‘Bad News’ Is Bad News Again: Stocks Slammed On Macro Meltdown, Bonds Shrug

Well that rotation didn’t last long.

Yesterday’s ‘good news’ spoiled the ‘growth scare’ narrative (which would pressure The Fed to lift its foot off the market’s throat) and sent stocks lower.

Today, a disastrous set of data reignited the ‘bad news is bad news’ mantra as Consumer confidence crashed, Richmond Fed was routed, Retail and Wholesale sinventories rose less than expected (not good for GDP and a signal that comanies are losing confidence in the consumer), Home Price acceleration slowed a smidge, Goldman’s Retail Spending comps in dex tumbled to its weakest since 2019, and Nielsen data showed increasing price pressures on the US consumer.

All of which pushed ‘hope’ back near pre-Trump lows with soft survey data leading hard real economic data lower…

Source: Bloomberg

All of which means the relative resilience of consensus margin and earnings estimate is likely to come increasingly under scrutiny which sent stocks significantly lower on the day with Nasdaq the biggest loser (down over 3% on the day). NOTE that overnight futures were bid towards the Asia close as China eased its COVID travel restrictions but after an initial mini spike at the US cash open, everything got clubbed like a baby seal…

The Nasdaq dived shortly after the kneejerk higher on the US cash open and erased all gains to the cash open on Friday. The S&P 500 and Dow also erased all of its post-Friday-open gains…

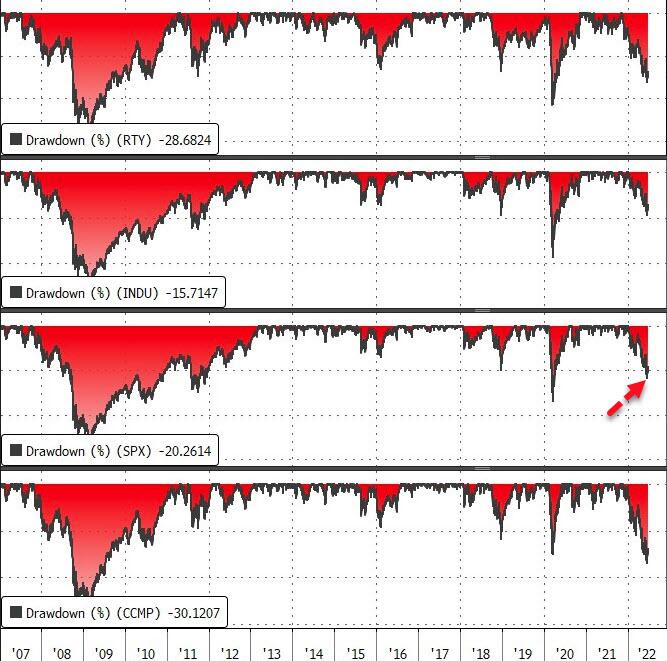

The S&P 500 fell back into bear market territory…

Source: Bloomberg

We note that today’s ugly data did nothing to stop the reversion to a hawkish trend in rate-hike expectations that hit yesterday…

Source: Bloomberg

VIX retraced all of yesterday’s drop, trading back up near 29 today…

Despite an ugly 7Y auction – following yesterday’s ugly auction – and the bloodbathery in stonks, Treasuries ended the day basically unchanged. Asia was buying bonds, Europe was selling, and US session saw the bid come back to leave 30Y yields -1bps and the rest unch…

Source: Bloomberg

The dollar spiked today as the Euro weakened as the ECB claimed it would start its defragmentation tool this weekend, just as QE ends…

Source: Bloomberg

Crypto was slammed.. again… with Bitcoin dropping back near $20k…

Source: Bloomberg

Gold rallied overnight in the Asia session then was sold all the way through Europe and US sessions…

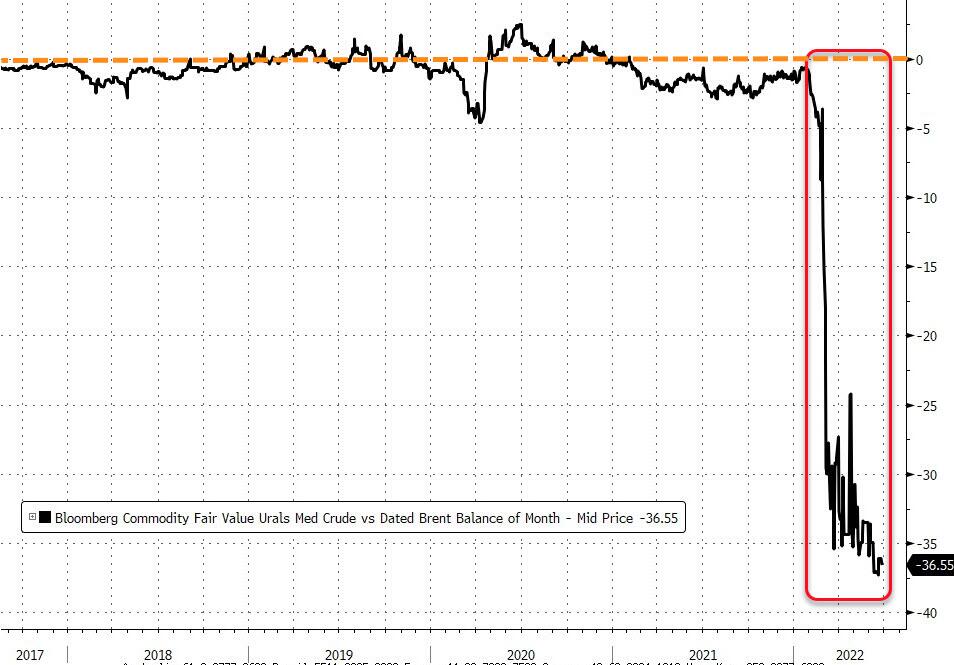

Oil traded higher once again ahead of tonight’s API inventory data (note tomorrow’s official EIA data will include last week’s delayed data) helped by G-7 price cap malarkey and relatively positive news from China easing its quarantine restrictions…

Notably, while the G-7 were busily trying to persuade the world to cap the price they pay for Russian oil, the discount from brent for URALS Med Crude hit a new high of $36…

Source: Bloomberg

Remember, 1) they will never persuade China or India to agree, and 2) western nations already don’t buy Russian oil.

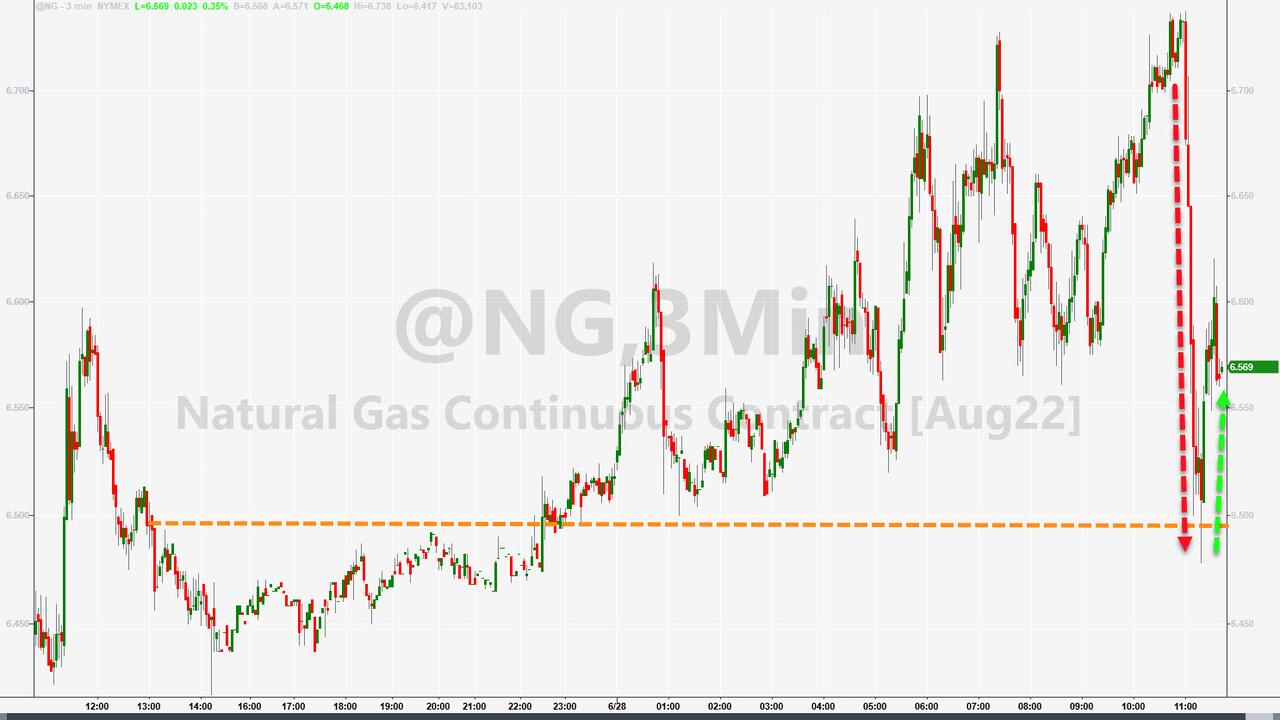

US NatGas tumbled in the afternoon – after Europe closed – perhaps on news that gas flows returned through Turkstream and the G-7 price caps – but ended modestly higher…

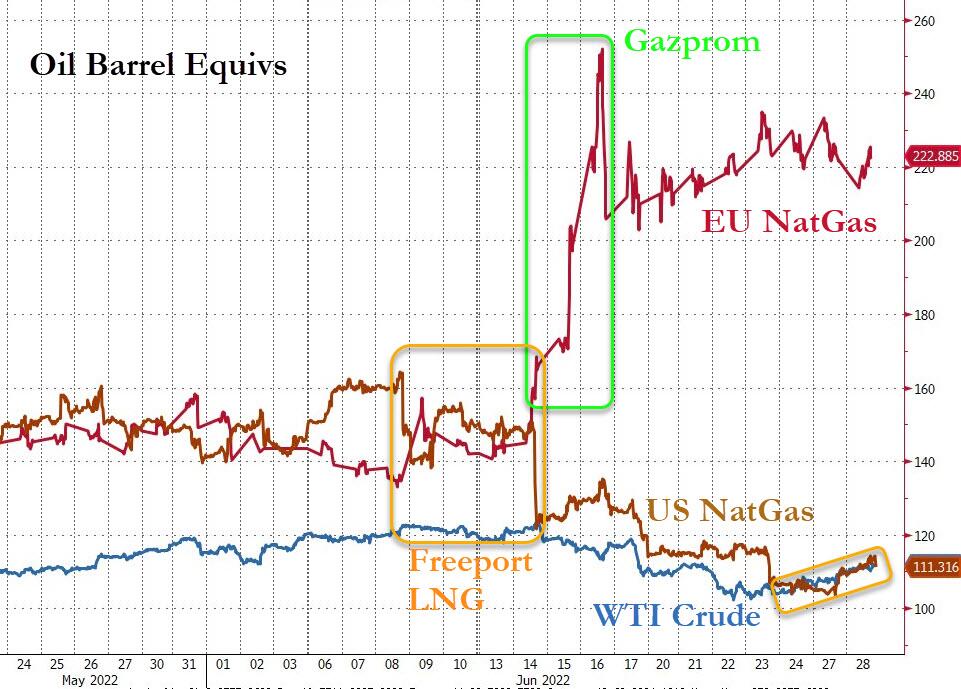

But US NatGas is trading in line with WTI on an oil barrel equivalent price (and EU NatGas trading almost 100% higher)…

Source: Bloomberg

Copper pumped and dumped today to end modestly lower, rallying during the Asia session (China easing restrictions) then selling off through Europe and US….

Finally, we note that US TSY Bonds are at their cheapest relative to stocks since 2011 and at a level of cheapness that has previously prompted rotation from stocks into bonds…

Source: Bloomberg

TINA is dead and quarter-end rebalancing may be a problem for those expecting stocks’ losses to mean some refills.

Also, as a reminder, the dollar liquidity market remains under stress…

Source: Bloomberg

Nothing to panic about yet but the closer we get to quarter-end, we will see who’s swimming naked.

Tyler Durden

Tue, 06/28/2022 – 16:01

via ZeroHedge News https://ift.tt/mu8Npke Tyler Durden