Speculators Brace For Commodity Prices Surge As Open-Interest Hits $1.25 Trillion

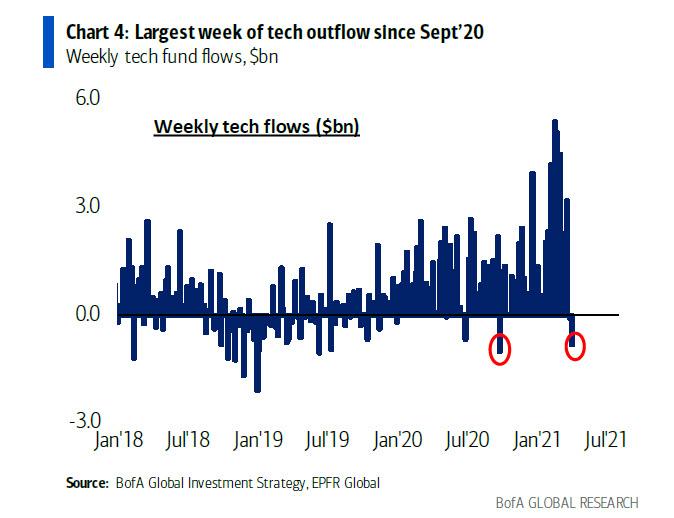

Throughout 2020, investors left the commodity sector discarded at the trash heap of the market, focusing instead entirely on growth and deflation names. Fast forward to today and boy have things changed: not only have growth names done little to nothing in 2021, a year which has seen near record shorting of tech names and a constant outflow of equity funds…

… but as sentiment shifts toward “value”, commodity-linked stocks have been rising every day, and even such boring names as Exxon and Chevron have recently turned into hedge fund darlings, attracting a bevy of activist shareholders and pushing higher by the day.

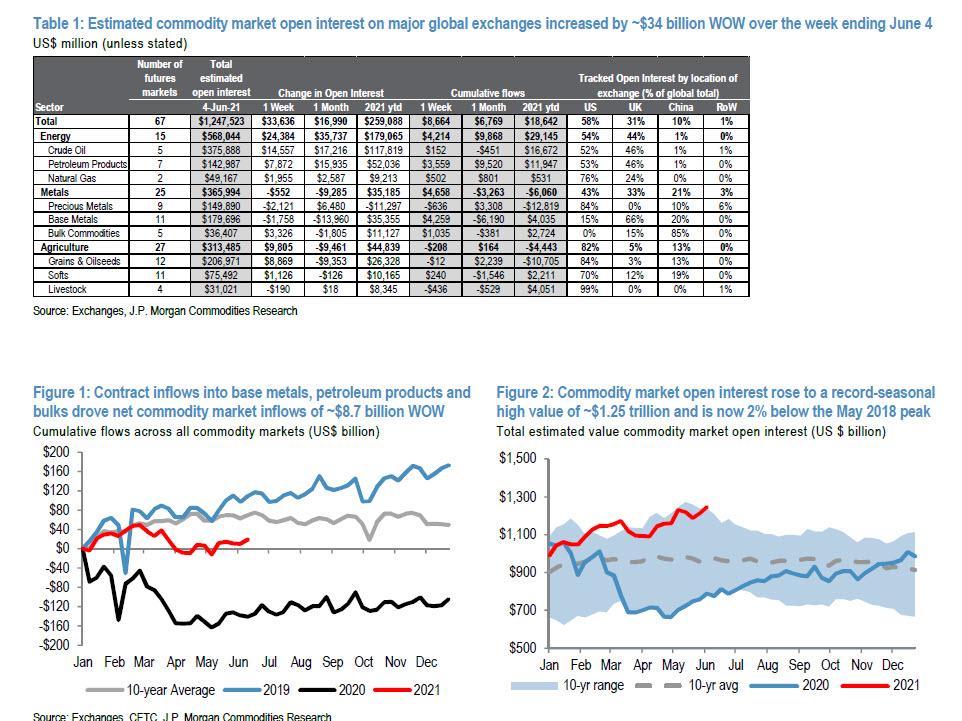

And now, according to JPMorgan, we may be poised for an even more powerful move higher in the commodity space, where estimated market open interest surged by ~$34 billion WoW to a record-seasonal high value of ~$1.25 trillion and is now only 2% shy of the historical peak of May 2018.

In the report authored by Ruhani Aggrawal, the largest US bank notes that price-led gains across crude oil and G&O drove the weekly increase, coupled with price- and contract-based gains across petroleum products, bulks, natural gas and softs. In contrast, precious and base metals open interest posted a combined weekly decline of ~$3.9 billion.

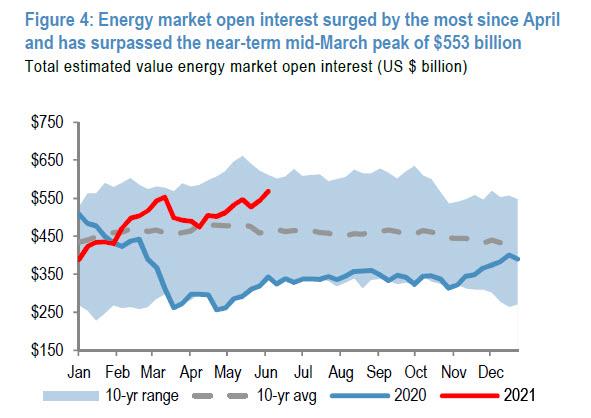

The report also reveals that contract inflows into base metals, petroleum products and bulks drove net commodity market inflows of ~$8.7 billion WOW, increasing the year-todate inflows to ~$18.6 billion. While energy is not nearly at a record level yet, it may soon get there: as shown in the next chart, energy market open interest surged by the most since April and has surpassed the near-term mid-March peak of $553 billion.

Some more details:

- Managed Money net length in oil F&O (NYMEX WTI and ICE Brent) jumped by 4% WoW over the week ending June 1 after three straight weeks of declines though, at ~649,520 lots,the net length is 12% below the near-term mid-February peak. Here JPM notes that “with summer now underway inthe northern hemisphere, oil demand tracking will be critical over the coming months.” As a reminder, last week we noted that JPM’s fundamental strategists’ base case is for a peak in prices around $80/bbl in late 2021; however if demand were to come in hotter than their projections over the next months, prices could peak towards $80/bbl earlier than their expectations.

- Non-Commercial net length across US traded agri markets bounced by 7% WOW to ~737,760 lots (June 1) after a month of declines, as the ongoing Brazilian drought supported net length additions, notably across ICE #11 Sugar, CBOT Corn and ICE Coffee. Moreover, F&O open interest rose by 2% WOW led by G&O, with contributions from softs.

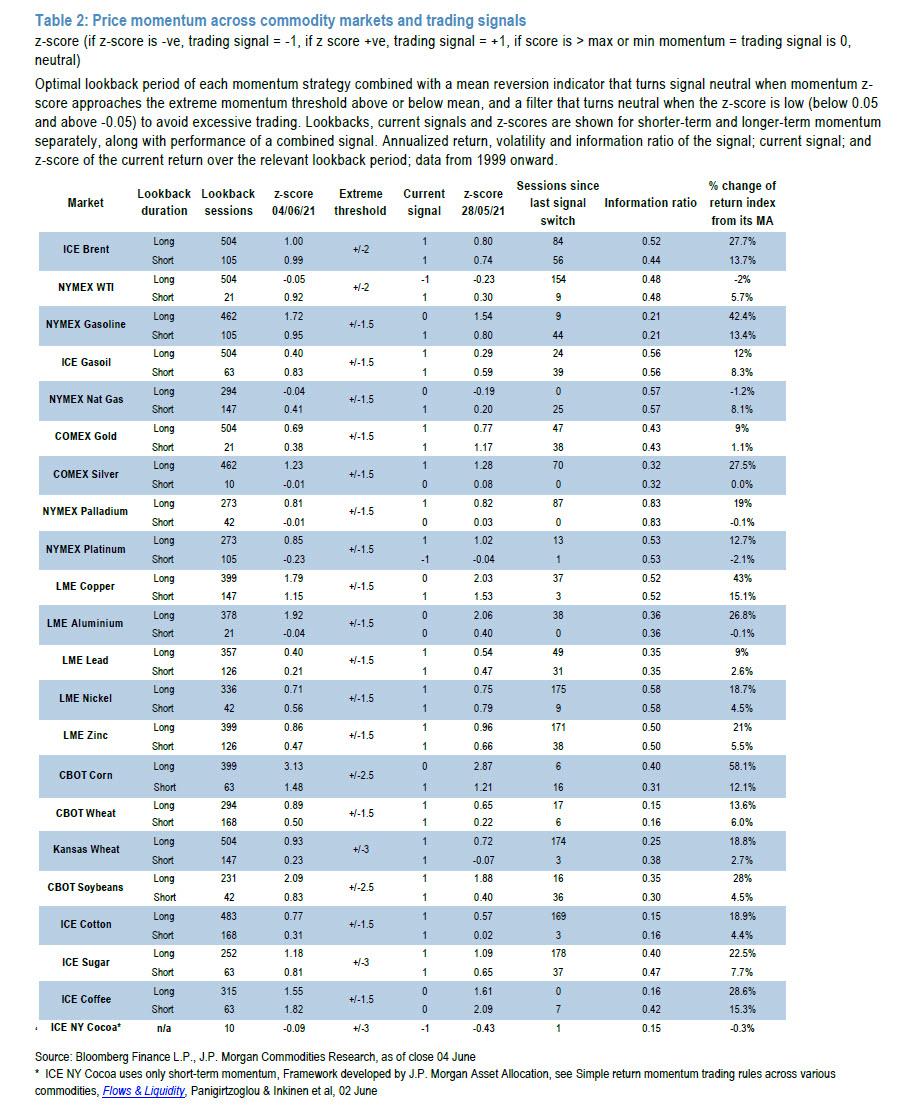

Due to the reflexive nature of the derivatives sector, where positioning often dictates price, price momentum across energy markets increased in the past week, in part due to the near-record accumulation of bullish bets.

But what is perhaps most notable for oil bulls, JPM notes that the long-term NYMEX WTI trading signal is approaching a ‘sell-to-buy’ switch for the first time since January 2020.

Sadly for precious metal bulls, price momentum across precious and base metals slumped WoW with the short-term trading signals across COMEX Silver, NYMEX Palladium and LME Aluminum tracking close to a negative switch. At the same time, positive momentum across ags rose WOW, led by G&O.

Bottom line: with oil already trading at the highest level since 2018, and on pace to surpass its October 2018 highs, bets are surging that the next stop could be prices not seen since before the 2014 OPEC Massacre…

Tyler Durden

Tue, 06/08/2021 – 14:28

via ZeroHedge News https://ift.tt/3vdrYLv Tyler Durden