4,000 US Troop Surge To Middle East Could Be Imminent Amid Baghdad Chaos

Three U.S. defense officials told Fox News on Tuesday that the U.S. Army’s 82nd Airborne Division’s alert brigade has been given orders to deploy to Kuwait amid the social unrest in Baghdad.

Even though all supporters of Iran-backed militias have withdrawn from the heavily fortified U.S. Embassy in Baghdad on Wednesday, the reinforcement of U.S. troops could be imminent.

Defense Secretary Mark Esper said in a statement on Tuesday that 750 troops are immediately deploying to the Middle East because of the attack on the U.S. embassy.

The US says it’s sending 750 troops to Iraq after its embassy in Baghdad was stormed by protesters.

Esper said he had authorized the deployment of an infantry battalion from the Immediate Response Force (IRF) of the 82nd Airborne Division.

“This deployment is an appropriate and precautionary action taken in response to increased threat levels against U.S. personnel and facilities, such as we witnessed in Baghdad today,” Esper said in a statement.

Apart from the rapid deployment, the three sources told Fox that approximately 4,000 paratroopers could be deployed to the region in the coming days.

There are 5,000 US troops currently stationed in Iraq supporting local forces, among the more than 60,000 troops positioned in military bases across the Middle East.

President Trump blamed Iran for the attack on the U.S. embassy in Baghdad in a tweetstorm on Tuesday.

“Iran killed an American contractor, wounding many. We strongly responded, and always will,” tweeted Trump. “Now Iran is orchestrating an attack on the U.S. Embassy in Iraq. They will be held fully responsible.”

“In addition, we expect Iraq to use its forces to protect the Embassy, and so notified!” he added.

Trump said, “….Iran will be held fully responsible for lives lost, or damage incurred, at any of our facilities. They will pay a very BIG PRICE! This is not a Warning, it is a Threat. Happy New Year!”

It appears that Trump isn’t pulling out of the Middle East after all, but rather a massive surge in troops into the region could be seen in the coming days. Is conflict with Iran nearing?

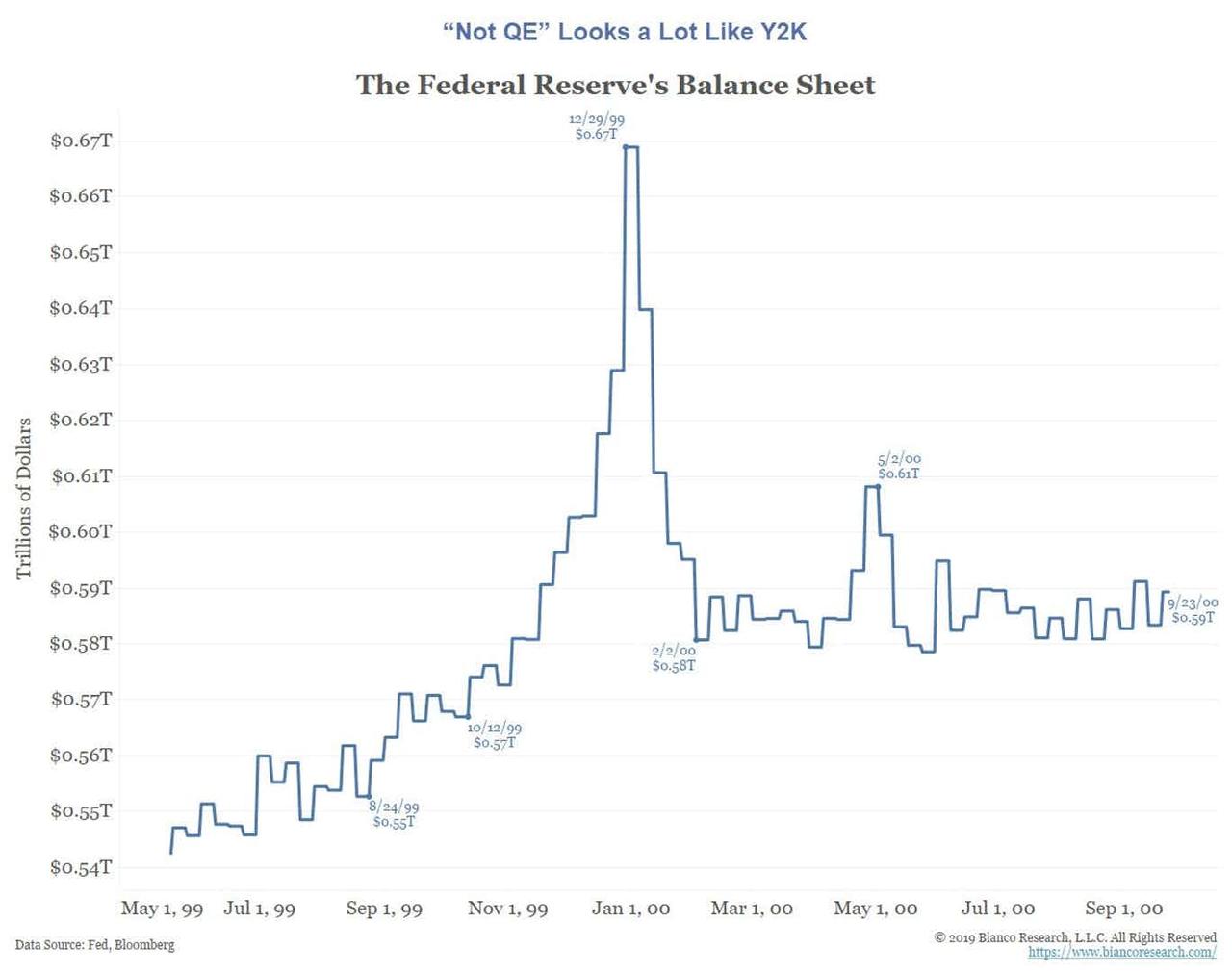

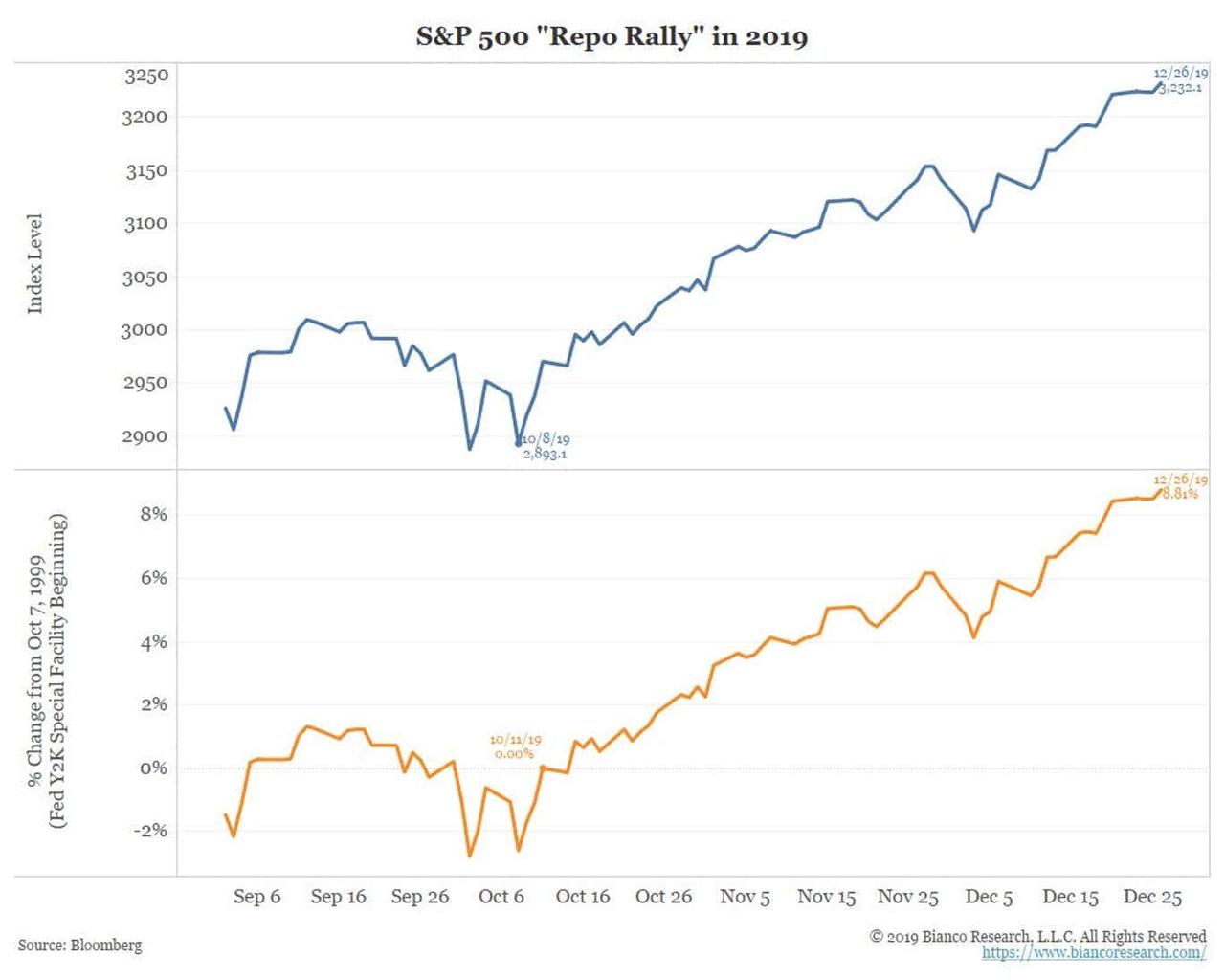

We would argue the special lending facility that started in late 1999 to support the feared Y2K computer glitch offers a historical analogy to the current period.

Stories 20 years ago sound like they are describing what is happening today:

Dow Jones News Service – (December 28, 1999)CASH IS FLOWING LIKE CHAMPAGNE FOR Y2K

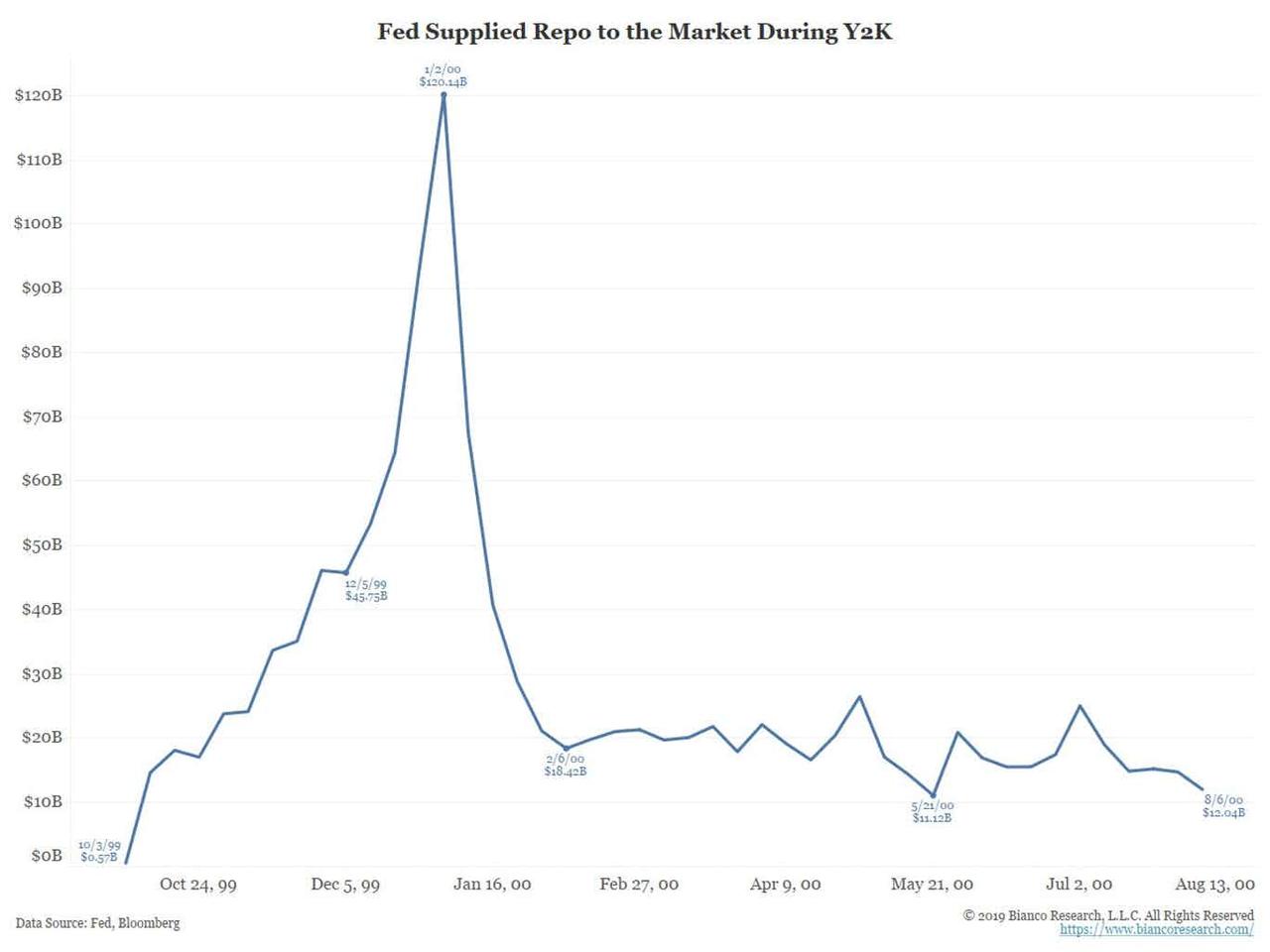

The volume of cash that the Federal Reserve has temporarily given to banks to avert potential Year 2000 strains is rising to dizzying levels. Including nearly $20 billion it gave to the banking system in the form of term “repurchase” agreements Monday, the Fed has almost $100 billion in hard currency loans outstanding to banks. That’s the most money lent out through repurchase agreements ever, said Peter Bakstansky, spokesman for the New York Federal Reserve. For some perspective, the Fed had $23 billion in outstanding “repos” in December 1998, and around $9 billion in December 1997.

The Y2K special lending facility had a similar effect on the Fed’s balance sheet. It was also done for “plumbing reasons.”

And, as the [Champagne] story points out, the Fed supplied record amounts of repo never before seen at the time.

Fed Supplied Repo to the Market During Y2K

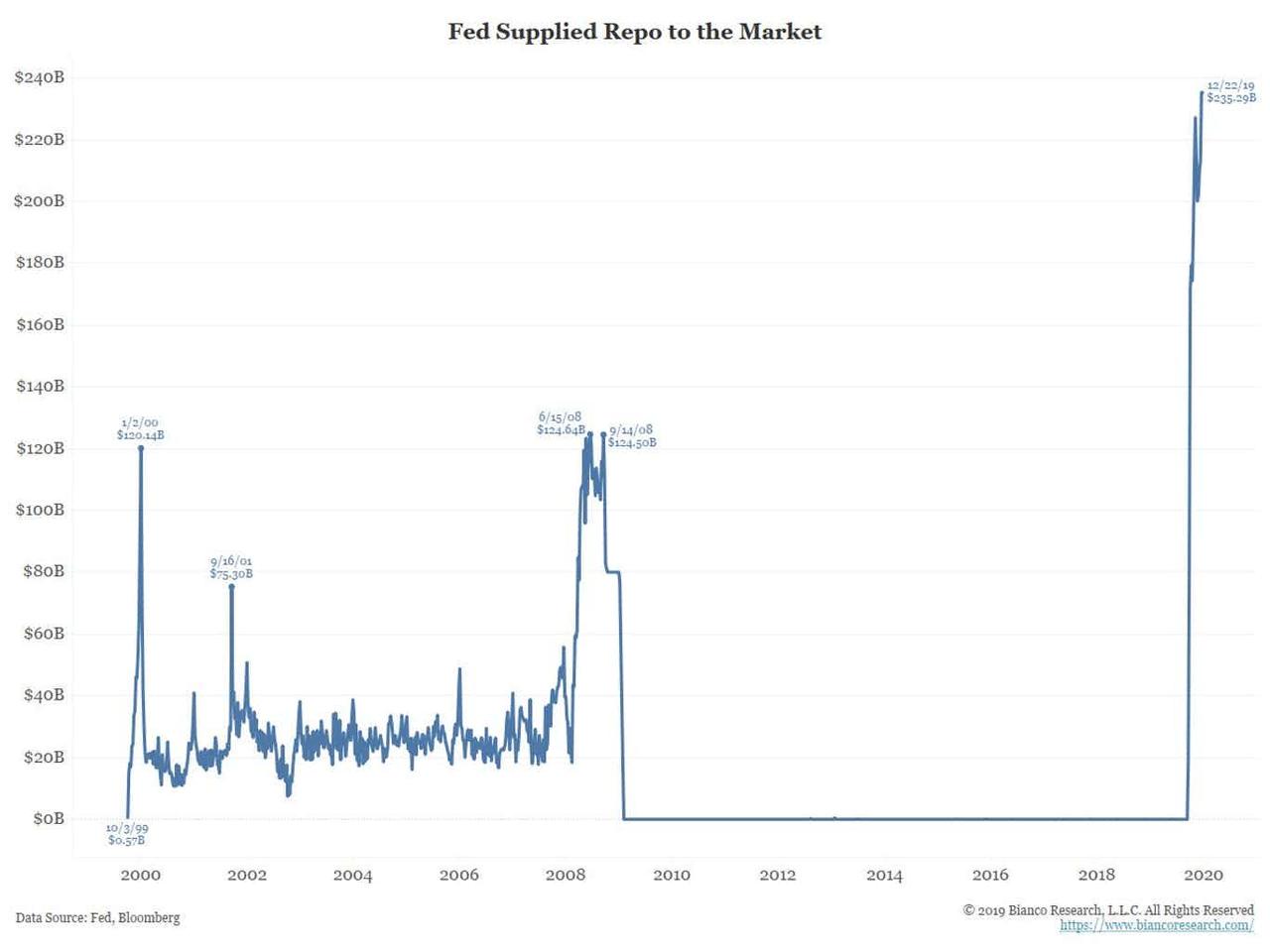

In fact, the amount of repo the Fed supplied in late 1999 was significantly more than on 9/11 and on par with the support offered during the financial crisis.

It was not until September 2019 that the Fed’s repo operations finally saw a meaningfully higher level.

Y2K Special Lending Starter Oct 7, 1999

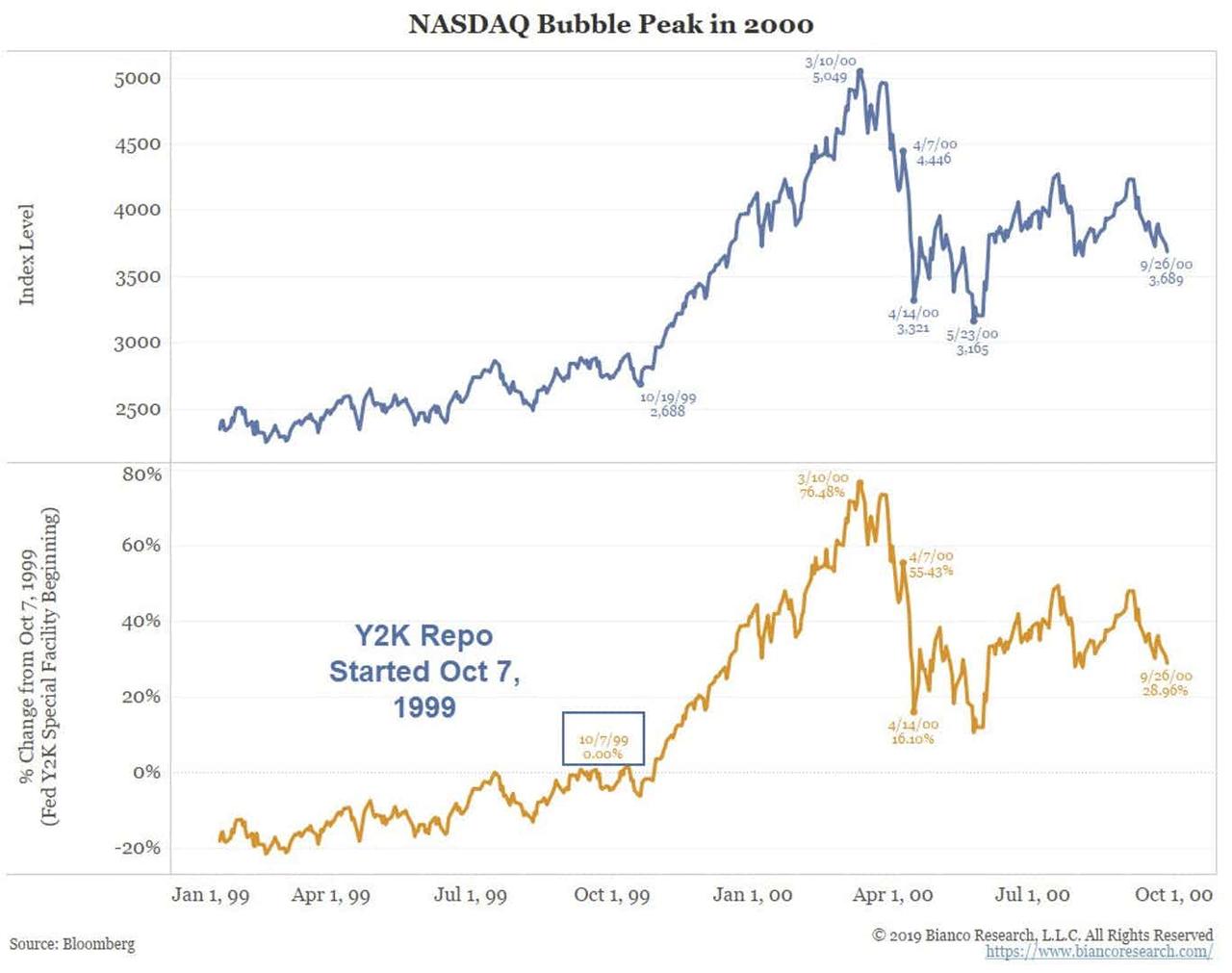

Note that the Y2K special lending facility ran from October 7, 1999, to April 7, 2000. And what did stocks do during this period? Below is the NASDAQ.

The Nasdaq went on a tear rarely seen in American finance, starting literally the day the Fed opened its Y2K lending facility. It crashed 25% the week the facility closed (April 7, to April 14, 2000).

2019 Repo Rally

How does this analogy currently compare? The Fed announced it would start buying T-bills on October 11, 2019. Stocks have gone a tear since (clearly the magnitude of the NASDAQ returns above were larger, but the timing of the bottom in each case is similar).

Conclusion

There is no such thing as a one-factor model to explain the stock market. Metrics such as the Fed’s balance sheet, repo, etc. cannot explain the stock market’s movements in isolation.

That said, when the Fed injects money, funds generally flow to the best-returning market. During the financial crisis, it was the bond market. Today, as was the case in 1999, it is the stock market.

There have been indications of how important the Fed’s balance sheet is to financial flows in the recent past.

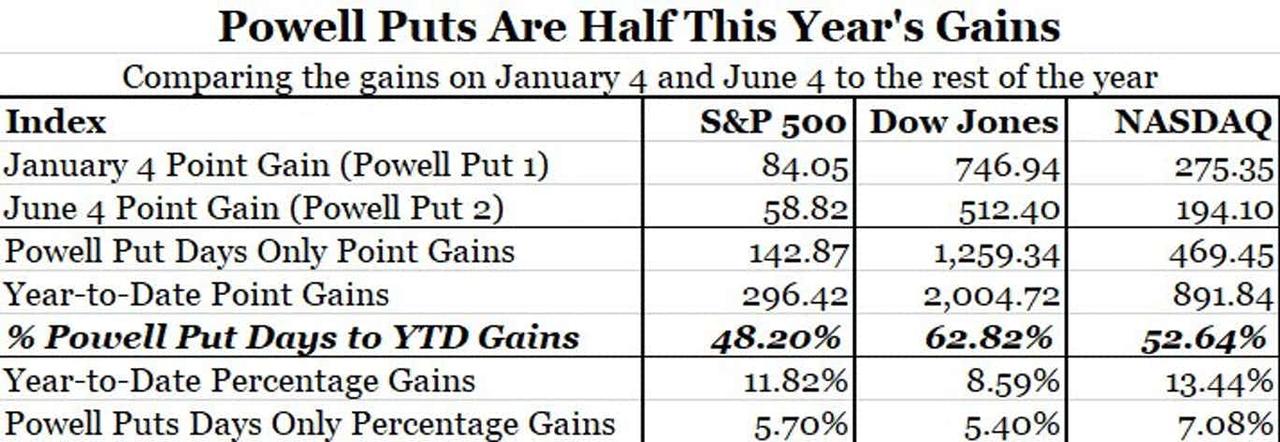

During the Fed’s Dec 19, 2018 presser, the stock market collapsed when Powell said the balance sheet was on “automatic pilot.” It soared almost a 1,000 DJIA points on January 4 when he said the Fed would be “patient and flexible.” On June 4, when he said the Fed would “act as appropriate,” stocks continued higher. Again, no single measure can predict the stock market, but these were clear signs that the size of the Fed’s balance sheet and policy matter.

The following table highlights this. Through June 5, half the gains to that point came on the two days Powell commented on policy.

Powell PUTs are Half This Year’s Gains

Another 9% of the stock market’s gains came after October 11, when the Fed announced its T-bill purchase problem. So, a big part of this year nearly 30% stock market gain has come on the heels of Fed moves, much like last year’s 20% decline was coincident with the Fed’s hawkish rhetoric.

Given all this, the big question is, what happens when the Fed ends T-bill purchases and repo support in Q2 (the current projected end date)? Will the April 2000 analogy apply?

* * *

The above was a guest post generously provided by James Bianco.

It was part of his proprietary research.

I asked Bianco if he would make that post public, and he did.

Although the point about Y2K is clear, I asked Jim explicitly if this was QE.

He replied:

By saying it is “Not QE” they are arguing it is not impacting financial markets. By detailing the Y2K “Not QE” episode, I’m arguing that not only is is QE, but we also have a historical example of how it has worked previously.

In retrospect, it is not important how one labels this.

My friend Pater Tenebrarum at the Acting Man Blog pinged me with this comment on Hussman’s thoughts.

Who cares what it is called, the result is an explosive increase in the money supply!! And it’s not bank lending that’s behind that, because bank lending growth continues to slow down. So the economic effect is exactly the same as with “QE”. It walks like a duck, quacks like a duck, guess what: it’s a duck!

Iraqi Protesters Retreat From US Embassy In Baghdad

In the end, calls for a second “Benghazi” proved grossly unfounded.

An attempt by supporters of Iran-backed militias to storm the heavily fortified US Embassy in Baghdad went into retreat Wednesday, as American troops reinforced the besieged compound and as protesters withdrew from the area after their leadership ordered the suspension of a violent challenge to American troop presence in Iraq (where US troops have been stationed for nearly two decades).

The retreat was instigated by paramilitary leaders from the Popular Mobilization Forces, which is part of the Iraqi security apparatus and an umbrella body for dozens of militia groups including factions aligned with Iran. The PMF said protesters demanding the expulsion of American troops from Iraq had delivered their message to the US.

According to the WSJ, dozens of protesters who had camped overnight on New Year’s Eve near the gates of the U.S. Embassy began to dismantle their tents following the PMF’s call to withdraw. Earlier, they had appeared to be in for the long haul, setting up portable bathrooms and a podium. The PMF said the protest site would be moved to the other side of the Tigris River, which bisects Baghdad—still within sight of the embassy. Meanwhile, Iraqi security forces took up positions around the embassy.

Iraqi soldiers stand guard in front of the U.S. Embassy as Iran-backed militia supporters take part in a sit-in outside the gates of the embassy on Wednesday. Photo: Zuma Press

The withdrawal was intended “to preserve the authority of the state” and “out of respect for the government’s decision” protesters should move away from the embassy, according to the PMF, which ordered the crowds at the embassy to withdraw, claiming that their “message has been heard.”

Separately, President Trump spoke to Iraqi Prime Minister Adel Abdul-Mahdi overnight and declared the embassy safe, saying the Iraqi government had “stepped up.” He blamed the assault on the U.S. outpost on Iran.

Footage from Ruptly showed protesters with Hezbollah flags withdrawing in their vehicles. It was not immediately clear from the video how many have remained at the scene of clashes, where tear gas and stun grenades were reportedly fired again on Wednesday.

“We decided to leave after our superiors received an urgent request from [Prime Minister] Abdul-Mahdi himself asking us to because… there is a lot of pressure on him now,” said a senior member of Kataib Hezbollah who declined to be named.

“Abdul-Mahdi is on our side and has been helping us a lot, so we don’t want to harm him or cause him problems,” he added.

A day earlier, supporters and members of Kataib Hezbollah and other Iran-backed militias attempted to violently force their way into the US Embassy compound located inside the heavily fortified Green Zone, but failed to break in. Enraged by Sunday’s US airstrikes against the Kataib Hezbollah militia, the crowd lit fires and pelted the embassy with stones. Shortly after, a contingent of US Marines arrived on Tuesday night to bolster security. The attack prompted the U.S. to deploy military reinforcements and exposed the power of Tehran’s allies in Iraq.

Pro-Iranian militia and their supporters light a fire while U.S. soldiers fire tear gas during a sit-in outside the U.S. Embassy in Baghdad on Wednesday. Photo: AP.

Kataib Hezbollah, which the U.S. sees as a terrorist group and a proxy for Iran, left its yellow flag flying over an outer entrance to the embassy compound on Wednesday, having earlier said it wouldn’t back down.

Earlier on Wednesday, U.S. troops fired tear gas to disperse militia supporters crowding outside the embassy for a second day as Apache helicopters flew overhead.

“We will never stop demanding to kick the Americans out of Iraq,” said a cleric from the podium in front of the embassy before the withdrawal. “We demand the Parliament approve the law of expelling the Americans.”

The assault on the U.S. Embassy however, was condemned by some Iraqi politicians, including a Sunni block that described it as a “dangerous development” that risked isolating Iraq. Parliament Speaker Mohammed al-Halbousi also said the incident was “unacceptable” and damaging to Iraqi interests.

The attack strained relations between Washington and Baghdad and revived calls for a vote in Parliament on the expulsion of U.S. troops, which returned to Iraq in 2014 to fight Islamic State. Despite their retreat from the embassy area, Iran’s allies are expected to keep pressing for a parliamentary vote on the withdrawal of U.S. troops, further undermining the U.S.’s influence in the country. Tehran, meanwhile, has shown that its allies in Iraq are stronger than the government of which they are a part.

Washington blamed Iran for orchestrating the embassy riots, and for directing militias like Kataib Hezbollah to attack its forces in Iraq. Meanwhile, Tehran has denied all responsibility, with Iranian Supreme Leader Ayatollah Ali Khamenei telling Trump that “your crimes in Iraq, Afghanistan… have made nations hate you.”

As the Iraq embassy showdown turned into yet another proxy battle between Iran and the US, Iraqi Prime Minister Adel Abdul Mahdi sought to balance relations with both sides. The PM called the US airstrikes a “vicious assault that will have dangerous consequences,” but warned protesters against any aggression towards foreign embassies.

On Tuesday, Secretary of State Mike Pompeo the assault on the U.S. Embassy “should not be confused with the legitimate efforts of the Iraqi protesters who have been in the streets since October working for the people of Iraq to end the corruption exported there by the Iranian regime.”

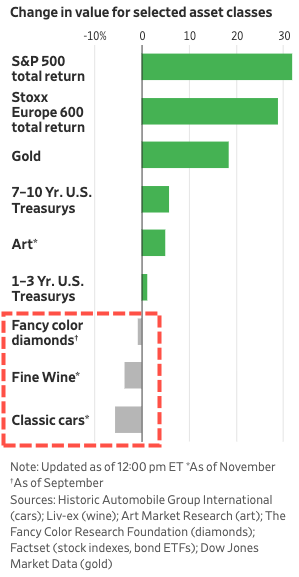

“Tail-End Of A Big Bull Market” – Wine, Diamonds, Classic Cars Are Now Money-Losing Investments For Ultra-Rich

Luxury assets of the ultra-wealthy, if that were expensive wine, fancy diamonds, and rare antique cars all had a down year as the stock market ramped to new highs, reported The Wall Street Journal.

In the last decade, luxury assets performed exceptionally well as central bankers handed out free money to the elite class to hoard assets of their liking. And naturally, these people, with exceptional taste, bought things that the common man has only seen on television.

Now, these luxury assets are underperforming – have been for the last several years – and is a symptom of late-cycle distress.

“The froth has gone out of the market. People have realized you can’t just buy stuff and expect the value to go up,” said Andrew Shirley, a partner at Knight Frank and editor of the group’s Wealth Report.

The Journal blames the underperformance on the global slowdown and the lack of Asian demand. Chinese buyers account for 33% of global luxury goods sales.

“There is a lot of uncertainty in Chinese markets and the riots in Hong Kong didn’t make it easy for people to come spend money in Hong Kong,” said Eden Rachminov, chairman of the board at the Fancy Color Research Foundation.

Colored diamonds in 2019 lost about 1% in the first three quarters.

Fine wine was also another losing asset through Nov., lost 3.6%, according to the Liv-ex 1000 index.

And the biggest loser on the year were classic cars, lost 5.6%, according to Historic Automobile Group International’s (HAGI) Top Index.

HAGI founder Dietrich Hatlapa said the classic car market has been cooling following a massive rise in price after the 2008-09 financial crisis. He said classic car prices saw double-digit gains after the recession, rallying 50% Y/Y through 2013. “We are at the tail-end of a big bull market,” Hatlapa warned.

What’s becoming evident is that ‘Not QE’ and other monetary gimmicks deployed by central banks are failing to raise asset prices of some luxury goods in 2019. Perhaps the world is stumbling into a period where toolkits of central banks are becoming less responsive to stimulate asset price inflation, and if that is the case, then everyone will figure out that prices of luxury goods have been hyperinflated over the last decade with nothing but hot air.

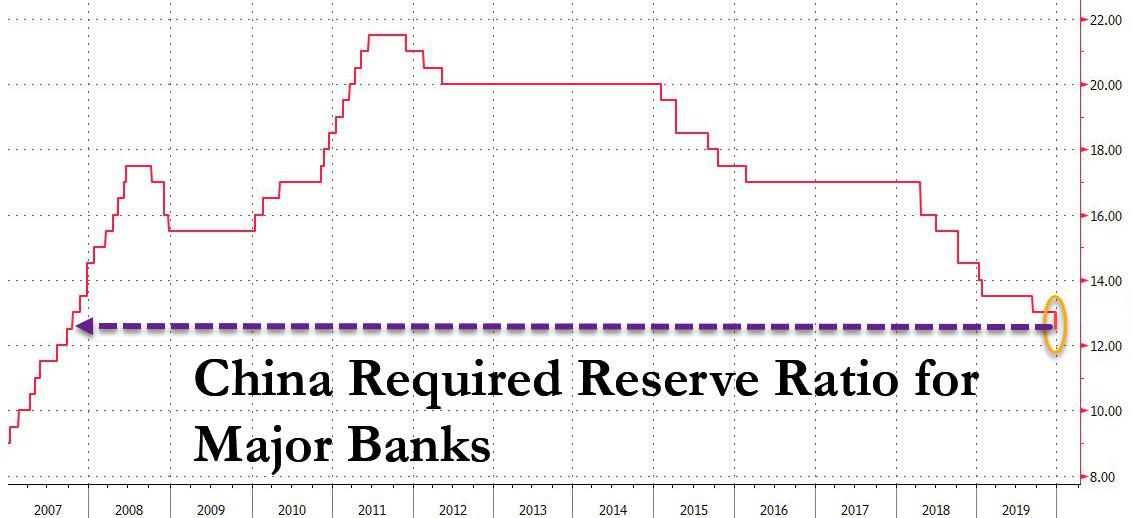

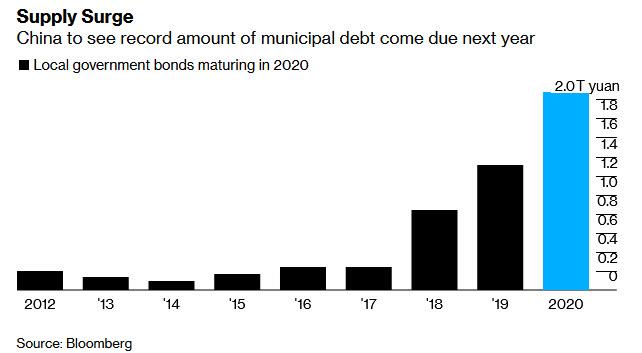

China Cuts Reserve Ratio By 50bps Ahead Of January’s $400 Billion “Liquidity Hole”

Just three days after China quietly cut rates by 20bps when it ordered banks to switch from the traditional Benchmark 1 year rate to the new Loan Prime Rate (aka China’s LIBOR) as the reference rate for new short-term loans, effectively lowering the prevailing rate from 4.35% to 4.15% (in the process further pressuring bank net interest margins), on the first day of the new 2020, the PBOC unveiled widely expected another boost for the slowing Chinese economy: the central bank announced that starting Jan 6, it will lower the required reserve ratio (RRR) – or the amount of money banks are required to have on hand – by 50bps for commercial lenders, in the process releasing about 800 billion yuan ($115 billion) in liquidity from the cash-strapped financial system.

Currently the required reserve ratio is 13% for large banks and 11% for small banks. The cut, which is the first since September, will bring the blended reserve ratio for Chinese banks to the lowest level since October 2007.

The 50bps RRR cut is meant to help banks reduce their lending rate to businesses, the PBOC said in a separate statement, which is ironic because while on one hand the PBOC pressures commercial banks by ordering them to lower the amount of interest they can charge customers by 20bps (with the benchmark rate recalibration), on the other it boosts systemic liquidity to offset the adverse effects of its first action, something we predicted would happen earlier this week, to wit:

… with more than half of China’s banks failing a recent central bank stress test, the only guaranteed outcome from this weekend’s effective rate cut is that, paradoxically, it will only accelerate the rate of failure of China’s already cash strapped, and in many cases insolvent, banks. As such we expect that the PBOC will promptly follow through with another RRR cut to offset the adverse side-effects of this particular rate cut, by injecting more liquidity in the banking system.

Of course, it wasn’t just us predicting an imminent RRR reduction: the cut was first signaled by Chinese premier Li Keqiang in December 2019. It’s also in line with market expectations that the PBOC will increase funding to the financial system in January to ease a liquidity crunch caused by rising local government debt sales and increasing cash demand during the Spring Festival holidays.

As a reminder, two weeks ago we warned that China is facing a potentially destabilizing “liquidity hole” of 2.8 trillion yuan ($400 billion) in January as people across the nation will withdraw cash for the Lunar New Year holiday, which this year falls on Jan 25. China’s most important annual holiday is a time when companies and individuals typically need large amounts of cash on hand to pay bonuses, clear debts and cover other expenses. In addition to seasonal cash needs, China’s bond market also faces a major maturity deluge, as more than 2 trillion yuan in notes mature in early 2020, and fresh debt to refinance the borrowing thus shoring up economic growth will probably start hitting the market soon.

Sure enough, in addition to offsetting the reduced net interest margin, the PBOC said that the injection will be offset as banks provide more cash to the public before the Spring Festival, and the overall liquidity level at banks will be kept stable. “Prudent monetary policy stance remains unchanged,” it added.

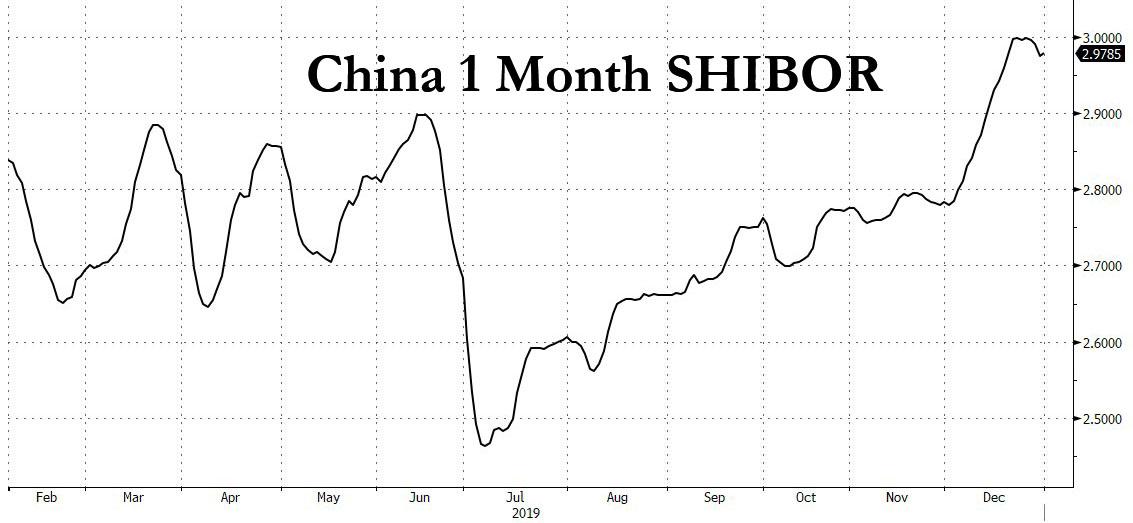

It was fears about an impending liquidity shortfall that sent China’s 1Month SHIBOR to the highest level in one year, briefly touching 3% a few days ago.

However, now that China is engaged in a delicate balancing act, on one hand reducing the amount of cash banks can earn by lending money to customers, and on the other releasing systemic liquidity, the question is whether the PBOC’s latest efforts to stimulate the economy will destabilize the banking sector further.

Addressing just this, the PBOC said the planned reduction will save about 15 billion yuan in funding costs for banks in a year, indicating that the benchmark loan prime rate will likely be lowered as banks reduce their submissions for the rate’s calculation in late January, which in turn will force the PBOC to cut the RRR further, resulting in an even lower loan prime rates and so forth, which brings to mind a recent striking op-ed published in the Global Times, which predicted that China would be the next major country to cut rates to zero.

And while Xinhua quoted an unidentified central bank official as saying that Wednesday’s move does not presage a large-scale government stimulus program, noting that “the stance of prudent monetary policy has not changed” and ruling out the possibility of a “flood-like” flow of fresh money, Beijing may have no choice, even if food inflation is now far higher than 2011, when the RRR was just shy of 22%.

“Looking ahead, there’s still room for more reserve ratio cuts in 2020” to mitigate the impact of deleveraging at small banks, wrote CICC economist Eva Yi. “Should economic growth show more signs of stabilization and recovery after the cut, it’s likely the central bank will slow down the pace of further reserve ratio cuts.” Then again, since China’s economic slowdown had little to do with the trade war and everything to do with its massive debt load, accelerating bank failures, record debt defaults and record bad debts, we have a feeling that if there is a change to the pace of RRR cuts it will be the opposite of “slowing.”

Every week seems to bring a new story about how vaping is really, really, really bad for you. Only a few years ago, electronic cigarettes were hailed as a new and healthier way for people to consume nicotine and pot; the number of vapers worldwide has grown sevenfold since 2011, to an estimated 41 million users. But now vaping is being attacked as a deadly habit that might be as bad for you as traditional smoking.

Reports of vaping-related deaths and respiratory illnesses appear daily on cable news shows, in newspapers, and online. The FDA is considering a ban on flavored e-cigarettes, and many states have already instituted strict regulations on vaping sales and use. Congress has voted to change the age for legal tobacco and e-cigarette sales to 21, up from 18. President Donald Trump signed the legislation into law just before Christmas.

Is vaping bad for you? Should we be panicking? What sorts of policies should govern the use of electronic cigarettes for nicotine and marijuana? To answer these and other questions, Nick Gillespie sat down with Reason Senior Editor Jacob Sullum, who has spoken extensively and authoritatively about the issue for years. Sullum argues that the current anti-vaping freakout is a classic case of moral panic, and that it is in fact making it harder for current smokers to transition to a safer method of getting nicotine or to quit altogether.

from Latest – Reason.com https://ift.tt/39tRouv

via IFTTT

Every week seems to bring a new story about how vaping is really, really, really bad for you. Only a few years ago, electronic cigarettes were hailed as a new and healthier way for people to consume nicotine and pot; the number of vapers worldwide has grown sevenfold since 2011, to an estimated 41 million users. But now vaping is being attacked as a deadly habit that might be as bad for you as traditional smoking.

Reports of vaping-related deaths and respiratory illnesses appear daily on cable news shows, in newspapers, and online. The FDA is considering a ban on flavored e-cigarettes, and many states have already instituted strict regulations on vaping sales and use. Congress has voted to change the age for legal tobacco and e-cigarette sales to 21, up from 18. President Donald Trump signed the legislation into law just before Christmas.

Is vaping bad for you? Should we be panicking? What sorts of policies should govern the use of electronic cigarettes for nicotine and marijuana? To answer these and other questions, Nick Gillespie sat down with Reason Senior Editor Jacob Sullum, who has spoken extensively and authoritatively about the issue for years. Sullum argues that the current anti-vaping freakout is a classic case of moral panic, and that it is in fact making it harder for current smokers to transition to a safer method of getting nicotine or to quit altogether.

from Latest – Reason.com https://ift.tt/39tRouv

via IFTTT

In the wake of the Fukushima disaster in Japan in 2011, Germany ordered the immediate shutdown of eight of its 17 reactors, and plans to phase out nuclear power plants entirely by 2022.

The Philippsburg 2 reactor near the city of Karlsruhe in southwestern Germany has provided energy for 35 years. The Philippsburg 1 reactor—opened in 1979—was taken offline in 2011.

Over the past few years, nuclear power generation in Germany has been declining with the shutdown of its nuclear plants, while electricity production from renewable sources has been rising.

In January 2019, Germany became the latest large European economy to lay out a plan to phase out coal-fired power generation, aimed at cutting carbon emissions—a metric in which Berlin has been lagging in recent years.

A government-appointed special commission at Europe’s largest economy announced the conclusions of its months-long review and proposed that Germany shut all its 84 coal-fired power plants by 2038.

Germany, where coal, hard coal, and lignite combined currently provide around 35 percent of power generation, has a longer timetable for phasing out coal than the UK and Italy, for example—who plan their coal exit by 2025—not only because of its vast coal industry, but also because Germany will shut down all its nuclear power plants within the next three years.

The closure of all nuclear reactors in Germany by 2022 means that Germany might need to retain half of its coal-fired power generation until 2030 to offset the nuclear phase-out, German Economy and Energy Minister Peter Altmaier said earlier this year.

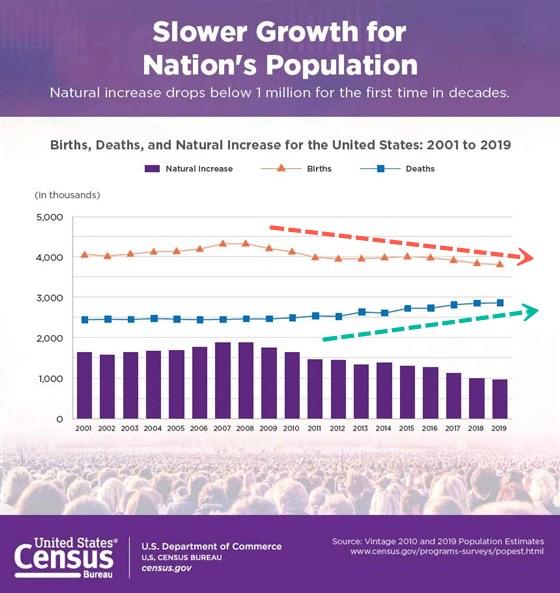

US Records Slowest Population Growth In Century As Births Decline

New figures from the US Census Bureau detail a troubling trend in the “greatest economy ever,” one where this year’s population growth is the slowest in a century due to decline births and lower immigration trends, reported AP News.

From 2018 to 2019, the population in the US expanded at .48% or about 1.5 million people, with a total population outstanding of around 328 million.

The report mentions how a lack of migrants entering the country along with a decline in natural increase has led to waning population growth since the 2008 financial crisis.

William Frey, a senior fellow at The Brookings Institution, told AP that the 2019 population growth is the slowest since 1917/18.

“With the aging of the population, as the Baby Boomers move into their 70s and 80s, there are going to be higher numbers of deaths,” Frey said. “That means proportionately fewer women of childbearing age, so even if they have children, it’s still going to be less.”

The Census Bureau said the natural population increased by 957,000 from 2018 to 2019, which is the first time it has breached 1 million since the late 1970s.

Immigration has also been on the decline since adding 1 million in 2016. From 2018 to 2019, immigration inflow only added 595,000 to the total population.

On a state by state analysis, New York lost 77,000 people; Illinois lost 51,000 residents; West Virginia lost 12,000 people, Louisiana lost 11,000 residents, and Connecticut lost 6,200 people. Alaska, Hawaii, Mississippi, New Jersey, and Vermont each lost about 5,000 residents over the period.

Regionally, the South recorded .8% population growth from 2018 to 2019, due mostly to natural increases and inbound domestic immigration. The Mid-Atlantic and Northeast regions saw population declines for the first time in a decade, declining .1% because of people moving to the South.

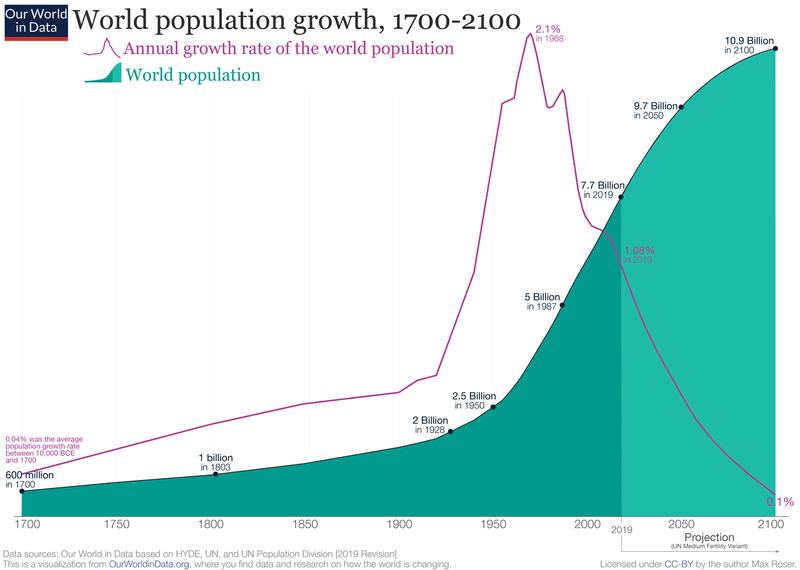

And while the population increases across the world are mainly behind us, the next big demographic trend is one where the global fertility rate could collapse in the coming decades.

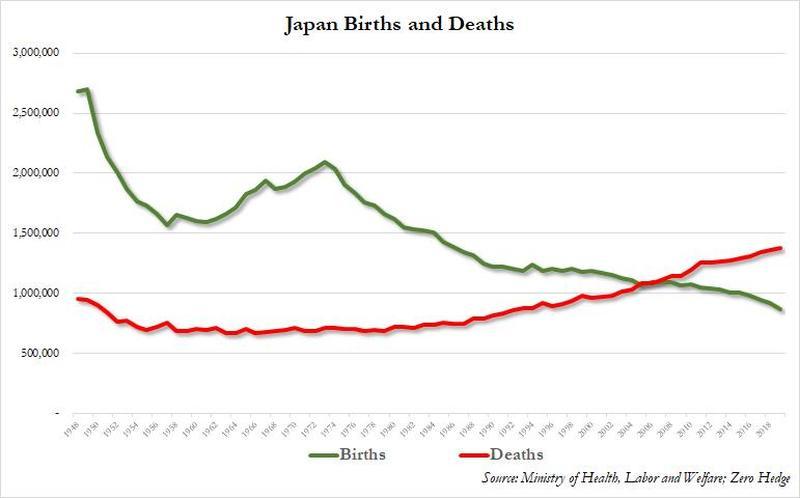

We recently noted how Japan, the world’s third-largest economy, just recorded the lowest amount of births since 1874.

In China, the world’s second-largest economy, a significant dip in the country’s birth rate was recorded earlier this year that showed births in 2018 hit levels not seen since 1949.

Decelerating growth of the world’s births and soaring deaths are visible around the globe. This means policymakers in the US will take a page from China and Japan’s playbook and create incentives for women to have more children with hopes of starving off demographic armageddon.

With the large Conservative majority in government, both UK markets and the economy are likely to enter a honeymoon period in the months ahead. While many are focused on Brexit as the main shock that could hit the UK economy, there are at least three other potential shocks that could be as significant.

And crucially they could all materialise in the next five years during the term of the newly elected UK government:

(1) Recession shock

Since the 1950s there has been a recession every nine years on average. The last UK recession was in 2008 around the global financial crisis, and we are now entering 2020. So on that metric, we are overdue. Perhaps the UK facing no inflation problem (allowing the Bank of England to keep interest rates very low) has kept a recession at bay. Equally, perhaps the US fiscal stimulus of recent years has prolonged the global business cycle, and the UK has been a beneficiary.

But the odds of a UK recession in the next five years are very high. There is no new large China-sized economy that will emerge like it did in the 2000s. Nor are tech advances having the same economy-wide productivity boosts as they were in the 1990s. At the same time, UK debt levels are high, the UK current account deficit is widening, and unit labour costs are on the rise. All these factors suggest the foundations for a recession are being set. And though the timing is unclear, within the first term of the new UK government looks probable.

(2) Market shock

No economies escaped the trauma of the 2008 financial crisis, not even the UK. It was caused by credit-fuelled asset bubbles, notably in real estate. Banks were at the heart of this and, ever since 2008, they have been regulated to ensure such a crisis will not repeat itself. However, crises typically do not follow the script of their predecessors. The next crisis will probably occur just where regulators fail to focus, or worse, because of mistakes regulators make where they have been focused.

The most obvious candidate would be a crisis in the non-bank financial sector. Regulators have constrained bank balance sheets, while asset managers have more freedom. Moreover, private markets – where private equity and leveraged finance live – have exploded. And these have even fewer constraints.

Perhaps the biggest advantage these players have is that they can more easily invest in illiquid assets. And much like banks incorrectly valued their ‘level 3’ assets in the run-up to 2008, private equity and asset managers could be overvaluing their illiquid assets. Their potentially obvious error would be to assume those assets have liquid markets into which they can be sold.

Already in the UK we have seen the Woodford fund and M&G property funds suffer on this score. In the US we have seen spikes in the repo market as pools of liquidity have been segmented. If these are the early signs, then we could be in for a much larger market liquidity shock. This could have far-reaching consequences for the economy, especially business investment and household wealth.

(3) Pension shock

The long-heralded pension crisis is almost upon us. Twenty years ago in the UK, one in eight people were over the age of 65. Today that number is nearing one in five. Throw in people in their fifties and early sixties, then close to 40% of the population are worrying about their pensions.

What makes matters worse is that people are expected to live well beyond the statutory retirement age of 65. For example, on a cohort-basis, women in the UK are now expected to live to 92 years. That means – at the current age of retirement – potentially 27 years living off their pensions. The trouble is that current pension schemes will only offer on average 28% of earlier earnings in retirement. This is well below the OECD average of 60% and closer to what is seen in Mexico and Lithuania than France (74%), Germany (52%) or even the US (49%). This is a recipe for social unrest.

But what will trigger a crisis in the coming years is the collapse in bond yields. In the 1990s and 2000s, UK 10-year bond yields (adjusted for inflation) averaged over 4%. As a pension fund, if you compounded this out, funding future retirement benefits was straightforward. However, in the 2010s, the real yield has collapsed to 0.15%. Worse still, since 2017 the real yield has been negative. Now the compounding accelerates against pension funds.

Of course, many pension funds, especially in the public sector with its crippling defined benefits, have diversified into private equity and other riskier investments. The trouble with these are that their returns are falling too. If anything, they appear to be converging to those of public equity markets. This begs the question, why is the public sector paying the high fees of private equity to get an illiquid version of public equity returns?

In the end, public sector workers and others will need to increase their contributions to make up for any shortfalls. One of the largest pension schemes in the UK, the Universities Superannuation Scheme (USS), did try to do just that. However, their request was met by university lecturers and support workers going on strike. This is likely just the beginning. And lest one think this a UK problem – French workers have recently taken to the streets over sweeping pension reforms

Bottom Line

The UK is not only facing the potential of a Brexit-related shock, but there are three other plausible shocks and crises the UK government will face in its five-year term. This will require adept and creative central bank policy – that crucially will have to differ from the post-2008 policies that have led to these coming crisis. Moreover, with the central bank policy toolkit severely constrained, the onus will be on the government to avert or mitigate these. But is it ready to do so?

{kind=link}

{kind=link}