As discussed last night, going into today’s Fed decision there is a concern among traders that, as Nomura’s Charlie McElligott recaps today, it will be difficult for the Fed to not sound somewhat “hawkish” (relatively-speaking) and disappoint “doved-up” markets expectations following the recent policy outlook shift and the subsequent engineered market rally since the Dec meeting, where Committee members have delivered a coordinated “patience” message on further hikes (which are now largely on hold until the Summer at the earliest), as well as voiced a willingness to be open-minded regarding balance-sheet adjustments due to potential impact on the economic- and market- outlook.

McElligott has further “refined” (or perhaps simplified) this dynamic as follows: it will be difficult for the Fed to get “more dovish”— something which appears to be now priced in following last Friday’s WSJ article hinting the Fed may halt an unwind to the balance sheet — without US data turning lower again, when in fact recent stabilization of both data and the market brings the “financial conditions tightening” negative feedback loop back “in-play,” as Fed tightening re-enters the picture, and the higher stocks rise, the more rate hikes will have to be priced in.

All of that was covered in our preview of why the Fed may “massively disappoint” markets today.

However, as McElligott adds in his latest daily note, “there is some VERY provocative, 11th hour talk through the ‘consultant/macro advisory’ circles that the Fed could state today that at a future meeting, they will lay out an actual timetable to end the balance-sheet runoff”, which would be seen by the market as a clear escalation of the thought trial-ballooned in the WSJ piece last week (to end QT “sooner-than-expected”).

This raises a key question: with no catalysts to be incrementally dovish, “why would the Fed do this, and/or how could the they justify this, if at-the-same-time they have noted little evidence that the adjustment of the balance-sheet is having a significant impact on the outlook for the economy?”

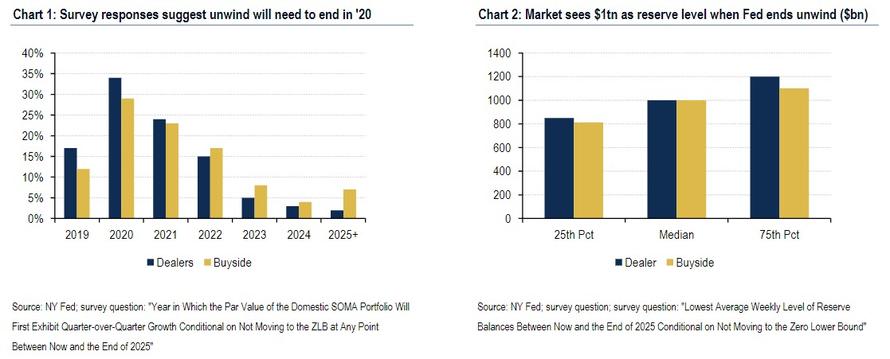

According to McElligott, the answer is that the Fed could say they are making this purely about “mechanics/plumbing” of the system — i.e. saying that per Primary Dealer surveys they have noted the appropriate level of Reserves in the system is ‘X’ trillion for proper function (a number much higher than the generic prior estimates from years-past that the Fed would work to get the balance sheet down to ~$1.5-$2.0T).

As we pointed out yesterday, using data from Bank of America, the market – both dealers and buyside – now sees $1 trillion as the appropriate reserve level when the Fed ends its unwind.

Assuming currency in circulation rises to $2 trillion in two years, this means that the balance sheet would shrink by another ~$1 trillion, or just over two more years of balance sheet shrinkage at the current pace of roughly $36BN per month.

And while the implication from such a disclosure is that the Fed anticipates a lenghty rolloff period, McElligott correctly notes that “this type of granular commentary on adjustments to the balance-sheet would be interpreted as VERY dovish“, so it is difficult to imagine this move occurring without a counter-balancing statement(s) that being either of the following scenarios, or a mix of both (again, want to note this is purely my speculation on POTENTIAL contingencies that would come with this idea of a “defined end to QT” timeline announcement in future):

- The Committee is working to increase market odds of additional hikes coming down the pipe (as in, “multiple” hikes) based upon their outlook for the economy remaining strong

Or…

- Discussing the potential in shifting the composition of the balance-sheet going-forward in order to shorten the weighted average maturity of the portfolio—a.k.a. a “Reverse Operation Twist” plan to tilt reinvestment proceeds towards the front-end, which would could see the curve meaningfully steepen.

While a theoretical “Reverse Twist” would be “sterilized” and not affect the overall level of liquidity, it is not duration-neutral, so viewed from this angle, a transition of the Fed’s portfolio back to shorter-term Treasuries then would actually be risk negative and act as a headwind for overall risk-assets, as long-term yields rise relative to front-end.

What does all of this mean for today?

As McElligott concludes, there is low, but binary risk going into today’s Fed meeting: either the first “disappoint the doves” scenario of message sounding more hawkish than anticpated currently with stocks lower as Fed-driven “FCI tightening” remains an ongoing risk, or this “fringe-potential” for a very granular dovish “end the balance-sheet run-off” market speculation which was hinted by the WSJ, and which the Nomura strategist notes could zoom the S&P to 2700-2750 fast.

There is one foonote: as Charlie adds, “for what it’s worth, we are NOT seeing new “Equities Upside” expressions in the market—in fact, WoW we have seen monetization of prior short-term upside expressions” as a result the Nomura strategist does not believe this speculation on the potential for this “hard timetable to end run-off” scenario is viewed with high conviction, or simply has not been widely disseminated.

via ZeroHedge News http://bit.ly/2MH3Ps3 Tyler Durden