Authored by Lance Roberts via RealInvestmentAdvice.com,

Just recently, a report was released discussing why you should NOT try and time the market, but rather “just stay invested for the long-haul.” To wit:

“Periods of high volatility and occasional bouts of uncertainty are a part of the investing process. When markets correct, you can’t control their length or severity, but you CAN control how you respond. The temptation is to exit the market entirely and sit on the sidelines waiting for the ‘right’ time to re-enter and re-invest. We believe that unfortunately, for the typical investor, this is not a prudent investment strategy. Why? Because we are not aware of anyone who can successfully time the market on a consistent basis and the consequences of missing just a few of the best days in the market can really put a dent in your long-term returns.”

The report then continues:

“Additionally, bear markets have tended to be short-lived while bull markets have been longer, stronger and more powerful creating a net positive for the long-term investor vs the ‘buy low, sell high’ investor.”

Unfortunately, the entirety of the analysis is based on faulty, mainstream, assumptions.

The “Math” Problem

For years, the investment industry has tried to scare clients into staying fully invested in the stock market at all times, no matter how high stocks go or what’s going on in the economy. The warnings are always the same:

“You can’t time the market.”

“Studies show that market timing doesn’t work.”

Of course, the reasoning for promoting “buy and hold” investing is not necessarily for “your benefit,” but generally for those wishing to extract a “fee” for their services.

But let’s get right to the “math” of it.

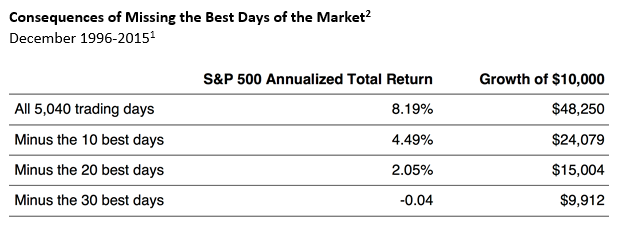

Is it true that over the long-term investors made most of their money from just a handful of big one-day gains? In other words, if you missed any of those days, your return would be “bupkis.” Obviously, since no one can predict when those few, big jumps are going to occur, it’s best to stay fully invested at all times, right? So just give them your money and bask in the warm blow of the “efficient market hypothesis.”

But, that’s entirely wrong. What it doesn’t address is the other half of the equation which makes the real difference to whether you should invest, when and how.”

While it is true, that missing out on the 10-best days did reduce your gains, missing out on the 10-WORST days was far more lucrative.

Clearly, avoiding major drawdowns in the market is the key to long-term investment success. Given that markets spend roughly 95% of their time making up previous losses, avoiding major drawdowns leads to a greater probability of reaching long-term goals.

As Brett Arends once stated:

“The cost of being in the market just before a crash is at least as great as being out of the market just before a big jump and may be greater. Funny how the finance industry doesn’t bother to tell you that.”

The reason that the finance industry doesn’t tell you the other half of the story is because it is NOT PROFITABLE for them. The finance industry makes money when you are invested – not when you are in cash. Therefore, it is of no benefit to Wall Street to advise you to move to cash.

The Percentage Problem

If the “math problem” wasn’t bad enough, the author then climbs right into the “percentage problem” in the second chart trying to prove his point yet again.

Unfortunately, this is also incorrect.

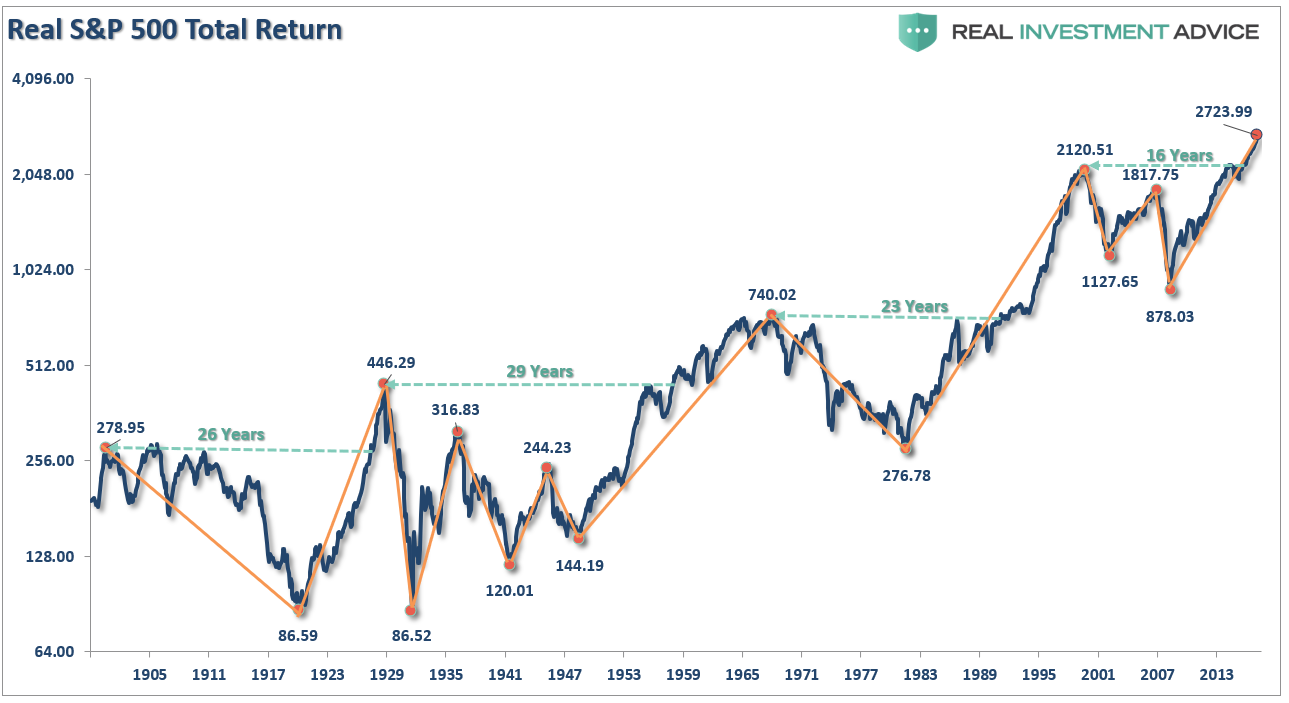

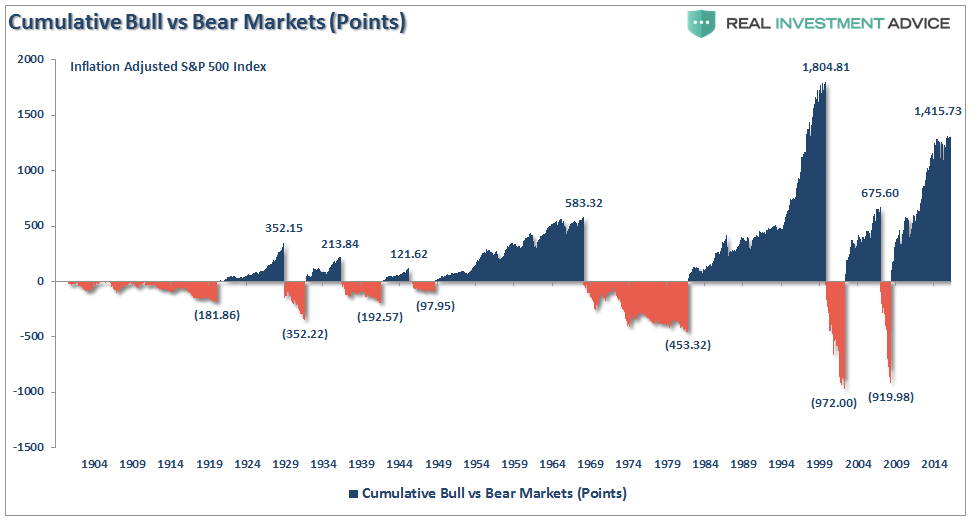

Since the chart above was nominal, I have rebuilt the analysis presented above using inflation-adjusted total returns using Dr. Robert Shiller’s monthly data. The chart shows the S&P 500 from 1900 to present and I have drawn my measurement lines for the bull and bear market periods. Also, notice the very long periods before the markets make “new highs.”

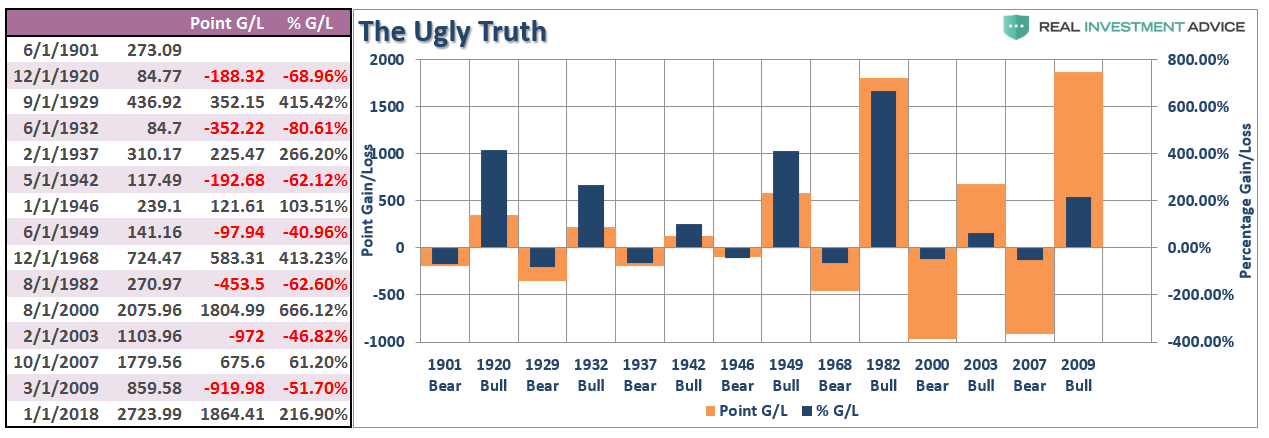

The table below is the most critical. The table shows the actual point gain and point loss for each period. As you will note, there are periods when the entire previous point gains have been either entirely, or almost entirely, destroyed.

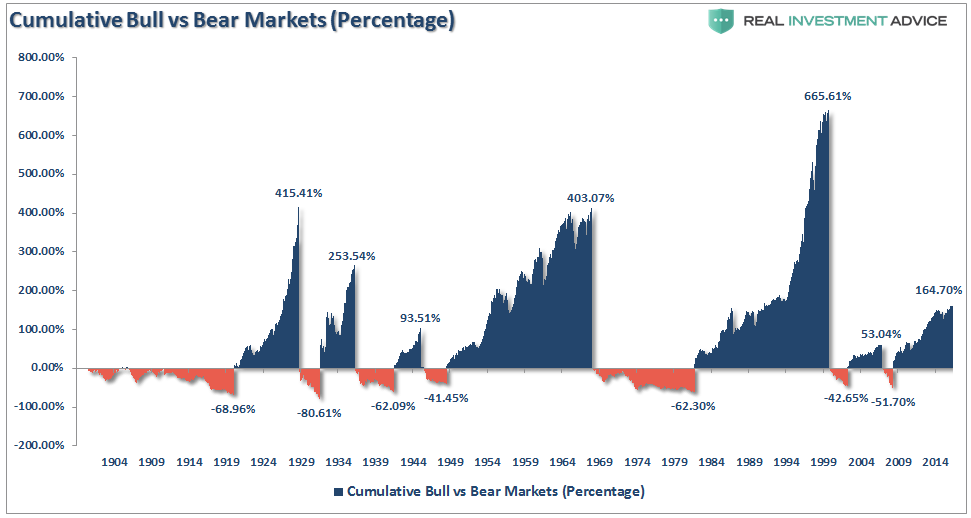

The next two charts are a rebuild of the first chart above in both percentage and point movements.

Again, even on an inflation-adjusted, total return, basis when viewing the bull/bear periods in terms of percentage gains and losses, it would seem as if bear markets were not worth worrying about.

However, when reconstructed on a point gain/loss basis, the ugly truth is revealed.

Percentages are very deceiving especially when you start talking about very large numbers. However, when it comes to your money, it is about how many points are lost which is critically more important.

So, what’s the solution?

No, You Can’t Time The Market

I do agree with the statement above that you “can’t time the market.” Importantly, I do not endorse “market timing” which is specifically being “all in” or “all out” of the market at any given time.

The problem with “market timing” is consistency.

But answer this question:

Why are there are no great investors of our time that “buy and hold” investments?

Because all great investors manage risk.

Having a methodology to “buy” and “sell” investments is the core of investing, hence the very basic rule of investing which is to “buy low and sell high.”

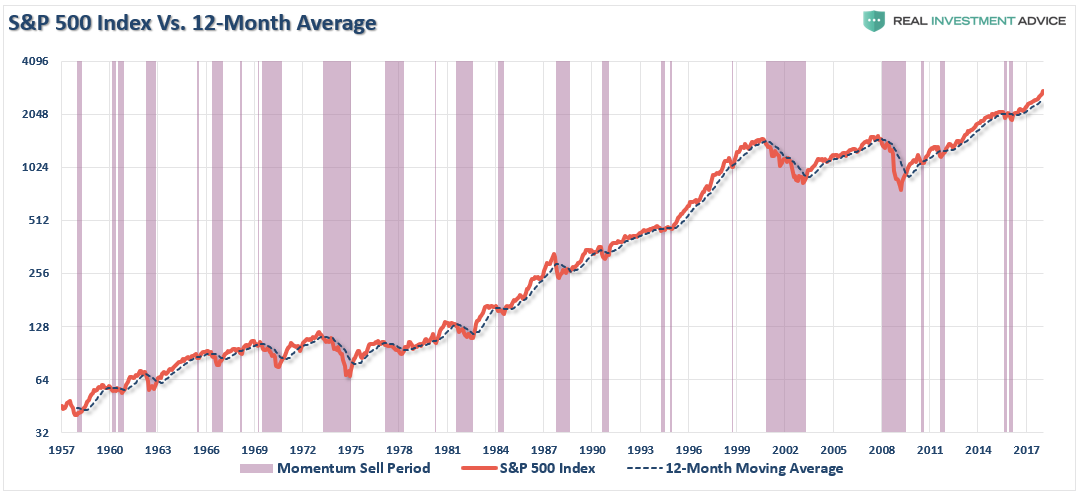

While there are many sophisticated methods of handling risk within a portfolio, even using a basic method of price analysis, such as a moving average, can be a valuable tool over the long-term holding periods. Will such a method ALWAYS be right? Absolutely not. However, will such a method keep you from losing large amounts of capital? Absolutely.

The chart below shows a simple 12-month moving average study. What becomes clear is that using a basic form of price analysis can provide useful identification of periods when portfolio risk should be REDUCED. Importantly, I did not say risk should be eliminated; just reduced.

Again, I am not implying, suggesting or stating that such signals mean going 100% to cash. What I am suggesting is that when “sell signals” are given that is the time when individuals should perform some basic portfolio risk management such as:

- Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

By using some measures, fundamental or technical, to reduce portfolio risk by taking profits as prices/valuations rise, or vice versa, the long-term results of avoiding periods of severe capital loss will outweigh missed short-term gains. Small adjustments can have a significant impact over the long run.

Buy & Hold Won’t Get You There

If you just “buy and hold” and “dollar cost average” you will make money over the long-term.

This is a true statement.

It will just leave you very short of your required investment goals.

Let me give you an example of what I mean.

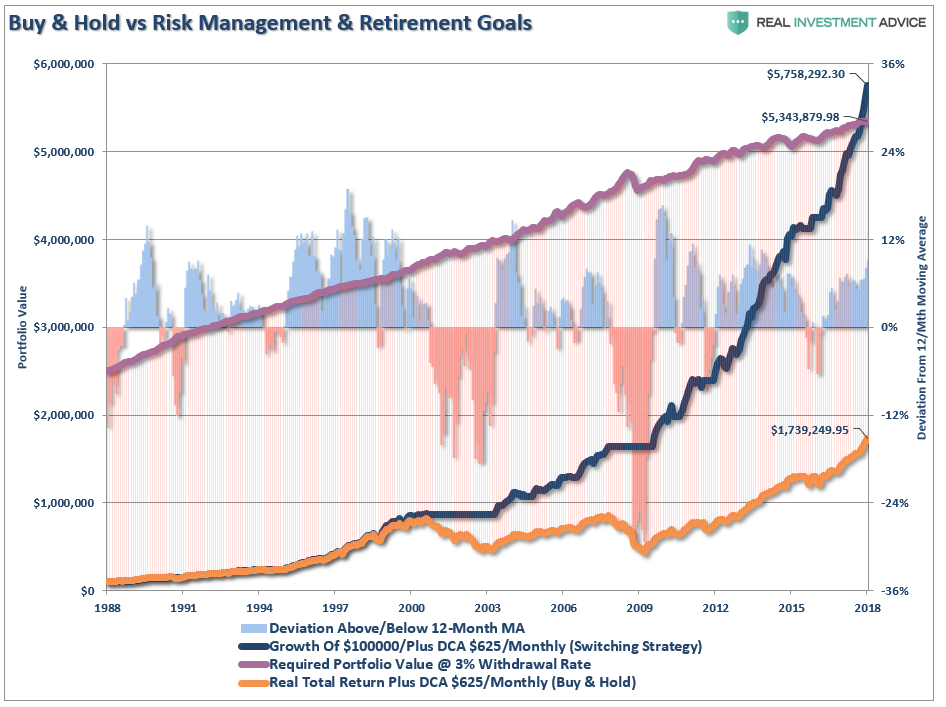

In 1988, Bob was 35 years old, had saved up a $100,000 nest egg and decided to invest it in the S&P 500 index. He added $625/month to the index every month and never touched it. When Bob retires at 65, he wants to maintain his current $75,000 lifestyle. We will assume he can generate 3% a year in retirement on his nest egg.

The chart below shows the difference between two identical accounts. Each started at $100,000, each had $625/month in additions and both were adjusted for inflation and total returns. The purple line shows the amount of money required, inflation-adjusted, to provide a $75,000 per year income to Bob at a 3% yield. The only difference between the two accounts is that one went to “cash” when the S&P 500 broke the 12-month moving average in order to avoid major losses of capital.

There is a clear advantage to providing risk management to portfolios over time. The problem, as I have discussed many times previously, is that most individuals cannot manage their own money because of “short-termism.”

Despite their inherent belief that they are long-term investors, they are consistently swept up in the short-term movements of the market. Of course, with the media and Wall Street pushing the “you are missing it” mantra as the market rises – who can really blame the average investor “panic” buying market tops and selling out at market bottoms.

Yet, even after two major bear market declines, it never ceases to amaze me that investors still believe that somehow they can invest in a portfolio that will capture all of the upside of the market but will protect them from the losses. Despite being a totally unrealistic objective this “fantasy” leads to excessive risk-taking in portfolios which ultimately leads to catastrophic losses. Aligning expectations with reality is the key to building a successful portfolio. Implementing a strong investment discipline, and applying risk management, is what leads to the achievement of those expectations.

Planning To Win

Many individuals have been led believe that investing in the financial markets is their only option for retiring. Unfortunately, they have fallen into the same trap as most pension funds which is believing market performance will make up for a “savings” shortfall.

With valuations elevated, the economic cycle very long in the tooth, and the 3-D’s (debt, demographics, and deflation) applying downward pressure to future economic growth rates, investors need to consider the following carefully.

- Expectations for future returns and withdrawal rates should be downwardly adjusted.

- The potential for front-loaded returns going forward is unlikely.

- The impact of taxation must be considered in the planned withdrawal rate.

- Future inflation expectations must be carefully considered.

- Drawdowns from portfolios during declining market environments accelerate the principal bleed. Plans should be made during rising market years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

- The yield chase over the last 8-years, and low interest rate environment, has created an extremely risky environment for retirement income planning. Caution is advised.

- Expectations for compounded annual rates of returns should be dismissed in lieu of plans for variable rates of future returns.

Chasing an arbitrary index that is 100% invested in the equity market requires you to take on far more risk that you most likely want. Two massive bear markets over the last decade have left many individuals further away from retirement than they ever imagined. Furthermore, all investors lost something far more valuable than money – the TIME that was needed to reach their retirement goals.

Investing for retirement, no matter what age you are, should be done conservatively and cautiously with the goal of outpacing inflation over time. This doesn’t mean that you should never invest in the stock market, it just means that your portfolio should be constructed to deliver a rate of return sufficient to meet your long-term goals with as little risk as possible.

It should be clear that market corrections are indeed very bad for your portfolio in the long run. However, before sticking your head in the sand, and ignoring market risk based on an article touting “long-term investing always wins,” ask yourself who really benefits?

This outcome this time will not be “different,” so isn’t it worth considering a different approach?

via RSS http://ift.tt/2nusKn4 Tyler Durden