It’s Fed day and I honestly can’t bring myself to repeat what was already said on Monday and Tuesday other than “Yes, the Fed will cut but it won’t be enough”. Instead, let us take a moment to contemplate several laws that seem pertinent to our current situation.

First, Gresham’s Law: that bad money drives out good. That used to be the measure of how far a government or a central bank could debase money before everyone hoarded the good stuff and circulated only less valuable coinage. Yet as we contemplate everyone slashing rates again, the opposite appears to be true: everyone is piling into bad and/or directly money-losing assets as benchmark rates decline! One could make the argument for gold, of course, given there is a clear desire to see currencies go lower on the part of central banks, even if they can’t openly say so. (They now leave that to the politicians, of course.) But USD is still, for now, a modern version.

Second, Say’s Law: supply creates its own demand. This is the “Just build and they will come!” hope as we re-embark on monetary policy previously reserved for extreme crisis: Of course, first you have to get them to build, not speculate on money-losing assets. And even then Say’s Law doesn’t hold true – you can and do get over-supply of goods relative to demand both in one market and in aggregate. Then we end up with all vs. all as sluggish economies parasite the consumers of others – all the more so if the central banks nudge-nudge wink-wink their currencies lower too.

Consider those laws and is it any surprise that as the US and China sit down to talk trade we see US President Trump tweet: “China is doing very badly, worst year in 27 – was supposed to start buying our agricultural product now – no signs that they are doing so. That is the problem with China, they just don’t come through. Our Economy has become MUCH larger than the Chinese Economy is last 3 years. My team is negotiating with them now, but they always change the deal in the end to their benefit. They should probably wait out our Election to see if we get one of the Democrat stiffs like Sleepy Joe. Then they could make a GREAT deal, like in past 30 years, and continue to rip-off the USA, even bigger and better than ever before. The problem with them waiting, however, is that if & when I win, the deal that they get will be much tougher than what we are negotiating now…or no deal at all. We have all the cards, our past leaders never got it!”

Meanwhile, a Bloomberg editorial today argues “Hong Kong is running out of time. Signs are building that the city’s political crisis is starting to affect its financial and business prospects…Hong Kong’s reputation for political stability, reliable institutions and effective governance was won over decades. Once lost, it will be hard to regain.” This, as it appears protestors arrested Sunday night are to be charged with rioting (maximum sentence: 10 years) whereas the ‘white-shirts’ who violently attacked protestors the previous Sunday have been released without charge or face much less serious offenses. Bloomberg also reports: “White House Eyeing Chinese Forces Gathered on Hong Kong Border”. That carries implications here that I don’t need to go in to.

But let me now bring in the third law – Godwin’s Law: as an online discussion grows longer, the probability of a comparison involving Nazis or Hitler approaches 1. Indeed, nowadays it usually takes no more than two Tweets to get to that accusation in most online interaction. What’s the relevance? There is a growing swell of anti-China opinion in US policy circles. Seasoned pro-China journeymen have been elbowed aside by younger, hawkish experts who sound even more confrontational that Trump: and some of them use Godwin-esque language. Yes, there are still voices in markets lobbying or pricing for US-China free trade winning out. But let’s rewind the clock and see what the economic debate looked like in the mid-1930s before Godwin.

As a recent Jerusalem Post editorial shows, US President F.D. Roosevelt–the progressive champion of the New Deal–had a pre-WW2 policy to maintain trade and diplomatic relations with Nazi Germany; the Treasury Department even permitted the Nazis to forego a “Made in Germany” label and instead mark goods as having been made in a particular city or region to confuse US consumers. The liberal establishment also shared that stance. Smith College’s president visited Nazi Germany in 1933 and found “no cases of mistreatment” of Jews; Barnard College’s dean toured Germany in 1935 and announced Hitler’s desire to acquire “new land” was “legitimate”; Vassar College’s president saw the boycott as a step toward war, and in 1934, organized a tour of Nazi Germany; and a Bryn Mawr professor similarly denounced the boycott as “simply war without bloodshed.”

Let me make myself abundantly clear: I AM NOT MAKING ANY COMPARISONS OF ANYONE TO HITLER! There is no Godwin goin’ on.

What I am trying to show is that Gresham’s Law matters for markets even in a world without coinage; Say’s Law is a nonsense that will make central banks ignoring Gresham’s Law create worse global imbalances that lead to geopolitical tensions; and hence as US policy hawks start to circle those who think we can avoid a trade rift between the US and China using highfalutin free trade arguments overlook the chequered history of such a principled stance. Anyway, something to think about while we wile away the hours waiting for the Fed.

via ZeroHedge News https://ift.tt/2LTVeoa Tyler Durden

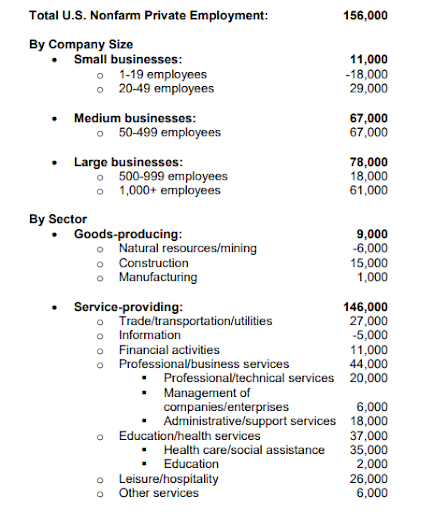

While The Fed has clearly veered from any data-dependence (aside from the level of The Dow), some still care about the state of the nation’s ‘real’ economy and today’s ADP was expected to rebound from dismal May and June data and its did with a better-than-expected 156k print for July.

“While we still see strength in the labor market, it has shown signs of weakening,” said Ahu Yildirmaz, vice president and co-head of the ADP Research Institute.

“A moderation in growth is expected as the labor market tightens further.”

Goods-producing jobs rose 9k while Services dominated once again, rising 146k in July, but notably very small businesses (1-19 employees) have seen job losses for three straight months…

Mark Zandi, chief economist of Moody’s Analytics, said, “Job growth is healthy, but steadily slowing. Small businesses are suffering the brunt of the slowdown. Hampering job growth are labor shortages, layoffs at bricks-and-mortar retailers, and fallout from weaker global trade.”

Goldilocks? Or enough bad data for Powell to cut?

via ZeroHedge News https://ift.tt/2KhPYr0 Tyler Durden

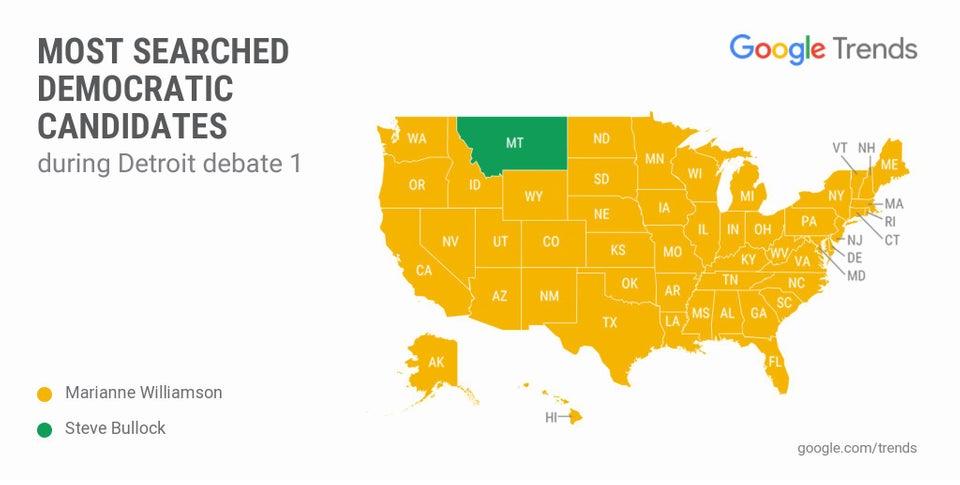

One word – “Racism” – dominated the first night of the second round of Democratic Party Presidential Nominee debates…

Former Democratic Colorado Gov. John Hickenlooper came in last with 8 minutes, 49 seconds of speaking time. The debate lasted for more than two hours. Here is a complete list of the totals:

Democratic Massachusetts Sen. Elizabeth Warren: 18:33

Independent Vermont Sen. Bernie Sanders: 17:45

Democratic South Bend, Indiana, Mayor Pete Buttigieg: 14:07

Democratic Montana Gov. Steve Bullock: 10:59

Former Democratic Texas Rep. Beto O’Rourke: 10:58

Democratic Minnesota Sen. Amy Klobuchar: 10:49

Former Democratic Maryland Rep. John Delaney: 10:31

Democratic Ohio Rep. Tim Ryan: 9:47

Author Marianne Williamson: 8:52

Former Democratic Colorado Gov. John Hickenlooper: 8:49

And despite having almost the least time and at one point appearing to almost yodel while warning of ‘dark psychic forces’…

Ten of the remaining Democratic Party presidential contenders faced off July 30 on the first night of the second primary debate. A definite split in ideology has emerged between those candidates who believe government should take a greater role in American life and those who believe government should take complete control of American life.

Sens. Bernie Sanders (I-VT) and Elizabeth Warren (D-MA) are defining themselves as candidates who oppose any policy that would result in a single cent of profit for the private sector. They believe that government – and only the government – should provide solutions to every problem. Health care dominated the evening’s discussion, and Sanders, in particular, became clearly irate when others on the stage spoke about solutions which involved private insurance companies.

Health Care Issue Reveals A Deep Divide

Montana Governor Steve Bullock, Ohio Representative Tim Ryan, Former Colorado Governor John Hickenlooper, and Senator Amy Klobuchar of Minnesota all acknowledged that the private sector has a role to play in providing coverage for health care. Each of these candidates recognized the numerous and significant negative consequences of doing away with private insurance.

It was John Delaney – the former Maryland representative – who really went after Sen. Sanders on the latter’s wildly idealistic proposals for universal health care. Like every other Democrat in the race, Delaney claims to support the idea that health care is a right but disputed the idea that the government should simply deprive 180 million Americans of their private insurance – most of those policies subsidized by employers.

As usual, Sanders came over as angry, strident, and completely intolerant of any idea that involved private citizens and corporations making money without government approval. His entire platform appears based on the idea that the government should provide everything and that any private enterprise generating a profit is, by definition, greedy and evil.

To the senator’s credit, he was the only Democrat on the stage advocating single-payer health care who admits that Americans will pay more in taxes to finance the system. Warren, Robert O’Rourke, and South Bend Mayor Pete Buttigieg all dodged the question, despite the moderators’ best efforts to get a straight answer.

The most hilarious moment of the debate, possibly, was the claim by Sanders that, under his universal health care system, hospitals would save money by not having to deal with the bureaucracy of the insurance companies. While it is certainly true that insurance companies put their policyholders through the wringer when it comes time to settle a claim, the notion that handing over the nation’s entire health care system to the federal government would reduce paperwork is not only laughable, it is patently untrue. If there is one thing governments excel at, it is creating pointless bureaucratic nightmares.

Who Goes Big, Who Goes Home?

Pete Buttigieg

As is par for the course in any primary debate – Democrat or Republican – there was a lot of rhetoric and little substance. On immigration, gun violence, and foreign policy, this was particularly true. It is certainly clear that, as a whole, the Democratic Party has decided health care is the one issue upon which it can effectively campaign. Every other issue seems to be nothing more than dressing.

The split between moderates (relatively speaking) and the hardcore progressive/socialist wing is becoming ever more apparent. Of the former group, Delaney and Ryan obviously tried to make their mark – possibly because they saw this debate as their last chance to stake their claim to the nomination on a national stage. Of the latter faction, Sanders and Warren commanded the spotlight.

Sen. Klobuchar may have done just enough to keep her nomination run afloat for a while longer, as did Hickenlooper, but O’Rourke, Buttigieg, and the author Marianne Williamson did little to move the needle on their respective campaigns.

For the first time, the Democratic Party’s extreme left came under fire from some of its own, but the question is whether any of those more moderate candidates – who tried to present alternative, more realistic policy options – will even survive long enough to take the stage for the next round of primary debates.

via ZeroHedge News https://ift.tt/2MupG7Q Tyler Durden

Recently, the Supreme Court decided Gundy v. United States. This case considered whether a provision of the Sex Offender Registration and Notification Act (SORNA) violated the nondelegation doctrine. Justice Kagan’s controlling opinion found that it did not. Justice Alito concurred in the judgment. However, in the appropriate case, he would be “willing to reconsider the approach we have taken for the past 84 years.” Justice Gorsuch wrote a dissent on behalf of Chief Justice Roberts and Justices Thomas. (Justice Kavanaugh had not yet joined the Court when Gundy was argued.) Justice Gorsuch found that the provision of SORNA did violate the nondelegation doctrine. Moreover, he cast serious doubt on how the Supreme Court’s jurisprudence in this area has developed over the past seven decades.

In his analysis, Justice Gorsuch recounted the facts of A. L. A. Schechter Poultry Corp. v. United States (1935). The so-called Sick Chicken Case found that the enforcement of the National Industrial Recovery Act violated the nondelegation doctrine. He wrote:

Included in the code was a rule that often made it a federal crime for butchers to allow customers to select which individual chickens they wished to buy. Kosher butchers such as the Schechters had a hard time following these rules. Yet the government apparently singled out the Schechters as a test case; inspectors repeatedly visited them and, at times, apparently behaved abusively toward their customers. When the Schechters finally kicked the inspectors out, they were greeted with a criminal indictment running to dozens of counts. After a trial in which the Schechters were found guilty of selling one allegedly “unfit” chicken and other miscellaneous counts, this Court agreed to hear the case and struck down the law as a violation of the separation of powers.

Here, Gorsuch cited a well-known book about the New Deal: The Forgotten Man by Amity Shlaes.

Harvard Law Professor Mark Tushnet criticized Justice Gorsuch for relying on Shlaes’s work. He also alleged that Shlaes was mistaken. He wrote:

One of the requirements the Schechters violated was a “straight killing” rule, under which buyers had to purchase all the chickens in a coop (or half coop) after chickens unfit for consumption had been removed. Shlaes writes that “to suggest … that Schechter chickens were unfit was … to suggest that their kosher slaughterhouse was not really kosher,” because, she suggests, under Jewish law “[c]ustomers … had the right to choose their birds, and this in turn ensured that everyone involved had a chance to determine whether the product was as healthy as possible.” (I write “suggests” because Shlaes doesn’t lay out the argument she appears to be making, but I can’t figure out anything else that she could mean by “not really kosher.”)

Shlaes provides no citation to, or discussion of, the applicable Jewish law, and according to one academic expert in the field I consulted, nothing in the law of ritual slaughter appears to require that customers as well as the sellers’ employees who qualified as slaughterers for purposes of Jewish law have the right to inspect chickens before sale. Nor, as far as I know after reading the trial transcript, did the Schechters ever claim in court that they had violated the straight-killing requirement because of their view of the requirements of Jewish law. (Once the Schechters allowed customers to pick out scrawny chickens, the Schechters sold those chickens to “the colored trade,” as one witness at the trial put it.)

Michigan Law Professor Richard Primus accepted Tushnet’s account, and criticized Justice Gorsuch for relying on a “fictionalized account of the facts behind Schechter Poultry.” He wrote:

An earlier post on this blog by Mark Tushnet explained that Justice Gorsuch’s dissent in Gundy v. United States, which fires a loud shot across the bow of the administrative state, contained something like a fictionalized account of the facts behind Schechter Poultry. In Gorsuch’s presentation, the Schechters were caught between the regulatory demands of the New Deal and their own religious commitments. “Kosher butchers such as the Schechters,” Gorsuch wrote, “had a hard time following these rules. Yet the government apparently singled out the Schechters as a test case[.]” In other words, the Schechters were victims of the government’s failure to accommodate their religious beliefs. Worse yet, the government deliberately went after them, the people whose violations arose for religious reasons. But as Tushnet explains, none of this is true. Nothing about the Schechters’ violations of the New Deal’s Codes of Fair Competition arose from any need to comply with the rules for kosher butchering. For the details, I highly recommend Tushnet’s post.

Shlaes has responded to Tushnet in an essay on National Review. Here is an excerpt:

The “straight killing” rule did strain adherence to Kashruth, a Jewish dietary regime that blends custom and law, and this seems to be the source of Tushnet’s confusion. He appears to be laboring under the mistaken assumption that Jewish culture is governed by something resembling a uniform code. There is no Supreme Court of Judaism, no single book comprising the whole of Judaic law. Some Jewish law is written in the Bible. Some is imparted via later commentaries. And some is not law at all, but largely unwritten custom, which varies considerably from region to region and may be enforced as stringently as law in some Jewish communities. An action that one rabbi allows, another rabbi might stigmatize. The onus is on the congregant to demonstrate his right to stay in the rabbi’s community through rigorous observance. For any kosher butcher to slaughter animals in a fashion that the local rabbi rates inconsistent with law or custom is for the butcher to risk his livelihood.

Shlaes’s account comports with how I’ve long understood the rules of Kashruth: both butchers, and customers, have an obligation to ensure that all animals for consumption by Jews are Kosher. Different communities have different ways to follow this rule. The straight-killing rule made it impossible to reject unkosher animals; buyers would have to take whatever chickens were available. I invite Rabbis or anyone else familiar with this area to comment below.

Moreover, Shlaes adds that trial record explored how the straight-killing rule burdens Jewish dietary laws.

That the Orthodox custom of picking a live animal to be slaughtered, Tushnet’s emphasis, prevailed in New Deal-era New York is evident in the lower-court testimony from Schechter Poultry. One of the prosecutors asked a witness to affirm that Orthodox Jews insisted on special selection from live poultry. “Absolutely correct,” the witness replied. Could not one slightly alter the custom, and let customers’ inspection of a bird be conducted postmortem? One could, said the witness, though “they wouldn’t eat it anyhow.” New York’s Orthodox Jews demanded to pick a live chicken themselves, or rely on someone they trusted to do so.

“In other words,” the government asked of another witness, the customers “have a right to reject chickens or not to buy certain chickens if they so desire?” “That is right,” the witness said. As the witness testified, “the customer went in and handled each bird himself and picked out just what he wanted.” The assembly line of “straight killing” forced a bitter choice upon the butcher: Choose to offend a prosecutor who could put him in jail or offend his community and risk being shunned.

Shlaes was kind enough to send me excerpts of the trial record, which I have posted here.

This debate illustrates, with precision, why courts do not determine the doctrines of a faith; instead they can only ascertain if a certain belief is sincerely held. Trying to parse what beliefs are, and are not within a religion should be avoided at all costs.

Tushnet also suggests that the Schechters may not have been sincere in their beliefs, and did sell unkosher animals. He writes:

Nor were they completely honest businesspersons. They clearly did sell chickens infected with respiratory illnesses, which might have included tuberculosis.

There is a prohibition against selling unkosher (that is, unhealthy) animals to fellow Jews. A similar obligation did not exist towards non-Jews.

Justice Gorsuch was right to rely on Shlaes’s account. And, given that there are at least four votes to revisit the nondelegation doctrine, I suspect we will be hearing much more about Schechter Poultry in the years to come.

from Latest – Reason.com https://ift.tt/2Yf57DF

via IFTTT

The unexpectedly early end to the latest round of trade talks in Shanghai, indicating that any goodwill to restore US-China trade is now dead and buried, weighed on global stocks on Wednesday ahead of the highly anticipated Fed meeting, even as US equity futures levitated higher on the back of strong results and even stronger guidance from Apple (which is expected to surpass a $1 trillion market cap again today), with Treasury rates unchanged, the dollar holding firm and Britain’s pound subdued amid rising fears of no-deal Brexit.

Combative warnings from President Trump cast a shadow over the day’s other main event, as the Sino-U.S. trade talks concluded in Shanghai on Wednesday, with Beijing attributing the lack of progress to Washington’s flip-flopping.

“Trade talks have finished without an agreement,” said Justin Onuekwusi, fund manager at Legal & General Investment Management. “Of course, it doesn’t help that almost as a prelude to the conversation you get tweets that are quite antagonistic,” he said, referring to a tweet by Trump warning China against waiting out his current presidential term before finalizing a trade deal.

The fresh trade tensions come ahead a FOMC meeting which is expected to see interest rates reduced by 25 basis points in its first rate cut in more than a decade. Yet the focus is on whether this will be a “one and done”, or Powell will leave the door open for further easing to shore up the world’s largest economy in the face of slowing global growth and the fallout from trade conflicts.

A 25bps rate cut is certain as is another 25 basis point reduction by September – with the market pricing in a 20% chance of a 50bps rate cut today – but what will matter is whether this is seen as a recessionary cut (validated by a 50bps cut), or an “insurance”, or precautionary easing. How Powell frames today’s move will determine if stocks will rise or fall before the end of the day. Expectations for Fed easing helped lift the S&P 500 index 2.4% so far this month.

“Exactly what happens today is far from a foregone conclusion,” said Deutsche Bank’s Jim Reid. “Although the Fed have given no real encouragement to the notion of a 50 basis point (bps) cut it’s worth noting that the last time the Fed began a series of rate cuts, in September 2007, their opening move was a 50 bps cut, and a similar 50 bps cut happened when the Fed began cutting in January 2001.”

Trump on Tuesday reiterated his call for the Fed to make a large interest rate cut, saying he was disappointed in the U.S. central bank and that it had put him at a disadvantage by not acting sooner.

“The bond and equity markets have fully priced in a cut,” Paul Brain, head of fixed income at Newton Investment Management, said in a note. “On balance, there may be some that are disappointed by the size of the cut and the subsequent messaging, but once that is out of the way there will be a realization that rates are heading lower.”

Until the 2pm FOMC announcement, global stocks were biding their time, with the MSCI world index and Europe’s pan regional Stoxx 600 slipping 0.1%, the latter flirting with a fresh one-month low and decidedly underperforming the S&P500, as worries over trade wars and Brexit offset encouraging signals from the earnings season. The Stoxx Europe 600 index struggled for direction amid mixed company reports, with personal and household-goods shares among the biggest losers as L’Oreal dropped after posting disappointing sales figures. Construction companies led gains after upbeat results from Vinci. London’s FTSE fell 0.3% while Frankfurt stocks gained 0.2% and Paris was treading water.

In focus were banks, with strong results from French lender BNP Paribas and Switzerland’s Credit Suisse countering a poor report from British bank Lloyds. Also of note is the sharp rebound in German retail sales, which surged 3.5% M/M, smashing expectations of a modest 0.5% increase, and the biggest monthly increase since 2006.

Asian stocks ex-Japan fell to a six-week low with China mainland stocks down nearly 1% and Hong Kong tumbling 1.3% as China and the U.S. concluded their Shanghai trade talks without signaling any progress and disappointment among investors with corporate earnings. The MSCI Asia Pacific Index fell as much as 0.8% to the lowest level since June 19. Technology was the worst-performing group Wednesday, mainly dragged by Samsung Electronics as the company reported lower profit and said it faces uncertainty due to growing macroeconomic issues. Hong Kong market closed early Tuesday as a storm struck the city. Philippines’ PSEi Index fell 1.3%, led by basic materials companies. Elsewhere, India’s Sensex traded little changed.

Overnight, Chinese data showing factory activity shrank for the third month in a row in July added to the somber mood.

Seemingly oblivious to the global equity woes, US futures pointed to main indexes opening higher as General Electric delivered strong results. On Tuesday, major Wall Street stock averages ended slightly lower with the S&P 500 losing 0.26%, however, momentum reversed after the closing bell when Apple shares soared 4.2% as its Q3 earnings beat estimates and CEO Tim Cook cited “marked improvement in Greater China”.

In currency markets, the dollar index traded flat around 98.064 after pulling back from a two-month high of 98.206 touched on Tuesday. The dollar index was set for a monthly gain of 1.4%, its best since last October. The greenback was also steady against the yen and the euro, with the former undermined on Tuesday by the BOJ’s decision to refrain from expanding stimulus though it committed to doing so “without hesitation” if required. Most other currencies traded in narrow ranges before the Fed meeting.

Meanwhile the British pound hovered near a 28-month low hit the previous day on growing concerns about a disorderly Brexit. GBPUSD recovered from the drop seen in the past two sessions but was still set for a 4% decline this month, its worst showing since 2016. The Australian dollar climbed against all its major peers as headline inflation was higher than the estimate.

Treasuries were modestly higher, led by front-end ahead of the Fed’s expected rate cut. Volumes were light during Asia session and European morning with several additional key events ahead including July ADP employment change, quarterly refunding announcement and month-end. The 10-year yield was at 2.05% after a 3bps decline since July 25. The TSY curve had a small steepening bias, with yields richer by 1.2bp to 2bp across the curve with 10-year ~2.047%, lower by 1bp; Around the world, gilts underperformed, cheaper by 1.5bp vs. Treasuries, as sterling stabilizes following recent sell-off, while bunds keep pace.

In geopolitics, North Korea fired multiple projectiles early on Wednesday which was said to be 2 short-range ballistic missiles and a different type of weapon than previous launches, Following the launch, South Korea convened a national security meeting, while Japan Defense Ministry said no ballistic missiles reached Japan’s territory or exclusive economic zone and sees no immediate impact on Japan’s security from the North Korea launch.

In commodity markets, crude oil futures rose for the 5th straight day, buoyed by a bigger-than-expected drop in U.S. inventories. U.S. WTI crude gained 28 cents to $58.34 per barrel while Brent crude futures LCOc1 added 48 cents to $65.2. Three-month copper on the London Metal Exchange (LME) CMCU3 was almost unchanged at $5,950 a ton.

Expected data include mortgage applications. CME Group, Carlyle Group and Spotify are among companies reporting earnings.

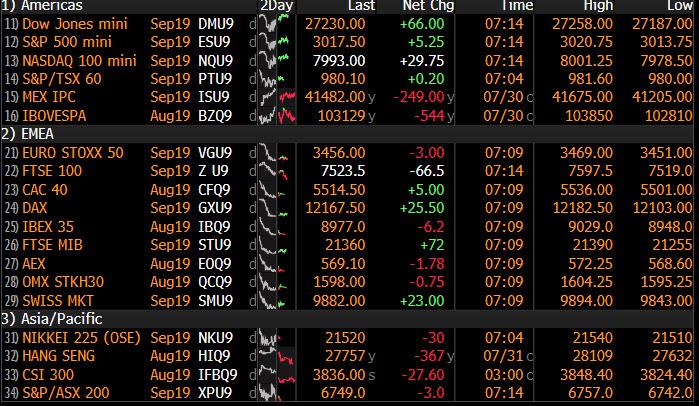

Market Snapshot

S&P 500 futures up 0.2% to 3,019.50

STOXX Europe 600 up 0.06% to 385.36

MXAP down 0.6% to 158.48

MXAPJ down 0.7% to 519.26

Nikkei down 0.9% to 21,521.53

Topix down 0.7% to 1,565.14

Hang Seng Index down 1.3% to 27,777.75

Shanghai Composite down 0.7% to 2,932.51

Sensex up 0.06% to 37,418.69

Australia S&P/ASX 200 down 0.5% to 6,812.56

Kospi down 0.7% to 2,024.55

German 10Y yield fell 0.7 bps to -0.406%

Euro down 0.08% to $1.1146

Brent Futures up 0.7% to $65.16/bbl

Italian 10Y yield rose 8.7 bps to 1.308%

Spanish 10Y yield fell 2.8 bps to 0.324%

Brent Futures up 0.9% to $65.16/bbl

Gold spot down 0.02% to $1,430.53

U.S. Dollar Index up 0.06% to 98.11

Top Overnight News

China and the U.S. concluded a new round of trade talks in Shanghai on Wednesday following a hiatus of almost three months, with little immediate evidence of progress being made toward ending their year-long dispute

The talks come at a time when President Trump lashed out at China for what he said is its unwillingness to buy American agricultural products and said it continues to “rip off” the U.S.

A tropical storm shut Hong Kong’s financial markets for the first time in almost two years, adding chaos to a city which has been wracked by protests for weeks

German unemployment rose and demand for new workers dwindled, a sign that weakening economic momentum is starting to affect the labor market. Spanish economic growth slowed more than expected in the second quarter, adding another layer of gloom to an increasingly fragile situation in the euro region

“We now have a fresh approach to negotiating a deal and are well prepared to leave the EU,” U.K. Brexit Secretary Stephen Barclay said on Twitter, adding that he was confident as two new Brexit committees “are now up and running”

The White House is monitoring what a senior administration official called a congregation of Chinese forces on Hong Kong’s border

North Korea fired multiple unidentified projectiles off its east coast early Wednesday, Yonhap reports, citing the South Korean Joint Chiefs of Staff

Asian equity markets followed suit to the negative performance seen across global peers amid trade concerns following US President Trump’s Twitter rant regarding China, while the looming FOMC decision, mixed Chinese PMI data and earnings deluge added to the cautious tone. ASX 200 (-0.5%) was dragged lower by losses in utilities and financials but with downside stemmed by strength in the energy sector after a rally in oil prices, while Nikkei 225 (-0.9%) suffered the ill-effects of a firmer currency with the best and worst performers in Tokyo driven by their quarterly results. KOSPI (-0.7%) weakened after North Korea conducted another launch which was said to be a new type of weapon and with earnings also in focus including index heavyweight Samsung Electronics which showed final Q2 oper. profit and revenue topped preliminary results but still suffered a 56% Y/Y drop in profits. Conversely, its main rival Apple saw a different fate with the US tech giant gaining around 4.5% after-hours due to a beat on both top and bottom lines and although it missed on iPhone sales its revenue forecast for next quarter surpassed Street estimates. Elsewhere, Hang Seng (-1.3%) and Shanghai Comp. (-0.7%) conformed to the wide risk averse tone after President Trump’s recent criticism on China and warning of a much tougher deal if China holds out until after the next US elections, with participants also digesting mixed Chinese PMI data in which the headline Manufacturing PMI beat expectations but remained below the 50 benchmark level and Non-Manufacturing PMI missed forecasts. Finally, 10yr JGBs traded relatively flat and were only marginally supported by the risk averse tone as well as the BoJ’s presence in the market for JPY 1.24tln of JGBs with 1yr-10yr maturities.

Top Asian News

China, U.S. Trade Talks End Early in Shanghai

Hong Kong Rioting Charges Signal Harsher Line Against Protesters

Hintze’s CQS Strikes Deal With Asia Managers in Regional Push

Major European indices are mixed [Euro Stoxx 50 Unch], as this morning saw the early finish of US-China trade talks with initial reports indicating that the talks ended with no sign of a breakthrough after an earnings dominated morning for indices. Sectors are also mixed with no standout sector at present. In terms of this mornings earnings, L’Oreal (-3.8%) are under pressure after missing on sales growth in-spite of the Co’s CEO noting that H1 was the strongest in terms of like-for-like growth in decades; notably the Co. also announced a EUR 750mln share buyback. Sticking with the CAC 40 (+0.1%) this morning also saw earnings from Airbus (+0.8%) who beat on Q2 revenue and confirmed FY guidance; recently, the Co. also benefitting recently from WSJ reports indicating that internal risk analysis at Boeing (BA) showed the likelihood was high of further cockpit emergencies following the first crash. Elsewhere, of note for banking names Credit Suisse (+4.2%) are firmer after beating on Q2 net revenue and net income as are BNP Paribas (+3.5%) post earnings where the Co’s Q2 revenue beat on consensus.

Top European News

Salvini Weighs Early 2020 Vote, Govt Breakup in Fall: Repubblica

Polish Inflation Unexpectedly Surges to Highest Level Since 2012

Next Surges as E-Commerce Sales Boost Fuels Guidance Upgrade

DUP’s Foster Says Ireland Must ‘Get Real’ on Deal: Brexit Update

In FX, AUD, NZD – The Aussie stands as this morning’s G10 winner amid promising domestic inflation data which follows the RBA’s back-to-back rate cuts since June. CPI Y/Y rose to 1.6% (Prev. 1.3%) in Q2 but remains below the Central Bank’s 2-3% target. In terms of implications on monetary policy, the CB is likely to stand pat on rates for now in order to examine further effects of its recent rate cuts and the government’s tax cut package. AUD/USD trades closer to the top of the intraday range thus far, after testing 0.6900 to the upside. Elsewhere, the Kiwi is lacklustre after the ANZ business confidence further deteriorated alongside the activity outlook. NZD/USD hovers just above the 0.6600 mark having visited a current intra-day low of 0.6590.

DXY, CNY – Relatively side-ways trade for the DXY (for now) heading into the FOMC’s latest policy decision (full preview available in the Research Suite) and with little impetus from the fallout of US-China talks in Shanghai. The initial reports/commentary on the meeting provided little substance. Although no breakthrough was reached (as expected), discussions are said to have been constructive and future talks between the nations will happen. DXY remains flat above 98.00 having earlier tested the figure to the downside. Meanwhile, the CNH also remains tentative and within a narrow range vs. the Buck after having visited its 50 DMA (6.8967) at the European open.

GBP, EUR – Overall little changed thus far with the Pound capped amid fears of a Halloween no-deal crash and tomorrow’s BoE policy decision and QIR (full preview available in the Research Suite). GBP/USD continues to meander sub-1.2200, and as a reminder, the following support levels are still in play: 1.2110 (March 17 low), 1.2085 (Jan 17 low), 1.2000 (psychological) and 1.1841 (2016 flash crash low). Elsewhere The EUR remains flat within a 20-pip intraday range as mostly in-line inflation, growth and unemployment metrics failed to spur a reaction ahead of the FOMC’s policy decision. EUR/USD trades just below 1.1150 ahead of minor support levels at 1.1133/14/21/01, although large option expiries (1.3bln at 1.1145 and 1.2bln at 1.1100-05) may keep the pair contained heading into today’s NY cut.

EM – Another day of gains for the Lira as traders anticipated the CBRT’s QIR to signal further normalisation in its domestic economy, in which it delivered. The Central Bank cut its 2019 year-end inflation forecast mid-point to 13.9% from 14.6% whilst its 2020 figure was maintained at 8.2%, adding that the economic outlook has brightened compared to the April release. USD/TRY breached its 200 DMA (5.5600) to the downside and took out a support level at 5.5500 to print a low of 5.5150 ahead of a Fib support at 5.4172.

In commodities, the oil complex has held onto most of its API-induced gains with WTI futures hovering just below USD 58.50/bbl and Brent north of USD 65/bbl. The report showed that crude inventories fell by 6.02mln barrels over the last week, a larger decline than the expected 2.60mln barrel drawdown. Traders today will be eyeing two events as catalysts: 1) The weekly EIA report for confirmation of the decline in stocks, 2) the FOMC’s policy decision for any Dollar or sentiment-induced action. Elsewhere, sources stated that Libya’s El-Sharara oilfield (300k BPD) has halted production amid a valve closure on a pipeline, although it is not clear how long the closures could last. Of note, WaPo reported that the Trump administration is set to announce that it will waiver five difference nuclear related sanctions on Iran, although it is currently unclear whether the waivers will be oil related. Looking at metals, gold and copper remain flat, as usually the case ahead of the FOMC’s decision.

US Event Calendar

8:15am: ADP Employment Change, est. 150,000, prior 102,000

8:30am: Employment Cost Index, est. 0.7%, prior 0.7%

9:45am: MNI Chicago PMI, est. 51, prior 49.7

2pm: FOMC Rate Decision

DB’s Jim Reid concludes the overnight wrap

So today is the long-awaited Fed decision day, where markets are fully pricing in what is expected to be the first rate cut since December 2008. But exactly what happens today is far from a foregone conclusion, as the question still on investors’ minds is by how much the Fed will cut, and whether there’ll be any messages about the future path of rates going forward. The market currently fully prices a 25bp cut and implies an 16% chance of a larger 50bp cut. Although the Fed have given no real encouragement to the notion of a 50bps cut it’s worth noting that the last time the Fed began a series of rate cuts, in September 2007, their opening move was a 50bp cut, and a similar 50bp cut happened when the Fed began cutting in January 2001. Rates were higher back then though. The last time the Fed started an easing cycle with a 25bps cut was in September 1998, when they ultimately cut rates 3 times and successfully prolonged the expansion until the recession in 2001.

In their preview last Friday (link here ), our US economists predict a 25bp cut, but they say that “the key question is how Chair Powell and the Committee frame the narrative for further easing through year end.” With this in mind, investors will be paying close attention to Chair Powell’s press conference. Our economists write that they “do not expect the Committee to pre-commit to another cut in September”, but instead the amount of further easing is going to be data dependent. Will a market hungry for stimulus accept this?

Indeed we’re at a fascinating juncture in markets. It feels like the global macro risks are building for late summer/autumn (hard Brexit, US/China trade uncertainty, US/EU trade issues to come before year-end and global manufacturing effectively in recession) but all of us are reluctant to fight the central banks. Is this a trap? Indeed even our traditionally bullish Binky Chadha has some reservations about the risk/reward from this starting point. In his piece last week ( link ) he suggested that there have been 19 Fed easing cycles since the 1950s and this one fits almost exactly inline timing wise with the average slowdown in ISMs and LEIs through history. However, where it differs markedly is that only once (in 1995) has a rate cut occurred when the S&P 500 was around record highs. On average, the market has peaked 4 months before the cutting cycle started and was down a median -12% in between the two points. Also, he pointed out that 9 of the 19 rate cutting cycles failed to avert a recession. The recessions typically saw a -27% peak to trough drawdown in the S&P (mostly after the first cut) and on average bottomed 5 months after the Fed started cutting. Of the 10 that didn’t end in recessions, growth rebounded quickly – on average after 2-3 months – and although the S&P still fell around -7%, within 6 months of the first cut they had gained 12% from the lows and sat comfortably above pre-cut levels. So history would suggest quite a binary outcome from here and based on this alone one would have to say that the risk/reward doesn’t look particularly compelling especially as we’re at record highs. So don’t fight the Fed is a famous refrain but nearly 50% of the time they’ve been powerless to stop negative economic and market momentum in a growth slowdown.

Ahead of today’s FOMC decision, President Trump said yesterday that “I would like to see a large cut” in rates, maintaining his calls for easier monetary policy from the Fed. Separately, comments via Twitter from the President sent S&P futures lower before the US open, as he said that “China is doing very badly, worst year in 27 – was supposed to start buying our agricultural product now – no signs that they are doing so. This is the problem with China, they just don’t come through.” In response, The People’s Daily – the official paper of the Communist Party, said overnight that China has no motive to “rip off” the US and has never done so, and China won’t make concessions against its principles on trade. All this is occurring as the US and China have kick started a new round of trade talks in Shanghai. Watch this space for any headlines.

After this set back pre-market, US equities didn’t fall any further during the actual session but failed to get back to flat after trading in a relative narrow band through the day. The S&P 500 (-0.26%), NASDAQ (-0.24%), and DOW (-0.09%) all ended lower, though US bank stocks did gain +0.47% in contrast to their European cousins (more below). Fixed incomes moves were also muted, with 2- and 10-year treasury yields -1.4bps and -0.9bps lower, while HY credit spreads mirrored the moves in equities, widening +3.5bps. Earnings news was again mixed, with Under Armor (-12.28%) underperforming after signaling for a revenue decline from its core North American market. Procter and Gamble (+3.82%) and Merck (+0.96%) both gained after beating analyst expectations. After markets closed, Apple reported better-than-expected revenue and traded +4.42% overnight. Though iPhone sales and revenue disappointed, the company performed better via its mac, iPad and wearable business lines. Apple also reported gross margins at the top end of analyst estimates, illustrating that they continue to generate growth without lowering prices.

Meanwhile in Europe it was a gloomy day for equities, with the STOXX 600 falling -1.47%, its worst fall in 12 weeks and the index’s lowest close in a month. The continent’s indexes were lower across the board, with the DAX (-2.18% and worst day for 6 months), CAC 40 (-1.61%) and the FTSE MIB (-1.99%) all losing ground. Banks in particular suffered, with the STOXX Banks down –2.90%, bringing the index’s falls over the last two days to -3.77%, the biggest two-day fall since May. It’s not 100% clear to me why yesterday was such a bad day but weak Euro area data (see below), disappointing earnings, and perhaps worries about US/China trades talks may have weighed.

Bonds advanced for the most part, with ten-year bund yields matching their record low from earlier this month at -0.399% after falling -0.8bps yesterday. Spreads widened however, with Italian ten-year spreads over bunds up +2.1bps, while European HY spreads were up +6bps. Gilts rallied -1.9bps as fears of a hard Brexit continued to build.

The FTSE 100 outperformed again, only down -0.52%, although as before this was due to sterling’s continued slide, with the currency down -0.52% (trading largely unchanged this morning) against the dollar as it fell to fresh two-year low (only 0.89% off 34 year lows) as investor’s concerns over a no-deal Brexit outcome continued. The falls came as Prime Minister Johnson spoke to the Irish Taoiseach, Leo Varadkar, with a press release from Downing Street saying that “the Prime Minister made clear that the UK will be leaving the EU on October 31, no matter what”. He is also making it quite clear that he won’t sit down with EU leaders unless they agree to re-open the Withdrawal Agreement – something they have shown no appetite in doing. So unless someone blinks, or Parliament finds a way (including an election) to reverse course, then we are heading for a hard Brexit.

Overnight in Asia we have seen China’s July PMIs with manufacturing printing at 49.7 (vs. 49.6 expected), marking it the third consecutive month in contractionary territory. There was improvement in conditions for large enterprises (at 50.7 vs 49.9 last month) while small (at 48.2 vs 48.3 last month) and medium (at 48.7 vs. 49.1 last month) enterprises continued to deteriorate. The new export orders component rose to 46.9 (vs. 46.3 last month) but continues to remain well below 50. The services PMI came in at 53.7 (vs. 54.0 expected) bringing the composite PMI to 53.1 (vs. 53.0 last month). After the official PMIs, the focus is likely to turn to China’s Caixin manufacturing PMI tomorrow which focuses more on private sector/SME and is expected to print at 49.5. Meanwhile, China’s political leadership has announced its priorities for 2H 2019 by pledging to tackle ongoing tensions over trade “effectively” while offering incremental additions to stimulus policies.

Staying with Asia, Hong Kong’s Chief Executive Carrie Lam said yesterday that there is “no room for optimism for the second quarter and the entire year,” on GDP growth given the US-China trade war and other “uncertainties,” while pledging to “spare no efforts” to deal with anti-government protests that risk harming the city’s growth. Hong Kong’s GDP data is due today at 4:30 pm (Hong Kong time). Elsewhere, this morning North Korea fired two short-range ballistic missiles off its east coast, conducting its second such test in a week ahead of US Secretary of State Michael Pompeo’s visit to Asia. South Korean Defense Minister Jeong Kyeong-doo said in remarks after the launch that “If they threaten us and provoke us, North Korea’s regime and the North Korean military is with no doubt defined as our ‘enemy.’” This suggests that such actions could cause Seoul to reconsider its decision to downgrade the threat level of its neighbour.

This morning in Asia markets are following Wall Street’s lead with the Nikkei (-0.74%), Hang Seng (-1.11%), Shanghai Comp (-0.53%) and Kospi (-0.15%) all down. Elsewhere, futures on the S&P 500 are up +0.23% while WTI crude oil prices are up +0.67% on a report from the American Petroleum Institute that US crude inventories dropped by 6.02 million barrels last week.

In terms of data yesterday, the Conference Board’s consumer confidence came in well-above expectations at 135.7 in July (vs. 125.0 expected), the highest level in 8 months. The present situation reading also rose to 170.9 while the expectations measure rose to 112.2. Also encouragingly, the prior month’s readings on each of those metrics were revised several points higher. The closely-watched labour differential, which is a good leading indicator for the labour market, rebounded +5.2pts after last month’s sharp drop, approaching again its highest level of the expansion. Separately, the core PCE inflation figure for June came in at 1.6%, consistent with DB econ’s forecast but 0.1pp below consensus. Our economists also noted that, as a function of revisions, the trend over the last few months has weakened while 2017-2018 looks even stronger. This gives further ammunition to the FOMC’s doves at today’s meeting.

In Europe however, ahead of today’s Q2 GDP and July inflation release for the Eurozone, the releases only added to concerns over the economic slowdown. French GDP in Q2 grew by a smaller-than-anticipated 0.2% qoq (vs. 0.3% expected), while the Swedish economy actually contracted by -0.1% (vs. 0.3% growth expected). The European Commission’s economic sentiment indicator for the Eurozone fell to 102.7 in July, down from 103.3 in June and its lowest level since March 2016, and the sectoral breakdowns didn’t offer much hope either, as the industrial confidence reading fell to -7.4, its lowest since July 2013, and services confidence fell to 10.6, its lowest since September 2016. And to finish off the gloomy picture, Germany’s GfK consumer confidence reading fell to 9.7, the lowest figure in over two years, while German HICP inflation fell to 1.1% in July, the lowest since November 2016. The ECB and market tends to focus on the HICP, which is used for German inflation-linked bonds, though it has different weights from CPI (which surprised to the upside at 1.7%).

Turning to the day ahead, the outcome of the much-anticipated FOMC meeting is obviously the highlight for investors. It’s also a very big day for data releases, with the highlights being the advance reading of Eurozone GDP in Q2, along with the June unemployment rate and July CPI. In addition, there are German retail sales for June and the unemployment change for July, Italian Q2 GDP and unemployment for June, French CPI inflation for July, Canadian GDP for May, and from the US the MNI Chicago PMI for July. In terms of earnings, the main releases tomorrow include General Electric, Airbus and Lloyds Banking Group, and we have the second night of Democratic primary debates.

via ZeroHedge News https://ift.tt/2Yx0AaI Tyler Durden

Recently, the Supreme Court decided Gundy v. United States. This case considered whether a provision of the Sex Offender Registration and Notification Act (SORNA) violated the nondelegation doctrine. Justice Kagan’s controlling opinion found that it did not. Justice Alito concurred in the judgment. However, in the appropriate case, he would be “willing to reconsider the approach we have taken for the past 84 years.” Justice Gorsuch wrote a dissent on behalf of Chief Justice Roberts and Justices Thomas. (Justice Kavanaugh had not yet joined the Court when Gundy was argued.) Justice Gorsuch found that the provision of SORNA did violate the nondelegation doctrine. Moreover, he cast serious doubt on how the Supreme Court’s jurisprudence in this area has developed over the past seven decades.

In his analysis, Justice Gorsuch recounted the facts of A. L. A. Schechter Poultry Corp. v. United States (1935). The so-called Sick Chicken Case found that the enforcement of the National Industrial Recovery Act violated the nondelegation doctrine. He wrote:

Included in the code was a rule that often made it a federal crime for butchers to allow customers to select which individual chickens they wished to buy. Kosher butchers such as the Schechters had a hard time following these rules. Yet the government apparently singled out the Schechters as a test case; inspectors repeatedly visited them and, at times, apparently behaved abusively toward their customers. When the Schechters finally kicked the inspectors out, they were greeted with a criminal indictment running to dozens of counts. After a trial in which the Schechters were found guilty of selling one allegedly “unfit” chicken and other miscellaneous counts, this Court agreed to hear the case and struck down the law as a violation of the separation of powers.

Here, Gorsuch cited a well-known book about the New Deal: The Forgotten Man by Amity Shlaes.

Harvard Law Professor Mark Tushnet criticized Justice Gorsuch for relying on Shlaes’s work. He also alleged that Shlaes was mistaken. He wrote:

One of the requirements the Schechters violated was a “straight killing” rule, under which buyers had to purchase all the chickens in a coop (or half coop) after chickens unfit for consumption had been removed. Shlaes writes that “to suggest … that Schechter chickens were unfit was … to suggest that their kosher slaughterhouse was not really kosher,” because, she suggests, under Jewish law “[c]ustomers … had the right to choose their birds, and this in turn ensured that everyone involved had a chance to determine whether the product was as healthy as possible.” (I write “suggests” because Shlaes doesn’t lay out the argument she appears to be making, but I can’t figure out anything else that she could mean by “not really kosher.”)

Shlaes provides no citation to, or discussion of, the applicable Jewish law, and according to one academic expert in the field I consulted, nothing in the law of ritual slaughter appears to require that customers as well as the sellers’ employees who qualified as slaughterers for purposes of Jewish law have the right to inspect chickens before sale. Nor, as far as I know after reading the trial transcript, did the Schechters ever claim in court that they had violated the straight-killing requirement because of their view of the requirements of Jewish law. (Once the Schechters allowed customers to pick out scrawny chickens, the Schechters sold those chickens to “the colored trade,” as one witness at the trial put it.)

Michigan Law Professor Richard Primus accepted Tushnet’s account, and criticized Justice Gorsuch for relying on a “fictionalized account of the facts behind Schechter Poultry.” He wrote:

An earlier post on this blog by Mark Tushnet explained that Justice Gorsuch’s dissent in Gundy v. United States, which fires a loud shot across the bow of the administrative state, contained something like a fictionalized account of the facts behind Schechter Poultry. In Gorsuch’s presentation, the Schechters were caught between the regulatory demands of the New Deal and their own religious commitments. “Kosher butchers such as the Schechters,” Gorsuch wrote, “had a hard time following these rules. Yet the government apparently singled out the Schechters as a test case[.]” In other words, the Schechters were victims of the government’s failure to accommodate their religious beliefs. Worse yet, the government deliberately went after them, the people whose violations arose for religious reasons. But as Tushnet explains, none of this is true. Nothing about the Schechters’ violations of the New Deal’s Codes of Fair Competition arose from any need to comply with the rules for kosher butchering. For the details, I highly recommend Tushnet’s post.

Shlaes has responded to Tushnet in an essay on National Review. Here is an excerpt:

The “straight killing” rule did strain adherence to Kashruth, a Jewish dietary regime that blends custom and law, and this seems to be the source of Tushnet’s confusion. He appears to be laboring under the mistaken assumption that Jewish culture is governed by something resembling a uniform code. There is no Supreme Court of Judaism, no single book comprising the whole of Judaic law. Some Jewish law is written in the Bible. Some is imparted via later commentaries. And some is not law at all, but largely unwritten custom, which varies considerably from region to region and may be enforced as stringently as law in some Jewish communities. An action that one rabbi allows, another rabbi might stigmatize. The onus is on the congregant to demonstrate his right to stay in the rabbi’s community through rigorous observance. For any kosher butcher to slaughter animals in a fashion that the local rabbi rates inconsistent with law or custom is for the butcher to risk his livelihood.

Shlaes’s account comports with how I’ve long understood the rules of Kashruth: both butchers, and customers, have an obligation to ensure that all animals for consumption by Jews are Kosher. Different communities have different ways to follow this rule. The straight-killing rule made it impossible to reject unkosher animals; buyers would have to take whatever chickens were available. I invite Rabbis or anyone else familiar with this area to comment below.

Moreover, Shlaes adds that trial record explored how the straight-killing rule burdens Jewish dietary laws.

That the Orthodox custom of picking a live animal to be slaughtered, Tushnet’s emphasis, prevailed in New Deal-era New York is evident in the lower-court testimony from Schechter Poultry. One of the prosecutors asked a witness to affirm that Orthodox Jews insisted on special selection from live poultry. “Absolutely correct,” the witness replied. Could not one slightly alter the custom, and let customers’ inspection of a bird be conducted postmortem? One could, said the witness, though “they wouldn’t eat it anyhow.” New York’s Orthodox Jews demanded to pick a live chicken themselves, or rely on someone they trusted to do so.

“In other words,” the government asked of another witness, the customers “have a right to reject chickens or not to buy certain chickens if they so desire?” “That is right,” the witness said. As the witness testified, “the customer went in and handled each bird himself and picked out just what he wanted.” The assembly line of “straight killing” forced a bitter choice upon the butcher: Choose to offend a prosecutor who could put him in jail or offend his community and risk being shunned.

Shlaes was kind enough to send me excerpts of the trial record, which I have posted here.

This debate illustrates, with precision, why courts do not determine the doctrines of a faith; instead they can only ascertain if a certain belief is sincerely held. Trying to parse what beliefs are, and are not within a religion should be avoided at all costs.

Tushnet also suggests that the Schechters may not have been sincere in their beliefs, and did sell unkosher animals. He writes:

Nor were they completely honest businesspersons. They clearly did sell chickens infected with respiratory illnesses, which might have included tuberculosis.

There is a prohibition against selling unkosher (that is, unhealthy) animals to fellow Jews. A similar obligation did not exist towards non-Jews.

Justice Gorsuch was right to rely on Shlaes’s account. And, given that there are at least four votes to revisit the nondelegation doctrine, I suspect we will be hearing much more about Schechter Poultry in the years to come.

from Latest – Reason.com https://ift.tt/2Yf57DF

via IFTTT

Alas and alack, after 10 years, my special assistant and counsel at the U.S. Commission on Civil Rights will soon be leaving for a new job. Her position with me will therefore be vacant. If this sounds like a gap you might want to fill, further details are here.

from Latest – Reason.com https://ift.tt/2YBhFR7

via IFTTT

Alas and alack, after 10 years, my special assistant and counsel at the U.S. Commission on Civil Rights will soon be leaving for a new job. Her position with me will therefore be vacant. If this sounds like a gap you might want to fill, further details are here.

from Latest – Reason.com https://ift.tt/2YBhFR7

via IFTTT

After roughly half-a-day of negotiations, the US trade delegation has broken off talks with its Chinese counterpart and is already on its way back to Washington, a sign that no new progress was made, and that trade talks between the US and China remain at an impasse.

According to Bloomberg, US delegates including Treasury Secretary Steven Mnuchin and Trade Representative Robert Lighthizer wrapped up talks with Vice Premier Liu He and their other Chinese counterparts on Wednesday afternoon at the Xijiao State Guest Hotel in Shanghai, according to a pool report.

As the talks ended, China’s Ministry of Foreign Trade issues a response to President Trump, who has been warning the Chinese not to keep stalling on the talks.

In response to a question about Trump’s tweets, Chinese Foreign Ministry spokeswoman Hua Chunying said that although she was not aware of the latest developments during the talks, it was clear it was the US that continued to “flip flop.”

“I believe it doesn’t make any sense for the US to exercise its campaign of maximum pressure at this time. It’s pointless to tell others to take medication when you’re the one who is sick,” Hua said.

This week’s meetings, the first in-person trade talks since a G20 truce last month, amounted to a working dinner on Tuesday at Shanghai’s historic riverfront Fairmont Peace Hotel and a half-day of negotiations on Wednesday, Reuters reports. Neither team commented publicly.

Liu He bid farewell to his US counterparts as their motorcade pulled away from the Guest Hotel following a group photo. The talks concluded at around 1:45 pm local time – roughly 30 minutes before they were scheduled to begin.

The Chinese apparently didn’t make any new concessions to the US, despite last night’s PMI report which showed that China’s factory activity continued to shrink in July, a sign that the trade dispute is taking a serious toll on the Chinese economy.

What’s worse, the talks were supposed to focus on “goodwill” gestures, like the agricultural purchases promised by China, and the rollback of sanctions on Huawei promised by Trump. Apparently, the two sides are still at an impasse regarding these two issues. These issues, as Reuters reports, are “somewhat removed” from the more core US complaints in the trade dispute, including US demands surrounding forced technology transfers and state subsidies.

Of course, few analysts expected this week’s talks – the first round of live talks since the second trade truce was struck between Trump and President Xi in Osaka – to yield much progress. But now that they’ve collapsed, does the Fed have the green light to deliver a 50 bp rate cut?

via ZeroHedge News https://ift.tt/2Ore6wO Tyler Durden

There’s no hiding place down here

You know, there’s no hiding place down here

I went to the rock to hide my face

But the rock cried out, no hiding place, now No Hiding place down here

–Gospel Standard

I really like Dwayne “The Rock” Johnson. His work ethic, attitude and humility are an inspiration.

In an age when it seems every third person attached to the entertainment industry is a pedophile at worst and a scumbag at best, Johnson’s superhero persona on and off screen is exactly what this society needs.

And no one knows this better than Dwayne Johnson himself.

“Breaking: PM Boris Johnson is in fact my cousin [though we clearly look more like twins],” the Hollywood actor tweeted. “Jokes aside, PM did say something in his speech I liked – ‘the people are our bosses’. 100% agree. The people/audience/consumer will always matter most. #ourboss.”

DWAYNE “THE ROCK” JOHNSON — DELETED TWEET 7/29/2019

Johnson knows that everyone goes to see his movies. His latest movie exists because he won’t work with Vin Diesel who Johnson feels takes his job for granted.

And, despite holding very strong opinions, he is always inclined to look for the positive in everything. It’s refreshing for a cynic like me to see that.

It’s also good PR. Conservatives watch movies. So do Marxists.

I don’t begrudge him that. It’s his business, his brand and his choice.

Taken at face value Dwayne Johnson said nothing objectionable. Taken cynically Dwayne Johnson said nothing objectionable.

But that’s no reason to let him off the hook by the perpetually offended Twitterati.

If anything, it’s the main reason he had to be attacked by a rabid and, frankly, insane Remain twitter mob who are so triggered, so ideologically possessed they can’t bear to hear someone they like condone something said by someone they despise, Boris Johnson.

Even if what was said was a basic tenet of polite and decent society: that if we have to suffer the indignity of government, that government should be our servant not our master.

It was particularly galling that it was said by a Prime Minister ‘elected’ by a super-minority of the British People. I get that.

But some things, like the Magna Carta, should transcend even Brexit.

And it shows just how deeply scarred our political life is. We’re to the point where Thomas Jefferson could come back from the dead and recite the Declaration of Independence. It would be decried as racist because Jefferson was a slave-owner.

And then he’d have a milkshake thrown on him before being hauled off to jail for spouting hate speech. Snopes would then ‘fact-check’ his words and declare it ‘fake news.’

Facebook would ban people for sharing the video.

Because who says something today is far more important than what they said. In today’s internet culture wrongthink is forever.

How far have we sunk in our political cynicism that founding tenets of what we’re supposed to be fighting for are stifled because the wrong person uttered them?

You don’t have to like Boris Johnson to agree with the sentiment. But in the world of ideological possession, purity of essence trumps all other considerations.

It’s a sad and pathetic state of the times that someone as obviously conscientious and well-meaning as Dwayne Johnson can’t express a political thought that should be non-partisan.

All Dwayne Johnson did was remind everyone that the key to success is hard work and humility. Because that’s what good government, if there is such a thing, demands. Being humble enough to do right by the people even if it is at odds with your personal beliefs.

Dwayne Johnson should not have deleted the tweet. He should have let it stand. It’s what he believes. It’s who he is. Anyone who follows him even obliquely knows this.

Once it’s out there it won’t go away. There’s no hiding from this once it starts. And no halfway competent Hollywood publicist should have advised Johnson to do so.

The box office for Hobbes and Shaw is immune to this tweet. But it may not be by his deleting it.

By backing down Johnson empowers the ugly people who don’t embody any of what he stands for and alienates those who do.

And it shows me that Dwayne Johnson isn’t ready to lead.

Because leadership means having the moral courage to be vilified. To have principles means being lambasted for them. No matter how good or positive a person you are, someone will throw shade on you simply because you highlight how ugly they are.

People throw shade at the Dalai Lama for pity’s sake.

This admittedly minor incident is however indicative of where we are headed culturally. People feel so dis-empowered they take to Twitter to vent their spleens at anyone who sports any deviance from their ideological purity.

It speaks to exactly what the Johnson bros were saying. There’s something wrong with our politics that is deeper than the issues du jour.

The way back from the brink of societal collapse is remembering who the true bosses are, empowering ourselves to rise above petty partisan politics and stop tweeting about how unfair it all is.

Lesson to Dwayne: No matter how much you try to couch something in non-confrontational terms someone is looking to be offended. There are whole squads of people paid to be so offended, shape the narrative and drown out rationality.

For this reason and so many others Twitter is a terrible form of communication. It’s also a worse mechanism for societal change.

In fact, it’s the opposite of that. Sitting on your ass decrying Tory corporatism on your iPhone over your Vodaphone connection at a Starbucks is not a revolutionary act.

In fact, it’s the exact opposite. And it doesn’t matter if you’re the people who hate Boris Johnson and Brexit or the ones decrying Dwayne Johnson for deleting the tweet.

You’re all ineffectual narcissists trapped in the Matrix; doing the bidding of the worst people in the world who are supposed to work for you.

And that’s the thing everyone is searching for a hiding place from, their own lack of humanity and, more importantly, humility.

“And when the sinners gonna be runnin’

At the knowledge of their fate

They’re gonna run to the rocks and the mountains

But their prayers will be too late

I went to the rock to hide my face

But the rock cried out, no hiding place, now No Hiding place down here “