Chicago Fed’s Evans Tries To Set Record Straight On “Rate Hike” Miscommunication, But Dollar Barely Notices Tyler Durden

Wed, 09/23/2020 – 12:20

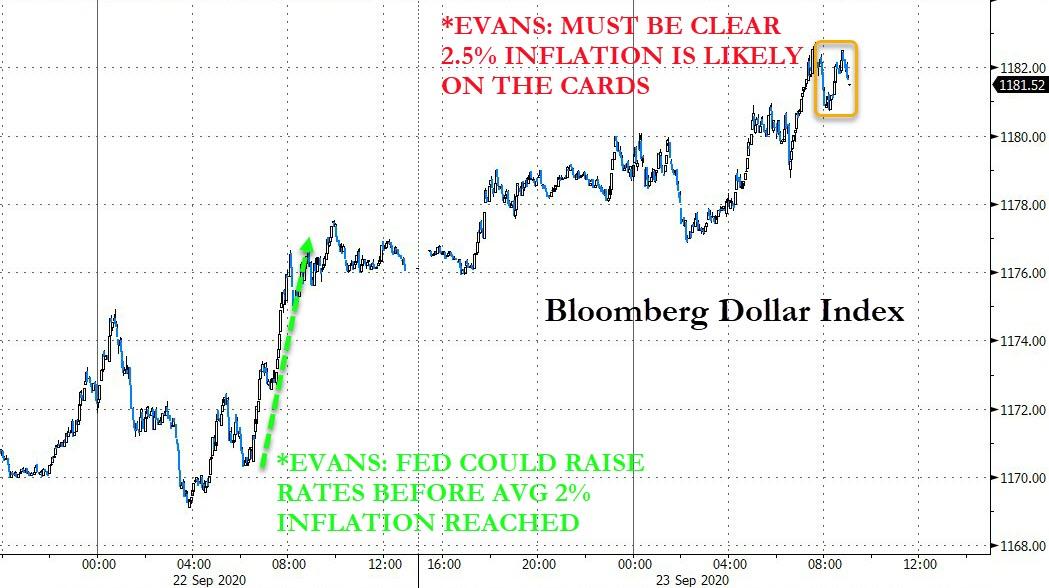

Yesterday just after 11am, the dollar spiked and risk assets slumped after what was a significant miscommunication between Chicago Fed president Charles Evens, the Bloomberg headline algo and traders. As we explained at the time, the dollar hit a 1 month high after a Bloomberg headline hit according to which Evans said that the “Fed May Raise Rates Before Average 2% inflation reached.”

The problem, as economist Julia Coronado explained, is that much was lost in translation as contrary to the Bloomberg headline, Evans merely “acknowledged flexibility in the statement, that the inflation bogeyman still lurks in the minds of some on the FOMC, but NOT HIM. He prefers to run it hotter, not limit to a “timid overshoot.”

In parting, we said to “expect upcoming Fed speakers in the coming days to undo the damage that this particular “lost in translation” headline achieved.”

We didn’t have long to wait, because amid a barrage of Fed speakers today (and tomorrow), Chicago Fed’s Evans spoke again this time in a moderated discussion hosted by MNI, and set the record straight on what he actually meant, saying that in his view, “we just have to be pretty clear that 2.5% inflation for some period of time is likely in the cards if we’re doing our jobs right” adding that “we need to be above 2% for some time,” referring to inflation.

Underscoring that the market’s reaction yesterday was wrong – as we expected he would – Evans then made it abundantly clear that “I don’t fear stronger accommodation to support inflation,” and “the setting of monetary policy I think is quite adequate.” He concluded by toeing the party line, namely that fiscal-policy stance -i.e., Congressional stimulus – will be “crucial” going forward.

It was too little, too late, and with the dollar igniting upward momentum on his comments yesterday, his reversal today barely registered in the dollar’s continued ascent.

Meanwhile, the initial risk off mood in markets that was sparked by his comment on Tuesday has only accelerated, with stocks trading near session lows by the time his second at bat came, and nobody cared.

via ZeroHedge News https://ift.tt/2RSPhZO Tyler Durden

For Volatility Traders, November Election Will Be A Career “Maker Or Breaker” Tyler Durden

Wed, 09/23/2020 – 12:06

Uncertainty surrounding the election was already maxing out amid armies of lawyers on both sides of the aisle preparing to argue over every ‘hanging chad’ they can find with a “never concede” precedent being discussed. And then the sad passing of RBG turned the risk up to ’11’ as stimulus hopes fade amid SCOTUS nominations.

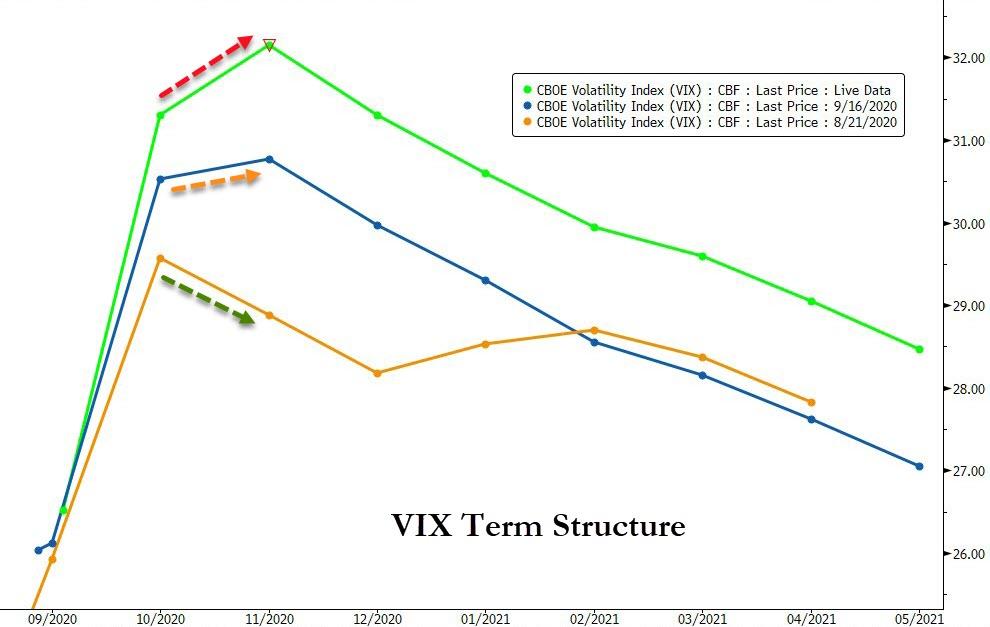

The rising uncertainty can be seen clearly in the VIX term structure which has ‘humped’ more and more over the last month…

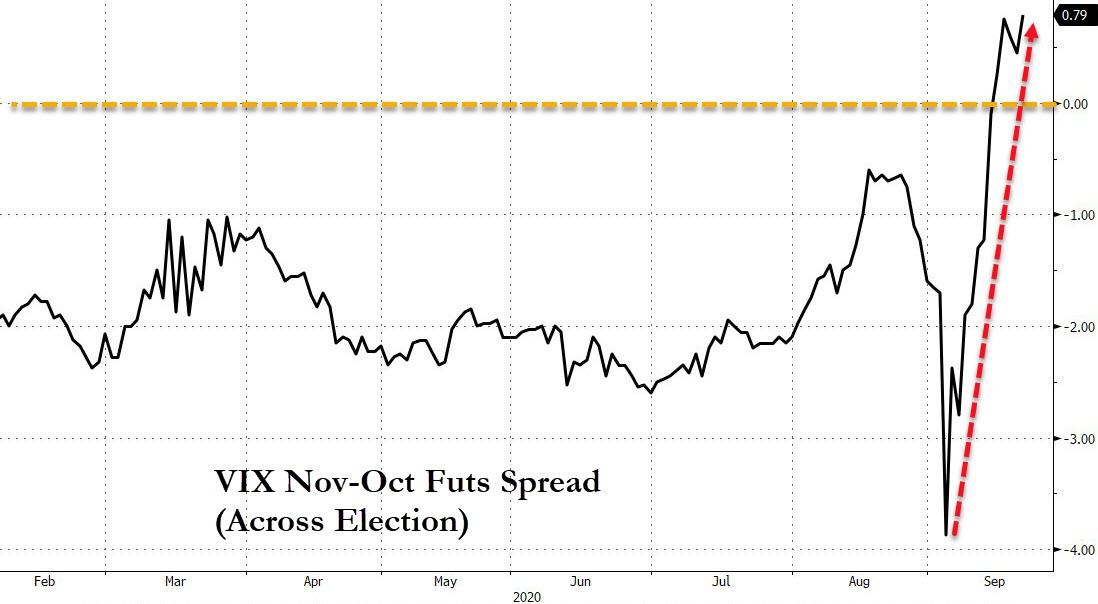

With the cross-election spread spiking to highs…

As investors price in the possibility of delayed results or contested election (via Goldman):

One consequence of the pandemic is the fraction of voting occurring via mail is likely to significantly exceed that in prior US elections. Because verification and counting of these mailed ballots does not occur until election dates in some states (including battlegrounds), and given the experience of the primaries, there is a good chance that the result may not be clear on election night.

While markets appear to have internalized this possibility, there are additional potential sources of uncertainty. In particular, there appears to be a significant bifurcation in voting method preferences between Democrats and Republicans, with a significant majority of Democrats expressing an interest in voting by mail and a majority of Republicans preferring to vote in person. This could lead to the appearance of a Trump lead on election day, but a potentially significant portion of the Biden vote still to be counted in the mail-in ballots. In a close election, such an outcome could result in claims/counter-claims of victory and/or litigation, and result in significant market volatility over an extended period.

And while the volatility market is beginning to price in this uncertainty, Nomura’s Charlie McElligott points out that the market feels like Dealers are back long vol and long downside again (we have spoken about clients “buying the dip” through selling QQQ Puts etc to Dealers), comfortably supporting a much “stickier” long-gamma market which continues to firm

“High” implied vols still screening “rich” and thus continue to compress meaningfully (providing mkt support), although skew in QQQ’s seems super cheap ahead of what implieds around- / post- Nov Election are telling you.

The SPX curve / term structure however was already steep, and yday saw election straddles “trueing up” higher again—after all, it has become consensus thinking that recounts and likely a Supreme Court decision are likely to drag the determination of the next POTUS through the end of the year.

But McElligott has an ominous warning for market participants:

This also likely means that some brave vol traders will try to take advantage as a perceived “generational” opportunity to sell this POST-NOV election “richness” (Dec / Jan) – could be a career “maker or breaker,” with the potential to see monster returns if the event were to pass and all that crash is puked back into the ether… or conversely be turned to dust into a God-forbid realization of chaos, with civil disorder, dual claims to the throne etc

These vols as I have previously stated will likely “stay rich” as no dealers / MMs will be able to go short vol / short gamma in said time buckets from a risk management perspective, while hedging demand likely continues to grow through the roof into the event risk – thus, due to this extremely likely “lack of supply”, implied vol will go even higher and more extremely optically “rich”

VIX space has now become day trading with futures “stuck” – buying UX1 when it dips 28-29 and selling it 31-32 before things get weird again on Nasdaq unwind / SCOTUS implications on NO stimulus deal / Election.

Finally, we remind readers that, while there isn’t an exactly analogous episode in history to the divisive chaos we are facing, we note that it took roughly a month for the results of the 2000 US presidential election to be settled, and over that time, the S&P500 and 10y UST yields declined by roughly 6% and 50bp respectively.

Do you think investors are ready (priced-in) for a move similar (or worse) than that? Will long high beta stocks be the new widowmaker across November 3rd?

via ZeroHedge News https://ift.tt/33QV33r Tyler Durden

Many investors, especially those with limited investment experience, are declaring that value investing is dead.

If one’s investment experience runs over the last ten years, who can blame them? Since 2010, growth stocks have outperformed value stocks, on average, by 6.11% a year.

If one’s experience runs deeper, and/or they appreciate history, they may have a different perspective. Over the last 100 years, including the last ten, value has outperformed growth by 3.19% a year.

So, is value dead or does value offer incredible opportunities versus growth?

Value stocks can be defined in many different ways. The basic premise, however, is the inclusion of stocks trading at a low price relative to their fundamentals; low price-to-earnings, low price-to-book, low price-to-sales, etc. The benefit of buying value stocks is the expectation that prices return to fair value. Quite often, the return benefits from above-market dividends. Equally important, buying a discounted asset reduces your risk.

Like value, there is no simple formula defining growth stocks. Growth stocks are companies whose earnings are expected to grow at a faster rate than the market. Because of the promise of future earnings, these stocks tend to trade at valuation premiums. Fewer of these stocks have meaningful dividends to bolster returns. Assets trading at a premium have a more daunting risk profile.

There is an appeal to owning value stocks and growth stocks. Mr. Market, however, makes deciding between the two difficult. At times, the premium for growth stocks can far exceed their potential growth. Frequently in such times, value is neglected and offers enormous relative performance potential. Other times growth stocks may be beaten down and offer a cheap entry point versus value stocks that have traded up to, or through, their fair value.

Historical Perspective

We firmly believe in mean reversion. The extreme highs for one asset class will eventually normalize closer to the long-term average. Often this occurs after dropping well below the long-term average. There is no example in the history of markets where mean reversion did not exert influence.

As mentioned, value has underperformed growth annually by 6.11% over the past decade. Over the last 100 years, value beats growth by 3.19% annually.

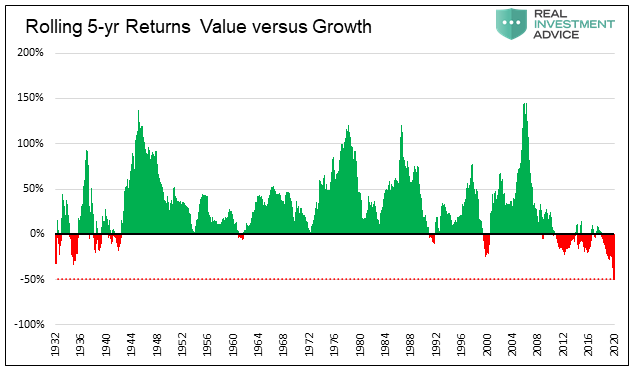

The graph below shows the rolling five year total returns for value versus growth.

As shown, there are very few five year periods where growth beats value. 82 percent of the time value outperforms growth. If we exclude the last ten years and the 1930’s the percentage climbs to 96%.

It is also notable that periods of value underperformance are followed by periods of strong outperformance. As we will highlight, this was last on display in the technology bubble of the late 1990s. From July of 2001 to July of 2006, value outperformed growth by nearly 150%.

As the chart above illustrates, the current period of value underperformance is the most extreme both in terms of duration and magnitude. Mean reversion argues that this trend will soon shift back to favor value.

Tech Boom and Bust

The graph below details the value-growth under- and outperformance of the late 1990s and early 2000s.

The chart tracks the cumulative net performance of value stocks versus growth stocks between 1998 and 2002. Like today, investors caught up in the tech boom only cared about growth. They bought into every story about the promise of technology. At the same time, companies trading with low valuations and steadily rising earnings are being thrown by the wayside.

In just two years, as markets rose to record-breaking valuations, growth beat value by 37.64%. However, when the markets came to their senses in early 2000, value rose from the dead. From low to high, just two years later, value beat growth by over 70%.

Value investors that held to their beliefs, stuck with their discipline, and shunned growth stocks may have lost the day in the late 1990s but won the battle. Not only did value stocks provide a great return but they provided a nice cushion. Owning value stocks in the early 2000s not only limited losses but actually produced gains in a down market.

20 Years Later

The experiences of the tech boom and bust have been long forgotten by most investors. There are a few value investors remaining today who are aware of what happened then. Like then, they are waiting for a second showing, but the wait is tedious.

The graph below shows that over the last two years growth has beaten value by 45%, 7% more than the two years leading into the tech bust.

Like the 1990s, every investor is chasing the same set of growth stocks. Today, they go by the name of FANGS. In the late 90s, they were called the Big Five.

The magnitude growth outperformance is amplified today due to the overwhelming popularity of passive investing. Those companies with the largest market caps receive a disproportionate percentage of investable dollars. Companies with the largest market caps today are predominantly growth companies.

2000 vs 2020

While the two periods may appear similar in their speculative nature and the value – growth divide, their fundamental backdrops are worlds apart.

In 2000, share prices of growth stocks, and in particular specific tech high flyers, got ahead of themselves. Their future earnings, however, had strong economic and fundamental underpinnings. Today they do not.

GDP was growing annually at 3.2% in the 1990s. That compares to 2% over the last ten years and most likely below 1.5% in the future. In the 1990s, debt as a percentage of GDP was a fraction of what it is today. Productivity growth was much stronger twenty years ago than today as well. In the 1990s, companies invested in their future development. Today they prefer to buy back stock and neglect their future earnings capabilities.

Today’s economy is not backed by organic growth and strong productivity, but rather debt and fiscal and monetary schemes. Given the environment, the argument for speculation over reliable earnings growth is befuddling.

Summary

If you appreciate history and understand that hangovers follow periods of excess, this article should be compelling. Growth’s recent outperformance over value goes beyond any historical precedence. Accordingly, any future underperformance, like its outperformance, might be one for the record books.

Exact timing on trend changes are difficult to predict. Growth may have already peaked versus value, or it may still have months or years to go. Regardless, the current period provides us precious time. Time to research stocks and slowly add value stocks to our portfolios. Adding value may seem futile like the late 1990s, but we know how that ended.

via ZeroHedge News https://ift.tt/304g0qz Tyler Durden

It was March 2, 2018, when President Donald Trump’s top trade adviser appeared on Fox Business Network to reassure Americans that other countries wouldn’t retaliate against new tariffs proposed by the White House.

Those tariffs on imported steel and aluminum were the first major battle in what’s become an expensive and largely unsuccessful 2 1/2 year-long trade war. But even at that early stage, it was obvious to some observers that the trade war wouldn’t be as easy or beneficial as the Trump administration was promising. “Should we expect China and others to come back and say, ‘Oh really America? Well take this, I’m going to raise tariffs and retaliate on farm goods,” Fox Business’ Maria Bartiromo directly asked Peter Navarro, director of the White House Office of Trade and Manufacturing Policy, during that March 2 interview.

“I don’t believe any country is going to retaliate for the simple reason that we are the most lucrative and biggest market in the world,” Navarro told her.

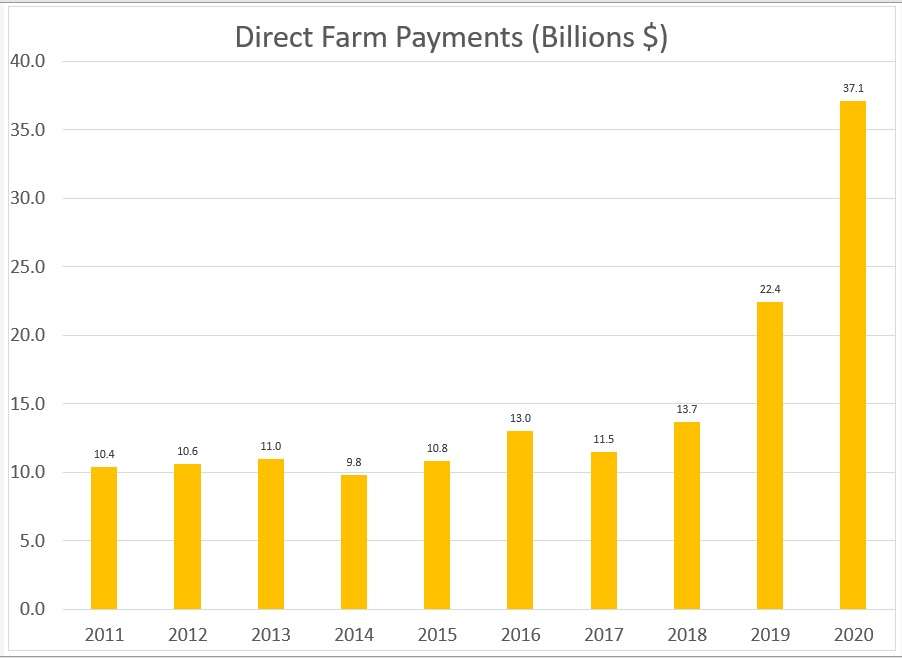

Well, he was wrong. Retaliation from several countries, but especially from China, caused exports of American agricultural goods to plummet in the years that followed. In 2017, the last year before the trade war began, China imported more than $19 billion in American farm goods, which fell to $9 billion in 2018 and rebounded weakly to $13 billion in 2019. Exports to other countries have been unable to make up the difference and, as a result, overall agricultural exports have fallen since the trade war began—ironically, given Trump’s focus on trade deficits, that means America now has a smaller farm goods trade surplus than at any time since 2006.

But to fix one self-inflicted wound, the Trump administration made another. Starting in 2018 and ramping up last year, the White House began making billions of dollars of direct payments to farmers who had been economically injured by the trade war. The Trump farm bailouts are on pace to cost taxpayers more than $37 billion this year—a huge increase over the total cost of direct farm payments, as tracked by the U.S. Department of Agriculture, in pre-trade war times.

The whole thing is exactly the sort of unaccountable executive overreach that Republicans used to campaign against. Now, Trump is using those bailouts as part of his reelection pitch, effectively telling voters in farm-heavy states that the money will keep flowing as long as they keep him in office.

“I am doing even more to support Wisconsin farmers,” Trump said during a rally in Wisconsin on Friday. “Starting next week, my administration is committing an additional—you have been asking for this for a long time—$13 billion in relief to help farmers recover from the China virus, including Wisconsin’s incredible dairy, cranberry and ginseng farmers who got hurt badly.”

Blaming the coronavirus pandemic is a clever bit of campaign-trail rhetoric, but it’s clear that American farmers were hurting long before the world knew about COVID-19. Wisconsin dairy farmers have been hit particularly hard recently—the state saw roughly 10 percent of its dairy farms close in 2019, before coronavirus hit—and the state is, of course, a key battleground in the upcoming presidential election.

If the farm bailouts were an exception, maybe Republicans could be forgiven for looking the other way. But Trump has expanded the cost of government on almost every front during the past four years. For a guy running against the supposed socialism of the political left, Trump sure has embraced a lot of socialism on his own when it has been politically advantageous to do so.

But even if Trump is defeated and the trade war comes to an end, taxpayers may end up footing a larger bill for farm subsidies for years. There’s nothing as permanent as a temporary government program, after all.

“It’s hard rolling back these things,” Joseph Glauber, a senior fellow at the International Food Policy Research Institute and former USDA chief economist told Politico in July. “The headlines are going to scream when [USDA] puts out a February 2021 farm income forecast that doesn’t show any ad hoc payments.”

from Latest – Reason.com https://ift.tt/33Xo9OC

via IFTTT

It was March 2, 2018, when President Donald Trump’s top trade adviser appeared on Fox Business Network to reassure Americans that other countries wouldn’t retaliate against new tariffs proposed by the White House.

Those tariffs on imported steel and aluminum were the first major battle in what’s become an expensive and largely unsuccessful 2 1/2 year-long trade war. But even at that early stage, it was obvious to some observers that the trade war wouldn’t be as easy or beneficial as the Trump administration was promising. “Should we expect China and others to come back and say, ‘Oh really America? Well take this, I’m going to raise tariffs and retaliate on farm goods,” Fox Business’ Maria Bartiromo directly asked Peter Navarro, director of the White House Office of Trade and Manufacturing Policy, during that March 2 interview.

“I don’t believe any country is going to retaliate for the simple reason that we are the most lucrative and biggest market in the world,” Navarro told her.

Well, he was wrong. Retaliation from several countries, but especially from China, caused exports of American agricultural goods to plummet in the years that followed. In 2017, the last year before the trade war began, China imported more than $19 billion in American farm goods, which fell to $9 billion in 2018 and rebounded weakly to $13 billion in 2019. Exports to other countries have been unable to make up the difference and, as a result, overall agricultural exports have fallen since the trade war began—ironically, given Trump’s focus on trade deficits, that means America now has a smaller farm goods trade surplus than at any time since 2006.

But to fix one self-inflicted wound, the Trump administration made another. Starting in 2018 and ramping up last year, the White House began making billions of dollars of direct payments to farmers who had been economically injured by the trade war. The Trump farm bailouts are on pace to cost taxpayers more than $37 billion this year—a huge increase over the total cost of direct farm payments, as tracked by the U.S. Department of Agriculture, in pre-trade war times.

The whole thing is exactly the sort of unaccountable executive overreach that Republicans used to campaign against. Now, Trump is using those bailouts as part of his reelection pitch, effectively telling voters in farm-heavy states that the money will keep flowing as long as they keep him in office.

“I am doing even more to support Wisconsin farmers,” Trump said during a rally in Wisconsin on Friday. “Starting next week, my administration is committing an additional—you have been asking for this for a long time—$13 billion in relief to help farmers recover from the China virus, including Wisconsin’s incredible dairy, cranberry and ginseng farmers who got hurt badly.”

Blaming the coronavirus pandemic is a clever bit of campaign-trail rhetoric, but it’s clear that American farmers were hurting long before the world knew about COVID-19. Wisconsin dairy farmers have been hit particularly hard recently—the state saw roughly 10 percent of its dairy farms close in 2019, before coronavirus hit—and the state is, of course, a key battleground in the upcoming presidential election.

If the farm bailouts were an exception, maybe Republicans could be forgiven for looking the other way. But Trump has expanded the cost of government on almost every front during the past four years. For a guy running against the supposed socialism of the political left, Trump sure has embraced a lot of socialism on his own when it has been politically advantageous to do so.

But even if Trump is defeated and the trade war comes to an end, taxpayers may end up footing a larger bill for farm subsidies for years. There’s nothing as permanent as a temporary government program, after all.

“It’s hard rolling back these things,” Joseph Glauber, a senior fellow at the International Food Policy Research Institute and former USDA chief economist told Politico in July. “The headlines are going to scream when [USDA] puts out a February 2021 farm income forecast that doesn’t show any ad hoc payments.”

from Latest – Reason.com https://ift.tt/33Xo9OC

via IFTTT

Tesla Systems Reportedly Suffer ‘Complete Network Outage’ Tyler Durden

Wed, 09/23/2020 – 11:32

Tesla’s global network has inexplicably crashed, according to Elektrek, which cited users around the world being unable to access their cars via their mobile apps.

Developing…

via ZeroHedge News https://ift.tt/2EwPVZS Tyler Durden

It Will Take Up To 59 Years For The Fed To Hit Its Inflation Target Tyler Durden

Wed, 09/23/2020 – 11:23

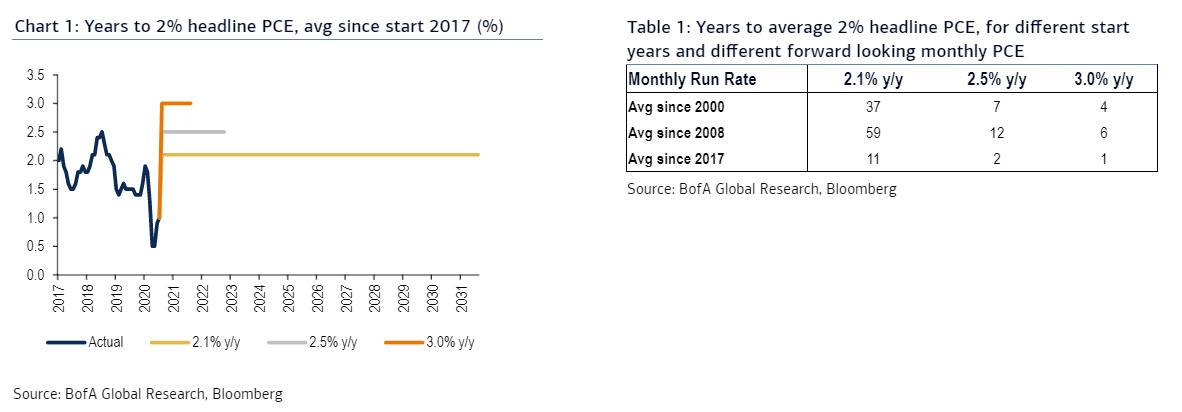

Two days before Powell unveiled Flexible Average Inflation Targeting (FAIT) as the Fed’s new monetary doctrine on August 27, some analysts were already pricing it in and analyzing how long it would take for the Fed to hit its “target” using conservative assumptions, with BofA concluding that “it would take 42 years to reach the price level target if core PCE remained at 2.1% yoy” but just 2 years if core PCE rocketed to 4.0% (good luck hitting 4% inflation).

And while analysts had no choice but to make sweeping assumptions before AIT was unveiled, they have to do the same now as well after AIT became official, simply because the Fed refused to provide key details about the program it is now operating under, and as Bank of America writes in a post-mortem on FAIT, “The Fed will seek to average 2% inflation over time but specifics around the time frame for averaging and the extent of inflation overshoot were light.“

Still, one can model some scenarios using simple assumptions.

These clearly show just how difficult the Fed’s new inflation objective could be to achieve as the following analysis from BofA’s Claudio Irigoyen shows, using a few scenarios for average 2% headline PCE assuming a non-flexible average inflation target.

To wit: if the Fed began its averaging period at the start of 2017 and monthly headline PCE is equal to 2.1% y/y going forward it would take 11 years to achieve the inflation target. Alternatively, if one uses 2008, or even 2000, as the starting year for the “average period” and the monthly PCE inflation print is 2.1% y/y, then it would take either three generations – 59 years – or two generations of trades, (37 years) to average 2% headline PCE.

Sadly, it’s not starting off well: as the strategist notes, the BofA’s house view is for headline PCE of 1.6% y/y for 2021, “which would mean an even longer time until the target is achieved.”

Of course, the time period would be truncated if the Fed somehow managed to hit monthly headline PCE of 3.0% y/y (or higher): in that case, achieving the target would take about one year. Unfortunately, such inflation – which would only materialize if these was a burst in wages – appears impossible to none other than the Fed: as the FOMC’s latest economic projections show, the max inflation overshoot in the Fed’s 2023 inflation forecasts is 2.1%.

In other words, even the Fed admits that we are looking at decades before the Fed will hike rates, unless of course the Fed is given a greenlight to wire digital money into US households directly… something which the Fed itself admitted is the last-ditch attempt to spark inflation at any cost.

via ZeroHedge News https://ift.tt/2ZZRGWI Tyler Durden

De Blasio Furloughs Another 9,000 NYC Employees Due To “Massive Budget Shortfall” Tyler Durden

Wed, 09/23/2020 – 11:05

One week ago, New York City Mayor Bill de Blasio announced that he will furlough himself and his City Hall staff for one week as the city weathers a budget (and everything else too) crisis.

“We’ve already had to make some tough cuts,” de Blasio announced last Wednesday.

“We’re doing everything we can to stop those cuts from becoming worse.”

Blasio, his wife first lady Chirlane McCray, and nearly 500 other staff members will take a week of unpaid furlough sometime between October and March 2021. The largely symbolic move is projected to save the city $860,000. And since “symbolic” was the key word here, moments ago the socialist mayor announced that New York City would expand its week long furloughs to another 9,000 employees to save $21 million, they mayor said this morning.

All managerial and non-represented employees must take five furlough days from Oct. 1 through March, the mayor revealed.

Alas, this latest round of furloughs will not be nearly enough as the city faces a $9 billion shortfall in revenue through June 2021. The mayor has warned of as many as 22,000 layoffs in the absence of federal financial aid or approval from the state for long-term borrowing.

“I know this is difficult news for the dedicated public servants of our city,” de Blasio said. “But we are forced to make these difficult decisions as we face a massive budget shortfall with no help in sight.”

The furloughs come as New York State is contemplating following New Jersey in slapping millionaires with higher taxes. A tax hike appears virtually inevitable should Gov Andrew Cuomo’s hope that Congress will appropriate additional aid fails.

via ZeroHedge News https://ift.tt/2HrKwV1 Tyler Durden

The Eiffel Tower in Paris has been evacuated after a bomb threat from a man shouting “Allahu Akbar”.

A security perimeter was established around the famous landmark after authorities received a bomb threat via an anonymous phone call.

This was followed by reports of a man near the tower threatening to “blow up everything” while shouting “Allahu Akbar,” a common refrain of Islamic terrorists, a police source told Sputnik.

Social media users posted image of armed forces on the scene.

The area around the tower is currently closed to traffic as authorities investigate the incident.

Back in 2017, Paris announced that it would be spending 20 million euros on a protective barrier around the Eiffel Tower to restrict access after a series of attempted terror attacks.

This put an end to the landmark’s spacious surrounding area which had provided a pleasant experience for both tourists and locals for decades.

Then diversity arrived.

* * *

In the age of mass Silicon Valley censorship It is crucial that we stay in touch. I need you to sign up for my free newsletter here. Also, I urgently need your financial support here.

via ZeroHedge News https://ift.tt/348jfPd Tyler Durden

The U.S. Army has deployed the first batch of its newly established military branch, the “Space Force”, outside the United States, specifically in the Arabian Peninsula.

The Chargé d’Affairs at the United States Embassy in Qatar, Greta C. Holtz, said on her Twitter account on Tuesday, that “Washington has deployed the first group of the space force at Al-Udeid Air Force Base in Qatar.”

Combat utility uniform of the U.S. Space Force

She added: “The deployment of the first group of members of the U.S. Space Force to Al-Udeid Air Force Base in Qatar represents the commitment of the United States and Qatar to continue building their strategic partnership in the future and in the space field.”

The Space Force was established by a decision of U.S. President Donald Trump on December 21, 2019, and is the first to be established in the country in more than 70 years, and represents the sixth branch of the U.S. military.

In a swearing-in ceremony earlier this month at Al-Udeid, 20 Air Force troops, flanked by American flags and massive satellites, entered Space Force. Soon several more will join the unit of “core space operators” who will run satellites, track enemy maneuvers and try to avert conflicts in space.

“The missions are not new and the people are not necessarily new,” Benson said.

That troubles some American lawmakers who view the branch, with its projected force of 16,000 troops and 2021 budget of $15.4 billion, as a vanity project for Trump ahead of the November presidential election.

The deployment of the first members of the U.S. Space Force to Qatar’s #AlUdeid Air Base symbolizes the United States’ and #Qatar’s commitment to further building our strategic partnership into the future – and into space! @SpaceForceDoDhttps://t.co/smdDw0rqHF

The U.S.-Qatari relations in the military field are deepening, as about 13,000 American soldiers, most of them from the Air Force, are stationed at Al-Udeid base, 30 km southwest of the capital, Doha.

* * *

Meanwhile…

This is kind of like a coming-of-age ceremony for Space Force. You’re not a full branch of the American military until you’ve deployed to the Middle East on some vaguely-defined and never-ending mission. https://t.co/JGYDBj7JGu

{kind=link}