Goldman Doubles Down On Oil: Says Ignore OPEC+ Drama, World Desperately Needs Extra 5 Million Bpd To Avoid “Critically Low Inventories”

As is well-known by now, the July OPEC+ meeting never concluded as the UAE and Saudi Arabia/Russia failed to overcome their differences, with the former asking for a higher baseline from April 2022 and the latter for an extended commitment through 2022. Picking up on this development Goldman’s commodity strategist Damien Courvalin – who has been extremely bullish oil in recent months – concedes that while this lack of agreement has introduced uncertainty into the OPEC+ production path, its base-case remains “for a gradual increase in production through 1Q22 that would ultimately help meet their preferences, with Brent prices at $80/bbl this summer.”

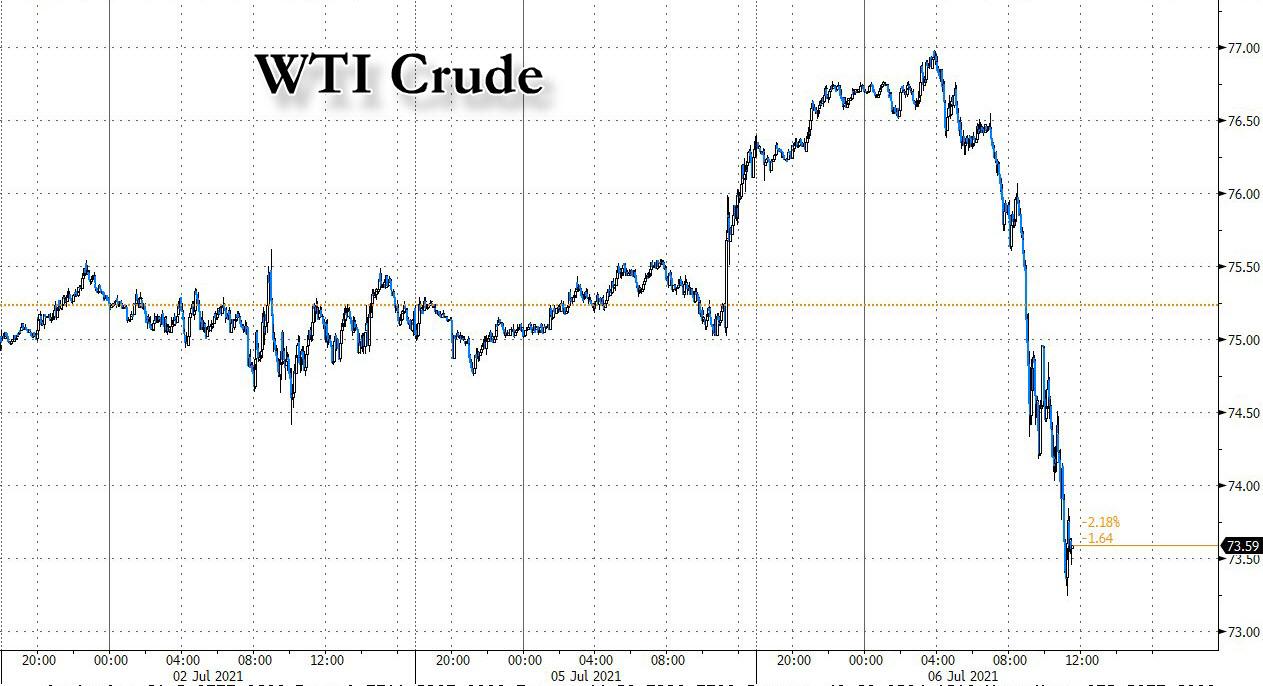

Looking ahead, Goldman predicts that as negotiations continue, most outcomes (1) still imply higher prices in coming months as the physical market tightens, (2) with higher OPEC+ production than the group discussed needed by the global oil market next year. That said, Goldman warns that price volatility will likely rise – which can be clearly seen in today’s violent reaction which saw WTI surge then slide – with the release of the August OSP the key next catalyst.

But the most important observation in the Goldman note is that OPEC+ drama notwithstanding, the world will still be in trouble unless an additional 5mmb/d in production emerge by year-end, to wit: “while the threat of a new OPEC+ price war is no longer negligible, “its negative price impact would be dampened by a global market starting in a 2.5 mb/d deficit and in need of an extra 5 mb/d in production by year-end to avoid critically low inventories.”

Big picture, Courvalin writes that typical OPEC+ histrionics aside, the differences between both parties seem surmountable as they agree on ramping-up production into year-end with the still high uncertainty for 2022 oil balances making a pledge to any long-term commitment unnecessary today.

Goldman’s base-case therefore remains for a gradual increase in production in 2H21 – slightly larger than that discussed by the group (at a 0.5 mb/d monthly rate – akin to lower compliance), followed by similar increases in production in 1Q22 to finally bring the fall in inventories to an end, at their lowest levels since 2013.

And here a key point: given Goldman’s forecast for rising demand offset by slow global production recovery (largely due to the mothballing of US shale due to ESG), as well as the decline in productive capacity expected from many OPEC+ producers due to under-investment, Goldman believes that “such a path would further allow the UAE, Saudi and Russia to bring production to or near quarterly average records, helping meet all their preferences.”

Always bullish, Courvalin also writes that the recent stalemate has introduced the potential for alternate OPEC+ production paths, and mapping these into Goldman’s pricing model point to c. $3/bbl upside to the bank’s forecast under a delayed production ramp-up scenario and instead $9/bbl downside relative to our forecast in an all out price war and higher quota scenario (as describe further below).

Importantly, and unlike last year, such an “all out price war” remains a low probability outcome in Goldman’s view, with its price impact significantly muted by the current large oil deficit “and a market requiring a 5 mb/d increase in global production by year-end to prevent inventories from collapsing to critically low levels.”

In summary, Goldman continues to expect that its forecast for higher OPEC+ production in 2022 (akin to higher baselines) would justify Brent prices settling at $75/bbl, above market forwards with Dec-22 Brent still trading at $68.6/bbl. At the same time, the binding nature of a physically tight oil market would still warrant higher prices this summer even if higher output is expected next year, as real assets like commodities are not anticipatory and cannot price future supply-demand changes in the face of low inventories.

Finally, Goldman lists the following four likely outcomes from the ongoing OPEC+ standoff:

- Our base-case. A deal to increase production as discussed last week could still be reached in coming weeks – as proposed this would nearly match our base case for 2H21, with monthly increases of 0.4 mb/d and offsets for a potential increase in Iran exports. We forecast this would take Brent prices to $80/bbl this summer.

- A deal to ramp-up. Barring a deal in coming weeks, the current OPEC+ agreement would imply August production at July’s level, 0.5 mb/d less supply than our forecasts. If this is made up in September (so a 1 mb/d increase that month), the bullish impact on our forecast would simply be of $1/bbl. If instead, the monthly increases only start in September, with no make-up for the August miss, the bullish impact would be $3/bbl.

- Higher baseline. As we have argued previously, the UAE’s request for a higher baseline is warranted given its investments in recent years although it is not as bearish as first appears. A new baseline would likely replicate the Saudi and Russia model, based off April 2020 surge product levels. Saudi reached 11.6 mb/d of production that month and was allocated an 11 mb/d baseline. Applied to the UAE, this would imply a 3.6 mb/d baseline vs. 3.17 mb/d currently (with Kuwait’s baseline rising modestly from 2.8 mb/d to 2.95 mb/d and most other countries actually having a lower baseline than currently). Importantly, this would in no way imply that the UAE’s baseline would rise to its stated production capacity, just like Saudi’s baseline is not its productive capacity. If such new baselines are used for August onward – with a similar 0.4 mb/d monthly rate of increase – the net impact on our balances would be 0.55 mb/d extra production going forward, representing only $3/bbl dollars downside relative to our base-case.

- Price war. If the current impasse leads to an outright price war, we aggressively assume that the main OPEC+ producers return to Apr-20 production levels for 2 months before they agree to either of the scenarios above (which would translate into additive price impacts)[1]. This would represent 3.6 mb/d extra production versus our base-case, which over two months would represent $6/bbl downside to our price forecast. Followed by a deal to increase production gradually but from higher baseline production, for example, this would represent, combined, $9/bbl downside to forecast oil prices. This is a much more limited impact than last year given the large current deficit. While still net bearish relative to spot price levels, our higher summer fair value forecast and the elevated level of Brent put skew still leaves forwards pricing with a non-negligible probability of such an outcome, with Oct-21 Brent options (expiring at the end of August) already pricing in a 31% probability of prices falling to $71/bbl, $9/bbl below our summer forecast, for example.

Tyler Durden

Tue, 07/06/2021 – 12:10

via ZeroHedge News https://ift.tt/3dOgbgw Tyler Durden