Authored by Lance Roberts via RealInvestmentAdvice.com,

In our portfolio management practice, we focus on weekly and monthly data to smooth out daily volatility. Since we are longer-term investors, our focus remains on being invested during rising (bullish) trends and more heavily weighted to fixed income and cash during declining (bearish) trends. Therefore, the only data that really matters to us is where the market closes at the end of each week.

As I stated in this past weekend’s missive:

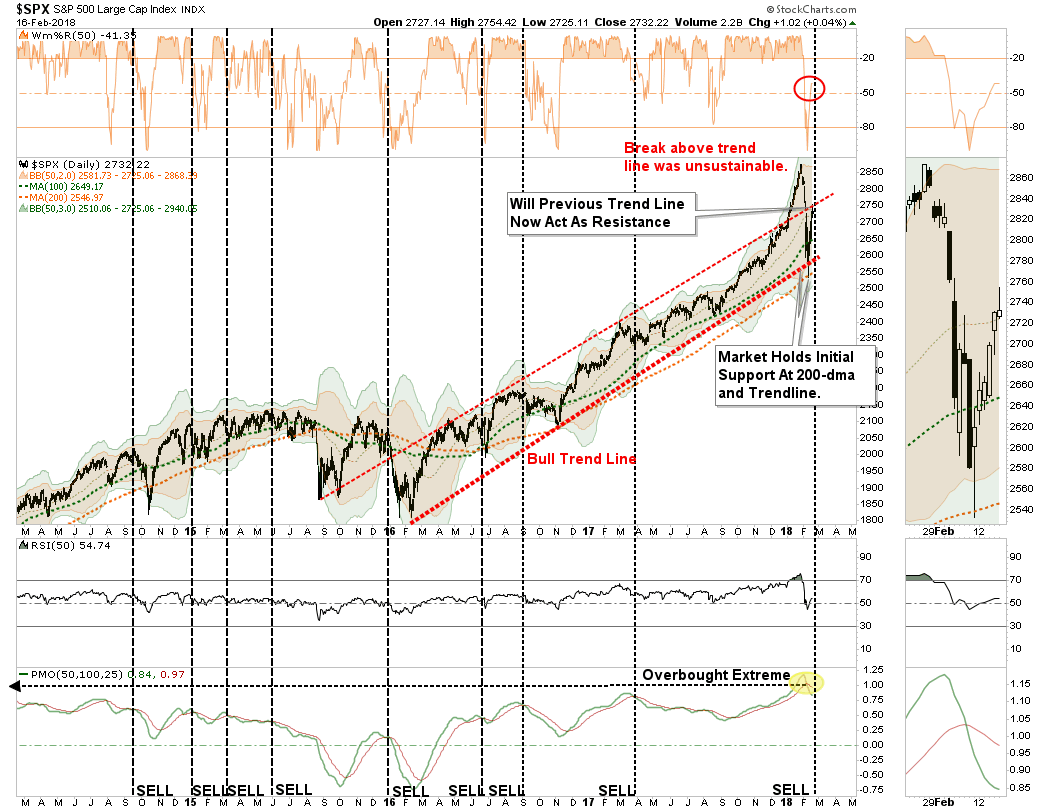

“While the immediate consensus is the ‘bear market of 2018’ is now over, there are several important points about the chart below that should be considered.

- Despite the correction, the market did hold support at the 200-dma

- The bullish trend line, which goes back to the beginning of 2016, has also not been violated.

- However, the upper red “trendline” may provide some overhead resistance temporarily and is worth watching closely.

- While the market did get oversold on a short-term basis, which suggested a bounce was likely, the longer-term overbought condition, and subsequent ‘sell signal’ remain intact.

The bottom line is that while there was much ‘angst’ in the markets last week, the market has not violated any important trend lines that would suggest the current sell-off is anything more than just an ordinary ‘garden variety’ correction.”

This morning, the market opened back below the 50-dma.

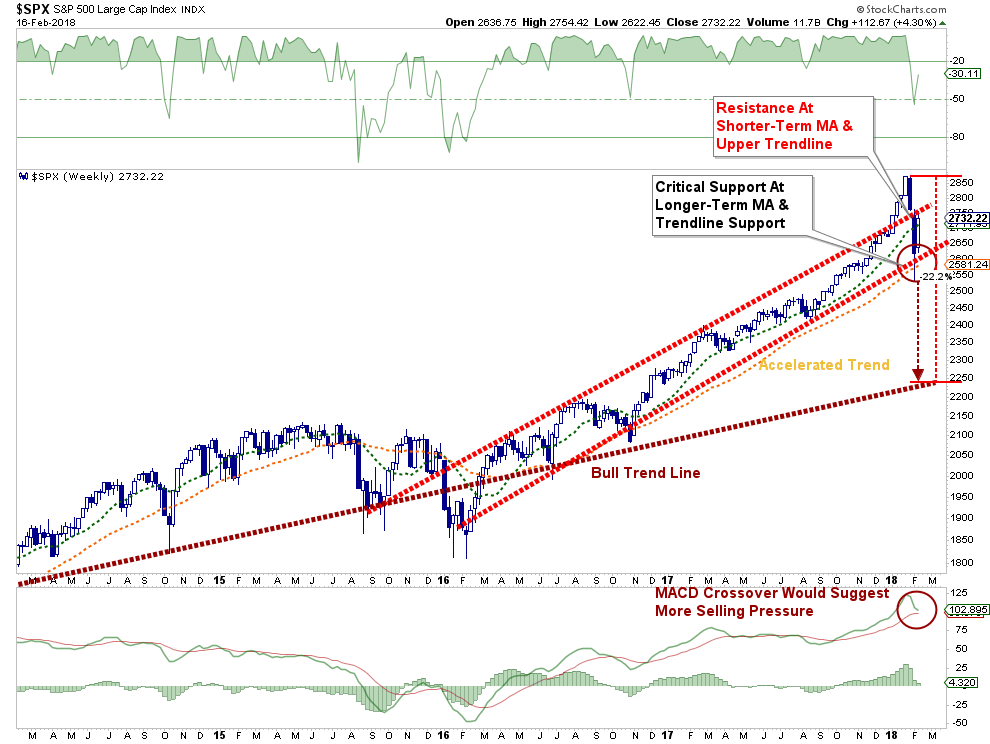

While this is concerning, and keeps our short-hedge in place for now, it is where we finish this trading week that will determine out next positioning changes. The chart below is a weekly view of the S&P 500 index. With much of the volatility stripped away, the important levels for the close of trading on Friday become more evident.

In order for us to fully remove hedges, the market must close above the 50-dma on Friday.

As noted, there is tremendous resistance from the upper trendline of the bullish trend channel that began at the beginning of 2016. We currently expect the market to remain confined to the currently rising bullish trend channel, but there are risks to that view which keeps us cautious.

A failure at resistance which leads to a retracement back to recent lows and the 200-dma is very likely. Here is what we are looking for if that happens.

- If the market holds support at the 200-dma and completes a successful retest, we will begin removing hedges and adding to equity exposure.

- The retracement to the 200-dma will trigger the MACD sell-signal which is already at historically high levels. That “sell signal” will put additional downward pressure on the market.

- As long as the market holds at the rising bullish trend and 200-dma, the bullish backdrop remains intact keeping portfolios weighted towards equity exposure.

- However, if the market breaks below those “critical support” levels, as noted above, the risk of a deeper correction rises. Such a break will lead to increased hedging and a reduction of equity risk in our portfolio models.

- A break of that critical support will likely lead to a retest of the longer-term bullish trend around 2250 which would be a 22% decline from recent highs and an “official bear market.”

- A break below 2250 will likely coincide with the onset of the next recession and is an entirely different portfolio management strategy.

While I have laid out the risks, the bullish trend remains intact. While we are currently hedged, we remain primarily long-biased in our portfolios.

However, don’t completely dismiss the “bearish” case either.

The Bear Still Cometh

Back the newsletter:

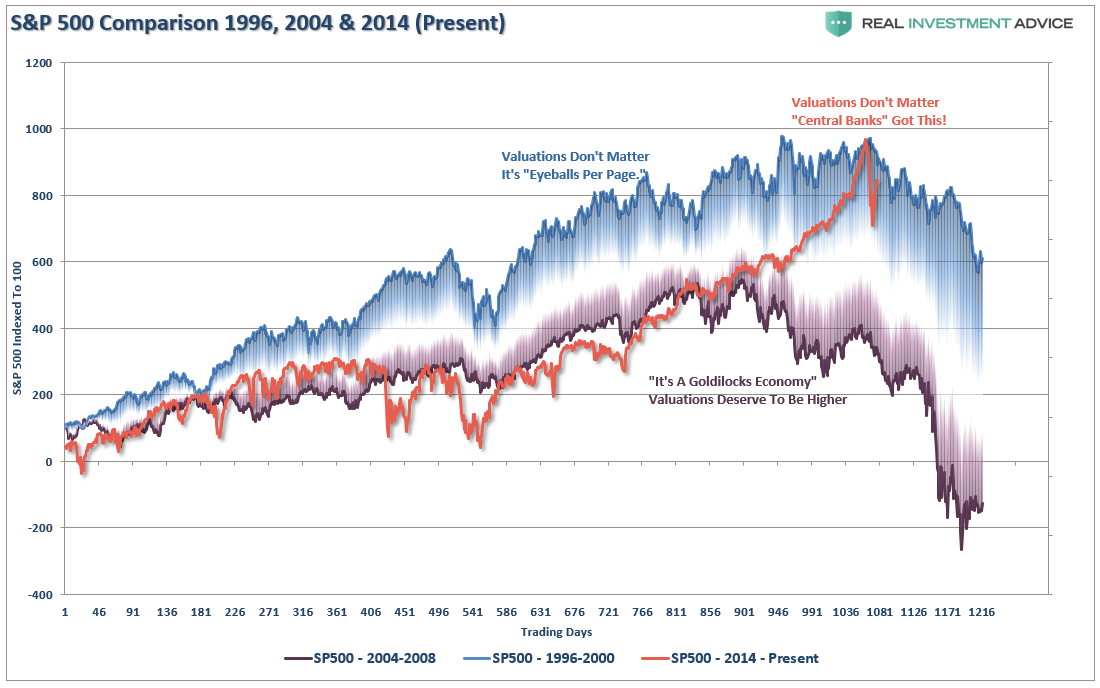

“The good news, for those who remain ever bullishly inclined, is on a long-term, monthly basis, the bull market remains intact for now. Unfortunately, despite the rather harrowing correction, little was done to relieve any of the underlying pressures.

- Valuations still remain elevated

- Bearishness and volatility, despite the recent spike, remain at historically low levels, and;

- Investors simply could not jump “back” into the markets fast enough.

These are not signs of a real, lasting bottom, which long-term investors should aggressively buy into.”

In that missive, I laid out two charts of the 2000 and 2007 market topping processes. In both previous cases, the first 10% correction was a precursor to a bear market. The chart below shows this a little differently by comparing the both previous bull markets to the current bull run. As you can see, the recent correction, which followed an accelerated advance, is behaving in much the same fashion as seen previously.

Does this mean we are the cusp of the next great “bear market?”

Simply looking at prices without context can be misleading. While markets are driven in the short-term by momentum, or better termed “psychology,” it is the long-term underlying fundamentals which ultimately determine a market’s fate.

Not surprisingly, given the surge in monetary liquidity by the Federal Reserve, combined with the underlying sluggishness of economic growth, investors are once again betting on a “this time is different” scenario as market valuations, on many measures, are at, or near, historically high levels.

But, again, just weak economic growth, or high valuations, or rising prices does not necessarily immediately result in a substantial mean-reverting event.

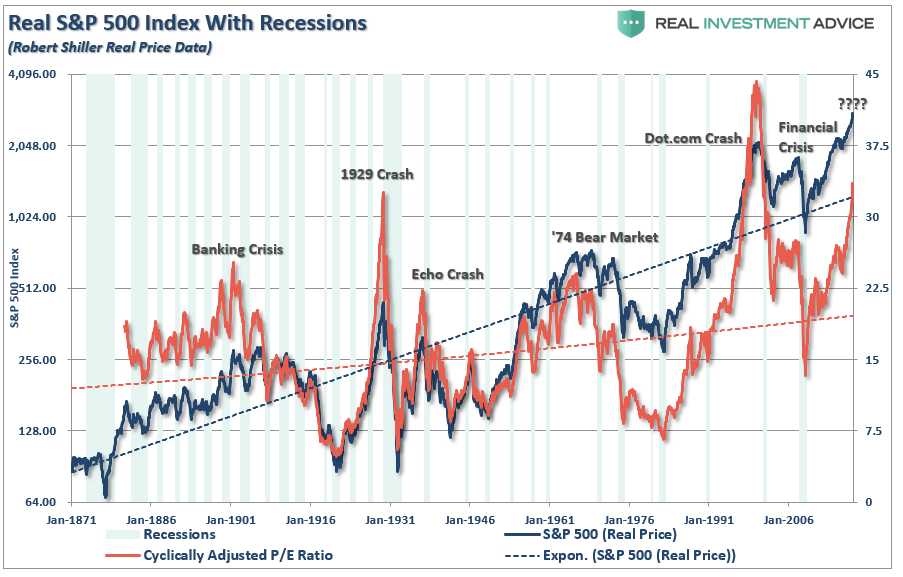

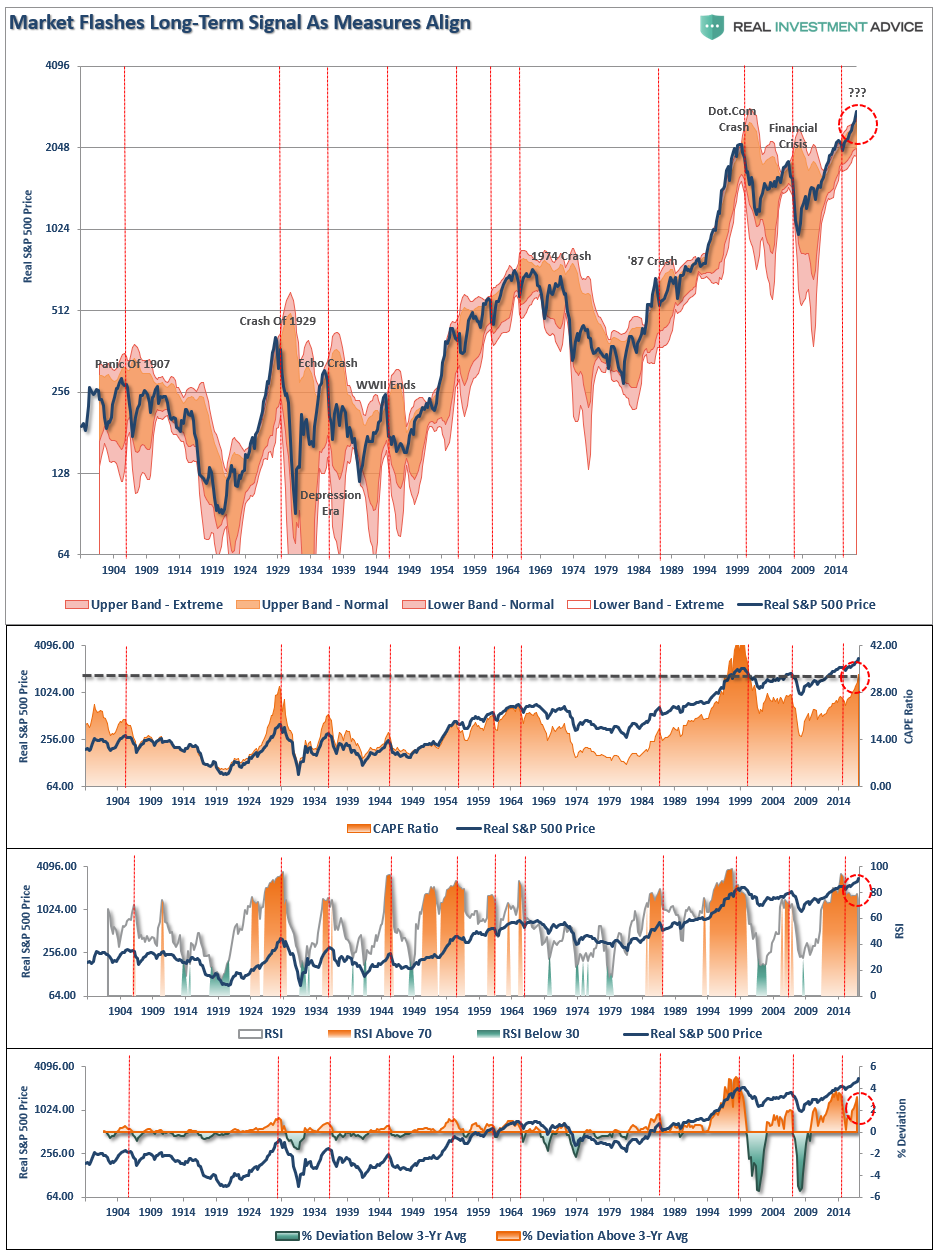

Major mean reverting events are generally tied to the combination of more major extremes in long-term measures of price deviations, economic growth, and valuations. Using quarterly data we can calculate several long-term measures for the S&P 500:

- The 12-period (3-year) Relative Strength Index (RSI),

- Bollinger Bands (2 and 3 standard deviations of the 3-year average),

- CAPE Ratio, and;

- The percentage deviation above and below the 3-year moving average.

- The vertical RED lines denote points where all measures have aligned

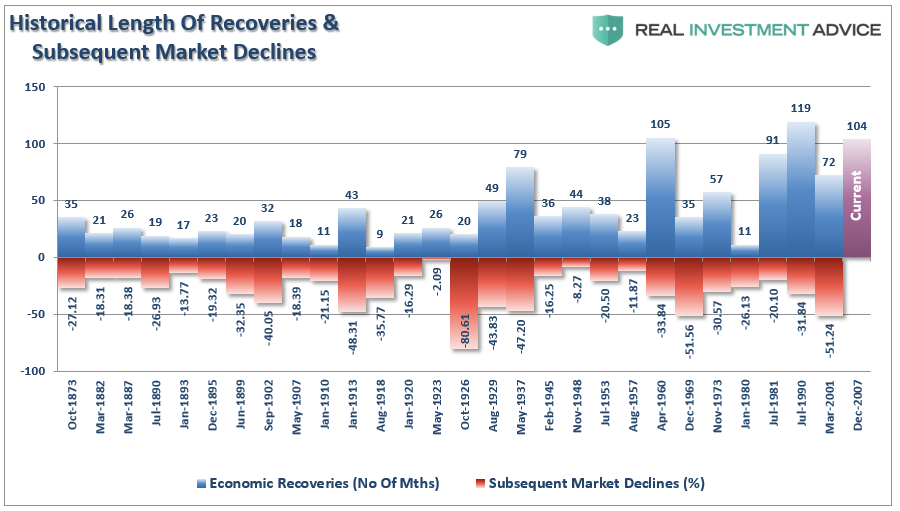

On virtually every measure price and valuation, the markets are grossly extended. However, it is when these measures coincide with the onset of an economic recession that “mean reverting” events tend to occur. The table below looks at the S&P 500 going back to 1873, based on Robert Shiller’s data, to detail economic recessions and bear markets.

In April, the current economic expansion will become the second longest in U.S. history. However, that period of expansion will also be the slowest, based on annualized economic growth rates, as well.

Could the current economic expansion become the longest in U.S. history?

Absolutely.

Over the next several weeks, or even months, the markets can certainly extend the current deviations from long-term means even further. But such is the nature of every bull market peak, and bubble, throughout history as the seeming impervious advance lures the last of the stock market “holdouts” back into the markets.

The correction over the last couple of weeks did little to correct these major extensions OR significantly change investor’s mental state from “greed” to “fear.”

As discussed above, the bullish trend remains clearly intact for now, but all “bull markets” end….always.

Do not be mistaken, the next “bear market” is coming.

Of that, there is absolute certainty.

As the charts clearly show, “prices are bound by the laws of physics.” While prices can certainly seem to defy the law of gravity in the short-term, the subsequent reversion from extremes has repeatedly led to catastrophic losses for investors who disregard the risk.

There are substantial reasons to be pessimistic about the markets longer-term. Economic growth, excessive monetary interventions, earnings, valuations, etc. all suggest that future returns will be substantially lower than those seen over the last eight years. Bullish exuberance has erased the memories of the last two major bear markets and replaced it with “hope” that somehow “this time will be different.”

Maybe it will be.

Probably, it won’t be.

The Reason To Focus On Risk

Our job as investors is to navigate the waters within which we currently sail, not the waters we think we will sail in later. Greater returns are generated from the management of “risks” rather than the attempt to create returns by chasing markets. That philosophy was well defined by Robert Rubin, former Secretary of the Treasury, when he said;

“As I think back over the years, I have been guided by four principles for decision making. First, the only certainty is that there is no certainty. Second, every decision, as a consequence, is a matter of weighing probabilities. Third, despite uncertainty, we must decide and we must act. And lastly, we need to judge decisions not only on the results, but on how they were made.

Most people are in denial about uncertainty. They assume they’re lucky, and that the unpredictable can be reliably forecast. This keeps business brisk for palm readers, psychics, and stockbrokers, but it’s a terrible way to deal with uncertainty. If there are no absolutes, then all decisions become matters of judging the probability of different outcomes, and the costs and benefits of each. Then, on that basis, you can make a good decision.”

It should be obvious that an honest assessment of uncertainty leads to better decisions, but the benefits of Rubin’s approach, and mine, goes beyond that. For starters, although it may seem contradictory, embracing uncertainty reduces risk while denial increases it. Another benefit of acknowledged uncertainty is it keeps you honest.

“A healthy respect for uncertainty and focus on probability drives you never to be satisfied with your conclusions. It keeps you moving forward to seek out more information, to question conventional thinking and to continually refine your judgments and understanding that difference between certainty and likelihood can make all the difference.”

We must be able to recognize, and be responsive to, changes in underlying market dynamics if they change for the worse and be aware of the risks that are inherent in portfolio allocation models. The reality is that we can’t control outcomes. The most we can do is influence the probability of certain outcomes which is why the day to day management of risks and investing based on probabilities, rather than possibilities, is important not only to capital preservation but to investment success over time.

Just something to consider.

via Zero Hedge http://ift.tt/2FgCCIT Tyler Durden