Authored by Wolf Richter via WolfStreet.com,

US Treasury Yield v. Euro “Junk Bond” Yield. A new record in central-bank engineered absurdity.

US Treasury Securities with longer maturities fell this morning, with the 10-year Treasury yield rising above 2.37% early on and currently trading at 2.34%. This is still low by historical standards, and it’s still in denial of the Fed’s monetary tightening: Four rate hikes since it started this cycle, and the QE unwind has commenced as of today. But it cannot hold a candle to the Draghi-engineered negative-yield absurdity still unfolding in the Eurozone.

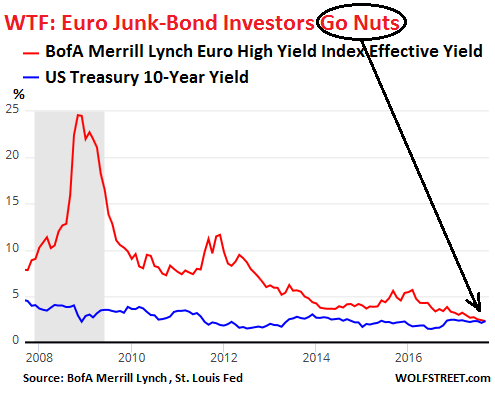

The average yield of junk bonds denominated in euros hit a new all-time record low at the close on Friday of 2.30%.

Let that sink in a moment. These euro corporate bonds are rated below investment grade. Companies, unlike the US, cannot print their own money to prevent default. There is little liquidity in the junk bond market, and selling these bonds when push comes to shove can be hard or impossible. The reason they’re called “junk” is because of their high risk of default.

And yet, prices of these junk bonds have been inflated by the ECB’s policies to such a degree that their yield, which falls as prices rise, is now lower than that of 10-year US Treasury securities that are considered the most liquid securities with the least credit risk out there.

The average yield of the euro junk bonds is based on a basket of below-investment-grade corporate bonds denominated in euros. Issuers include junk-rated American companies with European subsidiaries – in which case these bonds are called “reverse Yankees.”

They include the riskiest bonds. Plenty of them will default. Losses will be painful. Investors know this. It’s not a secret. But they don’t mind. They’re institutional investors plowing other people’s money into these bonds, and they don’t need to mind, but they have to buy these bonds because that’s their job.

This chart, based on BofA Merrill Lynch Euro High Yield Index Effective Yield via the St. Louis Fed, shows that the average euro junk bond yield is on the way to what? Zero?

During the peak of the Financial Crisis, the average junk bond yield hit 25%. During the dog days of the euro debt crisis in the summer of 2012, when Draghi pronounced the magic words that he’d do “whatever it takes,” these bonds yielded about 9%. The yield dropped below 5% in October 2013, for the first time ever.

This juxtaposition of the already low 10-year US Treasury yield and the even lower euro junk bond yield creates one of the most fascinating WTF-charts for our amusement at central-bank absurdist policies – and we’d be laughing at these bond investors gone nuts, if it weren’t so serious:

The ECB’s monetary policies include negative deposit rates and vast purchases of securities, including euro corporate bonds, as long as they’re not junk-rated, though it holds bonds that were downgraded to junk after it had acquired them, and it holds bonds that mercifully are not rated at all.

This has pushed yields on various government bonds below zero, though the Eurozone’s consumer price inflation is alive and well at an annual rate of 1.5% in September, despite the fake-deflation mantra that has long become the laughing stock of consumers who are confronted on a daily basis with rising prices.

With the average junk bond yield at 2.30%, investors are barely able to stay ahead of inflation at the moment, and get no compensation for the large credit risks they’re taking. In other words, credit risk is not priced into these risky junk bonds. The reckoning will be painful for them.

But this is Draghi’s ultimate accomplishment in his nutty bailiwick: The total destruction of the market’s risk-pricing mechanism at the expense of other people’s money – this includes pension funds and life insurance companies that play a large role in Europe’s private pension system. They have to buy corporate bonds. Their beneficiaries that paid into the systems will have to bear the costs in future years. And then there’s the comforting thought that when markets can no longer price risks, they cannot price anything at all because the price of risk underlies all prices in the financial markets.

These central bank policies have created extraordinary asset price inflation.

Read…. The US Cities with the Biggest Housing Bubbles

via http://ift.tt/2xWDL6q Tyler Durden