Can governments refuse to use religious foster and adoption agencies that won’t place children with same-sex couples? The issue will soon come before the Supreme Court.

This morning the Supreme Court announced that it would hear Fulton v. City of Philadelphia. The case centers around how Philadelphia applies its antidiscrimination policies to Catholic Social Services (CSS), with whom the city contracts for a number of child welfare programs. CSS objects to same-sex marriages for religious reasons and declines to put children with such couples.

This puts it at odds with Philadelphia’s antidiscrimination ordinances, and so the city stopped referring children to the group for foster care placement. CSS and some foster parents it represents filed suit in 2018, arguing that the group is exercising its religious rights by declining to accept gay couples as caretakers. They want their contract reinstated.

The city resisted, arguing that religious exemptions don’t apply here because the antidiscrimination laws are being neutrally enforced and aren’t based on any sort of anti-Catholic animosity. So far the courts have agreed with the city.

Conflicts like this are playing out in several cities and states across the country. Some places, such as Philadelphia, are refusing to let adoption or foster care agencies discriminate against gay couples. But some states, such as Tennessee and Michigan, have passed laws to let private agencies turn away potential parents whose religious beliefs don’t match theirs (not just on same-sex issues).

The most important Supreme Court precedent here may be 1990’s Employment Division v. Smith. That case, about two men fired from their jobs and denied unemployment for using peyote, held that people can’t use their freedom of religious expression to demand exemption from neutrally applied laws that satisfy a “compelling government interest.” (Traditional libertarian disclaimer: In a libertarian universe, stopping people from taking hallucinogenic mushrooms would fail the “compelling government interest” test. But that’s not the current universe.)

This Supreme Court challenge explicitly argues that the Employment Division v. Smith precedent should be revisited. If there’s a remote chance of that happening, we’ll see a lot of public worrying about whether the conservatives of the Supreme Court will enshrine what folks like the American Civil Liberties Union call a “license to discriminate.”

I’m skeptical that the court would rule that broadly, but we’ll see. When the Supreme Court addressed whether a Colorado bakery could refuse to provide a wedding cake for a same-sex couple in Masterpiece Cakeshop v. Colorado Civil Rights Commission, the court elegantly sidestepped the thorny central question of when exemptions should be allowed by determining that Colorado was not neutrally applying its antidiscrimination laws and that there was clear evidence of anti-religious bias in how the bakery was treated.

Philadelphia insists that that’s not the case here. The city notes in its brief to the Supreme Court that it is continuing to contract with CSS in other areas. Thus, it’s only keeping the group from participating in the foster care program and only because it is violating the city’s antidiscrimination rules.

The justices could simply rule that Philadelphia is indeed neutrally applying the lawt. If that’s all they do, they won’t overturn the laws passed in those other states that do offer exemptions to agencies that don’t want to place kids with same-sex couples.

For a useful libertarian perspective on this conflict, I recommend Walter Olson, a Cato Institute senior fellow, Reasoncontributor, and gay man in a same-sex relationship who has adopted a son. Taking a broad view, Olson notes that children and adults in the adoption and foster care system benefit when there is a wide “marketplace” where qualifying agencies aren’t shut out of the system when it’s not necessary. If the goal is to help connect more children with families to care for them, shutting out religious agencies doesn’t necessary help achieve that goal, even if those agencies are discriminating. What matters is the existence of meaningful alternative options; there are downsides when religious groups are denied participation, and downsides when religious organizations are the only choices in an area. Olson offers his argument here. SCOTUSblog has a page devoted to Fulton v. City of Philadelphia here.

from Latest – Reason.com https://ift.tt/397vRHe

via IFTTT

As the global coronavirus (COVID-19) case toll rises, what can Chinese refinery activity reveal about the state of oil demand? S&P Global Platts editors examine this and other energy and commodity market trends, including Asian bunker sales, Americas corn exports and more.

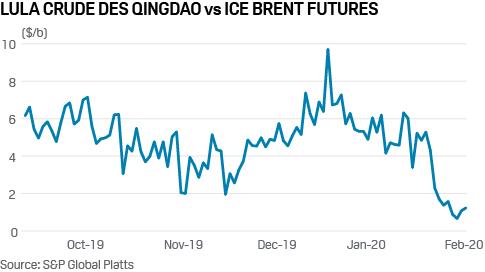

1. China, crude and COVID-19: are low prices the best cure for low prices?

What’s happening? The COVID-19 outbreak and resulting economic slowdown has seen refineries slash their run rates, impacting demand for refining feedstocks. This has seen a collapse in the price of crudes sold delivered ex-ship to ports in China. The premium for Lula, a Brazilian crude popular with independent refiners, DES Qingdao over ICE Brent fell to a low of just 66 cents/barrel last week, down from an average of just under $6 a barrel throughout January.

What’s next? Low crude prices are encouraging China’s independent refineries to return to the international market for April and May delivery, reflected in the slight rise in the Lula premium to ICE Brent at the end of last week. But short term buying aside, longer term the demand outlook remains uncertain. Look for a sustained rise in the premium of Lula over ICE Brent as evidence that the economy is at last getting back on it feet.

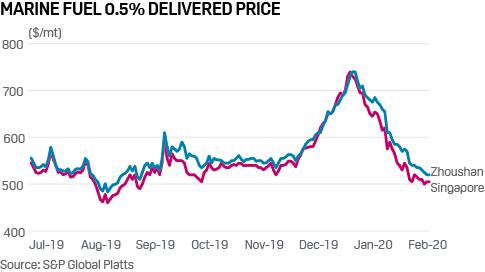

2. Singapore’s competitive edge in bunkering challenged by Chinese ports

What’s happening? China’s refineries have increasingly geared up to produce low sulfur fuel oil as demand for cleaner fuels has surged due to the International Maritime Organization’s global sulfur limit for marine fuels. In addition, China’s tax waiver on bonded bunker fuel effective February 1 is also set to boost the country’s bunkering prospects. China typically imports about 1 million mt/month of bunker fuel, with the bulk of this from Singapore. The full 13% value added tax rebate for ships using fuel oil as bunker fuel should attract ships on international routes to refuel at Chinese ports, while paving the way for domestic producers to boost bunker fuel output and reduce Chinese imports from Singapore.

What’s next? Singapore’s position as the world’s top bunkering port could be threatened in the new low sulfur emissions world. At the moment, Singapore’s bunker fuel prices are the lowest in the region. With both China poised to contribute substantially to the availability of low sulfur marine fuel in Asia, bunker fuel prices in the region and especially at China’s Zhoushan port, will become extremely competitive.

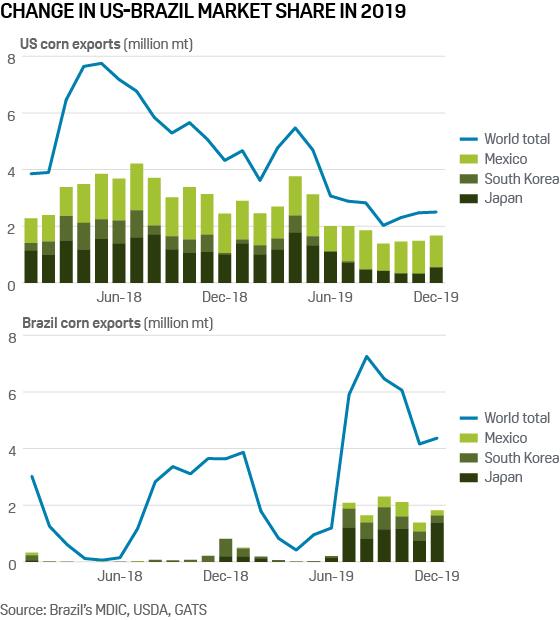

3. US corn has narrow window in export race against South America

What’s happening? Historically the world’s largest corn exporter — the US, lost its market share in the top importing countries of the coarse grain, Mexico, South Korea and Japan. Meanwhile, Brazil has gained a bigger chunk of the market share in these three countries. Brazil harvested a record corn crop last year, and the ample supplies from that crop were available throughout the year at cheaper prices. After June 2019, when Brazil’s corn supplies started coming in the market, exports from the country surged, while those from the US declined.

What’s next? In the current marketing year which will end in August, the US has got a very small window to push out its supplies to global markets before Argentina comes in with its supplies in March, followed by Brazil in June-July. According to the latest estimates from the US Department of Agriculture, the US is expected to export 43.82 million mt of corn in the 2019-20 marketing year, down 16.5% from 2018-19 levels. Market sources say the country will have to do exceptionally well to meet the 2019-20 target. Since its first estimates made at the start of 2019-20 season, the USDA has already made a steep cutback in US corn export projections by 11.8 million mt.

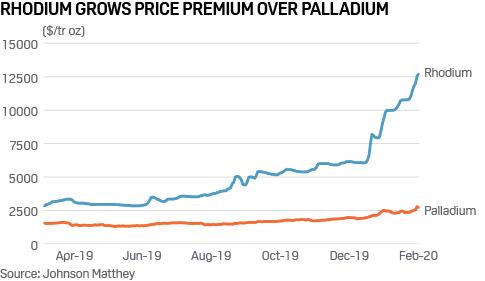

4. Rhodium’s meteoric rise fuelled by tightening emissions standards

What’s happening? Platinum group metals used in catalytic converters have seen strong demand as higher emissions standard are implemented globally, with rhodium prices soaring faster than other products in the group. Rhodium is considered the best catalyst for the reduction of nitrogen oxides to nitrogen, as well as the oxidation of CO and hydrocarbons, and is seven times more efficient than palladium or platinum. Johnson Matthey’s rhodium spot price in January surpassed the previous 2008 all-time record of $10,100/oz and edged up to $10,775/oz in the first week of February. Rhodium set another new record last Thursday, jumping 3.2% day on day, with spot price at $12,700/oz.

What’s next? Market participants see little downside to rhodium prices. Analysts have said that China is likely to buy whatever rhodium stock it can find in order to meet its China VI emissions targets, even with no global surface stocks of the precious metal available. The coronavirus outbreak could cause a slight reduction in car production over the next two or three months, however.

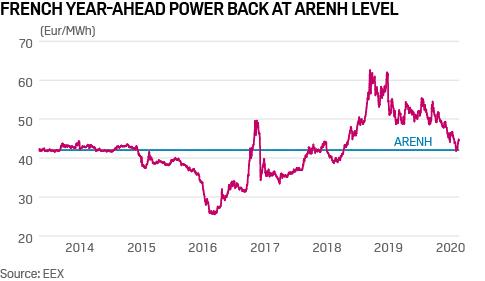

5. Eyes on regulated nuclear price in France, Europe’s top power exporter

What’s happening? French year-ahead power has fallen to the ARENH regulated price at which EDF sells 100 TWh of nuclear generation to smaller competitors. Above-average temperatures this winter have kept French electric heat demand in check, while strong wind and hydro production have created oversupply conditions across northwest Europe. Even with reduced nuclear availability, prices have continued to fall with cheap gas filling the thermal gap.

What’s next? The French government is in the process of reforming the ARENH nuclear release mechanism. A proposed cap and floor price is to cover all EDF’s nuclear output in future, with a price corridor of Eur6/MWh allowing some flexibility in the central regulated price. The measure, which requires EC approval, could be in place by 2022. Corridor or not, fixing the price for close to 400 TWh a year will fundamentally change Europe’s power markets because France is the continent’s biggest net exporter with a growing annual surplus. French Cal 2022 baseload power has rebounded above Eur47/MWh after EDF management last week said it was confident the reform could apply from January 2022.

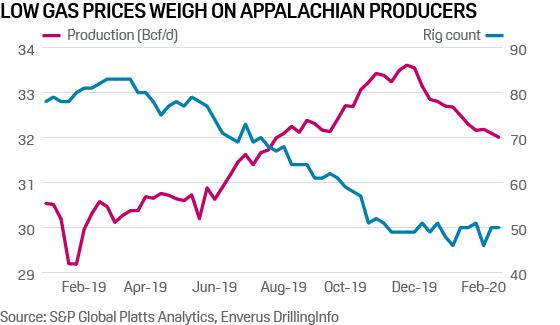

6. Appalachian Basin rig counts, production drop as gas prices slide

What’s happening? Persistently low commodity prices this year are beginning to take their toll on US dry gas producers operating in the prolific Appalachian Basin. At the region’s benchmark Dominion South hub, cash prices have averaged just $1.57/MMBtu this month and $1.61/MMBtu, year to date, S&P Global Platts data shows. On February 19, total rig count in the Marcellus and Utica shales was estimated at 50, which is hovering just above a recent 42-month low, according to Enverus DrillingInfo data. Production levels have followed rig counts lower with output this month estimated at 32.1 Bcf/d – about 1.3 Bcf/d or nearly 4% lower compared to a monthly record-high in November.

What’s next? Forwards markets aren’t holding out much hope for a meaningful recovery in Appalachian gas prices this year. On February 19, the balance-2020 forward curve at Dominion South was assessed at just $1.71/MMBtu. According to S&P Global Platts Analytics, average producer cash flows at current price valuations will likely keep production flat this year around 32 Bcf/d, resulting in year-on-year declines by the fourth quarter.

The fact that Nancy Pelosi and her fellow establishment Dems aren’t too fond of AOC and her ‘squad’ of female leftist ideologues is hardly news. And now that AOC has launched the first Democratic Socialist Super PAC (whoever thought we’d be writing such a sentence five years ago?) to back ‘progressive’ primary candidates, oftentimes against candidates backed by the DNC, including several longtime lawmakers.

With Bernie Sanders now on track to win the Democratic nomination and avert a brokered convention largely thanks to his dedicated core of fanatical supporters who believe Bernie can do no wrong, the DNC is finally being forced to confront the socialist threat on its left flank.

AOC is doing all of this to push through her nightmarish and neo-communist agenda of reforms that will ensure a much bigger government and restrictions on business that are seemingly tailor-made to tank the economy, like a federal jobs guarantee.

“It’s time to elect a progressive majority in Congress accountable to strong, grassroots movements that push support for issues like Medicare for All, a Green New Deal, racial justice, & more,” she said on Friday.

And in keeping with the left’s preference for gimmicks and fixation on identity politics, AOC is launching an “All-female slate of progressive candidates”.

It’s all evidence that AOC is trying to “leverage her influence among activists to try to reshape the Democratic Party.”

But as the world has learned in the months and years since President Trump triumphed over Hillary Clinton, the DNC has no interest in ‘changing’ the Democratic Party, and it mostly views this insurgent leftist threat as a bunch of loudmouthed clowns and soyboy leftists whose most strident quality is a pervasive sense of entitlement.

As the NY Post editorial board pointed out in an editorial in Monday’s paper, AOC is already in trouble with the leadership over her refusal to pay dues to the Dems’ fundraising arm.

It ended the review with a warning: Don’t be surprised when the party’s powerbrokers move to eliminate her seat during the redistricting that will follow the 2020 Census.

And it would certainly make for an interesting twist in AOC’s inevitable best-selling autobiography about her rise from behind the bar to Capitol Hill.

Do presidential debates have you considering likely places to stash your cash? Do political polling results have you contemplating waiting it all out in a mountain retreat? Rest assured that you’re not overreacting; you’re sensibly responding to a political culture that has turned very welcoming to authoritarian candidates and intrusive policies.

There’s a good chance that freedom in the days to come will be most available to those willing to hide from the state, break its laws, and sabotage its efforts.

Incumbent President Donald Trump has spent much of his first term catering to xenophobia. He demonizes foreigners, whether they want to come here as immigrants or just sell products to Americans. Immigration restrictions and protectionism inherently require a larger and more intrusive role for the state, leaving little room for a government that will just leave you alone. That trade and migration restrictions both inflict domestic economic damage seems largely irrelevant to his supporters, who embrace nativism as a cause in place of leaving people free to make their own way in the world.

The Democrats who hope to unseat Trump have also sidelined any talk of liberty in favor of appeals to envy and the desire for stuff paid for by somebody else. The wealth tax favored by candidates including Sens. Bernie Sanders (I-Vt.) and Elizabeth Warren (D-Mass.) is likely unconstitutional. It’s also bound to cripple economic dynamism while driving the rich—who not only have more money than you and I, but better financial advisers—to hide their cash overseas.

Many of the president’s rivals are fond of promising “free” stuff, like college. It’s a tempting offer for students groaning under debt burdens who don’t realize that earlier government attempts to make college more accessible play a big role in soaring tuition. And never mind that “free” college is going to cheapen the value of the resulting credentials putting the supposed rewards of the policy further out of reach.

Candidates of both major parties offer something else that’s likely to be expensive in the long run—an opportunity to punish rival political tribes through the force of law. Amidst lots of huffing and puffing about “deplorables” and “coastal elites,” most of the candidates get lots of mileage out of channeling the partisan rage that too many Americans feel toward their fellow countrymen. Actually, those kinds of insults are becoming quaint, since calling opponents “traitors” is the popular new way of expressing strong disagreement.

And political disagreements these days really are strong. Just over 42 percent of the people in each party view the opposition as “downright evil,” according to research published last year by Nathan P. Kalmoe and Lilliana Mason, political scientists at Louisiana State University and the University of Maryland. “Violence would be justified” if the opposing party wins the 2020 presidential election say 18 percent of the surveyed Democrats and 13 percent of Republicans.

There’s not a lot of room for live-and-let-live in satisfying the demands of supporters who want to battle “downright evil” enemies.

In this climate of political animosity, it’s no surprise that the leading candidates of the moment have lots of comfort with wielding the power of the state.

In addition to his taste for border controls and trade wars, the president has a penchant for threatening to use government against those who annoy him. Trump threatened both tax and antitrust actions against Amazon, explicitly linking his threats to criticism of his administration by The Washington Post, which shares Jeff Bezos as an owner.

Michael Bloomberg won Reason‘s ranking in 2013 as the number one enemy of freedom for his nanny-state approach to public health and personal choice, as well as “his enthusiasm for gun control, his illegal crackdown on pot smokers, and his unflagging defense of the New York Police Department’s stop-and-frisk program.”

Current Democratic frontrunner Bernie Sanders appears to have (we hope) abandoned his early support for government takeovers of businesses including utilities and the oil industry. Likewise, he’s no longer affiliated with the Trotskyite Socialist Workers Party. But his brand of “democratic socialism” apparently offers lots of wiggle room for unilateral action, including the dozens of executive orders his campaign has reportedly prepared as a means of bypassing congressional opposition to his policies if he wins the presidency.

That’s not to say that President Trump or his Democratic opponents are purely authoritarian across the board.

But these aren’t the defining issues in a campaign in which candidates rarely propose leaving people alone, and no major-party candidate has made that a central feature of his or her campaign. Instead, this has turned into an election season defined by different flavors of control freakery, competing proposals to expand government, and warnings about the awesome power of the state to squash domestic opposition.

For those of us looking not for goodies or political thuggery, but for more breathing room instead, there’s little encouragement to be found in the debates and the polls. Instead, we’ll have to look for loopholes in laws, exceptions to intrusive policies, and ways to confound tax men and inspectors. Our real votes will be for preferred encryption software, places to hide our money and information, and caches for forbidden goods. If we want to retain or expand our freedom, we’ll need to stay under the radar as we ignore the powers-that-be, or else make ourselves more trouble to push around than we’re worth.

While Trump’s Democratic opponents have spent the years since the last presidential election valorizing themselves as “the resistance,” all they have to offer is a competing brand of authoritarianism. The real resistance is made up of those who refuse to be governed by any of the wannabe rulers.

from Latest – Reason.com https://ift.tt/2Tat2Pd

via IFTTT

For years Greyhound, by far the largest operator of intercity bus service in the United States, has routinely allowed Border Patrol agents to board its buses without warrants or probable cause. During those “transportation checks,” which have become increasingly common under the Trump administration, agents interrogate passengers with brown skin or foreign accents, asking for proof that they are in the country legally. Last Friday, Greyhound announced that it would no longer tolerate such harassment of its customers, reversing a policy that was based on an unconstitutionally broad understanding of the Border Patrol’s legal authority.

Even while complaining about the impact of the bus sweeps on its customers and its operations, Greyhound had justified its policy by citing 8 USC 1357. That law says Border Patrol agents “shall have power without warrant…to board and search for aliens any vessel within the territorial waters of the United States and any railway car, aircraft, conveyance, or vehicle,” provided the search occurs “within a reasonable distance from any external boundary of the United States,” defined as a 100-mile zone that happens to include about two-thirds of the country’s population.

But as the American Civil Liberties Union pointed out, that sweeping power is inconsistent with the Fourth Amendment’s ban on unreasonable searches and seizures. In Almeida-Sanchez v. United States, a 1973 case involving a Border Patrol car search 25 miles from the Mexican border that was conducted without probable cause or consent, the Supreme Court rejected the government’s claim that the search was authorized by 8 USC 1357. “No Act of Congress can authorize a violation of the Constitution,” it noted.

The Department of Homeland Security, which includes the Border Patrol and its parent agency, Customs and Border Protection (CBP), seemed to acknowledge the implications of that decision in its regulations, saying “an immigration officer may not enter into the non-public areas of a business…unless the officer has either a warrant or the consent of the owner or other person in control of the site to be inspected.” Those “non-public areas” include Greyhound’s buses, which ordinarily are open only to employees and passengers with tickets. But that general policy was not enough to reassure Greyhound CEO David Leach, who worried that barring the Border Patrol from the company’s buses would lead to confrontations between armed agents and its drivers.

Greyhound’s reversal is based on a more specific internal CBP memo that the Associated Press recently obtained. “When transportation checks occur on a bus at non-checkpoint locations, the agent must demonstrate that he or she gained access to the bus with the consent of the company’s owner or one of the company’s employees,” Border Patrol Chief Carla Provost says in that January 28 memo.

“We welcome the clarity that this change in protocol brings, as it aligns with our previously stated position, which is that we do not consent to warrantless searches,” Greyhound said. “We are providing drivers and terminal employees with updated training regarding this policy change.” The company said it would put signs on its buses “clearly displaying our position” and send “a letter to the Department of Homeland Security formally stating we do not consent to warrantless searches on our buses and in terminal areas that are not open to the general public.”

The ACLU welcomed Greyhound’s new policy. “We are pleased to see Greyhound clearly communicate that it does not consent to racial profiling and harassment on its buses,” said Andrea Flores, deputy director of policy for the ACLU’s Equality Division. “By protecting its customers and employees, Greyhound is sending a message that it prioritizes the communities it serves. We will continue to push other transportation companies to follow its leadership.”

from Latest – Reason.com https://ift.tt/32nHEPf

via IFTTT

Do presidential debates have you considering likely places to stash your cash? Do political polling results have you contemplating waiting it all out in a mountain retreat? Rest assured that you’re not overreacting; you’re sensibly responding to a political culture that has turned very welcoming to authoritarian candidates and intrusive policies.

There’s a good chance that freedom in the days to come will be most available to those willing to hide from the state, break its laws, and sabotage its efforts.

Incumbent President Donald Trump has spent much of his first term catering to xenophobia. He demonizes foreigners, whether they want to come here as immigrants or just sell products to Americans. Immigration restrictions and protectionism inherently require a larger and more intrusive role for the state, leaving little room for a government that will just leave you alone. That trade and migration restrictions both inflict domestic economic damage seems largely irrelevant to his supporters, who embrace nativism as a cause in place of leaving people free to make their own way in the world.

The Democrats who hope to unseat Trump have also sidelined any talk of liberty in favor of appeals to envy and the desire for stuff paid for by somebody else. The wealth tax favored by candidates including Sens. Bernie Sanders (I-Vt.) and Elizabeth Warren (D-Mass.) is likely unconstitutional. It’s also bound to cripple economic dynamism while driving the rich—who not only have more money than you and I, but better financial advisers—to hide their cash overseas.

Many of the president’s rivals are fond of promising “free” stuff, like college. It’s a tempting offer for students groaning under debt burdens who don’t realize that earlier government attempts to make college more accessible play a big role in soaring tuition. And never mind that “free” college is going to cheapen the value of the resulting credentials putting the supposed rewards of the policy further out of reach.

Candidates of both major parties offer something else that’s likely to be expensive in the long run—an opportunity to punish rival political tribes through the force of law. Amidst lots of huffing and puffing about “deplorables” and “coastal elites,” most of the candidates get lots of mileage out of channeling the partisan rage that too many Americans feel toward their fellow countrymen. Actually, those kinds of insults are becoming quaint, since calling opponents “traitors” is the popular new way of expressing strong disagreement.

And political disagreements these days really are strong. Just over 42 percent of the people in each party view the opposition as “downright evil,” according to research published last year by Nathan P. Kalmoe and Lilliana Mason, political scientists at Louisiana State University and the University of Maryland. “Violence would be justified” if the opposing party wins the 2020 presidential election say 18 percent of the surveyed Democrats and 13 percent of Republicans.

There’s not a lot of room for live-and-let-live in satisfying the demands of supporters who want to battle “downright evil” enemies.

In this climate of political animosity, it’s no surprise that the leading candidates of the moment have lots of comfort with wielding the power of the state.

In addition to his taste for border controls and trade wars, the president has a penchant for threatening to use government against those who annoy him. Trump threatened both tax and antitrust actions against Amazon, explicitly linking his threats to criticism of his administration by The Washington Post, which shares Jeff Bezos as an owner.

Michael Bloomberg won Reason‘s ranking in 2013 as the number one enemy of freedom for his nanny-state approach to public health and personal choice, as well as “his enthusiasm for gun control, his illegal crackdown on pot smokers, and his unflagging defense of the New York Police Department’s stop-and-frisk program.”

Current Democratic frontrunner Bernie Sanders appears to have (we hope) abandoned his early support for government takeovers of businesses including utilities and the oil industry. Likewise, he’s no longer affiliated with the Trotskyite Socialist Workers Party. But his brand of “democratic socialism” apparently offers lots of wiggle room for unilateral action, including the dozens of executive orders his campaign has reportedly prepared as a means of bypassing congressional opposition to his policies if he wins the presidency.

That’s not to say that President Trump or his Democratic opponents are purely authoritarian across the board.

But these aren’t the defining issues in a campaign in which candidates rarely propose leaving people alone, and no major-party candidate has made that a central feature of his or her campaign. Instead, this has turned into an election season defined by different flavors of control freakery, competing proposals to expand government, and warnings about the awesome power of the state to squash domestic opposition.

For those of us looking not for goodies or political thuggery, but for more breathing room instead, there’s little encouragement to be found in the debates and the polls. Instead, we’ll have to look for loopholes in laws, exceptions to intrusive policies, and ways to confound tax men and inspectors. Our real votes will be for preferred encryption software, places to hide our money and information, and caches for forbidden goods. If we want to retain or expand our freedom, we’ll need to stay under the radar as we ignore the powers-that-be, or else make ourselves more trouble to push around than we’re worth.

While Trump’s Democratic opponents have spent the years since the last presidential election valorizing themselves as “the resistance,” all they have to offer is a competing brand of authoritarianism. The real resistance is made up of those who refuse to be governed by any of the wannabe rulers.

from Latest – Reason.com https://ift.tt/2Tat2Pd

via IFTTT

For years Greyhound, by far the largest operator of intercity bus service in the United States, has routinely allowed Border Patrol agents to board its buses without warrants or probable cause. During those “transportation checks,” which have become increasingly common under the Trump administration, agents interrogate passengers with brown skin or foreign accents, asking for proof that they are in the country legally. Last Friday, Greyhound announced that it would no longer tolerate such harassment of its customers, reversing a policy that was based on an unconstitutionally broad understanding of the Border Patrol’s legal authority.

Even while complaining about the impact of the bus sweeps on its customers and its operations, Greyhound had justified its policy by citing 8 USC 1357. That law says Border Patrol agents “shall have power without warrant…to board and search for aliens any vessel within the territorial waters of the United States and any railway car, aircraft, conveyance, or vehicle,” provided the search occurs “within a reasonable distance from any external boundary of the United States,” defined as a 100-mile zone that happens to include about two-thirds of the country’s population.

But as the American Civil Liberties Union pointed out, that sweeping power is inconsistent with the Fourth Amendment’s ban on unreasonable searches and seizures. In Almeida-Sanchez v. United States, a 1973 case involving a Border Patrol car search 25 miles from the Mexican border that was conducted without probable cause or consent, the Supreme Court rejected the government’s claim that the search was authorized by 8 USC 1357. “No Act of Congress can authorize a violation of the Constitution,” it noted.

The Department of Homeland Security, which includes the Border Patrol and its parent agency, Customs and Border Protection (CBP), seemed to acknowledge the implications of that decision in its regulations, saying “an immigration officer may not enter into the non-public areas of a business…unless the officer has either a warrant or the consent of the owner or other person in control of the site to be inspected.” Those “non-public areas” include Greyhound’s buses, which ordinarily are open only to employees and passengers with tickets. But that general policy was not enough to reassure Greyhound CEO David Leach, who worried that barring the Border Patrol from the company’s buses would lead to confrontations between armed agents and its drivers.

Greyhound’s reversal is based on a more specific internal CBP memo that the Associated Press recently obtained. “When transportation checks occur on a bus at non-checkpoint locations, the agent must demonstrate that he or she gained access to the bus with the consent of the company’s owner or one of the company’s employees,” Border Patrol Chief Carla Provost says in that January 28 memo.

“We welcome the clarity that this change in protocol brings, as it aligns with our previously stated position, which is that we do not consent to warrantless searches,” Greyhound said. “We are providing drivers and terminal employees with updated training regarding this policy change.” The company said it would put signs on its buses “clearly displaying our position” and send “a letter to the Department of Homeland Security formally stating we do not consent to warrantless searches on our buses and in terminal areas that are not open to the general public.”

The ACLU welcomed Greyhound’s new policy. “We are pleased to see Greyhound clearly communicate that it does not consent to racial profiling and harassment on its buses,” said Andrea Flores, deputy director of policy for the ACLU’s Equality Division. “By protecting its customers and employees, Greyhound is sending a message that it prioritizes the communities it serves. We will continue to push other transportation companies to follow its leadership.”

from Latest – Reason.com https://ift.tt/32nHEPf

via IFTTT

China Cancels Top Political Meeting As Virus Crisis Worsens

China announced Monday it had canceled the biggest political event of the year, the National People’s Congress (NPC), slated for March 5, as the Covid-19 outbreak continues to worsen, reported The Washington Post.

The cancellation suggests the virus outbreak continues to worsen with more than 77,000 confirmed cases and nearly 2,500 deaths across mainland China. As we’ve explained before, the real numbers are much higher.

China is attempting to reboot its economy as production shutdowns have crashed economic output. The most significant problem with rebooting the economy is that the virus must be completely eradicated first; otherwise, it will continue to spread across towns and factories – forcing even longer shutdowns and prolonging the crisis. This is China’s Catch-22, where in the past, it could lie itself out of almost every problem, now the more lying it does, the worse the situation gets.

China’s top leader, Xi Jinping, told officials at a Communist Party meeting on Sunday that the virus outbreak is a “big test” for the country, and policy adjustments would cushion the economy for a downturn. Xi acknowledged “obvious shortcomings in response to the epidemic,” warning that short-term financial stress could be imminent.

We’ve noted on several occasions that China’s economy remains paralyzed.

Xi said the “the epidemic situation is still severe and complex, and prevention and control work is in the most difficult and critical stage.”

The NPC and its chief advisory body usually begin on March 5 will be pushed out this year – this all suggests conditions in China will remain severe and highlights that Beijing is having a difficult time in controlling the “contained” narrative.

China backtracked on an earlier announcement that would ease travel restrictions on Wuhan, suggesting, once again, the virus outbreak is far from contained.

As we’ve noted, China revised the definition of what a confirmed case is to ease public fears about a runaway pandemic and get more people back to work. But explained above, its Catch 22 situation, as fake data for optically pleasing headlines of a crisis abating, will do more harm than good.

This is the first time the Chinese have postponed the NPC since 1995. China’s economy will likely remain in economic paralysis through March.

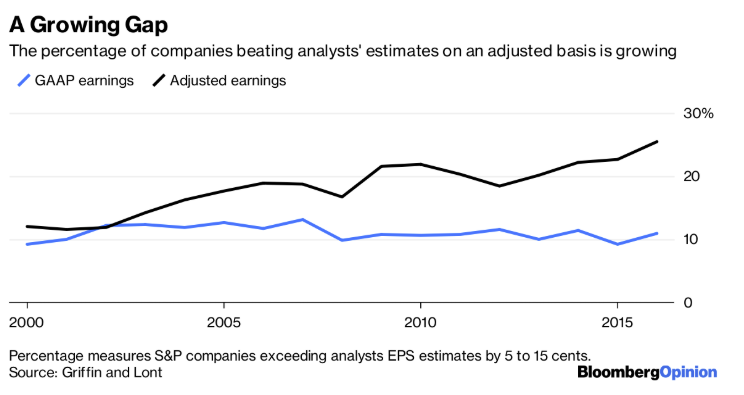

Just like the hit series “House Of Cards,” Wall Street earnings season has become rife with manipulation, deceit and obfuscation that could rival the dark corners of Washington, D.C.

What is most fascinating is that so many individuals invest hard earned capital based on these manipulated numbers. The failure to understand the “quality” of earnings, rather than the “quantity,” has always led to disappointing outcomes at some point in the future.

“Non-GAAP financials are not audited and are most often disclosed through earnings press releases and investor presentations, rather than in the company’s annual report filed with the Securities and Exchange Commission.

Once upon a time, non-GAAP financials were used to isolate the impact of significant one-time events like a major restructuring or sizable acquisition. In recent years, they have become increasingly prevalent and prominent, used by both the shiniest new-economy IPO companies and the old-economy stalwarts.”

Back in the 80’s and early 90’s companies used to report GAAP earnings in their quarterly releases. If an investor dug through the report they would find “adjusted” and “proforma” earnings buried in the back.

Today, it is GAAP earnings which are buried in the back hoping investors will miss the ugly truth.

These “adjusted or Pro-forma earnings” exclude items that a company deems “special, one-time or extraordinary.” The problem is that these “special, one-time” items appear “every” quarter leaving investors with a muddier picture of what companies are really making.

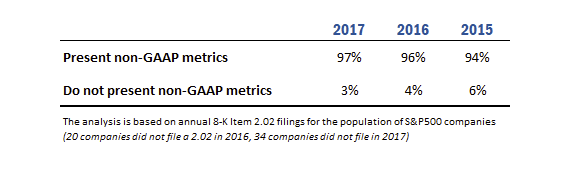

An in-depth study by Audit Analytics revealed that 97% of companies in the S&P 500 used non-GAAP financials in 2017, up from 59% in 1996, while the average number of different non-GAAP metrics used per filing rose from 2.35 to 7.45 over two decades.

This growing divergence between the earnings calculated according to accepted accounting principles, and the “earnings” touted in press releases and analyst research reports, has put investors at a disadvantage of understanding exactly what they are paying for.

As BofAML stated:

“We are increasingly concerned with the number of companies (non-commodity) reporting earnings on an adjusted basis versus those that are stressing GAAP accounting, and find the divergence a consequence of less earnings power.

Consider that when US GDP growth was averaging 3% (the 5 quarters September 2013 through September 2014) on average 80% of US HY companies reported earnings on an adjusted basis. Since September 2014, however, with US GDP averaging just 1.9%, over 87% of companies have reported on an adjusted basis. Perhaps even more telling, between the end of 2010 and 2013, the percentage of companies reporting adjusted EBITDA was relatively constant, and since 2013, the number has been on a steady rise.

So, why do companies regularly report these Non-GAAP earnings? Drew has the answer:

“When management is asked why they resort to non-GAAP reporting, the most common response is that these measures are requested by the analysts and are commonly used in earnings models employed to value the company. Indeed, sell-side analysts and funds with a long position in the stock may have incentives to encourage a more favorable alternative presentation of earnings results.”

If non-GAAP reporting is used as a supplemental means to help investors identify underlying trends in the business, one might reasonably expect that both favorable and unfavorable events would be “adjusted” in equal measure.

Why has there been such a rise is Non-GAAP reporting?

Money, of course.

“A recent study from MIT has found that when companies make large positive adjustments to non-GAAP earnings, their CEOs make 23 percent more than their expected annual compensation would be if GAAP numbers were used. This is despite such firms having weak contemporaneous and future operating performance relative to other firms.” –Financial Executives International.

The researchers at MIT combed through the annual earnings press releases of S&P 500 firms for fiscal years 2010 through 2015 and recorded GAAP net income and non-GAAP net income when the firms disclosed it. About 67 percent of the firms in the sample disclose non-GAAP net income.

The researchers then obtained CEO compensation, accounting, and return data for the sample firms and found that “firms making the largest positive non-GAAP adjustments… exhibit the worst GAAP performance.”

The CEOs of these firms, meanwhile, earned about 23 percent more than would be predicted using a compensation model; in terms of raw dollars. In other words, they made about $2.7 million more than the approximately $12 million of an average CEO.

It should not be surprising that anytime you compensate individuals based on some level of performance, they are going to figure out ways to improve performance, legal or not. Examples run rampant through sports from Barry Bonds to Lance Armstrong, as well as in business from Enron to WorldCom.

“One out of five [20%] U.S. finance chiefs have been scrambling to fiddle with their companies’ earnings.”

This rather “open secret” of companies manipulating bottom line earnings by utilizing “cookie-jar” reserves, heavy use of accruals, and other accounting instruments to flatter earnings is not new.

“The tricks are well-known: A difficult quarter can be made easier by releasing reserves set aside for a rainy day or recognizing revenues before sales are made, while a good quarter is often the time to hide a big ‘restructuring charge’ that would otherwise stand out like a sore thumb.

What is more surprising though is CFOs’ belief that these practices leave a significant mark on companies’ reported profits and losses. When asked about the magnitude of the earnings misrepresentation, the study’s respondents said it was around 10% of earnings per share.“

Manipulating earnings may work in the short-term, eventually, cost cutting, wage suppression, earnings adjustments, share-buybacks, etc. reach an effective limit. When that limit is reached, companies can no longer hide the weakness in their actual operating revenues.

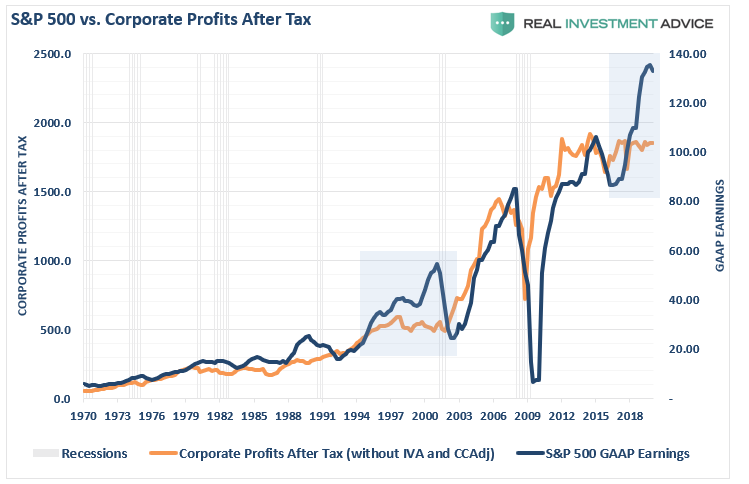

There’s a big difference between companies’ advertised performance, and how they actually did. We discussed this recently by looking at the growing deviation between corporate earnings and corporate profits. There has only been one other point where earnings, and stock market prices, were surging while corporate profits were flat. Shortly thereafter, we found out the “truth” about WorldCom, Enron, and Global Crossing.

TheAmerican Accounting Association found that over the past decade or so, more companies have shifted to emphasizing adjusted earnings. But those same companies’ results under generally accepted accounting principles, or GAAP, often only match or slightly exceed analysts’ predictions.

“There are those who might claim that so far this century the U.S. economy has experienced such an unusual period of economic growth that it has taken analysts and investors by surprise each quarter … for almost two decades. This view strains credulity.” – Paul Griffin, University of California & David Lont, University of Otago

After reviewing hundreds of thousands of quarterly earnings forecasts and reports of 4,700 companies over 17 years, Griffin and Lont believe companies shoot well above analysts’ targets because consistently beating earnings per share by only a penny or two became a red flag.

“If they pull out all the accounting tricks to get their earnings much higher than expected, then they are less likely to be accused of manipulation.”

The truth is that stocks go up when companies beat their numbers, and analysts are generally biased toward wanting the stock they cover to go up. As we discussed in “Chasing The Market”, it behooves analysts to consistently lower their estimates so companies can beat them, and adjusted earnings are making it easier for them to do it.

For investors, the impact from these distortions will only be realized during the next bear market. For now, there is little help for investors as the Securities and Exchange Commission has blessed the use of adjusted results as long as companies disclose how they are calculated. The disclosures are minimal, and are easy to get around when it comes to forecasts. Worse, adjusted earnings are used to determine executive bonuses and whether companies are meeting their loan covenants. No wonder CEO pay, and leverage, just goes up.

Conclusion & Why EBITDA Is BullS***

Wall Street is an insider system where legally manipulating earnings to create the best possible outcome, and increase executive compensation has run amok,. The adults in the room, a.k.a. the Securities & Exchange Commission, have “left the children in charge,”but will most assuredly leap into action to pass new regulations to rectify reckless misbehavior AFTER the next crash.

For fundamental investors, the manipulation of earnings not only skews valuation analysis, but specifically impacts any analysis involving earnings such as P/E’s, EV/EBITDA, PEG, etc.

“One of the things that I thought that I knew well was the importance of income-based metrics such as EBITDA, and that cash flow information is not as important. It turned out that common garden variety metrics, such as EBITDA, could be hazardous to your health.”

The article is worth reading and chocked full of good information, however, here are the four-crucial points:

EBITDA is not a good surrogate for cash flow analysis because it assumes that all revenues are collected immediately and all expenses are paid immediately, leading to a false sense of liquidity.

Superficial common garden-variety accounting ratios will fail to detect signs of liquidity problems.

Direct cash flow statements provide a much deeper insight than the indirect cash flow statements as to what happened in operating cash flows. Note that the vast majority (well over 90%) of public companies use the indirect format.

EBITDA, just like net income is very sensitive to accounting manipulations.

The last point is the most critical. As Charlie Munger recently stated:

“I think there are lots of troubles coming. There’s too much wretched excess.

I don’t like when investment bankers talk about EBITDA, which I call bulls— earnings.

It’s ridiculous. EBITDA does not accurately reflect how much money a company makes, unlike traditional earnings. Think of the basic intellectual dishonesty that comes when you start talking about adjusted EBITDA. You’re almost announcing you’re a flake.”

In a world of adjusted earnings, where every company is way above average, every quarter, investors quickly lose sight of what matters most in investing.

“This unfortunate cycle will only be broken when the end-users of financial reporting — institutional investors, analysts, lenders, and the media — agree that we are on the verge of systemic failure in financial reporting. In the history of financial markets, such moments of mental clarity most often occur following the loss of vast sums of capital.” – American Accounting Association

Imaginary worlds are nice, it’s just impossible to live there.

Profs. Michael C. Dorf (Cornell), Andrew Koppelman (Northwestern), and I have filed a couple of amicus briefs arguing that anti-BDS laws generally don’t violate the First Amendment (see, e.g., here, plus this follow-up post from Mike). A Harvard Law Review unsigned student note described us as supporters of such laws, apparently assuming that, since we thought the laws were constitutional, we thought they were wise.

After we pointed out the error, the editors promptly corrected the online versions of the note; but this prompted Mike and Andy to post further on the subject, explaining that they don’t endorse such laws as a policy matter. (My own inclination is to be skeptical of such laws, too, even when limited to conditions on government contracts, though my views on the subject are not firm, at least when applied to large contracts with large organizations.) In any event, if you’re interested in the laws, please check out Mike’s and Andy’s follow-up posts.

from Latest – Reason.com https://ift.tt/32oCoLl

via IFTTT