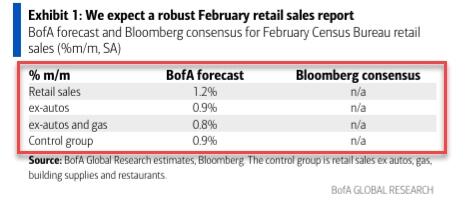

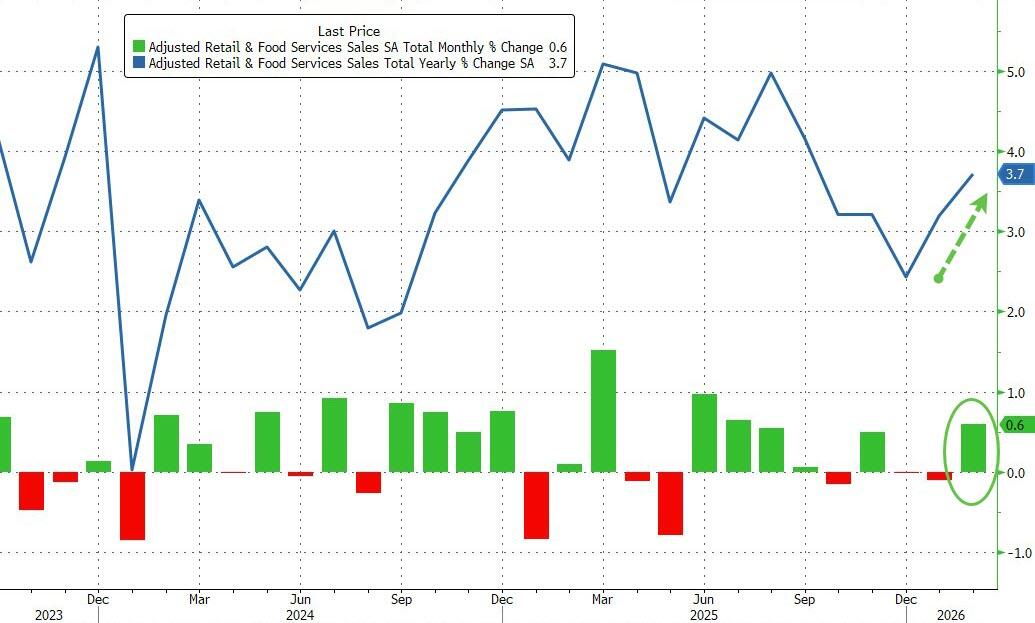

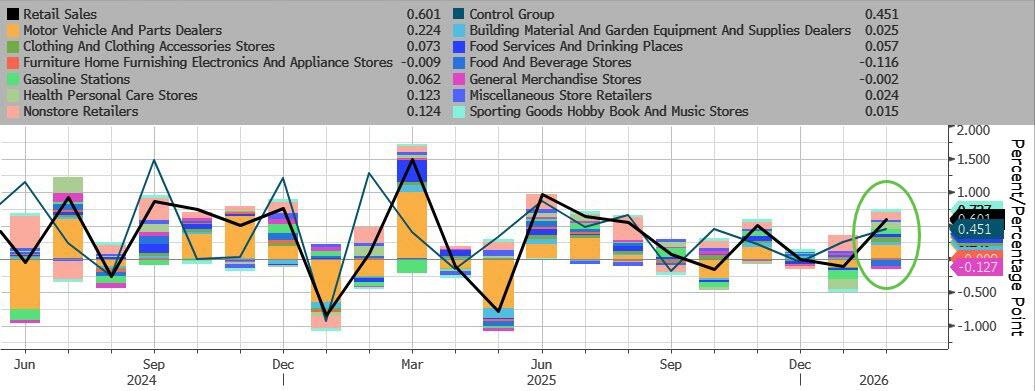

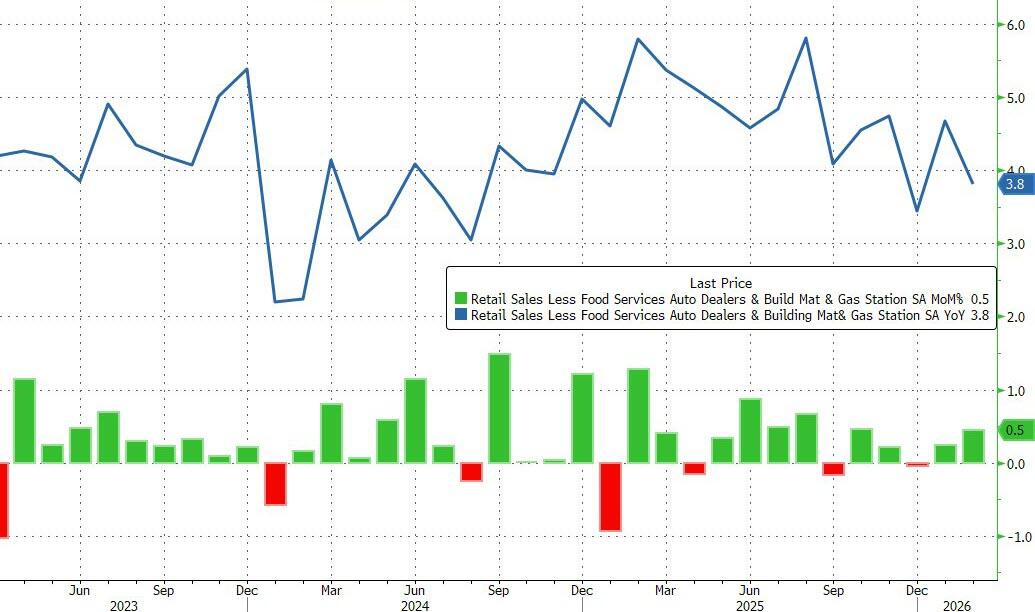

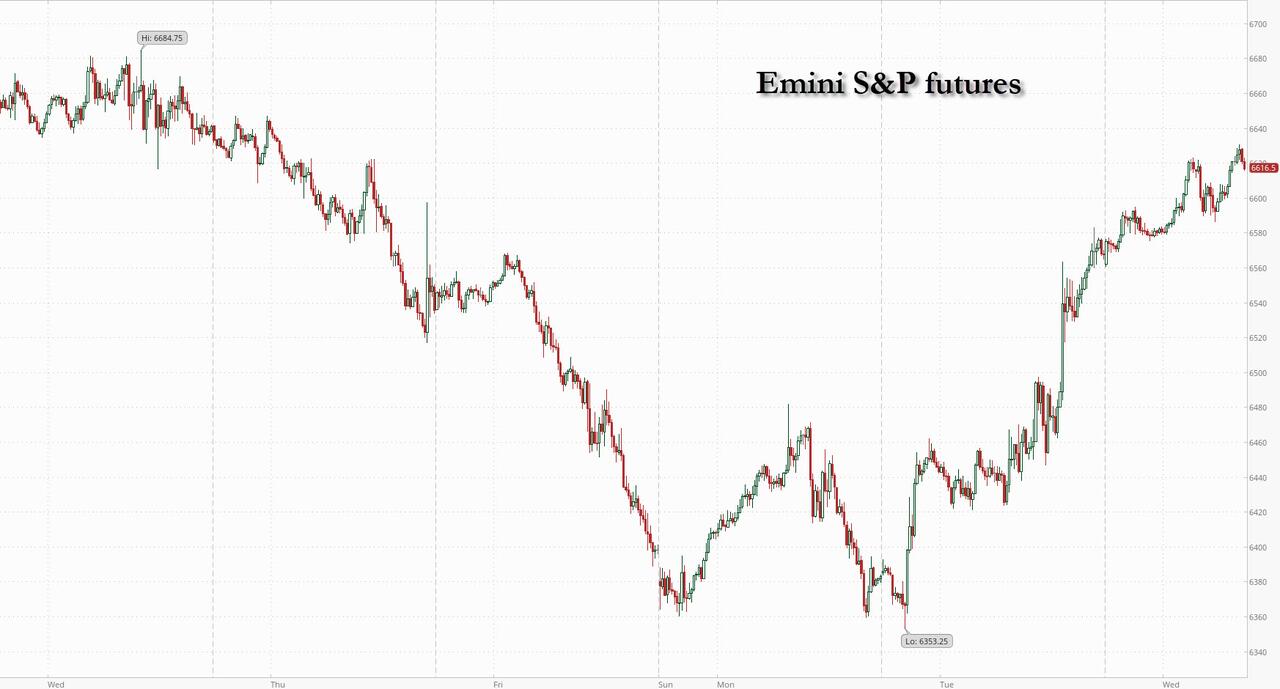

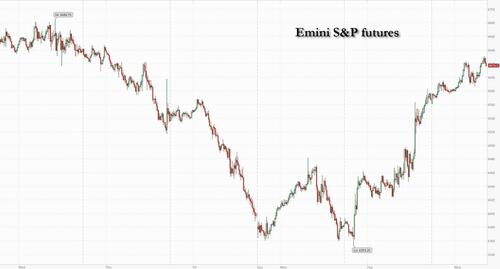

Futures and bonds jump and oil fell, sending Brent briefly below $100 a barrel, as the de-escalation/technical/macro led relief rally continues on hopes of the Middle East conflict reaching an end soon after Donald Trump said he expects the war in Iran to end in two to three weeks, and indicated that it was possible that Iran could still reach a deal with the US during that timeframe. Trump has a national address tonight at 9pm ET to discuss Iran, but the content is unclear, with the market is expressing the view that this will be details on a wind-down rather than an escalation. As of 8:15am ET, S&P Futures were 0.7% higher, after the cash index posted a near 3% advance on Tuesday, the best end to a quarter since September 2008. Nasdaq futures jumped 1.1% with all Mag 7 names higher premarket. European stocks jumped 2.6%, alongside a 4.9% surge in Asian shares. Final Mfg PMIs from the Europe were mixed (EU, Germany, Italy small beats/UK, France small missed) while Japan/Korea Manf PMIs were slightly better. Trump is set to address the nation tonight at 9pm EST and said he expects the war to end in two to three weeks/US would withdraw once Tehran can no longer obtain nuclear weapons. Otherwise, the US is sending a third aircraft carrier to the region, Iran said the US “isn’t serious about diplomacy”, the WSJ reported that the UAE wants to force the Strait of Hormuz open and is willing to join the fight, and attacks continued on both sides with Qatar saying Iran struck an oil tanker. Brent fell 5.4% before paring the move as the Strait of Hormuz remained largely closed and attacks continued across the Gulf. Traders trimmed bets on tighter monetary policy, sending two-year Treasury yields three basis points lower to 3.76%. Comparable UK gilt yields dropped 10 basis points to 4.30%. Looking at today’s US economic calendar, we get March ADP employment change (8:15am), February retail sales (8:30am), March final S&P Global US manufacturing PMI (9:45am), March ISM manufacturing and January business inventories (10am). Fed speaker slate includes Musalem (9:05am) and Barr (9:10am)

In premarket trading, Mag 7 stocks are all higher (Tesla +2.1%, Microsoft +1.5%, Amazon +0.9%, Nvidia +1.4%, Meta +0.6%, Alphabet +0.9%, Apple +0.5%)

- Li Auto ADRs (LI) rise 4% after the Chinese EV firm reported March vehicle deliveries that surpassed its own guidance and analyst estimates.

- MSC Industrial (MSM) falls 6% after the distributor of metalworking products reported adjusted earnings per share for the second quarter that missed the average analyst estimate.

- NCino (NCNO) jumps 24% after the cloud-banking software company’s subscription revenue forecast for 2027 beat the average analyst estimate.

- Nike (NKE) falls 10% after the retailer gave a surprisingly gloomy outlook for the year ahead, complicating Chief Executive Officer Elliott Hill’s efforts to turn around the business.

- RH (RH) plunges 17% after the home furnishing company forecast revenue for the first quarter that missed the average analyst estimate.

- Oric Pharmaceuticals (ORIC) slides 21% after the clinical-stage oncology company gave safety and efficacy data from an early-stage trial of its drug-candidate for prostate cancer that underwhelmed Wall Street.

- Target Hospitality (TH) rises 24% after the provider of modular housing announced secured a multi-year contract worth more than $550 million. The company will construct and provide hospitality services for a hyperscaler’s data center development in North Texas.

In other corporate news, Unilever said talks to sell most of its food business to McCormick are advanced and a final deal could be announced later on Tuesday. Boeing will team up with Rheinmetall to offer drones known as the Ghost Bat to Germany’s military.

Signs of an increased desire for de-escalation from Trump may reduce anxiety over his threats to attack Iranian energy infrastructure. On the other hand, Tehran would be left in control of the key oil shipment chokepoint. Meanwhile, Iran hit a fully laden Kuwaiti oil tanker off Dubai in a drone attack. Without a ceasefire or tangible progress in negotiations, the market will keep “fading the administration’s ‘everything is going well’ happy talk,” Vital Knowledge’s Adam Crisafulli wrote in a note. Carmignac Gestion’s Kevin Thozet observed that “Trump can’t simply turn an on/off switch on the crisis.” Other observers argue that rhetoric alone about a potential end to the conflict cannot create certainty for the market.

Equities are, nonetheless, primed to rip higher on positive news about the war following large-scale unwinding of risk by hedge funds and CTAs. The concern is that, post an initial bounce, worries about the economy and the path for interest rates will trigger further volatility episodes, setting up stocks for months of roller-coaster conditions.

In any case, traders said it would take time for oil flows to return to normal even if the war ends within Trump’s timeframe, especially given the damage to some energy facilities. Trump’s team has also suggested that reopening the Hormuz strait, which carries 20% of global crude, may not be necessary to end the hostilities.

“The correlation between Brent oil prices and global equity markets has been exceptionally strong since the conflict started,” said Wolf von Rotberg, equity strategist at Bank J Safra Sarasin. “This goes to show that a return to previous equity market highs would need the Strait of Hormuz to reopen and oil prices to drop significantly. It is probably too early for an all-clear yet.”

Trump, who will give an address at 9 p.m. Eastern Time to provide an “important update” on Iran, said the Islamic Republic could still reach a deal with the US. He added, however, that an agreement with Tehran isn’t a prerequisite to conclude the war. “We are seeing a relief rally, and with more information we may see a reversal, so we just need to be careful here,” Remi Olu-Pitan, multi-asset growth and income head at Schroders, told Bloomberg TV. “There’s still a lot of volatility, the market is still fragile.”

Oil remains in focus for traders, policy makers and consumers. WTI futures are trading above $100 a barrel, while there’s been more commentary around the risks of spikes to $200. Crucially, retail unleaded pump prices climbed above $4 a gallon, the highest since August 2022. With higher gas prices adding near-term pressure on household budgets, Tuesday’s consumer confidence print will be closely watched. Oil, and the uncertainty around the magnitude and duration of supply disruption, was cited by strategists at Morgan Stanley as they downgraded global equities to equal-weight.

The Middle East conflict has caught high-flying chip stocks in its tentacles. Citigroup’s Jim McCormick describes a market wake-up call, noting “we’re looking at a world of sustained higher yields and sustained higher energy costs and that doesn’t help the AI sector.”

Traders at Goldman Sachs Group Inc. and JPMorgan Chase & Co. suggested Tuesday’s sharp rebound in US stocks was more about the unwinding of negative positioning by market participants than a shift in sentiment over the war. “Investors have been counting on a swift off-ramp to war essentially since it began, but I think from a market or global economy perspective it’s important to define what the true clearing event to revisit risk and take down recession odds really is,” wrote JPMorgan industrials sector specialist sales Paige Hanson.

Space is also making the headlines this week, with Virgin Galactic soaring in late trading after it resumed some sales of commercial space flights. NASA is making final preparations for the Artemis II missions, while what a history-making SpaceX IPO could mean for the space economy is discussed in the Big Take podcast.

European stocks are rallying, with the Stoxx 600 up 2% as markets look toward a potential resolution to the Iran conflict. Banks as well as travel and leisure shares are leading gains, while the energy sector is the biggest laggard. Stoxx 600 rises 2.2% to 595.73 with 65 members down, 532 up, and 3 little changed. Here are the biggest movers Wednesday:

- Athens Stock Exchange Index rises as much as 4.3% at Wednesday open, following index provider MSCI’s decision to upgrade the Greek market to developed status

- Thule rises as much as 5.7% after SEB Equities upgrades to hold, removing the only sell rating on the maker of roof and bike racks, to reflect “more reasonable expectations” now baked into the stock

- Sandoz shares rise as much as 5.1%, the most in five weeks, after Goldman Sachs initiated coverage on the stock with a buy recommendation

- Inficon gains as much as 8.1%, the most since Jan. 15, as JPMorgan starts coverage at overweight, saying the vacuum instrument maker should be a beneficiary of the multiyear upcycle in wafer fabrication equipment

- Arcadis shares rise as much as 6.6%, the most in six months, after Bank Degroof Petercam upgraded the engineering services firm on expectation that the new management team will be able to drive a recovery

- Jungheinrich shares rise as much as 9.8%, their steepest ascent in around a year, as Bernstein boosts its price target on the German machinery company, citing enticing long-term prospects

- Nordex falls as much as 3.8% after Bank of America downgraded the German wind turbine manufacturer to neutral from buy following a 56% year-to-date rally that the bank says has priced in most of the bull case

- Berkeley Group shares plunge as much as 19% to hit a nine-year low, after the housebuilder’s profit goal for the FY27 to FY30 period significantly undershot expectations

- SoftwareONE shares drop as much as 8.9%, hitting a seven-month low, after an investor offloaded shares at a discount to yesterday’s closing price. Shares have fallen below the offer price this morning

- Cirsa Enterprises drops as much as 5% after one of its investors offloaded shares at a discount to Tuesday’s closing price. The stock is holding above the offer price on Wednesday

UK Prime Minister Keir Starmer said his government will coordinate a diplomatic push for the strait’s reopening, affirming Britain’s desire not to be dragged into the military conflict. “I would expect further volatility in the days to come and the market to oscillate between losses and gains for a few more sessions until we get clarity on how the crisis unfolds,” said Alexandre Baradez, chief market analyst at IG Markets. “This is likely more a temporary respite than a final game changer.”

Earlier in the session, Asian stocks jumped the most in nearly a year, tracking Wall Street’s rally on optimism that the war in Iran may end in the near future. The MSCI Asia Pacific Index gained as much as 5.2%, the most since April 10, with shares in South Korea, Taiwan and Japan leading the gains. Technology giants Taiwan Semiconductor Manufacturing Co., Samsung Electronics Co. and SK Hynix Inc. provided the biggest boost to the gauge’s advance. Asian markets would stand to gain more than others if the US manages to defuse the war with Iran, as investors unwind an energy‑driven risk premium that has hit the region harder than most. The conflict has pushed oil prices sharply higher, driving equity sell‑offs and currency volatility across Asia’s oil‑importing economies. Still, the regional gauge remains down about 9% from a peak in February, with investors questioning how quickly oil can fall and how credible Trump’s assurances are. Market focus will now shift to an “important update” on Iran that Trump is scheduled to deliver at 9 p.m. Washington time.

In FX, the Bloomberg Dollar Spot Index fell as much as 0.4%, while Treasury yields dropped four basis across the curve. Swaps imply 11 basis points of Federal Reserve rate reductions by year-end, compared to 5bps on Tuesday. EUR/USD up as much as 0.5% to 1.1611, while GBP/USD up as much as 0.6% to 1.3301. USD/CHF drops 0.8% to 0.7928, EUR/CHF down 0.5% to 0.9190; leveraged desks seen unwinding franc shorts, a Europe-based trader says

In rates, fixed income markets have rallied but lost a bit of steam in recent trade. US yields are around 3bps lower across the curve as markets assign a 40% chance of a Fed rate cut by year-end versus a 64% chance of a hike last week. Treasury futures are off session highs in early US session, although yields remain 2bp-4bp lower across a steeper curve. US 10-year is about 3bp richer on the day near 4.29%, while 5s30s spread is steeper by ~1bp. Gilts outperform, with UK front-end yields richer by 8bp as oil broadly holds losses. Investors face the prospect that US President Trump, slated to speak at 9 p.m. in Washington, will soon declare an end to the war in Iran.

In commodities, despite the optimism in stocks, crude prices have faded declines in the European session. Brent is now back above $100 per barrel having earlier dropped below the key level. WTI crude oil contract has pared a 4.8% slump to about 2.5%, and was last trading just around $99. Precious metals are diverging, with spot gold up 1.4% and silver down 0.5%. Bitcoin has added 0.5%.

Looking at today’s US economic calendar, we get March ADP employment change (8:15am), February retail sales (8:30am), March final S&P Global US manufacturing PMI (9:45am), March ISM manufacturing and January business inventories (10am). Fed speaker slate includes Musalem (9:05am) and Barr (9:10am)

Market Snapshot

- S&P 500 mini +0.9%

- Nasdaq 100 mini +0.8%

- Russell 2000 mini +1.4%

- Stoxx Europe 600 +0.7%

- DAX +0.7%

- CAC 40 +0.5%

- 10-year Treasury yield -3 basis points at 4.32%

- VIX -1.7 points at 28.87

- Bloomberg Dollar Index little changed at 1221.56

- euro little changed at $1.147

- WTI crude -0.9% at $101.92/barrel

Top Overnight News

- Trump will deliver a speech on Wednesday at 9 p.m. Washington time to give an update about the war in Iran: BBG

- Oil fell, sending Brent briefly below $100 a barrel, after Donald Trump said he expects the war in Iran to end in two to three weeks. The US would withdraw once Tehran can no longer obtain nuclear weapons, he said. Attacks continued across the Middle East. Qatar said a cruise missile from Iran struck an oil tanker. BBG

- The United Arab Emirates is preparing to help the U.S. and other allies open the Strait of Hormuz by force, Arab officials said, a move that would make it the first Persian Gulf country to become a combatant, after being hit by Iranian attacks. WSJ

- Trump said he’s strongly considering pulling the US out of NATO after it didn’t join the war on Iran. He told the Telegraph that leaving the block was now “beyond reconsideration.” BBG

- California is confronting sky-high petrol prices and the threat of jet fuel shortages because of disruption caused by the Iran war, exposing US energy insecurity as the Strait of Hormuz remains closed. The most populous US state is vulnerable to the turmoil in world energy markets because it relies on imports of refined products such as petrol and jet fuel from Asia after introducing ambitious plans to phase out fossil fuels and significantly reduce refining capacity in favor of renewables. Californians pay the most for petrol in the country, with a gallon averaging $5.88 — the highest level since the pandemic — compared to $4.01 in the rest of the US, according to the American Automobile Association. FT

- Russia exported more liquefied natural gas in the first quarter of 2026 than it did a year earlier, with shipments to Europe increasing despite Moscow’s push to redirect supply away from the region. RTRS

- China’s factory activity slowed in March for export-oriented firms as their costs surged, according to RatingDog’s PMI. That contrasts with an official gauge that showed manufacturing improving despite the Iran war. BBG

- Chinese government bonds have sidestepped a global debt sell-off since the start of the Iran war, as the world’s second-biggest economy emerges as a haven from soaring energy prices and rising global inflation. Investors are betting that whereas major central banks in the US and Europe will be forced to keep interest rates at higher levels than previously expected to counter inflation triggered by rising oil and gas prices, China will be relatively insulated thanks to its energy mix and very low inflation before the conflict. FT

- Japan may face stagflation risks from the Iran war that would be challenging to deal with using monetary policy, new Bank of Japan board member Toichiro Asada said on Wednesday. RTRS

- Trump signs executive order related to mail-in voting, said working on proof of citizenship and that voter ID and citizenship proof are subjects for another time.

- OpenAI raised $122 billion at an $852 billion valuation in its largest funding round yet. BBG

- Since the start of the Iran war, market pricing for the fed funds rate has swung sharply, and it now implies a roughly 45% chance that the FOMC will hike in 2026. While some of this reflects changing demand for insurance against the tail risk of more hikes, the market-implied probability that the FOMC delivers 1-2 cuts—the modal case before the war—has declined from 35-40% to about 18%. Expectations for other central banks have moved even more, and market pricing now implies about 70bp of hikes from the ECB in 2026, compared to 8bp of cuts before the war

- Trump asks CPA for lists of insurers who were good to clients, and list who were bad in response to California fires.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly rallied with global risk sentiment buoyed by hopes for an end to the Iran conflict following encouraging comments from the US and Iran, while President Trump also suggested that the war could end in 2 or 3 weeks, and he will deliver a nationwide address on Wednesday evening to give an important update regarding Iran. ASX 200 gained at the open and was led by outperformance in mining, materials, resources and tech, with nearly all sectors in the green aside from some defensives, while the index also shrugged off weak PMIs. Nikkei 225 surged back above the 53,000 level amid hopes of a nearing end to the conflict and after the latest BoJ Tankan survey mostly topped forecasts, with the headline large manufacturing index at its highest in more than five years. Hang Seng and Shanghai Comp conformed to the broad upbeat mood across the region with notable strength seen in mining, tech and biopharmaceuticals, while a miss on Chinese RatingDog Manufacturing PMI and the smallest PBoC injection in more than a decade failed to derail the momentum.

Top Asian News

- Chinese RatingDog Manufacturing PMI (Mar) 50.8 vs. Exp. 51.6 (Prev. 52.1, Low. 50.5, High. 53).

- Japanese Tankan Large Manufacturers Index (Q1) 17 vs. Exp. 16 (Prev. 15, Low. 8, High. 18).

- Japanese Tankan Large Non-Manufacturing Index (Q1) 36 vs. Exp. 33 (Prev. 34, Low. 28, High. 36)

- Japanese Tankan Small Manufacturers Index (Q1) 7 vs. Exp. 7 (Prev. 6, Low. -1, High. 9)

- Japanese Tankan Large Manufacturing Outlook (Q1) 14 vs. Exp. 13 (Prev. 15, Low. 5, High. 15)

- Japanese Tankan Large Non-Manufacturing Outlook (Q1) 29 vs. Exp. 28 (Prev. 28, Low. 24, High. 34)

- Japanese Tankan Large All Industry Capex (Q1) 3.3% vs. Exp. 13% (Prev. 12.6%)

European bourses (STOXX 600 +2.1%) continue to rebound, printing a third straight day of gains thus far. The positive was helped following reports that Iranian officials are leaning towards dialogue, while President Trump said that the war is coming to an end. European sectors are entirely in the green, ex. Energy. Banks and Travel and Leisure top the sector pile. Oil prices have been the main driver for airlines, with the drop in energy prices making jet fuel cheaper. Banks have been hit throughout the Iran war, so the prospects of it coming to an end have boosted the sector. To add, HSBC was added to Goldman Sachs’ European conviction list.

Top European News

- Germany’s VDMA said German Engineering Orders -8% in Dec-Feb Y/Y (Domestic Orders -6%, Foreign Orders -8%).

- German Economic Institutes confirm cutting 2026 and 2027 GDP growth forecasts.

- UK government said new measures to ease cost of living pressure to come into force on April 1st. Increasing national living wage to £12.71. Energy bills are to be cut by average £117 a year for millions across the UK and locked in until end of June.

FX

- DXY is on the backfoot this morning with markets pricing in a “de-escalation” trade, after US President Trump said to NBC News regarding the Iran war that “it is coming to an end”, with a White House official suggesting Trump is confident an agreement will be reached soon. Interestingly, from the Iranian side, President Pezeshkian noted that Iran seeks to end the war with guarantees against further attacks. DXY currently holds at the lower end of a 99.41-99.88 range. It is worth highlighting that the index saw some strength after the Iranian Deputy Speaker of Parliament said that the “Strait of Hormuz will never be opened, there has been no negotiation and there will be no negotiation”.

- G10s are entirely stronger against the USD, albeit to varying degrees. The CHF outperforms, benefiting from lower energy prices – the likes of GBP and EUR also benefit. For the GBP specifically, the UK government confirmed new measures to ease the cost of living pressure are to come into force today, including an increase in the national living wage to GBP 12.71 and with energy bills to be cut by an average GBP 117 a year for millions across the UK, which will be locked in until end of June.

- JPY also gains vs USD, albeit to a lesser degree vs peers. The seemingly easing Iran tensions has benefited the JPY, which builds on the strength seen in recent sessions, facilitated by jawboning and a hawkish-leaning BoJ SOO earlier this week. As for today, Japan’s Tankan survey was mostly stronger-than-expected, which supports the case for an April BoJ rate hike. USD/JPY currently trades within a narrow 158.27-159.01 range.

Central Banks

- BoJ new Board Member Asada does not comment on any specific stance. Rising oil prices put upward pressure on inflation while weighing on growth, creating a stagflationary trend.

- ECB’s Stournaras said if oil prices rise over USD 150/bbl Europe could face a recession.

- ECB’s Dolenc said ECB’s adverse scenario is more likely to be the next baseline and current baseline is more like the best-case scenario.

Fixed Income

- An overall positive start in the fixed income benchmarks, with energy prices falling and higher hopes of a potential end to the Iran conflict. President Trump stated that the war is coming to an end, while a White House official said that the President is confident that an agreement will be reached soon.

- USTs are trading at the upper end of a 111-10 to 111-14+ range, albeit off best levels, as energy prices rebound slightly. Price action is set to remain rangebound ahead of a flurry of data and Fed speak, while Trump is set to speak at 21:00EDT/02:00BST.

- Bunds, in tandem with its peers, are gaining and currently holding above the 126 handle. The 10yr yield extends further below 3.0%, printing a trough at 2.933% before bouncing slightly. EZ final manufacturing PMI ticked slightly higher above the prelim. Figure but failed to drive any move in EGBs. In addition, ECB speakers reiterated the impact higher energy prices have on the European economy.

- Gilts outperform, continuing to be the beneficiary of lower energy prices, as BoE pricing remains sensitive to oil prices. Pricing for rate hikes have pulled back, now price in 44bps of hikes in 2026.

- Germany sells EUR 3.025bln vs exp. EUR 4.0bln 2.50% 2032 Bund: b/c 1.11x (prev. 1.51x), average yield 2.78% (prev. 2.60%), retention 24.3% (prev. 20.1%).

Commodities

- In geopolitics, optimism was seen on Tuesday over a potential end to the war, particularly following Trump’s overnight comments that the US could leave Iran in two to three weeks. This follows reports that the US could exit Iran without reopening the Strait of Hormuz, with Trump calling on users of the strait to secure it themselves. Trump is due to make an announcement tonight at 21:00 EDT/02:00 BST. Some of yesterday’s optimism waned after commentary from the Iranian Deputy Speaker of Parliament, who said: “Strait of Hormuz will never be opened, there has been no negotiation, and there will be no negotiation.”

- WTI and Brent initially dipped to lows of USD 96.50/bbl and USD 98.35/bbl respectively as markets initially continued the move from yesterday, although a floor was later found on the Iranian deputy speaker comments, with Brent back above USD 100/bbl and WTI near USD 99/bbl at the time of writing, both still lower intraday by over USD 2/bbl apiece. Dutch TTF prices are softer once again after slipping over 7% in the prior session, with desks citing favourable weather alongside hopes of an Iranian war de-escalation.

- Spot gold is slightly firmer amid the softer USD and lower oil prices, with the yellow metal back above its 100 DMA (4,642.48/oz) in a current USD 4,661.61-4,747.77/oz parameter. Conversely, spot silver is softer on the day following yesterday’s +7% gains, with the metal today finding resistance near its 100 DMA (USD 75.22/oz).

- Base metals mostly eke out mild gains in what is seemingly a function of the USD alongside recent positive sentiment amid hopes of a de-escalation of the Iranian situation. 3M LME copper resides in a current USD 12,380.00- 12,499.75/t range after finding resistance around USD 12,500/t.

- IEA Chief Birol says more than 12mln BPD of oil supply has been lost so far due to the Middle East crisis; the current crisis is worse than the 1970s oil shocks and the loss of Russian gas in 2022 combined. Oil supply losses in April are expected to be twice as high as in March. Biggest problem is a lack of jet fuel and diesel, already affecting Asia and coming to Europe in April–May.

- UK PM Starmer said the fuel duty will remain where it is until September.

- South Korea has raised its energy disruption alert to the second-highest level due to the possible crude oil supply crisis, via Yonhap.

- US extended a Russian oil transit license via Kazakhstan to China until March 2027, according to IFX cites Kazakh Energy Ministry.

- US Private Inventory Data (bbls): Crude +10.3mln (exp. -1.3mln), Distillate -10.4mln (exp. -1.3mln), Gasoline -3.2mln (exp. -2.2mln), Cushing +0.8mln.

Trade/Tariffs

- India grants one-time customs duty relief for goods made in special economic zone and sold into domestic market.

- US is rushing to put in place a system to pay back USD 166bln it collected now after Trump tariffs were ruled to be unconstitutional, according to Nikkei.

Geopolitics

- US President Trump said he is strongly considering pulling the US out of NATO after it failed to join his war on Iran, The Telegraph reported.

- US President Trump tells NBC News on Iran war “it is coming to an end”.

- US advisers who speak regularly with the US President are reportedly uncertain about the mixed signals from Trump, according to Axios. “Some Trump aides and allies say he’s mostly improvising rather than following any clear plan”. “Aides have been convinced at various points that Trump was leaning toward a major escalation, and at others that he was eager for a swift resolution. “Nobody knows in the end what he’s really thinking,” a senior adviser said.”.

- US Secretary of State Rubio said have largely destroyed Iran’s air force and can see the finish line with Iran objectives, adds end to Iran war is not today, not tomorrow but it is coming. said:. There’s nothing any country is doing to help Iran that is in any way impeding our mission. There is potential for a direct meeting with Iran at some point. US is to re-examine NATO ties post-Iran war.

- Iranian Foreign Minister, when asked about the status of negotiations with the US, said “No decision has been made yet. We have many considerations. Our conditions for ending the war are very clear. We do not accept the ceasefire; We seek a complete end”.

- Iranian Foreign Minister Araghchi reiterates Strait of Hormuz is closed to countries at war with Iran and said the US President must change his approach, also noted that a guarantee from 1-2 countries or from the UN Security Council is not enough. Iran has no plans for negotiations with the US. We are ready for any ground threat and are ready for at least six months of war.

- Iran’s Foreign Minister Araghchi said Iran has zero trust in the US and dismisses the effectiveness of any potential ground operation targeting Iran.

- Iranian Deputy Speaker of Parliament said “Strait of Hormuz will never be opened, there has been no negotiation and there will be no negotiation”, Fars reported.

- Iran began a new round of missile attacks against Israeli positions, according to SNN.

- Yemeni Houthi spokesperson claims a joint attack with Hezbollah against Israel, said the escalations will only drive Yemen “to further escalation in the coming period until the aggression stops and the blockade is lifted”.

- Daily Mail columnist Andrew Neil posted “I am told by White House sources that Trump is seriously considering taking Kharg Island”.

- Iran began a new round of missile attacks against Israeli positions, according to SNN.

- Iranian drone reportedly strikes US Victoria base in Baghdad, according to Fars news agency.

- Israeli military identified launch of missile from Yemen towards Israel.

- US and Israel attacked weather facilities of Bushehr again, via ISNA.

- Reports of a drone attack on an oil field in the “Chamanke” region, located in the north of Dohuk province in Iraqi Kurdistan; attack caused a fire in this oil field. The field is managed by an American company, Fars News reported.

- Reports of explosions in Saudi Arabia; reporting in proximity to Saudi announcing the interception of two drones in the last few hours.

- Qatari Defence said a cruise missile struck an oil tanker chartered for QatarEnergy in the economic waters, Al Arabiya reported.

- United Arab Emirates is preparing to help the US and other allies open the Strait of Hormuz by force, according to WSJ.

- Powerful explosion rocks American base in Erbil, according to Press TV.

- Iran’s Mobarakeh steel plant hit in US-Israel strike and Khuzestan steel plant also targeted, Mehr News reported.

- UK PM Starmer reaffirmed that the war in the Middle East is not our war and will not be dragged into the conflict. Exploring every diplomatic avenue to reopen Hormuz.

- Russia’s Deputy Foreign Minister Galuzin told TASS that talks on Ukraine are on pause.

US Event Calendar

- 9:00 am: United States Jan FHFA House Price Index MoM, est. 0.1%, prior 0.1%

- 9:45 am: United States Mar MNI Chicago PMI, est. 55, prior 57.7

- 10:00 am: United States Mar Conf. Board Consumer Confidence, est. 87.9, prior 91.2

- 10:00 am: United States Feb JOLTS Job Openings, est. 6890k, prior 6946k

- 12:00 pm: United States Fed’s Goolsbee Gives Opening Remarks at Eco Mobility Project

- 1:10 pm: United States Fed’s Schmid Speaks on Monetary Policy and Economic Outlook

- 3:00 pm: United States Fed’s Barr Discusses Stablecoin Regulation

- 5:10 pm: United States Fed’s Bowman Speaks on Small Business

DB’s Jim Reid concludes the overnight wrap

What had been a torrid month of March for markets ended on a positive note yesterday, as the S&P 500 (+2.91%) posted its best day since last May as comments by US and Iranian officials drove hopes that an end to the Iran war could be coming closer into view. The increased optimism boosted a variety of asset classes including credit (-18bps for US HY spreads) and gold (+3.48%). Oil markets themselves saw more modest relief given still very uncertain prospects for the Strait of Hormuz, with Brent crude falling -3.18% yesterday but trading +1.36% higher at $105.21/bbl this morning. Meanwhile, US officials have joined in suggesting that the US may look for an offramp before long, with Secretary of State Rubio saying last night that the US “can see the finish line” on Iran objectives. And the White House posted last night that Trump will address the nation at 9pm EST today “to provide an important update on Iran”. S&P 500 futures (+0.20%) have solidified yesterday’s gains, while those on the Europe’s STOXX 50 (+1.80%) are catching up to yesterday’s US rally, having risen by a more modest +0.50% yesterday.

The biggest trigger for yesterday’s rally came shortly after the European close as Iran’s state news agency reported Iranian President Pezeshkian saying that Iran is willing to end the war but only if there are guarantees “to prevent the recurrence of aggression”. While it wasn’t clear if these comments represented a material change in Iran’s position – indeed, in large part they reiterated demands floated by Tehran last week – they helped drive an extension of the rally that emerged amid signals that the US may be looking for offramps out of the war.

The latest US comments then saw Trump say last night that he foresees ending the war “within two weeks, maybe three” and that while a deal with Iran was possible, such an agreement was not necessary for the US to end the conflict. Trump also suggested that “we’re not going to have anything to do with” what happens in the Strait of Hormuz, adding to a cacophony of signals that the US did not see reopening Hormuz as necessary to end the war. These ranged from the WSJ report we mentioned yesterday morning to Trump’s post earlier yesterday that countries who are reliant on energy from the Gulf should “go to the Strait and just TAKE IT” as well as his comments to the New York Post that the waterway would open “automatically” after the US leaves.

Oil prices moved lower following the Pezeshkian comments but are a little higher again this morning. WTI crude in particular saw modest moves in aggregate, down -1.46% yesterday to $101.38/bbl, after almost reaching $107/bbl in Asia trading yesterday, but edging back up to $103.19/bbl this morning as Trump’s comments overnight left plenty of uncertainty over Hormuz, especially if there isn’t a negotiated settlement. When it comes to talks, Iran’s Foreign Minister told Aljazeera yesterday that while there has been an exchange of messages with the US, these were not “negotiations”.

By contrast, US equities delivered a stunning rebound as the S&P 500 rose by +2.91%, its best day since May 12 last year, the day that US and China agreed to defuse their post-Liberation Day tariff escalation. The NASDAQ (+3.83%) and the Mag-7 (+4.48%) outperformed as tech stocks led the gains, while the S&P 500 airlines sector rebounded by +5.77%. The rally was also a broad one, with 421 advancers in the S&P 500, the most year-to-date, while the VIX index (-5.36pts to 25.25) saw its biggest daily decline since last April.

The positive mood has fed into Asian hours overnight, with key Asia indices also rebounding strongly. The KOSPI (+7.73%) is leading the way, also boosted by strong export data, while the Nikkei is up +4.58%. The Hang Seng (+1.97%), CSI (+1.43%), Shanghai Composite (+1.36%) and the S&P/ASX 200 +1.90% are also visibly higher.

The risk-on mood has also been visible across other asset classes, with US HY credit spreads tightening by -18bps yesterday, also their best day since last May’s US-China trade truce. Elsewhere, gold rose +3.48% to $4,668/oz in its best day since early February, while the dollar index fell -0.55% and is another -0.17% overnight.

In the rates space, Treasuries extended Monday’s rally, with the 2yr yield down -3.4bps to 3.80% and the 10yr down -3.1bps to 4.32%. 10yr yields are another -2.7bps lower overnight, which leaves them almost 20bps down from their 4.48% intra-day peak on Friday. Meanwhile, this morning in Asia, 10yr JGBs are -2.8bps lower at 2.32%.

European bonds also rallied yesterday, with yields on 10yr bunds down -3.0bps to 3.00%, while OATs (-4.5bps) and BTPs (-7.6bps) outperformed amid the risk on moves. The bond rally was also aided by the March euro area HICP print which saw both headline (+2.5% yoy) core inflation (+2.3%) come in a tenth below consensus. Gilts were a relative underperformer, with 10yr yields down a modest -1.7bps as the final Q4 GDP release saw 2025 real GDP growth revised up from +1.3% to +1.4%.

Yesterday’s cross-asset rally came at the end of what has been a pretty torrid month and quarter for markets, as you can see in our regular performance review that Henry will be publishing shortly. Clearly the Iran conflict dominated the agenda, with Q1 seeing the biggest quarterly rise in Brent crude oil since Q3 1990 when the Gulf War began. It also triggered a major cross-asset selloff, and March saw Europe’s STOXX 50 post its biggest monthly decline since the first Covid lockdowns in March 2020, whilst 10yr Treasury yields had their biggest monthly jump since December 2024. So nearly all the major assets struggled, and there were plenty of other stories to look out for too. In fact, the software component of the S&P 500 saw its biggest quarterly decline since the height of the GFC in 2008, whilst March saw gold’s biggest monthly decline since 2008 as well. See the full review in your inboxes shortly.

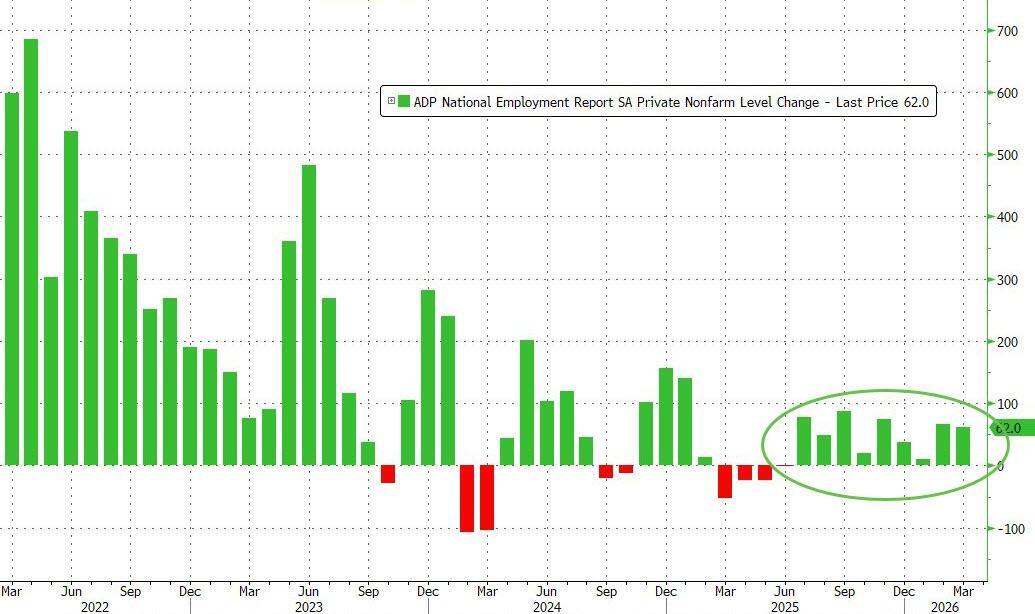

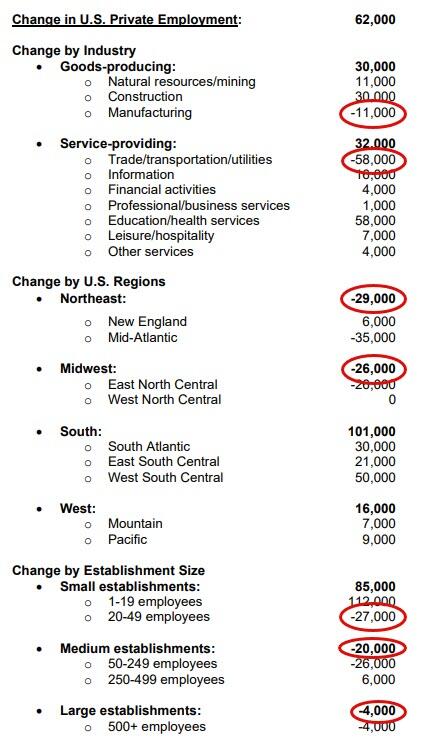

Recapping yesterday’s other news, we saw mixed data out of the US. On the positive side, the Conference Board consumer confidence unexpectedly improved in in March to 91.8 (versus 91.0 previous, 87.9 expected). So US consumer sentiment is proving relatively resilient in the face of the Iran shock, even if the expectations series did deteriorate from 72.6 to 70.9 (vs. 68.4 expected). However, the February JOLTS employment survey was on the softer side, with job openings largely in line with expectations but the quits rate edging down from 2.0% to 1.9% and layoffs rising to a 4-month high of 1,721k (vs 1,668k expected).

Turning to the data out of Asia this morning, in China the RatingDog manufacturing PMI came in at 50.8 in March, down from 52.1 in February and below the expected 51.6. Rising oil prices contributed to increased cost pressures, dragging from the strong momentum in February. Meanwhile in Japan, the BoJ’s Tankan survey improved for a fourth consecutive quarter, with sentiment among large manufacturers rising to +17 from +16 in December. Companies are also signaling a larger-than-expected increase in capital expenditure though they are more cautious about the future.

Finally, turning to the day ahead, the final manufacturing PMIs for March will be the highlight on the data side. In the US, we’ll also have the latest weekly ADP employment figures and the February retail sales data. Among central banks, the Fed’s Musalem and Barr and ECB’s Cipollone are due to speak.