At the start of August, we explained how – by scapegoating the global economy for the Fed’s July 31 rate cut – the central bank had now trapped itself, having certified before the world that any further escalations in Trump’s trade war are effectively a justification for more rate cuts. Whether this was Powell’s intention is unclear, although as we said at the time, “it certainly means that Trump is now de facto in charge of the Fed’s monetary policy by way of US foreign policy, and it also means that as BofA wrote, “the Fed is unintentionally underwriting the trade war.”

Here, the only thing one can perhaps add is that the Fed may very well be intentionally underwriting Trump’s trade war. In either case, as Bank of America’s chief economist Michelle Meyer said, such a circular framework is a problem for many reasons, and as the bank admits, it is worried about an adverse feedback loop where the trade war hinders economic growth, therefore prompting additional Fed easing, which in turn allows for greater trade war escalation. This is shown in the chart below.

Fast forward to today, when in what in retrospect may be seen as a watershed moment in exposing just how “political” the Federal Reserve always has been despite repeated lies by various officials claiming otherwise, none other than former Goldman chief economist and the former head of the NY Fed, Bill Dudley, after looking at the chart above and having realized that the Fed is underwriting Trump’s trade war, made a “modest proposal” in a Bloomberg op-ed in which he advised Powell to take a political stand against enabling Trump’s trade war, and potentially go so far as to push the economy into a recession to prevent Trump from getting reelected!

Echoing what Powell said in his Jackson Hole speech, where he dedicated a section to Trump’s ongoing trade wars, and blaming them for the Fed’s rising inability to interfere in the US economy, Dudley begins with what is a clear political statement, arguing that “Donald Trump’s trade war with China keeps undermining the confidence of businesses and consumers, worsening the economic outlook.”

Dudley, who was among those globalists who enabled China’s tremendous ascent, and assured that Beijing will surpass the US economically and militarily at some point by 2032 if the status quo is left unchanged…

… ignores the consequences of his actions, and instead slams Trump for being the one president willing to challenge China’s hegemonic ascent and upcoming Thucydides Trap (which as we noted before virtually assures war with China if nothing is done), saying that “this manufactured disaster-in-the-making presents the Federal Reserve with a dilemma: Should it mitigate the damage by providing offsetting stimulus, or refuse to play along?”

Dudley’s advice: “If the ultimate goal is a healthy economy, the Fed should seriously consider the latter approach.”

While Dudley then spend the bulks of his op-ed explaining the diagram shown at the top, a relationship which our readers are already familiar with, what is of particular note is Dudley’s discussion of why the Fed should ‘refuse to play along’ and refuse to underwrite, as BofA said, Trump’s trade war.

One thing Dudley recommends is that “the Fed could go much further” beyond merely warning, as Powell did, that the Fed’s tools are not suited to mitigating the damage from trade war, but “could state explicitly that the central bank won’t bail out an administration that keeps making bad choices on trade policy, making it abundantly clear that Trump will own the consequences of his actions.”

Economic threat.

What immediately stands out here is that it is only Bill Dudley’s subjective opinion that Trump is making “bad choices” on trade policy, an argument that immediately becomes political when one considers that Trump was elected on a platform of, among other things, reducing the US-China trade deficit and, by extension, limiting China’s economic growth which if left unchecked, would assure war between the two superpowers.

No, instead to Dudley, what a myopic Trump should focus on is today and tomorrow, and leave the long-term to someone else. In other words, do precisely what the Fed has been doing for decades, even though as Mark Carney recently hinted, it was the Fed’s monetary policy, that has been responsible for much of the world’s crises and wars. You won’t find a discussion of that in Dudley’s brief op-ed, however.

Going back to Dudley’s argument, the former Goldman banker claims that “such a harder line could benefit the Fed and the economy in three ways”.

First, it would discourage further escalation of the trade war, by increasing the costs to the Trump administration.

Second, it would reassert the Fed’s independence by distancing it from the administration’s policies.

Third, it would conserve much-needed ammunition, allowing the Fed to avoid further interest-rate cuts at a time when rates are already very low by historical standards.

Here the narrative gets downright absurd, because while Dudley refers to the Fed as apolitical, underscoring that further in the next paragraph where he says that “I understand and support Fed officials’ desire to remain apolitical”, he immediately refutes himself by admitting that the Fed has never been apolitical and in fact, it is the US central bank that, through its actions chooses who the US president is, to wit:

Central bank officials face a choice: enable the Trump administration to continue down a disastrous path of trade war escalation, or send a clear signal that if the administration does so, the president, not the Fed, will bear the risks — including the risk of losing the next election.

And the punchline: “There’s even an argument that the election itself falls within the Fed’s purview.”

Translation: “there is even an argument”, Dudley implies, that the Fed should crush the economy (arguably by hiking or not cutting rates) and start the next recession, thereby preventing Trump from getting re-elected.

And while we appreciate Dudley’s de facto confirmation of what we have said for years, namely that the Fed is not only a political entity, one which picks the US president as the former NY Fed president admitted, but that the Fed is an even more powerful entity than the top US executive (an entity which as Bernanke’s former advisor once said: “people would be stunned to know the extent to which the Fed is privately owned”). One hopes that finally a discussion can take place, whether in Congress or elsewhere, if such an entity should exist.

As for Dudley’s “modest proposal”, we look forward to Trump’s response, because if there is one thing the US president needed in writing, it was just such an op-ed, one written from a former Fed member to the current Fed chair, recommending what amounts to mutiny against Trump should Trump proceed with his current course of action. Because if things don’t work out, well Trump now has documentary evidence that, by extension, the Fed also had the ability to ensure his re-election, and if things seem like they are headed off course on the way to November 2020, we will sit back and enjoy as the war between Trump and the Fed goes nuclear.

via ZeroHedge News https://ift.tt/2PjL2aY Tyler Durden

In what will likely be remembered as one of his more desperate and transparent bids to start a fire under the market, President Trump tweeted early Monday morning that his team had received multiple calls from Beijing about the prospects for restarting trade talks. However, China swiftly denied this, and insisted that it had no knowledge of any calls going out to the Trump Administration.

And on Tuesday, more than 24 hours after the supposed ‘olive branch’ was offered, China’s Foreign Minister clarified that it it still isn’t aware of any calls to President Trump’s camp, like the one the president described in his tweet.

A spokesman for the foreign ministry also complained about the US’s ‘regretful’ decision to move ahead with raising tariffs again.

Speaking to Bloomberg, a spokesman for the foreign ministry said he wasn’t aware of any detente between Washington and Beijing.

“I’m not aware of that,” Chinese Foreign Ministry spokesman Geng Shuang said at a regular briefing in Beijing on Tuesday.

“Regretfully the U.S. has announced its decision to add new tariffs on Chinese products. Such maximum pressure will hurt both sides and is not constructive at all.”

Trump famously said Monday that the prospects for a deal were better now than at any time in the recent past, though the market largely ignored him as Chinese sources continued to insist that the relationship between the two sides remained strained.

Hu Xijin, the Global Times editor-in-chief, tweeted that, to the best of his knowledge, the two sides hadn’t spoken at all in recent days.

Based on what I know, Chinese and US top negotiators didn’t hold phone talks in recent days. The two sides have been keeping contact at technical level, it doesn’t have significance that President Trump suggested. China didn’t change its position. China won’t cave to US pressure.

During a briefing on Tuesday, Geng reiterated China’s view, saying it hoped “the US can exercise restraint, come back to reason and create conditions for our consultation based on mutual respect equality and mutual benefit.”

Meanwhile, China’s top trade negotiator, Vice Premier Liu He, said Monday that China is “willing to solve the problem through consultation and cooperation with a calm attitude.”

But the People’s Daily warned that the US “shouldn’t misjudge” China’s determination to retaliate if the US follows through with its plans to raise tariffs.

via ZeroHedge News https://ift.tt/2KXVb95 Tyler Durden

In the U.S., corporate insiders have been selling stocks at an average rate of 600 million dollars per day during the month of August.

This kind of wild selling indicates that there is a tremendous amount of fear among corporate insiders right now, and such selling would only make sense if a stock market crash is imminent. And without a doubt, we have already seen volatility return to Wall Street in a major way as our trade war with China has dramatically escalated. Many Americans are hoping that things will start to calm down and that our trade conflict with China can be resolved calmly, because if things take a bad turn many analysts are warning that we could soon be facing the worst financial crisis since 2008. Here is one example…

Remember the brutal sell-off last year when stocks suffered their worst December since the Great Depression? Something worse than that could happen in days, a Nomura analyst said.

Macro and quant strategist Masanari Takada turned heads earlier this month with his bold call for a “Lehman-like” plunge. He’s sticking with this prediction as market sentiment shows no signs of improving, leading him to believe a monster sell-off could arrive this week.

With chilling forecasts like that being thrown around on a regular basis these days, it is understandable that corporate insiders would be tempted to get out of the market, and right now they are racing for the exits at a pace that is absolutely breathtaking. The following comes from CNN…

Corporate insiders have sold an average of $600 million of stock per day in August, according to TrimTabs Investment Research, which tracks stock market liquidity.

August is on track to be the fifth month of the year in which insider selling tops $10 billion. The only other times that has happened was 2006 and 2007, the period before the last bear market in stocks, TrimTabs said.

In other words, the last time we saw corporate insiders dump stocks like this was just before the last financial crisis.

Clearly, many among the elite are preparing for the worst. They can see financial disaster looming on the horizon, and they are getting out of the market while the getting is still good.

On the other hand, there are multitudes of Americans out there that are completely convinced that President Trump will be able to successfully navigate us through any storms that may be ahead.

When Barack Obama was in the White House, national interest in prepping soared to all-time highs, but since Trump entered the White House things have completely reversed. The following comes from Business Insider…

But since President Trump took office in 2016, prepping has taken a dive nationwide. There are fewer prepper conventions held across the US, and several prepper business owners who spoke with Business Insider (as well as Mills), say the prepping community is not as active as it was three years ago. It’s an indication of how Trump relieves many of the worst fears of his voters, including conservative preppers.

“It definitely seems to be cycling with the White House,” prepper and inventorMikhail Merkurieff, who builds and sells prepping and camping tools including stoves, cooking utensils, and portable shelters, told Business Insider.

With a Republican in the White House, many conservatives simply do not see any reason to prep anymore, and so things are completely different than they were about four or five years ago. Many former preppers seem to believe that having Trump in the Oval Office means that “we don’t have to worry about anything”…

Rick Austin, who organizes a popular “Prepper Camp” in the hills of North Carolina every year, which is attended by roughly 1,400 worst-case-scenario preparers hoping to beef up their skills, also noted a downturn.

“Businesses are down because people have kind of gone, ‘Oh, you know, Trump’s in office, we don’t have to worry about anything,’” he said while milking his goats from an “undisclosed location” in the Appalachian Mountains.

So we are witnessing something extremely strange right now.

Corporate insiders and the Wall Street elite are feverishly preparing as if a “perfect storm” was about to strike, but meanwhile millions upon millions of hardcore conservatives feel completely relaxed because they feel like Trump has everything under control.

And President Trump did cause quite a turnaround in the financial markets on Monday when he told the press that China had called and had requested a return to the negotiating table…

“China called last night our top trade people and said. ‘Let’s get back to the table,’ so we will be getting back to the table and I think they want to do something. They have been hurt very badly but they understand this is the right thing to do and I have great respect for it. This is a very positive development for the world,” Trump said.

In Beijing, Foreign Ministry spokesman Geng Shuang said he was not aware that a phone call between the two sides had taken place. And Hu Xijin, editor-in-chief of Chinese state-run newspaper the Global Times, denied that negotiators had held the phone calls Trump described.

“China didn’t change its position. China won’t cave to U.S. pressure,” said Hu, who is widely seen as a mouthpiece for Beijing’s messaging.

We shall see where things go from here.

It would certainly be a step in the right direction if the two sides start talking again, and the Chinese have definitely expressed a desire to avoid any further escalations…

In response, Chinese Vice Premier Liu He told a state-controlled newspaper on Monday that “China is willing to resolve its trade dispute with the United States through calm negotiations and resolutely opposes the escalation of the conflict,” Reuters first reported, citing a transcript of his remarks provided by the Chinese government. Liu is China’s top trade negotiator.

Speaking at a technology conference in China, Liu added: “We believe that the escalation of the trade war is not beneficial for China, the United States, nor to the interests of the people of the world.”

But with a presidential election looming about a year away, the Chinese are simply not going to accept any deal that is appreciably different from what they expect that they could get from Joe Biden or Elizabeth Warren.

And it is also very unlikely that President Trump will cave in and give the Chinese what they want. So ultimately we will see episodes of hope on Wall Street on the days when it looks like the two sides may start talking again, but there won’t be a deal any time soon.

At this moment, corporate insiders are dumping stocks as if “the everything bubble” was about to burst in a major way. And if those corporate insiders are correct, millions upon millions of other Americans will be completely and utterly unprepared for what is about to happen.

via ZeroHedge News https://ift.tt/2Hvv5IC Tyler Durden

While we may preserve information about your account, we have not turned over any information. We will not turn over any information unless we receive a valid request for the information, or a court order. If we do receive such a request, unless we are legally prohibited from doing so, we will inform you and provide you time when you may attempt to quash or legally challenge the request….

While we may preserve information about your account, we have not turned over any information. We will not turn over any information unless we receive a valid request for the information, or a court order. If we do receive such a request, unless we are legally prohibited from doing so, we will inform you and provide you time when you may attempt to quash or legally challenge the request….

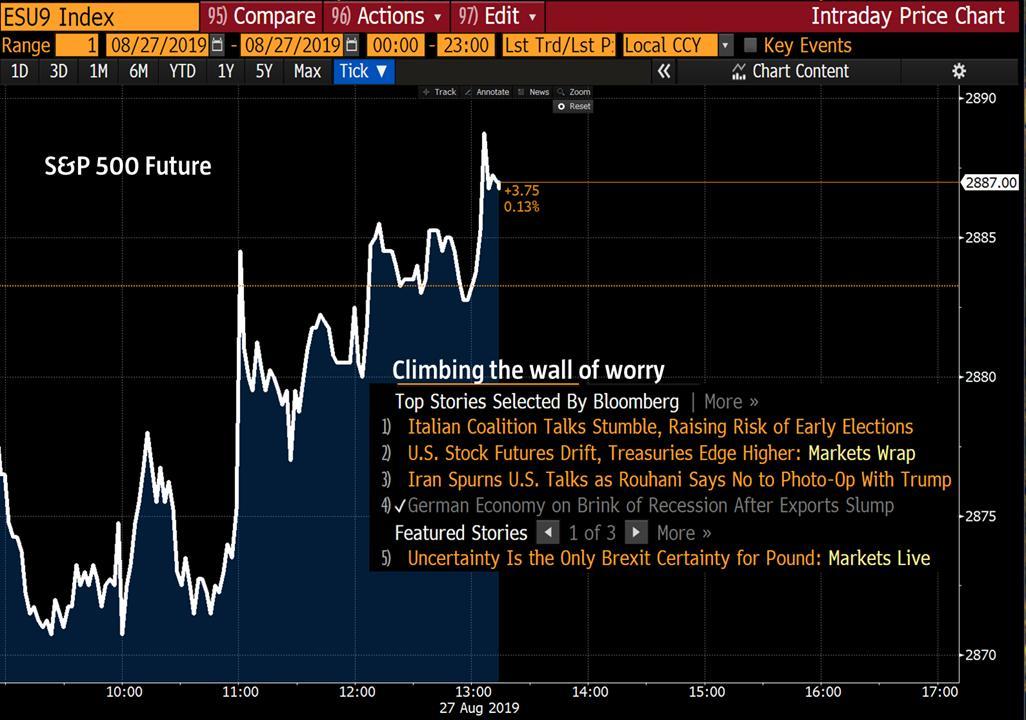

In what has been a relatively quiet session, US equity futures and European stocks first drifted lower as trade war concerns dominated the early part of the trading session when China’s Communist Party flagship newspaper, People’s Daily, said the U.S. shouldn’t misjudge the nation’s ability and determination to firmly retaliate if America follows through with higher tariffs, before rebounding following positive auto-relative news out of China.

US equity futures faded drifted lower into the European open, erasing much of the last minute burst higher noted at the Monday close…

… before climbing today’s wall of worry, which as Robeko Jeroen Blokland showed, consisted of stumbling Italian coalition, German economic fears and geopolitical concerns about Iran.

Europe’s Stoxx 600 erased a decline of as much as 0.3% as traders shrugged off earlier data showed Germany was on the brink of recession as final Q2 GDP printed at -0.1%…

… with carmakers surging after Xinhua reported that China will ease car-purchase restrictions, and “actively” support purchases of new-energy vehicles in some cities. According to the report, China is considering relaxing and removing restrictions on auto purchases, looking through the full release it appears to be on the domestic front referring to restrictions around the circulation of used cars.

The Stoxx 600 autos rallied 1.1% for a second daily advance, with Porsche, Fiat Chrysler and Volkswagen up 1.3% or more. Suppliers gaining include Pirelli +1.6%, Valeo +1.5%, Hella +1%. The Stoxx 600 traded up 0.3% last, with carmakers as top performers, offsetting declines in media and insurance shares.

Earlier in the session, Asian stocks advanced, led by technology and consumer discretionary firms, after Trump softened his tone toward China, allaying fears for a further escalation of trade tensions. Most markets in the region were up, with China and Indonesia leading gains. The Topix added 0.8%, with technology companies and automakers among the biggest boosts. The Shanghai Composite Index climbed 1.4%, nearly erasing Monday losses, as 360 Security Technology and large financial firms offered strong support. However, as Bloomberg notes, Chinese companies have dialed back dollar-denominated junk bond sales just as demand for the riskier assets weakens. India’s Sensex rose 0.2%, heading for a third day of gains, with ICICI Bank and Larsen & Toubro advancing. The Indian government is deciding whether to use a 1.76 trillion-rupee ($24.4 billion) windfall from the central bank to reduce its borrowing or stimulate the economy.

In Hong Kong, Chief Executive Carrie Lam said her government can handle unrest without assistance from Chinese forces, and still wants to hold talks with protesters despite a flare-up in violence.

But the biggest risk which algos have yet to notice is that the 2s10s curve inverted as much as -2.5bps this morning, the most inverted the curve has been since the financial crisis.

The reason behind today’s inversion: the 10Y yield drifted lower by 3bps to 1.505% while the 2Y was down just 1.3bps pushing the yield curve to the biggest inversion in 12 years. Meanwhile, German Bunds settled down after a few wobbles alongside Gilts and US Treasuries with latest Chinese commentary on trade still suggesting that relations are strained and tetchy compared to President Trump’s more cordial view of the current situation. However, BTPs have pulled back quite sharply from just a few ticks away from 144.00 towards 143.00 on more political party bickering in Rome and another delayed meeting before President Mattarella finally calls time and has to defer to another election.

While futures levitated higher, it was on zero volumes as investors remained cautious over this week’s dialing down of trade tensions as fresh evidence emerged that increased protectionism is weighing more on the global economy – and to blame for Germany’s deepening manufacturing recession. Sentiment remains fragile, according to Bloomberg, as investors remember that previous periods of trade calm have been quickly ended by surprise escalations.

“August may be coming to a close, but volatility does not appear to be going anywhere,” Erik Knutzen, chief investment officer, multi-asset class, at Neuberger Berman, said in a note Tuesday. “As the late cycle continues, markets will likely remain sensitive to the daily news flow, with many letting headlines drive short-term decisions.”

In FX, the yen gained the most among G10 currencies as skepticism sets in about the prospect of any future U.S.-China trade negotiations. Haven assets rose after China’s Communist Party flagship newspaper People’s Daily says the U.S. shouldn’t misjudge the nation’s ability and determination to firmly retaliate if America follows through with higher tariffs. The Bloomberg Dollar Spot Index extended losses after the London open. The euro gained with Italian bonds on hopes the country could avert fresh elections despite reports that negotiations had hit a snag, while the pound rose for a third day in four as the opposition Labour party stepped up efforts to stave off a no-deal Brexit.

Elsewhere, oil futures edged higher after Trump struck a more conciliatory tone on the trade war with China. Gold pushed above $1,530 an ounce.

Market Snapshot

S&P 500 futures down 0.1% to 2,879.75

STOXX Europe 600 down 0.2% to 370.61

German 10Y yield fell 0.7 bps to -0.673%

MXAP up 0.5% to 150.95

MXAPJ up 0.3% to 486.61

Nikkei up 1% to 20,456.08

Topix up 0.8% to 1,489.69

Hang Seng Index down 0.06% to 25,664.07

Shanghai Composite up 1.4% to 2,902.19

Sensex up 0.2% to 37,568.93

Australia S&P/ASX 200 up 0.5% to 6,471.22

Kospi up 0.4% to 1,924.60

Euro up 0.05% to $1.1108

Italian 10Y yield rose 0.9 bps to 0.978%

Spanish 10Y yield fell 2.2 bps to 0.111%

Brent futures up 0.7% to $59.12/bbl

Gold spot up 0.2% to $1,530.84

U.S. Dollar Index down 0.2% to 97.93

Top Overnight News from Bloomberg

A collapse in exports pushed Europe’s largest economy to the brink of recession in the second quarter, in a sign that an increasingly hostile trade war between the U.S. and China is at least partially to blame for Germany’s deepening manufacturing malaise

Trump left the G-7 summit on Monday taking a softer tone toward China, just days after spooking financial markets with another escalation in their trade war

Hong Kong’s leader said her government can handle unrest without assistance from Chinese forces, and still wants to hold talks with protesters despite a flare up in violence

Iran’s top officials all but ruled out talks with the U.S. a day after President Donald Trump extended his most expansive offer yet to the Islamic Republic. The U.S. must lift sanctions on Iran if it wants to negotiate, President Hassan Rouhani said on Tuesday

Asian stock markets were higher as they followed suit to the rebound across their global peers after US President Trump provided a more conciliatory tone at the G7 regarding US-China trade, while he was also optimistic about reaching a deal with EU and was open to meeting Iran President Rouhani under the right circumstances. ASX 200 (+0.5%) was led by the tech sector amid trade hopes and as retailers cheered encouraging earnings from Wesfarmers, while Nikkei 225 (+1.0%) rode on the currency wave and eyed a reclaim of the 20.5k level. Shanghai Comp. (+1.4%) was underpinned after US President Trump’s softer tone on China in which he suggested that negotiations will begin shortly and thinks a deal will be reached. Furthermore, the PBoC injected liquidity through reverse repos and Chinese Industrial Profits returned to growth, although Hang Seng (Unch.) lagged amid a deluge of earnings, ongoing unrest and continued contraction in both Imports and Exports. Finally, 10yr JGBs weakened amid the improvement in risk sentiment and as prices homed in on the 155.00 level to the downside, although it eventually found some mild support following improved demand at the enhanced liquidity auction for super-long JGBs.

Top Asian News

India Is Said to Mull Cutting Borrowings After Record Windfall

Hedge Funds Betting on Yen Strength Have One Implacable Foe

Iran Spurns U.S. Talks as Rouhani Says No to Photo-Op With Trump

European equities are mixed [Eurostoxx 50 +0.2%] following on from a mostly higher Asia-Pac handover as optimism surrounding President Trump’s conciliatory tone somewhat waned. Italy’s FTSE MIB (+1.0%) outperforms its peers as the Italian political landscape seems to be shifting away from a snap election, with a PD/5SM coalition seemingly materialising, albeit some sticking points remain around Conte’s role. Sectors are also mixed with the energy sector outperforming amid price action in the oil complex, whilst consumer discretionary follows a close second amid reports that China considers relaxing and removing restrictions on auto purchases, albeit it appears to be on the domestic front referring to restrictions around the circulation of used cars. Nonetheless, the European car and auto supplier index rose 1.0% amid hopes of spurred activity in China. In terms if individual movers, G4S (+1.9%) and E.ON (+1.5%) shares are supported by positive broker moves at RBC and Barclays respectively. Also of note, US judge ruled against Johnson & Johnson (JNJ) in a landmark opioid case in Oklahoma. JNJ have been ordered to pay USD 572mln; however, the fine is less than investors had feared it may be, thus the Co. are +1.9% in the pre-market.

Top European News

Weidmann Revisits Dr. No Stance as ECB Stimulus Decision Nears

Siemens, GM Fuel Bond-Sales Rebound as Market Wakes After Lull

In Switzerland, the Trade War Is Mixing Up a Painful Cocktail

Norway’s $1 Trillion Wealth Fund Wants a Bigger Bite of Big Tech

In FX, not quite all change down under, but there has been shift in cross-currents to the detriment of the Aussie vs its Antipodean peer with Aud/Nzd back under 1.0600 and Aud/Usd slipping back below 0.6750. Comments from RBA’s Debelle overnight about the potential for further Aussie depreciation are weighing alongside guidance suggesting that other policy options would have to be mulled if the OCR was lowered to 0.5% (from 1% at present) and more stimulus is needed. Meanwhile, China’s Foreign Ministry continues to deny reports that calls were made to US trade negotiators over the weekend and maintains that Beijing will respond to additional US tariffs, but Nzd/Usd is holding up better between 0.6397-61.

JPY/GBP/EUR – All firmer vs the Dollar as the DXY loses grip of the 98.000 handle again and Yen retains an underlying safe-haven bid above 106.00 where decent option expiries reside (1.2 bn) as a counterweight to similar size interest at 105.00 (1.1 bn). Meanwhile, Cable is rebounding from the low 1.2200 area to 1.2250+ and Eur/Gbp has retreated from just shy of 0.9100 as Brexit deal hopes vie with expectations that Italy could be on the verge of forming a new Government coalition and avoid a snap election. However, talks between the 5SM and PD to that end are contingent on the former party’s insistence that PM Conte is reinstalled and Eur/Usd appears reluctant to rally too far from the 1.1100 mark in advance.

CAD/CHF – The Loonie and Franc are narrowly mixed against the Greenback, with the former recovering from recent lows and meandering between 1.3257-28 amidst firmer crude prices and technical resistance providing support vs expiries forming resistance (1.3260 Fib and 1.3 bn at the 1.3200 strike respectively). Conversely, Usd/Chf is back up around 0.9800 and Eur/Chf is closer to 1.0900 than 1.0850 in wake of latest weekly updates showing record high Swiss sight deposits.

SEK – The Swedish Krona is outperforming on the back of supportive data in the form of household spending and trade over mixed PPI, with Eur/Sek down around 10.7000 vs 10.7550+ at one stage, while Eur/NOK straddles 10.0000 in tighter parameters.

EM – The steady rise in official Usd/Cny fixes continues, but the on-shore and off-shore Yuans are still trading considerably weaker than the official rate despite Chinese bank intervention to calibrate the declines. Indeed, the former closed at 7.1670 compared to 7.0810 and Usd/Cnh is currently around 7.1725 even though reports are circulating that China may relax and/or remove restrictions on auto purchases.

In commodities, WTI and Brent futures have come off worst levels but remain in largely side-ways trade with little by way of catalysts to influence price action thus far. The benchmarks have been fluctuating on either side of 54/bbl and 59/bbl respectively throughout most of the session after finding bases at 53.60/bbl and 58.60/bbl. Ahead of the 12th September JMMC meeting, the committee noted that healthy oil demand and slowing global oil inventory growth should lead to significant draws in the second half of this year. The JMMC also noted that average July compliance among members stood at 159%, +22ppts M/M. Looking further ahead, the committee notes that the forecast for oil market fundamentals by major forecasters remains robust in 2019 and 2020. Elsewhere, gold prices have retreated from overnight highs but remain comfortably above the 1500/oz mark with little news-flow to sway prices. Copper posts mild gains, albeit more on the back of a slightly softer Buck. Finally, Chinese steel fell in excess of 3%, declining the most since November amid fears of weakening demand.

DB’s Jim Reid, who is back from vacation, concludes the overnight wrap

So first day back in two and a half weeks after a lovely holiday in the Alps. It’s nice that the first thing I do in the mornings again now is the EMR and all the overnight surprises that brings rather than double nappy duty and all the nighttime surprises that brings. Please don’t tell my wife but the best moment of my time off was undoubtedly the climax of the third test match of the Ashes two days ago. As a global daily I’d imagine 80-90% of the readers would have been blissfully unaware of this greatest English Ashes cricketing victory of all time, only 6 weeks after the previous greatest game of all time where England won the World Cup. It truly is a majestic summer for cricket in England in spite of the frailties of our team.

The frailties of markets have been exposed in my absence led by the deepening trade war, and the US yield curve inversion claiming its final and in my opinion most important victim – namely 2s10s. Given there hasn’t been a single lead indicator as good as the yield curve at predicting US downturns in the past 70 years, then the inversion has to be taken very seriously. My views on this have been well documented but feel free to use “ Yield Curve 101 ” from last year for more on this.

Turning to yesterday’s news now. The trade war again drove market action, this time in a supportive way. President Trump told reporters that “China called last night our top trade people and said let’s get back to the table.” Though no one in the US administration could offer specifics on the calls, and the Chinese Foreign Ministry did not confirm them, the change in tone was enough to push risk assets higher. Trump said that “we’re having meaningful talks, much more meaningful than I would say at any time” and also predicted “we’re going to make a deal.” This apparent optimism helped the S&P 500 to end +1.12% higher, while the NASDAQ and DOW gained +1.32% and +1.05%, respectively. Before Trump’s remarks, S&P 500 futures had opened -1.58% lower, in their first trading since the US increased tariffs on Friday, on top of the -2.58% drop from Friday.

To quickly recap that yo-yoing trade action from the end of last week now for those who have also been on holidays or have understandably struggled to keep up. Markets were pressured overnight on Thursday as China expanded tariffs on another $75 billion of imports from the US, in retaliation for the US’s announced tariffs earlier this month. Those duties will be at 5-10% and will take effect on either 1 September or 15 December, depending on the product, thus mirroring the US’s timetable. President Trump responded by escalating the trade war even further, first saying that the US “would be far better off without” China and then declaring “our great American companies are hereby ordered to immediately start looking for an alternative to China.” The S&P 500 dropped -2.58% on Friday, with semiconductor stocks, who disproportionately rely on Chinese supply chains, down -4.36%. After markets closed, Trump announced a suite of across-the-board tariff hikes on China, taking the existing set of taxed products from a rate of 25% to 30% and increasing the rate on the duties due later this year from 10% to 15%. So most of the commentary over the weekend was that yesterday was going to be horrible for markets. However Mr Trump made his much more positive trade comments three minutes before Europe opened, completely changing the complexion of the day.

Eventually the STOXX 600 ended -0.02% lower, and with London closed, trading volumes were 66% below normal. Other European indexes were similarly muted, though bank stocks did gain +1.00%. Moves in bonds were also subdued, with Bund yields rising +0.9bps and BTPs up +0.5bps. Treasury yields rose slightly, up +0.3bps to 1.54% although 2s10s stayed marginally inverted. Cash HY credit spreads were -6bps tighter in the US but flat in Europe with most London traders out. The dollar rallied +0.45%, appreciating against both DM and EM currencies, while gold gained +0.16% to a fresh six-year high of $1,529.

This morning in Asia, markets are following Wall Street’s lead with the Nikkei (+1.25%), Shanghai Comp (+1.68%), Kospi (+0.71%) and Hang Seng (+0.10%) all up. In FX, the Japanese yen is trading up +0.44% this morning while the Chinese onshore yuan is trading down -0.13% to 7.1603. Elsewhere, futures on the S&P 500 are trading flattish while WTI is up +0.65%. In terms of overnight data releases Japan’s July services PPI came in one tenth lower than consensus at +0.5% yoy.

We also saw some more trade headlines overnight with China’s People’s Daily saying in a commentary today that the US shouldn’t misjudge China’s ability and determination to firmly retaliate if the US follows through with higher tariffs while adding that anyone who wants to use maximum pressure to force China to accept unreasonable demands is doomed to fail. The commentary also added that, facing maximum pressure from the US, China maintains a rational and measured attitude, and will never cave on major matters of principle.

As for economic data, the highlight was the durables goods figures from the US. While the headline measure rose +2.1% mom compared to expectations for 1.2%, the more important core orders rose only 0.4%. That beat expectations for 0.0%, but the prior month was revised down by 0.6pp, leaving the overall trend roughly flat and taking the yoy figure to -0.5%, its first negative reading since November 2016. Core shipments, a direct input into the GDP figures, fell -0.7% mom. That will likely drag down third quarter GDP trackers a touch. In Europe, the only major data release was the German IFO survey, which fell to 94.3 from 95.7. Based on the historical link between the survey and GDP growth, that print would be equal to a contraction of -0.6% qoq. Our economists are not that bearish, but they do expect Germany to enter a technical recession this quarter.

Data releases for the day includes Germany’s final Q2 GDP and France’s August confidence indicators. Meanwhile in the US, we get the Q2 house price index, June FHFA house price index and S&P CoreLogic house price index along with the August Richmond Fed manufacturing index and Conference board confidence indicators.

via ZeroHedge News https://ift.tt/2ZvnWy6 Tyler Durden

With the Amazon ‘on fire’, everybody expected the climate talks at the G-7 Summit this weekend to be particularly contentious, as leaders like France’s Emmanuel Macron insisted that the international community must do something, while President Trump refused to support anything along those lines. But in a ‘symbolic’ gesture that was quickly seized upon by the media, President Trump skipped the G-7 session on climate change, giving photographers ample opportunity to snap photos of his empty chair.

And so, while Trump’s fellow world leaders were hashing out a “solution” to the fires in the Amazon (which, as we’ve explained, have been greatly exaggerated), Trump was elsewhere, talking to reporters about how he’s more focused on growing the “tremendous wealth” of the US.

“I feel that the United States has tremendous wealth. The wealth is under its feet. I’ve made that wealth come alive…We are now the No. 1 energy producer in the world, and soon it will be by far,” Trump told reporters when asked about his views on climate change.

“I’m not going to lose that wealth, I’m not going to lose it on dreams, on windmills, which frankly aren’t working too well,” he added.

Instead of attending the meetings on climate change, Trump held bilateral meetings on climate change with Indian Prime Minister Narendra Modi and German Chancellor Angela Merkel.

Trump’s administration has reversed U.S. environmental protections put in place by his Democratic predecessor Barack Obama and has weakened the Endangered Species Act wildlife conservation law.

The Republican president skipped a session on climate change and biodiversity at the summit, instead holding bilateral meetings with German Chancellor Angela Merkel and Indian Prime Minister Narendra Modi.

Meanwhile, the G-7 leaders discussed the fires in the Amazon and ‘what is to be done.’

The G7 leaders discussed the rainforest fires in Brazil and agreed to draw up an initiative for the Amazon to be launched at the U.N. General Assembly in New York next month.

French President Emmanuel Macron downplayed Trump’s absence at the meeting, saying that, though the president wasn’t there, “his team was.”

“He wasn’t in the room, but his team was,” Macron said. “You shouldn’t read anything into the American president’s absence…The U.S. are with us on biodiversity and on the Amazon initiative.”

Trump added that he’s not going to squander the tremendous wealth that the energy has created “on windmills.”

“I’m not going to lose that wealth, I’m not going to lose it on dreams, on windmills, which frankly aren’t working too well,” he added.

Why waste money on wind turbines when all they do is cause cancer?

via ZeroHedge News https://ift.tt/2Ucnhka Tyler Durden

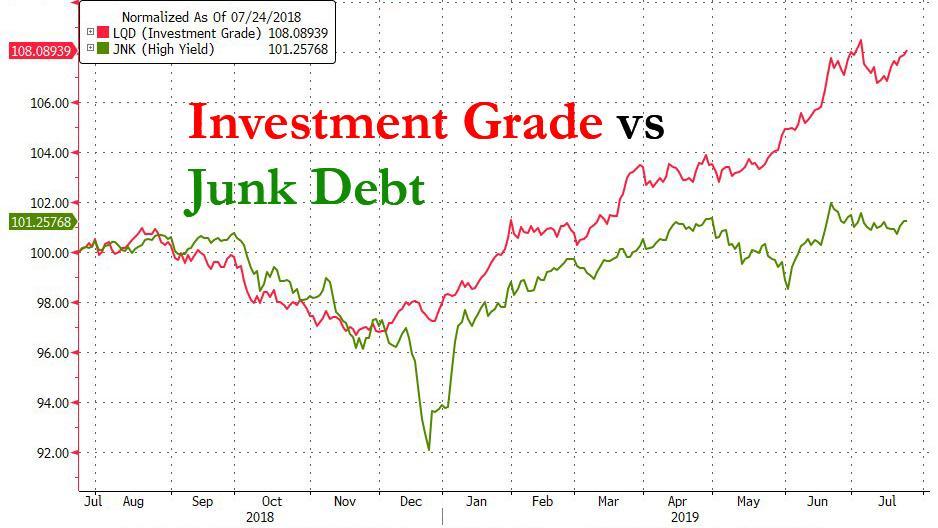

Amid one of the most stunning bond rallies in recent memory, all three of the most widely regarded American bond managers – Jeffrey Gundlach (DoubleLine), Scott Minerd (Guggenheim) and Dan Ivascyn (PIMCO) – are underperforming their benchmarks this year largely for the same reasons: ultra-low and negative yields are making them uneasy.

And while demand for corporate bonds has picked up this year as investors from all over the world search for yield in the US, all three of these managers refuse to invest in corporate debt, believing it to be a troubled asset class with too many landmines (of which the neutron bomb is the $3 billion BBB-rated “soon to be fallen angel” bonds which we have discussed one too many times to go over again) .

Gundlach, for his part, has been warning about a blowup in US corporate debt markets for months.

But according to Reuters, all three men now have adopted roughly the same strategy, stay long government bonds and wait for the turbulence that they see ahead to pass by before buying back into corporate debt.

Investors had been feasting on U.S. corporate credit bonds for years, though recession fears and mounting defaults late last year put an abrupt end to that. This year, the appetite for U.S. corporate bonds picked up dramatically when investors’ views on the economy began to improve and central banks became more accommodative.

U.S. corporate bonds have posted a total return of 13.4% this year, measured by the Bank of America Merrill Lynch US Corporate Bond Index while year-to-date Treasury returns are up 8.1%, according to an index compiled by Bloomberg and Barclays.

What’s more, a lack of alternatives against the backdrop of ultra-low, even negative-yielding, debt has made U.S. corporate bonds the natural destination for many investors. Some 95% of all investment-grade corporate debt in the world that has a positive yield is in the United States, according to Bank of America Merrill Lynch.

All three investors – Gundlach, the chief executive of DoubleLine Capital; Ivascyn, group chief investment officer of Pacific Investment Management Co, known as Pimco; and Minerd, global chief investment officer of Guggenheim Partners – have been underweight corporate credit relative to their benchmarks.

All three told Reuters they can live with the underperformance for now.

“We have never owned a single corporate bond in the Total Return Strategy dating back to 1993. Look it up,” Gundlach said. “When corporate bonds become very overvalued, especially when rates fall due to recession prospects increasing – well?” he added of why he has avoided the asset class.

Gundlach added that he expects there will be times when his fund is out of favor, and there will be times when it’s extremely popular: Same with all of the other managers.

Ivascyn, who oversees $1.84 trillion in assets under management at Pimco as of June 30, shares Gundlach’s sentiments. “We believe that corporate credit is fundamentally weak and could overshoot to the downside if the economy deteriorates,” he said.

The Pimco Income Fund, the largest actively managed bond fund, with assets of more than $130 billion, is lagging 93 percent of its Multisector Bond category so far this year, according to Morningstar data as of Aug. 23. The Multisector category typically invests in U.S. government obligations, U.S. corporate bonds, foreign bonds and high-yield U.S. debt securities and has assets of $259 billion.

Minerd’s Guggenheim Total Return Bond Fund is lagging 95% of its Intermediate Core-Plus Bond category so far this year, for the same period.

“As the Fed begins its easing campaign to try to extend an already long-in-the-tooth expansion, credit spreads are already tight across the fixed-income spectrum,” Minerd said. “Credit spreads could get tighter in this liquidity-driven rally, but history has shown that the potential for widening from here is much greater.”

All three have agreed that they’re keeping their duration as low as possible, and ultimately, they expect to win in the long run.

“I’ve said this a thousand times…we always run shorter duration,” Gundlach said.

[…]

“We think developed government bond yields are too low and could easily reverse so we are comfortable with low rate exposure,” Ivascyn said.

When yields finally snap higher, that’s the time to think about buying. The only question is when will that happen and what will be the catalyst.

via ZeroHedge News https://ift.tt/2U7NEaD Tyler Durden

From Trump’s trade wars to Brazil’s fires, the world is on the brink

‘Hey, Toreador! . . . We head for the edge, and the first man who jumps is a chicken. All right?”

In Rebel without a Cause, Jim (James Dean) and Buzz (Corey Allen) play the most famous game of chicken in Hollywood history, driving their jalopies at full speed towards a Californian cliff. At the last minute, Jim jumps. Buzz, his sleeve caught on the door handle, plunges to his death.

Games of chicken are all around these days. Indeed, it starts to feel as if the whole world is playing a massive, multiplayer game of chicken.

Clearly, Boris Johnson’s jaunts to Berlin and Paris last week were part of a diplomatic game of chicken. The prime minister repeated his readiness to go over the cliff of a no-deal Brexit if the European Union is not prepared to scrap the Irish backstop. Contrary to some UK press reports, the German chancellor, Angela Merkel, and French president, Emmanuel Macron, essentially reiterated their commitment to the existing withdrawal agreement. Vroom!

If Mr “Million-to-One-Against” himself were driving, there would be no chance of the Europeans chickening out. But the man at the wheel of the British jalopy is not Boris but the prime minister’s chief adviser, Dominic Cummings, and the glint in his eye tells you that he would quite enjoy hurtling over the precipice. After all, for him, Brexit is just a means to a higher end: the revolutionary disruption of Britain’s broken system of government.

A bigger game of chicken is going on between America and China.The trade war that Donald Trump initiated last year by imposing tariffs on Chinese imports has escalated because neither side’s negotiators have jumped. Not only have the two sides ramped up the tariffs this summer; there has also been an intensification of the tech war over Chinese companies, notably Huawei, as well as the first phase of a currency war.

Frustrated by the strength of the dollar, which he sees as a drag on US exports, Trump has resumed his other game of chicken: with the Federal Reserve. “We have a very strong dollar and a very weak Fed,” he tweeted on Friday. “My only question is, who is our bigger enemy, Jay Powell [the Fed chairman] or Chairman Xi [Jinping]?”

Even the president’s own advisers know that the economic warfare between the world’s two largest economies is lowering growth everywhere and that the insouciant US consumer will eventually feel the effects. Yet neither Trump nor his Chinese counterpart wants to be the chicken. On they both drive, pedal to the metal.

The stock market hates it, so Trump piles more pressure on Powell. Will he cut interest rates again next month? Or will he drive over the cliff marked “recession”?

Xi also has a subsidiary game of chicken — with the Hong Kong protesters. Will he tolerate their defiance, or will he send in mainland security forces? Will the protesters jump or keep driving for democracy?

Rebel without a Cause was released in 1955. The English philosopher Bertrand Russell clearly didn’t go to see it. We know this because in his classic account of the game of chicken published four years later (in Common Sense and Nuclear Warfare) he gave a different version of the game.

Chicken, he explained, “is played by choosing a long straight road with a white line down the middle and starting two very fast cars towards each other from opposite ends. Each car is expected to keep the wheels of one side on the white line. As they approach each other, mutual destruction becomes more and more imminent. If one of them swerves . . . the other, as he passes, shouts ‘Chicken!’.”

“As played by irresponsible boys,” Russell went on, “this game is considered decadent and immoral . . . But when the game is played by eminent statesmen, who risk not only their own lives but those of many hundreds of millions of human beings, it is thought on both sides that the statesmen on one side are displaying a high degree of wisdom and courage.”

The target of Russell’s critique was the US secretary of state, John Foster Dulles, who had described “the ability to get to the verge without getting into the war” as “the necessary art”.

“If you try to run away from it,” he argued, “if you are scared to go to the brink, you are lost.”

To Russell, such brinkmanship had become “absurd” in the age of nuclear weapons.

“The moment will come”, he argued, “when neither side can face the derisive cry of ‘Chicken!’ from the other side. When that moment is come, the statesmen of both sides will plunge the world into destruction.”

Just three years later, the superpowers came perilously close to doing just that in the Cuban missile crisis.

Pioneers of game theory and nuclear strategy – notably Thomas Schelling and Herman Kahn – sought to turn Russell’s logic on its head, arguing that the alternative to playing the game of chicken was surrender, and that the way to win was to put on a blindfold or remove the steering wheel, signalling that swerving was not an option. But I am not sure how strong those arguments really were.

Today’s games of chicken, you may say, are for lower stakes. There are economic risks to a no-deal Brexit and to an all-out US–China trade war, but no one is about to launch nuclear missiles. That may explain why so many games of chicken are being played: even if nobody jumps or swerves, it’s not Armageddon.

There is, however, a possible exception to the rule, and that is the game of chicken being played by the Brazilian president, Jair Bolsonaro, with the planet itself. In defiance of climate science and educated opinion, he has rolled back environmental protections for the Amazon rainforest. The result is a vast conflagration.

Nothing could better illustrate the dilemma of the modern green movement in Europe and North America. All the efforts they expect their own governments and peoples to make will be ineffectual if Brazil — and, more importantly, India and China — brazenly increase their carbon dioxide and other emissions. Yet environmentalists shrink from the imperialist implication: if Brazil, India and China won’t mend their wicked ways, then they must be forced to do so.

Bolsonaro is not just playing chicken with the planet. He is playing chicken with an international system that, until now, assumed global warming could be halted by voluntary agreements between sovereign states. And he does not look like a jumper — or a swerver — to me.

Trump ended his Friday on the phone to Bolsonaro.

“Our future Trade prospects are very exciting and our relationship is strong,” he tweeted, “perhaps stronger than ever before. I told him if the United States can help with the Amazon Rainforest fires, we stand ready to assist!”

Fried chicken, anyone?

via ZeroHedge News https://ift.tt/2HmVsQT Tyler Durden

Police in Portland, Ore., received tips that Tyrone Lamont Allen was the man who committed robberies of four banks and credit unions. One problem. Allen’s forehead and right cheek have fairly large tattoos. No witnesses described the robber having tattoos. The solution? Cops used Photoshop to remove Allen’s tattoos from photos they showed to witnesses in a lineup. Some of those witnesses, looking at the altered photos, picked Allen out of the lineup as the robber. Cops didn’t tell Allen’s defense attorney what they did. He only found out because he noticed the altered photo in material prosecutors gave him. He has asked the court to throw out those witnesses IDs.

from Latest – Reason.com https://ift.tt/2zngNVN

via IFTTT

{kind=link}