We’re thrilled to see the far-left in America has the same respect for the Democratic process as their forebears did (for a reference to their forebears, see here).

On Tuesday, Calif. Gov. Gavin Newsom signed a bill requiring President Trump to either release his tax returns or he won’t appear on the ballot in the state.

Calif Gov. Gavin Newsom

Under SB 27, called the “Presidential Tax Transparency and Accountability Act,” any candidate running for president or governor in California must file copies of their tax returns from the previous five years to the California secretary of State, or their names will be stricken from the ballot, the Hill reports.

Newsom argued that, as the largest economic engine within the US, California has a “responsibility” to demand this additional information (for the record: the Constitution doesn’t say anything about candidates releasing tax returns – though the federal income tax didn’t exist back on).

“As one of the largest economies in the world and home to one in nine Americans eligible to vote, California has a special responsibility to require this information of presidential and gubernatorial candidates,” Newsom said.

“These are extraordinary times and states have a legal and moral duty to do everything in their power to ensure leaders seeking the highest offices meet minimal standards, and to restore public confidence. The disclosure required by this bill will shed light on conflicts of interest, self-dealing, or influence from domestic and foreign business interest.”

A Trump campaign spokesman called the new law “unconstitutional,” and insisted that there was a good reason why California’s last governor, Jerry Brown, refused to sign the legislation.

In a statement, Trump campaign spokesman Tim Murtaugh called the move “unconstitutional.”

“There are very good reasons why the very liberal Gov. Jerry Brown vetoed this bill two years ago – it’s unconstitutional and it opens up the possibility for states to load up more requirements on candidates in future elections. What’s next, five years of health records?” he said.

Murtaugh said states cannot add requirements to presidential candidates’ qualifications for running.

“The Constitution is clear on the qualifications for someone to serve as president and states cannot add additional requirements on their own,” he said. “The bill also violates the 1st Amendment right of association since California can’t tell political parties which candidates their members can or cannot vote for in a primary election.”

Unsurprisingly, the bill was overwhelmingly passed by California’s assembly and the state senate earlier this month. Among its more appalling provisions, the bill includes an “urgency clause”, which would allow it to take effect before the 2020 vote, meaning any Californians who want to vote for President Trump might need to write his name in.

Though it has faded from the headlines somewhat, the battle over Trump’s tax returns continues to rage. The administration is already suing New York State, which recently passed a law allowing the state to request Trump’s tax returns, while in Congress, the Ways and Means Committee has filed a lawsuit over the administration’s refusal to release Trump’s returns, which is likely the beginning of a lengthy legal battle.

Surprisingly, Trump was joined in his outrage by some liberal pundits who have stood out for their opposition to Trump’s ideas.

This remains a terrible, anti-democratic idea and California should be embarassed. https://t.co/dYHAEtrnE5

We imagine California won’t be the last state to pass such a bill, but given Trump’s deep unpopularity throughout most of the state, he was unlikely to win any delegates from California: Imagine what will happen when swing states like Colorado and New Hampshire start trying to pass these types of laws?

And finally….

via ZeroHedge News https://ift.tt/2GAjF5W Tyler Durden

Pennsylvania Law School Professor Amy Wax is known for generating controversy, and she produced a fresh round of outrage earlier this month when she spoke at the National Conservatism Conference in Washington, D.C.

Wax was accused by Vox‘s Zack Beauchamp of making “an outright argument for white supremacy.” In her remarks at the conference, Wax claimed that the U.S. should be wary of immigrants who do not share the cultural values of native-born Americans. Prioritizing immigrants who do share our values, according to Wax, would mean prioritizing immigrants who come from countries that are disproportionately European, Christian, and white. “Embracing cultural distance, cultural distance nationalism, means in effect taking the position that our country will be better off with more whites and fewer nonwhites,” said Wax. “Well, that is the result, anyway.”

Those who have defended Wax argue that her remarks were not racist because she isn’t literally disparaging immigrants for their non-whiteness—she just thinks undesirable immigrants are likely to be non-white. This seems like a distinction without much of a difference.

Whether or not Wax’s immigration views may properly be described as racist, they are clearly ignorant. Even from a conservative perspective, it’s not necessarily the case that white European nations are the best cultural match for the U.S., as both Rod Dreher and David French have noted.

Criticism of Wax is perfectly fair and well-deserved. But many people—including many Penn students and alumni—want the university to fire her. Students have created several petitions, according to The Daily Pennsylvanian:

Rising first-year Penn Law student Randy Kim, who also signed LALSA’s statement, said, “It’s outrageous that this person’s employment at a private institution is being protected under the guise of protecting scholarly disagreement and free speech.”

Wax has tenure, though, which protects her academic freedom. So far, Penn’s administration has appeared to recognize that it cannot actually fire her, and instead has resorted to stripping her of mandatory teaching assignments. She will also take a year-long sabbatical.

Kim and 2019 Penn Law graduate Bill Fedullo acknowledged the University’s “difficult position” given Wax’s status as a tenured professor. Both students, however, said the University should end Wax’s teaching duties if she cannot be fired.

“It seems very reasonable to say that she should not be able to teach or interact with any students whatsoever,” Kim said.

The thinking here must be that Wax’s immigration views are so odious that students should not be required to take any of her classes—that college is meant to be a place where students never feel uncomfortable or offended by the views of their professors. For more about student-activists’ attempts to enact this vision of the emotionally “safe” campus, read my new book, Panic Attack: Young Radicals in the Age of Trump, which received a rave review in The Guardian this week.

from Latest – Reason.com https://ift.tt/2OuZTPt

via IFTTT

Juan Rodriguez, a doting upstate New York dad, forgot his twin one-year-olds in the back seat when he went to work on Friday. When he got back to his car at the end of the day, he realized his mistake and started screaming. They were dead.

Adding to Rodriguez’s almost incomprehensible grief, the state decided to charge him with manslaughter, criminally negligent homicide, and endangering the welfare of a child. The judge set his bail at $100,000—as if Rodriguez is a risk to others. As if he hasn’t suffered enough. As if this will teach the rest of us some sort of lesson.

It will not.

On social media, many people understand this. “There but for the grace of God go I,” they write. Plenty of others are saying this man is guilty because no decent person would ever forget their kids in the car.

But we know that stories like this are not unheard of and that, in fact, humans are human. A baby in a car seat, facing backward, making no sound—it is all too easy to forget they are there and proceed on autopilot to work.

For this reason, many states have made it illegal to let a child wait in the car more than a few minutes, or at all. The stated desire is to prevent tragedies like these. But if the father had remembered that his kids were in the car, he would have taken them out. The fear of breaking the law does nothing to prevent a tragedy like this.

This story is particularly hard to bear because the dad is a disabled war vet, a social worker, and a conscientious father who lives for his kids. Now he will be held up as a reason more states should pass even more draconian no-kids-left-in-the-car laws. These laws would make sense if kids died the instant a parent dashed into the store for a gallon of milk, but they don’t. In fact, more kids die in parking lots than in parked cars.

The vast majority of kids who do die in cars either climbed in when no one was looking and weren’t found until too late, or were forgotten there. They are not in danger because their parents are running brief errands. Criminalizing parents who consciously let their kids wait in the car a few minutes is not the answer.

A better solution is to publicize and spread the act of always putting something else in the back seat at the same time you put the child there: your shoe, your phone, etc. When you exit the car, it’s impossible not to notice you’re missing something. Fetching the item brings you to the back seat and the baby.

Public service announcements—Baby In, Shoe Off!—could save more lives than laws against letting kids wait in the car during a short errand.

A technological answer—having an alarm sound if someone is left in the car (or if the back door opened at the beginning of the trip but not the end)—would also be good, but not if this makes it illegal to let the kids wait in the car a few minutes, in the same way it is illegal to drive without first putting on a safety belt.

In any case, the shoe or the alarm make a lot more sense than tormenting a dad who is already living in hell.

from Latest – Reason.com https://ift.tt/2K3aE7w

via IFTTT

Pennsylvania Law School Professor Amy Wax is known for generating controversy, and she produced a fresh round of outrage earlier this month when she spoke at the National Conservatism Conference in Washington, D.C.

Wax was accused by Vox‘s Zack Beauchamp of making “an outright argument for white supremacy.” In her remarks at the conference, Wax claimed that the U.S. should be wary of immigrants who do not share the cultural values of native-born Americans. Prioritizing immigrants who do share our values, according to Wax, would mean prioritizing immigrants who come from countries that are disproportionately European, Christian, and white. “Embracing cultural distance, cultural distance nationalism, means in effect taking the position that our country will be better off with more whites and fewer nonwhites,” said Wax. “Well, that is the result, anyway.”

Those who have defended Wax argue that her remarks were not racist because she isn’t literally disparaging immigrants for their non-whiteness—she just thinks undesirable immigrants are likely to be non-white. This seems like a distinction without much of a difference.

Whether or not Wax’s immigration views may properly be described as racist, they are clearly ignorant. Even from a conservative perspective, it’s not necessarily the case that white European nations are the best cultural match for the U.S., as both Rod Dreher and David French have noted.

Criticism of Wax is perfectly fair and well-deserved. But many people—including many Penn students and alumni—want the university to fire her. Students have created several petitions, according to The Daily Pennsylvanian:

Rising first-year Penn Law student Randy Kim, who also signed LALSA’s statement, said, “It’s outrageous that this person’s employment at a private institution is being protected under the guise of protecting scholarly disagreement and free speech.”

Wax has tenure, though, which protects her academic freedom. So far, Penn’s administration has appeared to recognize that it cannot actually fire her, and instead has resorted to stripping her of mandatory teaching assignments. She will also take a year-long sabbatical.

Kim and 2019 Penn Law graduate Bill Fedullo acknowledged the University’s “difficult position” given Wax’s status as a tenured professor. Both students, however, said the University should end Wax’s teaching duties if she cannot be fired.

“It seems very reasonable to say that she should not be able to teach or interact with any students whatsoever,” Kim said.

The thinking here must be that Wax’s immigration views are so odious that students should not be required to take any of her classes—that college is meant to be a place where students never feel uncomfortable or offended by the views of their professors. For more about student-activists’ attempts to enact this vision of the emotionally “safe” campus, read my new book, Panic Attack: Young Radicals in the Age of Trump, which received a rave review in The Guardian this week.

from Latest – Reason.com https://ift.tt/2OuZTPt

via IFTTT

Juan Rodriguez, a doting upstate New York dad, forgot his twin one-year-olds in the back seat when he went to work on Friday. When he got back to his car at the end of the day, he realized his mistake and started screaming. They were dead.

Adding to Rodriguez’s almost incomprehensible grief, the state decided to charge him with manslaughter, criminally negligent homicide, and endangering the welfare of a child. The judge set his bail at $100,000—as if Rodriguez is a risk to others. As if he hasn’t suffered enough. As if this will teach the rest of us some sort of lesson.

It will not.

On social media, many people understand this. “There but for the grace of God go I,” they write. Plenty of others are saying this man is guilty because no decent person would ever forget their kids in the car.

But we know that stories like this are not unheard of and that, in fact, humans are human. A baby in a car seat, facing backward, making no sound—it is all too easy to forget they are there and proceed on autopilot to work.

For this reason, many states have made it illegal to let a child wait in the car more than a few minutes, or at all. The stated desire is to prevent tragedies like these. But if the father had remembered that his kids were in the car, he would have taken them out. The fear of breaking the law does nothing to prevent a tragedy like this.

This story is particularly hard to bear because the dad is a disabled war vet, a social worker, and a conscientious father who lives for his kids. Now he will be held up as a reason more states should pass even more draconian no-kids-left-in-the-car laws. These laws would make sense if kids died the instant a parent dashed into the store for a gallon of milk, but they don’t. In fact, more kids die in parking lots than in parked cars.

The vast majority of kids who do die in cars either climbed in when no one was looking and weren’t found until too late, or were forgotten there. They are not in danger because their parents are running brief errands. Criminalizing parents who consciously let their kids wait in the car a few minutes is not the answer.

A better solution is to publicize and spread the act of always putting something else in the back seat at the same time you put the child there: your shoe, your phone, etc. When you exit the car, it’s impossible not to notice you’re missing something. Fetching the item brings you to the back seat and the baby.

Public service announcements—Baby In, Shoe Off!—could save more lives than laws against letting kids wait in the car during a short errand.

A technological answer—having an alarm sound if someone is left in the car (or if the back door opened at the beginning of the trip but not the end)—would also be good, but not if this makes it illegal to let the kids wait in the car a few minutes, in the same way it is illegal to drive without first putting on a safety belt.

In any case, the shoe or the alarm make a lot more sense than tormenting a dad who is already living in hell.

from Latest – Reason.com https://ift.tt/2K3aE7w

via IFTTT

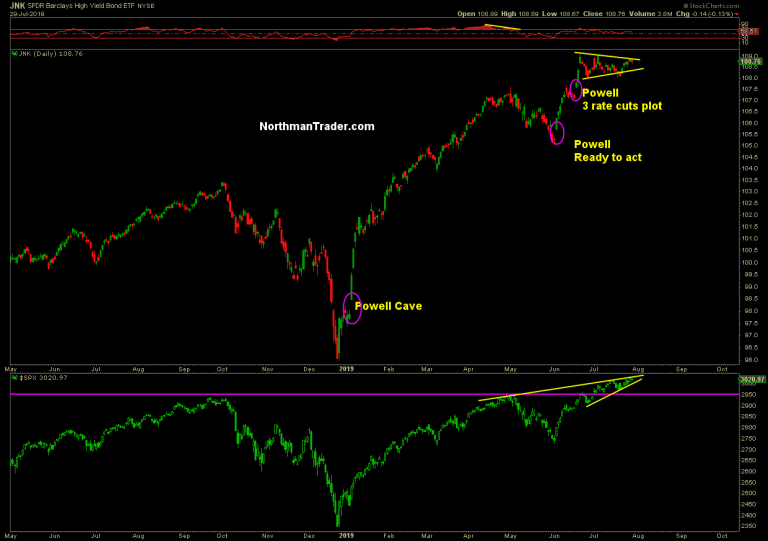

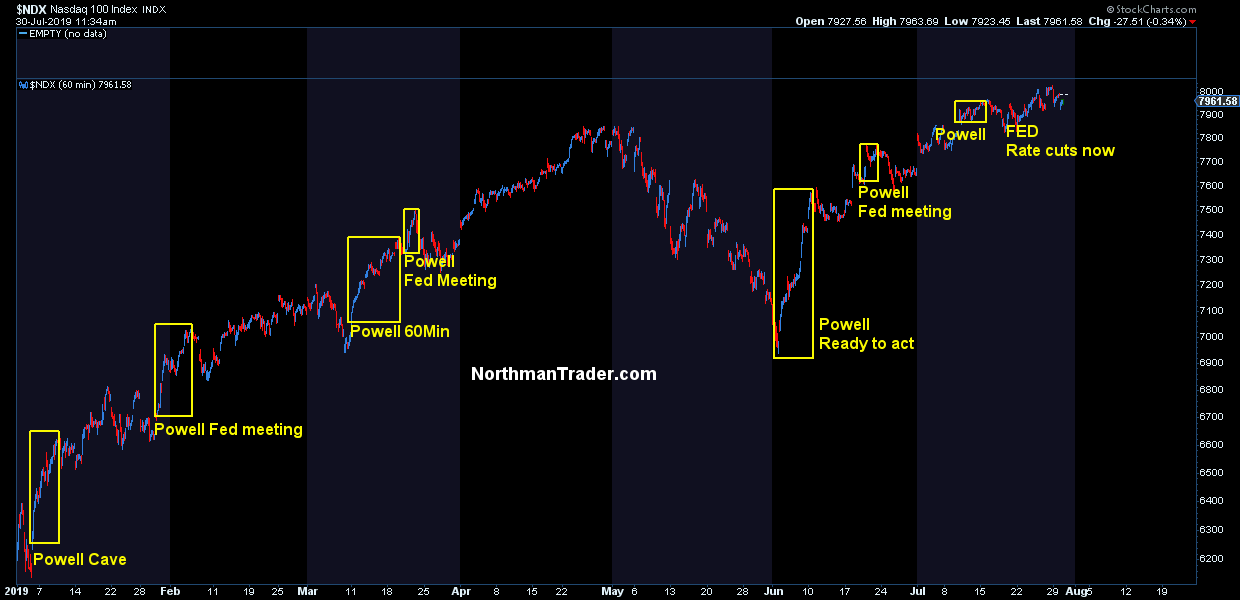

The circus is back in town and it’s putting on a major show, the rate cut show.

Some thoughts for your consideration:

Firstly, the expectation is for a 25bp rate cut. That’s what all signaling by the Fed has led to. That’s the market’s expectation. There is no way, no how, that they will not cut. The risk of stock market carnage would be to high. They can simply not afford to disappoint markets. Fact is a market sell-off of size would virtually set the stage for a massive reversal in confidence which in turn could be self fulfilling given slower growth.

One other piece of evidence: The Fed’s in a blackout period. Cute then that they paraded out Greenspan and Yellen in the past couple of days to give cover for a rate cut. Don’t think this was not done without behind the scenes approval and encouragement. Everything is a big game of managing expectations.

Powell has already declared that their goal is to extend the business cycle which, by the way, is a monumentally bad idea in my view because the only way they can extend the business cycle is by deepening the market bubble.

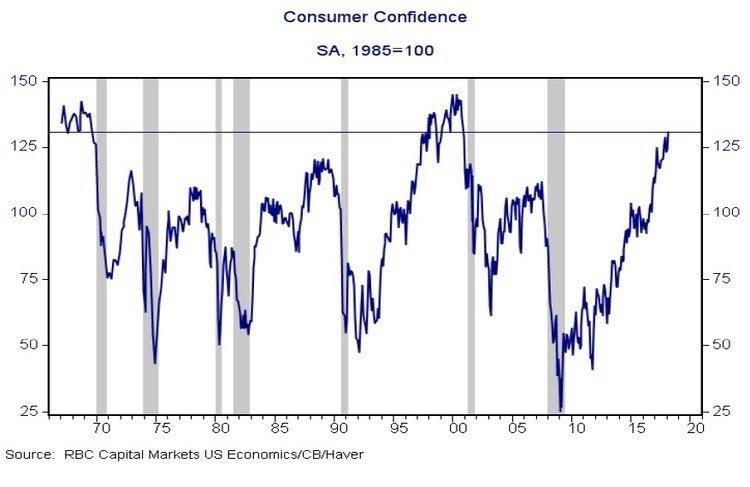

Cut rates here with consumer confidence at 135.7?

Cut rates here with key market cap stocks massively and historically extended after having rallied virtually non stop for 10 years?

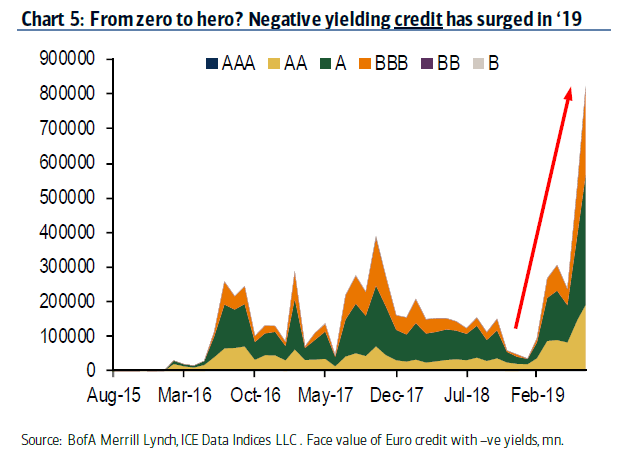

Everything is distorted and propped up by central banks and it’s causing massive dislocations, look no further than European bonds:

About €825bn of corporate debt in Europe now trades with negative yields, a chunk of that is rated triple-B.

When markets do extreme things that are completely outside the norm of history everybody better pay attention. Dislocations lead to relocations.

And let’s be clear without the surge in high yield credit this year stock markets wouldn’t be anywhere near here.

For the Fed it has to be all about not disappointing and managing market expectations. What if they cut 25bp and they have 1,2 or even 3 dissenters on the vote?

Markets don’t like an internal Fed fight. Rosengren wants to wait he said on Friday.

And you know what? Cutting in my view is a mistake here from a managing the economy perspective. From a managing the stock market perspective it makes sense to cut, from an economy perspective it’s a mistake. Why? Again, the Fed has limited ammunition, it should use it judiciously and not waste it on insurance. If you have limited ammunition, make it count, a big bang, shock and awe if you will.

If the slowdown is persisting, and CAPEX, business investment and global PMIs are telling you that a recession is coming and not an expansion, then you better have all the ammunition available to you to combat that. But US data has been beating on some key reports, so why diddle with a 25bp cut here? Because you are beholden to the market’s reaction and can’t disappoint. Well, that’s just pitiful.

But if the threat is real, and suppose you even have a peek at Friday’s job’s numbers ahead of time and you see bad news coming down the pike, then it may make sense to shock the market right here and there and do a 50bp cut even though you dialed back expectations for a 50bp rate cut following the William’s speech.

Here’s the evil alternative: Maybe, just maybe, the Fed wanted to surprise markets with a 50bp rate cut and Williams bollixed it up when he gave his speech and expectations were moving in the 50bp direction. In this context suddenly it made sense why the Fed came out and dialed back expectations. Now 80% think it’s a 25 bp rate cut so mission accomplished.

But there’s a problem with a 50bp rate cut, while perhaps causing another market rally on the surprise the underlying message is one of panic. Things are worse than they seem, the ghosts of 2001 and 2007 would make their presence felt and that could be damaging to confidence, and when you damage confidence you lose buyers or, worse, invite sellers.

Bottomline:

If it’s a decision to manage markets they need to cut either 25bp or 50bp.

If it’s a decision to manage the economy they shouldn’t cut yet. Why? Because they have limited ammunition & need to make it count when it matters.

They can’t afford frivolous cuts.

The irony: If they don’t cut to appease marktes, markets would sell off hard resulting in an adverse economic reaction & loss of confidence forcing to Fed to cut rates.

Nice circle jerk they got themselves into.

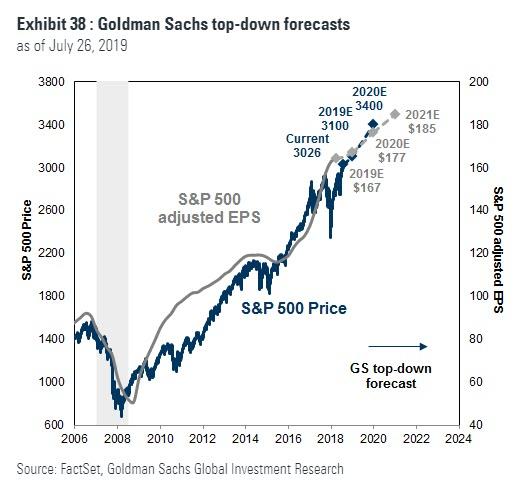

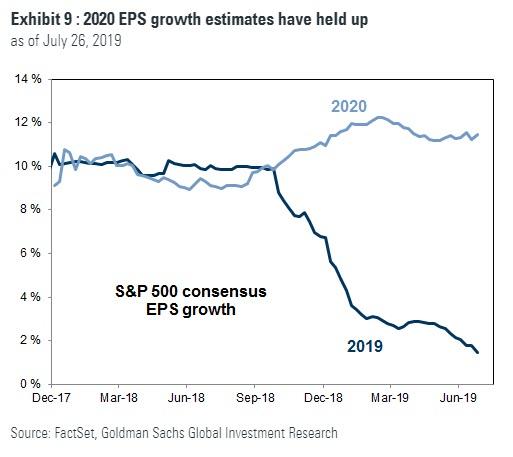

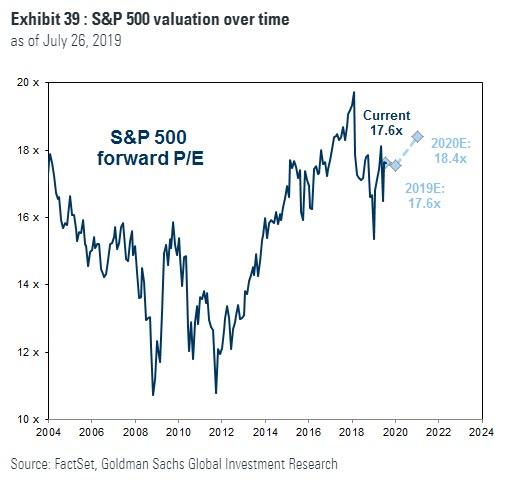

But no worry, Wall Street sees no downside either way, only multiple expansion. Case in point: Goldman raised its price target today for $SPX, 3,100 in 2019 and 3,400 in 2020. Their rationale: Not earnings expansion, no Sir, rather it’s earnings growth reduction and multiple expansion courtesy the Fed:

“David Kostin, the bank’s chief U.S. equity analyst raised his target for the S&P 500 stock index despite lowering his estimate for 2019 earnings-per-share growth from its November estimate of 6% to 3% today, resulting in a higher expected price-to-earnings ratio.

“Our target implies a 3% appreciation through year-end 2019, implying a 24% fully year-gain,” Kostin wrote. “Valuation models have expanded by 22% year-to-date, and the S&P 500 trades at roughly fair value relative to interest rates and profitability.”

Goldman analysts now predicts the S&P 500 forward price-to-earnings multiple will end the year at 17.6 times earnings, a marked increase from the 16 times predicted in their 2019 outlook published in November.

The bank sees Federal Reserve policy as a key driver of higher valuations, as it earlier predicted the Fed would raise interest rates 100 basis points in 2019, but now see the fed funds rate ending the year 50 basis points lower.”

As I’ve said many times: The Fed is the market’s primary price discovery mechanism and looks like Goldman implicitly agrees.

And it is very much self evident in investor behavior:

Whatever decision the Fed will make on Wednesday be sure it will be keeping 3 data points in mind: $SPX, $NDX & $DJIA.

Enjoy the rate cut show.

* * *

For the latest public analysis please visit NorthmanTrader. To subscribe to our market products please visit Services.

via ZeroHedge News https://ift.tt/2ypIixA Tyler Durden

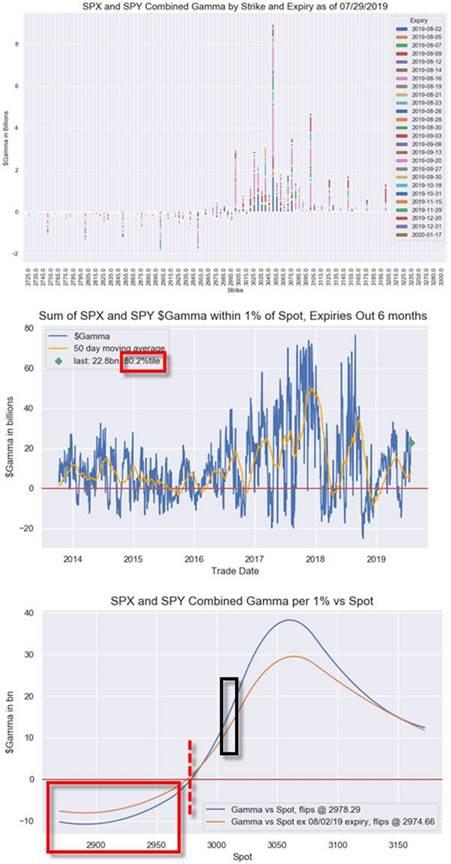

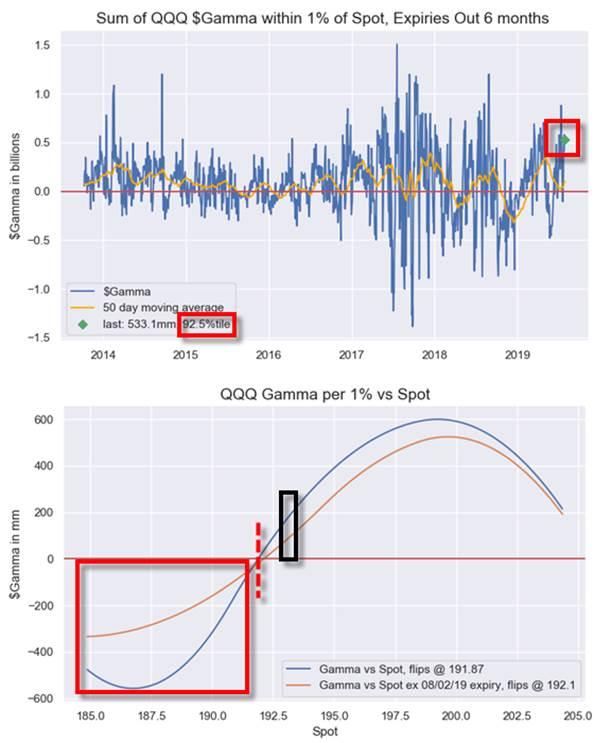

With all eyes focused on whether Jay Powell will go 25, 50, and/or end QT, Nomura’s Charlie McElligott notes that dealers are generally positioned aggressively long and additionally ‘long gamma’. However, given the potential for some serious volatility tomorrow, what levels should investors be watching for chaotic unwinds to begin.

Via Nomura,

Our analysis shows that Dealers are currently “long Gamma” across combined SPX / SPY options, with $Gamma at 80th %Ile since 2013.

However, we would see that position “flip” to “Short Gamma” down at 2978, or 2974 ex the 8/2/19 expiry

Strikes that matter: 3050 ($9.375B), 3100 ($5.000B) and 3000 ($4.507B)

Also worth noting is the VERY long positioning in crowded Nasdaq.

This leaves QQQ too nearing a flip from current Dealer “Long Gamma” positioning to the “Short Gamma” flip-zone at 191.87 / 192.10 (ex 8/2/19 expiry)…

Particularly relevant at the $Gamma is currently extreme at 92.5 %ile since 2003.

Trade accordingly.

via ZeroHedge News https://ift.tt/2YcehAB Tyler Durden

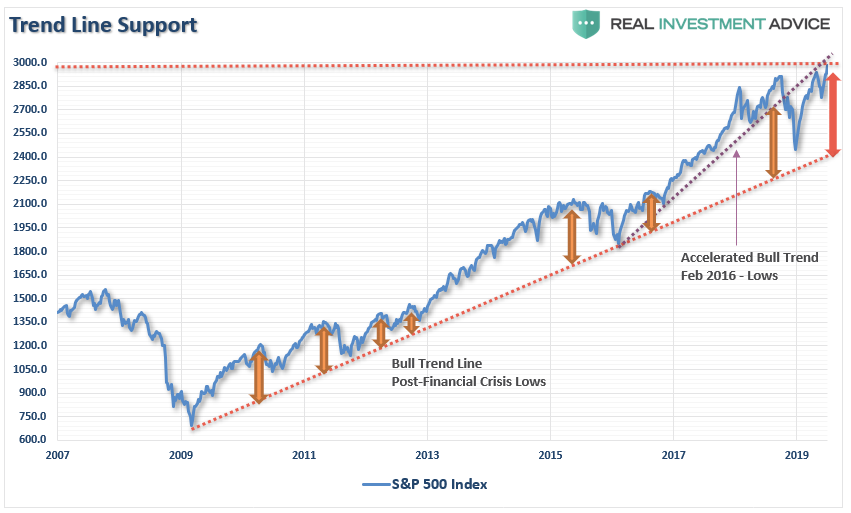

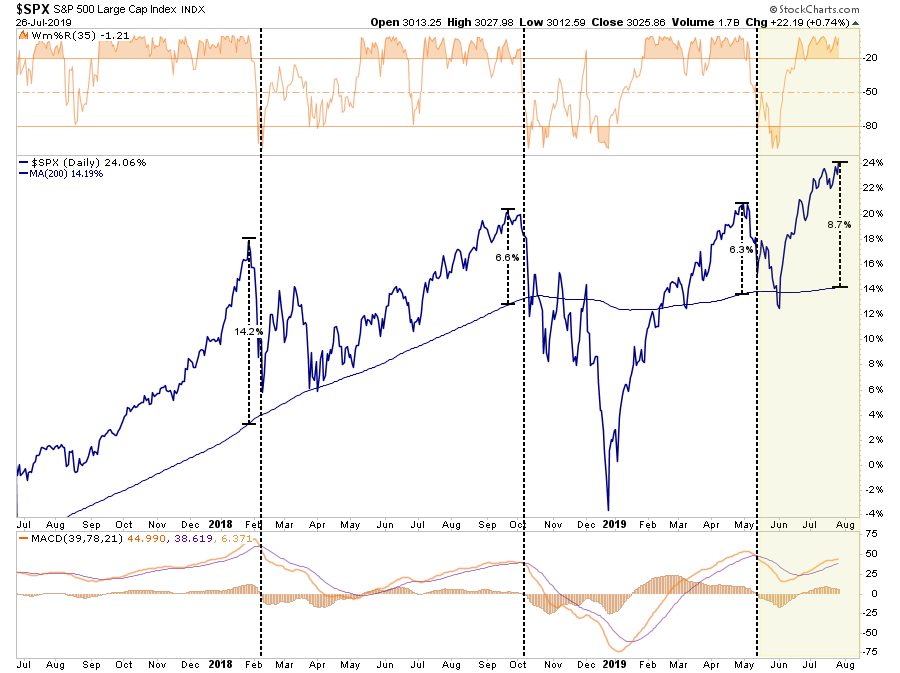

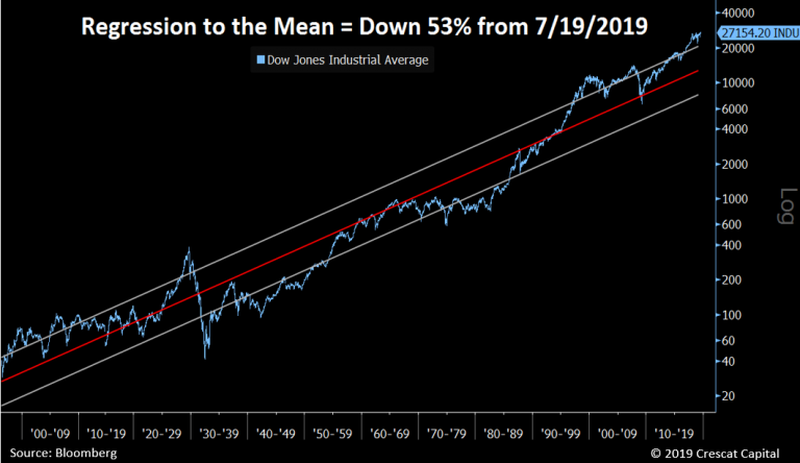

In this past weekend’s newsletter, I discussed the rather severe extensions of the market above both the longer-term bullish trend and the 200-dma. To wit:

There is also just the simple issue that markets are very extended above their long-term trends, as shown in the chart below. A geopolitical event, a shift in expectations, or an acceleration in economic weakness in the U.S. could spark a mean-reverting event which would be quite the norm of what we have seen in recent years.”

“As shown below, while the market is on a near-term “buy signal”(lower panel) the overbought condition, and near 9% extension above the 200-dma, suggests a pullback is in order.”

Of course, discussing the potential of a market correction is almost always perceived as being “bearish.” Therefore, by extension that must mean that I am either all in cash or shorting the market. In either case, it is assumed I “missed out” on previous advances.

If you have been reading our work for long, you already know we have remained primarily invested in the markets, but hedge our risk with fixed income and cash, despite our “bearish” views. I am reminded of something famed Morgan Stanley strategist Gerard Minack said once:

“The funny thing is there is a disconnect between what investors are saying and what they are doing. No one thinks all the problems the global financial crisis revealed have been healed. But when you have an equity rally like you’ve seen for the past four or five years, then everybody has had to participate to some extent.

What you’ve had are fully invested bears.”

While the mainstream media continues to misalign individuals expectations by chastising them for “not beating the market,” which is actually impossible to do, the job of a portfolio manager is to participate in the markets with a predilection toward capital preservation. This is an important point:

“It is the destruction of capital during market declines that have the greatest impact on long-term portfolio performance.”

It is from that view, as a portfolio manager, the idea of “fully invested bears” defines the reality of the markets that we live with today. Despite the understanding the markets are overly bullish, extended and overvalued, portfolio managers must stay invested or suffer potential “career risk” for underperformance.What the Federal Reserve’s ongoing interventions have done is push portfolio managers to chase performance despite concerns of potential capital loss.

Managing portfolios for both risk adjusted returns while protecting capital is a delicate balance. Each week in the Real Investment Report(click here for free weekly e-delivery) we discuss the risks and challenges of the current market environment and report on how we are adjusting our exposures to the market over time. I wanted to share these charts from our friends at Crescat Capital which are all sending an important message. Currently, these are “risks” the market is ignoring, but eventually they will matter, and they will matter a lot.

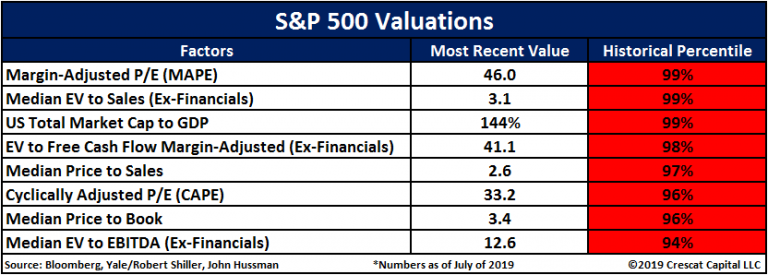

Valuations

One of the consistent drivers behind the bull market over the last few years has been the idea of the “Fed Put.”As long as the Federal Reserve was there to “bailout” the markets if something went wrong, there was no reason NOT to be invested in equities. In turn, this has pushed investors to not only “chase yield,”due to artificially suppressed interest rates but to push valuations on stocks back to levels only seen prior to the turn of the century. As Crescat notes:

“ The reality is that stocks have never been this expensive for how low the 10-year Treasury yield is today. It’s true that all else equal, low interest rates justify higher valuations. However, the lowest interest rates historically haven’t corresponded to the highest P/E markets because extremely depressed yields also signal fundamental problems in the economy. Ultra-low rate environments are often marked by highly leveraged economies where future growth is likely to be weak.”

Given that valuations are all in the 90th percentile of historical values, it suggests that a reversion to the mean is increasingly likely.

Given these valuations are occurring against a backdrop of deteriorating economic growth and corporate profits, the risk to investor capital is high.

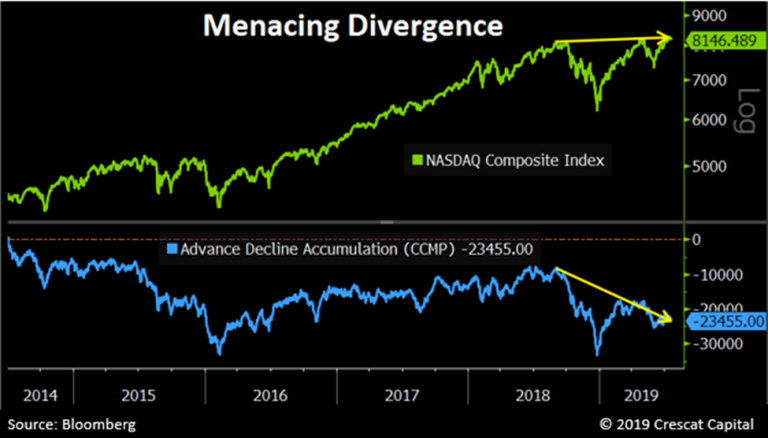

Divergences

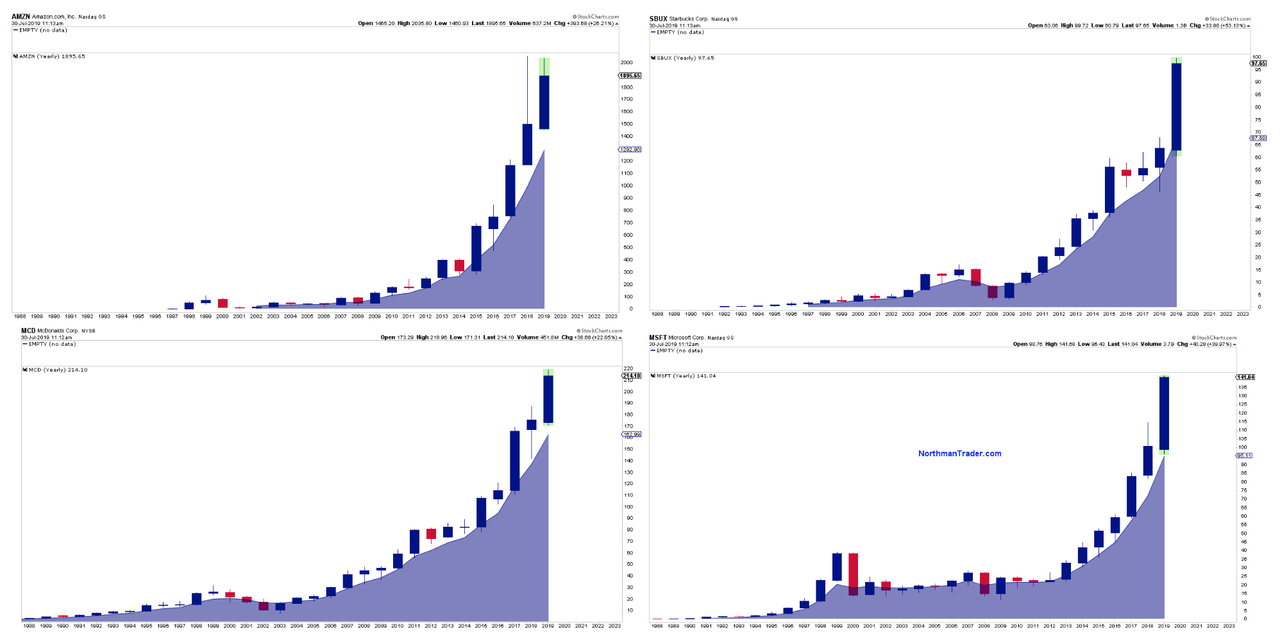

I have previously addressed the narrowing of participation in the markets. Much of the advance in the markets this year alone can be solely accounted for by a handful of mega-capitalization stocks. Since those mega-cap reside in both the Nasdaq and the S&P 500 index, the lack of breadth is worth noting. As Crescat points out:

“While many US equity indices have marginally broken out to new highs recently, they have done so in the face of weakening market internals. Equity indices are being propped up by a narrowing group of leaders. The deteriorating breadth is most evident in the NASDAQ Composite, home to today’s leading growth stocks. While the overall index has reached record levels, the number of declining stocks has significantly outpaced the number of advancing stocks since last September. The collapsing internals point to an exhausted bull market.”

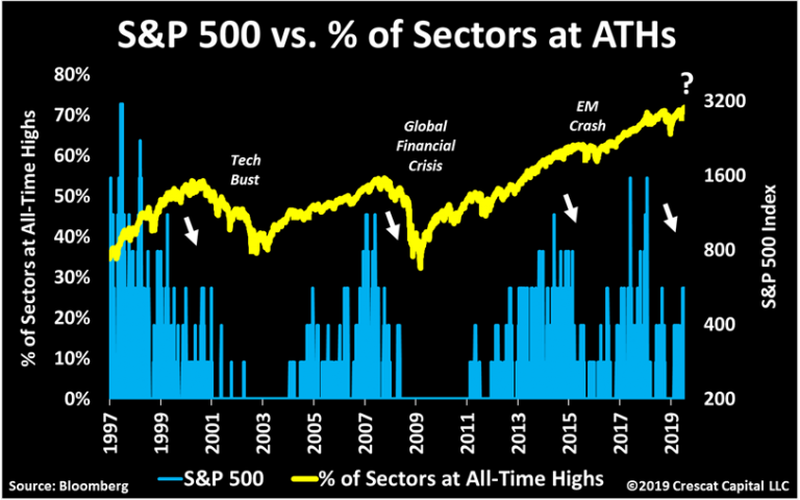

Volume & Participation

Another warning sign is that volume and participation have have also weakened markedly. These are all signs of a market advance nearing “exhaustion.” Back to Crescat:

“Stocks are also rising in defiance of extremely low volume. On July 16th, the SPDR S&P 500 ETF (SPY) had its lowest daily volume in almost 2 years. In a 15-daily average terms, volume is now as low as it was at the peak of the housing bubble and prior to the last two selloffs in 2018. Unusual calmness and breadth deterioration are not a good set up for record overvalued stocks.”

“The following chart is yet another illustration of how this recent rally in equities is running on empty, and again lacking substance. On July 15th, S&P 500 reached record levels, but only three sectors were at all-time highs. Market breadth today is faltering just as much as it did ahead of the last two recessions. In 2015, this was also the case, but back then only 20% of the yield curve was inverted. Now it’s close to 60%!”

Deviation

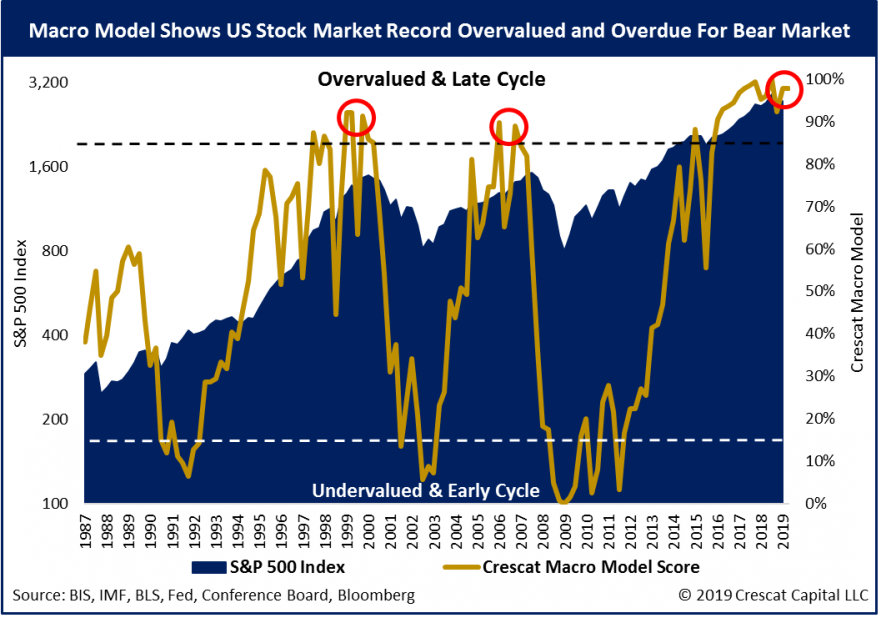

I have written many times in the past that the financial markets are not immune to the laws of physics. As I started out this missive, the deviation between the current market and long-term means is at some of the highest levels in market history.

There is a simple rule for markets:

“What goes up, must, and will, eventually come down.”

The example I use most often is the resemblance to “stretching a rubber-band.” Stock prices are tied to their long-term trend which acts as a gravitational pull. When prices deviate too far from the long-term trend they will eventually, and inevitably, “revert to the mean.”

As Crescat laid out, a “mean reverting” event would currently encompass a 53% decline from recent peaks.

Does this mean the current bull market is over?

No.

However, it does suggest the “risk” to investors is currently to the downside and some caution with respect to equity-based exposure should be considered.

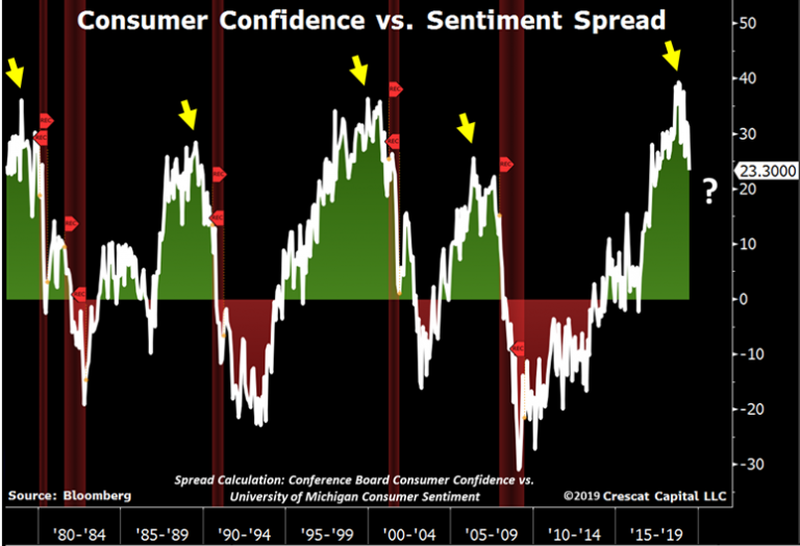

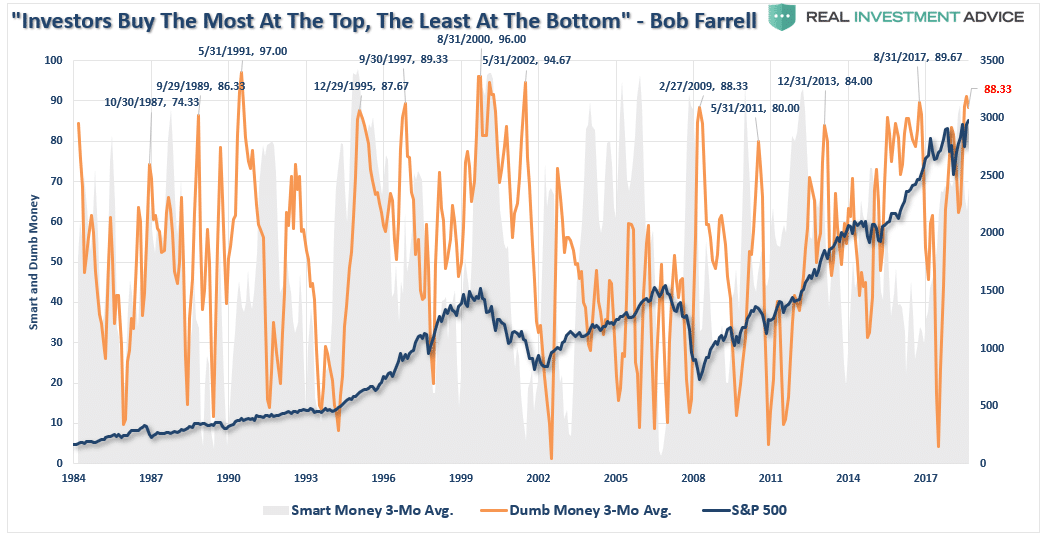

Sentiment

Lastly, is investor sentiment. When sentiment is heavily skewed toward those willing to “buy,” prices can rise rapidly and seemingly “climb a wall of worry.” However, the problem comes when that sentiment begins to change and those willing to “buy” disappear.

This “vacuum” of buyers leads to rapid reductions in prices as sellers are forced to lower their price to complete a transaction. The problem is magnified when prices decline rapidly. When sellers panic, and are willing to sell “at any price,” the buyers that remain gain almost absolute control over the price they will pay. This “lack of liquidity” for sellers leads to rapid and sharp declines in price, which further exacerbates the problem and escalates until “sellers” are exhausted.

With sentiment currently at very high levels, combined with low volatility and excess margin debt, all the ingredients necessary for a sharp market reversion are present. Am I sounding an “alarm bell” and calling for the end of the known world?

Of course, not.

However, I am suggesting that remaining fully invested in the financial markets without a thorough understanding of your “risk exposure” will likely not have the desirable end result you have been promised. All of the charts above have linkages to each other, and when one goes, they will all go.

So pay attention to the details.

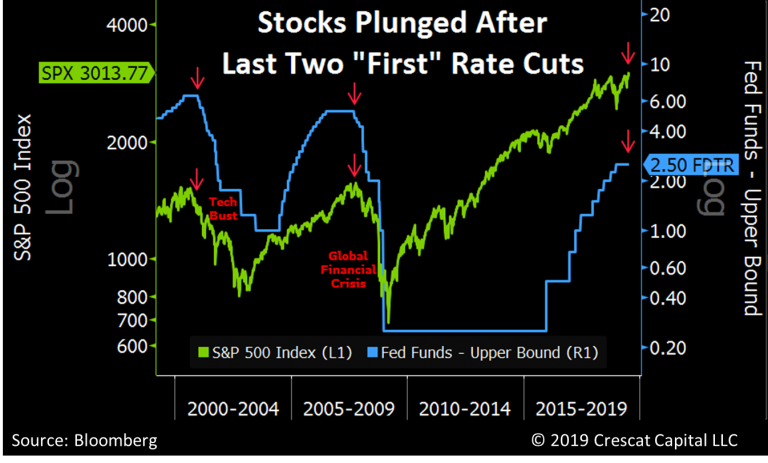

The markets currently believe that when the Fed cuts rates this week, the bull market will continue higher. Crescat, and history, suggest a different outcome.

As I stated above, my job, like every portfolio manager, is to participate when markets are rising. However, it is also my job to keep a measured approach to capital preservation.

Yes, I am bearish on the longer-term outlook of the markets for the reasons, and many more, stated above.

Just make sure you understand that I am an “almost fully invested bear.”

At least for now.

But that can, and will, rapidly change as the indicators I follow dictate.

What’s your strategy?

via ZeroHedge News https://ift.tt/2GEonPQ Tyler Durden

The U.S. Court of Appeals for the District of Columbia Circuit has ordered the Drug Enforcement Agency (DEA) to explain why it has yet to respond to nearly two dozen researchers around the U.S. who applied three years ago for a DEA license to grow research cannabis.

“Hopefully, DEA will finally explain, in a court-filing available for public inspection, the answer to this question that has frustrated everyone,” announced Sue Sisley, a physician and researcher at the Scottsdale Research Institute, a Phoenix-based clinical trial company that applied in 2016 for a DEA manufacturing license in order to grow its own cannabis for an ongoing study of medical marijuana as a treatment for veterans suffering from PTSD.

The Scottsdale Research Institute (SRI) sued the Justice Department and the DEA in June. It sought a “writ of mandamus” that would compel the DEA to respond to applicants seeking a license. SRI argued that the Improving Regulatory Transparency for New Medical Therapies Act, signed by President Obama in November 2015, requires “that the Attorney General, upon receiving an application to manufacture a Schedule I substance for use only in a clinical trial, publish a notice of application not later than 90 days after accepting the application for filing.” SRI and more than 20 other potential cannabis manufacturers applied for licenses from the DEA in 2016, but a notice of their applications has yet to appear in the Federal Register.

“Thus,” RSI’s suit argued, “agency action has been unlawfully withheld. And in view of an express directive to prioritize applications relating to clinical research, agency action has most certainly been unreasonably delayed.”

Despite congressional appeals to the DEA to complete the application review process, the applicants I’ve spoken to say they’ve received no substantive updates from the agency in over a year, and no applicant I spoke with has been contacted by their local DEA field office to schedule an inspection of their facilities, a crucial early step in the review process.

Sisley’s lawsuit and the court’s order are particularly newsworthy due to the lack of domestically grown cannabis suitable for research with human subjects. The University of Mississippi has the only DEA license for cannabis manufacturing in the U.S. and operates a 12-acre outdoor growing facility under a contract with the National Institutes for Drug Abuse, which is housed within the Department of Health and Human Services. Despite DEA claims to the contrary, researchers say that Mississippi’s cannabis is inadequate for testing in human subjects.

The Mississippi cannabis made available to Sisley and her team “arrived in powdered form, tainted with extraneous material like sticks and seeds, and many samples were moldy,” SRI’s lawsuit claimed. “Whatever reasons the government may have for sanctioning this cannabis and no other, considerations of quality are not among them. It is not suited for any clinical trials, let alone the ones SRI is doing.” What’s more, federal regulations prohibit the use of Mississippi’s cannabis in phase III clinical trials and thus make it practically impossible to develop pharmaceutical products using domestically grown cannabis.

Since August 11, 2016, when the DEA published an announcement in the Federal Register inviting applications for bulk cannabis manufacturers, Republican and Democratic members of both the House of Representatives and the Senate have sent multiple queries to the Justice Department requesting an update on the status of some two dozen applications.

In several appearances before Congress, then-Attorney General Jeff Sessions insisted that the Justice Department was limited by the United Nations Single Convention on Narcotic Drugs. However, many researchers in the U.S. legally import research cannabis from fellow convention signatories Israel and Canada, and the Food and Drug Administration last year approved Epidiolex, a drug developed using cannabis grown in the United Kingdom, another signatory of the narcotics treaty. In addition, the DEA regularly approves applications for the domestic manufacturing of other schedule I drugs, including synthetic cannabis.

The D.C. Circuit has instructed the DEA to respond to SRI’s suit by August 28, 2019. The lawsuit is available here.

from Latest – Reason.com https://ift.tt/2KcJppX

via IFTTT

The U.S. Court of Appeals for the District of Columbia Circuit has ordered the Drug Enforcement Agency (DEA) to explain why it has yet to respond to nearly two dozen researchers around the U.S. who applied three years ago for a DEA license to grow research cannabis.

“Hopefully, DEA will finally explain, in a court-filing available for public inspection, the answer to this question that has frustrated everyone,” announced Sue Sisley, a physician and researcher at the Scottsdale Research Institute, a Phoenix-based clinical trial company that applied in 2016 for a DEA manufacturing license in order to grow its own cannabis for an ongoing study of medical marijuana as a treatment for veterans suffering from PTSD.

The Scottsdale Research Institute (SRI) sued the Justice Department and the DEA in June. It sought a “writ of mandamus” that would compel the DEA to respond to applicants seeking a license. SRI argued that the Improving Regulatory Transparency for New Medical Therapies Act, signed by President Obama in November 2015, requires “that the Attorney General, upon receiving an application to manufacture a Schedule I substance for use only in a clinical trial, publish a notice of application not later than 90 days after accepting the application for filing.” SRI and more than 20 other potential cannabis manufacturers applied for licenses from the DEA in 2016, but a notice of their applications has yet to appear in the Federal Register.

“Thus,” RSI’s suit argued, “agency action has been unlawfully withheld. And in view of an express directive to prioritize applications relating to clinical research, agency action has most certainly been unreasonably delayed.”

Despite congressional appeals to the DEA to complete the application review process, the applicants I’ve spoken to say they’ve received no substantive updates from the agency in over a year, and no applicant I spoke with has been contacted by their local DEA field office to schedule an inspection of their facilities, a crucial early step in the review process.

Sisley’s lawsuit and the court’s order are particularly newsworthy due to the lack of domestically grown cannabis suitable for research with human subjects. The University of Mississippi has the only DEA license for cannabis manufacturing in the U.S. and operates a 12-acre outdoor growing facility under a contract with the National Institutes for Drug Abuse, which is housed within the Department of Health and Human Services. Despite DEA claims to the contrary, researchers say that Mississippi’s cannabis is inadequate for testing in human subjects.

The Mississippi cannabis made available to Sisley and her team “arrived in powdered form, tainted with extraneous material like sticks and seeds, and many samples were moldy,” SRI’s lawsuit claimed. “Whatever reasons the government may have for sanctioning this cannabis and no other, considerations of quality are not among them. It is not suited for any clinical trials, let alone the ones SRI is doing.” What’s more, federal regulations prohibit the use of Mississippi’s cannabis in phase III clinical trials and thus make it practically impossible to develop pharmaceutical products using domestically grown cannabis.

Since August 11, 2016, when the DEA published an announcement in the Federal Register inviting applications for bulk cannabis manufacturers, Republican and Democratic members of both the House of Representatives and the Senate have sent multiple queries to the Justice Department requesting an update on the status of some two dozen applications.

In several appearances before Congress, then-Attorney General Jeff Sessions insisted that the Justice Department was limited by the United Nations Single Convention on Narcotic Drugs. However, many researchers in the U.S. legally import research cannabis from fellow convention signatories Israel and Canada, and the Food and Drug Administration last year approved Epidiolex, a drug developed using cannabis grown in the United Kingdom, another signatory of the narcotics treaty. In addition, the DEA regularly approves applications for the domestic manufacturing of other schedule I drugs, including synthetic cannabis.

The D.C. Circuit has instructed the DEA to respond to SRI’s suit by August 28, 2019. The lawsuit is available here.

from Latest – Reason.com https://ift.tt/2KcJppX

via IFTTT