European stocks and US futures were higher on Tuesday following a mixed session in Asia, although traders faded an earlier gain and the Stoxx 600 was little changed, erasing a gain of as much as 0.3% as traders awaited more details on a potential US-China trade deal, after earlier in the day China pledged more stimulus to stabilize slowing growth when it predicted its 2019 GDP would shrink to “6-6.5%.”

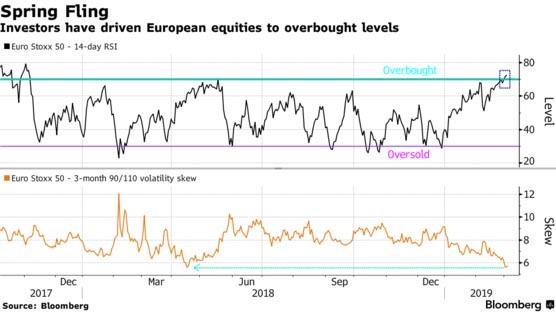

Europe’s Stoxx 600 Index inched fractionally higher, led by gains in telecommunications shares, pushing the broader index deeper into overbought territory…

… with traders pleasantly surprised for once by stronger European Services PMIs across the board, suggesting Europe’s economic slowdown may have found the reverse gear:

- EU Markit Services Final PMI (Feb) 52.8 vs. Exp. 52.3 (Prev. 52.3)

- Italian Markit/IHS Services PMI (Feb) 50.4 vs. Exp. 49.4 (Prev. 49.7)

- French Markit Services PMI (Feb) 50.2 vs. Exp. 49.8 (Prev. 49.8)

- UK Markit/CIPS Services PMI (Feb) 51.3 vs. Exp. 49.9 (Prev. 50.1)

Tobacco, healthcare, consumer staples, and other safe havens led the gains amid broader gloom about the global economy. British American Tobacco, Anheuser Busch and Unilever were up between 1.2% and 2.1%. Among individual movers, Evonik shares were close to four-month highs after the German chemicals group reported a slight rise in profits thanks to its coating additives and engineering plastics division. Vodafone added 2.3 percent after announcing plans to issue 4 billion euros ($4.5 billion) worth of convertible bonds to help finance its takeover of some Liberty assets. Elsewhere in the UK, British product testing company Intertek was the biggest faller in London, with a dealer attributing the drop to profit taking after largely in line full-year results. Luxury goods companies Richemont and Moncler were each down more than 3 percent after downgrades.

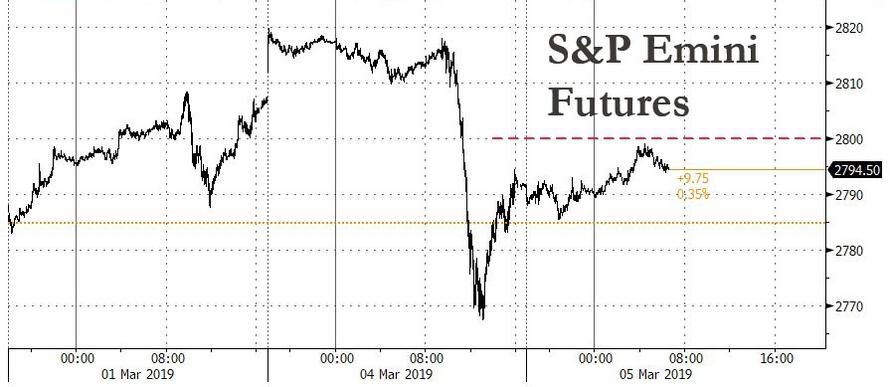

Meanwhile, in the US. S&P index futures traded higher following a lackluster start, although off their highs as the critical resistance at 2,800 is once again proving a solid barrier for the bulls.

Futures rebounded after yesterday’s surprising selloff, which took place despite the latest bout of “trade talk optimism”, and after stocks in Europe and Asia were buoyed on Monday by news that the world’s two-largest economies were close to a trade deal, investors are now hungry for concrete details before they push a global equities rally further. Meanwhile, trade and slowing growth are on the agenda as China’s most powerful officials gather in Beijing, while investors will get the latest read on the U.S. economy with the monthly jobs report Friday.

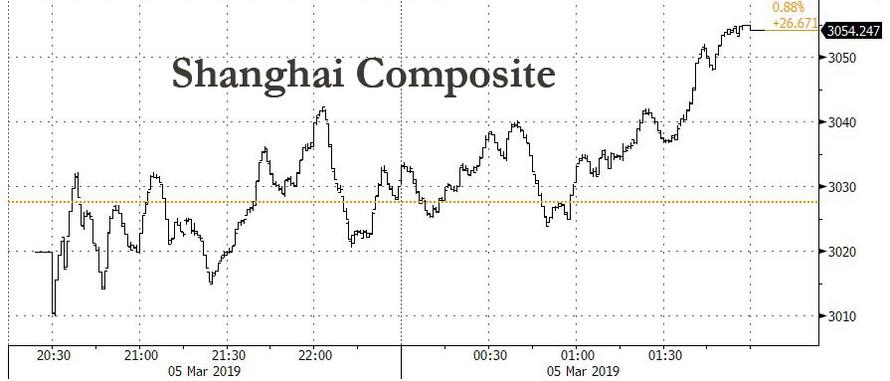

Earlier, during the Asian session shares declined in Japan, Korea and Australia and posted modest gains; the Shanghai Comp. nursed some opening losses following the release of the NPC work report which pledged to expand infrastructure investments and cut manufacturing VAT to 13% from 16%, whilst transport and construction VAT is to be reduced to 9% from 10%. Although the release of a dismal Caixin services PMI briefly dented the index, Chinese stocks closed at session highs, up 0.8%. The unchanged Hang Seng conformed to the overall risk-averse tone with its heavy-weight financial sector as the marked underperformer.

As part of the annual work report to the National People’s Congress, China lowered its 2019 GDP growth target to the range of 6.0-6.5% from “around 6.5%” and maintained CPI target at 3.0%, both as expected. Budget deficit for 2019 was set at 2.8% vs. 2.6% in 2018. China stated that fiscal policy to be proactive and monetary policy to be prudent will not resort to flood-like stimulus, whilst also saying it will keep the Yuan basically stable at reasonable equilibrium and is to increase the flexibility of the Yuan exchange rate while keeping liquidity reasonably ample. China will expand infrastructure investments in 2019 and plans to cut manufacturing VAT to 13% from 16%, as touted, VAT for transport and construction sectors to be reduced to 9% from prior 10%. China will make economic policy for forward-looking, targeted and effective whilst maintaining pace and strength in risk prevention, and higher budget deficit ration will leave more policy room for resolving potential risks. China will also step up targeted RRR cuts for smaller and medium-sized banks to support private and smaller firms. Growth in M2 Money Supply and social financial to be in-line with nominal GDP growth and basically the same as in 2018. China is to implement consensus reached between US and Chinese leaders in Argentina, but said it needs to brace for a tough economic battle.

While China’s GDP cut underlined the strain that has slowed growth and roiled global markets, stimulus steps reassured investors that Beijing was serious about steadying the economy. “I think we all saw it coming. The growth trend was going to be cut and they’re saying the right things about stimulus. They have plenty of policy levers to pull if needed,” said Peel Hunt economics and strategy research analyst Ian Williams.

Still, European autos and suppliers, which rely on Chinese demand, were under pressure, with Continental and Daimler among the biggest fallers in Frankfurt.

In FX, the Bloomberg Dollar Spot Index headed for a fifth day of gains, with the greenback trading stronger versus most G-10 peers. China cutting its growth target kept high-beta currencies under pressure, while the euro failed to gain momentum after PMI data from the currency bloc beat expectations. Loonie drops to its lowest since Jan. 25 amid a deepening crisis in Justin Trudeau’s government. The yen dipped while the Australian dollar recovered somewhat after falling earlier to a three-week low, after the central bank left its benchmark interest rate unchanged.

In other overnight news, President Trump plans to terminate India and Turkey as Generalised System of Preferences beneficiaries. The move comes as India has not assured the US that it will provide “equitable and reasonable” market access and Turkey is now “sufficiently economically developed”; according to US Trade officials. Indian Trade Ministry Official, in response, said US and India were able to work out an extensive and reasonable package which covered almost all US concerns, although the advantages under the US GSP are “minimal and moderate”.

In the latest Brexit tragicomedy news, UK PM May has been warned that she must whip her MPs to keep a no-deal Brexit on the table, whilst Senior Eurosceptics are convinced PM May will lose the vote on her Brexit deal and they do not expect Attorney General Cox to win concessions on the Northern Irish backstop. May is also reportedly considering a parliamentary vote on the UK’s future relationship with the EU, as per demands from Labour MPs. A source close to a cabinet minister also stated that there seemed to be “no chance” that her deal would pass next week. Meanwhile, the FT reported that UK Trade Secretary Fox’s department has cancelled its regular meetings with business after the details of a prior meeting were leaked to the media.

In other news, Treasury Secretary Mnuchin has urged Congress to lift the debt limit as soon as possible and added that the new debt issuance suspension will be from March 4th to June 5th, although the Treasury can easily extend debt suspension measures into September and perhaps October

Elsewhere, West Texas Intermediate crude oil ticked lower though remained above the $56 a barrel level. Brent (+0.2%) and WTI (+0.1%) prices are firmer although they were initially weighed on by the deteriorating risk tone, and Chinese Caixin Services PMI coming in below expectations at 51.1 vs. Exp. 53.5; with the complex also affected by dollar strength. Elsewhere, the El Sharara oil field has reopened at a current output of 30k BPD, far below the field’s capacity of around 300k BPD; although NOC has stated that a return to regular output is expected in the next few days. Looking ahead we have API Weekly release later in the session, which last week saw crude stocks fall by -4.2mln.

Gold (-0.1%) is relatively unchanged with the metal affected by both the stronger dollar and the deterioration in the risk tone seen overnight.

Gold futures slid for a seventh straight session, the longest slump since March 2017.

Market Snapshot

- S&P 500 futures up 0.2% to 2,796.50

- STOXX Europe 600 up 0.2% to 375.70

- MXAP down 0.3% to 159.41

- MXAPJ down 0.06% to 525.58

- Nikkei down 0.4% to 21,726.28

- Topix down 0.5% to 1,619.23

- Hang Seng Index up 0.01% to 28,961.60

- Shanghai Composite up 0.9% to 3,054.25

- Sensex up 1% to 36,410.29

- Australia S&P/ASX 200 down 0.3% to 6,199.29

- Kospi down 0.5% to 2,179.23

- German 10Y yield rose 2.0 bps to 0.178%

- Euro down 0.1% to $1.1329

- Brent Futures down 0.6% to $65.30/bbl

- Italian 10Y yield rose 0.5 bps to 2.38%

- Spanish 10Y yield fell 0.3 bps to 1.169%

- Brent Futures down 0.6% to $65.30/bbl

- Gold spot down 0.2% to $1,284.73

- U.S. Dollar Index up 0.04% to 96.72

Top Overnight News

- China’s GDP growth target in Premier Li Keqiang’s annual work report to the National People’s Congress was set at a range of 6-6.5% for 2019, compared with last year’s “about” 6.5% goal

- Services expanded across the 19-nation euro area, bolstered by gains in Germany, Ireland and Spain, according to IHS Markit. That pushed a composite Purchasing Managers’ Index to 51.9, the highest in three months. An initial reading was for an increase to 51.4

- The BOE is launching a new liquidity facility in euros in the final few weeks before the scheduled date for Britain to leave the European Union

- Bank of Japan board members are likely to discuss a possible downgrade of their assessments of industrial production, exports and overseas economies when they meet to set policy next week, according to people familiar with the matter

- The U.S. is giving American exporters a sizable tax break on the goods and services they sell overseas. But the benefit might not be enough to convince Corporate America to expand its U.S. operations beyond what it was already planning

- Australia is no stranger to heated debate about the direction of its housing market. This week, that spread to mortgage debt too. Suncorp Group Ltd. said Monday that arrears on one parcel of securities are creeping past the level that triggers a change in how principal repayments are carved up

Asian stocks traded lacklustre following a disappointing lead from Wall Street after the Dow slipped 0.8%, weighed on by Boeing and Goldman Sachs shares, whilst the S&P shed 0.4% amid underperformance in healthcare names. Both indices marked their worst turnaround since early February. ASX 200 (-0.3%) extended losses from the open amid underperformance in the Consumer Discretionary and Material sectors, whilst Nikkei 225 (-0.4%) was weighed on by commodity exposed stocks. Elsewhere, Shanghai Comp. (+0.8%) nursed some opening losses following the release of the NPC work report which pledged to expand infrastructure investments and cut manufacturing VAT to 13% from 16%, whilst transport and construction VAT is to be reduced to 9% from 10%, although the release of dismal Caixin services PMI briefly dented the index. Finally, Hang Seng (U/C) conformed to the overall risk-averse tone with its heavy-weight financial sector as the marked underperformer.

Top Asian News

- BOJ Is Said to Discuss Downgrading Its Views of Output, Exports

- What Analysts Are Saying About New Philippine Central Bank Head

- Mandiri Said to Eye Deal for $2 Billion StanChart- Backed Rival

- Tencent Jumps to 6-Month High on Optimism Over Key Game

Major European indices are moving towards negative territory, after starting the session somewhat firmer [Euro Stoxx 50 U/C] moving more in-line with the relatively poor performance seen overnight in Asia which was dictated largely by a disappointing lead from Wall Street. Sectors are mixed, with some slight underperformance in consumer discretionaries; the sector is weighed on by poor performance in Daimler (-0.8%), which represents around 7% of the sectors weighting, who are in the red after executives at the Co. stated they may have to lift prices to pass on potential US tariffs. Other notable movers include, Evonik (+3.8%) who are at the top of the Stoxx 600 after earnings where they beat on Q4 revenue. At the other end of the Stoxx 600, and weighed on by broker moves, are Altice (-9.1%) as are Richemont (-3.2%), who were both downgraded at Barclays and BOFA Merrill Lynch respectively. Elsewhere, Vodafone (+1.9%) are higher after after the Co. state they intend to raise around EUR 4bln through sterling denominated MCBS and there is the potential for a share buyback as part of this. Separately, British American Tobacco (+1.0%) are higher as the Co. state there will be no impact from the Quebec charge to their ratio of adj. net debt to adj. EBITDA.

Top European News

- Euro Area’s Resilient Services Sector Puts Mild Gloss on Economy

- BOE Starts Euro Lending Facility to Cushion Brexit Risks

- Italy’s State Lender May Back Elliott at Tel Italia Vote: Stampa

In FX, the DXY is off best levels, but the index continues to edge higher and just surpassed another chart resistance level (96.784) ahead of the next big figure on its way to a 96.815 high. The Greenback is still benefiting from weakness in rival currencies to an extent if not large part, or by default as a combination of negative/bearish factors inflict damage elsewhere (ranging from weaker macro fundamentals relative to the US, geopolitical instability/uncertainty and Central Bank policies aligning to Fed patience or even turning more dovish in certain cases, to name just a few). The DXY is now holding around 96.750 and well above Monday’s 96.331 low.

- NZD/CAD – The 2 biggest G10 losers, with the Kiwi slipping below 0.6800 amidst a broader fall-out in risk currencies following a considerably weaker than forecast Chinese Caixin services PMI and confirmation that the NPC has downgraded its GDP sights to 6-6.5% from 6.5% previously. Meanwhile, the Loonie has extended recent losses to fresh multi-month lows circa 1.3350 vs its US counterpart with the added weight of heightened strains between Canada and China, plus another downturn in crude prices.

- EUR/AUD/JPY/CHF – Also weaker vs Usd, as the single currency fails to derive much/any real support from surprise beats and upward tweaks to the Eurozone services PMIs, including the Italian headline that rebounded over 50.0 and was supplemented by an unexpected Q4 GDP revision to -0.1% q/q from -0.2%. Eur/Usd is hovering just above yesterday’s 1.1309 base and Fib support at 1.1305, but looks technically weak after breaching 1.1350 and key chart levels not far above. Similarly, the Aussie is struggling to mount a concerted recovery from recent lows towards 0.7100 after a dovish RBA policy statement on balance and yet more poor data overnight (Q4 net exports), and Aud/Usd could become increasingly drawn to a hefty option expiry down at 0.7050 as a result (1.6 bn). Meanwhile, the Yen and Franc continue to trade defensively on constructive US-China trade deal vibes, with Usd/Jpy edging back up to 112.00 and Usd/Chf straddling parity. Note also, decent option expiries in Usd/Jpy may impact into the NY cut, with 1 bn running off between 111.80-90 and 1.9 bn at the 112.00 strike.

- GBP/SEK – Relative outperformers on better than expected UK and Swedish services PMIs vs other more downbeat economic indicators. However, Cable remains capped ahead of 1.3200 and the 100 WMA (1.3207), with the 10 DMA (1.3161) and a Fib (1.3130) now flanking the pair as it pivots 1.3150 awaiting any further Brexit developments. Eur/Sek has retreated through 10.6000 again and retesting bids around 10.5500.

- EM – More angst for the Try and Inr after the US pulled the GSP plug from both nations, with the Lira attempting to pare losses and stay above 5.4000, but the Rupee staging a firmer recovery from almost 71.0000 at one stage as India’s Trade Ministry downplayed the impact of the trade pact being terminated.

In commodities, Brent (+0.2%) and WTI (+0.1%) prices are firmer although they were initially weighed on by the deteriorating risk tone, and Chinese Caixin Services PMI coming in below expectations at 51.1 vs. Exp. 53.5; with the complex also affected by dollar strength. Elsewhere, the El Sharara oil field has reopened at a current output of 30k BPD, far below the field’s capacity of around 300k BPD; although NOC has stated that a return to regular output is expected in the next few days. Looking ahead we have API Weekly release later in the session, which last week saw crude stocks fall by -4.2mln. Gold (-0.1%) is relatively unchanged with the metal affected by both the stronger dollar and the deterioration in the risk tone seen overnight. Elsewhere, metals were weighed on by China lowering its GDP growth target to 6.0-6.5% from the prior of around 6.5%. Separately, the amount of copper available in LME system, fell to the lowest level since 2005 of 21.6k tonnes.

US Event Calendar

- 9:45am: Markit US Services PMI, est. 56.2, prior 56.2; Markit US Composite PMI, prior 55.8

- 10am: ISM Non-Manufacturing Index, est. 57.4, prior 56.7

- 10am: New Home Sales, est. 600,000, prior 657,000; New Home Sales MoM, est. -8.68%, prior 16.9%

- 2pm: Monthly Budget Statement, est. $12.0b, prior $13.5b deficit

Central Banks

- 8am: Fed’s Rosengren Speaks on Current Economic Outlook

- 9:30am: Fed’s Kashkari Testifies Before Minnesota Senate Finance Panel

- 11:30am: Fed’s Barkin Speaks at the Rural Economy

DB’s Jim Reid concludes the overnight wrap

The flu-inspired daze continues. I can’t remember a four day period where I’ve slept as much as this one, albeit punctuated at regular intervals with choking coughing fits. If I make it into the city today please give me a wide berth for the sake of you and your family.

Markets seemed like they were suddenly struck down by a nasty ailment yesterday as the early optimism sparked by Asia this time yesterday reversed spectacularly by US lunchtime. Despite opening +0.47% higher, the S&P 500 ended up closing -0.39% lower, albeit well off the intraday lows of -1.29%. The DOW (-0.79%) and NASDAQ (-0.23%) had similar trajectories. There was not a clear macro catalyst, but it seemed like political tensions played a prominent role in the selloff, as headlines (per Bloomberg) surfaced about House Democrats deepening and broadening their investigations of the President. The House Judiciary Committee sent requests for documents to 81 entities, including the President’s son, his former CFO, and his lawyer. The VIX index mirrored the move in cash equities, rising as much as +3.1pts and on track for its sharpest rise since Christmas Eve before moderating in the afternoon to end end +1.06pts higher at 14.63.

Further weighing on sentiment was negative news in the healthcare sector, with the S&P 500 healthcare index dropping -1.34%. Despite making up only 14% of the S&P 500 by market cap, it drove over half of yesterday’s declines. Drugmaker Eli Lilly (-1.07%) announced that it would offer its insulin product at half price, possibly in response to political pressure over high pharmaceutical prices. The managed care sector (-4.41%) had its worst day since 2015, partially on worries over political risks and partially due to a positioning unwind. Data showed that the largest US-traded healthcare ETF saw outflows of -$855million last week, its most since 2015 as well.

This morning the focus has quickly turned to China’s National People’s Congress where the early headlines (per Bloomberg) are suggesting that China will resort to moderate fiscal stimuli to support slowing growth as China announced a fiscal deficit target of 2.8% of GDP in 2019 versus 2.6% in 2018 while pledging a “noticeable decrease” in the tax burdens for major industries. Premier Li Keqiang’s annual work report announced total tax and social security fees cuts of CNY 2tn ($ 298bn). China is now targeting GDP growth in the range of 6%-6.5% in 2019 (vs. last year’s goal of c. 6.5%), marking a shift from previous practice of using a point figure. The work report also indicated that further cuts to the required reserves ratio for smaller banks are planned. At first glance much of the above has been expected so no major surprises here. Chinese equity markets are seeing small gains this morning though with the Shanghai Comp (+0.11%) and Shenzhen Comp (+0.75%) both up following the news on tax breaks and also on the story yesterday that China is planning a three percentage point cut to the top VAT bracket – news that was also anticipated. We should note that we’ve had the remaining February Caixin PMIs in China too this morning with the composite reading at 50.7 (vs. 50.9 last month) and services PMI decelerating to 51.1 (vs. 53.5 expected). So a bit disappointing.

Sentiment is not as rosy across the remainder of Asia with markets largely following Wall Street’s lead from yesterday. The Nikkei (-0.46%), Hang Seng (-0.03%) and Kospi (-0.55%) are all down. Not helping sentiment overnight was news from China’s Commerce Minister Zhong Shan that it will take more efforts by China and the US to reach an agreement on trade. He suggested talks were difficult due to differences in culture and stages of development and that both sides need to meet each other half way to get a deal. So a slightly more cautious view than that seen of late. Elsewhere, futures on the S&P 500 are largely trading flat (-0.03%) while all G-10 currencies are trading weak (down in the range of -0.1% to -0.4%) this morning. In terms of other data releases, Japan’s February composite PMI came at 50.7 (vs. 50.9 last month) with the services PMI reading at 52.3 (vs. 51.6 last month).

Back to markets yesterday and early weakness for the Greenback post the Trump comments over the weekend quickly reversed after Europe walked in and then later once the US session kicked off. The Dollar index eventually ended +0.09% while EM FX was flat. Meanwhile the one laggard in the rates’ market yesterday was Greek bonds where 10y yields rose +3.0bps to 3.65% after the news that Greece had mandated six banks for a new 10y bond. The nation did do a 10y deal in 2017 albeit as part of a bond exchange. However prior to that the last syndicated deal was in 2010. It’s amazing that just 3 years ago Greek 10y bonds were trading around 10%.

Italian yields also underperformed a touch, with 10-year BTP yields up +0.5bps while bunds rallied -2.6bps. Attention focused on Bank of Italy Governor Visco’s comments ahead of this Thursday’s ECB meeting, in which he said that the “ECB’s money cannot be used to buy government bonds.” This suggests that any new TLTRO facilities could come with additional strings attached, to discourage banks from using cheap lending to finance carry trades, and to instead encourage lending to the corporate sector. Italian bank stocks ended the session flat.

In other central banks speak, Bank of Japan Governor Kuroda said that it will be difficult to reach the 2% inflation target in the current outlook period, but that factors slowing an acceleration in inflation will fade moving forward. This was interpreted as a signal that additional easing is not imminent, despite a deterioration in economic data, and Japanese government yields rose above 0.0% for the first time since January. This helped the yen appreciate +0.13% versus the dollar.

As for Brexit, there wasn’t a great deal of new news to report yesterday. Reuters did report that the Irish Prime Minister was supposedly willing to offer clarifications and reassurances to get a deal over the line. Today the UK’s Cox and Barclay are due to travel to Brussels so we may well get further headlines as the day progresses. While we’re on the UK it’s worth flagging a report from our UK economists yesterday on the domestic housing market. The headline conclusion is that underlying fundamentals remain strong, but Brexit, tighter macro prudential policy and tax changes have weighed on prices lately. That being said, they expect the housing market to start to recover from later this year – assuming ratification of a Brexit deal – so it’s not all doom and gloom. More in their report here .

On the data front, US construction spending fell -0.6% mom in December versus expectations for a 0.1% improvement and down from a 0.8% expansion previously. Our economists viewed the data as distorted by California wildfires, and they still expect a rebound in housing sector activity over the next few months as lower interest rates feed through to mortgage activity. An index of US homebuilder stocks rallied +2.43% yesterday. In the UK, the construction PMI printed at 49.5 from 50.6, dipping into contractionary territory for the first time in a year as the Brexit uncertainty weighs on activity.

Looking at the day ahead, this morning it’s all eyes on the remaining February services and composite PMIs in Europe including a first look at the data for the non-core and UK. We’ll also get the final Q4 GDP revisions for Italy where, as a reminder, the advanced reading (-0.2% qoq) confirmed a technical recession, and January retail sales data for the Euro Area. In the US we’ll also get the final PMIs as well as the February ISM non-manufacturing (+0.6pts to 57.3 expected) and December new home sales (-8.7% mom expected). Away from that we’re due to hear from Italy’s finance minister Tria this morning, before the BoE’s Carney speaks this afternoon before the House of Lord’s Economic Affairs Committee. The Fed’s Rosengren is also set to speak today.

via ZeroHedge News https://ift.tt/2BZvHDx Tyler Durden