Authored by Lance Roberts via RealInvestmentAdvice.com,

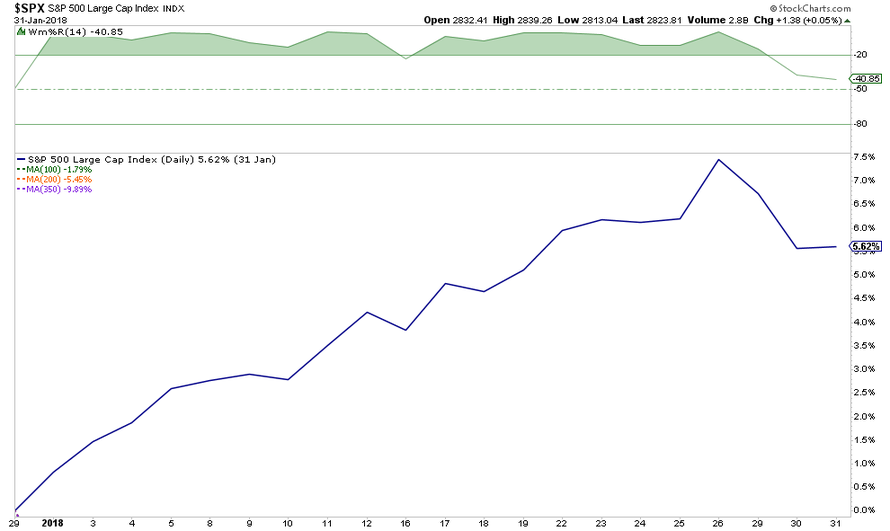

Since the day after Christmas, the markets have been in a surge very similar to what we saw in January of 2018.

Here is January 2018

And 2019

Of course, in February 2018, the rally ended.

While I am not suggesting that the markets are about to suffer a 10% correction, I am suggesting, as I wrote this past week, is that the markets have been “Too Fast & Too Furious.”

“Short-term technical indicators also show the violent reversion from extreme oversold conditions back to extreme overbought.”

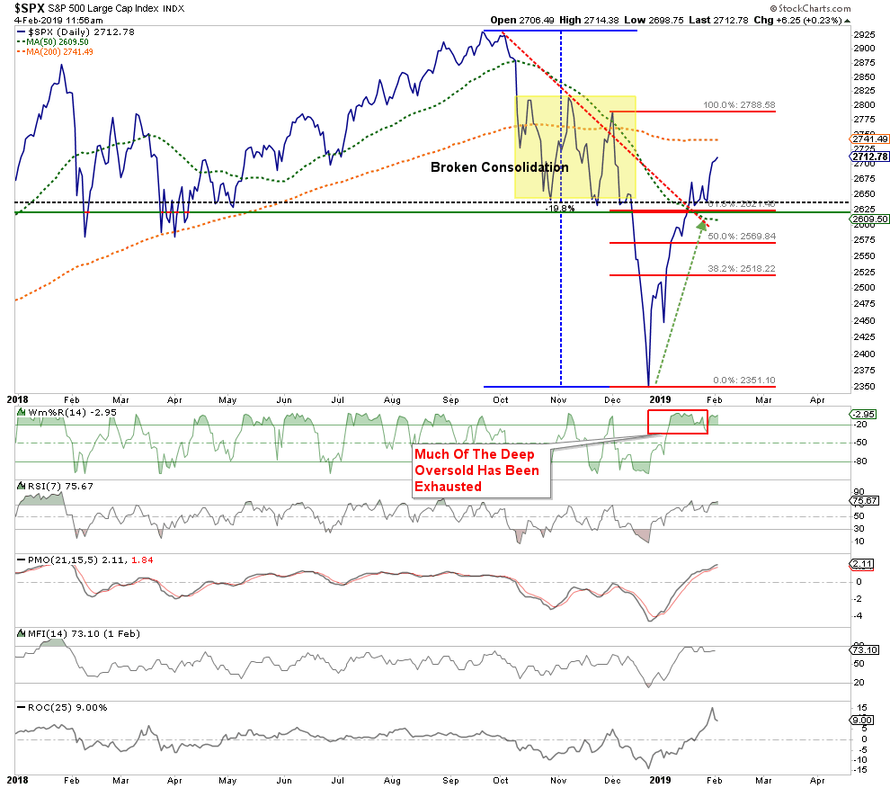

As we have discussed previously, price movements are very much confined by the “physics” of technicals. A couple of weeks ago, we drew out what we expected to be the movement over the market over the next couple of weeks.

We said then the most likely target for the rally was the 200-dma. It was essentially the level at which the “irresistible force would meet the immovable object.”

The chart below is updated through Friday afternoon:

As noted, we lifted profits at the 200-dma and added hedges to the Equity and Equity Long/Short portfolios. (If you are reading this as a non-RIA PRO subscriber you can see our 3-live portfolios at the site use code PRO30 for a 30-day free trial.)

What will be critically important now is for the markets to retest and hold support at the Oct-Nov lows which will coincide with the 50-dma. A failure of that level will likely see a retest of the 2018 lows.

A retest of those lows, by the way, is not an “outside chance.” It is actually a fairly high possibility. A look back at the 2015-2016 correction makes the case for that fairly clearly.

But even if a retest of lows doesn’t happen, you should be aware that sharp market rallies are not uncommon, but almost always have a subsequent retracement.

The point here is that the move off of the December lows is likely now complete, for now.

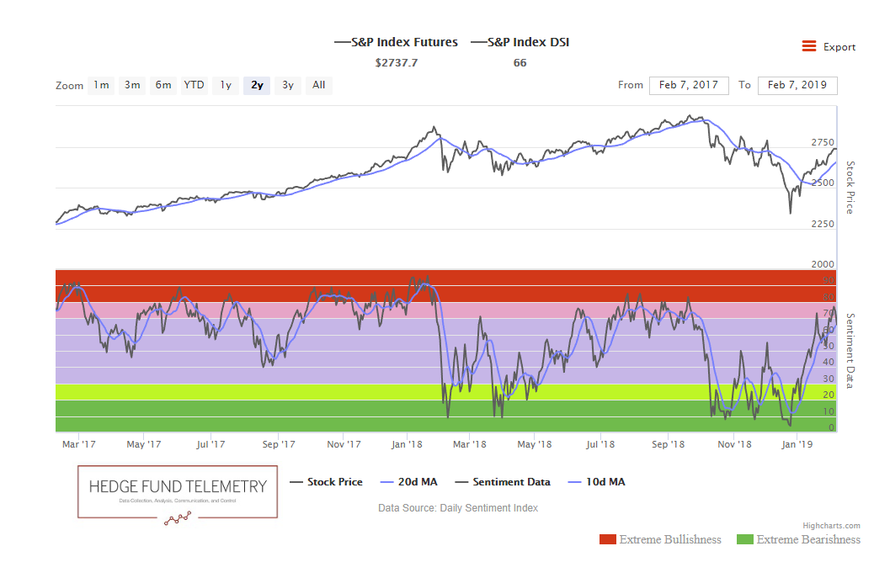

Thomas Thornton from Hedge Fund Telemetry had a great note out this past week on this point.

“The strong move off the lows in December is complete. As you have seen I’ve moved from a very high exposure level of 90% net long from mid December to now net short. Various internals are overbought, sentiment is back in the elevated zone, and price targets have been achieved. There have been 45 new DeMark sell signals and only 2 buy signals so far in February. Recall in December there were 225 buy signals and 25 sell signals which had an average gain together of 11.5% since. In January there were 72 total signals with the majority 53 sells/19 buys with only a gain of 0.5% since. It’s telling me a shift is coming and that’s lower. How low? As of now, I’m not saying new lows but higher lows but that could change if some Trend Factor levels break and we see downside Countdowns start.”

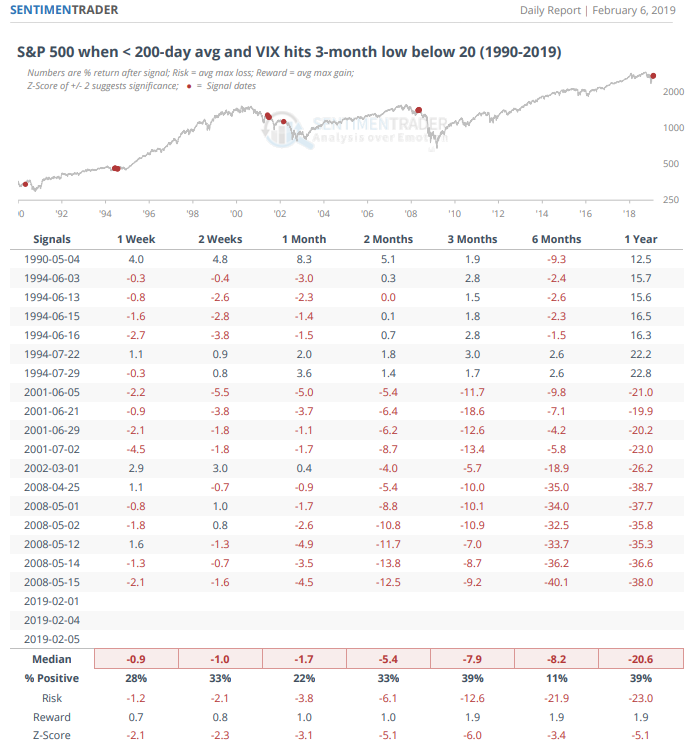

Sentimentrader also recently noted market performance when the VIX hits a 3 month low with the S&P under the 200 day. Performance is very negative going forward.

Signs Of Caution

As we noted last Tuesday, there are a litany of things that are worth paying attention to. To wit:

“It is too early to suggest the “bear market of 2018” is officially over.

But, the rally has simply been “Too Fast, Too Furious,” completely discounting the deteriorating fundamental underpinnings:”

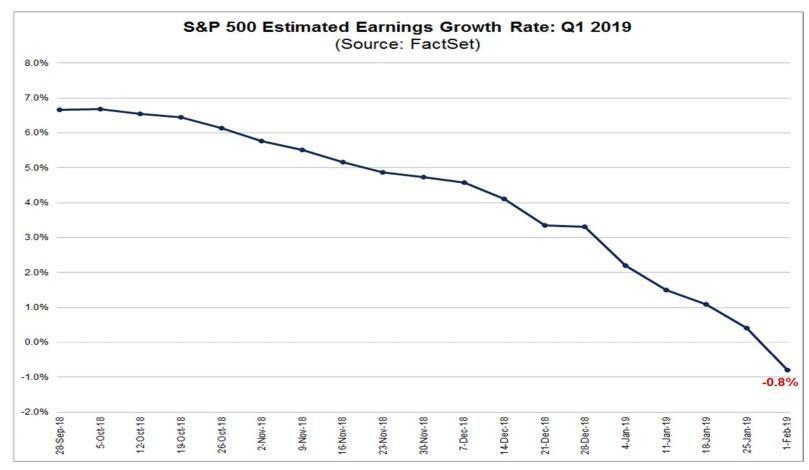

- Earnings estimates for 2019 have sharply collapsed as I previously stated they would and still have more to go. In fact, as of now, the consensus estimates are suggesting the first year-over-year decline since 2016.

-

Stock market targets for 2019 are way too high as well.

-

Despite the Federal Reserve turning more dovish verbally, they DID NOT say they actually WOULD pause their rate hikes or stop reducing their balance sheet.

-

Larry Kudlow said the U.S. and China are still VERY far apart on trade.

-

Trump has postponed his meeting with President Xi which puts the market at risk of higher tariffs.

-

There is a decent probability the U.S. Government winds up getting shut down again after next week over “border wall” funding.

-

The effect of the tax cut legislation has disappeared as year-over-year comparisons are reverting back to normalized growth rates.

-

Economic growth is slowing as previously stated.

-

Chinese economic has weakened further since our previous note.

-

European growth, already weak, will likely struggle as well.

-

Valuations remain expensive

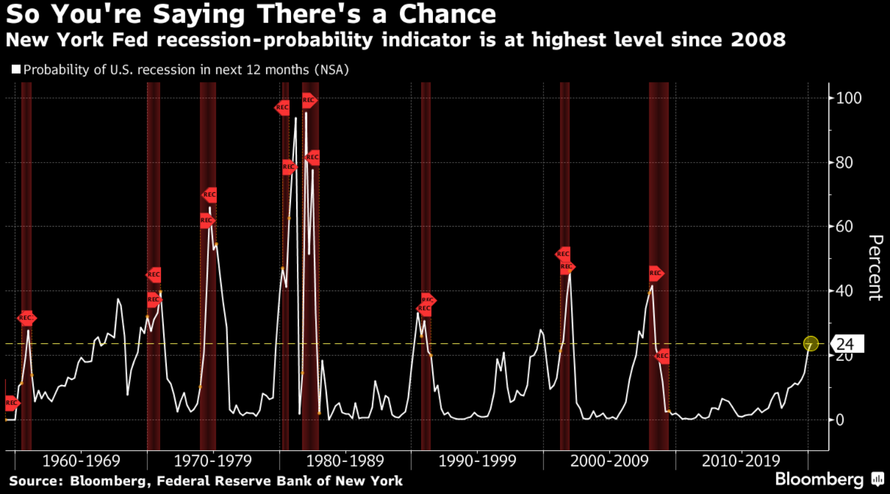

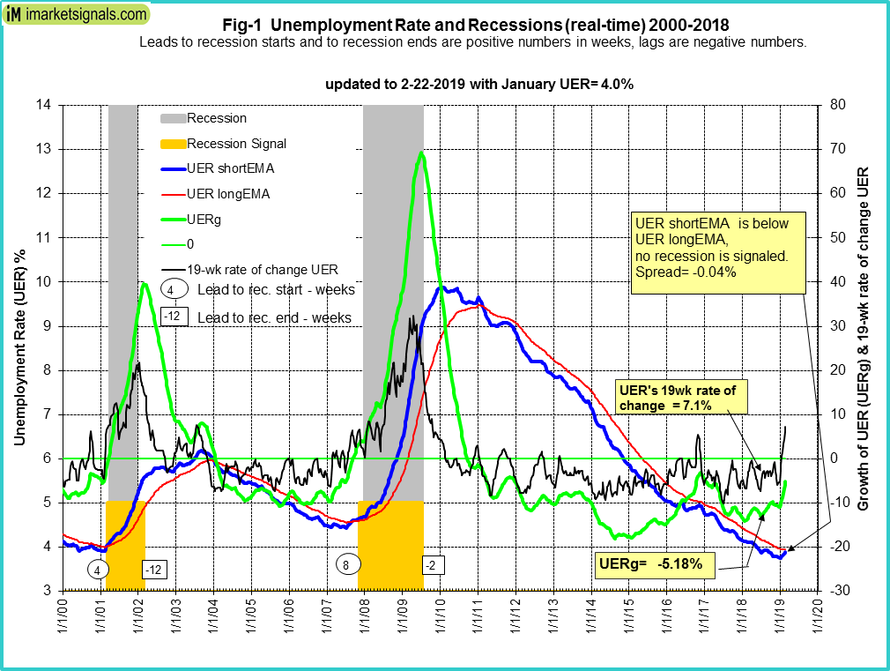

Despite recent comments that “recession risk” is non-existent, there are various indications which suggest that risk is much higher than currently appreciated. The New York Federal Reserve recession indicator is now at the highest level since 2008.

Also, as noted by George Vrba recently, the unemployment rate may also be warning of a recession as well.

“For what is considered to be a lagging indicator of the economy, the unemployment rate provides surprisingly good signals for the beginning and end of recessions. This model, backtested to 1948, reliably provided recession signals.

The model, updated with the January 2019 rate of 4.0%, does not signal a recession. However, if the unemployment rate should rise to 4.1% in the coming months the model would then signal recession.”

The point here is that ignoring the “risks” leaves you “exposed.” If you think its going to rain, you carry an umbrella.

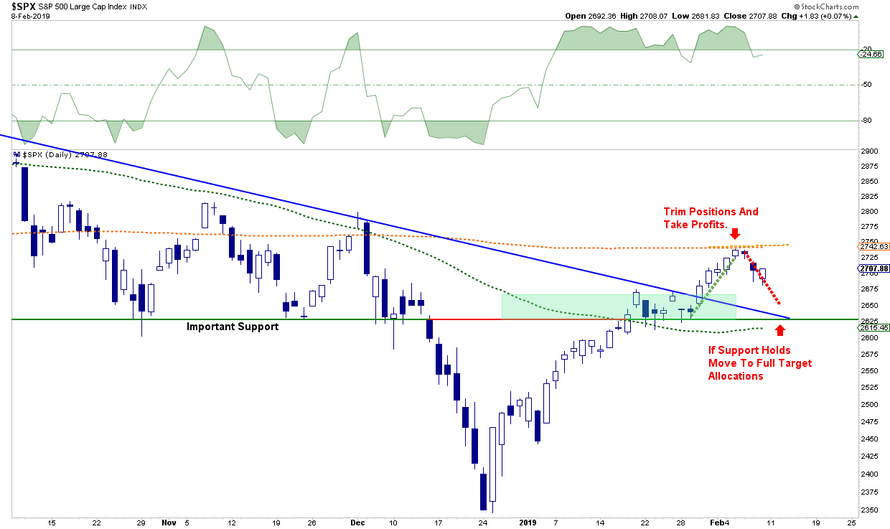

This is why we recently raised cashed and added hedges to portfolios – just in case it rains. And, right now, it seems to be sprinkling a bit. As John Murphy via StockCharts.com noted on Friday:

“It looks like the 200-day averages that we’ve all been watching have managed to contain the 2019 rally. Chart 1 shows the S&P 500 pulling back from that red overhead resistance line. That’s not too surprising considering the steepness of the recent rally which put stock indexes in a short-term overbought condition. The upper box in Chart 1 shows the more sensitive 9-day RSI line falling to the lowest level in a month after reaching overbought territory above 70. That also shows loss of upside momentum. The lower box shows daily MACD lines in danger of turning negative for the first time in a month. All of which suggests that the early 2019 stock rally has failed its first attempt to regain its 200-day moving average.”

However, one of the biggest “warning flags” we are watching currently, and why we have taken a more cautious stance in portfolios, is because “bonds ain’t buyin’ it.”

As shown in the chart below, the market has not only broken out of its rising wedge, but yields have been dropping sharply as “risk on” is rotating to “risk off.”

While the bulls clearly took charge of the market in late December, the question is whether or not they can maintain control.

The weight of macro-evidence is going to weigh on the markets sooner than later which is why we are opting to hedge risk and hold on to higher levels of cash currently.

The rally we discussed on December 25th, has hit all of our targets, and then some.

Don’t be greedy.

via ZeroHedge News http://bit.ly/2WMh4fs Tyler Durden