But, but, what about when Twitter creates a fact-check link and presents it after a user’s posts?” Courts have routinely ruled that a digital company’s decisions about how to present content (or what content to present at all) do not transform it into the speaker of user content.

But back to Trump’s new order: It’s an Orwellian document, defining federal government regulation of Americans’ speech as “free speech” and private questioning of government authority as “censorship.” In Trump’s formulation, private companies can censor the most powerful person in the country but not the other way around.

This is a bad joke. To put out something like this EO and disingenuously wrap it in the rhetoric of “free speech” is obscene. https://t.co/mH2YArUHAn

Interestingly, after years of downplaying the idea that foreign actors used social media in an attempt to influence the 2016 election, Trump now opportunistically claims that the U.S. government must have power over these platforms to stop the scourge of “disinformation from foreign governments.”

But his biggest complaint is about alleged ideological bias by private companies. Despite previously rallying around the rights of conservative businesses to choose who they do business with and decline to display liberal messages (think florists and bakers), Trump now says that private businesses should have to be totally content-neutral conduits of whatever messages that customers want to broadcast.

To justify his position that the feds can compel companies to display messages from private citizens and government officials alike, Trump turns to a mangled conception of the federal law known as Section 230. This is the 1990s statute stipulating that online platforms and publishers are not to be treated as the speaker of user-generated content (i.e., if I defame someone on Facebook, Facebook isn’t on the hook for defamation).

The order erroneously suggests that Section 230 only applies if online companies moderate content in ways that are explicitly laid out in their terms of service, though nothing in Section 230 comes close to saying this.

It complains that Twitter has been “restricting online content” for reasons other than those laid out as permissible reasons in Section 230(c)(2). This is the part of the statute saying companies don’t become liable for all user content by virtue of moderating content that is “obscene, lewd, lascivious, filthy, excessively violent, harassing or otherwise objectionable.”

But “otherwise objectionable” is a completely discretionary standard and can encompass just about anything.

The legal folks seem to think that this whole thing is both a) legally laughable and nonetheless b) a way of making Twitter and Facebook's life very difficult.

The order relies heavily on conservatives’ victimhood conspiracy du jour: that social media companies are colluding to suppress conservative voices. It’s an objectively untrue viewpoint, as countless booted and suspended liberal, libertarian, and apolitical accounts can tell you. But even if it were true that Twitter or Facebook only takes action against conservatives—or if we take the more believable assertion that current content moderation policies tend to hit some political viewpoints harder than others—it would still not fall outside the bounds of Section 230(c)(2) moderation, which requires only that the moderator find some speech to be “objectionable.”

Somehow, out of Trump’s several paragraphs of paraphrasing Section 230 with random erroneous asides, federal officials are supposed to intuit a new paradigm and “apply section 230(c) according to the interpretation set out in this section.”

The document also instructs the Federal Communications Commission (FCC) to define concepts that Trump just made up for this order and then propose ways to tell if companies are running afoul of them. Trump wants the FCC to determine the conditions under which content moderation will be considered “deceptive, pretextual, or inconsistent with a provider’s terms of service”—but then what? Nothing says a company can’t moderate in ways “inconsistent with” their terms of service. And it’s laughable to think that bureaucrats will be able to tell whether thousands of individual content moderators are making decisions based on the right reasons or on secretly “deceptive” grounds.

The FCC is also tasked with defining this bit of Trumpian gobbledygook: the conditions under which content moderation will be considered “the result of inadequate notice, the product of unreasoned explanation, or having been undertaking without a meaningful opportunity to be heard.”

If you've ever wondered why Internet companies don't follow their own rules, this is it. The one time Twitter attempts to elevate social discourse by experimenting with moderation that goes outside the binary leave up/takedown scheme, it's met with an #executiveorder.

One of the most concrete parts of the executive order, and perhaps the only feasible part, is a bit saying that all federal agencies must review and submit (within 30 days) a report on the amount of money they spend on social media advertising. It comes in a section titled “Prohibition on Spending Federal Taxpayer Dollars on Advertising with Online Platforms That Violate Free Speech Principles.”

Insofar as this order helps keep stupid government propaganda campaigns off social media and reduces what the public pays for those campaigns, great! Alas, Trump doesn’t really have any clue what the criteria for preventing these ads might be and didn’t bother finding out whether he has the statutory authority to require this before writing the order. It actually asks the heads of each executive department and agency to independently review “the viewpoint-based speech restrictions imposed by each online platform” and then tell Trump “the statutory authorities available to restrict advertising dollars to online platforms.”

The second-to-last part of the order is another bit that sounds vaguely weighty but is actually just a bunch of big words sort of strung together in the way that might fool random Trump fans into thinking he’s taking action. He declares that Facebook and Twitter are “the functional equivalent of a traditional public forum”—which would essentially mean that they are the “functional equivalent” of government property.

But of course, Trump has no authority to simply seize these private companies via executive order. And even if he could simply declare that Twitter and Facebook were the digital equivalent of the National Mall, this would mean that government actors would face serious hurdles to restricting speech on them. Bottom line: Unless government officials are going to completely take over Twitter and Facebook content moderation, invoking public forums here is just bluster.

Ultimately, the order’s lack of standard review very much shows.

It seems the White House apparently didn’t consult with the Federal Communications Commission about the order, which would mean it did not go through the standard interagency review process.

“Worth remembering that with prior WH attempts to draft an executive order targeting social media companies, the FCC and FTC (which are led by Republican chairmen) privately pushed back on being deputized to police political speech on social platforms,” noted CNN tech reporter Brian Fung on Twitter.

“Much of the order could quickly get bogged down in a thicket of legal and constitutional questions,” Fung added. “Just for example, the FTC reports to Congress, not the WH.”

FREE MINDS

Some positive signs on secret surveillance:

NEWS: The House has postponed the FISA vote expected tonight, Democratic aides tell @nataliewsj, after the bill faced uncertain passage due to a veto threat from President Trump and opposition from some progressive Democrats.

One person was killed and several buildings were set on fire in Minneapolis last night following protests over the police killing of George Floyd.

A man was shot at 9:25 p.m. at Bloomington and Lake. Pronounced dead at hospital, one in custody. Police spokesman would not confirm whether it was a looter. "That is one of the theories we are looking into…" but too early to say, police spokesman said. https://t.co/sttgejZCO6

This doesn’t seem like it will end well for the state:

A Maryland county has banned "consumption of food or beverage of any kind before, during, or after religious services, including food or beverage that would typically be consumed as part of a religious service.” https://t.co/WFOKw9Ib7b via @cnalive

“The average millennial has experienced slower economic growth since entering the workforce than any other generation in U.S. history,” writes Andrew Van Dam at The Washington Post.

As Congress squabbles over the next multitrillion-dollar phase of coronavirus relief, it’s worth asking the question: Do you feel $9,000 richer since March?

Unless you were an early investor in the vaccine-chasing Moderna Therapeutics, the answer is likely “no.” And yet the estimated $3 trillion price tag on the first four batches of COVID-19 stimulus, divided by 330 million increasingly underemployed U.S. residents, equals $9,000 per capita, which has ended up where government payouts usually go: to entities with better connections than you.

There was the $50 billion to airline companies—$25 billion in loan guarantees, $25 billion in grants—which promptly slashed worker hours while burning fuel on empty flights at the government’s request. There were the concierge-service clients of banking behemoths Citibank, U.S. Bank, and J.P. Morgan Chase, who got to the front of the line for the feds’ $349 billion loan program for small businesses. And don’t forget the Federal Reserve, which is propping up Wall Street by doing what Fed Chair Jerome Powell recently characterized on 60 Minutes as “a multiple of the programs that were done during the last crisis.”

You would think that politicians and other elites would have learned from their never-popular response to the 2008-2009 financial crisis. Back then, the bailout/stimulus combo averaged out to a little less than $7,000 per U.S. resident, not that normies saw much of it. With few exceptions, the money went toward propping up banks, socializing the losses of private capitalists, and backfilling the fiduciary irresponsibility of states.

If the federal government didn’t pass a huge emergency bailout, then-President George W. Bush warned in September 2008, “More banks could fail, including some in your community. The stock market would drop even more, which would reduce the value of your retirement account. The value of your home could plummet. Foreclosures would rise dramatically. And if you own a business or a farm, you would find it harder and more expensive to get credit. More businesses would close their doors, and millions of Americans could lose their jobs.”

Well, all of that happened anyway, as did the most anemic recovery in post-war history. As a direct consequence, so did populist anti-bailout political movements on both the right (Tea Party) and left (Occupy Wall Street). If the response to the 2008 financial crisis helped bring us Donald Trump and the rise of Sen. Bernie Sanders (I–Vt.), what might an even bigger and less effective response to the more injurious coronavirus bring?

“Millions of Americans are seeing that the government spent trillions of dollars and still didn’t get it right,” Rep. Justin Amash (L–Mich.) told me last month, during his brief flirtation with the Libertarian Party presidential nomination. “They didn’t get help to the people who need it most. Instead, most of the assistance went to people who have great connections, who run big corporations. Those people, they got it really fast.”

Why does this happen every time? As economists like to say, incentives matter. Sure, Congress could have just mailed us each a $9,000 check—or maybe $7,000, spending the rest on medical system capacity. But then the two major parties wouldn’t have been able to go back to their favored and most supportive constituencies and brag about their special treatment. Sure, there might be an eventual backlash, but as President Trump once said (before COVID-19) about a future debt crisis, “Yeah, but I won’t be here.”

New York Gov. Andrew Cuomo (D), that inexplicable media darling, complained in a recent press conference that all these helicopters full of money—government spending in the U.S. has doubled over just the past two decades—hasn’t managed to, you know, produce anything. “Every president has talked about the need to rebuild our infrastructure, our roads, our bridges, our airports,” Cuomo said. “Our country doesn’t build airports anymore….We haven’t built a new airport in 25 years.”

Governments, unlike businesses, have guaranteed (if fluctuating) revenue streams, in the form of taxes. The federal government has the added leeway of borrowing, apparently without limits. The more of GDP that gets soaked up and spit out by this process, the more that economic and political activity will be about directing and capturing the flow to line the pockets of bankers, corporate executives, and union bosses.

So what does Congress do for an encore? House Speaker Rep. Nancy Pelosi (D–Calif.) wants to double down on another $3 trillion. No, we’ll need $10 trillion to stave off another great depression, they tell us in The Atlantic.

Maybe by the time they reach eleventy trillion, we might see more than a $1,200 check. But I wouldn’t bet on it.

from Latest – Reason.com https://ift.tt/3gp3zMy

via IFTTT

Trump Offers Condolences To Families Of America’s 100k COVID-19 Victims; Brazil Case Count Passes 400k: Live Updates Tyler Durden

Thu, 05/28/2020 – 10:31

With Johns Hopkins finally confirming that the US death toll had passed the 100k mark…

…President Trump tweeted his condolences to the families of all those who lost loved ones during the pandemic.

We have just reached a very sad milestone with the coronavirus pandemic deaths reaching 100,000. To all of the families & friends of those who have passed, I want to extend my heartfelt sympathy & love for everything that these great people stood for & represent. God be with you!

With the US temporarily preoccupied by looting in Minneapolis and elsewhere – the focus during the early morning hours was on Asia, as Japanese health officials reported a new cluster: A hospital in Koganei city, located on the outskirts of Tokyo, have confirmed 3 infected patients, with 18 more reporting symptoms, including a fever. South Korea recently uncovered a ‘silent’ cluster after testing tens of thousands of people who had traveled to a popular nightlife district of Seoul one evening after a nightclubber tested positive, raising fears of a new ‘superspreader’ cluster.

With testing ramping up once again, officials are reportedly weighing whether to revive more-strict social distancing rules due to a recent increase in confirmed cases.

In the Philippines, President Rodrigo Duterte approved a recommendation to ease the lockdown in the capital Manila beginning on June 1 as he tries to pull his country’s economy back from the brink of what would likely be a bruising recession.

German Chancellor Angela Merkel urged her fellow world leaders to provide more money to multinational NGOs like the UN and WHO in the name of accelerating the global recovery from the virus.

Expanding on that point, UN Secretary-General Antonio Guterres agitated for more comprehensive sovereign debt relief for the poorest nations, insisting that “relief must be extended to all developing, middle-income countries that request forbearance as they lose access to financial markets” amid the coronavirus pandemic.

Later today, PM Johnson will set out the next steps on easing Britain’s lockdown, describing what will be possible from June 1.

As France and Germany abandon the drugs, Indonesia said Thursday it will continue to prescribe two anti-malarial drugs – chloroquine and its derivative, hydroxychloroquine – for coronavirus patients but monitor their use closely.

UK police have said Prime Minister Boris Johnson’s senior adviser Dominic Cummings did breach the coronavirus lockdown but that it was minor and they will take no further action, the Telegraph has reported.

Though Africa has been largely spared the brunt of the global outbreak, Al Jazeera warned that cases of community transmission of the coronavirus are growing, particularly in Ethiopia, and that a new strategy for testing is needed to prevent further spread.

“We are beginning to see sustained community transmission within Ethiopia and many other countries across Africa. That means we need to increase our public health measures like distancing, wearing of masks, washing of hands,” Head of the Africa Centers for Disease Control and Prevention John Nkengasong told journalists.

Brazil recorded more than 1,000 new deaths from the coronavirus over the past day, officials said Wednesday. The 1,086 new casualties bring the total number of deaths to 25,598. With 20,599 new cases, one of the largest single-day increases yet, the number of infected people has reached 411,821.

And finally, a partial reopening of schools in Denmark has not lead to an increase in coronavirus infections among pupils, a doctor of infectious disease epidemiology and prevention at the Danish Serum Institute said Thursday, citing newly released government data.

Denmark was one of the first countries to reopen, as it allowed some younger students – up to the fifth grade – to return to school on April 15 after a month-long break.

“You cannot see any negative effects from the reopening of schools,” the scientist said. In the US, NJ Gov Phil Murphy said earlier this week that he would allow outdoor high school graduation ceremonies to continue.

via ZeroHedge News https://ift.tt/2ZRIzYS Tyler Durden

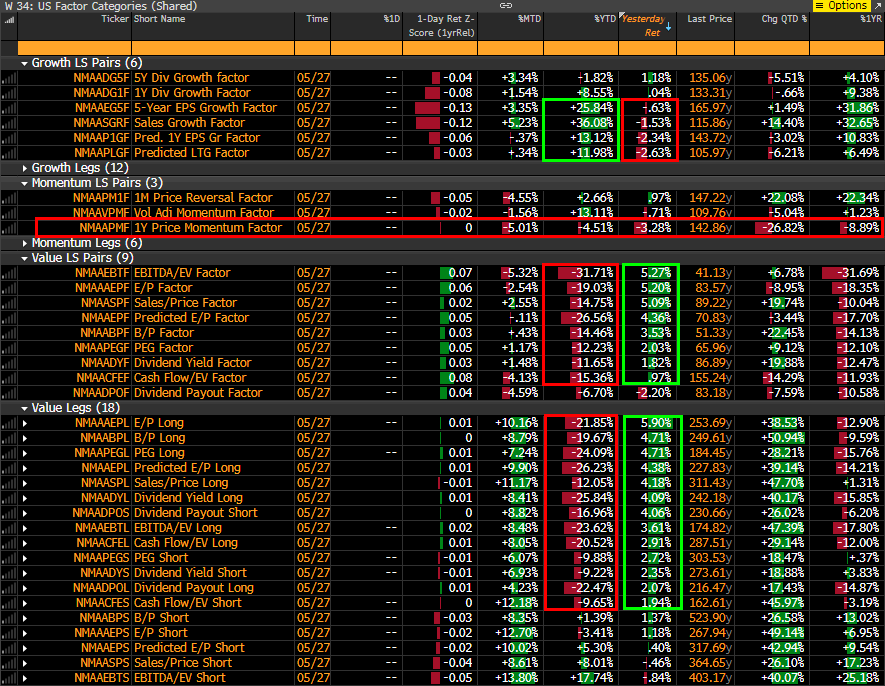

As we have discussed here over the past few days, there has been a tremendous rotation below the market surface in recent days, one on par with the great quant crash in early September 2019, with value stocks soaring – arguably on reopening optimism and expectations for a rebound in inflation on the back of the fiscal firehose we noted yesterday – as outperforming momentum names have been trampled…

… resulting in the latest shock to hedge funds, which were positioned for a continuation of the legacy momentum-over-value theme.

As usual, any time there are such momentous moves in market, Nomura’s quant Charlie McElligott is there to provide his unique perspective, and this morning he did just that, pointing out that “remarkable things” are occurring over the past few sessions within the US Equities space in the context of consensus positioning and what he calls “a tectonic “de-grossing” of short books and overall dynamic hedges, acting to propel both indices and prior “Value” laggards (being economically-sensitive “cyclical beta” Equities) violently higher, while crowded “secular growth” hiding-place longs are acting as an ongoing source-of-funds for this nascent rebalancing.”

As touched upon previously, there are 3 key factors behind this pro-cyclical “risk-on” narrative shift:

fiscal stimulus acceleration (Europe / Germany HUGELY symbolic for a capitulation away from austerity)

accelerating Yield Curve Control talk from Fed (as a curve steepener / reversal of trend catalyst)

The ongoing “rush to reopen” the global economy, while high-frequency mobility -and credit card spending – data seemingly shows fledgling indications of “return to normalcy” type behavior from American consumers.

This 3-peat shock to legacy deflationary positioning, has fallen into what Charlie calls “remarkably short/underweight positioning dynamics” where Asset managers remain net short (1st %ile leveraged fund net “short” position) and CTA’s having been “short” across 12 of 13 of global equities futures in the portfolio over much of the prior 2m.

But as a result of this narrative shift and corresponding realized vol compression, there has been a “spectacular systematic covering bid off lows—with the SPX futures model actually again flipping outright long yesterday, while both RTY and Estoxx legacy short signals were cut in half yesterday as well—and showing an aggregate ~$330B of gross “buying (almost predominately to cover) off the “max short” extreme of early March.”

Not surprisingly then, McElligott notes, the “Everything Duration” consensus trade in Equities—which became de facto Equities consensus “hiding place” positioning—has been hit hard, with US Equities “1Y Price Momentum” -9.8% in 2 days alone (which as the Nomura quant admits has filled “all the positive returns for my “Long Momentum” tactical call for May which mercifully ends imminently”), which has also corresponded with Nomura’s Equities Long-Short model portfolio experiencing its fifth-worst 2d drawdown of the past 1Y window.

So does this mean that after the biggest rout in history, investors can finally chase value shares again?

According to the Nomura quant, it is counter-intuitively the “Recession” which marks the “turn” for Value factor market-neutral per the back-test “as expensive stocks begin to break down (“Value Shorts” i.e. Secular Growth) as the market prices-in a growthier forward-state thereafter thanks to monetary and fiscal stimulus actions which contributes to a bear-steepening”, a point which is in keeping with what Goldman said a month ago when the firm said a handoff from growth to value would lead to a violent market repricing. Conversely, this would also benefit economically sensitive stocks which make up much of the “Value Long” universe, “and this is obviously what the market is debating right now in real time as per the above thematic behavior.”

And speaking of debating, the bears – at least in the systematic community are losing the argument – as a result of what appears to be a wholesale capitulation by shorts. But before we look at the quants, let’s not forget the carbon-based bearish discretionary traders who as we noted over the weekend, were steamrolled by euphoric retail, and have started to chase. As Nomura note, “last week’s trimming of longs in global risk proxy S&P 500 futures from Asset Managers (who sold -$5.4B of Spoos last week) and pressing of shorts from Leveraged Funds (an additional -$2.3B of Spooz sold last weekly period and now -$14.3B over the past month—making the overall net notional position just 1.1%ile in SPX at -$53.5B)” now serve as short fodder which is acting as “kindling for this acceleration higher in U.S. Equities futures.”

Meanwhile, the systematics – which until recently were max short, are puking, and according to Nomura, CTA Trend buying has been a mammoth source of “buy to cover” flows in Global Equities on the realized volatility reset:

Since the max of the “gross notional short” exposure in the CTA model across Global Equities futures (set March 9th), we have since seen an aggregate ~$380B of gross “buy (to cover)” flows (incl implied leverage) across the 13 Global Equities futures in the portfolio thereafter

There is more to come, because whereas S&P CTA are now 100% long, “there is still more fuel for the fire, as 11 of said 13 signals across Global Equities futures remain “short” in the model CTA Trend portfolio” representing a -$5.5B aggregate gross “short”, as both the Russell- and Estoxx- went from recent “-100% Short” to now “-50% Short” signal yesterday, while the S&P 500 futures signal again outright flipped yesterday from the prior “-50% Short” back to “+100% Long” resulting in $17B to BUY in ES alone and a total $49.3B to buy across S&P, Russell and Eurostoxx futs yesterday.

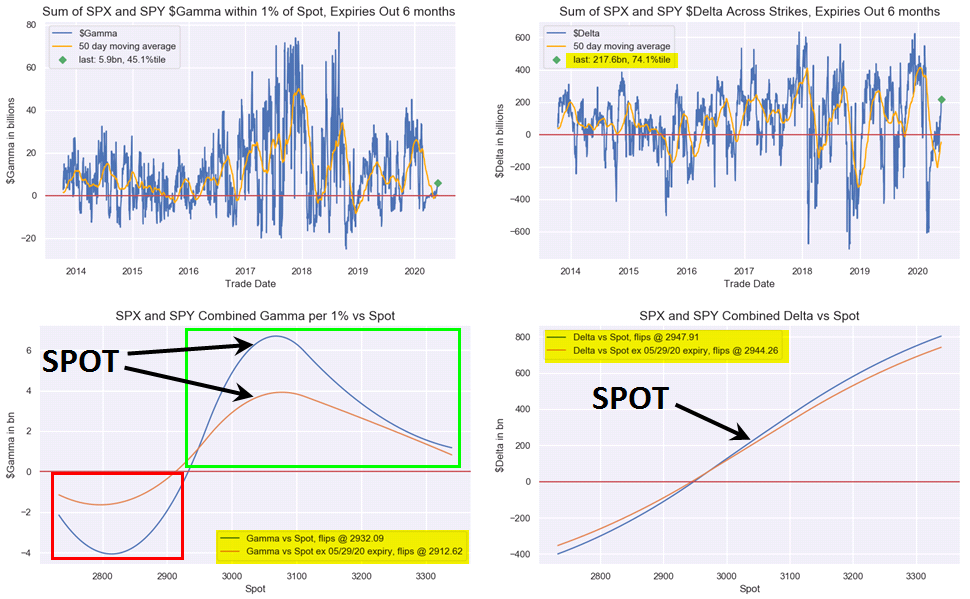

And while overall gamma levels have declined substantially after the recent op-ex, looking at SPX / SPY consolidated options positioning on the move, Nomura sees substantial Gamma building across the 3,000 ($2.63B), 3,050 ($2.39B) and 3,100 ($1.80B) levels…

… and thanks to the rally, seeing the Delta rank has spiked, and is suddenly long at 74th percentile.

via ZeroHedge News https://ift.tt/36As3Oz Tyler Durden

Pending Home Sales Plummet 35% YoY – Biggest Drop Ever As Buyers Forfeit Deposits Tyler Durden

Thu, 05/28/2020 – 10:07

Existing home sales collapsed but new home sales rebounded in April, which leaves pending home sales to break the tie and analysts expected a 17.3% MoM drop. However, pending home sales disappointed notably with a 21.8% MoM collapse, sending YoY sales crashing 34.6% – the most ever…

Source: Bloomberg

“The housing market is temporarily grappling with the coronavirus-induced shutdown,” which reduced listings and purchases, Lawrence Yun, NAR’s chief economist, said in a statement.

So while all sorts of narratives about lower rates were puked out to defend new home sales outlier data, it seems pending home sales did not get the message…

Source: Bloomberg

Every region crashed…

Northeast fell 14.5%; Feb. rose 2.8%

Midwest fell 22%; Feb. rose 4.2%

South fell 19.5%; Feb. fell 0.2%

West fell 26.8%; Feb. rose 5.1%

That is the lowest level of pending home sales since records began in 2001…

March historically begins the annual peak U.S. selling season as warming weather spurs home searches and families with children prepare for moves during the school summer break. That’s been drastically curtailed in 2020 as the virus triggers the biggest economic contraction in decades, closing workplaces, schools and other activities.

Pending home sales are leading indicators of housing activity, based on signed contracts to buy single-family homes, condos and co-ops, typically occurring one or two months before closings.

As MacroGuru (@macroguru9) noted, “The reason this is significant is it takes 4-8 weeks to close the sale once the contract has been signed. So this huge drop would indicate buyers forfeiting the deposit and walking away as they think the loss on the purchase would be higher than the deposit itself!!!”

via ZeroHedge News https://ift.tt/2ZJFj1L Tyler Durden

China Furious After Twitter Retroactively Tags Tweets From Top Officials Tyler Durden

Thu, 05/28/2020 – 09:50

Aside from a string of tweets from Jack Dorsey, Twitter’s PR machine has been strangely quiet during the dust-up over the extremely controversial decision to tag several tweets from President Trump as “misinformation”.

And now we know why. Among the reasons Facebook’s Mark Zuckerberg cited for why social media companies shouldn’t strive to be “arbiters of truth” is the Sisyphean task of filtering, screening and analyzing an endless stream of information. Given the massive user bases of these companies, consistency would be nearly impossible, opening the door to yet more accusations of bias. And for what?

Perhaps that’s why Twitter has spent the last day or so retroactively tagging tweets from certain officials with the Chinese government that also contain “misinformation” – some of it claiming that the coronavirus originated in the US.

Mouthpieces for Beijing, and for practically every government, even Venezuela and Iran (two countries that have drawn scrutiny from Twitter in the form of mass account-deletion) are active on Twitter. And one of the most effective arguments against Twitter’s decision to label Trump’s tweets is that the company hasn’t done nearly enough to filter out far more sinister actors, like ISIS recruiters, or stooges from Russia, China, Iran and America’s myriad geopolitical enemies – and some of our allies too.

Interestingly, a quick look at the foreign ministry spokesman’s feed shows that only a few tweets have been labeled.

Furthermore, aside from the occasional reference to the “terrorists” threatening law and order in Hong Kong, the feed looks almost identical to one of those left-wing rose emoji accounts with 5k-10k followers.

Meanwhile, Taiwan has continued to poke and prod at Beijing by speaking out in defense of Hong Kong. A top Taiwanese official said prosperity and stability cannot be easily disrupted by separatist forces, rebutting Beijing’s accusations of “terrorism”.

As the conversation about Twitter’s role in moderating ‘the conversation’ unfurls on twitter, two analysts with Height Capital Markets argued that the White House’s new executive order has “more bark than bite”. Investors, looking at this morning’s performance, have taken a decidedly different view.

President Donald Trump’s pending social media executive order is likely “more bark than bite,” Height Capital Markets analysts Chase White and Clayton Allen wrote in a note, citing news reports suggesting the order will address Section 230 of the Communications Decency Act, the liability shield intended to protect Internet platforms from content posted on their sites.

Meanwhile, we’re seeing some interesting action in twitter shares premarket…

…buybacks?

But whatever happens, we’ll definitely be keeping an eye on the Ayatollah’s twitter feed. Will the company dare to apply these misinformation labels to Iran’s supreme leader?

via ZeroHedge News https://ift.tt/3cbkmQ7 Tyler Durden

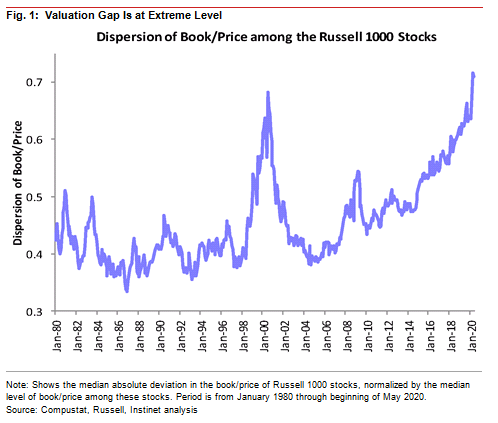

The remarkable deflationary and inflationary crosscurrents swirling through the economy are grossly underappreciated and misunderstood. Need proof? Watch CNBC or read Wall Street research and consider the likelihood of the smooth path back to “normal” they tout.

It is comforting to think about “normal” and what that may entail for our lives and portfolios. However, given the global economic tsunami and extraordinary monetary and fiscal stimulus, we would be remiss if we did not raise awareness that economic and market recovery may be far different from “normal.”

One of our deepest concerns is a highly inflationary outcome, an experience not seen in fifty years, and one for which we are least prepared. Markets always have a strange way of finding investors weakest points.

Disequilibrium Defined

“Inflation defined is, in fact, a disequilibrium between the amount of currency entering an economic system relative to the productive output of that same system.” – From our recent article, Jerome Powell & The Fed’s Great Betrayal:

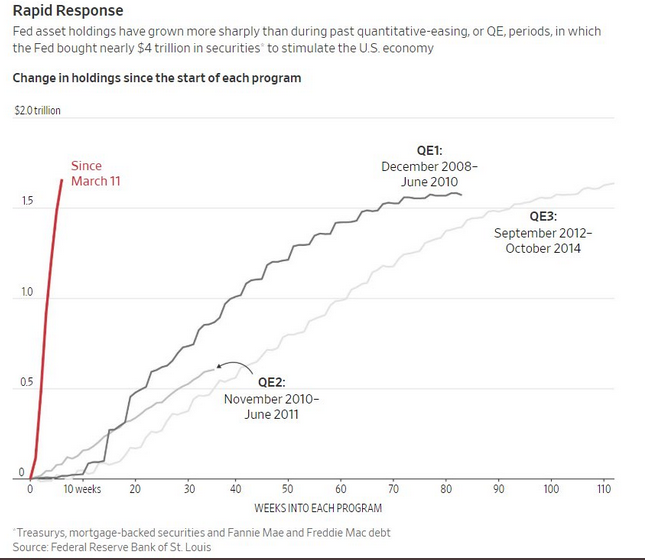

As of April 13, 2020, the money supply, measured by M2, has grown 15.9% on a year over year basis. The vast majority of the growth occurred over the last month as the Fed’s balance sheet exploded by 61%, dwarfing all prior QE operations.

The apparent reason for the Fed’s actions is a plunge in consumption and the productive output of the nation combined with an unprecedented flood of unemployment claims.

Despite those maneuvers, the economic decline is destroying economic output and is, thus far, deflationary in aggregate. We expect deflationary imbalances to continue to dwarf inflationary impulses while economic conditions languish.

However, we must consider that all of the newly created money and debt, crippled supply chains, and many other economic, social, demographic, and geopolitical factors can suddenly offset deflationary imbalances and supercharge prices when the economy does pick up.

In this article, we look back at history and gauge what has driven past bouts of inflation and compare them to the current one. In the next part two, for RIA Pro subscribers only, we share analysis of how 49 different industry sectors performed during prior inflation eras.

Given the enormous monetary and fiscal policy response to current circumstances, the growth in money supply and debt, and the low probability that the economy will ever be capable of servicing those obligations without inflation, this overlooked topic is essential.

The Monetary Exchange Equation

Before sharing our analysis, it is worth revisiting our article, Stoking the Embers of Inflation. In the article, we presented the well-known equation below, which provides a foundation for understanding how prices change.

Monetary Exchange Equation

To understand how the Fed’s commitment to continued interest rate hikes and balance sheet reduction (Quantitative Tightening – QT) affect inflation or deflation, the Monetary Exchange Equation should be analyzed closely. The equation is not a theory, like most economic frameworks based on assumptions and probabilities. The equation is a mathematical identity, meaning the result will always be true no matter the values of its variables. The monetary exchange equation is as follows:

PQ = MV

The equation states that the amount of nominal output purchased during any period is equal to the money spent. Said differently, the price level (P) times real output (Q) is equal to the monetary base (M) times the rate of turnover or velocity of the monetary base (V). The monetary base – currency plus bank reserves, is the only part of the equation that the Federal Reserve can directly control. Therefore, we believe to form future price expectations, an analysis of the Monetary Exchange Equation using the forecasted monetary base is imperative.

The Inflation Identity

Through simple algebra, we can alter the Monetary Exchange Equation and solve for prices. Once the formula is rearranged, the change in prices (%P) can be solved for, as shown below. In doing so, what is left is called the Inflation Identity.

%P = %M + %V – %Q

Prices are a function of the change in the money supply and the velocity of money less the economic output.

Today’s Equation

We know the money supply is soaring, but at the same time, the velocity of money and economic output are plummeting. The destruction of monetary velocity is offsetting inflationary pressures.

Someday soon, consumers and corporations will spend again, causing monetary velocity to pick up. At the same time, the Fed has been vocal that they will remain cautious about removing stimulus.

Our inflation concerns stem from the Fed’s sentiment and its track record over the last decade.

After the Financial Crisis and recession of 2008/09 ended, it took the Fed five years to halt the multiple quantitative easing (QE) campaign, seven years to begin raising interest rates from zero, and nearly a decade to attempt reducing the size of their balance sheet. In fact, in September of 2019, despite a strong economy, a 50-year low unemployment rate, and historically easy financial conditions, the Fed started up QE 4. The basis for that decision was that the repo markets were not allowing hedge funds to maximize their leverage, thus threatening support for risky assets.

Even in its infancy, this recession is worse than the previous crisis and recession. Based on the Fed’s activities from the last ten years, what is the likelihood that current or future Fed leadership will be any quicker to remove stimulus this time?

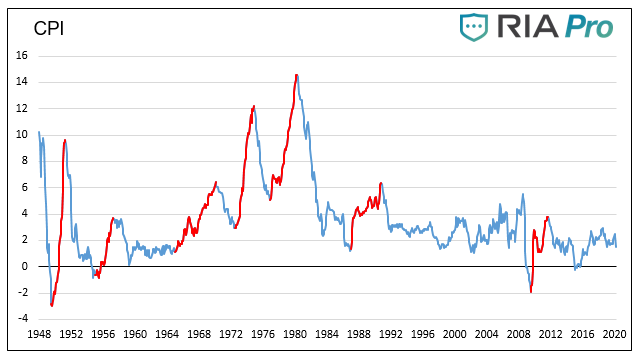

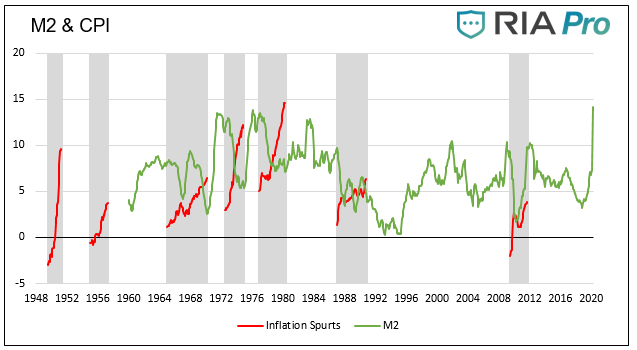

Historical Bouts of Inflation

Since the late 1940s, there have been seven periods in which inflation rose significantly over a relatively short period. Those periods, forming the basis of our analysis, are shown in red below.

The impetus for inflation during each instance is unique to that period. For example, inflation of the early late 1960s and the 1970s was, in part, the result of oil embargos, the emergence of the baby boomer generation, the Vietnam War, and the sexual revolution.

In 1971, President Nixon stoked inflationary pressures when he suspended the Gold standard. His action gave the Fed more flexibility to increase the money supply at its whim. For more on Nixon’s fateful decision, please read our article- The Fifteenth of August.

Inflation of the late 1940s and mid-1950s was in large part due to post-WWII global rebuilding and the suburbanization of America, respectively. The Fed played its role by goosing the money supply to cap interest rates from 1942 to 1951.

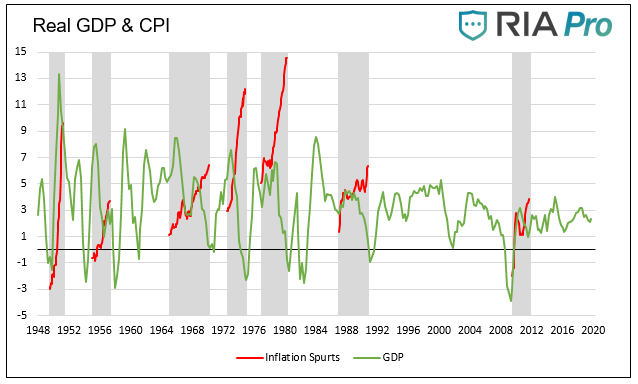

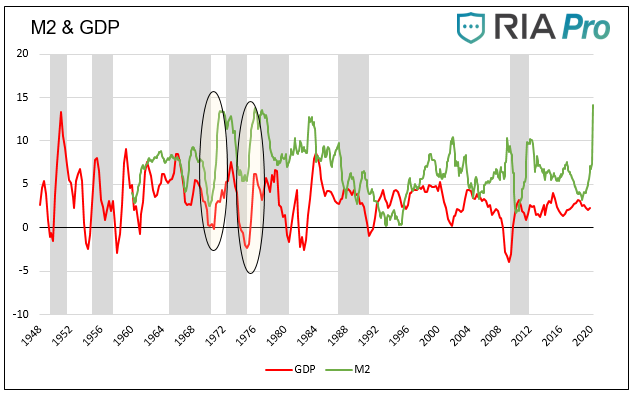

The following two graphs show how GDP and money supply varied during the highlighted inflationary periods.

Data Courtesy St. Louis Federal Reserve

As the graphs show, and as a reflection of the complexity of an economic system, there is no prescribed set of monetary and economic circumstances that determine if inflation will occur. We only know that inflation is a “monetary phenomenon” and is the result of a deliberate act of policy. Still, there are some important takeaways that we can apply to the current situation.

Note that in the GDP CPI graph, six of the seven inflation “events” happened during or after substantial increases in real (inflation-adjusted) GDP.

Data on money supply (M2) only goes back to 1960, so the first two instances of inflation are not comparable. The two most substantial increases in M2, the 1970s, were followed shortly by inflation. Looking at the others, however, the correlation between M2 growth and inflation is not as evident.

Comparing GDP and money supply to prior bouts of inflation leads us to consider that the two inflationary episodes of the 1970s are most applicable to current circumstances. Make no mistake; there are many economic and social differences between then and now.

But, the synchronization of increasing economic activity and the money supply was, in large part, responsible for inflation in the 1970s. It might also be the recipe for inflation in the coming years.

1970s Redux?

Once a reliable treatment and/or vaccine for COVID-19 is developed, economic activity will come out of its coma. The combination of people finding jobs, companies spending to grow production to meet rising demand, and the release of pent up consumption pressures will produce a sharp increase in GDP.

We have little doubt that the government will further fuel recovery with multi-trillion dollar deficits. We have even less doubt that the Fed will keep money flowing to fund the deficits at reasonable interest rates.

Such a scenario does not mean GDP will return to pre-COVID levels, but it implies that economic growth rates will be outsized compared to growth rates of the prior decade.

How does this experience compare to the 1970s?

Unshackled by the limits of the gold standard, the Fed twice sharply increased the money supply during the 1970s. As mentioned earlier, the first instance in the early 1970s was to fend off a recession and fund the Vietnam War. The second round of money printing was to combat economic weakness from 1973-1975 due to a gas price shock from the oil embargo. Both periods witnessed GDP growth of around 7% and annual money supply growth of about 10%.

Also, consider that even before the Coronavirus pandemic, there were only two periods on record where fiscal deficits expanded despite the economy running at full employment. One was during the Johnson administration in the mid-1960s, and the other was 2018-2019. Fiscal stimulus in the 1960s played a role in laying the foundation for inflation in the 1970s and early 1980s. It is an equally important point of consideration today.

It also bears mentioning that the extent of supply chain reconfigurations likely to take place will force companies to find alternative ways of sourcing and manufacturing products. That necessarily means companies will pay more for inputs, and customers will pay more for end products. That is not deflationary.

Maybe the economy will not grow as much as we think, but the Fed is sure to be very reluctant to remove stimulus. We believe the 1970s, with its corresponding economic and money supply growth, although imperfect, is a good analog for the future.

The graph below highlights the corresponding increases in GDP and M2 during the 1970s. As a point of comparison, the growth of M2 and GDP before the other three episodes in which M2 data is available occurred separately and thus sharply reduced the inflationary impact.

Summary

Given the scope of the current situation, a return to something other than normal is not a long-shot proposition. We would be failing you, our readers, if we did not put in the time and effort to think about and plan for something other than what supports the paychecks of “professionals.”

Inflation is a real and present danger, and policy decisions are the cause. A complex crosscurrent of influences will determine the magnitude of an inflation problem.

Make no mistake; regardless of whatever happens with the virus and economic activity, the Fed’s monetary actions today and tomorrow are the most significant input.

Having watched the Fed for decades and listened to many Fed Presidents’ urge for policies that drive inflation higher, it would be wise to think about how to structure a portfolio in times of inflation.

We cannot predict, but we can prepare, and the road ahead is likely to be very different than the road behind.

via ZeroHedge News https://ift.tt/2Xw1aqE Tyler Durden

{kind=link}