Beijing Gets Going With Nine Weeks Left For 2023

By Charlie Zhu and Helen Sun, Bloomberg markets live reporters and strategists

Three things we learned last week:

1. China’s top leadership is finally making a concerted effort to get the economy and external relations back on track. A rare move to raise the budget deficit mid-year, along with President Xi Jinping’s unprecedented visit to the central bank, underscored a sense of urgency among policymakers to support growth.

For starters, a plan to sell 1 trillion yuan ($137 billion) of sovereign debt over the last nine weeks of the year may finally be the bazooka many investors have been asking for earlier.

Beijing’s diplomatic moves also provided cause for some optimism. Xi sat down with California’s Gavin Newsom, the first time he met a US state governor in more than six years. Foreign Minister Wang Yi’s US trip has also paved the way for a leaders’ meeting next month.

The world’s two largest economies rebuilt communication lines on the economic and financial front. Two working groups which involve officials from the central banks, treasury departments, securities regulators held their first meetings last week respectively.

China also invited US officials to a defense forum to be held this week. While thorny issues remain for the two, these developments help Beijing create a more stable geopolitical environment that serves as a precondition to woo back foreign investors.

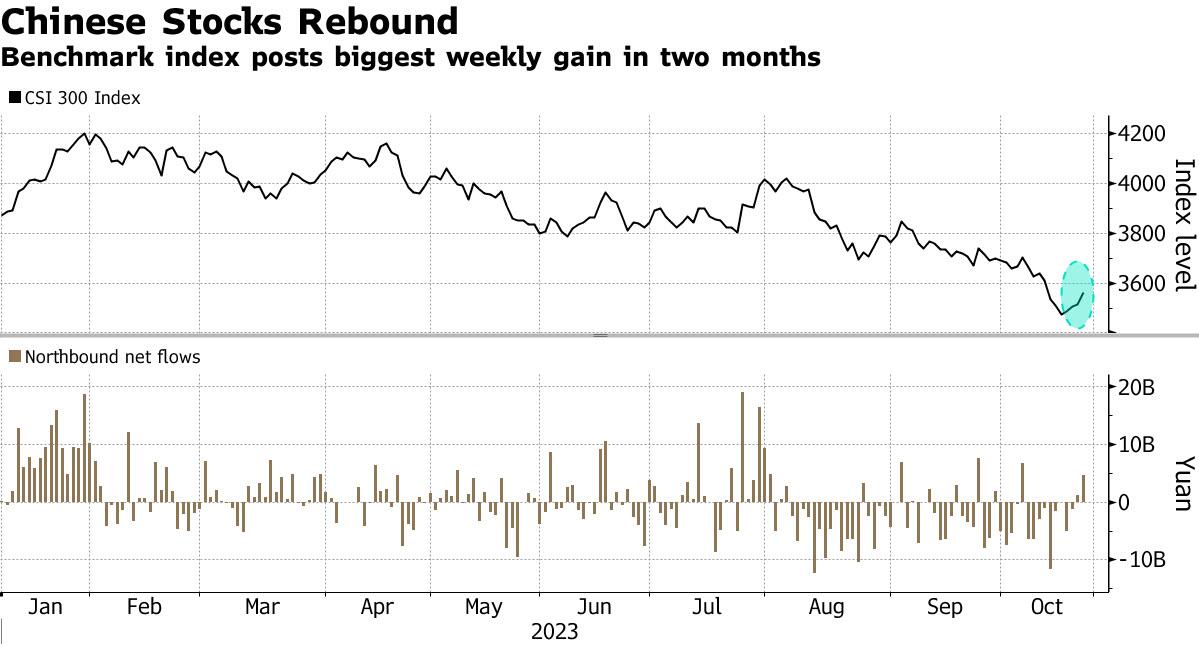

The benchmark CSI 300 Index posted the biggest weekly gain in two months. Foreign investors showed up via the northbound stock connect, buying for two consecutive days, the first time since early August.

2. Those are of course not silver bullets for China’s challenges. Among them, an ongoing property crisis comes on top of the list. With former top developer Country Garden Holdings Co. deemed to be in default on a dollar bond, recent weakness in China Vanke Co. and Gemdale Corp.’s notes spurs concerns that the sector is still deep in the doldrums.

Economic growth may drop below 3% in 2024 if the real-estate slowdown deepens, according to S&P Global Rating. Its base-case scenario is for growth rate to slow to 4.4%, down from Beijing’s targeted 5% this year.

A series of arrests across industries, an investigation into Taiwan’s Foxconn Technology Group — the biggest private employer — along with the removal of Li Shangfu as defense minister without explanation, again shook the confidence of foreign companies.

The recent reaction from market participants to earlier stimulus measures bear resemblance to the Tacitus Trap, Ken Cheung, Mizuho Bank Ltd.’s chief Asia FX strategist, wrote in a note, referring to a political theory where a government fails to win approval even for the right policies.

While building confidence in the economy will require time, adopting more timely and targeted policies to address socio-economic issues can help mitigate the risk of falling into the trap, and enhance the effectiveness of the economic stimulus, Cheung said.

3. China’s slowdown and financial risks are rippling through other markets and global businesses. Falling Chinese stocks are placing as much as $71 billion of structured products in South Korea at risk when they mature next year.

Meanwhile, Standard Chartered Plc’s profit missed estimates in the third quarter, as the lender took a $186 million charge on Chinese real estate and an impairment of $700 million on China Bohai Bank. Nomura Holdings Inc. is overhauling its local business after losses there snowballed.

Tyler Durden

Sun, 10/29/2023 – 22:30

via ZeroHedge News https://ift.tt/F3anrfw Tyler Durden