The Fatal Flaw In A Perfect Energy Solution

Authored by Irina Slav via OilPrice.com,

More than thirty years ago a giant tower was built in Manzanares, Spain, to produce electricity in a way that at the time must have seen even more eccentric than it seems now, by harnessing the power of air movement. The Manzanares tower was, sadly, toppled by a storm. Decades ago, several other firms tried to replicate the idea, but none has succeeded. Why?

A simple idea

The idea behind the so-called solar wind towers is pretty straightforward. The more popular version is the solar updraft tower, which works as follows:

On the ground, around the hollow tower, there is a solar energy collector—a transparent surface suspended a little above ground—which heats the air underneath.

As the air heats up, it is drawn into the tower, also called a solar chimney, since hot air is lighter than cold air. It enters the tower and moves up it to escape through the top. In the process, it activates a number of wind turbines located around the base of the tower. The main benefit over other renewable technologies? Doing away with the intermittency of PV solar, since the air beneath the collector could stay hot even when the sun is not shining.

A more recent take on solar wind towers involved water as well. Dubbed the Solar Wind Downdraft Tower, this project first made headlines in 2014, but since then there have been few updates, and those have been far between. The latest was from last year, when the company behind it, Solar Wind Energy Tower, announced a letter of intent by an investment company to provide financing for the project. That financing was to come from investors that the company was yet to find.

Here’s how the company describes the power generation process in the downdraft tower:

“To start, a series of pumps deliver water to the Tower’s injection system at the top where a fine mist is cast across the entire opening. The water introduced by the injection system then evaporates and is absorbed by hot dry air which has been heated by the solar rays of the sun.

As a result, the air becomes cooler, denser and heavier than the outside warmer air, and falls through the cylinder at speeds up to and in excess of 50 mph. This air is then diverted into wind tunnels surrounding the base of the Tower where turbines inside the tunnels power generators to produce electricity.”

The tough reality

There is normally one reason why otherwise promising—at least on the face of it—technologies never take off: cost. One solar tower executive said as much to National Geographic in 2014.

“The capital costs are very high,” said Rudolf Bergermann, who is co-founder of Schlaich-Bergermann and Partner, a company specializing in updraft solar tower technology. In a paper on its project, SBP admitted that costs of solar towers are high, but said the electricity that they generate is cheaper than all comparable solar technology.

The company also wrote, “However, the approaching shortfall of fuel reserves in combination with dramatically increasing demand will soon balance the cost difference of today and later even reverse it. We expect this ‘break-even-point’ already at a value of 60 to 80 $/barrel of crude oil.”

Brent is currently trading around $60 a barrel today, but there is no news of solar towers getting built on any scale. Investors are still wary of pouring money into a concept that has not been proved despite the promising theory behind it. That’s especially true of the downdraft tower: it sounds like it will need to use substantial amounts of water and the company is not saying where this water will come from and how much it will add to the cost of the whole thing.

Challenging the dominant tech

The way things stand now in renewable energy, solar wind towers may never become part of the global energy mix. While the electricity they could generate may indeed be cheaper than comparable technology, the upfront costs and the stability problems related to the height of the tower, which is in direct proportion to its efficiency, are enough to doom this technology. But the final nails come from the competition.

Solar and wind energy research has achieved impressive production cost reductions in the past decades when the technology has moved from an interesting alternative to power plants to a mainstream source of energy.

Solar panels are today a lot cheaper than they were just fie years ago, and costs continue to fall. These will doubtlessly reach a bottom at some point, before low cost begins to compromise quality, but the cheaper PV tech becomes, the less competitive their alternatives get.

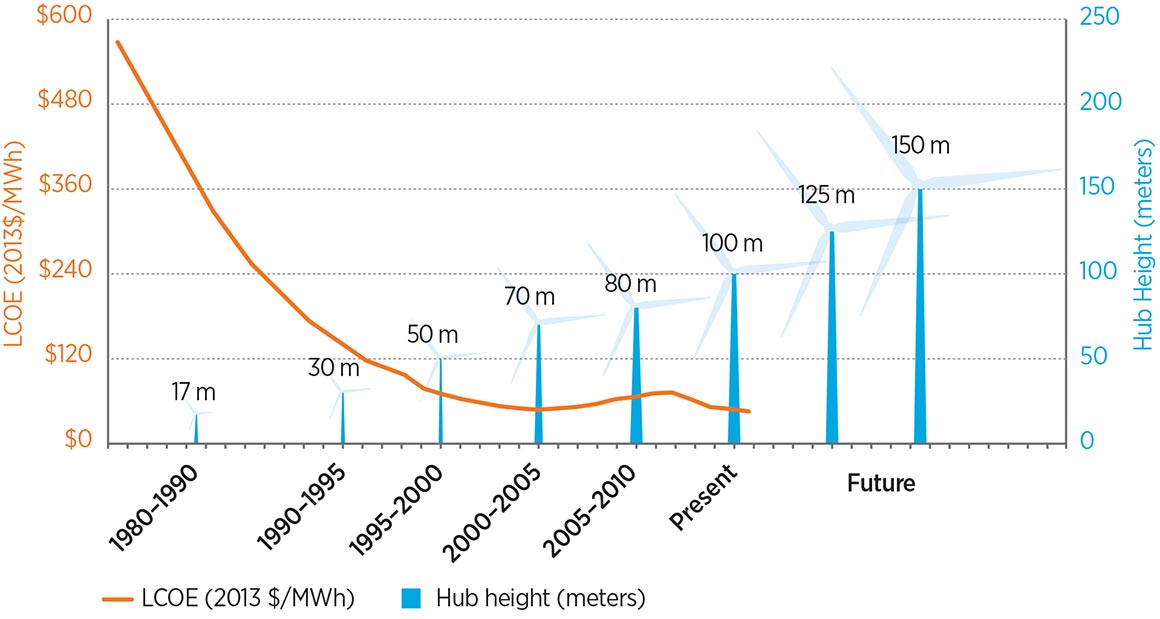

Wind energy is also getting cheaper as towers become taller and turbines become more efficient at no additional cost.

“Wind now supplies clean and efficient power to the equivalent of 32 million American homes, sustains 500 U.S. factories, and delivers more than one billion dollars a year in new revenue to rural communities and states,” the American Wind Energy Association said last month in a report that revealed the United States had more than 100 GW in wind capacity, most of it onshore.

The creators of the solar wind downdraft tower compare their facility in terms of cost with a nuclear power plant. However, what they should compare it to are solar installations and wind farms. Some of these are already cheaper than fossil fuel-fired power plants. They are the reason such fascinating but expensive technology will likely never make it to the market, not cheap oil and gas.

Tyler Durden

Sat, 11/30/2019 – 18:30

via ZeroHedge News https://ift.tt/2L9fDU2 Tyler Durden

{kind=link}

{kind=link}