“It’s got nothing to do with your Vorsprung Durch technique, you know..”

What do you want to hear first? The good new or the bad news?

The Good News

It now looks like the economic catastrophe the Virus has triggered could be shorter than we envisaged.

One of things I’ve come to understand though what we laughingly call my financial career is:“Things are never as great as you hope they will be, but they are never as bad as you fear they might be.” That looks likely to prove true with Coronavirus.

It remains vital governments force the R transmission number down through lockdown to drop the peak of infection curve so hospitals aren’t swamped.

But, the policy is working – the epidemiologists from Imperial College, whose report triggered the UK response, now say deaths could be less than 20,000 because the social distancing polices are working.

Sadly, global health services will still be tested to their limits over the next few weeks. There will still be a terrible crisis – and I stood on our balcony and clapped the NHS last night to show solidarity with them.

It now appears the disease may be far more widespread than thought – and that’s a good thing. It means immunity is building up – as a report from Oxford suggested earlier this week. There will still be a large number of people who get a very serious and life-threatening disease, but that’s a fall smaller proportion of the population than originally feared. The maths is not our friend – 1% of 50mm infected people being hospitalised is the same number as 5% of 10mm people.

It’s all down to testing – or the lack of it. Most of the modelling thus far has come up against the same problem: We have absolutely no idea of the number of people around the global actually infected.In the West testing has been pitifully slow and is weighted towards testing only those obviously exposed to, or suffering from the Covid-19 symptoms.

The result has been a bias towards the expectation of a high mortality rates – which although the bias has been factored in, clearly influences policy. The Italy number of around 80,000 cases and 8,000 desks suggests a 10% death rate – which we know is overly high because of the delay factor between infection and outcome, and the high numbers of elderly. In China we see around 3000 deaths against 81,000 cases, suggesting a much lower rate of 3.7%.

This is where it gets interesting. Korea comes in at 139 death against 9,300 cases, a 1.5% mortality rate, while Germany has 228 deaths agains 40,500 cases, a 0.5% mortality rate. Testing in Germany has been more rigorous in the run up than in any other European country – but the German papers are still full of how difficult it is to get tested, suggesting even Germany has also under-tested. (We’re looking to see if we can get numbers for positive versus negative tests – but that will still be biased.)

Once we get more data on just how wide the infection is – then governments will be able to reassess the effectiveness of lockdown as against other policies to ensure against future waves. If we have a high number of infected people, say 30% plus, then it’s possible we could see government allow many workers to return to work, but with many social distancing measures remaining in place. Activity could pick up quickly.

This is all supposition at this point. There are rumours of more cases breaking out in China but being under-reported. We won’t know for sure till we get proper testing in place.

Whats the Bad News?

If you bought the rally of the last few days, then I think you are in for disappointment. The shortest bear market in history ain’t over yet. There is too much noise and consequences to come. Just watch the jobs queue.

The economic reality – brought into painful context by yesterday’s US Initial Claims report showing US 3.2 million workers losing their jobs – remains dire. Every single country is publishing massive economic activity downgrades. Every finance minister is apologising for not being able to save everyone. The outlook wavers between a deep recession and outright global depression.

Yet the markets have rallied hard on the back of kitchen sink government and central banking support – ignoring the dire reality. You can’t fault markets for arbing the support packages. If the ECB is willing to be unlimited amounts of Italy paper – what’s not to like. If they want to buy copies of The Daily Mail at £1 each, then I am a buyer at 99p. (I don’t know which is fundamentally more worthless…. an Italian bond or the Mail?)

Some analysts say there isn’t much more left in the authorities ammunition cupboard if sentiment drops again. Yes there is. The authorities have gone this far – why not just start buying equities as well?

There are going to be consequences…

As always, I look to the bond market for clues. When it comes to corporate bonds, its really manky. Soaring defaults, downgrade escalation, chronic illiquidity. Excellent. Despite QE Infinity, the corporate bond market is close to breaking – which means massive opportunities!

I was amused by a piece in the FT about the “Doom Loop” in ETF bond funds. I still get “puff advertising” from firms telling me how ETFs are great liquid way to invest in markets. Yet, they are proving chronically illiquid with the ETFs dealers now arguing the definition of liquid actually is “as liquid as the underlying securities” which is as liquid as set concrete in the bond markets. Anyone who bought ETFs without question the dealer blandishments about liquidity should really be considering a different career.

Right now, I just want to go back to sleep. I will write more next week about just how vulnerable markets remain. Topics might include some of the following danger areas:

1) Headline Coronavirus Shock Threats

2) Cash crisis across Globe

3) What a bond market meltdown means for all financial assets

4) Unintended Consequences of Rescue Policies

5) Policy Deliverables – the risk of failure to deliver economic rescue likely to destabilise sentiment

6) Fundamentals – demand and supply shocks to continue longer rather than abate.

Futures Tumble As Best Rally Since Great Depression Crumbles

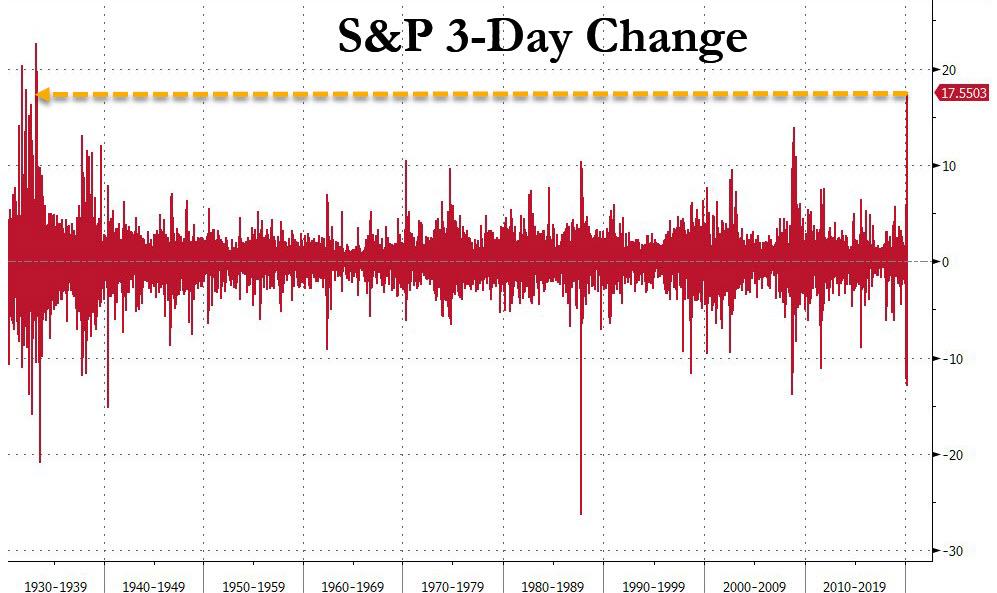

The market moves are coming fast and furious now, and after plunging 36% from its all time highs about a month ago, stocks staged a furious rebound, rising 20% in just the past four days and entering a new bull market, with the return in just the past 3 days a stunning 18%. The last time stocks were up so much, so fast? In 1931… the depths of the great depression.

But the euphoria is fading fast as the US becomes the new epicenter of the coronavirus, surpassing China, and after surging in the last 10 minutes of trading on Tuesday following a near record $7BN MOC amid a flood of pension rebalancing, futures have slumped and are down almost 3%, with Europe’s Stoxx 600 down over 3%, and the UK’s FTSE 100 down 4.1%, the drop accelerating following news that Boris Johnson tested positive for the coronavirus.

The drop takes place as debate on the fiscal stimulus bill aimed at flooding the country with cash in a bid to counter the economic impact of the intensifying coronavirus outbreak, is scheduled to start in the U.S. House of Representatives later on Friday.

On Thursday, the United States became the country with the most coronavirus cases, surpassing even China, where the flu-like illness first emerged late last year. Policymakers may need to offer more stimulus as the virus slams the brakes on economic activity and increases healthcare spending.

“I’m not sure what measures are left, but the reaction in stocks shows some people hoping for more stimulus thought the market was a little oversold,” said Yukio Ishizuki, FX strategist at Daiwa Securities in Tokyo. “Currencies tell a different story. The dollar is the lead actor. The mad rush to buy dollars due to liquidity concerns is starting to fade.”

European stocks also slumped, dropping more than 3% and led lower by banks and real estate shares after the region’s leaders struggled to agree on a concrete strategy to contain the fallout of the pandemic, leaving key details to be ironed out in the coming weeks.

Earlier in the session, Asian stocks gained, led by industrials and utilities, although markets in the region were mixed, with Jakarta Composite and Japan’s Topix Index rising, and Australia’s S&P/ASX 200 and Taiwan’s Taiex Index falling. The Topix gained 4.3%, with Kaneko Seeds and Segue rising the most. The Shanghai Composite Index rose 0.3%, with Guirenniao and Shanghai La Chapelle posting the biggest advances.

The recent surge in risk appetite (which according to Morgan Stanley was just a furious short covering spree) will promptly be tested by the continuing spread of the coronavirus and the crippling effect of business closures. Tokyo is now seeing a surge in cases, while global deaths from the pandemic surpassed 24,000. The Reserve Bank of India on Friday became the latest central bank to step up emergency action to cushion the economic impact.

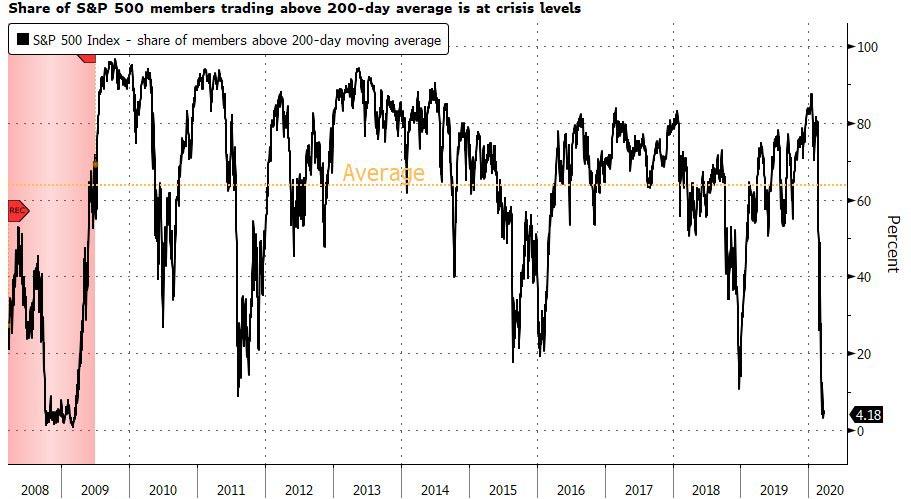

Meanwhile, traders argue that even with the jump in stocks, sentiment hasn’t reversed enough for the rally to be sustainable with the number of companies trading above the 200DMA still at crisis levels.

Leaders of the Group of 20 major economies pledged on Thursday to inject over $5 trillion into the global economy to limit job and income losses from the coronavirus.

In rates, the 10Y yield was about 10bps lower, trading to 0.75%, down from 0.85% overnight: “The market is pricing in a fairly short duration of weakness” for the economy, Priya Misra, global head of rates strategy at TD Securities, said on Bloomberg TV. “A month from now when we realize we are still stuck at home and the data is not looking any better, that is when you can get a further downside move in yields.”

In Europe, Italian bonds slid amid German opposition to coronabonds, underperforming euro-area peers which all advanced, as the latest stimulus figures fell short of its peers. BTPs bear-flattened, widening the spread to bunds by 16bps to 174bps; Rome’s latest stimulus figures, which fall short of peers, will have to be self-funded without the backstop of a euro-area bond. Elsewhere, bunds bull-flattened as equities slide, matching Treasury gains. Gilts bull-flatten ahead of next week’s BOE buyback schedule due at 4pm London time. German 10y yield -9bps to -0.45%; bund futures 126 ticks to 172.33; France 10y -8bps to -0.06%; Italy 10y +7bps at 1.30%.

Overnight, India’s RBI became the latest bank to slash rates by 75bps to 4.4%; voting 4-2 to cut rates as the reverse repo rate lowered to 4.15%. Governor Das said the move was designed to mitigate effects of the virus, revive growth and preserve financial stability. He added that the RBI’s response must involve conventional and unconventional measures. Das noted that inflation was running higher than projections in January and February, and that aggregate demand may weaken, and ease inflation further due to Covid-19. Das also said projections for growth and inflation will be dependent on how Covid progresses; he noted that uncertainties in the outlook and explained that is why the MPC has refrained from providing growth and inflation forecasts. Das also announced targeted long-term repo operations, offering up to INR 1trln.

In FX, the Bloomberg Dollar Spot Index headed for its biggest five-day drop on record, even as the gauge was set to gain for Friday’s session and appeared to be reversing upward, inversely proportional to risk sentiment. Traders pointed to a confluence of reasons, ranging from less stress in funding markets, the repatriation of funds as the quarter ends and the worsening coronavirus outbreak in the U.S. The dollar reversed Asia-session losses and advanced versus most Group-of-10 peers as month- and quarter-end flows came into play; the greenback traded around 1.10 per euro while the Norwegian krone led declines, slipping by almost 1%;

Elsewhere, Norway’s krone was set for its biggest weekly advance versus the U.S. dollar on record.The Yen rose on strong demand from Japanese exporters ahead of the country’s fiscal year end on March 31. The Aussie was set for the biggest weekly gain since 2011 as U.S. dollar weakness spurred early month-end hedging from exporters and momentum buying from investors.

To the day ahead now, and data releases out include personal income and personal spending data for February, along with that month’s PCE core deflator. The US will also see the final University of Michigan sentiment reading for March, and over in Washington, the House of Representatives are scheduled to vote on the coronavirus rescue package.

Market Snapshot

S&P 500 futures down 1.5% to 2,569.75

STOXX Europe 600 down 1.9% to 315.34

MXAP up 1.7% to 137.67

MXAPJ down 0.06% to 432.76

Nikkei up 3.9% to 19,389.43

Topix up 4.3% to 1,459.49

Hang Seng Index up 0.6% to 23,484.28

Shanghai Composite up 0.3% to 2,772.20

Sensex up 0.3% to 30,040.00

Australia S&P/ASX 200 down 5.3% to 4,842.43

Kospi up 1.9% to 1,717.73

German 10Y yield fell 6.5 bps to -0.426%

Euro down 0.09% to $1.1022

Italian 10Y yield fell 31.5 bps to 1.057%

Spanish 10Y yield fell 4.5 bps to 0.524%

Brent futures down 0.3% to $26.25/bbl

Gold spot down 0.7% to $1,619.67

U.S. Dollar Index up 0.2% to 99.50

Top Overnight News

U.S. President Donald Trump and China’s Xi Jinping pledged in a phone call to cooperate in the fight against the coronavirus pandemic, signaling a fresh detente between the two countries after weeks of rising tensions

President Donald Trump offered a plan to restore normal business by ranking counties by their virus risk. China seals borders to most foreigners starting Saturday

European leaders struggled to agree on a concrete strategy to contain the fallout from the deadly coronavirus, leaving key details to be hammered out in the weeks ahead

Treasury Secretary Steven Mnuchin reiterated that he wants U.S. financial markets to remain open even as the coronavirus fuels wild volatility, while adding that he’s focused on helping mortgage firms expected to be hit hard by the pandemic’s spreading economic pain

Oil was buoyed by a wider risk rally driven by monetary and fiscal responses to the coronavirus to head for its first weekly gain in five, despite a continued deterioration in demand

S&P Global Ratings cut its sovereign credit score for Mexico by one notch to BBB, saying shocks from the spread of coronavirus and an oil price rout will harm the country’s already grim economic outlook

The Federal Reserves dollar swap lines were tapped for more than $206 billion by other central banks as of March 25, while Europe and Japan took another $100 billion in three-month operations which settled March 26. This helped to cool cross-currency basis markets, one of the key borrowing channels

Major APAC indices initially took their cues from Wall Street, rising firmly at the open, amid optimism that policymakers will continue to roll-out stimulus measures to guard economies against covid-induced downside. However, as the European day comes into focus, the picture is mixed, as Aussie shares turned negative, and other bourses off highs. US indices finished up around 6%, with the Dow seeing its strongest three day run since 1931 and re-entering a bull-market, while the S&P had its best three-day performance since 1933. Gains were led by defensive sectors (utilities, telecoms, health care). Equities shrugged-off the highest weekly jobless claims print on record. Some desks also noted that month/quarter-end rebalancing will see 850bln of flows into equities. US equity futures opened firmer, though subsequently gave up gains, and are trading lower, albeit off worst levels. ASX 200 (-5.3%) was led lower by its heavyweight financial and mining sectors, while the Nikkei 225 (+3.8%) shrugged off a firmer JPY, with some optimism in the country emanating from Japanese Economy Minister Nishimura who stated that there was no need to declare a state of emergency over the outbreak. Elsewhere, Hang Seng (+0.6%) and Shanghai Comp. (+0.3%) remained in positive territory and were buoyed by increased efforts from Chinese officials to stem a substantial second wave of the virus in the country, with reports yesterday noting that airport tests will be ramped up for people arriving from abroad.

Top Asian News

The Second Virus Shockwave Is Hitting China’s Factories Already

WeDoctor Mandates Banks for $1b Hong Kong IPO, IFR Reports

A Grocery Tycoon Races to Keep India Fed and His Company Afloat

India’s RBI Unleashes $50 Billion of Liquidity, Slashes Rate

Fearing Next Wave, China Doesn’t Want Its Diaspora Coming Back

A downbeat session thus far for European equities (Euro Stoxx 50 -3.3%) as the bourses look set to snap its three-day rally heading into another risky virus-focused weekend. US equity futures follow suit from Europe with losses currently tallying to around 2% per index – with eyes State-side on the virus bill which is poised to make its passage through the House later today. Back to Europe, UK’s FTSE 100 (-3.9%) underperforms the region with a number of its stocks at the foot of the Stoxx 600 index as caution arises from the prospect of delayed UK/EU FTA negotiations, despite the already-tight schedule – whilst housing and banks names also see headwinds from the UK govt calling for the halt of home purchases/sales. Meanwhile, Italy’s FTSE MIB (-2.3%) continues to feel some support from the ECB dismissing the 33% issuer limit for its emergency program purchases. European sectors reside largely in the red but reflect risk aversion, whilst underperformance is seen in the Energy sector on account of the downside in Brent prices. The sector breakdown meanwhile sees Travel & Leisure pressured on the ongoing virus-induced demand woes for the sector. Looking at individual movers, ProsiebentSat1 (+7.0%) sees upside amid the immediate resignation of its CEO, and with potential tailwinds from work-from-home flows. LafargeHolcim (-3.5%) and Safran (-2.3%) shares are pressured after the Cos withdrew their respective FY targets.

Top European News

Europe Bonds Get $340 Billion Orders as Cheap Prices Allay Virus

ProSieben Jumps After Ousting CEO To Restore Focus on German TV

Domino’s Pizza to Suspend Final Dividend; Deliveries Accelerate

Merkel Pleads With Germans for Patience on Lockdown Measures

Housebuilders Slump as U.K. Government Urges Suspending Deals

In FX, the Greenback has regained an element of composure after yesterday’s slide and extended losses across the board, with some analysts suggesting that the DXY eventually found technical respite in the form of Fib support around 98.840 and others noting that the index is correlating quite well with moves in the VIX. Both theories appear credible and are backed up by price developments given the DXY’s subsequent recovery to 99.500+ and the so called fear gauge climbing to 67 from around 61 at settlement on Thursday. Certainly, traditional fundamentals and data do not seem to be driving sentiment or direction as the focus remains firmly on COVID-19 amidst the backdrop of swings in global stock markets and risk assets vs safe-havens.

JPY/GBP/AUD – Bucking the overall trend, or resisting the broad Dollar revival to be more precise, as the Yen retains its renowned safe-haven allure above 109.00, while Sterling appears to have formed another higher platform on the 1.2100 handle to probe above 1.2300 and match a key chart resistance level (50% retracement of reversal from 1.3200 to 1.1412), albeit with the aid of Eur/Gbp tailwinds as the cross recoils from almost 0.9100 to sub-0.9000, with month/quarter end positioning cited on top of possible official Pound buying interest. Elsewhere, the Aussie is holding up relatively well and again month-end demand has been touted alongside exporter bids, leverage stops and momentum accounts joining the break of 0.6100 to the overnight highs.

CAD/EUR/NZD/CHF – The Loonie is underperforming after failing to sustain momentum through 1.4000 and record low Canadian crude prices may be weighing along with contagion from the coronavirus after the huge spike in US weekly claims that is expected to be evident in domestic data given reports that 500k people applied for benefits last week. Similarly, the Euro topped out ahead of 1.1100 and is waning on the ongoing spread of pandemic cases and fatalities across the common currency community, with particular focus on Italy and Spain. However, decent option expiries at the 1.1000 strike (1 bn) may provide a buffer for Eur/Usd. In contrast, the Franc and Kiwi are both rangebound within 0.9645-0.9587 and 0.6126-0.5921 respective bands.

EM – Broad retracements as the Usd consolidates off its lows, but the Zar also conceding ground in the run up to Moody’s SA ratings review that could well see the sovereign lose its last non-junk standing. Note also, the Rand has been ruffled by the first COVID-19 deaths as the country starts a 3 week lockdown.

In commodities, WTI and Brent front-month futures see divergence, with outperformance seen in the former after yesterday’s -7.7% settlement, whilst ICE Brent closed lower by around 4% yesterday. Today’s narrowing in spread seems to be more of a consolidation of the prior session’s widening – which emanated from reports that the US Department of Energy suspended its SPR refill after the DoE failed to secure funding. ING notes that “The US government was keen to fill up the SPR in a bid to help domestic producers, however, news of the suspension has weighed heavily on WT.” Meanwhile, on the OPEC front, the Algerian Oil minister has called for an extraordinary meeting of the OPEC economic panel to assess current conditions and immediate prospects of the oil market, whilst Russia noted that its oil output could decline by 1.5mln BPD this year if prices meander around USD 30-35/bbl – levels above current oil prices, although communication with OPEC+ members remain. Desks note that production cuts needed to counter the sharp decline in demand would be too much for OPEC+ producers to cope with. WTI futures pulled back from ~USD 23/bbl whilst its Brent counterpart treads water just under USD 26/bbl. Elsewhere, spot gold remains lacklustre above USD 1600/oz as the Dollar recoups some of yesterday’s losses. Copper meanwhile remained largely uneventful around USD 2.2/lb following a mixed APAC session.

US Event Calendar

8:30am: Personal Spending, est. 0.2%, prior 0.2%

8:30am: Personal Income, est. 0.4%, prior 0.6%

8:30am: Real Personal Spending, est. 0.2%, prior 0.1%

8:30am: PCE Deflator MoM, est. 0.1%, prior 0.1%; PCE Deflator YoY, est. 1.7%, prior 1.7%

10am: U. of Mich. Sentiment, est. 90, prior 95.9; Current Conditions, est. 106, prior 112.5; Expectations, est. 77, prior 85.3

10am: U. of Mich. 1 Yr Inflation, prior 2.3%; 5-10 Yr Inflation, prior 2.3%

DB’s Jim Reid concludes the overnight wrap

So the second week of working from home comes to an end, and to be honest it’s flown by and I haven’t noticed that I’ve hardly left the perimeter of my house. We’ve been on self-isolation for a week as all three children now have coughs and a slight fever. As a result of the isolation, my wife, who is far more sociable than me, is struggling as she is only interacting with a 4 year old, two terrible two-year old twins and a dog! At least I have numerous conference calls. I pop down for food and drink occasionally and she usually appears frazzled. Thankfully the new trampoline arrived yesterday and my job is to erect it tomorrow. I think this might be even more stressful than the last two weeks as it’s in lots of boxes and when built extends to 16 foot. I’m not sure what’s more likely by Monday, an injury from erecting it or from bouncing on it.

Staying with the remarkable times we operate in, at the start of 2020 if you’d had pulled up a chart of US weekly jobless claims through history (data back to 1967) and seen that we were at around 200k with the highest ever being 695k back in 1982, I wonder what event you would have thought had to happen for there to be a weekly print of 3.28 million less than three months later. All answers welcome! This number yesterday was a more than ten-fold increase on the previous week’s revised 282k reading. We cannot stress enough how unprecedented numbers like this in a single week are. Even in the financial crisis, the peak week in March 2009 was at 665k.

Looking at the state-by-state data, the 2 states that saw the biggest increase in claims were Pennsylvania and Ohio, with a surge of 363k and 181k respectively compared with the prior week. Both are states in the US rust belt and are traditionally swing states in presidential campaigns. Indeed Pennsylvania, where there was the biggest increase in claims, was won by President Trump in 2016 by a margin of less than 1 percentage point. So the fact that they’re seeing the biggest increases in the country is certainly not something that’ll be welcomed by his campaign. Our economist’s previous work has found that jobless claims are the single best real-time indicator of recession (see “Jobless claims claim title for best recession indicator”), so this rise leaves no doubt that the US economy is currently in the midst of a recession. Consistent with the sharp rise in claims, their summary index of these high-frequency indicators has essentially gone into free fall indicating data which is about twelve standard deviations worse than average and consistent with -4% year-over-year GDP growth. This is worse than any readings during the financial crisis.

Given yesterday’s numbers, it was no surprise that Fed Chair Powell said in an interview on NBC’s Today show (a non-business channel) that the US “may well be in a recession”. His address was aimed at Main Street and he added that “When it comes to this lending we’re not going to run out of ammunition.”

Speaking of economic support, the House of Representatives are scheduled to vote on the $2 trillion coronavirus rescue plan today. In a Bloomberg TV interview yesterday, Speaker Nancy Pelosi said that she had “no doubts whatsoever” the package would pass today, which would set up the bill to go to President Trump’s desk for signature. However, overnight, House leader Hoyer has suggested that the legislature may not pass today by voice vote and instead the house could pass the bill by a Roll Call vote but will need quorum for that of typically 218 members. This is a potential thorn which we highlighted yesterday that can result in delaying the passage of bill. Futures on the S&P 500 are trading down -1.69% this morning.

With financial markets hopeful on the prospects for stimulus, global equities moved higher for a third straight day, a phrase that we haven’t said for a while (since February 12th in fact, according to the MSCI all-world index), with the S&P 500 up a further +6.24%. The index’s latest advance means it’s up over 17% from its closing low on Monday. The large gain adds to the run where 16 out of the 19 sessions so far this month have seen the S&P move by at least 2% in either direction. The Dow Jones hit a remarkable milestone of its own yesterday, after its +6.38% advance left the index +21.30% above its Monday low and in technical “bull market” territory!!! European equities also advanced on the day, with the STOXX 600 up +2.55% and nearly +15% since Monday, with every sector gaining on the day led by the most beaten up sector of late namely Travel and Leisure – up +7.47% on the day.

This morning Asian markets are a mixed bag with the Nikkei (+1.95%), Hang Seng (+1.21%) and Shanghai Comp (+1.41%) up while the Kospi is little changed and ASX (-5.30%) is down. In FX, the US dollar index (-0.36%) is on course for its fifth daily decline while in commodities, Brent crude oil is up +0.84%. As for overnight data releases China’s Jan-Feb industrial profits came in at -38.3% yoy, the lowest on record.

In other news, The Reserve Bank of India became the latest central bank overnight to cut rates as it lowered the key lending rate by 75bps to 4.40% from 5.15%. The central bank also reduced the reverse repo rate, the rate at which banks park funds with the RBI, by 90bps to 4% in order to incentivize lending by the banks. Elsewhere, S&P cut Mexico’s credit rating by one notch to BBB, saying shocks from the spread of coronavirus and an oil price rout will harm the country’s already grim economic outlook. The Mexican peso is down -1.23% this morning to 23.2305.

Back yesterday where sovereign debt also rallied strongly, with European sovereign bonds in particular gaining as a result of the ECB news that the limits on buying more than a third of a country’s bonds would not apply to their pandemic emergency purchase programme in certain conditions. For more details on this news see our rates team’s publication from last night here. Spreads narrowed in response, with the Italian 10yr spread over bunds down by -21.8bps to a 3-week low, while Spanish (-20.5bps) and Portuguese (-23.9bps) spreads also saw significant reductions. The biggest outperformer was Greece however, with the spread there falling by a massive -61.4bps. US Treasuries advanced as well, with 10yr yields down by -2.3bps (and a further -4.8bps this morning). Credit continued to rally with US HY cash spreads tightening -82bps, while IG tightened -21bps and Europe HY cash tightened -31bps although IG was flat.

Staying with credit, with all the big announcements of central bank support and fiscal stimulus packages over the last couple of weeks, all eyes in the credit world have been on corporate bond funds, hoping that their recent heavy outflows would finally stop. After the latest weekly fund flow data release overnight, we have published the report “Corporate Bond Fund Outflows Go On But More Slowly” which provide an update and commentary on the latest flows. It also attempts to explain some vastly different headline numbers on US IG corporate bond fund outflows based on data from different providers. You can download the report here.

Moving on. Although the ECB news was a positive, the EU leaders‘ summit late last night didn’t appear to be. A 2-hour scheduled meeting lasted 6 hours with no clear plan for a joint EU response to the crisis. There was no mention of the ESM in the communique which hints at Italy refusing to accept the conditionality this would bring. Italy believes that the virus is a common problem and can’t accept conditionality – which is a legal necessity. In addition “Coronabonds” seem to have hit an early dead end even as nine EU member states (including France, Italy and Spain) had earlier jointly written to the head of the EC requesting for it to be considered. The Eurogroup now has two weeks to come up with alternative proposals. It seems the age old problem for Europe has struck again. The more the ECB do, the less pressure there is on Governments to burden share. In fact the emergency ECB bazooka deployed last week probably helped cause the impasse.

Earlier and across the Channel, the Bank of England also announced their latest rate decision yesterday, voting unanimously to keep rates on hold at 0.1%, in line with expectations. To be honest though, the main BoE action already happened earlier in the month after the two emergency rate cuts saw rates lowered by 65bps in total, as well as the announcement of a further £200bn in QE. A notable line from the monetary policy summary released by the BoE was that “there is a risk of longer-term damage to the economy, especially if there are business failures on a large scale or significant increases in unemployment.” In terms of policy looking forward, there was also the line in the minutes that “If needed, the MPC could expand asset purchases further”, as well as the fact that the MPC “stood ready to respond further as necessary to guard against an unwarranted tightening in financial conditions, and support the economy.”

Turning to yesterday’s other data releases, in France the INSEE’s business confidence measure fell to by 10 points to 95 in March (vs. 97 expected), which was a 5-year low for the reading and the largest monthly decline since the series began. Meanwhile the Kansas City Fed’s manufacturing index in March fell to -17 (vs. -10 expected), which was the lowest reading since April 2009. Other data was more backward looking, with UK retail sales falling by -0.3% mom in February (vs. +0.2% expected). The effect of the coronavirus wasn’t generally visible at that point, though the ONS did remark that “a small number of retailers suggested that online orders shipped from China were reduced because of the impact of COVID-19.” The third reading of Q4 2019’s GDP growth in the US was also confirmed at an annualised 2.1%, unchanged from the second estimate.

To the day ahead now, and data releases out include French and Italian consumer confidence for March, while from the US there’s personal income and personal spending data for February, along with that month’s PCE core deflator. The US will also see the final University of Michigan sentiment reading for March, and over in Washington, the House of Representatives are scheduled to vote on the coronavirus rescue package.

The Senate’s $2 Trillion Coronavirus Relief Package is not fiscal stimulus and it’s not a lifeline for the tens of millions of working people who have suddenly lost their jobs. It’s a fundamental restructuring of the US economy designed to strengthen the grip of the corrupt corporate-banking oligarchy while creating a permanent underclass that will be forced to work for slave wages. This isn’t stimulus, it’s shock therapy.

Who can survive on $1,200 for one, two or three months time? And what happens to the millions of people who paid no taxes last year? Are they supposed to scrape by on nothing? Congress knows that most households live paycheck to paycheck. With no savings how will they pay the rent, the electric bill, the phone and the cable? Congress is quibbling over an extra $600 per month unemployment for those who are lucky enough to get it, when most people are just trying to figure out how they’re going to survive, how they’re going to pay the mortgage, when they’ll be able to go back to work, and whether their job will still be there when this nightmare is finally over?

Did you know that “if you don’t already have direct-deposit information on file with the IRS from previous tax returns, you won’t get the emergency funds for up to 4 months”? That means millions of people will have zero income for 4 months! What will become of them? Where will they go? Who will provide them with shelter and food? Shouldn’t congress be asking these questions?

And what happens to the 50% of the American people who had less than $400 saved before the crisis hit? What happens to them when they fall between the cracks and lose their apartments, lose their jobs, and lose their ability to maintain their tenuous standard of living? These people will never regain their financial footing. Never. It’s a death sentence. We’re going to see an explosion of homelessness, drug addiction, depression, alcoholism, suicide and crime unlike anything this country has ever seen before. Are the imbeciles in congress so blind that they can’t see that they’re condemning a large part of the population to permanent, inescapable, grinding poverty and desperation? Can’t they see that?

Do you understand why this bill is being rushed through congress?

It has alot to do with the falling stock market but more precisely with the hundreds of corporations that have been hawking bonds to gullible investors who thought they were buying the debt of responsible, well-managed companies that used the money to improve their product-line, train workers, or build new factories. But instead, greedy CEOs have been using the money to buy shares in their own companies to boost executive compensation and reward shareholders. It’s a multi-trillion dollar scam that blew up in their faces causing a complete freeze-over in the corporate bond market. That’s what’s really going on, there’s a massive credit crunch that has a stranglehold on the bond market and there are only two ways to fix the problem:

Let the failing corporations default and pick up the pieces after the dust settles or…

Launch a major $4.5 trillion bailout for busted corporations that drove their companies off a cliff.

Those are the two choices. Naturally Treasury Secretary Mnuchin chose the latter which suggests that the real motive for giving working people the $1,200 checks was simply to divert attention from the massive trillion dollar bailout to teetering corporations. That’s the real objective of the so-called fiscal stimulus bill. It’s another giant welfare check for the plutocrats.

The centerpiece of the new legislation is a provision for $425 billion giveaway to big business. The New York Times explains what is going on in a recent article. Here’s an excerpt:

“Republican senators have suggested creating a fund of $425 billion at the Treasury Department that the Fed could use to back emergency lending facilities — which would enable such programs to grow far beyond that scale.

Because the Fed cannot take on substantial credit risk itself, the Treasury Department backs its emergency lending, using money from a fund that contains just $95 billion. Treasury Secretary Steven Mnuchin on Sunday suggested that the new money in the Republican bill could be leveraged by the Fed to back some $4 trillion in financing.

“We do have limited amounts of money we’re using before Congress passes this bill, so we’re not waiting on Congress,” Mr. Mnuchin said in an interview on CNBC on Monday. “As Congress gives us the authority, we’ll be increasing the facilities substantially.” (“The Fed Goes All In With Unlimited Bond-Buying Plan”, New York Times)

What does it mean?

It means that Mnuchin is transforming the US Treasury into a hedge fund. That’s what it means. It means that the Treasury is going to use the $450 billion that is obliquely allocated in the emergency bill, to create a Special Purpose Vehicle (SPV)–which is a sleazy, off-balance sheet operation that is used to conceal underhanded bookkeeping, that will leverage up by 10x (which means that the Fed will use the $450 billion to borrow tens times more than the original amount or $4.5 trillion) that will be stealthily used to bail out underwater corporations, financial institutions and, yes, banks. (Note–The fairy-tale about “well capitalized banks” is pure bunkum. These guys have serious exposure through “sponsored repo” which is lending to hedge funds via the repo market.) The Fed has already created one SPV for the Commercial Paper market under the Treasury’s Exchange Stabilization Fund (ESF) which is supposed to be used to mitigate volatility in global currency markets, not for bailing out failing corporations. It’s a complete misuse of funds. Unfortunately, targeted suspension of the Sunshine Act will prevent the public from figuring out who is getting money in what amount and for what purpose. This whole scam has been carefully worked out right down to legal provisions preventing transparency.

By the way, Mnuchin’s personal bio is worth reviewing. According to Senator Ron Wyden:

“Mr. Mnuchin’s career began in trading the financial products that brought on the housing crash and the Great Recession. After nearly two decades at Goldman Sachs, he left in 2002 and joined a hedge fund….

“In early 2009, Mr. Mnuchin led a group of investors that purchased a bank called IndyMac, renaming it OneWest. OneWest was truly unique. While Mr. Mnuchin was CEO, the bank proved it could put more vulnerable people on the street faster than just about anybody else around.

“While he was CEO, a OneWest vice president admitted in a court proceeding to ‘robo-signing’ upward of 750 foreclosure documents a week…between 2009 and 2014, a period during which the bank foreclosed on more than 35,000 homes. ‘Widow foreclosures’ on reverse mortgages – OneWest did more of those than anybody else. The bank defends its record on loan modifications, but it was found guilty of an illegal practice known as ‘dual tracking.’ One bank department tells homeowners to stop making payments so they can pursue modification, while another department presses on and hurtles them into foreclosure anyway.” (“Stimulus Bill: The Fed and Treasury’s Slush Fund Is Actually $4 Trillion”, Wall Street on Parade)

Does that sound like someone who can be trusted in the distribution of $4.5 trillion in government funds?

The media is not even trying to hide the sordid details of what’s going on behind the scenes. Take a look at this excerpt from an article at Bloomberg:

“The Federal Reserve could now have as much as $4.5 trillion to keep credit flowing and make direct loans to U.S. businesses through the massive coronavirus stimulus bill being considered by U.S. lawmakers. The bipartisan agreement, which still needs to be passed by the Senate and House and signed into law by President Donald Trump, will include $454 billion in funds for the Treasury to backstop emergency actions by the Fed to support the U.S. economy, Senator Patrick Toomey said on Wednesday.

The central bank will work with the U.S. Treasury to use that money as a backstop against credit risk as it supports markets for corporate and short-term state and local debt, while also loaning directly to large and medium-sized businesses….

“It is a very, very big thing; it is unprecedented,” the Pennsylvania Republican told reporters Wednesday on a conference call, adding it was an opportunity to lever up “the unlimited balance sheet of the Fed.”

Toomey’s comments suggest Fed facilities could be expanded with the new funds, in effect doubling the Fed’s current $4.7 trillion balance sheet if necessary. On Sunday, Treasury Secretary Steven Mnuchin said the bill would provide up to $4 trillion in liquidity through broad-based lending programs operated by the Fed.” (“Fed’s Anti-Virus Lending Firepower Could Reach $4.5 Trillion”, Bloomberg)

Toomey is an idiot! Can’t he see what’s going on? Why does he say: “This is a very, very big thing.”… “an opportunity to lever up “the unlimited balance sheet of the Fed”??? Doesn’t he know that the US Treasury has now accepted full liability and credit risk for the Fed’s emergency bailout operations. Does he like the idea that the American people will now be on the hook for the CEOs who blew up their own companies to fatten their own bank accounts?? That’s what this means. Readers should parse these articles very carefully, word by word, phrase by phrase. The ugly truth is spelled out in black and white. Here’s the key phrase in the Times article:

“Because the Fed cannot take on substantial credit risk itself, the Treasury Department backs its emergency lending.”

And here’s the key phrase in the Bloomberg article: “The central bank will work with the U.S. Treasury to use that money as a backstop against credit risk as it supports markets for corporate and short-term state and local debt, while also loaning directly to large and medium-sized businesses.”

There it is: Credit risk, credit risk, credit risk. Who assumes the credit risk for this $4.5 trillion dollar giveaway??

The American taxpayer. Look: The Fed has always had the ability to print as much money as it chooses. (Remember: “Unlimited QE”??) So why did the Fed need to link-up with the Treasury for this operation?

Because the Fed is unwilling to accept the credit risk. Who will ultimately be accountable for all the bad bets and worthless bonds that are being downgraded as we speak? Who is going to mop up the trillions in red ink created by crooked, scheming, cutthroat corporations (and their financial counter-party accomplices) who plundered their companies for the sole objective of enriching themselves and their shareholders?

Who?

The US Treasury backed by the American taxpayer.

This is really the endgame. Wall Street has subsumed the US Treasury and turned it into a massively leveraged hedge fund that is controlled by an unscrupulous charlatan who made his bones evicting families from their homes during the worse economic slump since the Great Depression.

We’re truly fu**ed.

NOTE– As this was being written, stocks were shooting higher for a third consecutive day due, in large part, to the easing of credit spreads in the corporate bond market. According to Matt Maley, chief market strategist at Miller Tabak, “They’ve been able to come into the credit markets and stabilize that area; we see credit spreads starting to tighten up a little bit…..The fact that they’re starting to stabilize gives people the kind of confidence they need to be able to dip their toes back into the market at a time when we absolutely need it.”

In other words, the bailout appears to be working for the investor class. Yipee.

Stunning Visualization Reveals Where Spring Break Covidiots Traveled After Flooding Florida Beaches

On Monday we reported how thousands of young Americans laughed off warnings to self-isolate and partied on Florida beaches anyway for spring break – with several now testing positive for COVID-19.

The poster child for these selfish ‘covidiots’ – who will statistically survive coronavirus – was a spring breaker from Ohio, Bradley Sluder – told CBS News: “If I get corona, I get corona. At the end of the day, I’m not gonna let it stop me from partying,” adding “We’re just out here having a good time. Whatever happens, happens.”

“If I get corona, I get corona. At the end of the day, I’m not gonna let it stop me from partying”: Spring breakers are still flocking to Miami, despite coronavirus warnings. https://t.co/KoYKI8zNDHpic.twitter.com/rfPfea1LrC

In case you were wondering how far these spring break ‘covidiots’ traveled for their ill-advised debauchery data visualization company Tectonixused cell phone location data collected by company X-Mode to map out the travels of thousands of spring breakers, using special geo-spatial big-data analysis software.

The data – provided by cell phone companies in near real-time, was anonymized.

Watch:

This shows the location data of phones that were on a Florida beach during Spring Break. It then shows where those phones traveled.

First thing you should note is the importance of social distancing. The second is how much data your phone gives off. pic.twitter.com/iokUX3qjeB

This kind of data is obviously incredibly useful and has a wide-range of applications. But while the data used is “anonymized,” meaning it is not linked to the phone’s owner, researchers have found that it is incredibly easy to link the two. https://t.co/UmMej1ZKui

This Netflix documentary might have been custom made for people trapped in a plague lockdown with nothing but too much time on their hands. Although it follows real people engaged in real things they really did, Tiger King: Murder, Mayhem and Madness has the feeling of an alien artifact that just came screaming in from some faraway star cluster. There’s nothing in it—not the bad clothes, the bad haircuts, the lamentable life choices—that suggests an origin here on Earth. Or maybe I just need to get out more.

The story is set in the world of exotic-animal fanciers—the hinterland entrepreneurs who run private zoos in states like Oklahoma, Florida and South Carolina, and the family trade that flocks to them to have pictures taken with cuddly tiger cubs. There are specialists on this circuit—people devoted to camels, bears, bobcats and 20-foot pythons—but the main attraction is tigers. (We’re told that there are more of these endangered beasts living in captivity in this country than there are living in the wild throughout the rest of the world.)

The main attraction of this five-hour series—which is not some sort of do-goody nature doc—is an Oklahoma zoo owner named Joe Schreibvogel, who goes by the name “Joe Exotic,” and happily describes himself as a “gay, gun-carrying redneck with a mullet.” Look at this guy: the black-leather pants, the pistol on his hip, the rhinestone handcuffs on his belt, the earrings, the eyeliner, and, yes, the mullet, which is naturally dyed platinum. Joe describes his private zoo, which is located in rural Wynnewood, Oklahoma, as the “World’s Largest Big Cat Park.” But he has his eye on other prizes, as well. He has a studio on his property in which he records songs for his self-released albums (I’ve heard worse) and he also tapes a wildly eccentric Internet video program. His showbiz style combines the la-di-da cadences of Chris Guest’s Corky St. Clair in Waiting for Guffman and the cramped smirk deployed by Mike Myers in the Austin Powers movies. If Joe didn’t exist, no writer would dare to invent him.

Despite his unflagging air of manic exuberance, Joe has a problem. Her name is Carole Baskin, and she’s one of those PETA people who hates the idea of wild animals being forced to live in cages. So she hates Joe Exotic, and has devoted considerable time to bad-mouthing his cat park and harassing his porta-tiger roadshows. “I consider that bitch to be one of the biggest terrorists in the exotic-animal world right now,” Joe says.

Carole, who has an animal operation of her own (all rescues, she claims), can afford to make Joe’s life a living hell because, he says, she’s a multi-millionaire. This is where Tiger King gets really interesting. According to Joe, and to several other people from whom we hear, Carole inherited all her money from her wealthy second husband, Don, who went missing some years ago and has never been found. (Police remain suspicious and the case is still open.) Carole’s behavior at the time of Don’s disappearance was certainly odd, and rumors abound, the most colorful one being that Carole fed her dead hub to her tigers. Joe has improved on this story with his suggestion that Carole actually fed Don’s dissected body into a meat grinder. (Carole allows that she does own a meat grinder, but that it’s quite small.)

As Carole makes Joe’s life increasingly difficult, he becomes obsessed with her. “She was my number-one murdered-her-husband-and-fed-him-to-the-tigers crazy bitch,” he says. He mused about flying a helicopter over her animal park and dropping grenades on it. And in one installment of his Internet show, we see him taking aim at a blow-up sex doll that’s been rigged to look like Carole and then shooting it in the head. Lawsuits were inevitable and extensive.

Through all of this hoopla, we also get to make the acquaintance of some of Joe’s fellow zoo enthusiasts. One of these, a man who calls himself Bhagavan “Doc” Antle, is a ponytailed collector of young women, whom he enjoys dressing in sexy cat-centric party outfits. One woman says that Antle is a doctor of “mystical science”; another reports that he pressured her to get breast implants (which she did). There’s also a Las Vegas character named Jeff Lowe, a proud swinger whom we see with his very pregnant wife poring over some photos of potential nannies—searching for one who’ll be hot enough for Jeff’s continuing carnal needs. Then there’s Mario Tabraue, a major-league drug dealer (retired) who believes he may have been the model for Tony Montana in Scarface. Is there room here to note that Joe Exotic has two husbands, and a third on the way?

Made over a period of five years by directors Rebecca Chaiklin and Eric Goode, Tiger King bears unsurprising similarities to Errol Morris’s The Thin Blue Line (wisps of dreamtime pacing and a few unnecessary recreated scenes). The material—the wild characters and their insane machinations – is all that any connoisseur of weird Americana could want. Unfortunately, it becomes a bit of a slog as the end heaves into view——these are basically stupid, cruddy people, and having made their acquaintance, you may, after the third or fourth hour, find yourself growing eager to unmake it.

from Latest – Reason.com https://ift.tt/3bybiVx

via IFTTT

This Netflix documentary might have been custom made for people trapped in a plague lockdown with nothing but too much time on their hands. Although it follows real people engaged in real things they really did, Tiger King: Murder, Mayhem and Madness has the feeling of an alien artifact that just came screaming in from some faraway star cluster. There’s nothing in it—not the bad clothes, the bad haircuts, the lamentable life choices—that suggests an origin here on Earth. Or maybe I just need to get out more.

The story is set in the world of exotic-animal fanciers—the hinterland entrepreneurs who run private zoos in states like Oklahoma, Florida and South Carolina, and the family trade that flocks to them to have pictures taken with cuddly tiger cubs. There are specialists on this circuit—people devoted to camels, bears, bobcats and 20-foot pythons—but the main attraction is tigers. (We’re told that there are more of these endangered beasts living in captivity in this country than there are living in the wild throughout the rest of the world.)

The main attraction of this five-hour series—which is not some sort of do-goody nature doc—is an Oklahoma zoo owner named Joe Schreibvogel, who goes by the name “Joe Exotic,” and happily describes himself as a “gay, gun-carrying redneck with a mullet.” Look at this guy: the black-leather pants, the pistol on his hip, the rhinestone handcuffs on his belt, the earrings, the eyeliner, and, yes, the mullet, which is naturally dyed platinum. Joe describes his private zoo, which is located in rural Wynnewood, Oklahoma, as the “World’s Largest Big Cat Park.” But he has his eye on other prizes, as well. He has a studio on his property in which he records songs for his self-released albums (I’ve heard worse) and he also tapes a wildly eccentric Internet video program. His showbiz style combines the la-di-da cadences of Chris Guest’s Corky St. Clair in Waiting for Guffman and the cramped smirk deployed by Mike Myers in the Austin Powers movies. If Joe didn’t exist, no writer would dare to invent him.

Despite his unflagging air of manic exuberance, Joe has a problem. Her name is Carole Baskin, and she’s one of those PETA people who hates the idea of wild animals being forced to live in cages. So she hates Joe Exotic, and has devoted considerable time to bad-mouthing his cat park and harassing his porta-tiger roadshows. “I consider that bitch to be one of the biggest terrorists in the exotic-animal world right now,” Joe says.

Carole, who has an animal operation of her own (all rescues, she claims), can afford to make Joe’s life a living hell because, he says, she’s a multi-millionaire. This is where Tiger King gets really interesting. According to Joe, and to several other people from whom we hear, Carole inherited all her money from her wealthy second husband, Don, who went missing some years ago and has never been found. (Police remain suspicious and the case is still open.) Carole’s behavior at the time of Don’s disappearance was certainly odd, and rumors abound, the most colorful one being that Carole fed her dead hub to her tigers. Joe has improved on this story with his suggestion that Carole actually fed Don’s dissected body into a meat grinder. (Carole allows that she does own a meat grinder, but that it’s quite small.)

As Carole makes Joe’s life increasingly difficult, he becomes obsessed with her. “She was my number-one murdered-her-husband-and-fed-him-to-the-tigers crazy bitch,” he says. He mused about flying a helicopter over her animal park and dropping grenades on it. And in one installment of his Internet show, we see him taking aim at a blow-up sex doll that’s been rigged to look like Carole and then shooting it in the head. Lawsuits were inevitable and extensive.

Through all of this hoopla, we also get to make the acquaintance of some of Joe’s fellow zoo enthusiasts. One of these, a man who calls himself Bhagavan “Doc” Antle, is a ponytailed collector of young women, whom he enjoys dressing in sexy cat-centric party outfits. One woman says that Antle is a doctor of “mystical science”; another reports that he pressured her to get breast implants (which she did). There’s also a Las Vegas character named Jeff Lowe, a proud swinger whom we see with his very pregnant wife poring over some photos of potential nannies—searching for one who’ll be hot enough for Jeff’s continuing carnal needs. Then there’s Mario Tabraue, a major-league drug dealer (retired) who believes he may have been the model for Tony Montana in Scarface. Is there room here to note that Joe Exotic has two husbands, and a third on the way?

Made over a period of five years by directors Rebecca Chaiklin and Eric Goode, Tiger King bears unsurprising similarities to Errol Morris’s The Thin Blue Line (wisps of dreamtime pacing and a few unnecessary recreated scenes). The material—the wild characters and their insane machinations – is all that any connoisseur of weird Americana could want. Unfortunately, it becomes a bit of a slog as the end heaves into view——these are basically stupid, cruddy people, and having made their acquaintance, you may, after the third or fourth hour, find yourself growing eager to unmake it.

from Latest – Reason.com https://ift.tt/3bybiVx

via IFTTT

House Prepares Vote On $2 Trillion Stimulus Bill As US Death Toll From COVID-19 Passes 1,300: Live Updates

Just a few short days ago, the Dow was still trading below 20k, Italy still had a higher COVID-19 case count than the US and New York City hospitals still had a few available beds. Just a few days later, everything has changed. US stocks have rallied back, erasing roughly half of their losses since they dropped from record highs, and New York has cemented its position as the worst outbreak in the country, as the virus spread widely during the month of February, when US officials were still sitting on their hands.

Though one Republican Congressman from Kentucky is threatening to delay a vote until the weekend by throwing up another procedural hurdle, by all accounts, the House is preparing to vote on Friday on a $2 trillion stimulus package that will dole out money to out-of-work Americans. At the same time, President Trump has continued to press for parts of the country to “re-open” in the coming days.

According to Johns Hopkins data, the global case total has passed 537,000, while the US reported nearly 86k as of Friday morning after the size of the US outbreak surpassed China’s. For the last two weeks, China has reported either no new domestic infections, or just one or two domestic infections. Earlier this week, China shut its borders to foreigners to try and prevent a second wave of the outbreak. China’s travel ban affecting all non-resident foreigners is set to begin at midnight local time, or in roughly six hours.

For 2 weeks, #China reports new #coronavirus cases infected locally as zero or single digits. Health authority says 1 such case in Zhejiang, 54 cases traveled from abroad. https://t.co/26FC6usMOK (Concerns high of 2nd wave from overseas & if asymptomatic cases properly reported.)

The global death total was nearing 26K as of Friday morning, with more than 1,300 deaths counted across the US. According to an ABC News/Washington Post poll 77% of Americans said their lives had been disrupted by the outbreak, while 41% said that somebody in their own community had been impacted, and one in ten Americans claim to personally know somebody who has been infected. Still, Italy’s death toll, at roughly 8,200, remains by far the highest in the world. Iran’s official death toll, thought to be only a fraction of the real number, is still only ~2,300, after announcing another 144 new deaths Friday morning.

Africa has seen the virus spread far more slowly than many health officials feared, but as of Friday, COVID-19 had been detected in nearly every country on the continent.

South Africa started its official lockdown as of midnight on Friday: the shutdown will impact roughly 57 million citizens in the country. The country, which boasts the largest economy in Africa, reported its first 2 deaths on Friday as well.

Hong Kong reported 65 new coronavirus infections on Friday, its largest daily increase yet, bringing its total confirmed cases to 518, with 41 of the new cases being ‘travel-related’. It’s the latest disappointing news as the China-ruled city hopes to prevent a travel-related resurgence. In Singapore, which has also seen a jump in travel-related cases, intentionally standing or sitting too close to someone has been made a crime punishable by up to six months in jail or a fine of nearly $7,000.

Russia reported 196 new cases of coronavirus, a daily record, taking its official total for those infected with the disease to 1,036. the country reported another death over the last 24 hours, bringing its total to 4. A lockdown that had been imposed on Moscow earlier this week has now been expanded to cover the entire country. Russia’s Interfax news agency cited Prime Minister Mikhail Mishustin as asking all Russians to avoid all “non-essential” trips, and to avoid leaving their homes.

As Israel – which has reported roughly 3k cases and 10 deaths – scrambles to stave off an outbreak, the country has deployed about 500 army soldiers to assist police in enforcing the lockdown.

To reduce the number of social contacts, Hungary is joining the ‘lockdown’ club, imposing restrictions on citizens leaving their homes between March 28 and April 11, PM Viktor Orban said he will present a plan of action to restart the economy in the first half of April.

In North Korea, the government said late Thursday that about 2,280 citizens and two foreigners remain under coronavirus quarantine after authorities released thousands of people in past weeks who were confirmed to have no symptoms.

Chinese President Xi Jinping and President Trump participated in a call Thursday evening where they agreed to “unite to fight” the coronavirus, according to Chinese state media. Xi told Trump China “wishes to continue sharing all information and experience with the US” according to state broadcaster CCTV, while Trump tweeted that the two leaders were “working closely together”.

Just finished a very good conversation with President Xi of China. Discussed in great detail the CoronaVirus that is ravaging large parts of our Planet. China has been through much & has developed a strong understanding of the Virus. We are working closely together. Much respect!

Finally, Spain reported 769 deaths on Friday, its largest daily jump in deaths since the beginning of the outbreak. The country also reported 7,871 new cases, with the total climbing to 64,059.

Meanwhile, as US hospitals prepare to face an onslaught of new severe cases and deaths, many while also dealing with shortages of critical equipment like ventilators, as well as personal protective equipment, a Detroit area health system has developed a contingency plan to deny ventilators and intensive care treatment to coronavirus patients with a poor chance of surviving, according to the Washington Post.

In a rare piece of good news, the suburban Washington State hospital that handled the first onslaught of coronavirus patients weeks ago – a crush of seriously ill and dying nursing home residents that signaled the beginning of the national crisis in the US – is now cautiously optimistic that local officials have succeeded in “flattening the curve”, as the number of new cases has finally tapered off.

Monarchy is a soulless institution that stamps out all individuality, and its effects can be harshest on those at the top of the pyramid. That is the major ironic takeaway of the third season of Netflix’s The Crown, which continues its look at the modern British Royal Family, now in the turbulent 1960s and ’70s.

The characters are older, as are the new actors playing them, aged by both time and the demands of their roles. With that age has come a palpable sense of regret for Queen Elizabeth II and her husband, Prince Phillip. Sequential episodes in the middle of the season show the two grappling with the fact that conformity to the needs of “the Crown” has prevented them from spending their lives the way they’d have preferred (and perhaps with whom they would have preferred): Philip as a naval officer and Elizabeth as a horse breeder.

Barreling headlong into that same fate is their son, Prince Charles, whose attempts to bring his own personality to bear as heir to the throne are either dismissed or actively crushed by his family. The struggle from earlier seasons between the Crown and the people who wear it is over: The Crown won.

from Latest – Reason.com https://ift.tt/33QBjgb

via IFTTT