Just one day after the anniversary of “funding secured”, we have learned that newly released documents indicate that the NHTSA could be preparing a “formal investigation” into Tesla, according to a former agency official that spoke to Bloomberg.

The NHTSA has issued “at least five subpoenas” to the company since April 2018 for crash data, as was revealed in a FOIA request made by legal transparency group PlainSite. The NHTSA also asked the company for information about a sub-component of the Model 3 sedan’s emergency braking system and sales figures of vehicles sold with and without Autopilot beginning in mid 2016.

Frank Borris, a former director of the Office of Defects Investigation at NHTSA, said: “I think what this shows is that NHTSA has concerns about Autopilot performance. The subpoenas could mean the agency is gathering information that would be supportive of a formal investigation.”

The NHTSA responded, stating it was “committed to rigorous and appropriate safety oversight of the industry and encourages any potential safety issue be reported to NHTSA.”

Tesla hilariously suggested that they are the ones that required the subpoenas: “Any regulator like NHTSA would be interested in new vehicle technologies and how they make our highways safer. We routinely share information with the agency while also balancing the need to protect customer privacy. Tesla has required subpoenas when customer information is requested in order to protect the privacy of our customers.”

Regardless, Borris says that the use of subpoenas is “atypical” and could mean a “heightened degree of interest in Autopilot”.

He continued:

“The fact that they’ve had to issue subpoenas about it indicates that NHTSA hasn’t been satisfied by Tesla’s responses, because that’s just not normal.”

Data on the company’s driver engagement was also included in NHTSA correspondence and was reviewed by David Friedman, a former deputy administrator at NHTSA during the Obama administration, who’s now vice president of advocacy at Consumer Reports.

He simply said: “Data like this show the system does not appear to be able to keep the driver engaged, and it’s one company, not the others in the space. To me, that raises real red flags about a possible defect.”

We can only guess who is carrying the “tone at the top” torch for driver disengagement, despite the company repeatedly warning that it requires drivers to have their hands on the wheel, even with Autopilot engaged.

Two of the NHTSA subpoenas were issued on March 11, seeking information about a crash in Delray Beach, FL that we reported on here. The NHTSA and NTSB have both investigated numerous Tesla crashes in recent years.

Recall, in May, Consumer Reports called for the NHTSA to open another inquiry into the company after publishing a study of automated driving systems in October.

The NHTSA currently does not have an active defect probe ongoing into Tesla and may not open one.

We covered the documents released as a result of the FOIA request in an article yesterday, which you can read here.

via ZeroHedge News https://ift.tt/2YZTzDT Tyler Durden

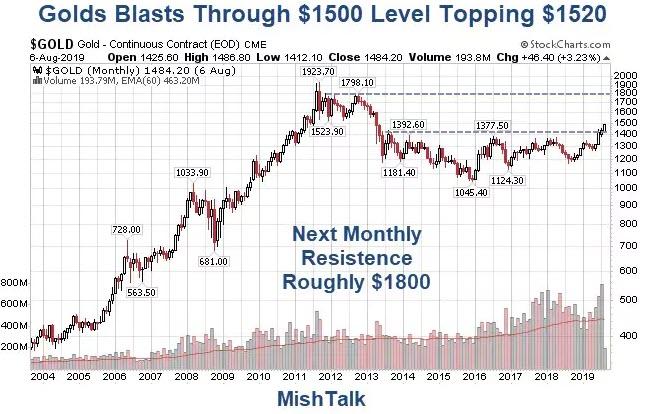

Gold blasted through the $1500 level this week. Let’s analyze the message. Here’s a hint: The message isn’t inflation.

The above chart is and end-of-day chart from yesterday. Gold closed at $1484.

At 11:30 AM Central, gold was at $1520, up $36 on the day.

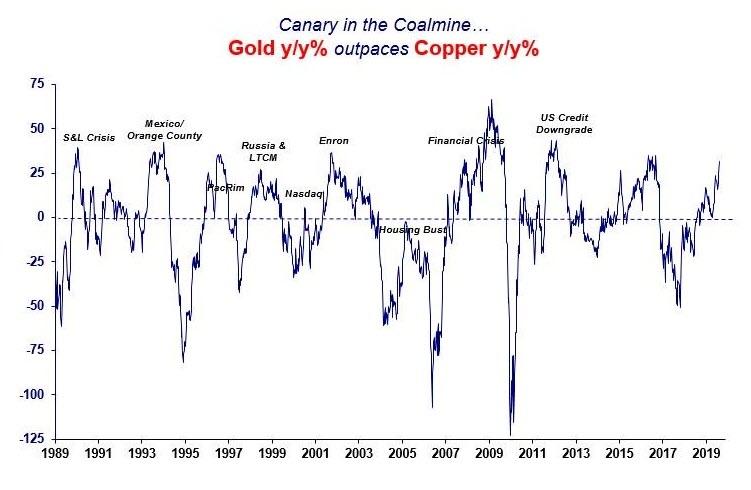

Gold vs Copper

What’s the Message?

Stephanie Pomboy at Macro Mavens nails it.

at the risk of piling-on,the canary in the financial crisis coalmine has been singing loudly. the relationship btw the metallic barometer of financial insecurity (gold) and the metallic barometer of economic activity (copper) has been a reliable predictor of trouble in the past. pic.twitter.com/K6rjNSpRcB

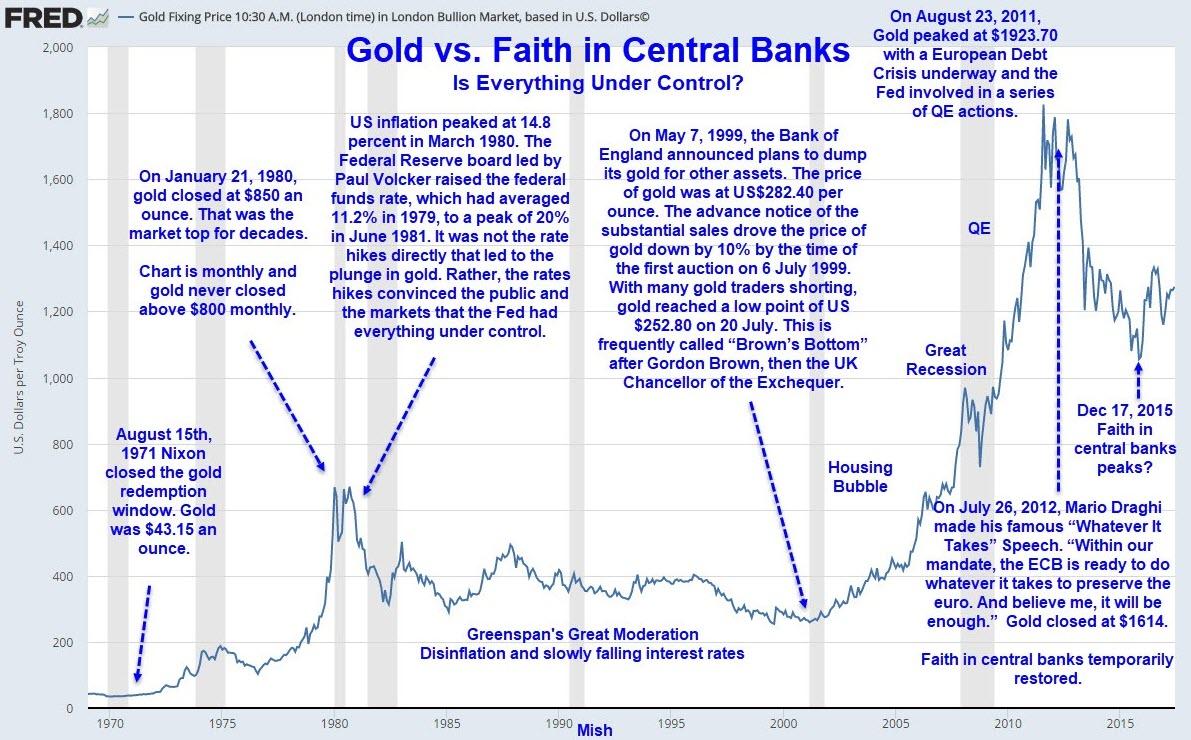

As I have pointed out numerous times, and contrary to popular belief, gold is not an inflation hedge. Gold fell from $800 to $250 with inflation every step of the way.

Rather, gold is a measure of faith in central banks that everything is under control.

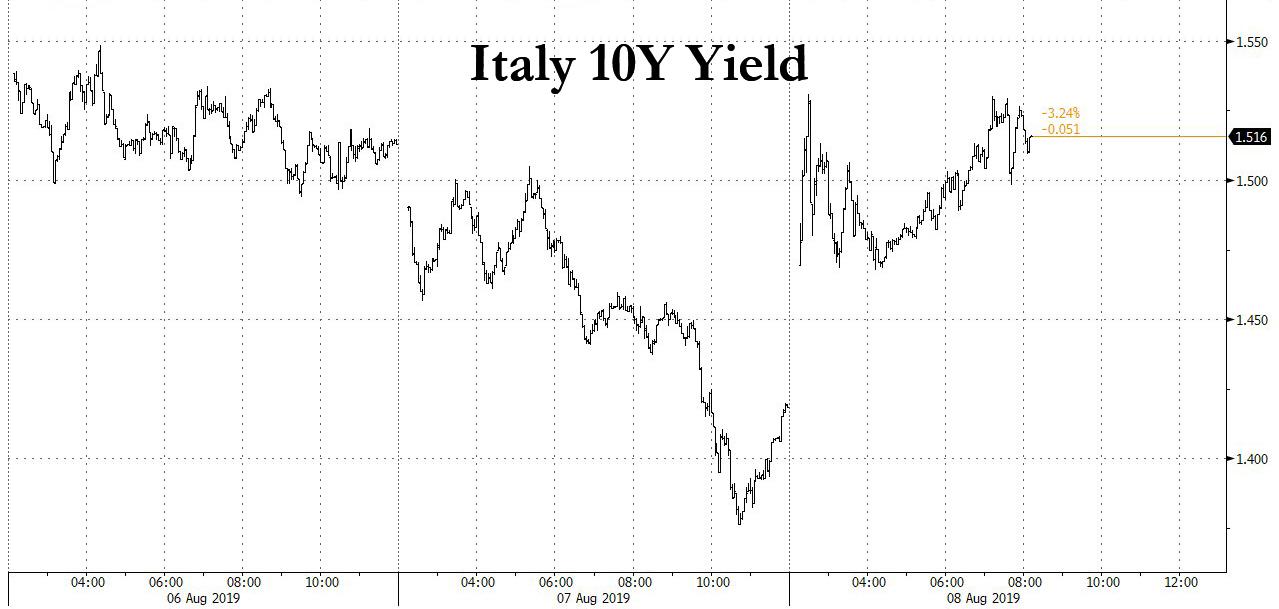

Italy is about to have an express date with political chaos again.

Overnight, Italian bond yields spiked following the latest media reports that Deputy PM, and Italy’s defacto leader, Matteo Salvini had issued a Monday ultimatum to shake up the cabinet and threatened that if his partners in the Five Star Movement don’t yield to his demands he’ll dissolve the government.

“I’m not one for half measures, either we can do things fully and well or I am not one who clings on to his seat,” Salvini said on Wednesday at a rally in the coastal town of Sabaudia. “Something has broken down in recent months,” he added, referring to the coalition.

Something that has not broken down in recent months has been Italian bonds, whose yields have bizarrely been tumbling despite the lack of ECB support, although overnight it emerged just who was the buyer of first and last resort was when Bloomberg reported that Japanese investors bought the largest amount of Italian sovereign bonds since at least 2005 in June; purchases of Italian government securities climbed to 278.8b yen ($2.6b), the highest since comparable data became available in 2005, according to Japanese balance-of-payments released Thursday.

And while we issue our sincerest condolences to Japanese pensioners who will eventually be repaid in Italian lira, there was some turmoil overnight in the Italian bond market following the Salvini ultimatum, with 10Y yields jumping by 10bps…

Source: Bloomberg

… while “lo spread”, or the 10-year yield premium over Germany climbing to the widest level in a month. It rose by as much as nine basis points to 2.09% before paring the increase to four basis points.

Source: Bloomberg

While hardly new, threats from Italy’s de facto leader to his Five Star government alliance “partners” have been escalating in severity in recent days, urging that either they stop trying to delay his agenda or he’s ready to pull the plug on the government and try to force early elections. Salvini, the League party leader, has called for deep tax cuts and investments, even if they fall afoul of European Union rules.

Salvini supporters have been pushing him for months to ditch the coalition as the League’s poll numbers approach 40%, a result that could allow it to govern on its own, and would likely result in another bond quake in Italy a la late 2018.

As Bloomberg adds, the deputy premier on Wednesday canceled rallies at beaches south of Rome as he preferred to stay in parliament and huddle with advisers and colleagues. In the evening he held a long meeting with Prime Minister Giuseppe Conte and has since called off events scheduled for Thursday. Conte has reportedly canceled events on his schedule for Thursday as well, suggesting he is about to make a major announcement, which could well mean the end of Italy’s government.

And speaking of the ultimatum, Salvini has given the prime minister until Monday to accede to his demands for changes in the cabinet or he could meet with Italy’s president to begin the process of breaking the government up, Corriere della Sera reported. The League leader is calling for the immediate ouster of Transportation Minister Danilo Toninelli. He’s also reported to be seeking to replace other cabinet members, notably Finance Minister Giovanni Tria.

There still may be some hope: in a Wednesday night speech, Salvini thanked Conte and fellow Deputy Premier Luigi Di Maio, who heads Five Star and with whom he has quarreled incessantly since the government was formed over a year ago. He also denied he is merely seeking more cabinet posts for the League and added that what happens next is “in the hands of the Italian people.”

“Like in marriage, if you spend more time quarreling and trading insults rather than making love, it’s better to look each other in the eyes and take an adult decision,” Salvini said, adding that decisions could be made “in the coming hours.”

Alas, that decision may well be a divorce: Italian bonds took another leg lower after reports that PM Conte was set to meet with President Mattarella, ahead of the coming government collapse and subsequent elections that will assure that Salvini is Italy’s undisputed leader, one who no longer need a coalition partner to govern.

via ZeroHedge News https://ift.tt/2MLYEsI Tyler Durden

Norway’s US$1-trillion fund – the world’s biggest sovereign wealth fund – sent shockwaves through global markets nearly two years ago when it said in November 2017 that it recommended the removal of oil and gas stocks – around US$35 billion worth of shares – from the fund’s equity benchmark index to make Norway’s wealth and economy less vulnerable to a permanent drop in oil and gas prices.

The initial proposal of the fund – which has amassed its vast wealth from none other than Norway’s oil and gas revenues and is therefore commonly referred to as ‘the oil fund’–was to dump all oil stocks from its portfolio, including significant stakes in Big Oil worth billions of U.S. dollars each.

Nearly two years later, after compromises and subsector changes in the index provider FTSE Russell that Norway uses as a reference, the initial proposal of dumping more than US$35 billion of oil stocks has been now narrowed down to stakes in purely exploration and production companies worth a total of less than US$6 billion – and also worth less than the fund’s stake in Shell alone.

Norwegian economists tell Bloomberg that the heavily reduced (not final yet) list of oil stocks for sale will likely have a very small effect and is reduced to a “symbolic” divestment, while Greenpeace’s finance campaign director for the Nordics, Martin Norman, described to Bloomberg the whittled-down proposal as “completely scandalous.”

The initial proposal shocked the markets as investors started questioning whether other major funds would follow suit and opt out of fossil fuels at a time when shareholders, investors, and environmentalists are increasingly pressing major oil companies to start taking climate change seriously and to prepare their business portfolios for a world of peak oil demand, whenever that may come.

After months of deliberations, Norway’s government proposed in March 2019 that the fund divest from 134 companies classified by the index provider FTSE Russell as belonging to the exploration and production subsector.

As at the end of 2018, the Norwegian fund held stakes in E&P companies—under FTSE Russell’s classification for such—with an approximate value of US$7.8 billion (66 billion Norwegian crowns).

To compare, as of the end of 2018, the fund’s total equity holdings in oil and gas firms had a value of US$37 billion, spread in investments in 341 companies, including just below 1 percent in each of Exxon and Chevron, 2.45 percent in Shell, 2 percent in Total, 2.31 percent in BP, and 1.59 percent in Eni. The stake in Shell alone was worth US$5.9 billion.

Now almost two years after the initial proposal, Norway is close to making the final decision on which companies it will dump from its sovereign wealth fund, but along the way, it has whittled the initial list down to a much smaller list of pure exploration and production companies, sparing all major integrated oil firms from divestment. A change in the categories of the FTSE Russell index provider as of July 1, 2019, further drops some of the oil companies from the ‘exploration and production’ category and moves them to ‘refining and marketing’, leaving the new category ‘crude producers’ as the companies Norway will likely target to divest.

According to Bloomberg calculations, the Norwegian fund held shares in the ‘crude producers’ category worth US$5.7 billion as of end-2018—less than the fund’s US$5.9-billion stake in Shell alone.

As per the ‘crude producers’ category in FTSE Russell, the fund may divest stakes in a number of U.S. oil producers, including Anadarko, Apache Corp, Chesapeake Energy, Concho Resources, Continental Resources, Devon Energy, Diamondback Energy, EOG Resources, Marathon Oil Corp, Murphy Oil, Occidental Petroleum, Pioneer Natural Resources—to name just a few of the drillers in the U.S. shale patch. As a whole, the ‘crude producers’ list is heavy on U.S. shale firms, Canadian oil producers with major oil sands operations, and companies exploring for oil in Africa.

While Norway’s currently planned divestment will likely have a negligible effect on global oil stock indexes, it will have an effect on those U.S. oil firms that will end up on the final list of stake sales.

While the overall effect of the world’s largest fund ditching oil stocks is likely to be insignificant for stock markets, it could be a significant step toward institutional investors increasingly reviewing their participation in the fossil fuel sector, as calls for divesting from oil and gas are set to only grow louder.

via ZeroHedge News https://ift.tt/2ZGXxOP Tyler Durden

In an event that we’re guessing will not have liberals grandstanding all over the media asking for a national knife ban, a 33-year-old Garden Grove man who was “full of anger” went on a “stabbing and robbery rampage” that lasted two hours on Wednesday night, according to Bloomberg. As a result, four people were killed and two others were left injured.

The man was taken into custody outside of a 7-Eleven in Santa Ana and relinquished both a knife, along with a handgun that he had stolen from a security guard.

Reports claim that the violence was “random”, with Garden Grove Police Lt. Carl Whitney stating that the man’s only motives seemed to be “robbery, hate, [and] homicide”. He also added that both the suspect and the victims were all hispanic.

Whitney stated: “We know this guy was full of anger and he harmed a lot of people tonight.”

Detectives are gathering evidence and interviewing the man in preparation for a court case. Lt. Whitney commented that security cameras also “caught some of the carnage”.

“We have video showing him attacking these people and conducting these murders.”

The owner of a bakery that the man robbed at about 4PM PST said: “He went directly to the register and tried to open the register … he showed me a gun. He took all the money and fled. I think I was very lucky because he thought I was a customer, not the owner.”

The man also robbed an insurance company and stabbed a 54 year old employee.

Lt. Whitney continued: “He was armed with some sort of machete knives when he confronted the woman. The woman was very brave. She fought as best she could.”

An alarm company caught the robbery happening live on video and called police. “They could see that the female victim was on the ground with blood and multiple injuries,” Whitney commented.

The killer then moved next door to a check cashing business, which he robbed. Shortly after 6PM, he attacked a man pumping gas at a Chevron station for no reason without robbing him. The man was stabbed in the back and nearly had his nose “severed off his face”.

A male employee of a nearby Subway restaurant was also fatally stabbed during a robbery.

Undercover detectives then tracked the killer’s Mercedes to the parking lot of the Santa Ana 7-Eleven, to find the man walking out of the store with a knife and a gun he had “cut from the belt of a security guard” after stabbing him. The killer reportedly stalked the guard walking into the store and stabbed him several times during an altercation.

The man lived in a Garden Grove apartment complex where he stabbed two men during a confrontation. Both men from the apartment complex died as a result of their injuries: one at the complex, the other at the hospital.

The attacks in both Garden Grove and Santa Ana took place at more than 6 places and lasted more than 2 hours. Two people who were injured were reported to be in stable condition and were expected to survive.

via ZeroHedge News https://ift.tt/2OKhdAf Tyler Durden

A quick case study on the power of expectations: On Monday, when the PBOC fixed the Yuan below 6.90 for the first time in 2019, well below consensus estimates, the offshore yuan collapsed, tumbling below 7.00 and as far as 7.10 for the first time since 2008, its biggest drop since the Aug 2015 devaluation and unleashing famine and pestilence across global capital markets. Then, on Thursday, one day after the comical fixing of 6.9996, the PBOC finally broke the seal, and set the daily reference rate of the yuan at 7.0039 per dollar, the first fixing weaker than 7.0000 in 11 years…

… but because the fix was a tad stronger than the 7.0156 rate estimated by analysts, the market took this as bullish and reacted with a relief rally sending S&P futures sharply higher from session lows.

And while China was quick to talk down the historic fix, and the market was clearly delighted by the fact that the fixing was not as worse as it could have been, the event was nonetheless momentous.

In a recent Bloomberg opinion piece, former UBS chief economist and China watcher George Magnus wrote “China allowing the yuan to slide below 7 to the dollar is a watershed moment for currency markets that’s symbolically equivalent to the U.S. and other countries abandoning the gold standard in the interwar period, or the collapse of the postwar Bretton Woods system of fixed exchange rates four decades ago. The implications for the global economy are equally significant.”

To be sure, the market has been eying the fix for insight on what constitutes a ‘comfortable’ level for the PBOC. UBS noted that although the PBOC has stepped up measures to slow the yuan’s pace of depreciation (including: introducing a larger counter cyclical factor, issuing central bank bills in Hong Kong to manage liquidity, pledging to keep the yuan stable) the market remains concerned about further weakening. “Today’s fixing is a clear message that China doesn’t mind letting its currency depreciate beyond any specific number, but would like to control the pace it weakens and mitigate market volatility as ‘stability’, which is PBoC governor Yi Gang’s main goal.” UBS believes that upward pressure on USDCNH is likely to persist in the near-term, as does Citi and SocGen, both of which expect the yuan to drift to 7.50 and lower against the USD.

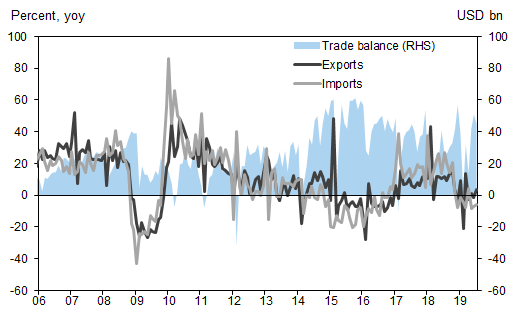

For now, however, China’s stronger than expected fix provided a brief comfort to markets, and global stock markets enjoyed a tentative recovery on Thursday after the PBOC print as well as better-than-expected Chinese export data. On the latter, China’s NBS reported that exports increased 3.3% yoy in July (USD terms), up from a decline of 1.3% yoy in June, and imports continued to soften, declining 5.6% yoy in July (v.s. -7.4% yoy in June). Both readings were above consensus expectations despite the Sino-U.S. tariff struggle.

In sequential terms, China’s exports rebounded 2.6% mom sa non-annualized in July, reversing a contraction of 0.9% in June. Imports went up by 2.6% mom sa non-annualized in July following two consecutive months of decrease. China’s trade surplus moderated to US$45.1bn in July from US$51.0bn in June. Exports to the US continued to contract by 6.5% yoy in July, and exports to Japan also declined 4.1% yoy. In contrast, exports to the EU rebounded 6.5% yoy in July from a decline of 3.0% yoy in June, and exports to ASEAN increased strongly by +15.6% yoy in July.

This was enough for the beaten down market to express some modest bullish sentiment overnight, and the MSCI world equity index rose 0.25%, led by Asia and Europe, even though it remains down more than 3% since the start of August.

Futures on all three of the main U.S. equity indexes advanced after the S&P 500 eked out a gain on Wednesday, although much of the gains have been pared as traders walk in to their desks.

The Stoxx Europe 600 also climbed for a second day, following Asia higher in early trade, led by tech and chemicals shares. European tech stocks lead gains, rising for a second day as investors bought into chip stocks and names which have lagged this year. The Stoxx Tech index rallied as much as 1.7%, led by chip maker AMS +3%, telecom carrier United Internet +2.5%, IT services co. Capgemini +1.9%, and Sweden’s Hexagon +2.1%. News that Japan has granted the first export license to South Korea also helped boost sentiment: “This is positive for the sector as this is one of the macro uncertainties (along with China-U.S.) with the potential to endanger a recovery,” Bankhaus Lampe analyst Veysel Taze said.

Earlier in the session, a gauge of Asia stocks increased as China’s Shanghai Composite rebounded from the lowest level since February. Asian stocks advanced for a second day, led by material firms, with most markets in the region up, led by Indonesia and Taiwan. Japan’s Topix slipped 0.1%, dragged by SoftBank Group and Takeda Pharmaceutical, after the yen extended gains against the dollar for a second day. The Shanghai Composite Index climbed 0.9%, driven by Kweichow Moutai and China Merchants Bank, as the nation’s July exports topped estimates. Chinese domestic equities are getting a boost in MSCI Inc.’s benchmark emerging-market indexes. India’s Sensex rose 0.8%, supported by HDFC Bank and Infosys, as investors weighed a bigger-than-expected rate cut against a less optimistic growth forecast by the central bank.

Emerging-market stocks headed for their first daily gain in 12 sessions, on track to end their longest losing streak in four years as investor concern over the yuan’s depreciation and the start of an all-out currency war faded. MSCI Inc.’s developing-nation equities index rose 0.9% after touching its lowest level since January earlier this week. “If the dovish pivot among global central banks manages to stay ahead of weaker growth data, risk and EM assets will likely find their feet even if USD/CNY stabilizes around a higher level,” Goldman Sachs strategists wrote in a client note.

Meanwhile, yields have continued to be volatile following the latest rate spasm which began when central banks in New Zealand, India and Thailand surprised markets on Wednesday with aggressive interest rate cuts. The Philippines followed suit and overnight the Monetary Board (MB) of Bangko Sentral ng Pilipinas (BSP) cut its key policy rates by 25bp, lowering the overnight borrowing rate, the overnight lending rate and the overnight deposit rate to 4.75%, 4.25% and 3.75%, respectively

“Financial markets are raising risks of recession,” said JPMorgan economist Joseph Lupton. “Equities continue to slide and volatility has spiked, but the alarm bell is loudest in rates markets, where the yield curve inverted the most since just before the start of the financial crisis.”

In response, markets ramped up their expectations for more easing by the U.S. Federal Reserve, but the question remains how fast Fed policymakers will move. Futures now price in a 100% probability of a Fed cut in September and a near 24% chance of a half-point cut. Some 75 basis points of easing is implied by January, with rates ultimately reaching 1%. Curiously, there is a non-trivial chance of an emergency, August rate cut.

In rates, U.S. government bond yields resumed their drop on Thursday, while in Europe German and French 10-year yields rose from record lows after a rally in recent sessions. The 10-year U.S. Treasury yield dropped to 1.7120%, although it reached a low of 1.595% on Wednesday.

Gold also benefited this week as investors scrambled to find somewhere safe to park their cash, rising above $1,500 for the first time since 2013. Spot gold was last at $1,498 per ounce, down from as much as $1,510 on Wednesday. Gold is up 16% since May.

In foreign exchange markets, the Japanese yen rose again, gaining 0.2% to 106.04 yen per dollar. China’s yuan also gained. In the offshore market it rose 0.2% to 7.0734 yuan per dollar after touching as high as 7.14 yuan on Tuesday. The Bloomberg Dollar Spot Index inched lower Thursday as the greenback fell against all G-10 peers. The biggest overnight gains were seen in Australia’s dollar, which rose from a 10-year low as risk appetite stabilized.

In commodities, oil prices regained some ground amid talk that Saudi Arabia was weighing options to halt its decline, offsetting an increase in stockpiles and fears of slowing demand. Brent crude futures climbed $1.25 to $57.48, though that followed steep losses on Wednesday, U.S. crude rose $1.46 to $52.53 a barrel.

Market Snapshot

S&P 500 futures up 0.2% to 2,885.75

MXAP up 0.3% to 151.68

MXAPJ up 0.8% to 489.77

Nikkei up 0.4% to 20,593.35

Topix down 0.08% to 1,498.66

Hang Seng Index up 0.5% to 26,120.77

Shanghai Composite up 0.9% to 2,794.55

Sensex up 0.7% to 36,927.55

Australia S&P/ASX 200 up 0.8% to 6,568.15

Kospi up 0.6% to 1,920.61

STOXX Europe 600 up 0.7% to 371.14

German 10Y yield rose 2.0 bps to -0.561%

Euro up 0.2% to $1.1223

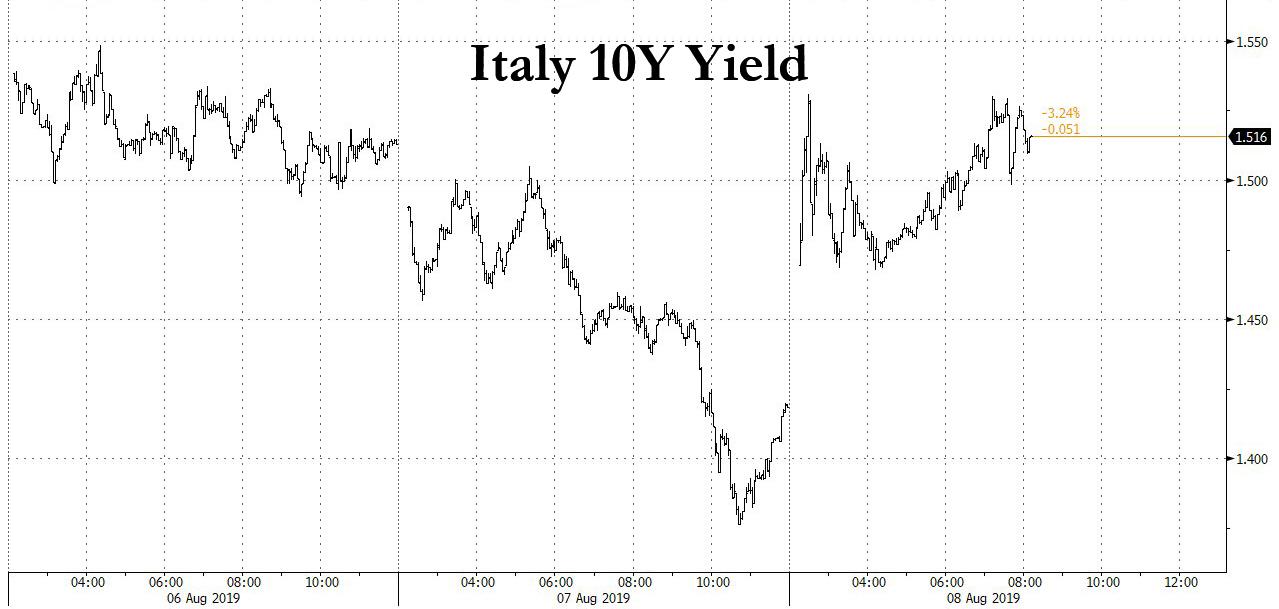

Italian 10Y yield fell 9.3 bps to 1.069%

Spanish 10Y yield rose 1.2 bps to 0.183%

Brent futures up 2.2% to $57.48/bbl

Gold spot down 0.2% to $1,497.66

U.S. Dollar Index little changed at 97.49

Top Overnight News from Bloomberg

The yuan steadied after China’s central bank set the daily fixing stronger than analysts expected, providing some reassurance to traders rattled by a tumultuous week in markets.

China’s export growth rebounded in July, and imports shrank less than forecast, signaling some recovery in trade just as companies brace for the arrival of new tariffs from the U.S.

The Trump administration is rushing to finalize a list of $300b in Chinese imports it plans to hit with tariffs in a few weeks’ time, as U.S. companies make a last-ditch appeal to be spared from the latest round of duties

China is mulling the biggest changes to its futures market since 2015, an overhaul that would give global investors unprecedented access, make it easier to execute bearish trades, and lay the groundwork for wagers on stock-market volatility

The global trade storm battering manufacturing in Europe’s largest economy is about to reach the labor market. German joblessness, which declined from one record low to the next for much of the past decade, is no longer falling and risks a reversal as workers endure the repercussions of the country’s factory slump

Deputy Premier Matteo Salvini increased pressure on Italy’s ruling coalition, reportedly giving Prime Minister Giuseppe Conte a Monday deadline to shake up the cabinet and indicating that if his partners in the Five Star Movement don’t yield to his demands he’ll dissolve the government.

The exodus from active funds has sent fees inexorably lower, led to the loss of thousands of jobs, forced large-scale consolidation among firms and pushed the industry to the brink of a shakeout that only the strongest will survive. Now, the $74 trillion industry, as measured by the Boston Consulting Group, is on the brink of a shakeout that only the strongest will survive

Large fluctuations in currency and stock markets are not good for the economy, Japanese Finance Minister Taro Aso said

Oil rebounded from the lowest level since January after Saudi Arabia contacted other producers to discuss options to stem a rout that’s been driven by the worsening U.S.-China trade war

Asian equity markets gained as a firmer than expected PBoC reference rate setting and Chinese trade data helped the region shake off the initial tentativeness following the tumultuous day on Wall St, where stocks staged a dramatic intraday recovery and although the DJIA closed in the red, it posted its largest rebound YTD. ASX 200 (+0.7%) was initially subdued amid losses in its top weighted financials sector following earnings from AMP Capital and Insurance Australia Group but then conformed to the improved risk tone led by gold miners after the precious metal rallied above USD 1500/oz for the first time since 2013, while Nikkei 225 (+0.4%) was underpinned by currency flows and KOSPI (+0.6%) outperformed after Japan approved some exports of tech materials to South Korea for the first time since curbs were imposed last month. Hang Seng (+0.5%) and Shanghai Comp. (+0.9%) were positive with sentiment underpinned by relief after the PBoC announced the reference rate which was set beyond the 7.0000 level for the first time since 2008 but not as weak as expected, while participants also digested Chinese trade data which topped estimates across the board and still showed a significant, albeit narrower imbalance in US-China trade. Finally, 10yr JGBs were initially lower with mild pressure seen amid the improved risk tone in the region, although prices then returned flat with support seen amid firmer demand at the 10yr inflation-indexed auction.

Top Asian News

China Plans Biggest Futures Market Overhaul Since 2015 Clampdown

Philippine Central Bank Cuts Interest Rate as Economy Slows

Shady Japan Bond Sale Practice Returning as Yields Fall

Major European stocks are higher across the board [Eurostoxx 50 +1.1%], following on from a positive Asia-Pac handover after optimistic Chinese trade data lifted sentiment in the region. Indices are posting broad-based gains, although UK’s FTSE 100 (+0.1%) lags its peers amid a slew of large cap ex-divs. Sectors are also in positive territory, although defensive sectors are somewhat lagging. Looking at individual movers, Adidas (-1.3%) shares opened lower by over 2% as investors for weeks sought an upgrade to guidance, particularly after its rival Puma (+2.5%) raised its sales and profit forecasts recently. Sticking with the DAX, Thyssenkrupp (+3.3%) shares rose despite an EBIT guidance cut as investors shifted focus to its elevator division IPO (expected in FY19/20) and expression of interests for other divisions. Finally, Osram Licht (-6.6%) slumped to the foot of the Stoxx 600 after the Co’s largest shareholder rejected the EUR 3.4bln takeover offer form Bain & Carlyle. It’s also worth noting that Goldman Sachs has downgraded trade sensitive sectors (EU autos and basic resources) in light of the recent developments between US and China, although individual stocks are little swayed by the broker update.

Top European News

Thyssenkrupp Open to Selling Divisions, Cuts Profit Outlook

The Inside Men Who Johnson May Tap for a More Understated BOE

Aviva Reviews Asia Unit as New CEO Tulloch Starts Turnaround

Novozymes Finance Chief Makes Sudden Exit as Outlook Darkens

In FX, the Dollar is on a softer footing against its G10 rivals, and most EMs amidst another revival in broad risk appetite, prompted in part by Chinese trade data that beat consensus across all key components and offset or appeased concerns over the ongoing incline in the Usd/Cny reference rate. However, the index is still straddling 97.500 and from a technical perspective holding above key Fib support at 97.392 on a closing basis, if not intraday, and it remains to be seen if the latest upturn in sentiment proves more sustainable or transitory like on Tuesday.

AUD/NZD/GBP/CAD – In keeping with the improved risk tone noted above, Aud/Usd has turned full circle and a bit more from midweek session lows towards 0.6800, but unlikely at this stage to reach hefty expiry options residing between 0.6840-50 (1.2 bn), while Nzd/Usd is still underperforming within 0.6468-35 parameters following more dovish RBNZ rhetoric on balance after yesterday’s double-barrelled ½ point OCR cut. Elsewhere, Cable is back around 1.2150 and the Loonie has rebounded through 1.3300 along side crude prices ahead of Canadian house price data.

JPY/EUR/CHF/XAU – The safer-havens are off best levels, but interestingly and perhaps tellingly still relatively bid as the Yen contains losses below 106.00 to circa 106.30 with decent option expiry interest likely to cap further upside in Usd/Jpy given 1 bn running off from 106.45-55. Similarly, the single currency is holding above 1.1200, but also likely to be stymied by expiries as 2.4 bn awaits between 1.1230-40, while the latest ECB monthly bulletin is far from Euro supportive given a downbeat assessment of the Eurozone economy and outlook, albeit largely a repetition of President Draghi’s post-policy meeting text. Elsewhere, the Franc is pivoting 0.9750 and Gold is rangebound either side of Usd1500/oz.

EM – The Rand continues to underperform with Usd/Zar mostly above 15.0000 after recent technical breaks to the upside and with weaker than forecast SA mining data not helping.

RBNZ Assistant Governor Hawkesby said outlook for rates is more balanced after 50bps cut but added there is still some probability OCR will need to be reduced further, while Hawkesby also stated the central bank are watching inflation expectations closely and that unconventional tools are a contingency in the event inflation tanks although they would need to exhaust conventional policy tools first. (Newswires)

In Commodities, a day of consolidation for the oil complex thus far after yesterday’s wave of downside in which the benchmarks declined almost 5% as demand concerns continue to materialise. WTI and Brent prices have rebounded off worst levels and reside around 52.23/bbl and 57.14/bbl respectively at the time of writing (vs. yesterday’s lows of 50.55/bbl and 55.90/bbl). The recent trade-induced sell-off has caught the attention of Saudi officials who are reportedly looking at options to stem the decline in the oil market. At the moment, no details of potential actions were mentioned, although desks note that anything else other than compliance control and further output cuts could be unrealistic, even then, reaching an OPEC+ consensus on further curbs could prove difficult given the debacle at the June meeting between the producers. Nonetheless, the media reports have seemingly underpinned the benchmarks for now. Elsewhere gold prices are tentative, albeit off its 6-year peak of 1510/oz and back below the psychological figure. Protectionism risk remains in the forefront for the yellow metal with trade sources noting that China expects the 10% levy on Chinese goods to be implemented on September 1 and thereafter be ramped up to 25% as China stands firm. Meanwhile, copper prices are flat on the day amid the cautiousness in the market, although the red metal did receive some short-lived impetus to test 2.60/lb to the upside as Chinese trade data topped estimates across the board, however, iron ore prices failed to benefit from the data amid ongoing supply glut and lower demand concerns. Finally, nickel prices surged over 10% overnight due to speculation that Indonesia could reel in an export ban on nickel ore in a regulatory move, although an official announcement is yet to be made.

US Event Calendar

8:30am: Initial Jobless Claims, est. 215,000, prior 215,000; Continuing Claims, est. 1.69m, prior 1.7m

9:45am: Bloomberg Consumer Comfort, prior 64.7

10am: Wholesale Trade Sales MoM, est. 0.2%, prior 0.1%; Wholesale Inventories MoM, est. 0.2%, prior 0.2%

DB’s Jim Reid concludes the overnight wrap

A couple of days left before a 2-week break for me and a period where I won’t be able to use the excuse that I can’t look after the children as I have work to catch up on. Well unless the trade war goes even further into overdrive! Holidays are always a bit of a culture shock for me in that regard as the terrors are full on and very demanding. Work is mentally demanding but childcare is physically and mentally demanding. I’m quite happy to sit on an exercise bike for an hour but when there are three nappies to change with them all moving in opposite directions (and wriggling when you catch them) then that is harder. August is always hectic for me as I hunker down and finish off writing the annual long-term study. I’ve been sending my team on various wild goose chases this week in terms of researching stuff so an open apology to them all. If you have any theories about how the global debt mountain develops over the next several years feel free to offer up your pearls of wisdom or send me in the direction of must read material. Although to be honest I probably should have asked this at the beginning of the process a few weeks back rather than 2 days before my holiday. Better late than never.

Talking of better late than never, US equities again bounced as yesterday’s session wore on mirroring the pattern from Tuesday. S&P 500 and Nasdaq futures were down -1.83% and -1.54% ahead of the New York open, but subsequently traded higher throughout the day to end +0.08% and +0.38%, respectively. Fixed income markets saw similarly sharp swings, with the 2y10y treasury curve flattening as much as -4.4bps to a new cycle low of 7.1bps at one point. The move was driven by a further sharp rally in the long end, with 10-year yields dropping as much as -10.9bps, as two-year yields fell a more modest -8.1bps. At one point, 30-year yields dipped below the fed funds rate to 2.122%. However, yields roared back alongside equities and 10-year bonds reversed all gains and actually ended +0.8bps higher, partially a reflection of improved sentiment and partially as a result of weak auction demand for fresh 10y paper. That auction tailed 1.6bps, despite being sold at the lowest yield since 2016 at 1.670%. The 2y10y curve ended just -0.2bps flatter in the end at 11.4bps

As for the improvement in sentiment yesterday, there wasn’t a single clear catalyst which makes sense if you look at the steady reversal higher all session. An article from the South China Morning Post used relatively optimistic language and said that “insiders on both sides expect September’s trade talks to go ahead,” which helped investors anticipate at least the potential for a trade war deescalation. On the other hand, the White House posted a rule effectively banning government agencies from purchasing equipment from five Chinese firms, including Huawei. The Huawei issue is likely still a major sticking point alongside the tariff subject. While the rule won’t have a large immediate impact, it will ban the US government from doing business with companies that separately do business with Huawei, making the measure a backdoor ban on many firms maintaining relationships with the sanctioned Chinese tech firm.

Over in Europe, bond markets shut before the rebound for risk, leaving closing prices there at fairly eye-watering levels. Benchmark 10y Bunds broke through -0.60% for the first time ever and closed -4.5bps lower at -0.581% yesterday. The entire Bund curve is negative again, with 30y Bunds now trading at -0.095%. To think it started the year at 0.875%. The cash price of that 2048 Bund is now 139.6 which means it is up around 30pts in cash terms alone in 2019. Curve flattening is also accelerating in Europe with the 2s10s Bund curve now at 26.9bps and the lowest since the GFC. Here in the UK we also saw the 2s10s curve get to just 2.7bps. Yields were 5-10bps lower elsewhere in Europe. Amazingly Spain and Portugal now trade inside of 0.20% and are racing towards zero. The amount of negative yielding debt unsurprisingly hit a new high given the moves yesterday at $15.62tn.

As for Austria’s 100 year bond, this security deserves its own paragraph. Since October, it has gone from a cash price of 107.3 to 191.6. It was also as “low” as 148.7 in mid-July. So that’s a rough return of +79% in ten months and +29% in four weeks. That takes its year-to-date gains to +64.40%, making it, to our knowledge, at or around the best performing asset of the year so far, better than the December Dalian iron ore future (+46.50%), Jamaica’s JSE index (+40.38%), Greece’s ASE index (+36.57%), and gold (+16.79%).

Oh and if you want to buy a UK 30 year inflation linked bond at the moment, your yield will be -2.08%. That’s their lowest levels ever.

The fixed income repricing also saw Fed Funds contracts move to price in 66bps of cuts by year end and 108bps by the end of 2020, though, in line with other moves, those were 9bps off their intraday highs. The various dovish central bank actions around the world yesterday obviously played a big role in the price action including the 50bp cut by the RBNZ (25bps more than expected), 35bps by the RBI (10bps more than expected), 25bp cut by the BoT (25bps more than expected) and 50bps cut by Belarus (might be the first mention for the country in the EMR). Today we have the Philippines and Peru rate decisions so we’ll be keeping an eye on whether the aggressive global easing trend continues.

Away from fixed income, European equity markets were initially playing catch up to the late gains on Wall Street on Tuesday but bourses did fade towards the end with the STOXX 600 eventually closing +0.24%. WTI oil prices slid -2.57% after US inventories data again disappointed, with a 2.3mn increase in stockpiles instead of the expected -2.5mn drawdown. However, prices did end a bit off their lows after Saudi Arabia said that they are considering all options to arrest the commodity’s price decline. WTI is now reversing these losses (+2.92%) this morning on news that Saudi Arabia has contacted other producers to discuss options to stem the rout. Gold crossed the $1500 level before ending +1.58% at $1497.78 yesterday. EM was mixed with the MSCI EM index gaining +0.45%, while the Turkish was up +0.58% against the dollar. The South African rand underperformed, falling -0.81%, likely harmed by headlines from the central bank governor that “we are not there yet” in terms of needing an IMF bailout. Not the cast-iron denial that perhaps investors wanted to hear.

After all that Asian equity markets are trading up this morning following Wall Street’s long climb from the lows last night with the Nikkei (+0.55%), Hang Seng (+0.67), Shanghai Comp (+0.91%), and Kospi (+0.96%) all advancing. Korean markets are also getting helped by the news that Japan has allowed exports of some semiconductor manufacturing materials to South Korea, the first such approvals since Japan tightened export controls in July. The Chinese onshore yuan is trading up this morning at 7.0430 (+0.24%), helped by the PBoC setting the daily reference rate at 7.0039 (vs. 7.0156 expected). This is encouraging a belief that the PBoC want a very controlled currency move even if they are slowly devaluing. Elsewhere, futures on the S&P 500 are up +0.44%.

We’ve also had the July trade numbers out of China where exports rose surprisingly by +3.3% yoy (vs. -1.0% yoy expected) while imports dropped -5.6% yoy (vs. -9.0% yoy expected) bringing the trade balance to $45.06b (vs. $42.65b expected). In terms of trade with the US, exports in July were down -6.5% yoy (YtD -8.2% yoy) while imports came down -19.1% yoy (YtD -28.3%) bringing the July trade balance to c.$28b (-0.41% yoy) and YtD trade balance at $168.3bn (+3.88%). So an expanding trade surplus with the US before the latest trade tensions. Interestingly the trade surplus increased with the EU perhaps suggesting more of their exports being switched there.

In other newsflow yesterday, President Trump delivered yet another salvo against the Fed via Twitter. He said that “Our problem is a Federal Reserve that is too proud to admit their mistake of acting too fast and tightening too much (…)They must Cut Rates bigger and faster, and stop their ridiculous quantitative tightening NOW.” Of course, the Fed already did cut rates last month and already ended its balance sheet runoff, effective last week. Trump went on to say that “Yield curve is at too wide a margin” which may be a reference to the flat curve. Whatever the intention behind the tweets, they unequivocally raise the pressure on the Fed.

As for actual Fedspeak yesterday, the only remarks came from Chicago President Evans, who said that “ inflation alone would call for more accommodation than we’ve put in place with just our last meeting” and said that on top of that, “risks now have gone up.” He, like his fellow dove Bullard yesterday, said that he had expected two 25bps rate cuts this year when he submitted his dot in June, but seemed to indicate that he favours more accommodation now.

Elsewhere, Italy’s Deputy Premier Matteo Salvini hinted yesterday that if his governing coalition partners M5S don’t yield to his policy demands then he could decide shortly to dissolve the power-sharing arrangement with his League party. He said, “I am not one for half measures, either we can do things fully and well or I am not one who clings on to his seat,” while adding, “something has broken down in recent months,” referring to the coalition. This morning Corriere Della Sera is reporting that Salvini, in a meeting with Prime Minister Conte, threatened to bring government down if some ministers aren’t replaced which includes Finance Minister Tria. The story also adds that Salvini has given Conte until Monday to act, after which he could meet with Italian president in the first step of breaking up government.

Finally to the day ahead, which is another painfully quiet one for data, with the only releases due in the US including jobless claims and the June wholesale inventories figures. Away from that there are central bank meetings due in the Philippines and Peru while Uber will report earnings.

via ZeroHedge News https://ift.tt/2YX7XZu Tyler Durden

Sen. Josh Hawley (R–Mo.) has taken a lot of heat for a recent proposal to ban autoplay videos in the name of stopping “social media addiction.” But Hawley’s new “SMART Act” may not even the nuttiest tech bill to grace Capitol Hill this year.

From the “Bot Disclosure” and “Biased Algorithm Deterrence” Acts, to net neutrality for speech on social media, new ways for the feds to snoop on user data, and a bill that could kill the teen YouTube star, legislative proposals from both Democrats and Republicans display a fundamental ignorance of the internet coupled with a willingness to micromanage even the smallest aspects of digital data and design. Here are six of the worst.

Hawley’s idea of “protecting children from online predators” is to prohibit social media from recommending any videos that feature anyone under age 18. Teen video makers couldn’t rely on algorithms to recommend any of their content. Sites like Facebook would be prohibited from recommending family videos featuring children to grandma and grandpa.

Across the board, the bill—introduced in June—would make it illegal for any computer service “that hosts or displays user-submitted video content, and makes recommendations to users about which videos to view,” to “recommend any video to a user of the covered interactive computer service if [the company] knows, or should have known, that the video features 1 or more minors.”

The so-called “Biased Algorithm Deterrence Act” would discourage web services from displaying content in anything but chronological order. Under Gohmert’s bill, any “social media service that displays user-generated content in an order other than chronological order, delays the display of such content relative to other content, or otherwise hinders the display of such content relative to other content” could face huge criminal and civil liabilities.

The bill, introduced back in January, would amend the federal law known as Section 230 to say that doing any of the above or otherwise using algorithms to determine how third-party content is displayed makes a company legally liable for that content. Users would have no choice in how content on the apps and sites they use would be displayed.

Feinstein’s bot bill, introduced last month, alleges that in order “to protect the right of the American public under the First Amendment,” candidates and political parties would be barred from using any “automated software program or process intended to impersonate or replicate human activity online” (it’s not quite clear what precisely that means) and that everyone must disclose to the federal government the use of any such software. The Federal Trade Commission FTC would be in charge of setting specific rules for the disclosure of this activity.

For now, the bill lays out this somewhat confusing guidance: the FTC will require “a social media provider to establish and implement policies and procedures to require a user of a social media website owned or operated by the social media provider to publicly disclose the use of any” so-called bots. People running such accounts would have to “provide clear and conspicuous notice of the automated program in clear and plain language to any other person or user of the social media website who may be exposed to activities conducted by the automated program.” And companies would have to develop tools to help people disclose bot status, as well as “a process to identify, assess, and verify whether the activity of any user of the social media website is conducted by an automated software program or process.”

The result would likely be a huge crackdown on the automated scheduling tools that many organizations and people use in perfectly benign ways all the time–all in the name of avoiding a small number of malicious actors who certainly aren’t going to play by the U.S. government’s bot-labeling requirements anyway.

This June bill from Hawley is ostensibly about preventing online “censorship,” but “ESIC” would actually put the Federal Communications Commission in charge of determining what constitutes politically neutral content moderation and link curation, and it would deny Section 230 legal protections to large companies that don’t fit the bill.

If ESIC passes, companies would be discouraged from investigating and filtering out abusive, hateful, threatening, defamatory, or otherwise objectionable content, and would instead be incentivized to simply delete content flagged by any other user, regardless of what rules or norms the content did or did not violate. Check out my recent article on Section 230 for more on how the law works and why Hawley is wrong about it.

Gosar’s as-yet-untitled bill was introduced on July 25 and still has no full text. But judging from his statements about it, we can expect it to be moderately-to-extremely dumb. In tweeting about the bill, Gosar doesn’t even accurately describe the law it’s meant to modify, claiming that Section 230 makes some sort of distinction between “platforms,” which are allowed “discretion for removing content,” and “publishers,” who are not allowed this discretion because “they monetize their users’ content.” This is not accurate.

Gosar goes on to say his bill would tweak language in Section 230 that makes it explicit companies can “restrict access to or availability of material that the provider or user considers to be obscene, lewd, lascivious, filthy, excessively violent, harassing, or otherwise objectionable.” He says it would revoke the part about “objectionable” material. This bit gives companies broader protection for content moderation efforts than they might have if only permitted to moderate based on obscenity, violence, or harassment.

Under Gosar’s vision of social media regulation, there would basically be two settings for social-media users: see everything, or stay on a strictly G-rated version of the internet. Users could choose, Gosar tweeted, between “a self-imposed safe space, or unfettered free speech.”

Warner’s bill would define digital entities that profit off of user data as “commercial data operators” and require those with “more than 100,000,000 unique monthly visitors, or users” in the U.S. to regularly provide each user with an individual data valuation estimate. At least every 90 days, companies would have to share with each user “an assessment of the economic value that the commercial data operator places on the data of that user.”

The bill would also require these companies to report to the Federal Securities and Exchange Commission the aggregate value of user data, along with information on all data-sharing contracts with third parties and “any other item the Commission determines, by rule, is necessary or useful for the protection of investors and in the public interest.”

from Latest – Reason.com https://ift.tt/2M6qpNe

via IFTTT

Global stock markets have been wobbly after the Federal Reserve failed to impress and the trade war heated-up. Combined with the weakening global economic outlook, there are not many reasons for stocks to rally.

Many are also wondering about the direction of the economy and markets, and for good reason. Although the Eurozone economy is close to imploding, the U.S. economy has produced decent growth numbers. Still, the underlying economic weakness is visible in the falling figures of Purchasers Managers surveys (PMIs) also in the U.S.

As we explained in our June forecasts, stopping the deterioration in economic conditions across the globe would require massive new stimulus programs from the major central banks and China. All of these have failed to materialize, and it is now getting late.

With the considerable increase in trade tensions, the situation in the global economy is becoming dire. Here we briefly explain what to expect.

China, China, China

Our subscribers have been continually briefed on the role China has played in the current expansion since September 2017. Our in-depth analysis of the global economy revealed the true source of global growth after 2009: The Chinese debt machine.

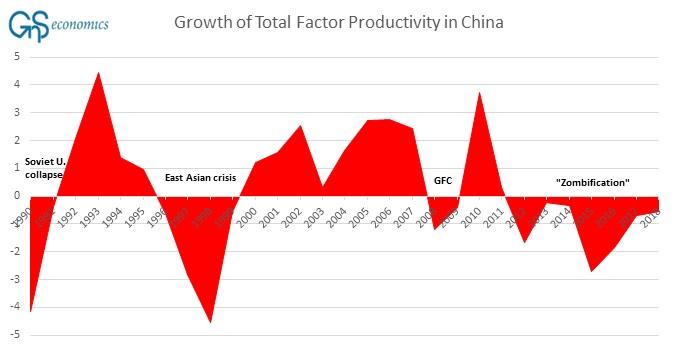

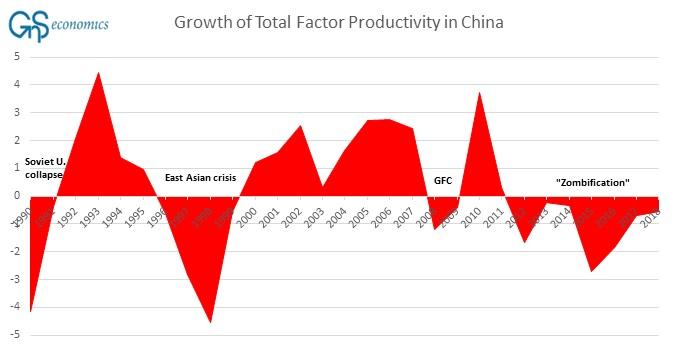

To our amazement, we found that not only has China been responsible for about 55 % of all credit created globally, but also close to 52% of all capital investments in major industrialized nations since 2009. Moreover, China had accomplished all this with a never-before-seen debt binge and investments through (mostly unprofitable) state-owned enterprises, which have led to a collapse of productivity growth (see Figure 1). As a result, China currently has a very high share of “zombie companies” (see, e.g., our blog).

Figure 1. Growth (%) of total factor productivity in China. Source: GnS Economics, Conference Board

As we speculated prior to the 19th Congress of the Communist Party of China in October 2017, the policies of China changed quite drastically after the Congress. In 2015/2016, the Chinese leadership organized a massive stimulus program through the ‘shadow banking sector’. It not only stimulated the global economy, but also pushed the debt-to-GDP ratio to astronomical levels.

Chinese leadership almost certainly understood the unsustainability of such policies very well, enacting a policy of deleveraging immediately after the Congress. OECD leading indicators testify that the slowdown of Chinese economy had, in fact, already started in the fall of 2017 (see the June forecast for details).

This policy removed crucial support from the global economy slowly but surely, pushing other economies down. Without the massive deficit-spending programs enacted by President Trump, a recession would probably have started in early 2018 (see our blog).

Late 2018 and early 2019 gave us a glimpse of the likely new economic policies of China. At that time China launched brief, but gigantic (record-breaking) debt and fiscal stimulus programs. They lifted global markets and, combined with a drastic U-turn at the Fed, saved the U.S. equity markets in early 2019. However, Chinese leaders withdrew most of the additional stimulus measures in the second quarter. It thus looks like China is trying to manufacture a ‘soft landing’.

As we explained in our June forecasts, China has only limited effective additional means left to stimulate the economy. If it would use them fighting the current downturn, it would eventually lead to a hard landing (crash) of the economy. It’s very likely that Chinese leadership will try to avoid this. This, however, implies that global recession is unavoidable.

Pushing on a string (but hard!)

One cannot blame the central bankers for trying. They have left no stone in monetary policy unturned in their efforts to stimulate global growth. Unfortunately, these attempts have caused more harm than good.

We’ve been warning about the unintended effects of very low/negative interest rates and the asset- buying programs of the central banks since June 2013. In the March issue of our Q-Review, we explained why the ‘unconventional means’ of central banks have destroyed the global growth model that has governed the rise in our living standards for the past 200 years.

Now, the “jig” of central bankers is almost “up”. Their role as managers of global and regional economies has been founded on the concept that the short-term interest rates they set would be enough to stop recessions and control inflation—in short, to regulate economic outcomes in a positive way. Now we know this hypothesis to be false.

Very low and negative interest rates have wreaked havoc in the banking sector, seriously undermining the standard profit mechanism of banks (by crushing the margins of maturity transformation), and fostered the growth of zombie corporations. Negative rates also undermine the profitability of other levered financial institutions and fixed-income investors (see Q-Review 1/2018 for a more detailed account). Very low or negative interest rates also highlight the extraordinary nature of the present economic situation—most likely hurting sentiment among savers, private investors and corporations.

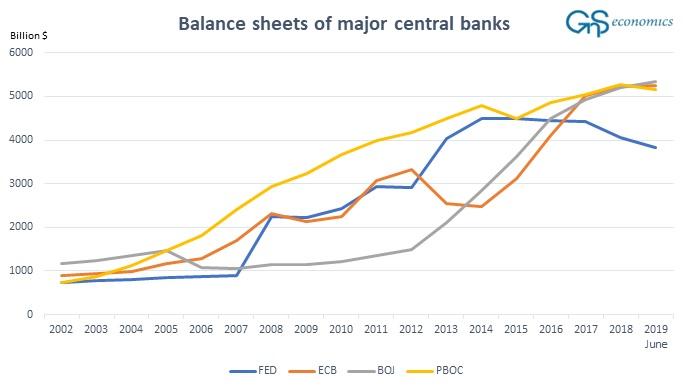

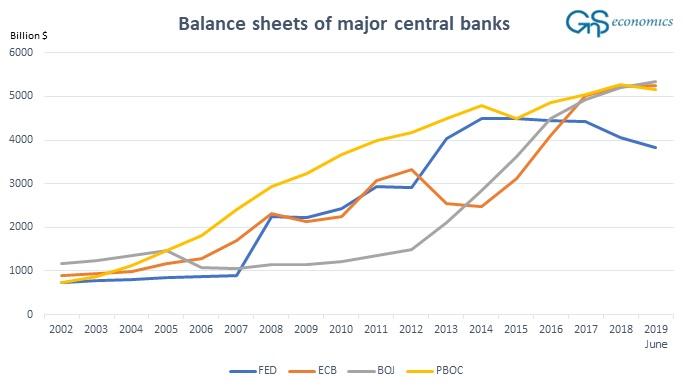

The bottom line is that central banks are effectively out of means to stimulate. Rates are low or negative everywhere. Central banks have loaded their balance sheets with government and corporate debt (see the Figure 2 below) and are now approaching their political limits.

Figure 2. The balance sheets of the Bank of Japan, European Central Bank, Federal Reserve and the People’s Bank of China in billions US dollars. Source: GnS Economics, BoJ, ECB, Fed, PBoC

If capital markets crash, the likelihood of the U.S. Congress accepting the bill for auditing the Fed is relatively high. The ECB, on the other hand, is bound by the strict Articles of the Treaty of the Functioning of the European Union (TFEU), and the German Constitutional Court.

Moreover, if a large country leaves the Eurozone and defaults on its ECB-held debt, the imperative to recapitalize the ECB could arise in short-order. This would also mean that the ECB has directly funded a member government, which is strictly forbidden by the Article 123 of the TFEU. Political and legal ramifications would likely be massive, and the Eurozone could shatter in the aftermath. Yet, many seem neither to recognize the looming political limits and risks faced by the major central banks nor their likely cataclysmic aftershocks.

In practice, central banks have only one potential ploy remaining. They could push interest rates even more deeply-negative, but this would only work if cash were banned. It’s highly unlikely that citizens in, for instance, Germany and in the U.S. would agree to this. Alas, central bankers are effectively “out of ammo”.

The King is dead (long live the King!)

China, not the central banks, saved the world economy from collapsing after 2008. The exceptional measures of central banks were crucial in the acute phase of the crisis, but after that phase had passed, they turned into a serious and dangerous drag on the global economy.

Now, with the ability of China to carry the world economy in irreversible decline, the “threat” of central bank intervention has been the only inoculation against a market crash. With the faltering response of the Fed to the demands of the markets in late July and the unimpressive posture of the ECB in early July, we thereby approach the point where markets call the bluff of central bankers. When that happens, a crash in capital markets is practically unavoidable.

Central bankers are not “masters of the universe” and they surely do not “have the back” of global capital markets. They are simply banks with the ability to earn seigniorage and to twist the accounting rules. Far from being “supermen” they are, in fact, mere mortals.

We have trusted the central banks to defend us in recessions and crises, and to generate economic growth and inflation. That time has now passed.

Thus, the “King” is dead, and any effort to resuscitate central bank hegemony will just make things worse. Unfortunately, whatever option policy makers choose after a decade of ill-advised policies, it will have dire consequences for us all.

via ZeroHedge News https://ift.tt/2Yy906x Tyler Durden

Sen. Josh Hawley (R–Mo.) has taken a lot of heat for a recent proposal to ban autoplay videos in the name of stopping “social media addiction.” But Hawley’s new “SMART Act” may not even the nuttiest tech bill to grace Capitol Hill this year.

From the “Bot Disclosure” and “Biased Algorithm Deterrence” Acts, to net neutrality for speech on social media, new ways for the feds to snoop on user data, and a bill that could kill the teen YouTube star, legislative proposals from both Democrats and Republicans display a fundamental ignorance of the internet coupled with a willingness to micromanage even the smallest aspects of digital data and design. Here are six of the worst.

Hawley’s idea of “protecting children from online predators” is to prohibit social media from recommending any videos that feature anyone under age 18. Teen video makers couldn’t rely on algorithms to recommend any of their content. Sites like Facebook would be prohibited from recommending family videos featuring children to grandma and grandpa.

Across the board, the bill—introduced in June—would make it illegal for any computer service “that hosts or displays user-submitted video content, and makes recommendations to users about which videos to view,” to “recommend any video to a user of the covered interactive computer service if [the company] knows, or should have known, that the video features 1 or more minors.”

The so-called “Biased Algorithm Deterrence Act” would discourage web services from displaying content in anything but chronological order. Under Gohmert’s bill, any “social media service that displays user-generated content in an order other than chronological order, delays the display of such content relative to other content, or otherwise hinders the display of such content relative to other content” could face huge criminal and civil liabilities.

The bill, introduced back in January, would amend the federal law known as Section 230 to say that doing any of the above or otherwise using algorithms to determine how third-party content is displayed makes a company legally liable for that content. Users would have no choice in how content on the apps and sites they use would be displayed.

Feinstein’s bot bill, introduced last month, alleges that in order “to protect the right of the American public under the First Amendment,” candidates and political parties would be barred from using any “automated software program or process intended to impersonate or replicate human activity online” (it’s not quite clear what precisely that means) and that everyone must disclose to the federal government the use of any such software. The Federal Trade Commission FTC would be in charge of setting specific rules for the disclosure of this activity.

For now, the bill lays out this somewhat confusing guidance: the FTC will require “a social media provider to establish and implement policies and procedures to require a user of a social media website owned or operated by the social media provider to publicly disclose the use of any” so-called bots. People running such accounts would have to “provide clear and conspicuous notice of the automated program in clear and plain language to any other person or user of the social media website who may be exposed to activities conducted by the automated program.” And companies would have to develop tools to help people disclose bot status, as well as “a process to identify, assess, and verify whether the activity of any user of the social media website is conducted by an automated software program or process.”

The result would likely be a huge crackdown on the automated scheduling tools that many organizations and people use in perfectly benign ways all the time–all in the name of avoiding a small number of malicious actors who certainly aren’t going to play by the U.S. government’s bot-labeling requirements anyway.

This June bill from Hawley is ostensibly about preventing online “censorship,” but “ESIC” would actually put the Federal Communications Commission in charge of determining what constitutes politically neutral content moderation and link curation, and it would deny Section 230 legal protections to large companies that don’t fit the bill.

If ESIC passes, companies would be discouraged from investigating and filtering out abusive, hateful, threatening, defamatory, or otherwise objectionable content, and would instead be incentivized to simply delete content flagged by any other user, regardless of what rules or norms the content did or did not violate. Check out my recent article on Section 230 for more on how the law works and why Hawley is wrong about it.

Gosar’s as-yet-untitled bill was introduced on July 25 and still has no full text. But judging from his statements about it, we can expect it to be moderately-to-extremely dumb. In tweeting about the bill, Gosar doesn’t even accurately describe the law it’s meant to modify, claiming that Section 230 makes some sort of distinction between “platforms,” which are allowed “discretion for removing content,” and “publishers,” who are not allowed this discretion because “they monetize their users’ content.” This is not accurate.

Gosar goes on to say his bill would tweak language in Section 230 that makes it explicit companies can “restrict access to or availability of material that the provider or user considers to be obscene, lewd, lascivious, filthy, excessively violent, harassing, or otherwise objectionable.” He says it would revoke the part about “objectionable” material. This bit gives companies broader protection for content moderation efforts than they might have if only permitted to moderate based on obscenity, violence, or harassment.

Under Gosar’s vision of social media regulation, there would basically be two settings for social-media users: see everything, or stay on a strictly G-rated version of the internet. Users could choose, Gosar tweeted, between “a self-imposed safe space, or unfettered free speech.”

Warner’s bill would define digital entities that profit off of user data as “commercial data operators” and require those with “more than 100,000,000 unique monthly visitors, or users” in the U.S. to regularly provide each user with an individual data valuation estimate. At least every 90 days, companies would have to share with each user “an assessment of the economic value that the commercial data operator places on the data of that user.”

The bill would also require these companies to report to the Federal Securities and Exchange Commission the aggregate value of user data, along with information on all data-sharing contracts with third parties and “any other item the Commission determines, by rule, is necessary or useful for the protection of investors and in the public interest.”

from Latest – Reason.com https://ift.tt/2M6qpNe

via IFTTT

In a potentially catastrophic escalation of tensions in the Persian Gulf, Russia plans to use Iran’s ports in Bandar-e-Bushehr and Chabahar as forward military bases for warships and nuclear submarines, guarded by hundreds of Special Forces troops under the guise of ‘military advisers’, and an airbase near Bandar-e-Bushehr as a hub for 35 Sukhoi Su-57 fighter planes OilPrice.com has exclusively been told by senior sources close to the Iranian regime. The next round of joint military exercises in the Indian Ocean and the Strait of Hormuz will mark the onset of this in-situ military expansion in Iran, as the Russian ships involved will be allowed by Iran to use the facilities in Bandar-e-Bushehr and Chabahar. Depending on the practical strength of domestic and international reaction to this, these ships and Spetsntaz will remain in place and will be expanded in numbers over the next 50 years.

This gradual roll-out of Russian capability in a country is the Kremlin’s tried and tested operating procedure for leveraging economic and/or political support for a country into that country allowing itself to be used as, effectively, one large multi-level forward military base for Russia. Exactly the same plan was used, and remains in place, in Syria, with Russia maintaining a massive army presence in and around Latakia, Syria, despite having repeatedly made assurances that it was to withdraw from this military theatre. In the early stages, these troops – again, in reality all Spetsnatz foreign operatives – appeared in the guise of military advisers and to provide ‘security staff’ for the huge Russian Khmeimim Air Base and the S-400 Triumf missile system in place in and around Latakia. This Russian presence was later duly expanded and formalised under an agreement signed with Syria in January 2017, which allowed Russia to continue its operations in Latakia and also to utilise the naval facility at Tartus for the next 49 years. This is precisely the format of agreement that has been agreed by Iran’s Islamic Revolutionary Guards Corp (IRGC) and Supreme Leader Ali Khamenei in the last few days, despite muted protest from the broadly pro-JCPOA (Joint Comprehensive Plan of Action) nuclear deal allies of President Hassan Rouhani.

Given how poorly Iran has fared in its recent dealings with Russia – most notably over its Caspian Sea oil and gas rights– Iran’s decision to go ahead with this latest deal may seem surprising to many but is the product of two key reasons.

First, Iran has no other choice of a potential geopolitical ally in its current fight against sanction-induced economic austerity and political marginalisation. There are only five Permanent Members on the United Nations Security Council: the U.S. (the prime mover against Iran), the U.K. and France (both toeing the U.S. line), China (whose support ebbs and flows according to its own agenda), and Russia. “If you have no means of getting food from the supermarket ten miles away then you have no choice but to shop at the store around the corner, no matter how crappy it is,” one senior Iran source told OilPrice.com last week.

The second reason is that President Rouhani and his broadly moderate pro-West, pro-JCPOA supporters have lost the confidence of many who voted for him due to his inability to deliver the economic prosperity that he promised would result from the nuclear deal agreed in 2015 and implemented on 16 January 2016. “This includes [Supreme Leader, Ali] Khamenei, who supported Rouhani for the first few years but now has no choice but to go along with the IRGC’s recommendations, and this Russia deal is at the forefront of these,” said a senior Iran source.

Why is the IRGC backing this deal with Russia, given that its senior personnel are extremely capable people and hardened military officers, well aware of the trouble that the deal could create on a global scale?

“Firstly, they [the IRGC] honestly believe that a corollary financial deal agreed with Russia last year is the only economic lifeline that Iran has that will stop it from falling into a popular revolutionary scenario, and the second reason is that some of the most senior figures in the IRGC also stand to gain monetarily by co-operating with Russia,” an Iran source told OilPrice.com last week.

The cornerstone deal in question was part of a wide-ranging 22-point memorandum of understanding signed by Iran’s deputy petroleum minister, Amir-Hossein Zamaninia, and Russia’s deputy energy minister, Kirill Molodtsov, at the time covering closer co-operation between the two countries across the board.

For the oil and gas sector, specifically, it involved Russia giving US$50 billion per year every year for at least five years so it could complete its top priority oil and gas projects to Western standards, which was estimated to cost around US$250 billion. Another US$250 billion would then be available for the following five years for Iran to build-out the remainder of its economy. In exchange for this, Iran would give Russian companies preference in all future oil and gas field exploration and development deals, to add to the seven already agreed at that time. These included: Zarubezhneft for Aban and Paydar-e Gharb, Lukoil for Ab Teymour and Mansouri, GazpromNeft for Changouleh and Cheshmeh-Khosh, and Tatneft for Dehloran. In addition – and crucial for what is now in view militarily – Iran also agreed to buy Russia’s S-400 missile defence system, to allow Russia to expand its number of listening posts in Iran, and to double the number of senior ranking IRGC officers that are seconded in Moscow for ongoing training, to between 120 and 130.

The deal also ensured that there was a clause not allowing Iran to impose any penalties on any Russian development firm for slow progress on any field for 10 years, including not being able to re-offer these fields in new bidding rounds even if no progress at all was being made. Over the 10-year period the Russians would have the right to dictate exactly how much oil was produced from each field (to the barrel), when it was sold (to the day), to whom it was sold (by company), and for how much it was sold (to the cent). “Added to this is the fact that within the contracts there was another killer clause: Russia had the right to be able to buy all of the oil – or gas – being produced from fields that their companies were supposedly developing at 55 to 72 per cent of its open market value, for the next 10 years,” said one of the Iran sources. In just the last week as well, Russia – despite it swindling Iran out of its arguably rightful share of Caspian Sea resources – has offered to extract oil and gas from Iran’s sector in the Caspian and sell supplies on in the international markets.

The other reason that has prompted the IRGC into allowing Russia to use Iran as a forward operating military base is that at least two of the most senior commanders have been given monetary inducements to champion Russia’s cause. This was also the reason why Iran ended up buying the inferior capability 28-year old S-300 missile system from Russia rather than the cutting edge new S-400 system.

“Russia told Iran that it didn’t actually need the S-400 system and that the S-300 system would be adequate for its needs, despite the S-300 system still costing in total US$7 billion – US$4 billion up front and US$3 billion when it was actually delivered – which was three times the cost that Russia charged Egypt for the better S-400 system,” said one of the Iran sources.

“At the same time, two of the key IRGC commanders who had allowed this deal to go ahead pocketed US$105 million each just from that one deal, and they and others get another cut of the US$50 billion per year deal if that fully re-emerges and of the newly-agreed Caspian deal,” he added.

As it stands, then, Russia not only has unfettered access to all of Iran’s onshore, offshore and Caspian Sea oil and gas reserves to sell on as it wishes, however it wishes, but also is set to secure two of the most strategically well-placed ports and surrounding areas in the world’s most sensitive oil and gas hotspot, giving it effective control over the Strait of Hormuz. The Strait, of course, remains the world’s most important oil transit chokepoint – and the key route from the Arabian Gulf to the Far East via the Indian Ocean – with roughly 35% of all seaborne oil and about a third of global liquefied natural gas supplies passing through it.

“Bandar-e-Bushehr and Chabahar will give Russia a potential stranglehold over the entire Persian Gulf area and into the Indian Ocean, which will allow it as well to conduct joint naval operations with China with more ease in the U.S. sphere of influence in the East, including around Japan, South Korea, and the Philippines,” a London-based intelligence analyst told OilPrice.com last week.

“The fact that Russia also intends to use these two ports not just for warships but for nuclear submarines as well when the waters in its more northern ports are frozen is significantly upping the Russian ante on the West in general and on the U.S. in particular,” he concluded.

via ZeroHedge News https://ift.tt/2YUff3S Tyler Durden

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}