Authored by David Stockman via Contra Corner blog,

The dirty secret of Keynesian central banking is that under current circumstances its interventions have almost no impact on its famous dual mandate – stable prices and full employment on main street.

That’s because goods and services inflation is a melded consequence of global central banking. The capital, trade, financial and exchange rate movements which result from the tug-and-haul of worldwide central banking policies generate incessant shape-shifting impacts on the CPI; and the ebb and flow of these forces completely dwarfs FOMC actions in the New York money and bond markets.

In today’s world, there is no such thing as inflation in one country. In that regard, the traditional Fed tool of pegging the funds rate is especially obsolete, impotent and ritualistically mindless. After all, if the 2.00% inflation target is meant as a long haul objective, it was achieved long ago. The CPI index for January 2018 at 249.2 compared to a level of 169.3 back in January 2000, thereby representing exactly a 2.17% compound annual gain over the 18 year period.

So where’s the Eccles Building beef about missing its target from below—even if that wasn’t one of the more ludicrous notions of “failure” ever to arise from the central banking fraternity?

On the other hand, if 2.00% is meant as a short-run target, how much more evidence do we need? Since the Fed shifted to deep pegging at or near the zero bound in December 2008, there has been no inflation rate correlation with the funds rate whatsoever.

In the sections below we will resolve the inflation matter once and for all by demonstrating that the very idea of 2.00% inflation targeting (or any other target) is singularly stupid and destructive. What the free market/sound money doctor actually calls for is just the opposite: That is, consistent, secular deflation so that domestic prices, wages and costs—which are perched near the top of global cost curves—-can be brought into better competitive alignment.

By the same token, the full employment objective is equally vestigial. That’s because the channels of monetary policy transmission to the real main street economy are broken and done.

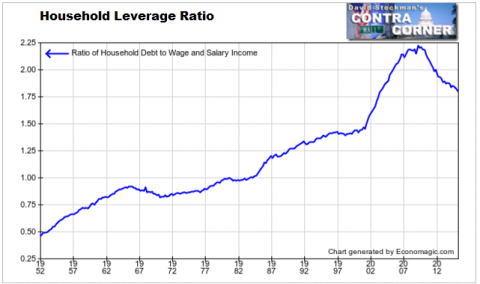

With households at Peak Debt, cheap interest rates do not stimulate incremental borrowing and consumption spending: Households have been left with only their paychecks to spend, and what remaining raining day funds (savings) they have not already tapped.

The current levels and risk spreads on unsecured personal loans, in fact, show exactly why the credit channel to households is frozen solid.

With more than $15 trillion of total household debt and other liabilities, it is now all about credit risk. Even in the case of the very highest credit scores, unsecured personal loan interest rates are essentially prohibitive and are designed to recover huge, predictable losses for dodgy credits, not stimulate a tsunami of new consumer borrowing and spending.

The (unsecured) personal loan rates quoted below are more or less in line with the current average APR on credit cards, which stands at 16.15%.

Excellent Scores (720-850)……………………10.5%-12.5%

Good Scores (680-719)………………………….13.5%-15.5%

Average Scores (640-679)…………………….. 17.8%-19.9%

Poor Scores (300-639)…………………………..28.5%-32.0%

The only real categories of household credit still growing are student loans, which are essentially government guaranteed entitlements, not commercial credits; and auto loans, which are collateralized by vehicular rolling stock. The latter, in turn, are kept liquid on a low cost basis by the repo man equipped with sophisticated vehicle tracking and disabling technology.

Growth in auto loans during the current recovery, however, has depended heavily on the inflated value of used cars. The latter became scarce in the years after the 2008 crash, but are already beginning to deflate owing to the soaring supply of off-loan, off-lease vehicles that have been generated by robust new car sales since 2012.

At length, of course, the car loan boom will crumble as used car prices plunge on a cyclical basis. So auto debt will soon join the no growth mortgage market. At that point, the entirety of household collateral will soon be tapped-out, thereby insuring the complete shutdown of the household credit channel of monetary policy transmission.

The fact that virtually every channel of household credit has already been blocked or become highly congested by Peak Debt is self-evident in the household debt data. According to the flow of funds report, household debt doubled between the 2000 peak and mid-2008, growing at a 9.1% annual rate.

By contrast, the growth rate of total household credit from all sources during the last nine years has been just 0.5% per annum

Needless to say, 0.5% per annum does not a consumption spending boom make. Our monetary politburo can declaim until the cows come home about how it “stimulated” the US economy back to full-employment health. But consumption spending growth has been tepid since the pre-crisis peak, and what did occur originated mainly in Say’s Law, not the Eccles Building.

To wit, real consumption spending (PCE) grew at a 1.7% rate between Q4 2007 and Q4 2017, while real wages gained about 1.4% per annum over the period. Clearly production and income came first and was the source of most of the spending gain (as it should in a healthy sustainable economy).

By contrast, real PCE grew at a considerably more robust 2.8% annual rate during the 2000-2007 peak-to-peak cycle compared to just 1.7% for real wages and salaries. This means that upwards of 40% of the gain during the Greenspan mortgage/credit boom was accounted for by borrowing and other unearned sources of spending power.

In any event, the Fed’s ability to supercharge income-based spending by ratcheting up household borrowing and leverage is over and done. Household consumption spending is being mainly driven by earnings and savings drawdown, and the Fed has nothing to do with either.

Indeed, the self-evident deleveraging of household earning since 2008 proves that whatever the Fed stimulated during its $3.7 trillion money printing campaign since the financial crisis, it wasn’t household borrowing and spending.

Moreover, the only other channel of transmission to main street has historically been through business sector CapEx. Yet under the auspices of the Fed’s regime of Bubble Finance, the C-suites of corporate America have morphed into financial engineering joints and have become hand-maidens of Wall Street speculation via stock buybacks, M&A deals and sundry forms of LBOs and leveraged recaps.

So the Fed can’t any longer stimulate investment in productive assets such as plant, equipment and technology, either. And that fact is plain as day from the data on business investment trends.

To wit, your can get output growth from both more productive capacity and from improved efficiencies of tools, equipment and technologies. But before either can happen, capital consumed in current period production must first be replaced.

That is to say, what counts for economic growth is net investment, not gross spending for fixed assets. Of course, the latter is the favorite metric of Keynesians in Washington and on Wall Street alike, but even a cursory review of the stats underscores the error.

Thus, in the year 2000, business capital consumed in current production (depreciation and amortization) totaled $1.016 trillion compared to gross capital spending that year of $1.553 trillion. So the pay dirt metric for net investment amounted to $537 billion.

Fast forward 17 years through the massive eruption of financial engineering in the C-suites and you get $1.98 trillion worth of annual capital consumption and $2.49 trillion of gross capital spending (non-residential in all cases). The math therefore computes to just $510 billion of net investment.

In other words, net business investment today is lower than it was 17 years ago, and that’s before factoring-in the cumulative 35-40% rise in the price level during the interim.

Accordingly, constant dollar net investment has been sharply declining on a trend basis for the entirety of this century. Thus, the 2000 peak level of $525 billion (constant 2009$) slipped by 10% to the 2007 cyclical peak ($473 billion), and by 13% to the 2014 peak ($457 billion) of the present cycle.

In fact, constant dollar net investment of $379 billion in 2016 was 28% below its 2000 level and only slightly ahead of real net investment two decades ag0 during 1997.

Needless to say, this explains why productivity gains and economic growth have been so punk during most of this century to date; and it also puts the kibosh on any notion that Fed policy any longer works through the CapEx channel to the main street economy.

The real message in the chart below is that the US economy has been eating its seed-corn—even as our monetary politburo has been taken bows for prosperity which is not all that, and which it had virtually no role in bringing about.

At the end of the day, the real scandal of central banking is that it takes credit for what it doesn’t cause and can’t achieve in the main street economy, while ignoring the mayhem its machinations bring to the financial system.

In fact, plodding 2% growth during the long stretches between financial crises is what capitalism does on its own; and it would do even better without anti-growth fiscal subsidies and regulatory barriers and especially without the central bank induced channeling of financial capital into speculation and financialization.

By contrast, what central banking does accomplish is the systematic inflation of financial assets. That is, the plenary pegging, manipulating, falsifying and distorting of prices, yield curves, credit spreads and other relationships among financial variables.

So doing, it clobbers, flattens and deforms the delicate clockwork of capitalism embedded in the money and capital markets; it’s putrid fruits are unhinged speculation and destructive financials bubbles on Wall Street and anti-growth barriers on main street.

And that gets us to the folly of 2.00% inflation targeting. The latter, in fact, is about all the monetary central planners have left to justify their heavy intrusions in the financial system.

As we have seen, the idea that the Fed had anything to do with the halting recovery of output growth and employment since the June 2009 bottom rests on pure assertion and ritualistic Keynesian rhetoric: Consumers have not spent up a storm and the true measure of business investment has been heading deeply south.

Nevertheless, consider the contrafactual. Had the Fed stayed out of the fiat credit business during the last several decades, market clearing interest rates would have been dramatically higher. In turn, a regime of market-based debt costs and financial asset prices would have caused the main street economy to evolve in a wholly different manner.

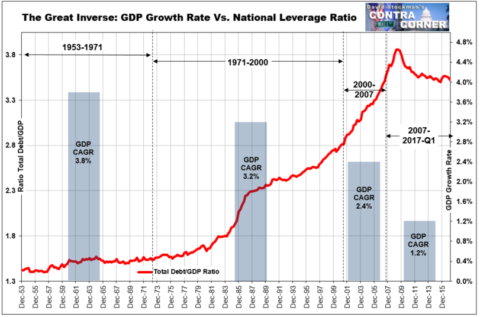

In the first place, there would have been no national LBO and therefore no growth-choking build-up of public and private debt. Yet as is evident in the chart below, the two turns of extra debt imposed on the US economy since the early 1980’s has been accompanied by an unmistakable secular decline in the trend rate of output growth.

Stated differently, had the national leverage ratio remained its it historic 1.5X rather than escalating to today’s 3.5X ratio, there would be about $30 trillion of total debt on the US economy, not today’s $67 trillion.

Absent this $37 trillion incremental debt albatross, we have no trouble believing that the trend growth rate of the US economy would have been a lot higher than the paltry 1.2% rate recorded since 2007.

On the margin, the effect of the above debt explosion was to permit the US economy to spend more than it produced for three decades running. That’s because the other major central banks of the world became infected with the same Keynesian delusions which have been rampant in the Eccles Building since 1987.

Consequently, when the Fed printed, they printed. That is, they bought up dollars on a massive multi-trillion scale owing to the mercantilist belief that their export-based prosperity (in both the Asian industrializing economies and the commodity and petro states) would be imperiled by rising exchange rates.

Alas, these central banks have now accumulated upwards of $7 trillion of UST and GSE debt, which they foolishly swapped for the sweat of their workers’ brows and mother nature’s endowments of natural resources. But it also meant that the US trade account never balanced, and that breadwinner jobs and middle class wages got massively and chronically off-shored.

In this regard, it is important to refute the canard of certain crypto-free marketers, who argue that the balance of trade doesn’t matter, and that foreigners have so much confidence in America that they are gladly swapping their goods and services for US debt paper.

Not a chance!

Under a sound money regime, trade accounts do balance over time due to the automatic discipline of the monetary system. That’s because persistent deficits lead to loss of the settlement assets (gold) to foreign creditors, and a corresponding rise of domestic interest rates and deflation of demand, costs, prices and wages.

At length, imports fall, exports rise, balance returns to trade and current accounts, and national economies cycle forward, but do not permanently bury themselves in debt. By contrast, America’s chronic trade deficits are a product of bad money, not free markets.

As we will demonstrate in Part 5, the above chart would have never materialized under a regime of sound money. Instead of 2% inflation (both targeted and actual for most of the period), the domestic price and cost level would have steadily fallen in response to the flow of cheap labor out of the rice paddies of Asia and cheap energy out of the sands of the Persian Gulf.

Most importantly, the anomaly in the chart below would not have happened. Workers have gotten nominal wage gains of 250% since 1987 (red line) but real earnings (blue line) have been virtually stagnant. The effect was simply to off-shore production and to sacrifice middle class jobs and wage levels to the China Price for goods, the India Price for services and the Technology Price for labor substitution.

That is the ultimate irony of Keynesian central banking. Aiming to solve a non-existent problem of alleged cyclical instability and sub-part growth on main street, it has actually brutalized middle class living standards—even as it has gifted the 1% and the 10% with unspeakable financial windfalls.

via Zero Hedge http://ift.tt/2swtwVu Tyler Durden