Authored by 720Global's Michael Lebowitz via RealInvestmentAdvice.com,

The Federal Reserve raised the Federal Funds rate on December 13, 2017, marking the fifth increase over the last two years. Even with interest rates remaining at historically low levels, the Fed’s actions are resulting in greater interest expense for short-term and floating rate borrowers. The effect of this was evident in last week’s Producer Price Inflation (PPI) report from the Bureau of Labor Statistics (BLS). Within the report was the following commentary:

“About half of the November rise in the index for final demand services can be traced to prices for loan services (partial), which increased 3.1 percent.”

While there are many ways in which higher interest rates affect economic activity, the focus of this article is the effect on the consumer. With personal consumption representing about 70% of economic activity, higher interest rates can be a cost or a benefit depending on whether you are a borrower or a saver. For borrowers, as the interest expense of new and existing loans rises, some consumption is typically sacrificed as a higher percentage of budgets are allocated to meeting interest expense. On the flip side, for those with savings, higher interest rates generate more wealth and thus provide a marginal boost to consumption as they have more money to spend.

This article focuses on borrowers and savers to show how the current interest rate cycle is squeezing consumers. Said differently, the rising cost of borrowing is dwarfing the benefit of saving.

Borrowers

As mentioned but worth repeating, personal consumption accounts for the bulk of economic activity. To gauge how higher interest rates might affect individuals’ spending, we classify personal debt into the following five categories: mortgages, home equity lines, auto loans, student loans and credit card debt. The following table shows the amount of debt outstanding in each category and estimates the percentage of each loan type that has fixed interest rates and floating interest rates.

Distinguishing between fixed and floating interest rates is important, as borrowers using fixed-rate loans are largely unaffected by higher interest rates. Accordingly, we focus this analysis on floating rate debt as those borrowers and consumers will see immediate increases in their interest expenses every time the Fed raises rates.

Based on the table, approximately $2.8 trillion of consumer loans outstanding are floating rate. We calculate that every 25 basis point (0.25%) interest rate hike by the Fed will increase interest expense higher by $7 billion annually for these consumers. Since December 2015, when the Fed began to hike interest rates, the Fed Funds rate and other interest rates to which consumer debt is frequently indexed are about 125 basis points higher. Thus on an annual basis, the additional cost of borrowing is approximately $35 billion. Looking forward, if the Fed raises rates three times in 2018 as they currently forecast, the annual interest expense will increase by another $21 billion to bring the total to $56 billion per year.

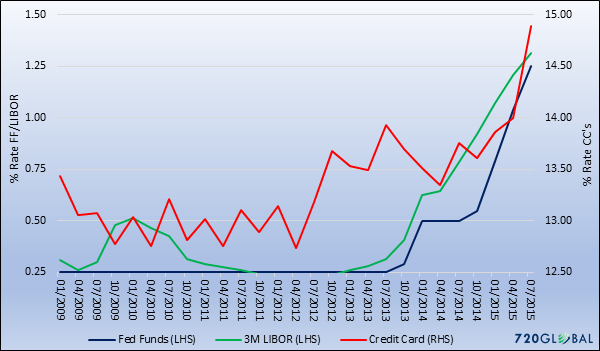

The graph below charts Fed Funds, 3-month LIBOR, and average credit card rates to show the nearly perfect correlation between Fed actions and short-term borrowing rates. 3-month LIBOR is the index most frequently used to determine floating rate interest rates.

Data Courtesy: St. Louis Federal Reserve (FRED)

Savers

To do a complete analysis of the effect of higher rates on consumption, we must look beyond the increased interest costs, as quantified above, and also consider the benefits of higher interest rates to savers. According to the Fed, personal savings equals $471 billion. The increase in interest rates should reward savers, which will help offset the economic burden related to the increase in interest expense.

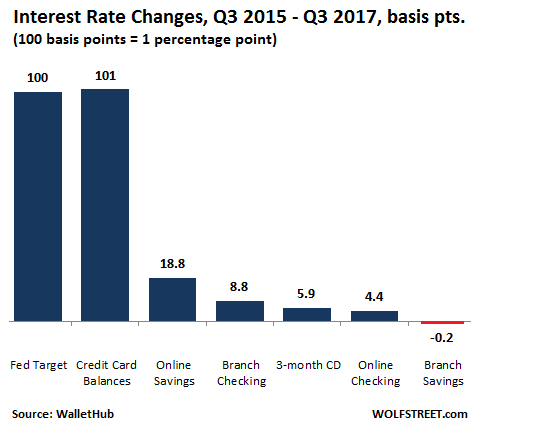

Interestingly, what should happen and what has happened are two different stories. The truth of the situation is that individual savers have barely benefited from higher rates as banks and financial intermediaries are not passing on higher rates to savers. The chart below provided by WalletHub and Wolfstreet.com compares the change in the Fed funds rates and credit card interest rates to instruments of savings. Please note the table does not include the most recent increase in rates on December 13, 2017.

To confirm the data in the chart, we searched for other sources of savings rate data. Data from the FDIC reports that bank savings rates, 3-month CD’s, money market accounts and interest checking rates have increased by 0, 3, 1, and 0 basis points respectively since the Fed began raising rates two years ago.

Based on the graph and the data above, it is fair to say that borrowers have benefited by less than ten basis points (0.10%) on average despite 125 basis points (1.25%) of interest rate increases. Based on total savings of $471 billion, we can approximate the benefit to borrowers is a mere $600 million.

Summary

Consumers are being squeezed. Debt linked to short-term interest rates is rising lockstep with the Federal Funds rate while savings rates remain stubbornly low. While the dollar amounts are not massive, the transmission mechanism of the Fed’s rate hikes is acting like a tightening vice that will result in less consumption and slower economic growth.

One of the key takeaways from the Fed’s action during and following the financial crisis of 2008 has been a prolonged and intentional effort aimed at crushing savers. Near zero percent savings rates is part of the Fed’s strategy to incentive savers to move out of the security of cash and invest in riskier assets and/or consume. Even today, despite the rise in interest rates, banks accept the benefits of higher rates imposed on borrowers while refusing to adjust rates for savers. As one of the primary regulators of the financial system, the Fed could encourage a change in that behavior, but to date, no such influence has even been mentioned. Interestingly, the savings rates that banks earn on deposits at the Fed has increased lockstep with Fed Funds.

After nearly a decade of imposing its unique brand of price controls over the cost of money, the Fed admittedly is not willing to do that which is in the best interest of the general public and continues to adhere to policies that favor their primary constituents, the big banks and major corporations.

via http://ift.tt/2CbtOCp Tyler Durden